Japan Modular Construction Market Size, Share, Trends and Forecast by Type, Material, End User, and Region, 2026-2034

Japan Modular Construction Market Summary:

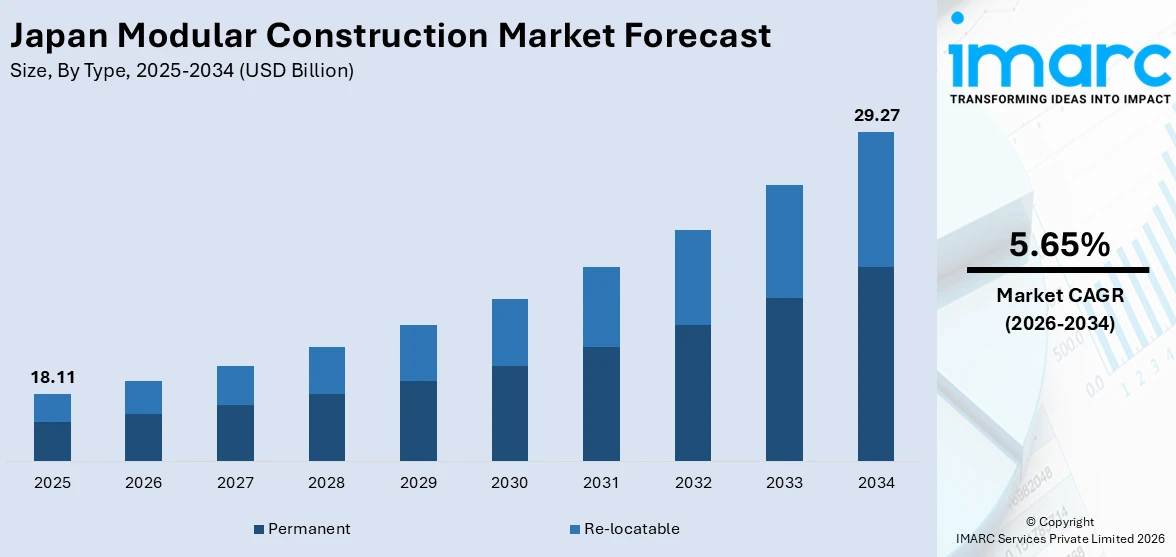

The Japan modular construction market size was valued at USD 18.11 Billion in 2025 and is projected to reach USD 29.27 Billion by 2034, growing at a compound annual growth rate of 5.65% from 2026-2034.

Japan's modular construction market is experiencing robust growth, propelled by intensifying labor shortages, accelerating urbanization, and a national imperative for disaster-resilient, energy-efficient building solutions. Advanced digital manufacturing technologies continue to transform construction delivery across residential, commercial, and industrial segments. Supportive government policy and green building mandates further accelerate adoption, collectively enhancing the Japan modular construction market share.

Key Takeaways and Insights:

- By Type: Permanent dominates the market with a share of 58.4% in 2025, owing to its extensive application across long-term residential and commercial developments, structural durability advantages, and alignment with Japan's stringent seismic safety requirements that strongly favor fixed, factory-built reinforced modular systems.

- By Material: Wood leads the market with a share of 42.3% in 2025, driven by Japan's deep-rooted tradition of timber construction, rising adoption of cross-laminated timber and engineered wood solutions, and alignment with national carbon reduction mandates and sustainable building certification schemes.

