Japan Office Real Estate Market Size, Share, Trends and Forecast by Property Type, Rental Model, Classification, and Region, 2026-2034

Japan Office Real Estate Market Size & Forecast 2026-2034

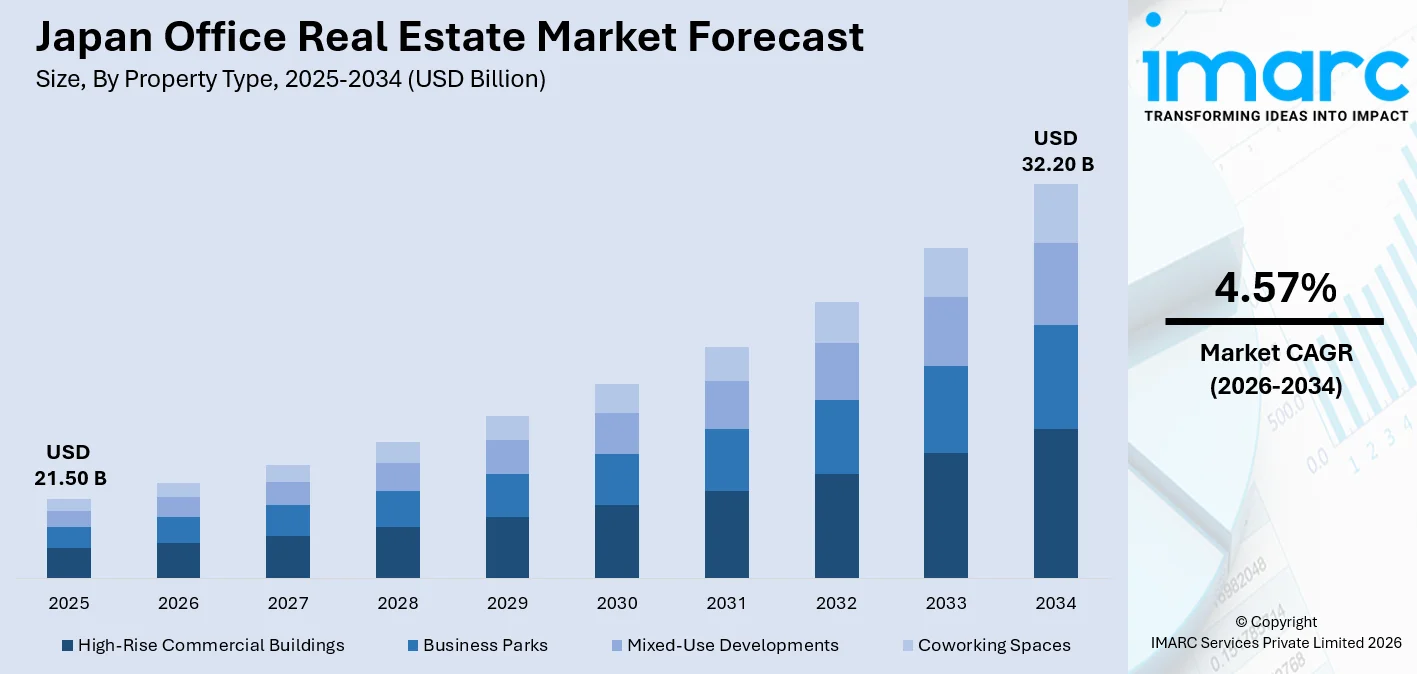

The Japan office real estate market size, valued at USD 21.50 Billion in 2025, is projected to reach USD 32.20 Billion by 2034, growing at a CAGR of 4.57% from 2026-2034, driven by sustained corporate demand for premium office spaces, accelerating urban redevelopment in the Kanto Region, and growing foreign institutional investment attracted by Japan's transparent regulatory framework and favorable yield differentials. As of Q3 2025, Tokyo's Grade A office vacancy rate fell to a historic low of 1.0% while average rents spiked 3.4% quarter-on-quarter to JPY 39,750, making the largest single-quarter increase since Q3 2007. This trend underscoring the structural supply-demand imbalance that continues to propel the Japan office real estate market share.

