Japan Palladium Market Size, Share, Trends and Forecast by Source, End Use Industry, and Region, 2026-2034

Japan Palladium Market Summary:

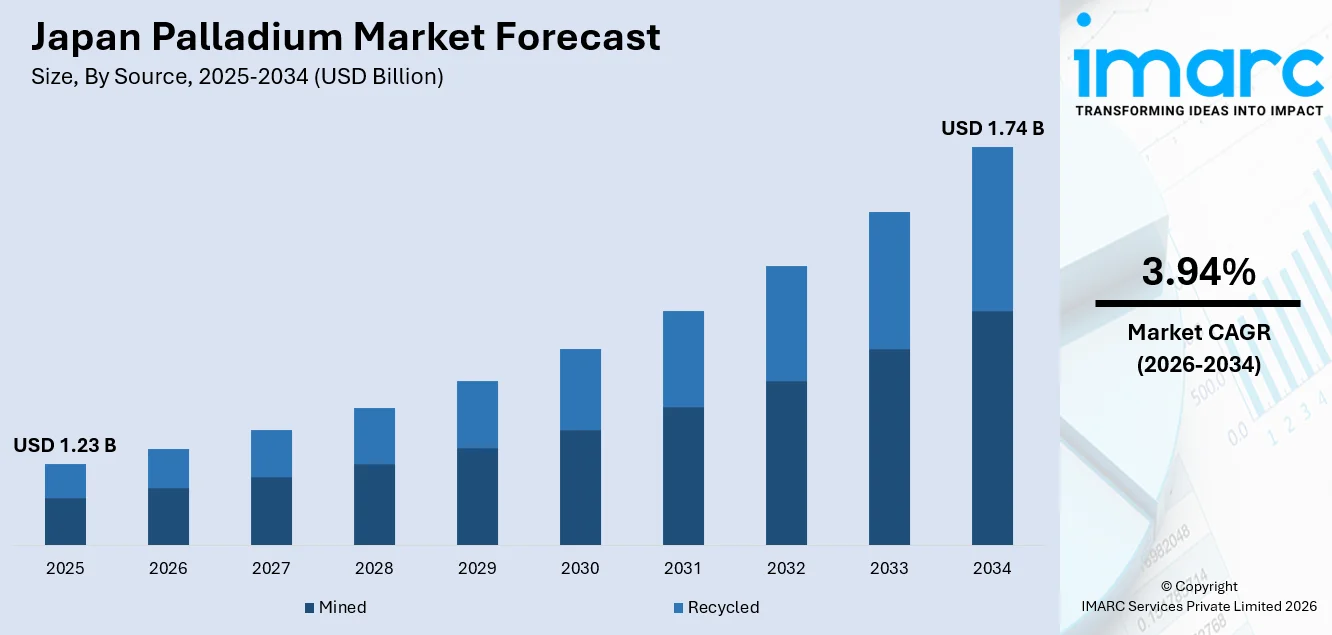

The Japan palladium market size was valued at USD 1.23 Billion in 2025 and is projected to reach USD 1.74 Billion by 2034, growing at a compound annual growth rate of 3.94% from 2026-2034.

Japan's palladium market is driven by the country's established automotive manufacturing base, which relies on the metal for catalytic converters in internal combustion engine and hybrid vehicles. Expanding applications in electronics, particularly multilayer ceramic capacitors and semiconductor components, further sustain consumption. Additionally, the government's commitment to hydrogen economy technologies and stringent vehicle emission compliance frameworks continue to reinforce demand across the Japan palladium market share.

Key Takeaways and Insights:

- By Source: Mined dominates the market with a share of 61.7% in 2025, owing to Japan's heavy reliance on imported palladium from major producing nations to meet its substantial industrial and automotive consumption requirements. Limited domestic extraction capabilities reinforce dependence on mined supply channels.

