Japan Mental Health Market Size, Share, Trends and Forecast by Disorder, Service, Age Group, and Region, 2026-2034

Japan Mental Health Market Size & Forecast 2026-2034

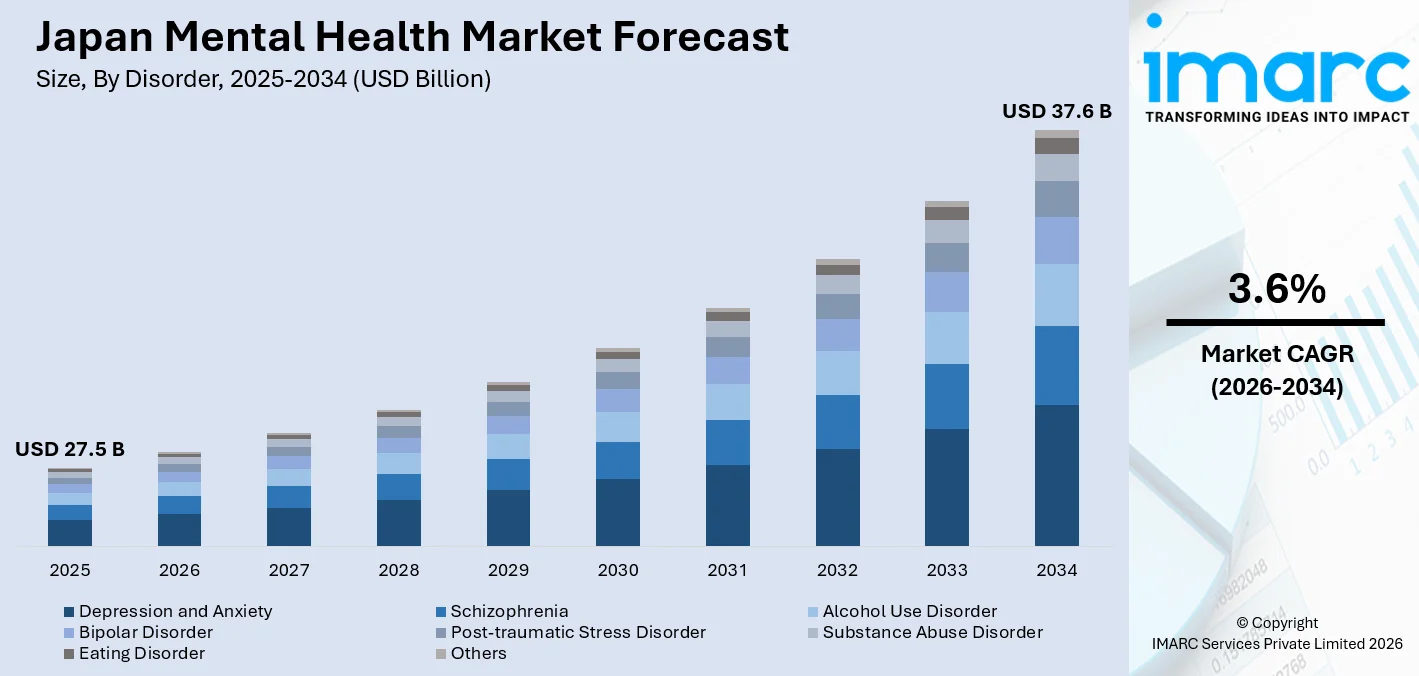

The Japan mental health market size was valued at USD 27.5 Billion in 2025 and is projected to reach USD 37.6 Billion by 2034, exhibiting a compound annual growth rate of 3.6% during 2026-2034. The market is driven by the growing incidence of anxiety, depression, and stress disorders related to the workplace; the quick growth of digital therapeutics and teletherapy platforms; ongoing government policy changes, such as the mandatory Stress Check Program; and demographic pressures from Japan's rapidly aging population, which reinforce the country's mental health market share.

To get more information on this market Request Sample

Japan Mental Health Market - Key Insights

- Depression and Anxiety hold a 42.0% share of disorder segment in 2025: This is the single greatest disease category in the market due to the combined prevalence of workplace-driven stress disorders and generalized anxiety, which is exacerbated by Japan's demanding academic environments, high-pressure corporate culture, and rising awareness of mental health concerns.