To get more information on this market Request Sample

Japan Office Real Estate Industry Analysis - Key Insights

- High-rise commercial buildings accounted for 44.0% of the property type segment in 2025, representing the largest share. Premium tower locations in Tokyo’s Marunouchi, Shinjuku, and Toranomon business districts continue to host headquarters of multinational corporations and major domestic conglomerates. These locations provide prestige and strategic advantages in Japan’s dense central business districts.

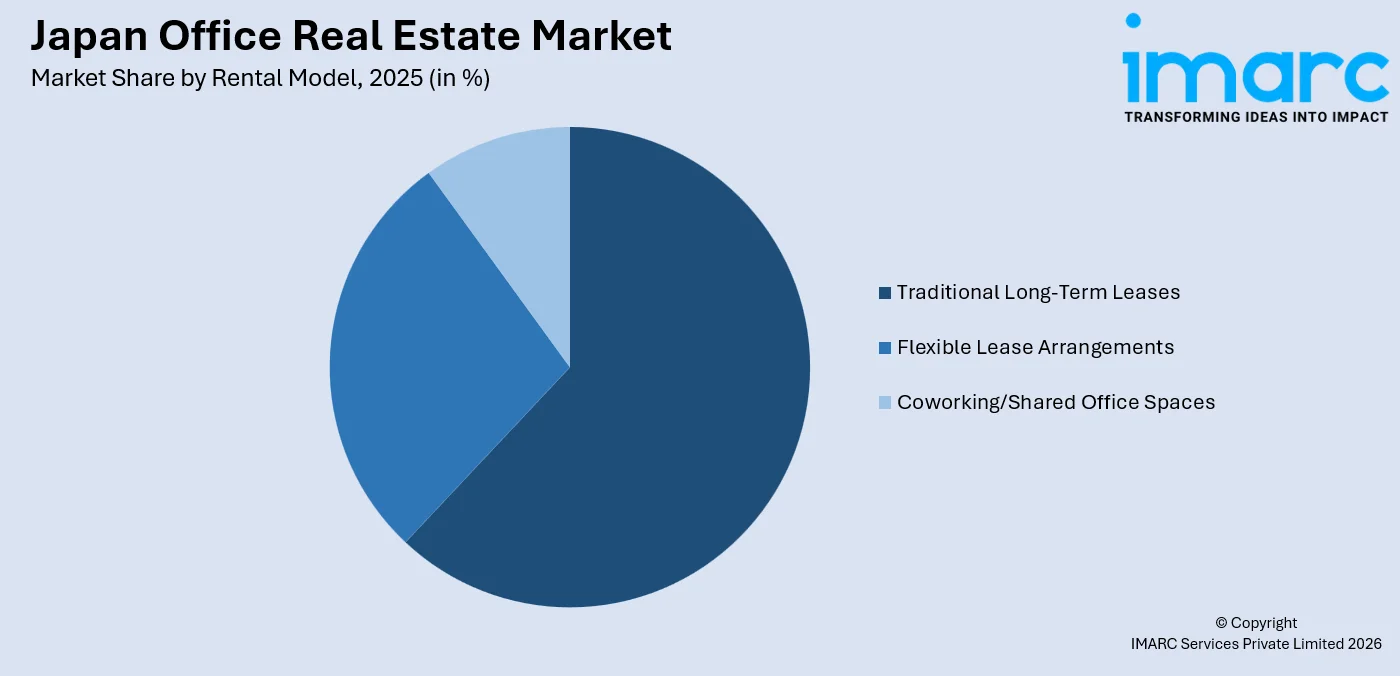

- Traditional long-term leases represented 62.0% of the rental model segment in 2025. Large corporations value predictable costs and the ability to customize office spaces. Japan’s corporate culture strongly favors long-term lease commitments over flexible arrangements.

- Class A leads classification at 54.0% in 2025, more than half the market by quality tier. The tenant "flight to quality" is real and structural: ESG mandates, smart-building specifications, and seismic compliance standards together channel occupier and investor demand almost exclusively toward top-grade assets, leaving lower classifications under sustained pressure.

- Kanto Region leads regionally at 46.0% in 2025, a substantial plurality, but not a monopoly. Tokyo's dominance is grounded in corporate clustering and infrastructure depth, yet the remaining 54% distributed across Kansai, Chubu, Kyushu-Okinawa, and other regions signals meaningful geographic diversification of Japan's office demand base.

