Japan Next-Generation Sequencing Market Size, Share, Trends and Forecast by Sequencing Type, Product Type, Technology, Application, End User, and Region, 2026-2034

Japan Next-Generation Sequencing Market Size, Share, Trends & Forecast (2026-2034)

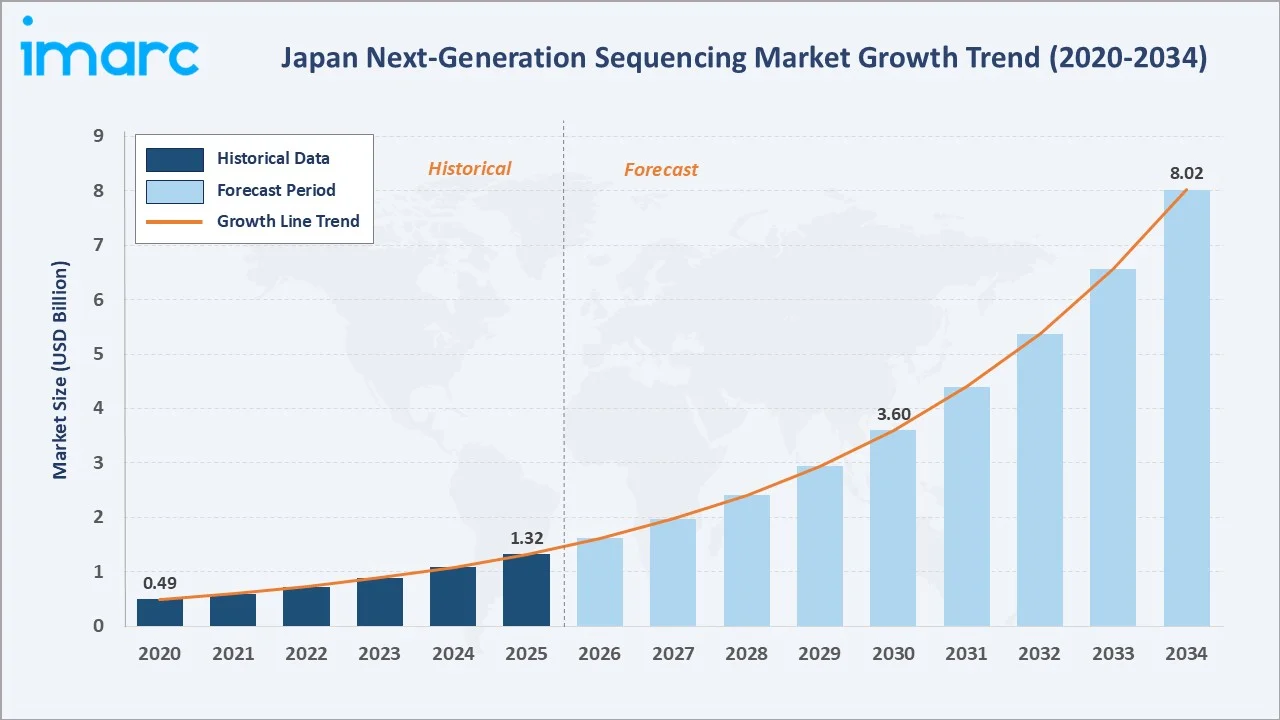

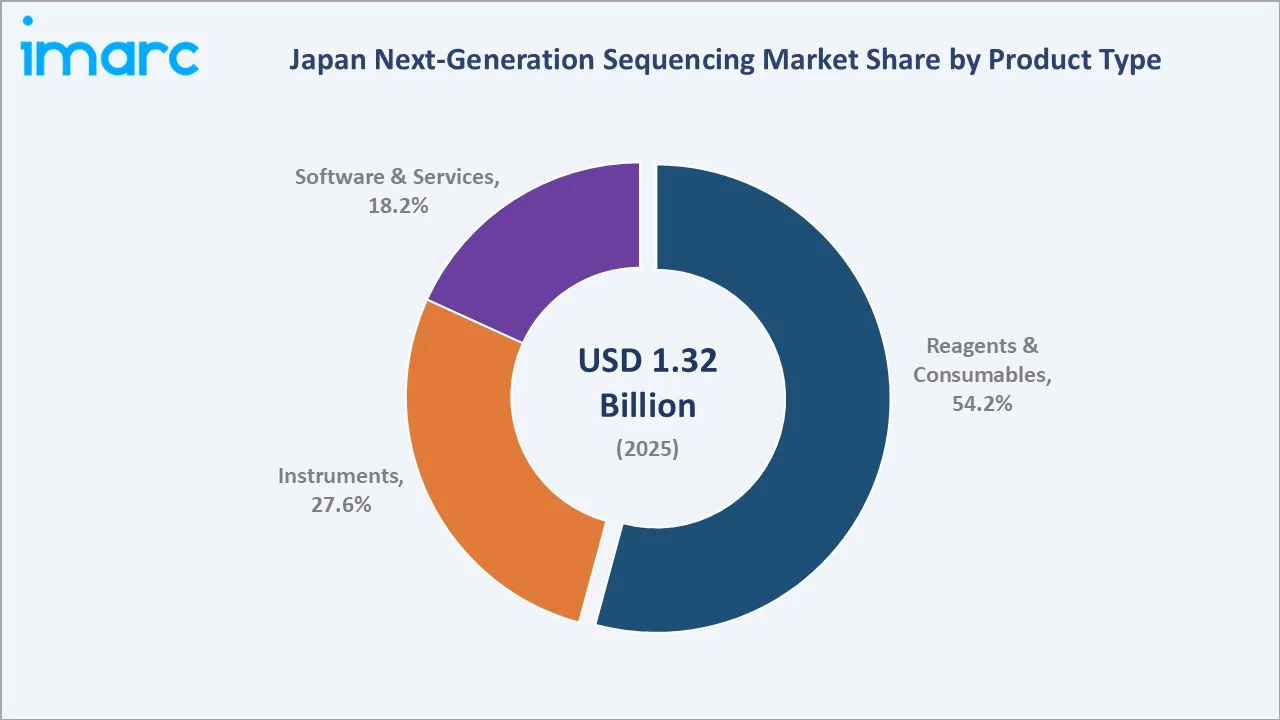

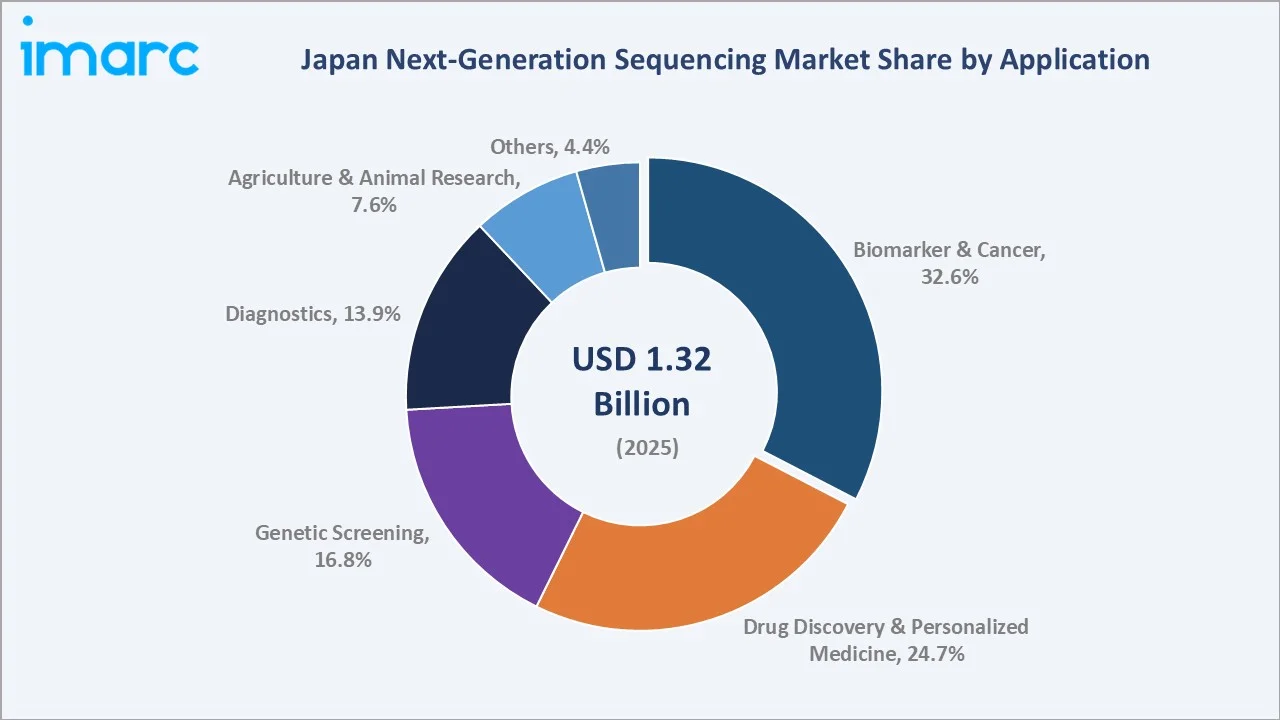

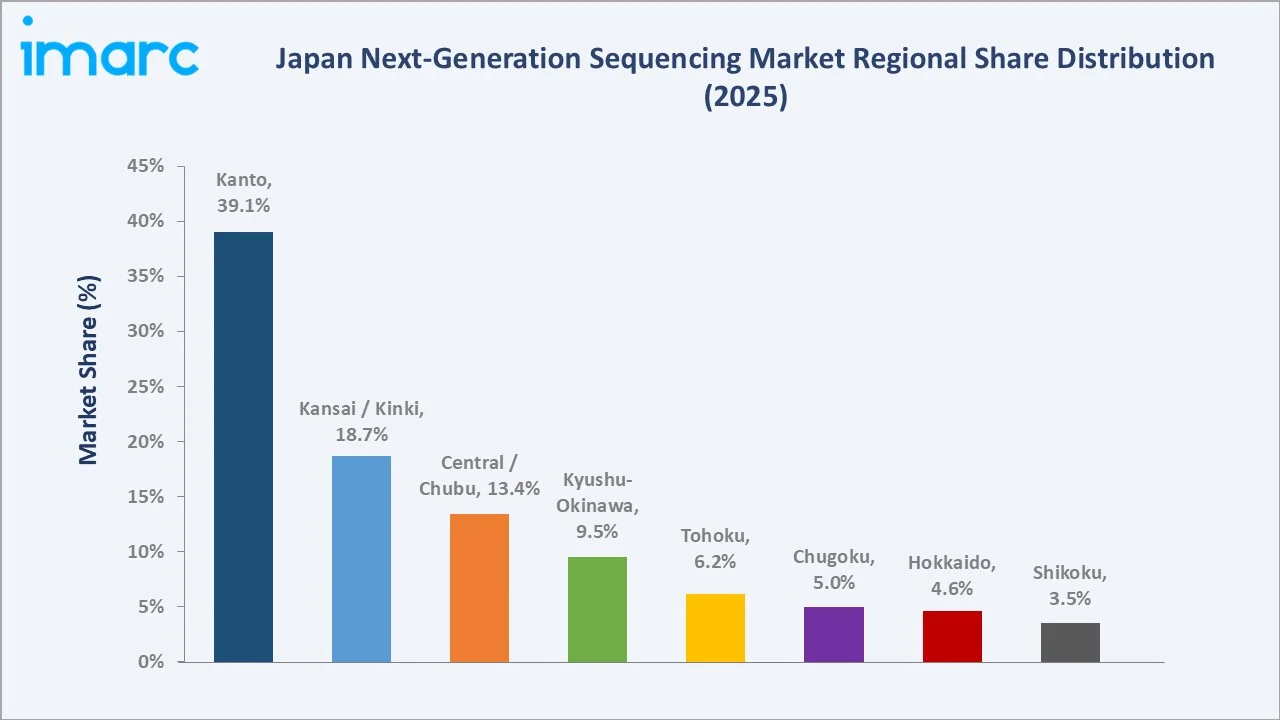

The Japan next-generation sequencing market size was valued at USD 1.32 Billion in 2025 and is projected to reach USD 8.02 Billion by 2034, exhibiting a CAGR of 22.18% during the forecast period 2026-2034. Rapidly falling sequencing costs, expanding precision oncology coverage, and government-funded genome initiatives are driving the Japan next-generation sequencing market growth. Reagents and consumables lead at 54.2% share in 2025, while biomarker and cancer applications account for 32.6% of total revenue. The Kanto region dominates with 39.1% of national demand in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.32 Billion |

|

Forecast Market Size (2034) |

USD 8.02 Billion |

|

CAGR (2026-2034) |

22.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto (39.1% share, 2025) |

|

Leading Product Type |

Reagents and Consumables (54.2%, 2025) |

|

Leading Application |

Biomarker and Cancer (32.6%, 2025) |

The Japan next-generation sequencing market growth trajectory from 2020 through 2034 contrasts a strong historical expansion against a steep forecast curve, supported by the Cancer Genomic Medicine programme, the AMED-led Initiative on Rare and Undiagnosed Diseases, BioBank Japan expansion, and rapidly falling per-genome sequencing costs across major Japanese hospitals and research centres.