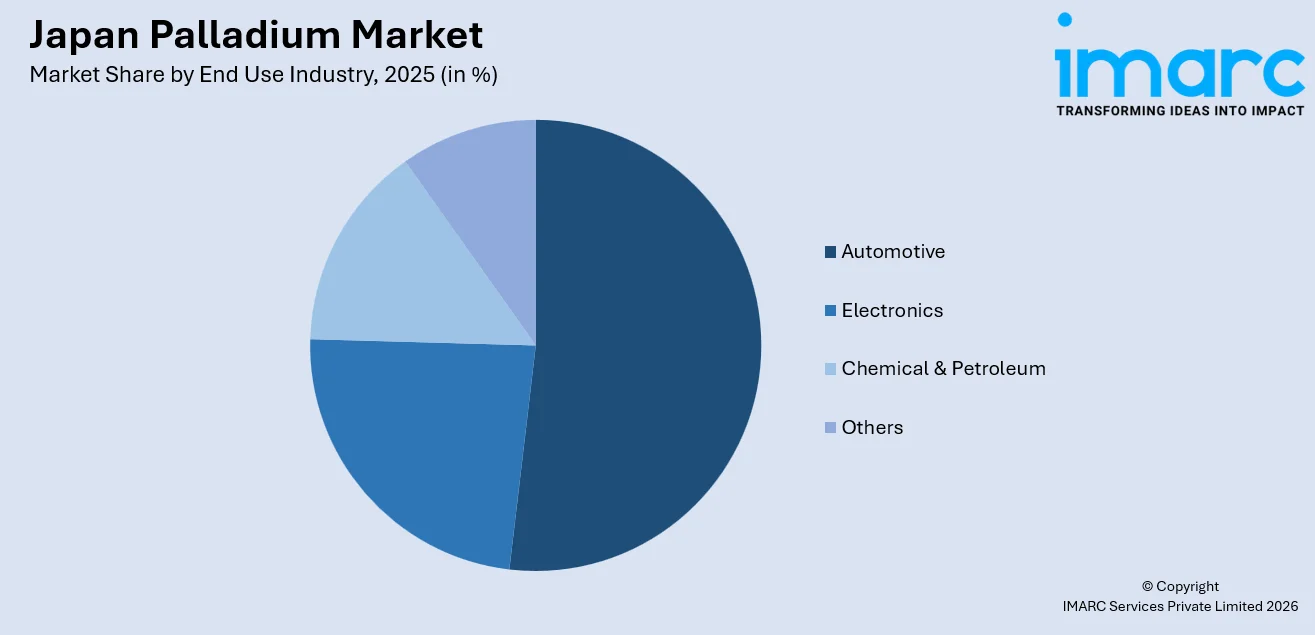

- By End Use Industry: Automotive leads the market with a share of 52.8% in 2025. This dominance is driven by Japan's position as a leading global automobile producer, with palladium remaining essential for three-way catalytic converters across gasoline-powered and hybrid vehicle fleets.

- By Region: Kanto Region comprises the largest region with 41.3% share in 2025, driven by the concentration of major automotive manufacturers, electronics conglomerates, and chemical processing firms across the Tokyo metropolitan area and surrounding industrial prefectures.

- Key Players: The market is competitive, shaped by global miners, metal traders, and industrial end-users in automotive and electronics. Companies compete through stable supply contracts, recycling capabilities, and price risk management. Demand trends, import dependence, and substitution efforts also influence market positioning.

To get more information on this market Request Sample

Japan's palladium market reflects the nation's dual role as a major industrial consumer and a global leader in precious metals recycling and refining technologies. The automotive sector remains the primary consumption anchor, supported by sustained hybrid vehicle production and tightening emission compliance requirements. The electronics industry contributes through palladium's use in high-reliability multilayer ceramic capacitors and semiconductor connectors, where Japanese manufacturers hold dominant global positions. In September 2025, TANAKA Precious Metal Technologies announced the successful development of a high-performance palladium-copper alloy hydrogen permeable membrane, designated PdCu39, capable of operating at approximately 300 degrees Celsius, which is a full 100 degrees lower than conventional membranes. Emerging applications in hydrogen purification and fuel cell technologies, aligned with the government's revised Basic Hydrogen Strategy targeting 12 million tons of annual hydrogen usage by 2040, are creating new demand avenues that complement traditional industrial consumption patterns.

