Japan Personal Protective Equipment Market Size, Share, Trends and Forecast by Equipment Type, End-Use Industry, and Region, 2026-2034

Japan Personal Protective Equipment Market Summary:

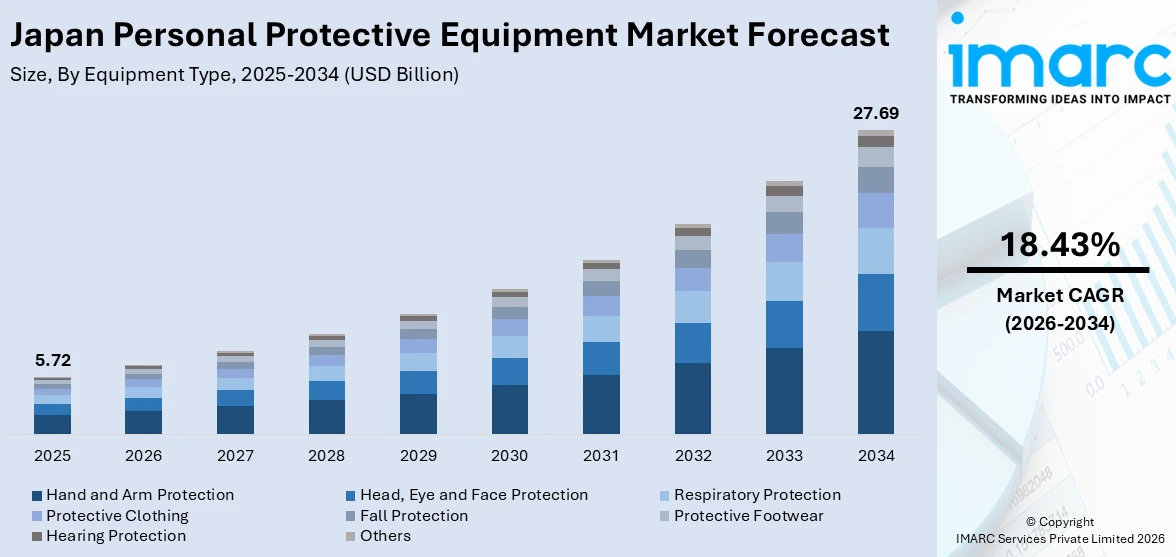

The Japan personal protective equipment market size was valued at USD 5.72 Billion in 2025 and is projected to reach USD 27.69 Billion by 2034, growing at a compound annual growth rate of 18.43% from 2026-2034.

Japan's personal protective equipment market is propelled by an increasingly rigorous regulatory environment under the Industrial Safety and Health Act, expanding industrial activities across manufacturing, construction, and chemical sectors, and heightened awareness of occupational health risks. The integration of advanced technologies such as IoT-enabled smart protective equipment and superior material innovations is further strengthening adoption, positioning Japan as a leading growth market for personal protective equipment market share.

Key Takeaways and Insights:

- By Equipment Type: Hand and arm protection dominates the market with a share of 22.3% in 2025, driven by the high prevalence of occupational hand injuries across manufacturing, construction, and chemical industries. Stringent safety regulations and cut-resistant material innovations are fueling adoption.