To get more information on this market, Request Sample

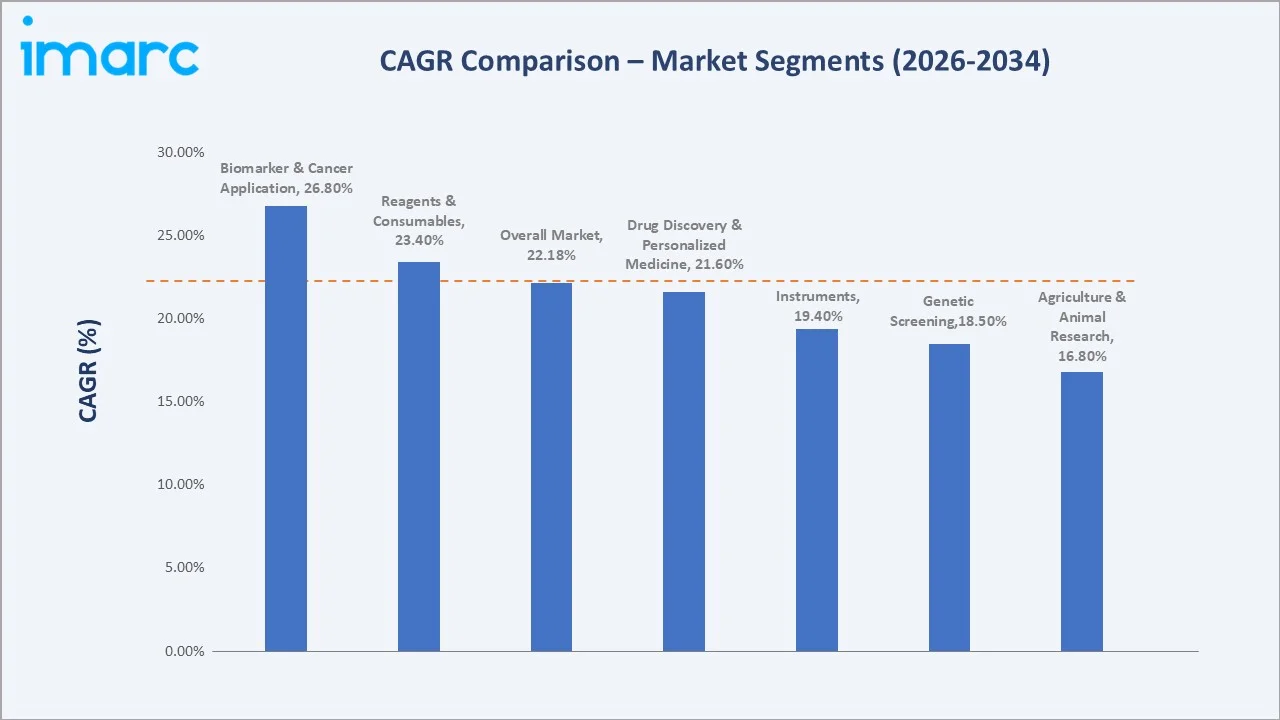

Segment-level CAGR comparisons highlight the biomarker and cancer application and the reagents and consumables product type as the fastest-growing sub-segments within the broader Japan next-generation sequencing market forecast through 2034, while traditional agriculture and animal-research applications grow at a more measured pace.

Executive Summary

The Japan next-generation sequencing market is undergoing a profound structural transformation. It is shaped by surging precision oncology adoption, the country's expanding genomic medicine programme, and a maturing bioinformatics ecosystem. Valued at USD 1.32 Billion in 2025, the market is projected to reach USD 8.02 Billion by 2034 at a CAGR of 22.18%, expanding strongly from USD 0.49 Billion recorded in 2020.

Reagents and consumables command 54.2% of market revenue in 2025, supported by recurring library preparation kits, flow cells, primers, and enzymes used across hospital, pharma, and academic sequencing workflows. Instruments follow at 27.6%, anchored by Illumina NovaSeq, NextSeq, MiSeq, Thermo Fisher Ion Torrent, PacBio Revio, and Oxford Nanopore platform deployments. Software and services contribute 18.2%, driven by demand for variant calling, secondary and tertiary analysis, and bioinformatics service contracts.

The Kanto region leads with a 39.1% revenue share in 2025, anchored by Tokyo, Yokohama, and Tsukuba research clusters. Biomarker and cancer applications dominate by use case at 32.6%, reflecting Japan's high cancer prevalence and the maturity of cancer genomic medicine reimbursement under the National Health Insurance system. The Japan next-generation sequencing market outlook remains exceptionally strong as precision oncology expansion, AMED-funded research, BioBank Japan growth, and AI-driven variant interpretation converge through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Reagents and Consumables – 54.2% share (2025) |

|

Second Product Type |

Instruments – 27.6% share (2025) |

|

Largest Application |

Biomarker and Cancer – 32.6% share (2025) |

|

Fastest-Growing Application |

Biomarker & Cancer – ~26.8% CAGR (2026-2034) |

|

Leading Region |

Kanto – 39.1% revenue share (2025) |

|

Top Companies |

Illumina Inc., Thermo Fisher Scientific Inc, Pacific Biosciences of California Inc., Oxford Nanopore Technologies Plc, F. Hoffmann-La Roche Ltd |

|

Forecast Market Size (2034) |

USD 8.02 Billion |

Key Analytical Observations Supporting the Above Data:

- Reagents and consumables' 54.2% dominance in 2025 reflects the recurring nature of next generation sequencing workflows. Library preparation kits, flow cells, primers, and reagent cartridges drive consistent demand across Japanese hospitals, pharma research labs, and academic genomics centres.

- Instruments' 27.6% share captures sequencer placements across teaching hospitals, cancer centres, and contract research organizations. Illumina NovaSeq X, NextSeq 2000, PacBio Revio, and Oxford Nanopore PromethION continue to anchor the high-end of the Japanese installed base.

- Software and services' 18.2% position is the fastest-rising tier-2 segment. Demand reflects variant calling pipelines, secondary and tertiary bioinformatics analysis, cloud-based genomic data platforms, and outsourced sequencing services delivered by Macrogen Japan, BGI Japan, and others.

- Biomarker and cancer applications' 32.6% lead reflects Japan's high cancer prevalence and the integration of comprehensive genomic profiling into reimbursed clinical workflows under the National Health Insurance scheme. Foundation Medicine CDx and OncoGuide NCC Oncopanel are widely used.

- Drug discovery and personalized medicine's 24.7% share is propelled by Japanese pharma sponsors such as Takeda, Astellas, Daiichi Sankyo, and Eisai integrating next generation sequencing into target identification, biomarker discovery, and companion diagnostic development across oncology and rare-disease pipelines.

- Kanto's 39.1% regional dominance is anchored by Tokyo, Yokohama, and Tsukuba clusters. The University of Tokyo, RIKEN Yokohama, AMED, the National Cancer Center, and BioBank Japan all concentrate in this region, supporting the country's deepest next generation sequencing infrastructure footprint.

Japan Next-Generation Sequencing Market Overview

Next generation sequencing (NGS) refers to massively parallel sequencing technologies that enable rapid, high-throughput, and cost-effective characterization of nucleic acid molecules. The Japan next-generation sequencing market spans short-read platforms from Illumina and Thermo Fisher, long-read platforms from Pacific Biosciences and Oxford Nanopore, reagents and consumables, software and services, and end-to-end sequencing services delivered by domestic and global providers.

The industry sits at the intersection of life-sciences research, clinical diagnostics, and pharmaceutical drug discovery. Macroeconomic and policy drivers include the Cancer Genomic Medicine framework launched by MHLW, the Initiative on Rare and Undiagnosed Diseases coordinated through AMED, BioBank Japan's expanded biospecimen collection, and the National Cancer Center Hospital's leadership in comprehensive genomic profiling. The Japan next-generation sequencing industry analysis must also factor in the continued decline in per-genome sequencing costs, which has fallen by orders of magnitude over the past decade.