Japan Office Real Estate Market Trends and Dynamic 2026

Market Trends

Accelerating tenant flight to Grade A and Class A office towers

Japan's occupier base is consolidating rapidly into top-tier assets, with companies prioritizing modern, ESG-compliant towers that satisfy both board-level sustainability targets and employee experience expectations. As of end-2024, 65% of large office buildings in Tokyo had obtained green building certification, according to JLL Japan research, reflecting the pace at which quality benchmarks are being institutionalised. Meanwhile, Tokyo's all-grade office vacancy dropped to 2.1% in Q3 2025, with Grade A vacancy tightening to just 1.0%, illustrating how quality polarization is reshaping the Japan office real estate market trends.

Smart building integration and IoT-driven office transformation reshaping tenant expectations

The integration of smart building technologies, including IoT sensors, AI-based security systems, smart energy management platforms, and high-speed digital infrastructure, is redefining the minimum standard for competitive Class A office space in Japan. Developers and landlords are embedding these technologies not merely as amenities but as lease-rate differentiators, particularly as multinational tenants consolidate their footprints into fewer, higher-specification buildings. This technological transformation is increasingly influencing leasing decisions, with occupiers prioritizing assets that offer operational efficiency, enhanced user experience, and data-driven building management capabilities.

Hybrid and flexible work models driving structural bifurcation in office demand

Japan's corporate sector is navigating a nuanced hybrid work transition with a 2025 World Economic Forum survey finding 82.2% of Japanese workers wishing to continue teleworking, creating a dual dynamic where demand for premium, experience-rich Class A headquarters strengthens while older secondary assets face elevated vacancy pressures. Tokyo introduced a four-day working week model in April 2025, becoming a catalyst for workplace reconfiguration across the country. The total stock of flexible workspace in Tokyo's CBD reached 421,457 sqm, with approximately 60% comprising coworking formats oriented toward hybrid team collaboration.

- Green Certification Premium: Tenants and investors are directing capital toward buildings with CASBEE, DBJ Green Building, and LEED certifications, creating measurable green rent premiums for certified assets.

- Urban Redevelopment Pipeline: Multi-billion-yen mixed-use projects including Yaesu 2-Chome and Toranomon corridors are delivering next-generation office inventory that integrates workspace with retail, hospitality, and transport.

- Foreign Investor Momentum: Institutional capital from North America and Southeast Asia is accelerating acquisitions of Tokyo Grade A assets, attracted by historically high yields relative to global gateway cities.

- Suburban and Regional Office Expansion: Hybrid work adoption is catalyzing satellite office growth in Kanagawa, Saitama, and secondary cities such as Fukuoka and Sendai as companies build hub-and-spoke real estate portfolios.

Growth Drivers

Corporate profitability expansion fuelling premium office leasing demand

The increase in corporate profits is driving demand for headquarter grade offices in the major central business districts (CBDs) of Japan. An analysis by Nikkei in 2025 shows all five of Japan's largest real estate developers (Mitsui Fudosan, Mitsubishi Estate, Sumitomo Realty & Development, Tokyu Fudosan Holdings, and Nomura Real Estate) are on track to have record profits for their fiscal year ending March 2025, which would be their second consecutive year of record earnings.

Foreign institutional investment inflows and J-REIT portfolio expansion

The Japanese regulatory framework is open, and very transparent for foreign investments, which continues to draw massive amounts of cross-border investment. In 2024 alone, Japanese domestic real estate investment activity reached approximately JPY 6.1 trillion (approximately USD 41.7 billion), which has remained stable through a period of global monetary tightening. Of foreign capital inflows to Japan, North American and European funds contributed approximately 68%.

Large-scale urban redevelopment and government infrastructure investment

Japan's central and metropolitan governments continue to drive significant public-private redevelopment investment across Tokyo, Osaka, and regional hubs. The March 2025 official land-price survey recorded the fourth consecutive annual increase in Tokyo commercial plots, up 8.2%, with Osaka up 6.7%, reflecting robust underlying demand tied to infrastructure projects.