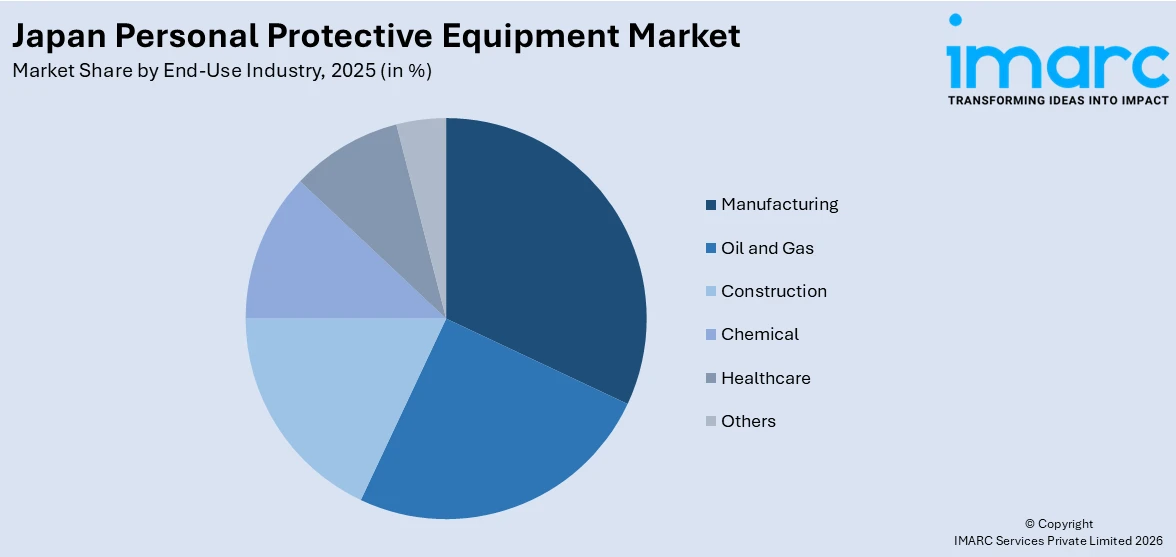

- By End-Use Industry: Manufacturing leads the market with a share of 28.4% in 2025, driven by Japan's highly industrialized environment, widespread automation-related safety requirements, and extensive workforce exposure to mechanical, chemical, and environmental hazards requiring comprehensive PPE.

- By Region: Kanto Region represents the largest region with 35.6% share in 2025, driven by the concentration of Japan's primary industrial corridors, dense healthcare infrastructure, and manufacturing clusters across Tokyo and neighboring prefectures supporting sustained PPE demand.

- Key Players: Key players drive the Japan personal protective equipment market through continuous product innovation, smart material research, and strategic capacity expansions. Their investments in IoT-integrated protective solutions, ergonomic designs, and compliance technologies strengthen competitive positioning and accelerate adoption across diverse industrial end-users throughout Japan.

To get more information on this market Request Sample

The Japan personal protective equipment market is undergoing a significant transformation, driven by an increasingly rigorous regulatory environment, rapid industrialization, and an aging workforce that demands more sophisticated occupational health solutions. The manufacturing segment, which represents the largest end-use contributor, continues to lead adoption across all PPE categories, from hand protection to fall prevention systems. The Kanto Region, encompassing Tokyo and its surrounding prefectures, hosts the country's largest industrial and healthcare concentration, making it the dominant regional contributor to market activity. Sustained investment in research and development by both domestic and international manufacturers is accelerating the creation of smart, sensor-integrated protective solutions tailored to Japan's precision-focused industrial environment. The convergence of regulatory compliance imperatives, technological innovation, and heightened workforce safety awareness is expected to drive robust market expansion across the forecast period.

Japan Personal Protective Equipment Market Trends:

Rise of Smart and Connected PPE Solutions

Japan's industrial landscape is increasingly embracing IoT-integrated and sensor-enabled PPE that provides real-time data collection and hazard monitoring. Smart helmets, wearable devices, and connected gloves equipped with biometric sensors are gaining rapid traction, particularly in manufacturing and construction applications. This shift reflects Japan's broader commitment to Industry 4.0 adoption, where data-driven safety management reduces workplace incident rates and enables proactive risk mitigation. Domestic manufacturers are investing heavily in proprietary sensor fusion technologies and AI-powered monitoring platforms to differentiate their product portfolios and address the evolving safety requirements of precision-oriented industries.