Market Dynamics

To evaluate market opportunities, Request Sample

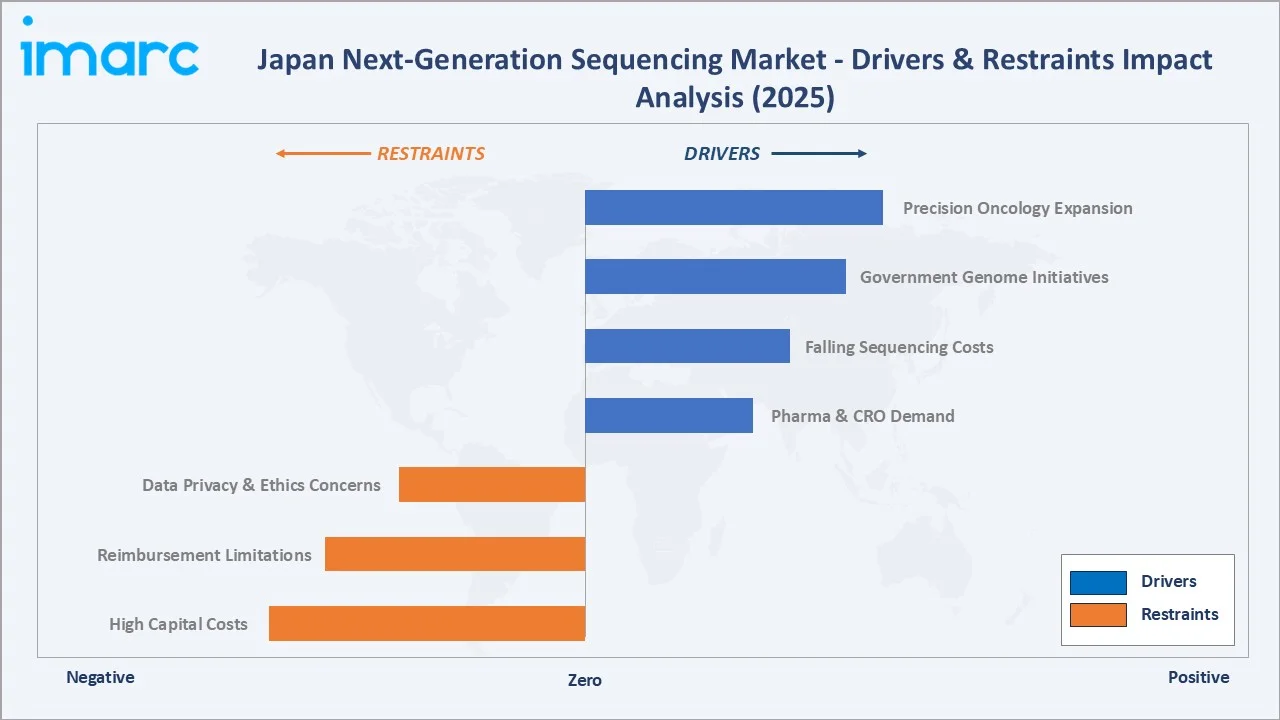

Market Drivers

- Precision Oncology Expansion: Japan's Cancer Genomic Medicine framework reimburses comprehensive genomic profiling tests under the National Health Insurance system. Foundation Medicine CDx and OncoGuide NCC Oncopanel are now embedded in standard care pathways at designated cancer-genomic-medicine core hospitals across the country.

- Government Genome Initiatives: AMED-funded programmes including the Initiative on Rare and Undiagnosed Diseases (IRUD), BioBank Japan, and the Genome Cohort Project channel sustained capital into next generation sequencing infrastructure across the country's research and clinical institutions.

- Falling Sequencing Costs: Per-genome sequencing costs have fallen by orders of magnitude over the past decade. Newer platforms such as Illumina NovaSeq X and PacBio Revio further reduce per-sample costs, expanding feasible use cases across diagnostics, drug discovery, and population-scale genomics.

- Pharma and CRO Demand: Japanese pharmaceutical sponsors such as Takeda, Astellas, Daiichi Sankyo, and Eisai continue to deepen next generation sequencing adoption for target identification, biomarker discovery, and companion diagnostic development. Domestic and global CROs serving Japan are scaling next generation sequencing service capacity accordingly.

Market Restraints

- High Capital Costs: High-throughput sequencer installations and supporting infrastructure remain capex-intensive. Smaller hospitals, regional research centres, and emerging biotechs continue to face budget barriers in adopting top-tier next generation sequencing platforms across Japan.

- Reimbursement Limitations: While oncology reimbursement is mature under the Japanese system, reimbursement coverage for non-oncology next generation sequencing applications remains uneven. Whole-genome sequencing for rare disease, polygenic risk scoring, and prenatal screening still face restricted reimbursement pathways.

- Data Privacy and Ethics Concerns: Japan's Act on the Protection of Personal Information and ethical guidelines for genomic and clinical research require careful consent management, secure data hosting, and ongoing compliance investments by all next generation sequencing service providers operating in the country.

Market Opportunities

- Liquid Biopsy and ctDNA-Based Diagnostics: Circulating tumour DNA (ctDNA) testing is gaining traction in Japan. Foundation Medicine Liquid CDx, Guardant360 CDx, and locally developed liquid biopsy assays are reshaping treatment selection and minimal residual disease monitoring across Japanese cancer centres.

- Population Genomics and Long-Read Sequencing: BioBank Japan's expanding biospecimen base, combined with the rising adoption of long-read PacBio and Oxford Nanopore platforms, supports next-generation population genomics and structural variant studies through 2034. This is a high-margin growth tier for instrument and reagent suppliers.

Market Challenges

- Skilled Bioinformatics Talent Gap: Hiring qualified bioinformaticians, clinical genomicists, and variant-curation specialists remains a structural challenge. AMED and several universities have launched dedicated training programmes, but talent supply continues to lag demand growth through 2025-2030.

- Variant Interpretation Standardization: Variant classification consistency across Japanese clinical laboratories remains a complex challenge. National efforts to standardize ACMG-aligned interpretation, AI-assisted annotation, and curated knowledgebase access are progressing but require sustained investment through 2034.

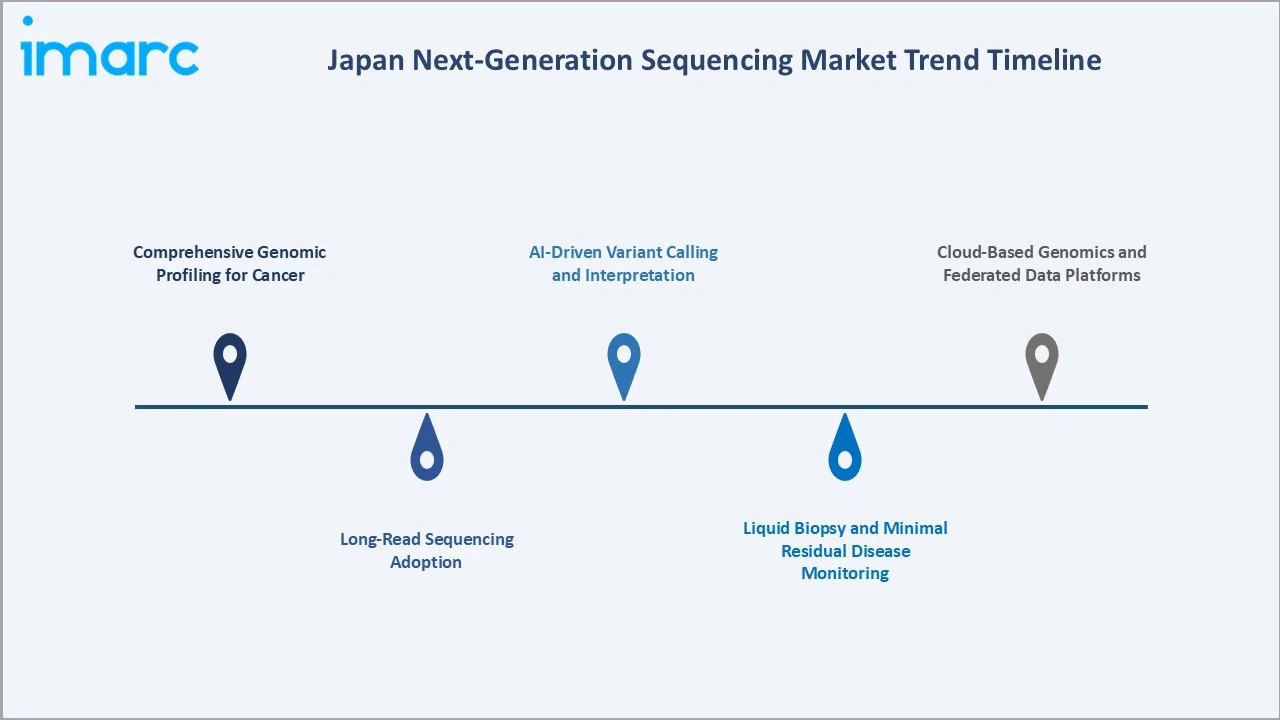

Emerging Market Trends

1. Comprehensive Genomic Profiling for Cancer

Comprehensive genomic profiling tests such as Foundation Medicine CDx and OncoGuide NCC Oncopanel are now standard at Japan's designated cancer-genomic-medicine core hospitals. Reimbursement under the National Health Insurance scheme has steadily expanded the patient population eligible for testing through 2024-2025.