Japan Palladium Market Trends:

Growing adoption of hydrogen purification technologies

Japan is rapidly advancing its hydrogen economy goals, opening new growth opportunities for palladium beyond its established role in automotive catalysts. Palladium-based membranes are widely regarded as a leading solution for ultra-pure hydrogen separation, a critical requirement for fuel cell vehicles, hydrogen refueling infrastructure, and high-grade industrial applications. As Japan scales up hydrogen production, storage, and distribution projects, demand for palladium in advanced purification technologies is expected to strengthen.

Expansion of advanced PGM recycling infrastructure

Japan is strengthening its palladium recycling capabilities to reduce import dependency and support circular economy objectives. Specialized smelting facilities are increasing recovery rates from spent automotive catalytic converters and electronic waste streams. As such, in October 2025, Gannon & Scott entered into an agreement to become part of Metalor Technologies, a TANAKA group company, subject to regulatory clearance. The deal strengthens precious metal refining, including palladium and PGMs, expands recycling access, and enhances operations through integrated global sourcing, R&D, and refining capabilities.

Rising hybrid vehicle penetration

Japan's automotive market is experiencing a pronounced shift toward hybrid powertrains, which continue to require palladium-loaded catalytic converters unlike battery electric vehicles. The sustained preference for hybrid vehicles ensures ongoing palladium consumption in the automotive supply chain. According to the Japan Automobile Dealers Association, hybrid vehicle sales in Japan surpassed 2 million units for the first time in 2024, representing 54.8% of all new passenger car sales in the domestic market.

Market Outlook 2026-2034:

The Japan palladium market is positioned for steady growth over the forecast period, supported by sustained automotive manufacturing, expanding hydrogen economy applications, and advancing electronics demand. Accordingly, in August 2025, Toyota announced plans to acquire land in Toyota City, Aichi Prefecture, to build a new vehicle manufacturing plant. Operations are expected in the early 2030s, supporting Japan’s 3 million-vehicle production capacity with future-focused technology. While the gradual transition toward electric mobility presents a long-term structural shift, hybrid vehicle dominance in Japan ensures continued catalytic converter consumption. Emerging applications in hydrogen purification membranes and fuel cell technologies provide incremental demand opportunities as Japan pursues its carbon neutrality objectives. Furthermore, strategic investments in PGM recycling infrastructure are expected to enhance secondary supply availability, partially offsetting supply chain vulnerabilities associated with geopolitical concentration of primary mining in South Africa and Russia. The market generated a revenue of USD 1.23 Billion in 2025 and is projected to reach a revenue of USD 1.74 Billion by 2034, growing at a compound annual growth rate of 3.94% from 2026-2034.

Japan Palladium Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Source |

Mined |

61.7% |

|

End Use Industry |

Automotive |

52.8% |

|

Region |

Kanto Region |

41.3% |

Source Insights:

- Mined

- Recycled

Mined dominates with a market share of 61.7% of the total Japan palladium market in 2025.

Japan possesses virtually no domestic palladium mining capacity, making the country almost entirely dependent on imported mined palladium to satisfy its industrial and automotive requirements. The nation sources its mined palladium primarily from South Africa and Russia, which collectively account for the majority of global primary production. According to WITS data, Japan ranked among the leading importers of unwrought or powder-form palladium in 2023, with imports valued at USD 1,780,617.48K and a total volume of 39,444 kilograms.

The dominance of mined palladium in Japan's supply structure reflects the sheer scale of industrial demand that secondary sources cannot yet fully accommodate. While recycling operations are growing, they currently supplement rather than replace primary mined supply due to the volume requirements of the automotive and electronics sectors. The geopolitical concentration of mining in South Africa and Russia introduces supply chain risks, prompting Japanese firms to diversify sourcing relationships and establish long-term procurement agreements with multiple mining entities across Canada, Zimbabwe, and other producing nations.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Electronics

- Chemical & Petroleum

- Others

Automotive leads with a share of 52.8% of the total Japan palladium market in 2025.