Emphasis on Ergonomic Design and Worker Comfort

Japan's aging industrial workforce is driving significant demand for ergonomically optimized PPE that reduces physical fatigue while maintaining high protection levels. Employers are prioritizing lightweight, breathable, and anatomically contoured protective gear to support worker wellbeing during extended operational shifts. The evolution toward comfort-centric design has accelerated innovation in materials science, including advanced polymer coatings, moisture-wicking fabrics, and flexible composite structures. This trend is particularly pronounced in automotive assembly and electronics manufacturing, where precision tasks demand effective hazard mitigation without compromising worker dexterity or productivity.

Growing Adoption of Sustainable and Eco-Friendly PPE Materials

Environmental consciousness is reshaping Japan's PPE procurement strategies, as manufacturers and industrial buyers increasingly prioritize eco-designed protective gear made from recycled fibers, biodegradable polymers, and sustainably sourced composites. This transition aligns with Japan's broader national sustainability agenda and corporate environmental responsibility commitments. Regulatory pressure, combined with growing end-user awareness of lifecycle impacts, is compelling PPE manufacturers to redesign product formulations and packaging. The adoption of green PPE solutions is creating competitive differentiation opportunities while simultaneously reducing the environmental footprint of industrial safety operations across Japan.

Market Outlook 2026-2034:

Japan's personal protective equipment market is poised for robust growth over the forecast period, supported by an evolving regulatory landscape, rising workplace safety awareness, and technological advancements in protective gear design and functionality. The transition toward smart, connected PPE solutions, combined with the continued expansion of Japan's manufacturing and construction sectors, is expected to sustain strong demand across all product categories. Growing emphasis on ergonomics, sustainability, and real-time hazard monitoring is reshaping how industries source and adopt protective equipment. The Kanto Region, as the primary industrial and commercial hub, is expected to lead regional demand, while emerging sectors such as healthcare and advanced manufacturing are anticipated to present new avenues for market participants. Continuous innovation in smart PPE and ergonomic protective solutions further underpins the market's long-term growth trajectory throughout the forecast horizon. The market generated a revenue of USD 5.72 Billion in 2025 and is projected to reach a revenue of USD 27.69 Billion by 2034, growing at a compound annual growth rate of 18.43% from 2026-2034.

Japan Personal Protective Equipment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Equipment Type |

Hand and Arm Protection |

22.3% |

|

End Use Industry |

Manufacturing |

28.4% |

|

Region |

Kanto Region |

35.6% |

Equipment Type Insights:

- Head, Eye and Face Protection

- Respiratory Protection

- Hand and Arm Protection

- Protective Clothing

- Fall Protection

- Protective Footwear

- Hearing Protection

- Others

Hand and arm protection dominates with a market share of 22.3% of the total Japan personal protective equipment market in 2025.

Japan's manufacturing, construction, chemical, and oil and gas sectors routinely expose workers to mechanical hazards, chemical substances, sharp materials, and extreme temperature conditions that directly affect the hands and arms. This persistent occupational risk profile has established hand and arm protection as the most universally demanded PPE category across the country's industrial landscape. Protective gloves, ranging from nitrile and latex variants to cut-resistant aramid-fiber designs, are mandated across numerous industrial processes under Japan's Industrial Safety and Health Act. The broad spectrum of applications, from precision electronics assembly to heavy-duty chemical handling, underscores the segment's cross-industry relevance and sustained commercial significance across the Japan personal protective equipment market.