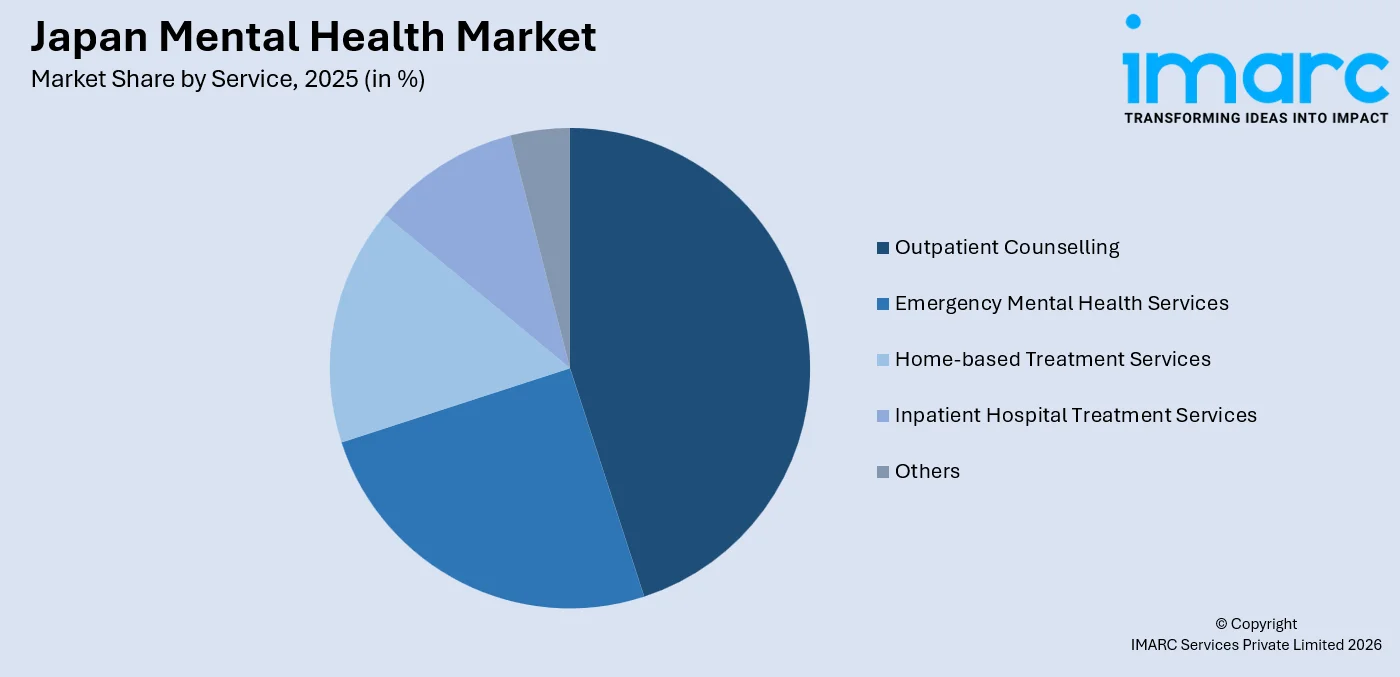

- Outpatient Counselling accounts for 38.0% share of service segment in 2025: Outpatient counselling has become the most popular service format due to growing patient preferences for easily accessible, non-stigmatizing care formats, increased insurance coverage for outpatient psychiatric consultations, and the use of telemedicine into outpatient delivery models.

- Adult segment commands 55.0% share of age group segment in 2025: Due to the high prevalence of professional stress, expanding corporate wellness initiatives, and rising use of counselling and pharmaceutical treatments for stress, depression, and anxiety among Japan's working-age population, adults between the ages of 20 and 64 make up the largest patient group.

- Kanto Region leads with 44.0% share of region segment in 2025: The densest concentration of psychiatric clinics, digital mental health companies, and corporate headquarters implementing employee wellness programs can be found in Tokyo and the larger Kanto region. This results in the largest regional concentration of mental health service demand and delivery infrastructure in Japan.

Japan Mental Health Market Trends and Dynamics 2026:

Market Trends:

Increased Mental Health Awareness

As social awareness grows and the stigma associated with mental illness progressively fades, Japan's mental health sector is growing. More people are seeking help for stress, anxiety, and depression as a result of public campaigns and educational programs. Sustained market growth is being driven by the increasing integration of mental health services in healthcare systems, schools, and workplaces.