2. Long-Read Sequencing Adoption

PacBio Revio and Oxford Nanopore PromethION have meaningfully expanded long-read next generation sequencing adoption across Japanese genomics centres since 2023. Long-read sequencing is increasingly used for structural variant detection, transcript isoform characterization, and complex disease genomics.

3. AI-Driven Variant Calling and Interpretation

AI and machine-learning models are reshaping variant calling, annotation, and clinical interpretation. Tools such as Google's DeepVariant, Illumina DRAGEN, and locally developed AI pipelines are reducing turnaround times and improving consistency across Japanese clinical laboratories.

4. Liquid Biopsy and Minimal Residual Disease Monitoring

Circulating tumour DNA (ctDNA) testing is gaining clinical traction in Japan. Foundation Medicine Liquid CDx, Guardant360 CDx, and locally developed liquid biopsy assays are increasingly used for treatment selection, MRD monitoring, and early relapse detection across Japanese cancer centres.

5. Cloud-Based Genomics and Federated Data Platforms

Cloud-based genomics platforms - including AWS HealthOmics, Microsoft Azure Genomics, and Illumina Connected Analytics - are scaling rapidly in Japan. Federated data architectures, on-premises hybrid storage, and PMDA-compliant data residency frameworks are reshaping how Japanese institutions manage and share genomic data through 2034.

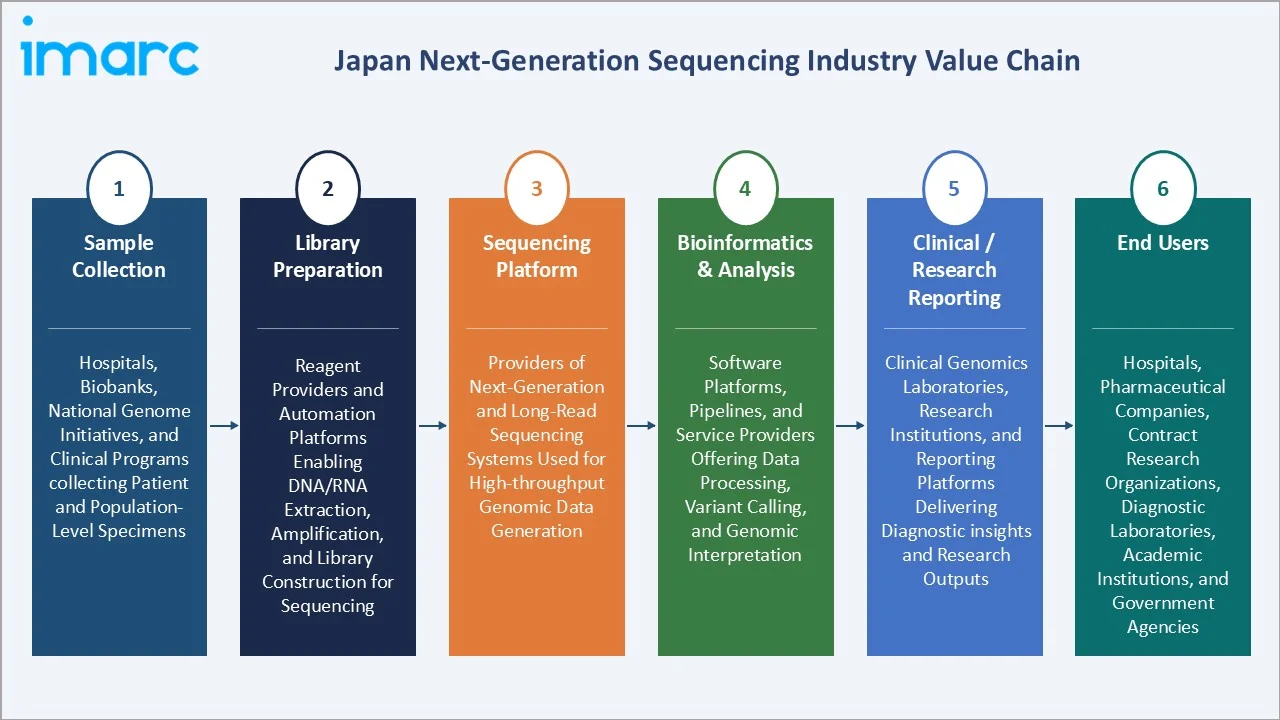

Industry Value Chain Analysis

The Japan next-generation sequencing industry value chain spans six integrated stages from sample collection through end-user reporting. Each stage shows distinct margin, capex, and regulatory profiles that shape the broader Japan next-generation sequencing market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Sample Collection |

Hospitals, biobanks, national genome initiatives, and clinical programs collecting patient and population-level specimens |

|

Library Preparation |

Reagent providers and automation platforms enabling DNA/RNA extraction, amplification, and library construction for sequencing |

|

Sequencing Platform |

Providers of next-generation and long-read sequencing systems used for high-throughput genomic data generation |

|

Bioinformatics & Analysis |

Software platforms, pipelines, and service providers offering data processing, variant calling, and genomic interpretation |

|

Clinical / Research Reporting |

Clinical genomics laboratories, research institutions, and reporting platforms delivering diagnostic insights and research outputs |

|

End Users |

Hospitals, pharmaceutical companies, contract research organizations, diagnostic laboratories, academic institutions, and government agencies |

Global sequencing platform providers and reagents suppliers capture the highest strategic value through scale, intellectual property, and recurring consumables revenue. Specialized service providers continue to differentiate through bioinformatics expertise, regulatory navigation under PMDA, and integrated clinical-trial next generation sequencing support that helps Japanese pharma sponsors and CROs accelerate biomarker programmes.

Technology Landscape in the Japan next-generation sequencing Industry

Short-Read Sequencing Platforms

Illumina NovaSeq X, NextSeq 2000, and MiSeq dominate the high-throughput short-read segment in Japan. Thermo Fisher Ion Torrent platforms continue to serve targeted clinical sequencing applications. These short-read platforms remain the workhorse for clinical NGS, biomarker discovery, and population-scale genomics across Japanese institutions.

Long-Read Sequencing and Single-Cell Technology

PacBio Revio and Oxford Nanopore PromethION are scaling rapidly in Japanese research centres for structural variant detection, full-length transcript characterization, and methylation analysis. Single-cell sequencing platforms from 10x Genomics also continue to expand across Japanese academic and pharma research workflows.

Bioinformatics, AI Variant Calling, and Cloud Genomics

Variant calling, annotation, and clinical interpretation are increasingly powered by AI. Illumina DRAGEN, Google DeepVariant, GATK, and locally developed AI pipelines are widely used across Japanese laboratories. AWS HealthOmics, Microsoft Azure Genomics, and Illumina Connected Analytics are reshaping how Japanese institutions store, analyse, and share large-scale genomic data.