The automotive sector serves as the primary consumption anchor for palladium in Japan, driven by the metal's indispensable role in three-way catalytic converters that reduce harmful emissions from internal combustion engines and hybrid powertrains. Japan remains one of the world's largest automobile manufacturing nations, and the continued dominance of gasoline-powered and hybrid vehicles in both domestic and export markets sustains substantial palladium demand. According to the Japan Automobile Manufacturers Association, motor vehicle production in Japan stood at 8.23 million units in 2024, with the overwhelming majority requiring palladium-based emission control systems.

Japanese automakers have increasingly focused on hybrid vehicle technologies, which require catalytic converters containing palladium, unlike fully battery electric alternatives. This strategic emphasis ensures sustained consumption even as the broader global automotive industry shifts toward electrification. The introduction of on-board diagnostics testing from October 2024 for new domestic vehicles has further reinforced the need for properly functioning emission control systems, indirectly supporting palladium usage in catalytic converter maintenance and replacement across the vehicle fleet operating throughout Japan.

Region Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The Kanto Region exhibits a clear dominance with a 41.3% share of the total Japan palladium market in 2025.

The Kanto Region leads Japan's palladium market owing to the concentration of major automotive manufacturers, electronics conglomerates, and chemical processing operations across the greater Tokyo metropolitan area and surrounding industrial prefectures. The region hosts headquarters and manufacturing facilities of leading catalytic converter producers and precious metals refiners. According to Japan's Semiconductor Equipment Association, semiconductor equipment sales in Japan increased by 27% in 2024, with a significant share of this activity concentrated in Kanto-based facilities that utilize palladium in advanced electronic components and connectors.

The Kanto Region enjoys advantages from its extensive research and development facilities which include national laboratories, university innovation centers and private-sector materials science institutes that research advanced metals and clean technologies. The existence of hydrogen energy demonstration projects together with fuel cell research initiatives creates an additional requirement for palladium which is used in membrane and catalyst manufacturing. The presence of established logistics systems, port facilities and financial institutions in Tokyo enables precious metal trading operations, recycling activities and efficient supply chain control which strengthens Kanto's dominance in Japan's palladium industry.

.webp)

Market Dynamics:

Growth Drivers:

Why is the Japan Palladium Market Growing?

Ongoing hybrid production supporting catalytic converter demand

Japan's automotive industry uses hybrid powertrains as its main electrification method, which results in continued palladium requirements for catalytic converters. Hybrid vehicles use internal combustion engines which need palladium-loaded three-way catalytic converters to meet environmental regulations, unlike battery electric vehicles. Japan's automotive manufacturers dominate the international hybrid vehicle market while their domestic production operations maintain steady demand for palladium-based emission control systems. The automotive industry focuses on hybrid technology development because it generates high palladium usage across all manufacturing operations that produce vehicles for both local markets and international markets, which supports continuous market growth.

Expanding hydrogen economy applications

Japan's ambitious hydrogen strategy is generating incremental demand for palladium through hydrogen purification membrane technologies. Palladium-based membranes are the preferred solution for separating ultra-pure hydrogen from mixed gas streams, essential for fuel cell applications and industrial hydrogen supply chains. The Japanese government's revised Basic Hydrogen Strategy targets substantial increase in hydrogen usage by 2040, supported by JPY 15 Trillion in investment over 15 years. The Tokyo Metropolitan Government increased its hydrogen-related budget to JPY 20.3 Billion for fiscal year 2024, a 1.8-fold increase over the previous year, reflecting growing public-sector commitment to hydrogen infrastructure that drives palladium membrane adoption.

Growing electronics sector demand for high-reliability palladium components

Japan's electronics industry sustains palladium demand through its use in multilayer ceramic capacitors, semiconductor connectors, and thick-film circuit applications. Japanese MLCC manufacturers, including industry leaders based in the Kanto and Kansai regions, collectively hold a dominant global market position, and palladium retains a niche role in high-reliability segments for aviation, defense, automotive electronics, and medical devices. Likewise, the expansion of artificial intelligence server infrastructure and advanced automotive electronics is driving demand for higher-specification components, supporting continued palladium usage in specialized electronic applications.