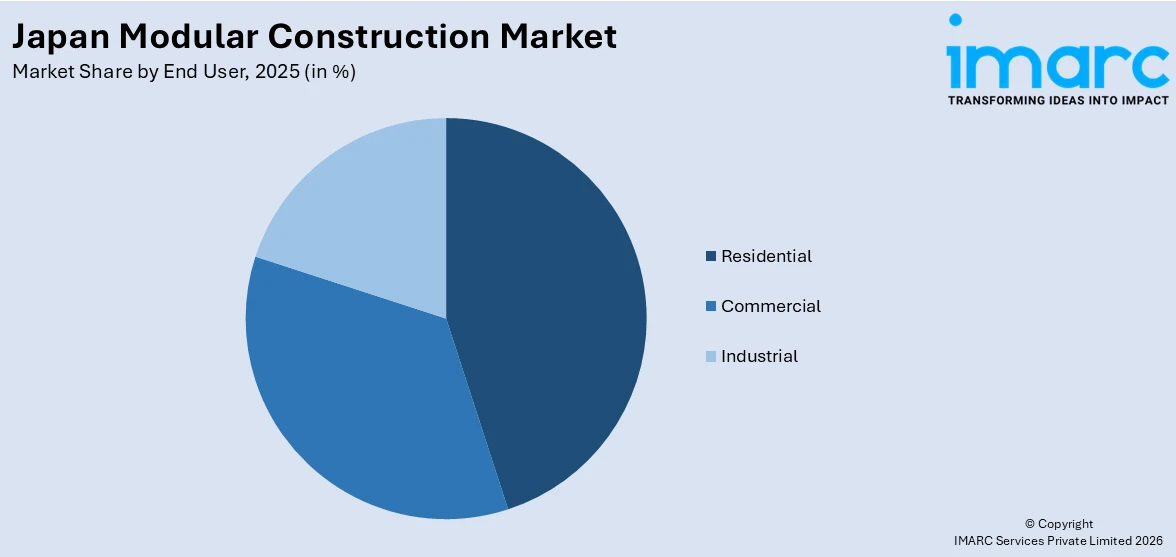

- By End User: Residential holds the largest segment with a market share of 45.6% in 2025, reflecting sustained demand for affordable, space-efficient, and disaster-resilient housing amid Japan's aging demographic trends, urban densification pressures, and acute skilled-labor shortages in the construction industry.

- By Region: Kanto Region represents the largest region with 38.5% share in 2025, driven by Tokyo's high population density, large-scale infrastructure and residential development activity, and the region's early adoption of building information modeling and net-zero construction standards.

- Key Players: Key players in the Japan modular construction market strengthen their competitive positions through factory automation investment, digital design platform integration, and product portfolio diversification. Strategic commitments to sustainable materials, seismic resilience technologies, and broadened distribution channels help maintain consistent product accessibility and bolster overall market presence across diverse construction segments.

To get more information on this market Request Sample

The Japan modular construction market is shaped by a powerful confluence of economic, demographic, technological, and policy-driven forces that are collectively accelerating the transition toward off-site, factory-based building delivery. Japan faces one of the world's most acute skilled labor shortages in construction, with the Ministry of Land, Infrastructure, Transport and Tourism reporting a sustained decline in the available construction workforce owing to demographic aging and an exodus from trade occupations. This mounting pressure compels widespread adoption of modular building systems that reduce on-site labor dependency while maintaining superior quality standards. Rapid urbanization concentrating population in metropolitan areas drives demand for faster, space-optimized delivery methods, underpinning enduring growth for the Japan modular construction market.

Japan Modular Construction Market Trends:

Growing Integration of Building Information Modeling in Off-Site Manufacturing

Japan's construction industry is witnessing accelerating integration of Building Information Modeling and digital twin technologies within modular and prefabricated manufacturing workflows. The Ministry of Land, Infrastructure, Transport and Tourism has issued guidelines strongly encouraging BIM adoption across public infrastructure and large-scale developments. This digital integration enables manufacturers to design, simulate, and optimize modular components with greater accuracy before production, reducing rework rates, minimizing material waste, and compressing delivery timelines — creating measurable efficiency gains across the Japan modular construction market.

Escalating Demand for Disaster-Resilient and Seismically Safe Modular Structures

Japan's persistent exposure to seismic activity and extreme weather continues to drive strong demand for modular structures engineered to advanced earthquake-resistance specifications. The 2024 Noto Peninsula earthquake underscored the national need for rapidly deployable, structurally resilient prefabricated housing. Following the disaster, new prefabricated housing units were built in Ishikawa Prefecture, demonstrating modular construction's critical role in rapid-response rebuilding. This growing national focus on disaster preparedness and post-disaster recovery is reinforcing long-term demand for resilient modular solutions across Japan.

Expansion of Wood-Based Modular Construction Aligned with Sustainability Goals

Growing adoption of engineered timber solutions, particularly cross-laminated timber and glulam panels, is reshaping Japan's modular construction landscape. Japan's extensive domestic forest resources and woodworking expertise position timber as both a sustainable and structurally effective modular material. The government actively promotes wood construction through pro-timber initiatives, housing quality programs, and carbon reduction mandates, catalyzing investment in wood-based prefabricated systems. University-industry collaborations on timber innovation and scalable wood modular platforms are embedding engineered timber as a premium, sustainable choice in Japan's construction evolution.