Innovation in hand and arm protection has advanced rapidly in Japan, driven by demand for solutions that balance superior barrier performance with enhanced comfort and dexterity. Manufacturers are developing high-performance coatings, composite materials, and ergonomic glove architectures that cater to increasingly specific end-user requirements. Specialized product lines featuring cut-resistant fibers, chemical-protective polymers, and anti-static properties are being commercialized to address the evolving hazard profiles of Japan's precision-oriented industrial sectors. This trajectory of materials science-driven product development, supported by strong regulatory compliance requirements, continues to reinforce hand and arm protection as the dominant equipment type across the Japan personal protective equipment market.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Oil and Gas

- Head, Eye and Face Protection

- Respiratory Protection

- Protective Clothing

- Hand and Arm Protection

- Protective Footwear

- Fall Protection

- Hearing Protection

- Others

- Construction

- Head, Eye and Face Protection

- Respiratory Protection

- Protective Clothing

- Hand and Arm Protection

- Protective Footwear

- Fall Protection

- Hearing Protection

- Others

- Chemical

- Head, Eye and Face Protection

- Respiratory Protection

- Protective Clothing

- Hand and Arm Protection

- Protective Footwear

- Others

- Healthcare

- Head, Eye and Face Protection

- Respiratory Protection

- Protective Clothing

- Hand and Arm Protection

- Others

- Manufacturing

- Head, Eye and Face Protection

- Respiratory Protection

- Protective Clothing

- Hand and Arm Protection

- Protective Footwear

- Fall Protection

- Hearing Protection

- Others

Manufacturing leads with a share of 28.4% of the total Japan personal protective equipment market in 2025.

Japan's manufacturing sector encompasses a broad and complex array of industrial operations, including automotive assembly, electronics fabrication, steel production, and chemical processing, each of which presents distinct occupational hazard profiles requiring comprehensive PPE coverage. Workers engaged in manufacturing activities regularly encounter mechanical risks, thermal extremes, chemical exposures, and noise pollution, necessitating a full suite of protective equipment from gloves and respirators to hearing protection and safety footwear. The sector's sheer scale, supported by decades of industrial development and a deep-seated safety culture, ensures that manufacturing remains the largest institutional consumer of personal protective equipment across Japan.

The accelerating adoption of advanced manufacturing technologies, including industrial robotics, automated assembly systems, and precision machinery, has introduced new categories of occupational risks while simultaneously elevating safety standards. Japan's manufacturers are increasingly integrating comprehensive safety management systems that go beyond minimum regulatory compliance, embedding PPE procurement within holistic occupational health strategies. The rising penetration of Industry 4.0 practices has created demand for smart PPE solutions capable of interfacing with automated monitoring platforms. These dynamics are expected to sustain manufacturing's dominance and catalyze continued innovation in protective equipment design throughout the forecast period.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The Kanto Region exhibits a clear dominance with a 35.6% share of the total Japan personal protective equipment market in 2025.

The Kanto Region serves as Japan's primary economic and industrial engine, encompassing Tokyo, Kanagawa, Saitama, Chiba, Ibaraki, Tochigi, and Gunma prefectures. This concentration of major manufacturing facilities, advanced technology companies, chemical processing plants, and a vast healthcare infrastructure positions Kanto as the leading PPE demand center. The region's high workforce density across multiple industries ensures that occupational safety compliance requirements generate robust and consistent procurement activity throughout the forecast period.

Kanto's industrial diversity spans automotive manufacturing, pharmaceuticals, electronics, petrochemicals, and construction, each demanding distinct and high-volume PPE solutions. Tokyo's role as Japan's dominant business and healthcare hub further amplifies demand for specialized protective equipment in clinical and commercial environments. The region benefits from well-established distribution networks, a highly safety-conscious workforce culture, and proximity to major PPE manufacturers, collectively reinforcing the Kanto Region's sustained market leadership in the Japan Personal Protective Equipment Market.

Market Dynamics:

Growth Drivers:

Why is the Japan Personal Protective Equipment Market Growing?