Liquid Biopsy and ctDNA Technology

Circulating tumour DNA (ctDNA) sequencing continues to expand in Japan. Foundation Medicine Liquid CDx, Guardant360 CDx, and locally developed liquid biopsy assays are used for treatment selection, minimal residual disease monitoring, and early relapse detection across Japanese cancer centres - a high-growth frontier through 2034.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Japan next-generation sequencing market, along with forecasts at the national and regional level from 2026 to 2034. The market has been categorized based on product type and application.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Sequencing Type | 🔒 | 🔒 | 2025 |

| Product Type | Reagents and Consumables | 54.2% | 2025 |

| Technology | 🔒 | 🔒 | 2025 |

| Application | Biomarker and Cancer | 32.6% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Kanto Region | 39.1% | 2025 |

By Product Type

Reagents and consumables lead the Japan next-generation sequencing market with a 54.2% share in 2025. This segment is anchored by recurring demand for library preparation kits, flow cells, primers, enzymes, and reagent cartridges across hospital, pharma, and academic sequencing workflows. Vendors including Illumina, Thermo Fisher Scientific, New England Biolabs, Takara Bio, and QIAGEN K.K. lead supply across Japanese institutions, with subscription-style consumables agreements supporting predictable revenue growth.

To access detailed market analysis, Request Sample

Instruments hold 27.6% of revenue and capture sequencer placements across teaching hospitals, cancer centres, and contract research organizations. Illumina NovaSeq X, NextSeq 2000, MiSeq, Thermo Fisher Ion Torrent, PacBio Revio, and Oxford Nanopore PromethION anchor the high-end of the Japanese installed base. Software and services contribute 18.2%, driven by demand for variant calling pipelines, secondary and tertiary bioinformatics analysis, cloud-based genomic data platforms, and outsourced sequencing services delivered by Macrogen Japan, BGI Japan, GeneBay, and other domestic and regional providers.

By Application

Biomarker and cancer applications lead the Japan next-generation sequencing market at 32.6% of revenue in 2025. This segment reflects Japan's high cancer prevalence and the integration of comprehensive genomic profiling into reimbursed clinical workflows under the National Health Insurance scheme. Foundation Medicine CDx and OncoGuide NCC Oncopanel are widely deployed at Japan's designated cancer-genomic-medicine core hospitals, supporting treatment selection across solid tumours and haematologic malignancies.

Drug discovery and personalized medicine accounts for 24.7% of revenue, propelled by Japanese pharma sponsors such as Takeda, Astellas, Daiichi Sankyo, and Eisai integrating next generation sequencing into target identification, biomarker discovery, and companion diagnostic development. Genetic screening contributes 16.8%, supported by carrier screening, prenatal testing, and inherited disease panels. Diagnostics holds 13.9%, driven by infectious disease testing, pharmacogenomics, and rare-disease diagnostic odyssey shortening through whole-genome and exome sequencing. Agriculture and animal research represents 7.6%, anchored by aquaculture genomics, livestock breeding, and agricultural biotechnology applications. The Others category accounts for 4.4% and includes microbiome research, environmental genomics, and forensic applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto |

39.1% |

Tokyo, Yokohama, Tsukuba clusters; RIKEN, U. Tokyo, AMED, BioBank Japan, NCC |

|

Kansai / Kinki |

18.7% |

Osaka, Kyoto, Kobe; Kyoto U, Osaka U, RIKEN Kobe; pharma R&D base |

|

Central / Chubu |

13.4% |

Nagoya hub, Aichi prefecture research, manufacturing-linked biotech demand |

|

Kyushu-Okinawa |

9.5% |

Fukuoka, Kyushu U; growing southern research and clinical next generation sequencing adoption |

|

Tohoku |

6.2% |

Tohoku University, Tohoku Medical Megabank, regional cohort genomics |

|

Chugoku |

5.0% |

Hiroshima University, Okayama University; specialty research workflows |

|

Hokkaido |

4.6% |

Hokkaido University, Sapporo cluster; agricultural and aquaculture genomics |

|

Shikoku |

3.5% |

Smaller research base, niche academic and clinical next generation sequencing deployments |

The Kanto region leads with a 39.1% revenue share in 2025. Tokyo, Yokohama, and Tsukuba host the country's deepest concentration of next generation sequencing infrastructure, anchored by The University of Tokyo, RIKEN Yokohama, AMED, the National Cancer Center Hospital, and BioBank Japan. The region also concentrates Japan's largest pharma research operations and the bulk of cancer genomic medicine core hospitals.

Kansai/Kinki holds 18.7% of national revenue, anchored by Osaka, Kyoto, and Kobe. Kyoto University, Osaka University, RIKEN Kobe, and the Kobe Biomedical Innovation Cluster support strong academic and pharma next generation sequencing activity. The region also hosts significant pharmaceutical R&D operations from Takeda, Astellas, and other domestic players.

Central/Chubu contributes 13.4%, led by Nagoya and the broader Aichi prefecture research base. Nagoya University, Fujita Health University, and several manufacturing-linked biotech operations drive steady next generation sequencing adoption across academic, clinical, and industrial workflows. Kyushu-Okinawa accounts for 9.5%, anchored by Kyushu University and a growing Fukuoka-based research base. Tohoku at 6.2% is propelled by Tohoku University, the Tohoku Medical Megabank, and large prospective cohort studies. Chugoku (5.0%), Hokkaido (4.6%), and Shikoku (3.5%) round out the regional landscape, with Hokkaido in particular contributing aquaculture, agricultural, and environmental genomics workflows.

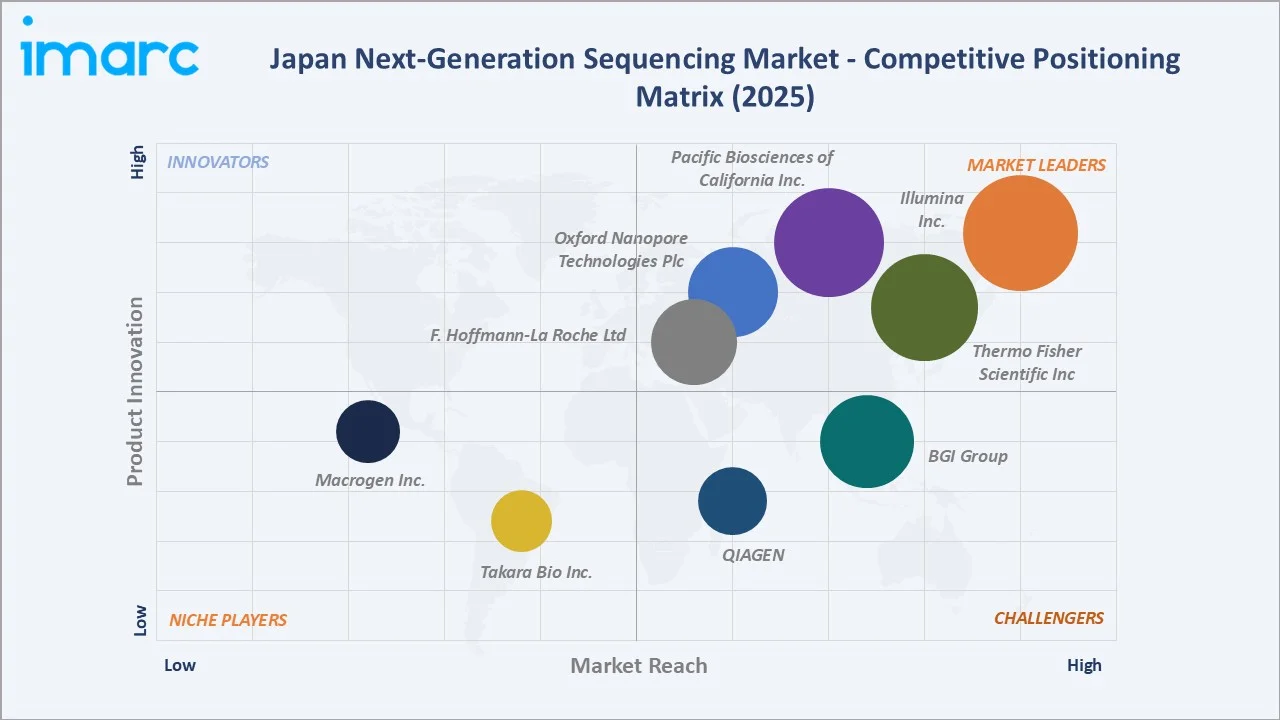

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Illumina Inc. |

Illumina |

Leader |

Largest installed base, market-defining short-read platforms, recurring consumables |