Market Outlook 2026-2034:

The Japan modular construction market is positioned for sustained and meaningful growth throughout the forecast period, supported by converging structural demand drivers that favor off-site, precision-manufactured building solutions. A persistently aging construction workforce and deepening labor scarcity will continue pushing developers and contractors toward factory-based methods that require fewer on-site operatives while achieving superior build quality. Government commitments to seismic resilience, embodied in national building codes and MLIT-led retrofit programs, will sustain modular demand across both new development and reconstruction segments. Digital transformation through building information modeling, robotic assembly, and digital twin-enabled quality management will continue elevating manufacturing precision and project delivery efficiency. The Kanto region will remain the dominant growth engine, while emerging regional markets will gain momentum through infrastructure investment and tourism-linked construction activity. The market generated a revenue of USD 18.11 Billion in 2025 and is projected to reach a revenue of USD 29.27 Billion by 2034, growing at a compound annual growth rate of 5.65% from 2026-2034.

Japan Modular Construction Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Permanent |

58.4% |

|

Material |

Wood |

42.3% |

|

End User |

Residential |

45.6% |

|

Region |

Kanto Region |

38.5% |

Type Insights:

- Permanent

- Re-locatable

Permanent dominates with a market share of 58.4% of the total Japan modular construction market in 2025.

Permanent modular construction encompasses structures intended for long-term, fixed-location use and represents the predominant construction type in Japan, favored for its structural integrity, design flexibility, and lifecycle performance advantages. These factory-built structures are constructed to the same or superior standards as conventionally built buildings, leveraging manufacturing precision to deliver consistent quality in wall assemblies, thermal insulation, and integrated mechanical systems. In Japan, permanent modular applications are especially prevalent in residential development, where developers deploy multi-story prefabricated housing systems to accommodate urban density demands efficiently and safely.

The enduring dominance of permanent modular construction in Japan reflects its alignment with the country's stringent building regulatory environment, which mandates high seismic resistance, energy efficiency, and structural durability across all building types. Factory-based production enables manufacturers to integrate seismic isolation systems, barrier-free design elements, and energy-saving technologies directly during module fabrication, reducing on-site complexities and schedule risk. The growing government emphasis on long-life, high-quality housing through quality certification and performance-labeling frameworks further reinforces preference for permanent modular systems, cementing their leadership position across the Japan modular construction market.

Material Insights:

- Steel

- Wood

- Concrete

- Others

Wood leads with a share of 42.3% of the total Japan modular construction market in 2025.

Wood holds a commanding position in Japan's modular construction material landscape, underpinned by the country's centuries-old tradition of timber architecture and a deeply established prefabricated wood building industry. Engineered timber products, particularly cross-laminated timber panels and glulam structural elements, have gained significant traction by offering high structural strength-to-weight ratios, excellent seismic performance, and substantially lower carbon embodied content compared to concrete and steel alternatives. Japan's pro-timber government policies actively encourage forest utilization and wood construction, providing financial incentives and certification pathways that favor wood-based modular projects in both residential and emerging commercial applications.

The growing acceptance of mass timber modular construction has been further accelerated by Japan's ambitious carbon neutrality targets and binding energy-efficiency mandates, which compel developers to select low-embodied-carbon materials capable of achieving net-zero performance benchmarks. A network of domestic timber processing firms and prefabricated wood homebuilders, with extensive expertise in panelized wall, roof, and floor systems, provides the supply-chain depth needed to scale wood-based modular delivery reliably. Joint research initiatives between leading universities and construction firms are continuously improving wood modular panel technology, fire resistance, and acoustic performance, broadening the application range of wood into mid-rise and commercial modular projects across Japan.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

Residential exhibits a clear dominance with a 45.6% share of the total Japan modular construction market in 2025.

Residential construction remains the largest and most enduring demand driver for modular construction in Japan, sustained by the country's unique combination of dense urban housing needs, favorable prefabrication tradition, and worsening labor constraints. Japan's major metropolitan regions, particularly those centered on Tokyo in the Kanto region and Osaka in Kansai, generate consistent demand for affordable, rapidly deployable housing that modular methods are well-positioned to satisfy. The aging population trend is creating additional demand for compact, barrier-free prefabricated homes designed for senior residents, while rising land costs in urban cores push developers toward high-efficiency modular multi-story solutions.

The deep-rooted culture of modular homebuilding in Japan, where lead times from order to move-in can be as short as 40 days, has cultivated a consumer preference for precision-manufactured, customizable homes that align with modular construction's core strengths. Government policy reinforces residential modular growth through mandatory energy-efficiency standards, earthquake-resistance certification requirements, and subsidies for high-performance housing. The growing zero-energy home market, supported by updated national building codes effective from April 2025, further strengthens the residential segment's centrality to Japan's overall modular construction market development.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represent the leading segment with a 38.5% share of the total Japan modular construction market in 2025.

The Kanto Region, anchored by the Tokyo metropolitan area, holds a commanding position in the Japan modular construction market owing to its unparalleled population density, sustained residential and commercial development pipeline, and concentration of major construction firms and prefabricated building manufacturers. Tokyo's persistent housing demand, driven by urban migration, limited developable land, and a growing preference for smart, energy-efficient homes, creates consistent and large-scale opportunities for modular delivery. The region's early and comprehensive adoption of Building Information Modeling and net-zero building codes positions Kanto as the national benchmark for advanced modular construction practice.

Kanto's outsized market contribution is also supported by a dense network of transport infrastructure that facilitates efficient factory-to-site module logistics across the broader metropolitan corridor. Large-scale redevelopment projects in central Tokyo, including mixed-use tower complexes spanning millions of square meters, drive demand for modular components across structural, MEP, and facade systems. Government investment in seismic retrofitting of aging buildings and urban resilience programs further bolsters construction activity in the region. The combination of private-sector investment depth, regulatory leadership, and infrastructure maturity entrenches Kanto's dominant role in shaping the trajectory of Japan's modular construction market.

Market Dynamics:

Growth Drivers:

Why is the Japan Modular Construction Market Growing?

Acute Labor Shortages Driving Transition to Factory-Based Construction

Japan's construction industry is confronting one of the most severe labor shortages of any major economy, a structural challenge rooted in decades of demographic decline and an aging craft workforce. The rapid graying of Japan's population has substantially reduced the pool of available skilled tradespeople, creating critical bottlenecks in on-site construction operations that constrain project delivery timelines and elevate wage costs. Young workers are increasingly reluctant to enter physically demanding, weather-exposed construction occupations, further deepening the workforce gap. Modular construction directly and effectively addresses this challenge by shifting the majority of productive work from outdoor construction sites to climate-controlled, automation-equipped manufacturing facilities. Factory settings enable the deployment of robotic assembly lines, precision cutting equipment, and standardized workflows that dramatically reduce the skilled-labor-per-unit requirement relative to conventional building methods. Japan's major construction firms are actively investing in modular production technologies, factory capacity expansion, and digital workflow integration to sustainably scale output without proportional increases in headcount. As the labor shortage continues to intensify with each passing year, modular construction's labor efficiency advantage becomes an increasingly decisive competitive differentiator in the market, reinforcing its long-term adoption trajectory across all building segments.

Rising Demand for Earthquake-Resistant and Disaster-Resilient Buildings

Japan's position as one of the world's most seismically active nations creates a perpetual and powerful structural demand driver for construction methods that can reliably deliver earthquake-resistant buildings at scale. Modular construction excels in this context because factory-fabricated modules can be engineered to exacting seismic specifications including base isolation systems, seismic damping mechanisms, and reinforced connection hardware that far exceed minimum code requirements. The controlled manufacturing environment eliminates the variability and quality risks associated with on-site construction in adverse weather or post-disaster conditions. National resilience initiatives, backed by substantial multi-year public investment, consistently prioritize construction approaches that combine speed of delivery with demonstrable structural performance, making modular methods the preferred strategic tool for Japan's disaster-preparedness and recovery infrastructure agenda.

Government Policy and Sustainability Mandates Accelerating Modular Adoption

Japan's regulatory and policy environment is a formidable growth catalyst for the modular construction market, with an expanding set of government mandates, incentive programs, and certification schemes specifically aligned with modular construction's inherent strengths. The Ministry of Land, Infrastructure, Transport and Tourism has established comprehensive Building Information Modeling guidelines that strongly encourage digital-first construction practices, creating a natural upstream driver for modular methods that are inherently BIM-compatible. New energy-efficiency standards mandated from April 2025 require all newly constructed buildings to achieve significantly higher thermal performance and carbon efficiency, specifications that modular manufacturers, with their factory-controlled insulation and airtightness processes are particularly well equipped to satisfy. Tax reductions for green-certified residential and commercial projects, combined with subsidies for energy-efficient home retrofits and zero-energy housing, make modular options economically compelling for cost-sensitive developers and buyers. Japan's ambitious national carbon-neutrality targets have further elevated demand for timber-based modular systems, as engineered wood construction offers a pathway to dramatically lower embodied carbon relative to steel and concrete alternatives. The interlocking set of regulatory requirements, financial incentives, and sustainability goals collectively functions as a comprehensive policy ecosystem that structurally advantages modular construction across the market.