Mandatory Workplace Stress Management Programs Boosting Corporate Mental Health Spending

The market for workplace mental health in Japan is expanding rapidly due to increased awareness of psychological risks and regulatory enforcement. In FY2024, the Ministry of Health, Labour and Welfare (MHLW) received a record 3,780 workers' compensation applications pertaining to mental illness, marking a significant milestone for the mandated Stress Check Program for businesses with 50 or more employees. With over 1,100 HR departments automating yearly stress assessments through mobile platforms and about 850 logistics companies implementing driver-focused stress monitoring applications after overtime regulation reforms in April 2024, corporate adoption of digital mental health solutions accelerated.

Destigmatisation and Increased Mental Health Awareness Expanding Outpatient Demand

As early intervention programs and awareness campaigns change public perceptions of psychological support, Japan's mental healthcare business is growing. While extensive student access to digital mental health applications is normalizing early help-seeking and supporting long-term demand for counselling and digital mental health services, national initiatives and workplace education have raised care-seeking behaviour.

- Four-Day Work Week and Work-Life Reform Initiatives: Tokyo's government introduced a four-day workweek option for city employees in 2025, reflecting broader Work Style Reform Laws aimed at reducing karoshi and improving long-term workforce mental wellbeing outcomes.

- Government-Technology Collaboration for Dementia Care: In November 2024, Japan's government partnered with technology firms to create digital dementia monitoring tools - Kakogawa City deployed an app-based system using BLE tags and Mimamori cameras - expanding geriatric mental health market scope.

Growth Drivers:

Rapidly Aging Population Driving Geriatric and Dementia-Related Mental Health Service Demand

Japan’s National Institute of Population and Social Security Research projects that by 2040, around 34.8% of the population will be 65 years or above. Even though life expectancy is still among the greatest in the world, age-related mental health issues like dementia, depression in later life, and anxiety brought on by loneliness are becoming more common. The government established a technological collaboration in November 2024 to create digital dementia care solutions, encouraging remote monitoring tools and boosting funding for geriatric mental health services and early detection.

Escalating Workplace Stress and Burnout Creating Sustained Outpatient and Digital Service Demand

Japan’s deeply rooted overwork culture continues to drive significant mental health challenges, with karoshi cases rising over 18% to a record 1,304 in 2024. In 2023, 883 workers, including 52 managers, were diagnosed with occupational stress-related mental disorders. Since 2015, mandatory annual Stress Check surveys for companies with more than 50 employees have enabled early risk detection, increasing demand for outpatient counselling and employee assistance programs (EAPs).

Government Policy Reforms and Digital Health Investment Creating Structural Market Enablers

Japan’s regulatory framework is fostering mental health sector growth through digital and AI-enabled care. From April 2025, practitioners must adopt tele-mental health tools, while five software-based treatments are approved. AI diagnostics, guided by Unified AI Guidelines, are expanding, with Google’s 2024 Ubie investment reaching 1,700 medical facilities, demonstrating institutional confidence.

- Sumitomo Pharma VR Therapy Development: Sumitomo Pharma's collaboration with BehaVR to develop three VR-based digital therapeutics addressing social anxiety disorder, generalised anxiety disorder, and major depressive disorder broadens Japan's pharmacological-digital hybrid treatment pipeline.

- Insurance Coverage Expansion: National health insurance coverage for two approved DTx products and ongoing revisions to telemedicine reimbursement rates are reducing financial barriers, increasing outpatient and digital mental health service uptake across income groups.

- School-Based Paediatric Mental Health Programs: Japanese schools and hospitals are expanding mental health intervention programs for children with anxiety, depression, and ADHD, driven by government measures supporting early intervention and preventive psychiatric care for paediatric patients.

Market Restraints:

Persistent Shortage of Psychiatrists and Mental Health Professionals in Rural Regions: Japan has a structural deficit of licensed psychiatrists, psychologists, and counsellors despite rising demand, especially outside of big cities like Tokyo and Osaka. Geographic treatment gaps result from the substantially lower per-capita availability to outpatient mental health services in rural and regional prefectures. This gap is being partially filled by telehealth, but the speed of market expansion in underserved areas is still constrained by the shortage of skilled professionals.

Residual Cultural Stigma Suppressing Formal Treatment-Seeking Rates: Formal treatment utilization rates in Japan are still suppressed by cultural norms surrounding emotional self-sufficiency, occupational loyalty, and perceived weakness in seeking psychiatric help, despite notable destigmatization advances since 2014. A reported constraint that lowers the efficacy of early intervention strategies and restricts the use of outpatient and counselling services is the underreporting of stress in the required Stress Check Program owing to fear of workplace reprisal.