Market Restraints:

What Challenges the Japan Palladium Market is Facing?

Rising EV adoption weakening long-term catalytic converter demand

The growing global shift toward battery electric vehicles presents a long-term challenge for palladium demand, since fully electric powertrains do not require catalytic converters. Although Japan’s domestic EV adoption remains relatively limited compared with other major markets, the broader transition toward electrification is expected to accelerate over time. As stricter emissions regulations and policy targets encourage higher EV penetration, palladium consumption in the automotive sector is likely to face gradual decline, reshaping future demand dynamics.

Geopolitical supply concentration creating procurement risks

Japan's near-total dependence on imported palladium exposes the market to supply chain risks associated with the geopolitical concentration of mining in South Africa and Russia. Ongoing disruptions from the Russia-Ukraine conflict, sanctions on Russian metal exports, and recurring energy shortages in South African mining operations introduce price volatility and procurement uncertainties that affect downstream Japanese industrial consumers and complicate long-term sourcing strategies for automotive and electronics manufacturers.

Platinum-for-palladium substitution trends pressuring demand fundamentals

The shrinking price gap between platinum and palladium is prompting automakers to replace palladium with platinum in catalytic converters, especially for diesel vehicles. This shift is driven by cost efficiency and supply considerations. Although some reverse substitution may occur over time, the ongoing material switching trend introduces uncertainty for palladium demand. As manufacturers adjust sourcing strategies and technology configurations, forecasting long-term palladium consumption within the automotive value chain becomes more complex and less predictable.

Competitive Landscape:

The Japan palladium market features a competitive landscape characterized by vertically integrated precious metals processors, specialized recycling firms, and global mining conglomerates with established Japanese distribution networks. Market participants compete on refining purity, recycling efficiency, supply chain reliability, and technological innovation in palladium-based applications. Strategic partnerships between domestic refiners and international mining companies ensure diversified procurement channels, while investments in advanced recycling technologies and hydrogen-related palladium applications provide differentiation opportunities across the evolving competitive environment.

Recent Developments:

- In December 2025, the inaugural Palladium Global Science Award, backed by Japan’s MDX Research Center and CPMIC, honored five scientists from multiple countries, sharing USD 350,000. Recognizing advances in clean energy, medicine, and materials, the initiative highlights palladium’s expanding role beyond autocatalysts, reinforcing Japan’s strategic interest in advanced precious metal innovation.

- In March 2025, Tokyo University of Science researchers developed palladium-based PdDI nanosheet catalysts for hydrogen production, offering platinum-like HER performance at lower cost. Activated E-PdDI showed a 34 mV overpotential versus platinum’s 35 mV and matched exchange current density at 2.1 mA/cm². The nanosheets remained stable for 12 hours in acidic conditions, supporting scalable clean hydrogen applications.

Japan Palladium Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Sources Covered |

Mined, Recycled |

|

End Use Industries Covered |

Automotive, Electronics, Chemical & Petroleum, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Palladium Market Report

The Japan palladium market size was valued at USD 1.23 Billion in 2025.

The Japan palladium market is expected to grow at a compound annual growth rate of 3.94% from 2026-2034 to reach USD 1.74 Billion by 2034.

Mined dominated the market with a share of 61.7%, driven by Japan's near-total reliance on imported primary palladium from major producing nations including South Africa and Russia to satisfy substantial automotive and electronics sector demand.

Key factors driving the Japan palladium market include sustained hybrid vehicle manufacturing requiring palladium-based catalytic converters, expanding hydrogen economy applications for palladium purification membranes, and growing electronics sector demand for high-reliability components.

Major challenges include gradual battery electric vehicle adoption reducing catalytic converter demand, geopolitical concentration of primary mining supply in South Africa and Russia, platinum-for-palladium substitution trends, palladium price volatility, and Japan's import dependency creating procurement vulnerabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)