- Osaka Expo 2025 and Regional Infrastructure: The Osaka-Kansai Expo 2025, which drew over 28 million visitors, catalyzed office space demand in the Kansai region as corporations establish regional hubs to capitalize on growing international business activity.

- Seismic Resilience Upgrade Demand: Mandatory earthquake resistance standards for new constructions and government incentives for retrofitting older buildings are driving tenant migration to compliant Class A office stock.

- Weak Yen Amplifying Foreign Demand: With the yen remaining near 140 per USD through 2025, Japan's office assets remain attractively priced for foreign investors, with Chinese, American, and Singaporean buyers actively expanding commercial real estate portfolios in Tokyo.

Market Restraints

Rising construction and development costs: The development of new office space in Japan has become increasingly expensive and logistically complex. Material costs continue to escalate, while the construction industry contends with a persistent structural labor shortage. These combined pressures are causing delays and, in some cases, halting project progression entirely. Developers moving forward must navigate difficult decisions, balancing budget constraints against environmental compliance and timely delivery. The viability challenges are most pronounced for mid-tier office developments located outside prime central business districts, where the financial returns on new construction are considerably harder to justify.

Demographic headwinds and workforce contraction: Japan's population is aging, and the number of working-age people is shrinking—and that's starting to show up in the office market. Fewer workers means less demand for office space in the long run. Sure, young people still move to big cities for jobs, which helps keep things going in places like Tokyo, but that can only do so much. Nationwide, the pool of potential office workers is getting smaller, so even if new buildings go up, it's getting harder to fill them at the same pace as before.

Secondary and peripheral asset displacement risk: The concentration of tenant demand in Class A and newly developed properties creates sustained vacancy pressure for older, lower-grade, and non-centrally located office buildings. Landlords of secondary assets face increasing difficulty attracting and retaining tenants without costly refurbishment or significant rent concessions, constraining portfolio-level returns.

Japan Office Real Estate Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Property Type | High-Rise Commercial Buildings | 44.0% | 2025 |

| Rental Model | Traditional Long-Term Leases | 62.0% | 2025 |

| Classification | Class A | 54.0% | 2025 |

| Region | Kanto Region | 46.0% | 2025 |

Property Type Insights

High-Rise Commercial Buildings- 44.0% Market Share (2025) | Leading Property Type

The skyline of Japan's office market is defined by high-rise commercial buildings, which will account for 44.0% of the region's office property market in 2025. These buildings have a concentration in the five central wards of Tokyo and in Osaka (Umeda/Namba). For many large international and top domestic corporations, occupying a high-rise building symbolizes more than simply having square footage: it also represents their corporate image, having modern floor layouts that function properly, and having the type of technology infrastructure necessary for attracting and maintaining the best talent.

|

Segment Breakdown High-Rise Commercial Buildings (44.0%) · Business Parks · Mixed-Use Developments · Coworking Spaces |

Rental Model Insights

Access the comprehensive market breakdown Request Sample

Traditional Long-Term Leases- 62.0% Market Share (2025) | Leading Rental Model

In 2025, conventional long-term leases will account for 62.0% market share of renting offices in Japan. Landlords like investment banks, technology companies, trading firms, and government-related companies typically prefer multi-year lease contracts. Long-term leases allow these large companies to predict costs, customize their office environment, and establish their brand over time. As a result, this approach aligns perfectly with Japanese culture's overall preference for long-term commitments to real estate.

|

Segment Breakdown Traditional Long-Term Leases (62.0%) · Flexible Lease Arrangements · Coworking/Shared Office Spaces |

Classification Insights

Class A- 54.0% Market Share (2025) | Leading Classification

Class A office buildings account for the highest revenue share in Japan's office real estate classification segment at 54.0% in 2025. This majority position reflects a multi-year structural trend of tenant consolidation into best-in-class assets that satisfy simultaneous ESG, seismic resilience, smart-building, and premium amenity requirements. For Class B and Class C buildings, the landscape is getting tougher. Tenants are no longer just looking at the base rent. They are doing the math on the full cost of being there, including what it takes to fit out the space, how much energy they will burn through, and whether the building meets evolving regulatory standards.

|

Segment Breakdown Class A (54.0%) · Class B · Class C |

Regional Insights

Kanto Region- 46.0% Market Share (2025) | Leading Region

The Kanto Region, anchored by the Tokyo Metropolitan Area, continues to lead Japan's office market, capturing 46.0% of national share in 2025. Tokyo's position as the country's primary business hub remains unchallenged, drawing multinational headquarters, financial institutions, government ministries, and technology firms. Demand for space in the capital shows no sign of cooling. CBRE's Japan Office MarketView reports Tokyo's Grade A vacancy at a historically tight 1.0% in Q3 2025, with all-grade vacancy dropping to 2.1%. These figures point to sustained pressure from occupiers seeking a presence in Japan's core commercial center. Ongoing redevelopment is also reshaping the city's office landscape, with major projects along the Yaesu corridor, the Toranomon-Azabudai district, and the Nihonbashi River Walk initiative collectively redefining prime locations.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

46.0%

|

|

Key States

|

Tokyo, Kanagawa, Saitama, Chiba |

|

Major Growth Drivers

|

Corporate headquarter clustering, Urban redevelopment pipeline, Foreign institutional investment, Smart-building demand |

|

Outlook

|

Tightest vacancy, strongest rent growth outlook |

|

Regional Breakdown Kanto Region (46.0%) · Kansai/Kinki Region · Central/ Chubu Region· Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai/Kinki Region, centered on Osaka, represents Japan's second-largest office real estate market, benefiting from a major demand catalyst in the Osaka-Kansai Expo 2025. Osaka's all-grade vacancy fell to 2.3% in Q3 2025, falling below the 3% threshold for the first time since Q2 2021. At the same time, Grade A rents reached JPY 28,300, the highest level since CBRE's surveys began. The JPY 4 billion Umekita Phase 2 development is integrating life-science, hospitality, and workspace functions in a mixed-use format that is positioning Osaka as a diversified global business destination beyond Tokyo's corporate pedigree.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Osaka, Kyoto, Hyogo, Nara, Shiga, Wakayama |

|

Major Growth Drivers

|

Expo 2025 demand catalyst, Umekita Phase 2 development, International trade route proximity, Mixed-use project growth |

|

Outlook

|

Rising rents, tightening vacancy, innovation hub positioning |

Central/Chubu Region:

The Chubu Region, with Nagoya serving as its primary commercial hub, benefits from strong integration with Japan’s automotive and aerospace manufacturing industries. This industrial presence creates consistent demand for office space from large manufacturers and their supplier networks. In Nagoya, the Grade A office vacancy rate declined to 2.3% in Q1 2025, marking the lowest level in four years, as automotive and aerospace companies secured long-term office spaces near key supplier clusters. The region’s strategic location between Tokyo and Osaka, along with comparatively lower operating costs than the Kanto market, is increasingly attracting companies looking for cost-efficient central business district alternatives with strong transportation connectivity.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Aichi, Shizuoka, Gifu, Mie, Nagano |

|

Major Growth Drivers

|

Automotive and aerospace industry anchoring, Lower operating costs vs. Kanto, Strategic geographic positioning, Transport corridor access |

|

Outlook

|

Mid-single-digit rent gains, demand stability |

Kyushu-Okinawa Region:

The Kyushu-Okinawa Region, led by Fukuoka, is emerging as a tech and startup-focused office market with growing relevance to Southeast Asia-facing corporate operations. Fukuoka's all-grade vacancy dropped a notable 0.6%age points to 4.0% in Q3 2025, per CBRE data, supported by relocations into larger or superior office premises by companies establishing regional headquarters. The city's Fukuoka City Startup Visa program, along with the opening of WeWork Tenjin Brick Cross in August 2025, reflects the region's deliberate positioning as Japan's startup capital and international business gateway.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Fukuoka, Kumamoto, Nagasaki, Kagoshima, Okinawa |

|

Major Growth Drivers

|

Tech and startup ecosystem growth, Southeast Asia gateway positioning, Flexible workspace expansion, Government startup incentive programs |

|

Outlook

|

Fastest-growing secondary regional market |

Market Outlook 2026-2034

What is the future outlook of the Japan office real estate market?

The Japan office real estate market is expected to sustain steady revenue growth through 2034.