Limited and Fragmented Insurance Coverage for Advanced Treatments and Newer Therapies: Basic psychiatric consultations are covered by Japan's universal healthcare system, but patients must pay a large amount of money out of pocket for more advanced treatment options like residential programs, specialized psychotherapies, and newly developed digital treatments. Financial access hurdles arise because not all mental health therapies are fully reimbursed by insurance. Cost-related treatment avoidance can harm long-term psychiatric outcomes for individuals with lower incomes and those with serious disorders requiring intensive care.

Japan Mental Health Market Report Segmentation:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Disorder | Depression and Anxiety | 42.0% | 2025 |

| Service | Outpatient Counselling | 38.0% | 2025 |

| Age Group | Adult | 55.0% | 2025 |

| Region | Kanto Region | 44.0% | 2025 |

Disorder Insights:

Depression and Anxiety - 42.0% Market Share (2025) | Leading Disorder

Depression and Anxiety dominate the disorder segment with a 42.0% share in 2025, driven by the high prevalence of occupational stress, academic pressure, social isolation, and Japan's deeply embedded overwork culture generating persistent demand for treatment across the working-age population.

The largest disorder group is Depression and Anxiety, which reflects the structural burden of social expectations, scholastic constraints, and professional stress in Japanese society. About 883 people were diagnosed with work-related mental disease in 2023, including depressive illnesses associated with extended work hours. The diagnosed pool has increased because of the increased awareness programs, which have further decreased the reporting undercount.

|

Segment Breakdown Depression and Anxiety (42.0%) · Schizophrenia · Alcohol Use Disorder · Bipolar Disorder · Post-traumatic Stress Disorder · Substance Abuse Disorder · Eating Disorder · Others |

Service Insights:

Access the comprehensive market breakdown Request Sample

Outpatient Counselling - 38.0% Market Share (2025) | Leading Service

Outpatient Counselling is the largest service segment with a 38.0% share in 2025, sustained by strong patient preference for flexible, accessible care, growing insurance reimbursement for psychiatric outpatient visits, and the integration of teletherapy platforms enabling remote counselling at scale.

For working individuals with stress, anxiety, and depression in Japan, outpatient counselling continues to be the major course of treatment. Psychiatric clinics are incorporating digital CBT tools in addition to traditional therapy to improve treatment delivery, while telepsychiatry services are being used by clinicians more frequently to enable more flexible access.

|

Segment Breakdown Outpatient Counselling (38.0%) · Emergency Mental Health Services · Home-based Treatment Services · Inpatient Hospital Treatment Services · Others |

Age Group Insights:

Adult Age Group- 55.0% Market Share (2025) | Leading Age Group

The Adult age group holds the largest share at 55.0% in 2025, driven by the high incidence of workplace-induced depression, anxiety, and burnout among Japan's working-age population, combined with growing uptake of corporate wellness programs and outpatient counselling services.

Japan’s working-age adults face high mental health demand due to long hours, harassment, and performance pressure, with 1,055 FY2024 workers’ compensation cases reported. While awareness efforts promote early help-seeking and lessen stigma among the working-age population, employers are increasingly incorporating stress monitoring, digital mental health tools, and preventive programs to enhance employee wellbeing.

|

Segment Breakdown Adult (55.0%) · Pediatric · Geriatric |

Regional Insights:

Kanto Region- 44.0% Market Share (2025) | Leading Region

The Kanto Region accounts for the highest revenue share at 44.0% in 2025, anchored by Tokyo's concentration of corporate headquarters, psychiatric institutions, digital mental health startups, and the highest density of working adults subjected to Japan's most intense workplace stress environments.

The majority of Japan's mental health services are found in large cities like Tokyo, Osaka, and Nagoya, where clinical research, corporate wellness initiatives, and the use of digital therapy are most prevalent. These cities are important centers for the implementation of mental health policies and market development since they are home to large healthcare providers and pharmaceutical businesses that foster innovation.

|

Regional Breakdown Kanto Region (44.0%) · Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Market Outlook 2026-2034

What is the future outlook of the Japan mental health market?