Market Restraints:

What Challenges the Japan Modular Construction Market is Facing?

High Initial Capital Investment and Complex Supply Chain Requirements

Establishing modular construction manufacturing infrastructure demands substantial upfront capital investment in factory facilities, precision equipment, and robotic assembly systems. For smaller construction firms, the cost barrier to entering or scaling modular production is prohibitive, limiting market participation to larger, well-capitalized players. Additionally, modular projects require highly coordinated supply chains for components, materials, and logistics, particularly for transportation of large modules to urban sites with constrained access, adding operational complexity and cost. Rising raw material prices and producer price index volatility further compress project margins, making accurate cost forecasting difficult and occasionally undermining the financial case for modular adoption relative to conventional construction in price-sensitive market segments.

Design Flexibility Constraints and Consumer Perception Challenges

Despite ongoing advances in modular design technology, perceptions of limited architectural flexibility remain a challenge for the Japan modular construction market. Certain building typologies, particularly high-end luxury residential and architecturally distinctive commercial developments, are difficult to fully realize within standard module dimensions and connection systems, reducing modular's attractiveness to premium-market clients. Consumer skepticism about the long-term quality, resale value, and aesthetic appeal of modular buildings, though diminishing as the market matures, continues to act as a friction point in certain buyer segments. Overcoming these embedded perceptions requires sustained investment in design showcasing, consumer education, and the development of mass-customization platforms that can convincingly demonstrate modular's ability to match bespoke construction outcomes.

Land Scarcity and Regulatory Complexity in Dense Urban Markets

Japan's densely urbanized environments, particularly in the Kanto and Kansai regions, present logistical and regulatory challenges that complicate modular construction deployment. Narrow streets, limited staging areas, and strict noise and vibration ordinances make it difficult to maneuver and assemble large, prefabricated modules efficiently, adding cost and scheduling risk to urban projects. Complex zoning regulations and building approval processes, which do not always fully accommodate the distinctive characteristics of modular construction methods, can extend project permitting timelines, partially offsetting the speed advantage that modular delivery typically provides. Streamlining the regulatory framework to better accommodate off-site manufacturing approaches remains an important systemic need for the market's continued urban expansion.

Competitive Landscape:

The Japan modular construction market is characterized by a moderately concentrated competitive structure, with a small number of large, vertically integrated homebuilders and construction firms holding substantial market positions built over decades of domestic prefabricated building expertise. These leading players differentiate through proprietary factory automation technologies, integrated digital design platforms, and comprehensive after-sales service networks. Competitive dynamics are intensifying as established firms invest in manufacturing capacity expansion and technology upgrades, while mid-tier contractors increasingly access shared prefabrication hubs to improve competitiveness. University-industry partnerships, government-backed consortia on timber technology, and digital construction collaborations between construction firms and technology companies are broadening the innovation landscape. International market expansion by major domestic players also reflects competitive confidence in Japan's modular construction expertise as a globally deployable capability.

Recent Developments:

- In February 2025, INFRONEER Holdings and Accenture jointly launched INFRONEER Strategy & Innovation, a new venture designed to digitize asset management and address skilled labor shortages across Japan's construction sector. The initiative integrates artificial intelligence and advanced data analytics into construction planning and facility management workflows, directly supporting modular and prefabricated building applications by enhancing production scheduling, resource allocation, and project quality control.

Japan Modular Construction Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Permanent, Re-locatable |

| Materials Covered | Steel, Wood, Concrete, Others |

| End Users Covered | Residential, Commercial, Industrial |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Modular Construction Market Report

The Japan modular construction market size was valued at USD 18.11 Billion in 2025.

The Japan modular construction market is expected to grow at a compound annual growth rate of 5.65% from 2026-2034 to reach USD 29.27 Billion by 2034.

Permanent dominated the market with a share of 58.4%, owing to its widespread use in long-term residential and commercial developments, structural durability, and strong alignment with Japan's seismic safety and energy-efficiency regulatory requirements.

Key factors driving the Japan modular construction market include acute skilled labor shortages accelerating off-site manufacturing adoption, rising demand for seismically resilient building solutions, government-led Building Information Modeling mandates, updated energy-efficiency standards, green building incentives, and rapid urbanization generating sustained housing demand.

Major challenges include high initial capital investment for factory infrastructure, limited architectural design flexibility in standard modular systems, consumer perception barriers around quality and resale value, complex urban site logistics in dense metropolitan areas, land scarcity constraining module assembly, and regulatory processes not fully adapted to modular construction methods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)