|

Thermo Fisher Scientific Inc |

Ion Torrent Rapid Next-Generation Sequencing (NGS) |

Leader |

Targeted clinical NGS, oncology panels, broad lab footprint |

|

Pacific Biosciences of California Inc. |

PacBio |

Leader |

HiFi long-read sequencing, structural variant leadership |

|

Oxford Nanopore Technologies Plc |

Oxford Nanopore Technologies |

Leader |

Real-time long-read sequencing, portable formats, methylation |

|

F. Hoffmann-La Roche Ltd |

Roche diagnostics k.k |

Leader |

Clinical NGS, companion diagnostics, hospital diagnostic footprint |

|

BGI Group |

MGI Tech |

Challenger |

Cost-competitive sequencing, growing Japan presence |

|

QIAGEN |

Qiagen K.K |

Challenger |

Sample-to-insight workflows, library prep, bioinformatics |

|

Takara Bio Inc. |

Takara Bio Inc. |

Emerging |

Japanese reagent supplier, library prep and consumables specialist |

|

Macrogen Inc |

Macrogen |

Emerging |

Sequencing services, bioinformatics, pharma and academic clients |

The competitive landscape in the Japan next-generation sequencing market is moderately concentrated. Tier-1 platform providers such as Illumina, Thermo Fisher, Pacific Biosciences, Oxford Nanopore, and Roche Diagnostics compete on platform scale, sequencing accuracy, recurring reagent revenue, and clinical-grade regulatory navigation under PMDA. Mid-market players including MGI Tech and QIAGEN differentiate through cost-competitive systems and integrated sample-to-insight workflows. Domestic specialists such as Takara Bio and Macrogen Japan continue to play important roles in reagents, services, and pharma-aligned next generation sequencing support.

Key Company Profiles

Illumina Inc.

Illumina K.K. is the Japanese subsidiary of Illumina Inc., the global leader in next generation sequencing platforms, headquartered in San Diego, California. Illumina K.K. supports Japan's largest next generation sequencing installed base across hospitals, pharma sponsors, CROs, and academic institutions through Tokyo-headquartered local operations.

- Product & Platform Portfolio: Illumina's portfolio in Japan spans the NovaSeq X, NovaSeq 6000, NextSeq 2000, NextSeq 1000, MiSeq, and iSeq sequencing platforms, alongside library preparation kits, flow cells, reagents, the DRAGEN bioinformatics platform, Connected Analytics cloud genomics, and integrated companion diagnostic offerings.

- Recent Developments: In February 2026, Illumina launched TruPath Genome and unveiled a comprehensive roadmap for its NovaSeq X Series. The roadmap includes major performance upgrades such as increased sequencing output, improved accuracy (up to Q70 quality scores), faster turnaround times, and enhanced workflow flexibility. These advancements are expected to significantly boost productivity and reduce the cost of large-scale genomic studies.

- Strategic Focus: Illumina K.K.'s strategy centres on scaling the NovaSeq X installed base, deepening DRAGEN AI bioinformatics adoption, expanding clinical next generation sequencing applications under PMDA pathways, and supporting Japanese pharma sponsors with companion diagnostic and translational genomics services through 2034.

Thermo Fisher Scientific Inc.

Thermo Fisher Scientific Inc. is a global leader in life-sciences instrumentation and reagents, headquartered in Waltham, Massachusetts, with significant Japan operations supporting the country's NGS, qPCR, and broader genomics workflows. The company operates extensive Japanese commercial and technical-support infrastructure across Tokyo, Yokohama, and Osaka.

- Product & Platform Portfolio: Thermo Fisher's next generation sequencing portfolio in Japan includes the Ion Torrent platform family (Ion GeneStudio S5, Ion Chef), Oncomine targeted oncology panels, AmpliSeq library preparation kits, Applied Biosystems sequencing reagents, and integrated bioinformatics solutions for clinical and translational research applications.

- Recent Developments: In 2024, Thermo Fisher expanded its oncology next generation sequencing capabilities through Oncomine-based companion diagnostics and collaborations, including a strategic alliance with Japan’s National Cancer Center East Hospital, while advancing automated sample-to-answer workflows via its Ion Torrent Genexus system.

- Strategic Focus: Thermo Fisher's strategy in Japan focuses on targeted clinical next generation sequencing leadership, deepening Oncomine and AmpliSeq adoption, supporting Japanese pharma sponsors and CROs with integrated genomics services, and leveraging its broad reagents and instruments portfolio to capture share across Japan's expanding next generation sequencing market through 2034.

Pacific Biosciences of California Inc.

Pacific Biosciences of California Inc. (PacBio) is a leader in long-read sequencing technology, headquartered in Menlo Park, California. PacBio's HiFi long-read sequencing platforms have become foundational tools for structural variant detection, full-length transcript characterization, and complex genome assembly across Japanese genomics centres.

- Product & Platform Portfolio: PacBio's Japan portfolio spans the Revio long-read sequencer, Sequel IIe, the Onso short-read platform, SMRT cell consumables, and integrated bioinformatics tools for HiFi data analysis. The company supports Japanese customers through both direct operations and key Japanese distribution and service partners.

- Recent Developments: In October 2025, PacBio announced major upgrades to its Revio and Vega sequencing platforms aimed at significantly reducing genome sequencing costs while expanding multiomic capabilities. The company introduced its new SPRQ-Nx sequencing chemistry, designed to deliver its most cost-efficient HiFi genome to date, with potential pricing dropping below $300 per genome at scale and up to ~40% cost reduction for high-throughput users.

- Strategic Focus: PacBio's strategic focus in Japan centres on scaling Revio HiFi long-read adoption, deepening clinical research applications, expanding structural variant and methylation analysis capabilities, and supporting Japanese pharma sponsors and academic research groups with high-accuracy long-read data through 2034.

Market Concentration Analysis

The Japan next-generation sequencing market exhibits high concentration. Illumina K.K. alone is estimated to account for over 50% of Japan next-generation sequencing revenue in 2025, with the top five players – Illumina Inc., Thermo Fisher Scientific Inc, Pacific Biosciences of California Inc., Oxford Nanopore Technologies Plc, F. Hoffmann-La Roche Ltd - collectively capturing more than 80% of the market. The remaining share is distributed across MGI Tech, QIAGEN K.K., Takara Bio, Macrogen Japan and a long tail of regional service and software providers.