Japan's mental health market has a very bright future ahead of it thanks to structural changes in the country's workplace, regulations, and demographics that are integrating mental health services into regular medical care. Preventive care, early diagnosis, and long-term therapy adoption are anticipated to increase across all age groups due to growing knowledge, decreasing societal stigma, and ongoing policy support from the Ministry of Health, Labor, and Welfare. The demand for counseling, stress monitoring, and employee support services will rise as companies include psychological risk management into their HR strategy, strengthening corporate mental wellness initiatives.

Competitive Landscape:

Japan’s mental health market is characterised by a diverse competitive landscape combining established pharmaceutical manufacturers, healthcare technology providers, and emerging digital therapeutics innovators. Major pharmaceutical companies such as Otsuka Pharmaceutical, Sumitomo Pharma, Shionogi, Takeda Pharmaceutical Company, and Eisai continue to lead the pharmacological treatment segment. Meanwhile, digital health companies including MICIN, Yume no Tobira, and MedPeer are expanding rapidly across outpatient care and teletherapy services. Competitive intensity is increasing as firms focus on AI-enabled counselling applications, digital therapeutics (DTx) approvals, and corporate employee assistance program (EAP) integration. By April 2025, nine digital mental health applications had received Class II medical device designation, signalling a progressively mature regulatory framework and a strengthening competitive ecosystem.

| Company | Leading Brands | Highlights |

|---|---|---|

| Otsuka Pharmaceutical | Abilify, Rexulti, digital adherence & psychiatric support solutions | Significant pioneer in the treatment of bipolar disorder and schizophrenia; works with public mental health organizations to improve national support networks; combines pharmaceutical therapy with digital monitoring and behavioural health programs, solidifying its leading position in Japan's psychiatric care ecosystem. |

| Takeda Pharmaceutical Company | Neuropsychiatric drug portfolio, depression & CNS disorder therapies | One of Japan’s largest healthcare companies investing in next-generation treatments for depression and neurological disorders; focuses on improved safety profiles and long-acting therapies to enhance patient adherence while expanding innovation across mental health R&D pipelines. |

| MICIN | Telemedicine platforms, AI symptom assessment tools, telepsychiatry solutions | Accelerating the adoption of digital outpatient mental healthcare services in Japan, this rapidly expanding digital health company provides hospitals and clinics with integrated telehealth infrastructure and AI-driven diagnostics, enabling remote psychiatric consultations and early mental health screening. |

Major key companies in the Japan mental health market are Sumitomo Pharma, Shionogi, Eisai, MedPeer, Ubie, Journey Health, and Yume no Tobira

Latest Development & News:

- February 2026: Designed for both California and Japan, Journey Health unveiled a comprehensive 360° digital mental health care model with an emphasis on hybrid care delivery that blends culturally appropriate digital services with distant treatment. In order to provide ongoing, lifetime mental health management, the platform incorporates outpatient teletherapy, AI-assisted wellness check-ins, and caregiver support modules. It specifically targets the demands of Japan's aging population and working-adult patient segments.

- November 2024: In order to create digital solutions that assist people with dementia and their caretakers, the Japanese government established a formal public-private partnership with the technology sector. In order to extend geriatric mental health monitoring into community home-care settings, Kakogawa City in western Japan installed a technological system that allows family members to keep an eye on dementia patients using a smartphone app, BLE location tags, and Mimamori security cameras.

Japan Mental Health Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Disorders Covered | Schizophrenia, Alcohol Use Disorder, Bipolar Disorder, Depression and Anxiety, Post-traumatic Stress Disorder, Substance Abuse Disorder, Eating Disorder, Others |

| Services Covered | Emergency Mental Health Services, Outpatient Counselling, Home-based Treatment Services, Inpatient Hospital Treatment Services, Others |

| Age Groups Covered | Pediatric, Adult, Geriatric |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan mental health market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan mental health market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan mental health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Mental Health Market Report

The Japan mental health market reached a value of USD 27.5 Billion in 2025.

The market is projected to grow at a CAGR of 3.6% during 2026-2034, reaching USD 37.6 Billion by 2034.

Key growth drivers include the rapidly growing geriatric population, rising prevalence of mental health disorders, increased awareness and destigmatization, government policy reforms, workplace stress and burnout, and expanding adoption of digital mental health and telehealth solutions.

The report covers segmentation by disorder, service, age group, and region. Each segment includes detailed market size and forecast analysis.

Key trends include growing mental health awareness and destigmatization, expansion of community-based and home-based treatment services, rising government-led suicide prevention and policy reform initiatives, and rapid proliferation of digital platforms, teletherapy apps, and AI-driven mental health solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)