Strengthening Regulatory Framework and Government Enforcement

Japan's Ministry of Health, Labour and Welfare continues to extend and enforce the Industrial Safety and Health Act, compelling employers across all industrial sectors to implement rigorous occupational safety programs that prominently feature personal protective equipment as a core compliance obligation. The Act mandates that employers not only provide appropriate protective gear but also ensure its proper use, maintenance, and timely replacement across all regulated operational environments. The framework governs chemical hazard management, heat stress prevention, respiratory protection, fall prevention, and hearing conservation, each mandating specific protective equipment categories relevant to distinct industrial applications. Japan's government has proactively expanded the roster of regulated chemical substances in recent years, broadening the scope of workplaces and job functions where specific PPE is legally required as a baseline protection measure. Non-compliance with ISHA standards carries significant legal, financial, and reputational consequences, providing powerful institutional incentives for organizations to maintain comprehensive, regularly audited, and well-documented PPE programs. Workplace safety inspections conducted by designated authorities reinforce adherence to these standards, ensuring that regulatory requirements translate into tangible procurement and usage behaviors across Japan's diverse industrial landscape. This regulatory momentum is expected to remain a sustained and primary growth driver throughout the forecast period.

Expanding Manufacturing Sector and Industry 4.0 Adoption

Japan's manufacturing sector, which encompasses automotive, electronics, aerospace, heavy industry, and precision component production, represents the largest and most diverse industrial consumer of personal protective equipment in the country. The ongoing integration of automation and robotics across production facilities creates evolving occupational hazard profiles that require continuous adaptation of protective equipment specifications and performance standards. Workers routinely encounter mechanical risks, exposure to industrial chemicals, extreme temperature conditions, noise pollution, and ergonomic strain across the full spectrum of manufacturing operations. Japan's strong commitment to Industry 4.0 implementation is further driving demand for connected, sensor-enabled protective solutions that interface with smart factory monitoring systems. Government-backed industrial modernization programs continue to expand Japan's manufacturing base, creating new facilities and workforce cohorts that require comprehensive PPE provisioning. The cultural emphasis on quality and safety embedded within Japan's industrial ethos ensures that organizations invest in high-performance, certified protective equipment rather than seeking cost-minimization alternatives. This combination of regulatory obligation, technological transformation, and institutional safety culture positions manufacturing as a principal and enduring growth driver for the Japan personal protective equipment market.

Growing Healthcare Demand Driven by an Aging Population

Japan has one of the world's most rapidly aging societies, with an unprecedented and consistently growing proportion of its population in advanced age categories placing substantial pressure on healthcare infrastructure and expanding the medical workforce. As the healthcare sector scales to meet escalating demand for eldercare, clinical, and long-term care services, the number of healthcare professionals requiring comprehensive protection from biological, chemical, and physical hazards is growing proportionally. Hospitals, clinics, diagnostic laboratories, nursing homes, pharmaceutical facilities, and home healthcare services collectively represent an expanding base of institutional PPE consumers across Japan. Healthcare workers require specialized protective equipment including disposable gloves, particulate respirators, surgical masks, protective gowns, eye shields, and full isolation apparel to maintain regulatory infection control standards and prevent occupational exposure. Japan's regulatory framework mandates comprehensive PPE protocols within healthcare environments, ensuring structured and consistent procurement behavior. The government's ongoing investments in healthcare infrastructure and eldercare expansion programs further broaden the institutional buyer base for protective equipment. Cultural adherence to hygiene, strong public awareness of infection prevention, and well-established workplace safety norms reinforce the healthcare sector's role as a major and growing driver of Japan's personal protective equipment market throughout the forecast period.

Market Restraints:

What Challenges the Japan Personal Protective Equipment Market is Facing?

Import Dependence and Supply Chain Vulnerability

Japan has historically relied significantly on imported PPE products, particularly disposable gloves, masks, and specialized protective textiles sourced from manufacturing-intensive economies in Southeast Asia. This dependence exposes the domestic market to supply chain disruptions caused by geopolitical tensions, logistics bottlenecks, natural disasters, and currency fluctuations. While domestic production capacity is gradually increasing, the transition from import reliance to self-sufficiency remains a multi-year process that introduces procurement risk for industrial buyers and healthcare institutions dependent on steady protective equipment availability.