The market is undergoing measured shifts in concentration. While Illumina retains dominant short-read leadership, Pacific Biosciences and Oxford Nanopore continue to capture share in long-read applications, and MGI Tech is gaining traction with cost-competitive systems. Japanese reagent and service specialists such as Takara Bio and Macrogen Japan remain important players in domestic supply chains. M&A and partnership activity continues to reshape the competitive set through 2034.

Investment & Growth Opportunities

Fastest-Growing Sub-Segments

Biomarker and cancer applications represent the highest-growth sub-segment at approximately 26.8% CAGR through 2034. Reagents and consumables follow at roughly 23.4% CAGR, supported by recurring library preparation kit and flow cell demand. Drug discovery and personalized medicine, alongside long-read sequencing applications, round out the highest-momentum opportunities for capital deployment.

Emerging Sub-Markets

Liquid biopsy and ctDNA-based diagnostics, AI-driven variant interpretation tools, cloud-based genomics platforms, single-cell sequencing applications, and population-scale long-read genomics all represent above-trend growth pockets through 2034. Japan's expanded BioBank Japan footprint and the Tohoku Medical Megabank further support large-scale population-genomics build-outs.

Strategic Investment Trends

Strategic capital continues to flow into the Japan next-generation sequencing ecosystem. Global platform providers continue to expand Japanese commercial and technical-support footprints. Domestic and global venture capital is funding bioinformatics start-ups, liquid biopsy ventures, and AI-led variant interpretation tools. Japanese pharma corporate venture arms are also actively co-investing in NGS-enabled biomarker and companion diagnostic platforms through 2034.

Future Market Outlook (2026-2034)

The Japan next-generation sequencing market forecast projects exceptional value expansion from USD 1.32 Billion in 2025 to USD 8.02 Billion by 2034 at a CAGR of 22.18%. The Kanto region is expected to retain leadership, while Tohoku and Kansai gain share on the back of cohort genomics expansion and pharma R&D growth. Reagents and consumables, biomarker and cancer applications, and long-read sequencing are forecast to outpace overall market growth through 2034.

Three structural shifts will shape the Japan next-generation sequencing market through 2034. First, comprehensive genomic profiling will become standard of care across all major Japanese cancer centres, supported by expanded reimbursement under the National Health Insurance scheme. Second, long-read sequencing and AI-driven variant interpretation will move from research-grade to clinical-grade workflows. Third, liquid biopsy, minimal residual disease monitoring, and population-scale genomics will progressively reshape clinical practice and research priorities across the country.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with Japan next-generation sequencing stakeholders, including platform provider commercial leaders, hospital genomics directors at cancer-genomic-medicine core hospitals, AMED programme managers, biobank operators, pharma sponsor R&D leaders, and bioinformatics service providers. These interviews validated revenue sizing, segmentation estimates, and adoption-rate benchmarks.

Secondary Research

Secondary sources included AMED programme publications, BioBank Japan reports, MHLW Cancer Genomic Medicine framework documents, PMDA approvals data, National Cancer Center Hospital genomics-medicine statistics, IQVIA Japan analyses, company annual reports, peer-reviewed Japanese genomics literature, and trade publications such as Nikkei Biotech, GenomeWeb, and DataCenter Dynamics-Asia.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating sequencer installed-base evolution, per-genome cost trajectories, reimbursement coverage expansion, AMED funding pipelines, and historical category-evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

Japan Next-Generation Sequencing Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sequencing Types Covered | Whole Genome Sequencing, Targeted Resequencing, Whole Exome Sequencing, RNA Sequencing, CHIP Sequencing, De Novo Sequencing, Methyl Sequencing, Others |

| Product Types Covered | Instruments, Reagents and Consumables, Software and Services |

| Technologies Covered | Sequencing by Synthesis, Ion Semiconductor Sequencing, Single-Molecule Real-Time Sequencing, Nanopore Sequencing, Others |

| Applications Covered | Biomarker and Cancer, Drug Discovery and Personalized Medicine, Genetic Screening, Diagnostics, Agriculture and Animal Research, Others |

| End Users Covered | Academic Institutes and Research Centers, Hospitals and Clinics, Pharmaceutical and Biotechnology Companies, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Illumina Inc., Thermo Fisher Scientific Inc, Pacific Biosciences of California Inc., Oxford Nanopore Technologies Plc, F. Hoffmann-La Roche Ltd, BGI Group, QIAGEN, Takara Bio Inc., Macrogen Inc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan next-generation sequencing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan next-generation sequencing market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan next-generation sequencing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Next-Generation Sequencing Market Report

The Japan next-generation sequencing market was valued at USD 1.32 Billion in 2025, supported by surging precision oncology adoption, the Cancer Genomic Medicine framework, falling per-genome sequencing costs, and AMED-funded research initiatives across all eight Japanese regions.

The market is projected to reach USD 8.02 Billion by 2034, growing at a CAGR of 22.18% during 2026-2034, driven by expanding cancer genomic medicine reimbursement, long-read sequencing adoption, AI-led variant interpretation, and continued pharma and CRO demand for biomarker discovery.

Reagents and consumables lead with a 54.2% share in 2025, anchored by recurring demand for library preparation kits, flow cells, primers, enzymes, and reagent cartridges across hospitals, pharma sponsors, CROs, and academic next generation sequencing workflows nationwide.

Biomarker and cancer applications dominate at 32.6% in 2025, reflecting Japan's high cancer prevalence and the integration of comprehensive genomic profiling into reimbursed clinical workflows under the National Health Insurance scheme at designated cancer-genomic-medicine core hospitals.

Biomarker and cancer applications are the fastest-growing sub-segment, advancing at an estimated 26.8% CAGR through 2034. Comprehensive genomic profiling, liquid biopsy, and minimal residual disease monitoring are the primary drivers across Japanese cancer centres and clinical laboratories.

The Kanto region leads with a 39.1% share in 2025. Tokyo, Yokohama, and Tsukuba host the country's deepest next generation sequencing infrastructure, anchored by the University of Tokyo, RIKEN Yokohama, AMED, the National Cancer Center Hospital, and BioBank Japan.

Key drivers include precision oncology expansion, government genome initiatives via AMED, falling per-genome sequencing costs, sustained pharma and CRO demand, expanded BioBank Japan biospecimen access, and the integration of next generation sequencing into reimbursed clinical workflows nationwide.

Major players include Illumina Inc., Thermo Fisher Scientific Inc, Pacific Biosciences of California Inc., Oxford Nanopore Technologies Plc, F. Hoffmann-La Roche Ltd, BGI Group, QIAGEN, Takara Bio Inc., Macrogen Inc.

Key restraints include high capital costs for sequencer installations, uneven reimbursement coverage outside oncology, data privacy and ethics constraints under Japanese law, skilled bioinformatics talent gaps, and complexity in standardizing variant interpretation across clinical laboratories.

Precision oncology is the largest single growth driver. Foundation Medicine CDx and OncoGuide NCC Oncopanel are widely deployed at designated cancer-genomic-medicine core hospitals, supported by expanded reimbursement under the National Health Insurance scheme through 2024-2025.

AI is reshaping variant calling, annotation, and clinical interpretation. Tools such as Illumina DRAGEN, Google DeepVariant, GATK, and locally developed AI pipelines are reducing turnaround times, improving consistency, and enabling Japanese clinical laboratories to scale their next generation sequencing analytical capacity.

Investment opportunities include liquid biopsy and ctDNA platforms, AI variant interpretation tools, long-read sequencing infrastructure, cloud-based genomics platforms, single-cell sequencing applications, and population-scale cohort genomics anchored by BioBank Japan and the Tohoku Medical Megabank.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)