Underpinned by enduring corporate demand for premium Class A space in major CBDs, a healthy foreign investment pipeline, and a transformative urban redevelopment cycle across Tokyo, Osaka, and regional hubs, Japan office real estate market outlook through 2034 is constructive. The convergence of sustainability mandates, seismic compliance standards, and digital infrastructure requirements will continue to sustain rent premiums for top-tier assets while accelerating functional obsolescence of lower-grade inventory. Japan's open foreign ownership framework, transparent transaction environment, and historically tight Grade A vacancy in Kanto will maintain the country's position as one of Asia-Pacific's most resilient commercial real estate destinations for global institutional capital.

Japan Office Real Estate Market - Leading Key Players

The Japan office real estate market is shaped by a group of large-scale integrated developers and real estate investment trusts that collectively control the majority of Grade A and Class A office inventory across the country's major CBDs. These firms combine large development pipelines with active portfolio management, sustainability certification programs, and growing international investment platforms to maintain their competitive positioning.

| Company | Leading Brands | Highlights |

|---|---|---|

| Sumitomo Realty & Development Co., Ltd. | Shinjuku Park Tower, Sumitomo Fudosan Roppongi Grand Tower, Yaesu 2-Chome South Tower | Committed JPY 2 trillion to central Tokyo redevelopment over 10 years; Yaesu 2-Chome South 39-storey tower (138,600 sqm GFA) targeting 2029 completion; earmarked 19 midsized Tokyo office buildings for ¥100 billion divestment |

| Tokyu Land Corporation | Cerulean Tower, Shibuya Scramble Square (Office Floors), Shinagawa Season Terrace | First Japanese real estate company to sign RE100 in 2019; converted all Japanese facilities to 100% renewable energy; active in Takeshiba Area international business hub revitalization |

| Nomura Real Estate Holdings, Inc. | PMO Series (Premium Mid-sized Office), Proud Tower, Human First Office network | Expanding Human First Office serviced office network nationwide; strong mid-sized Class A office pipeline in Tokyo's business districts; record FY2024 earnings from combined office leasing and condo sales |

Major key companies in Japan office real estate market are Mitsubishi Estate Co., Hulic Co., Ltd., ORIX Group, Mori Building Co., Ltd., Daiwa House Industry, Sekisui House, etc.

Latest Development & News

- In November 2025, Sumitomo Realty & Development acquired the land beneath its Yaesu 2-Chome South project, a planned 39-storey, 138,600 sqm mixed-use tower comprising office, retail, and hotel components at a ¥34.1 billion land transaction gain recorded by seller Nittobo. The project forms part of a wider Yaesu high-rise cluster alongside Tokyo Station that is set to redefine Tokyo's eastern CBD by 2029, representing one of the largest coordinated urban redevelopment investments in Japan's current construction cycle.

- In August 2025, Mitsui Fudosan announced that Honda Motor Co. will transfer its global headquarters functions to the Yaesu 2-Chome Central District redevelopment project near Tokyo Station, marking one of the most significant corporate headquarter relocations in Japan in recent years. Honda's decision to anchor into a new Class A tower reinforces the Yaesu corridor's status as a premium corporate address and validates the sustained demand for flagship high-rise commercial developments in the Kanto region.

Japan Office Real Estate Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Property Types Covered | High-Rise Commercial Buildings, Business Parks, Mixed-Use Developments, Coworking Spaces |

| Rental Models Covered | Traditional Long-Term Leases, Flexible Lease Arrangements, Coworking/Shared Office Spaces |

| Classifications Covered | Class A, Class B, Class C |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan office real estate market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan office real estate market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan office real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Office Real Estate Market Report

The Japan office real estate market reached a value of USD 21.50 Billion in 2025.

The market is projected to grow at a CAGR of 4.57% during 2026-2034, reaching USD 32.20 Billion by 2034.

The Japan office real estate market growth is driven by urban redevelopment projects, demand for premium Grade-A office spaces, expansion of technology and financial firms, and modernization of aging office infrastructure.

The report covers segmentation by property type, rental model, classification, and region. Each segment includes detailed market size and forecast analysis.

The Japan office real estate market trends include rising demand for flexible workspaces, integration of smart building technologies, sustainability-focused office designs, redevelopment of urban business districts, and hybrid work models influencing space utilization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)