High Cost of Advanced PPE Solutions

The increasing sophistication of personal protective equipment, particularly smart, sensor-enabled, and ergonomically advanced protective gear, carries a significantly higher price point compared to conventional PPE. For small and medium-sized enterprises operating within Japan's manufacturing and construction sectors, budget constraints can limit the adoption of premium protective solutions, resulting in continued reliance on basic, lower-cost alternatives. High upfront procurement costs, combined with maintenance and replacement expenses associated with advanced PPE, can deter organizations from fully upgrading their safety programs, potentially slowing adoption rates across price-sensitive market segments.

Proliferation of Counterfeit and Substandard Products

The presence of counterfeit and substandard PPE products in Japan's market represents a significant risk to worker safety and market credibility. Non-certified protective equipment that visually resembles compliant products but fails to meet established Japanese Industrial Standards and Ministry of Health, Labour and Welfare performance requirements can enter distribution channels, particularly through online procurement platforms and unregulated importers. The use of substandard PPE not only exposes workers to preventable hazards but also undermines trust in the broader PPE ecosystem, complicating procurement decision-making and potentially leading organizations toward over-reliance on brand recognition rather than verified performance certification.

Competitive Landscape:

Japan's personal protective equipment market is characterized by a competitive blend of established global manufacturers and specialized domestic producers, each leveraging distinct capabilities to address the country's diverse and demanding safety requirements. Major international players with well-established distribution networks and extensive product portfolios maintain strong market presence across key segments including respiratory protection, hand protection, and head and eye safety. Domestic Japanese manufacturers, particularly those specializing in industrial gloves and precision protective gear, have cultivated deep technical expertise and strong regulatory compliance capabilities that align closely with Japan's stringent Industrial Safety and Health Act standards. The competitive landscape is shaped by continuous product innovation, with participants investing in advanced materials research, smart PPE development, and sustainable design to differentiate their offerings. Strategic partnerships between technology firms and PPE manufacturers are expanding the availability of connected protective solutions. Distribution capabilities, after-sales support, and compliance certification remain critical competitive factors, particularly in serving industrial end-users who prioritize reliability and regulatory adherence in their procurement decisions.

Recent Developments:

- In February 2025, Towa Corporation, a prominent Japanese industrial glove manufacturer, launched the ActivGrip Omega-S series, an upgraded version of its established ActivGrip Omega product line. The new series features heavy-duty cut resistance, improved flexibility, and superior grip performance across dry, wet, and oily working conditions, catering to high-risk industrial environments within Japan's manufacturing, automotive, and construction sectors.

Japan Personal Protective Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Equipment Types Covered | Head, Eye and Face Protection, Respiratory Protection, Hand and Arm Protection, Protective Clothing, Fall Protection, Protective Footwear, Hearing Protection, Others |

| End Use Industries Covered |

|

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Personal Protective Equipment Market Report

The Japan personal protective equipment market size was valued at USD 5.72 Billion in 2025.

The Japan personal protective equipment market is expected to grow at a compound annual growth rate of 18.43% from 2026-2034 to reach USD 27.69 Billion by 2034.

Hand and arm protection dominated the market with a share of 22.3%, driven by the high prevalence of occupational hand injuries across manufacturing, construction, and chemical processing industries, supported by stringent regulatory mandates under Japan's Industrial Safety and Health Act.

Key factors driving the Japan personal protective equipment market include the strengthening of Japan's regulatory framework under the Industrial Safety and Health Act, rapid expansion of the manufacturing sector, adoption of Industry 4.0 technologies, growing healthcare infrastructure needs driven by an aging population, and continuous innovation in smart, ergonomic, and sustainable PPE solutions.

Major challenges include significant import dependence on Southeast Asian PPE suppliers creating supply chain vulnerabilities, high procurement costs for advanced smart and ergonomic protective equipment limiting adoption among SMEs, and the proliferation of counterfeit and substandard products undermining safety standards and market credibility across distribution channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade