Japan Power Market Size, Share, Trends and Forecast by Generation Source, and Region 2026-2034

Japan Power Market Size, Share, Trends & Forecast (2026-2034)

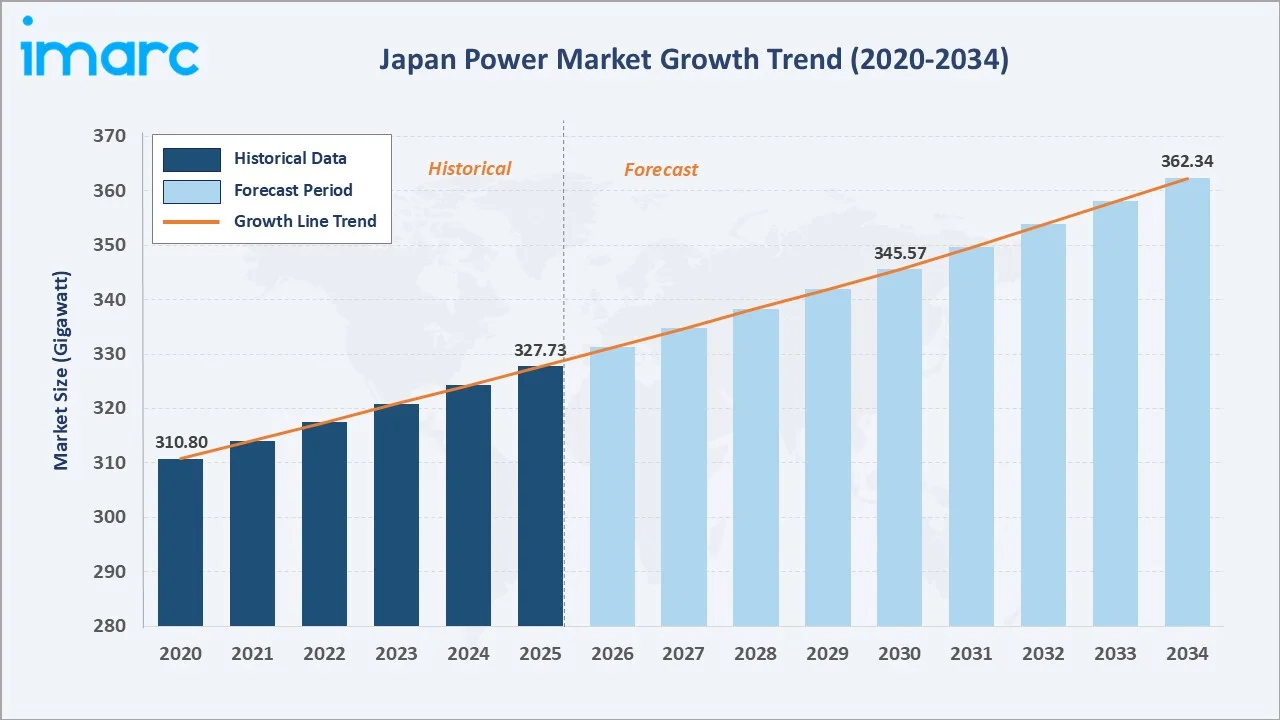

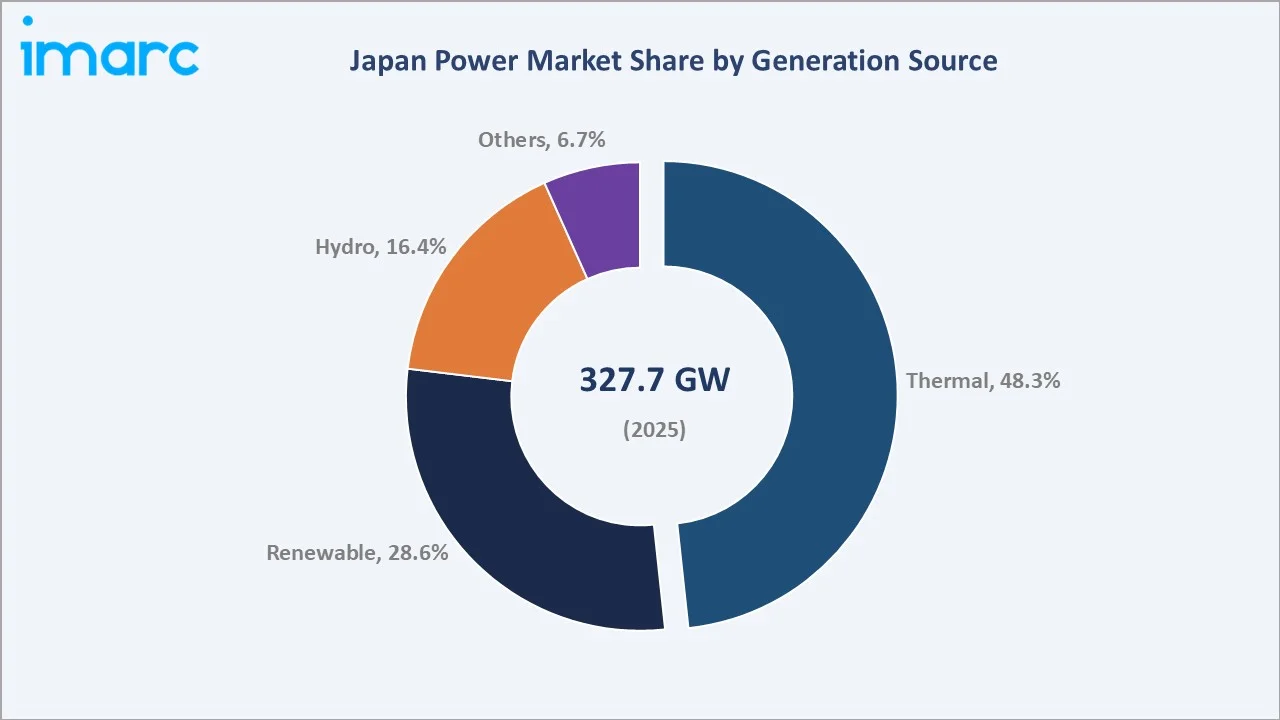

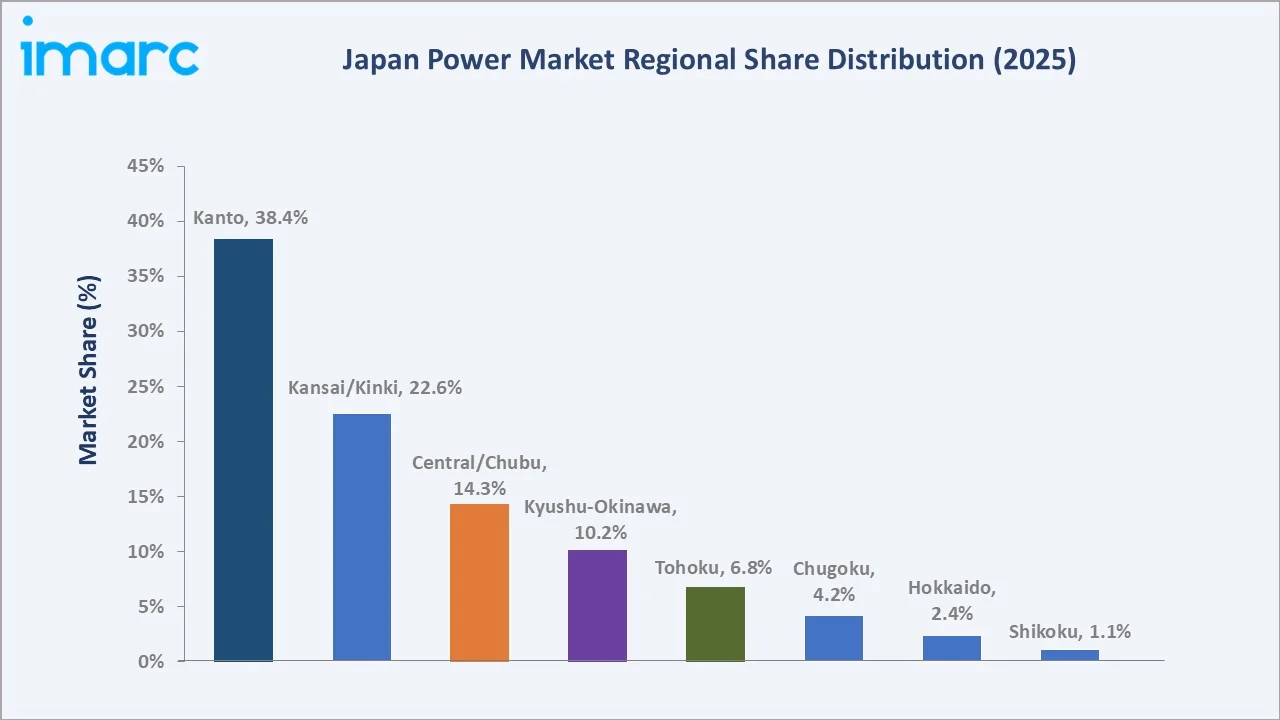

The Japan power market size reached 327.73 Gigawatt (GW) in 2025 and is projected to reach 362.34 Gigawatt (GW) by 2034, exhibiting a CAGR of 1.07% during 2026-2034. Thermal sources retain a dominant 48.3% share in 2025, while renewables account for 28.6% of installed capacity. Government carbon-neutrality targets for 2050, the GX Decarbonization Power Supply Bill, and surging investments in hydrogen and smart grid infrastructure are collectively propelling Japan power market growth. The Kanto Region leads all domestic markets with a 38.4% capacity share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

310.80 Gigawatt |

|

Market Size (2025) |

327.73 Gigawatt |

|

Forecast Market Size (2030) |

345.57 Gigawatt |

|

Forecast Market Size (2034) |

362.34 Gigawatt |

|

CAGR (2026-2034) |

1.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Gigawatt (GW) |

|

Largest Region |

Kanto Region – 38.4% share (2025) |

|

Fastest Growing Segment |

Renewable Energy (Solar & Offshore Wind) |

|

Dominant Generation Source |

Thermal – 48.3% share (2025) |

The chart shows Japan’s installed power capacity from 2020 to 2034, highlighting historical trends and projected growth driven by renewable policies and nuclear restarts.

To get more information on this market, Request Sample

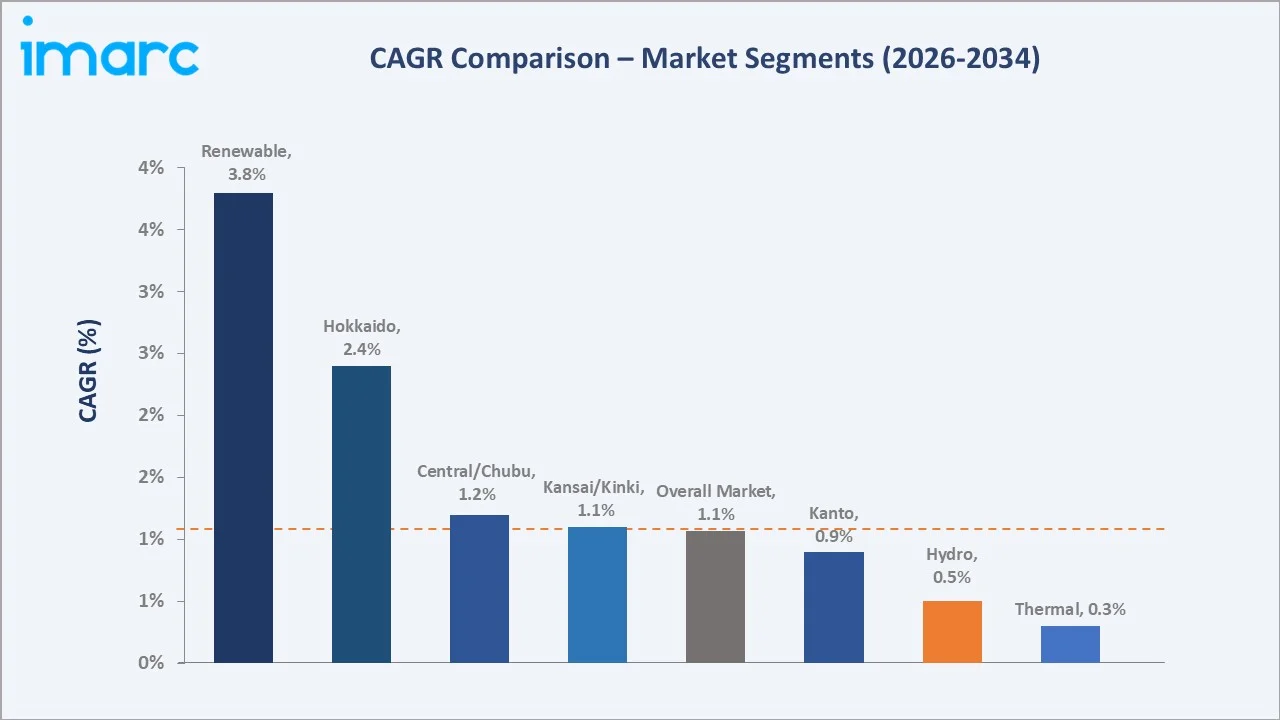

CAGR analysis indicates Renewable Energy and Others (Nuclear/Hydrogen) as the fastest-growing segments in Japan’s power market through 2034, outpacing overall market growth.

Executive Summary

Japan’s power market is navigating a structural transformation. The market reached 327.73 GW in 2025, expanding from 310.80 GW in 2020. Growth is measured but consistent at a 1.07% CAGR through 2034. Decarbonisation ambitions, grid modernisation, and a renewed focus on nuclear restart are reshaping the generation mix. The government’s GX Decarbonisation Power Supply Bill (2023) established firm targets for non-fossil fuel sources to represent 59% of the generation mix by 2030, creating a clear policy roadmap for investors and utilities.

Thermal power leads with 48.3% of installed capacity in 2025, supported by LNG and coal for baseload demand. Renewables grow fastest to 28.6%, driven by solar and offshore wind. Hydro remains stable at 16.4%, while other nuclear and hydrogen account for 6.7%.

Kanto leads with 38.4% of total capacity, followed by Kansai/Kinki at 22.6% and Chubu at 14.3%. Grid modernization, energy storage expansion, and offshore wind development across regions are creating new investment opportunities in Japan’s power market through 2034.

Key Market Insights

|

Insight |

Data |

|

Dominant Generation Source |

Thermal – 48.3% of installed capacity (2025) |

|

Fastest Growing Segment |

Renewable Energy – 28.6% share and rising (2025) |

|

Hydro Contribution |

16.4% of total installed capacity (2025) |

|

Others (Nuclear/Hydrogen) |

6.7% share with projected increase post-2026 |

|

Leading Region |

Kanto – 38.4% of national capacity (2025) |

|

Second Region |

Kansai/Kinki – 22.6% (2025) |

|

Market CAGR (2026–2034) |

1.07% |

|

Top Utilities |

TEPCO, KEPCO, Chubu Electric, JERA, Kyushu Electric |

Key Analytical Observations Supporting The Above Data:

- Thermal’s 48.3% share in 2025 reflects the continued reliance on LNG-fired generation for baseload stability, even as the government accelerates renewable integration targets under the 6th Strategic Energy Plan.

- Renewables at 28.6% represent the net result of over a decade of feed-in tariff (FIT) policy support and subsequent FIP (Feed-in Premium) reforms attracting private capital into solar and wind projects.

- Hydro’s stable 16.4% share underscores Japan’s mature hydropower infrastructure, with limited greenfield opportunity but significant scope for pumped-hydro energy storage expansion.

- The Kanto Region’s 38.4% dominance reflects Tokyo’s high industrial and commercial energy demand is reflected in TEPCO serving approximately 29 million customers across the region.

- The Kansai/Kinki Region at 22.6% benefits from KEPCO’s operational nuclear fleet, providing low-carbon baseload power and positioning the region as a decarbonisation leader within Japan.

- JERA, a TEPCO–Chubu Electric 50/50 JV, operates Japan’s largest thermal fleet, generating roughly 3,355.9 in FY2024 revenue.

Japan Power Market Overview

Japan’s power sector includes generation, transmission, distribution, and retail services across regional utilities and IPPs. The generation mix spans thermal, hydropower, renewables, and nuclear. With limited domestic resources and roughly 90% energy import dependence, energy security remains a key policy priority.

The ecosystem includes utility holding companies, OCCTO-controlled transmission operators, IPPs, energy storage developers, EV infrastructure providers, and regulators like METI. Market dynamics are shaped by yen-driven LNG import costs, global commodity price volatility, demographic demand shifts, and Japan’s international climate commitments under the Paris Agreement.

Market Dynamics

The following analysis maps the principal forces shaping Japan power market trends through 2034 across drivers, restraints, opportunities, and challenges.

To evaluate market opportunities, Request Sample

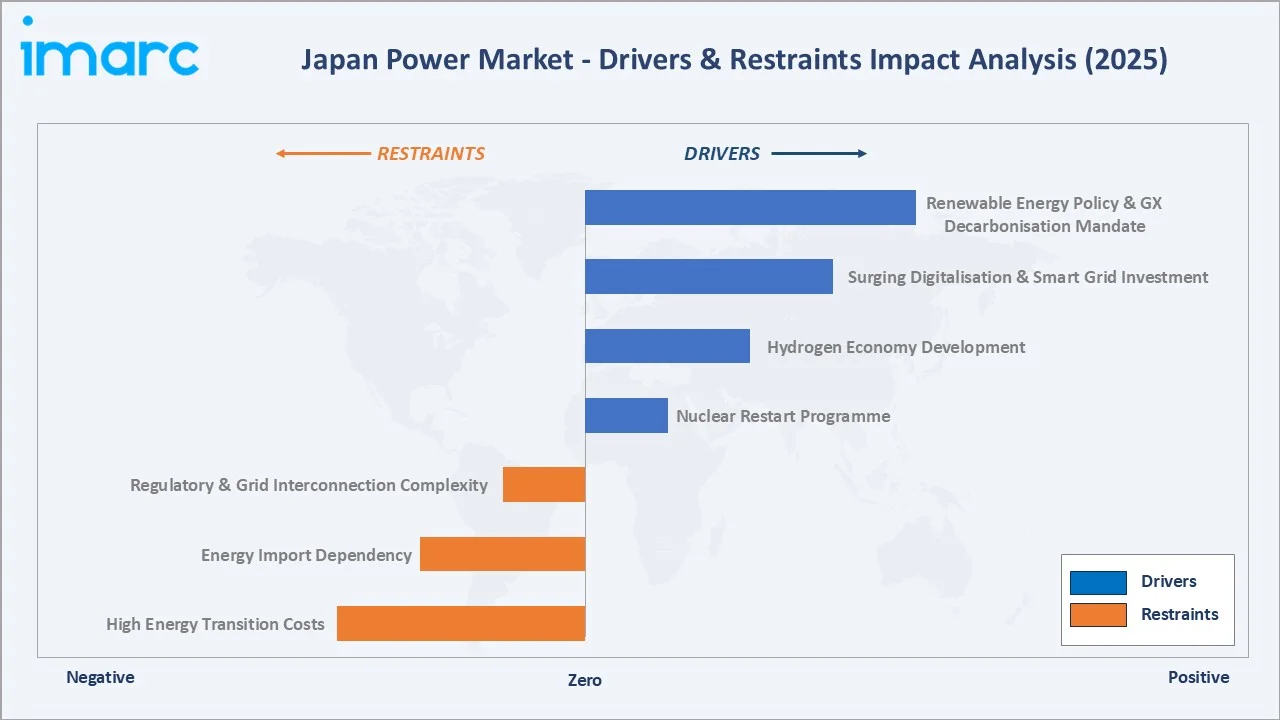

Market Drivers

- Renewable Energy Policy & GX Decarbonisation Mandate: Japan’s GX Decarbonisation Power Supply Bill (April 2023) mandates non-fossil fuel sources reach 59% of generation by 2030. Policies target renewable electricity share at 36–38% by 2030, up from 26% in 2022. This creates structural pull for solar, wind, geothermal, and biomass. PAG’s May 2024 launch of PAG REN I—targeting 108 GW of solar by 2030—illustrates the pace of private capital mobilisation.

- Surging Digitalisation & Smart Grid Investment: JERA and Toyota’s Sweep Energy Storage System expansion in 2023 underscores Japan’s smart grid rollout, with AI forecasting, IoT integration, and energy storage expected to improve grid efficiency and enable dynamic pricing.

- Hydrogen Economy Development: Japan’s amended Hydrogen Basic Strategy (June 2023) targets hydrogen supply of 3 million tonnes by 2030, 12 million by 2040, and 20 million by 2050. Mitsubishi Power’s Takasago Hydrogen Park, launched in September 2023, underscores Japan’s commitment to hydrogen as a zero-carbon baseload fuel.

- Nuclear Restart Programme: Following Fukushima, nuclear share fell from ~30% to near-zero by 2013. With 15 reactors restarted under NRA approvals, nuclear generation is recovering, supporting growth as additional reactors return to operation.

Market Restraints

- High Energy Transition Costs: Grid upgrades, offshore wind infrastructure, and battery storage are capital-intensive, with Japan’s GX transition expected to mobilize over ¥150 trillion for renewable expansion and grid modernization.

- Energy Import Dependency: Japan’s heavy energy import dependence exposed utilities to LNG price spikes during the 2022 crisis, with regulated retail tariffs limiting cost pass-through and compressing thermal generator margins.

- Regulatory & Grid Interconnection Complexity: Japan’s 50 Hz/60 Hz grid split restricts inter-regional power flows, increasing transmission constraints and raising renewable integration costs.

Market Opportunities

- Offshore Wind Expansion: Japan’s 30–45 GW offshore wind target by 2040, supported by expanding promotion zones, represents one of the largest greenfield investment opportunities.

- Battery Energy Storage Systems (BESS): Stonepeak’s May 2024 CHC partnership targeting ~1 GW of BESS capacity highlights Japan’s growing storage pipeline, with grid-scale batteries essential for integrating intermittent solar and offshore wind through 2034.

- EV Vehicle-to-Grid (V2G) Integration: Audi’s April 2024 150-kW charging hub in Tokyo’s Kioicho district signals growing EV adoption, while V2G technologies enable EVs to function as distributed storage and create new revenue streams.

Market Challenges

- Skilled Labour Shortage: Offshore wind and large-scale solar face acute shortages of certified marine engineers and construction workers, risking project delays and cost overruns.

- Social Acceptance of Nuclear Restarts: Community opposition remains a key risk, as NRA approval alone is insufficient reactor restarts typically require local government consent, creating potential delays.

- Grid Modernisation Financing: Upgrading Japan’s aging transmission infrastructure requires OCCTO-coordinated multi-utility investment, creating financing complexity and potential timeline slippage.

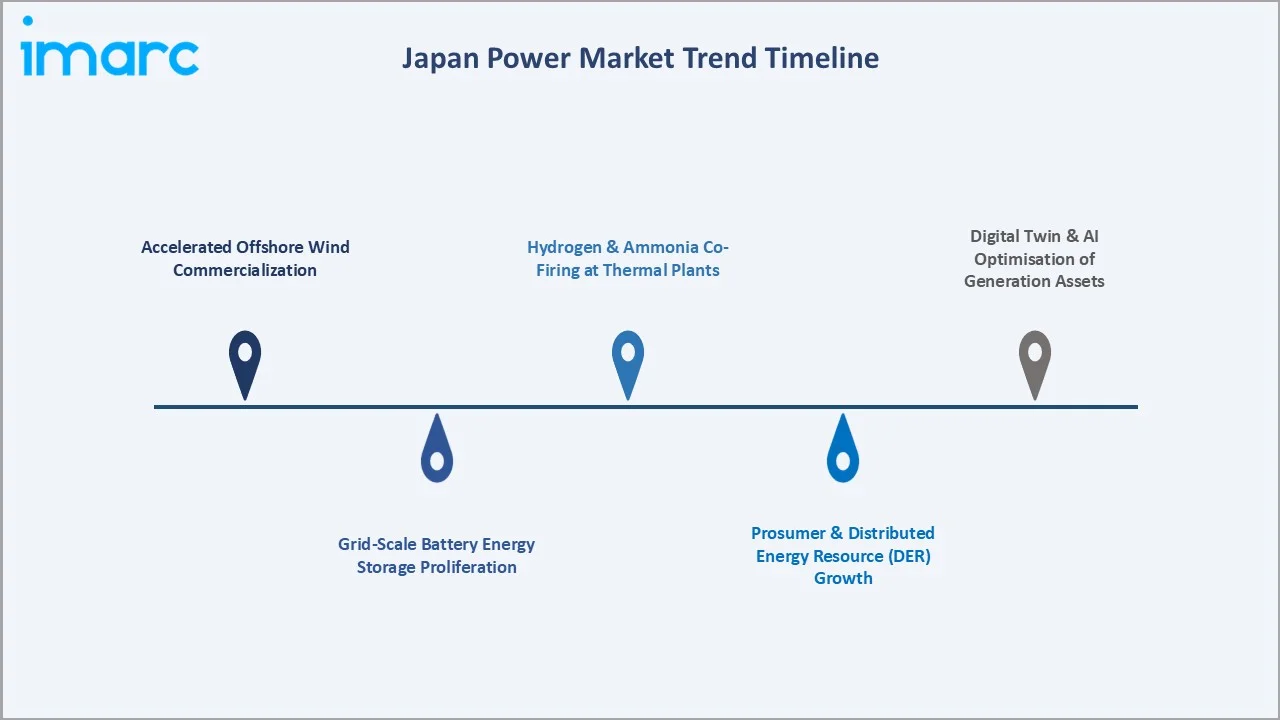

Emerging Japan Power Market Trends

Five structural themes are reshaping the Japan power market landscape between 2020 and 2034, as illustrated in the trend timeline below.

Trend 1: Accelerated Offshore Wind Commercialisation

Japan’s first offshore wind auctions in 2021–2022 and 30–45 GW 2040 target create a multi-decade pipeline, with Equinor, RWE, and Ørsted partnering Japanese utilities to develop local supply chains.

Trend 2: Grid-Scale Battery Energy Storage Proliferation

BESS deployment is accelerating with renewable growth. Stonepeak and CHC advanced a multi-region portfolio in May 2024, with utility-scale batteries increasingly providing frequency regulation and peak-shifting, replacing gas-fired peaker capacity.

Trend 3: Hydrogen & Ammonia Co-Firing at Thermal Plants

JERA and J-POWER are testing ammonia co-firing at coal plants, with JERA’s Hekinan project targeting 20% in the mid-2020s and up to 50% by 2030, reducing emissions while extending asset life.

Trend 4: Prosumer & Distributed Energy Resource (DER) Growth

Japan’s distributed rooftop solar capacity continues to expand. FIP reforms promote self-consumption and market participation, while Kyushu Electric and SB Energy are piloting VPPs aggregating residential solar and battery storage.

Trend 5: Digital Twin & AI Optimisation of Generation Assets

Japanese utilities are deploying digital twin and AI forecasting tools to optimize plant performance and reduce renewable curtailment. Variable renewables account for ~12% of generation, while fossil fuel electricity declined ~3% annually between 2019–2024, potentially falling 30% by 2040.

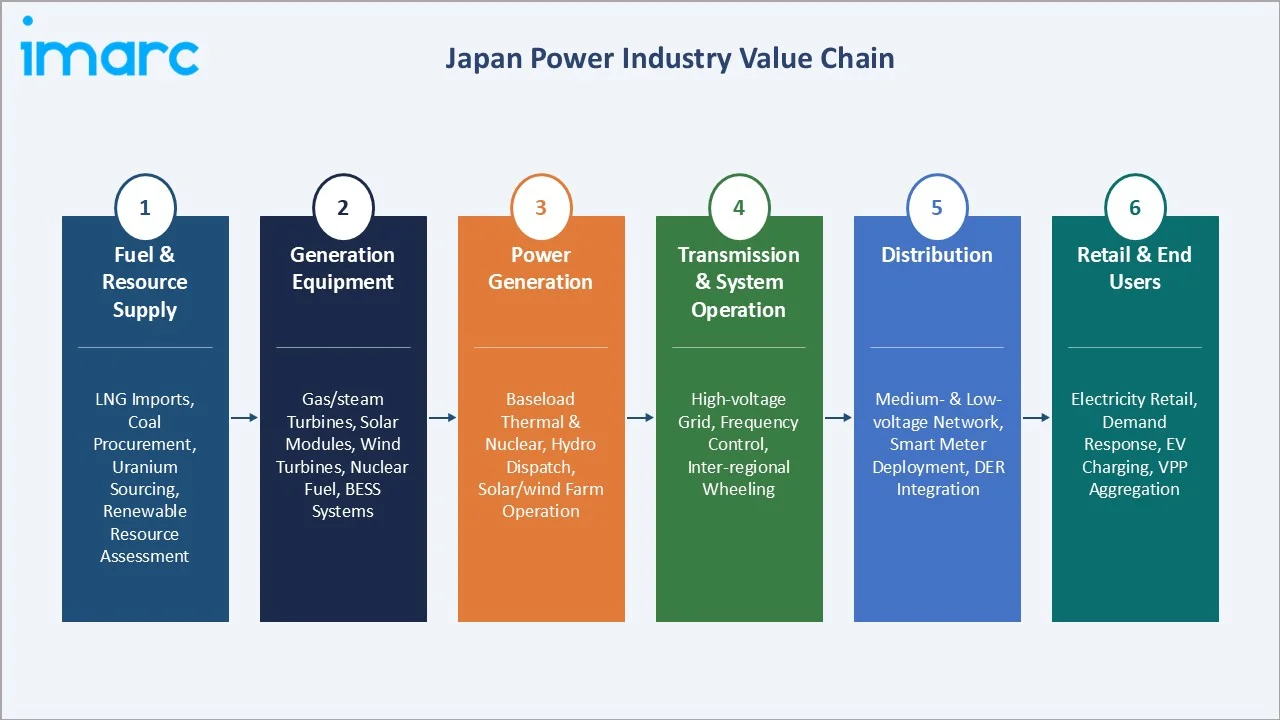

Japan Power Market – Industry Value Chain Analysis

Japan’s power market value chain spans fuel supply and equipment manufacturing to retail and end-use consumption, with each stage shaped by distinct regulatory, operational, and commercial dynamics.

|

Stage |

Key Activities |

Representative Players |

|

Fuel & Resource Supply |

LNG imports, coal procurement, uranium sourcing, renewable resource assessment |

JERA, Itochu, Marubeni, Mitsui, Mitsubishi Corp |

|

Generation Equipment |

Gas/steam turbines, solar modules, wind turbines, nuclear fuel, BESS systems |

Mitsubishi Heavy Industries, Toshiba, GE Vernova, Vestas |

|

Power Generation |

Baseload thermal & nuclear, hydro dispatch, solar/wind farm operation |

TEPCO, KEPCO, Chubu Electric, JERA, Kyushu Electric |

|

Transmission & System Op. |

High-voltage grid, frequency control, inter-regional wheeling |

OCCTO, TEPCO Power Grid, KEPCO T&D |

|

Distribution |

Medium- & low-voltage network, smart meter deployment, DER integration |

10 Regional Distribution Utilities |

|

Retail & End Users |

Electricity retail, demand response, EV charging, VPP aggregation |

TEPCO Energy Partner, Looop, ENNET, Tokyo Gas, Osaka Gas |

Technology Landscape in the Japan Power Industry

Renewable Generation Technology

Solar PV dominates renewable additions, with high-efficiency modules gaining adoption. Offshore wind is shifting from Fukushima FORWARD demonstrations to commercial deployment, using monopile and jacket foundations, while floating wind is being explored for deep-water Japan Sea sites.

Energy Storage & Grid Flexibility

LFP batteries dominate grid-scale BESS, while pumped hydro remains Japan’s largest storage asset. Flow battery pilots are underway in Hokkaido, and Stonepeak-CHC’s 1GW 2024 pipeline highlights growing private investment and revenue-stacking opportunities.

Smart Grid & Digitalisation

AMI deployment is largely complete in Japan, while OCCTO’s WAMS improves inter-regional visibility. AI-based forecasting tools from providers such as Hitachi Energy are increasingly integrated into utility control room operations.

Hydrogen & Ammonia Power

Mitsubishi Power’s Takasago Hydrogen Park supports hydrogen turbine validation, while Kawasaki Heavy Industries develops liquid hydrogen carriers. Japan is expanding hydrogen and ammonia-capable power generation through pilot and early commercial projects toward 2030.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Generation Source |

Thermal |

48.3% |

2025 |

|

Region |

Kanto Region |

38.4% |

2025 |

Breakup by Generation Source (2025)

The Japan power market is segmented into Thermal, Renewable, Hydro, and Others, with 2025 capacity shares showing Thermal dominance and Renewables as the fastest-growing segment.

To get more information on this market, Request Sample

Detailed segment-level analysis, growth drivers, and forward-looking outlook for each generation category is provided in the table below.

|

Generation Source |

2025 Share |

Key Insight & Outlook |

|

Thermal |

48.3% |

LNG-dominated; JERA’s fleet is the largest; co-firing with ammonia to reduce emissions. Share expected to decline to ~38% by 2034 as renewables and nuclear scale. |

|

Renewable |

28.6% |

Solar PV leading; offshore wind commercial scale from 2026. FIP policy and 108 GW solar target by 2030 drive investment. Fastest growing segment at 3.8% CAGR. |

|

Hydro |

16.4% |

Mature infrastructure; limited greenfield opportunity. Pumped hydro expansion (3 GW pipeline by 2030) supports grid flexibility services. |

|

Others |

6.7% |

Primarily nuclear restarts under NRA approval. Post-2025 restart approvals expected to lift segment to ~10% by 2034. Highest segment CAGR at 4.2%. |

Regional Market Insights

The Japan power market is analyzed across eight regions, with 2025 capacity shares highlighting Kanto’s dominance driven by Tokyo’s economic scale.

Detailed breakdown of each region’s market characteristics, growth drivers, and key players is presented in the table below.

|

Region |

2025 Share |

Key Characteristics & Growth Drivers |

|

Kanto |

38.4% |

Japan’s most populous region. TEPCO serves ~29M customers. High industrial load from manufacturing and data centres. Major offshore wind zones off Chiba and Ibaraki coasts. |

|

Kansai/Kinki |

22.6% |

KEPCO’s service territory. Benefits from nuclear baseload from Takahama and Ohi reactors. Osaka Expo 2025 infrastructure boosting demand. Strong industrial cluster. |

|

Central/Chubu |

14.3% |

Chubu Electric (JERA co-founder) serves Toyota’s manufacturing heartland. High industrial electricity intensity. Aggressive EV charging infrastructure rollout. |

|

Kyushu-Okinawa |

10.2% |

Kyushu Electric; high solar penetration causing curtailment challenges. Sendai nuclear plant operational. Okinawa pursuing energy self-sufficiency via renewables. |

|

Tohoku |

6.8% |

Tohoku Electric; some of Japan’s best onshore wind resources. Post-2011 reconstruction modernised grid. Offshore wind zones off Akita and Aomori are nationally advanced. |

|

Chugoku |

4.2% |

Chugoku Electric serves western Honshu. Mix of thermal and hydro. Lower industrial intensity vs. Kanto/Chubu. |

|

Hokkaido |

2.4% |

Hokkaido Electric; abundant onshore wind and geothermal. HVDC subsea cable to Honshu is a critical bottleneck constraining renewable export. |

|

Shikoku |

1.1% |

Smallest regional market. Shikoku Electric serves four prefectures. Hydro-heavy generation mix; limited offshore wind potential. |

Competitive Landscape

Japan’s power market remains concentrated among ten regional utilities, with a growing renewable IPP sector. While liberalization since 2016 enabled new retail entrants, transmission and distribution continue to operate as regulated monopolies.

The positioning matrix above illustrates the market standing of key players across two dimensions: global market presence and strategic investment level. TEPCO, KEPCO, and JERA occupy the Leaders quadrant, while SoftBank Energy and Enel Japan represent the Challengers and Emerging Players.

|

Company Name |

Primary Brand / Subsidiary |

Market Position |

|

Tokyo Electric Power Company (TEPCO) |

TEPCO Energy Partner / TEPCO Power Grid / TEPCO Renewable |

Market Leader – Kanto; ~29M customers |

|

Kansai Electric Power Company (KEPCO) |

KEPCO / Kanden Energy Solution |

Market Leader – Kansai; nuclear fleet operator |

|

JERA Co., Inc. |

TEPCO + Chubu Electric (50:50 JV) |

Japan’s largest thermal generator; LNG supply chain leader |

|

Chubu Electric Power Company |

JERA Nex bp |

Market Leader – Chubu; JERA founding partner |

|

Kyushu Electric Power Company |

Kyushu Electric |

Leader – Kyushu; highest solar penetration; nuclear operator |

|

Tohoku Electric Power Company |

Tohoku Electric |

Leader – Tohoku; top-tier onshore wind resource base |

|

Toyota Tsusho Corporation (Acquired SB Energy) |

Terras Energy |

Challenger – Renewable IPP & retail; VPP developer |

|

Enel X Japan K.K |

Enel X Japan / Enel Green Power |

Emerging – Solar & wind IPP; international developer |

Key Company Profiles

Tokyo Electric Power Company (TEPCO)

- Overview: Japan’s largest electric utility serving ~29 million customers across the Kanto region. TEPCO operates generation, transmission, and retail businesses through subsidiaries including TEPCO Power Grid, TEPCO Energy Partner, and TEPCO Renewable Power.

- Portfolio: LNG combined-cycle, pumped hydro, solar farms, offshore wind leases off Chiba. TEPCO-PG operates Kanto’s transmission & distribution network.

- Recent Developments: In 2026, Tokyo Electric Power Company restarted the 1.36 GW Kashiwazaki-Kariwa Unit 6 nuclear reactor, marking its first reactor restart since the 2011 Fukushima disaster and strengthening Japan’s energy security and low-carbon power supply. In January 2026: Tokyo Electric Power Company Holdings (TEPCO) announced a ¥3.1 trillion cost-cutting plan for FY2025–2034, including asset sales, restructuring, and strategic partnerships to strengthen financial stability and support long-term growth.

- Strategic Focus: Accelerating decarbonisation via offshore wind and BESS; ongoing Fukushima Daiichi decommissioning; smart meter rollout completion by 2025.

JERA Co., Inc.

- Overview: JERA is Japan’s largest power generator, created as a 50/50 JV between TEPCO and Chubu Electric. It operates 59 GW of domestic power generation capacity and handles approximately 36 million tons of LNG annually, manages one of Asia’s largest LNG supply portfolios.

- Portfolio: LNG-fired, coal-fired, and oil-fired thermal power plants, ammonia co-firing pilots at coal stations (Hekinan), hydrogen-based decarbonisation initiatives, and offshore wind development pipeline through JERA Nex and global joint ventures.

- Recent Developments: In August 2025, JERA and bp completed the formation of JERA Nex bp, their new 50:50-owned joint venture (JV) for the development and operation of offshore wind development. In June 2024, JERA successfully completed a 20% ammonia co-firing trial at its Hekinan coal-fired power plant, marking one of the world’s first large-scale demonstrations of ammonia fuel use at a commercial thermal power station.

- Strategic Focus: Ammonia co-firing at Hekinan coal plant (20% by 2024, 50% by 2030); hydrogen supply chain development; global LNG portfolio optimisation.

Kansai Electric Power Company (KEPCO)

- Overview: Kansai Electric Power Company serves Japan's Kansai region and operates a diversified generation portfolio across nuclear, thermal, and hydroelectric assets. The company operates approximately 164 power plants with a total installed capacity of about 35,760 MW, making it one of Japan’s largest regional utilities.

- Portfolio: Nuclear (Takahama, Ohi, Mihama), LNG-fired, coal-fired, hydro, and expanding solar & offshore wind assets.

- Recent Developments: In October 2025, Kansai Electric Power signed a Share Subscription Agreement with Simply Blue Group's offshore wind development arm. In September 2025, Activist investor Elliott Management acquired a 4–5% stake in Kansai Electric, becoming one of its top three shareholders, and urged the company to sell non-core assets, improve profitability, and enhance shareholder returns.

- Strategic Focus: Maximizing nuclear output, expanding Kanden Energy Solution retail business, and growing offshore wind portfolio.

Market Concentration Analysis

The Japan power market exhibits high concentration in generation and network infrastructure, with the top five utilities—TEPCO, KEPCO, Chubu Electric, Kyushu Electric, and Tohoku Electric—collectively controlling approximately 70–75% of total installed generation capacity in 2025.

As of March 2024, 729 registered electricity retail companies existed in Japan following market liberalisation. Despite market liberalisation, incumbent regional utilities still retain roughly 75–80% of household customers in Japan, reflecting relatively low switching rates and continued consumer trust in established utility brands. Renewable IPP development is driving incremental fragmentation in generation, with infrastructure funds aggregating assets to achieve operating scale.

Investment & Growth Opportunities

Offshore Wind Development

Japan has set offshore wind development targets of 10 GW by 2030 and 30–45 GW by 2040, creating a long-term project pipeline supported by government policy and competitive auctions, although project economics remain sensitive to rising construction and supply-chain costs.

Grid-Scale BESS

Japan’s BESS market is nascent but growing rapidly. Regulatory reforms enabling BESS participation in ancillary services markets improve project revenue stacking. Stonepeak’s 2024 BESS platform targets 1GW of projects across Japan, indicating strong institutional capital interest.

Hydrogen Supply Chain Infrastructure

Investment in hydrogen production, storage, and distribution infrastructure—aligned with Japan’s amended Hydrogen Basic Strategy—creates opportunities across electrolysis equipment, storage tanks, and hydrogen-capable gas turbine upgrades. Japan’s government has committed over 3 trillion yen in hydrogen-related subsidies through 2030.

EV Charging & V2G Infrastructure

Japan’s commitment to phasing out pure-ICE vehicle sales by the mid-2030s requires a nationwide EV charging network. V2G platforms present utility-scale opportunity to monetise EV batteries as distributed grid assets, generating new revenue streams for utilities and energy aggregators.

Future Japan Power Market Outlook (2026-2034)

The Japan power market is expected to reach 362.34 GW of installed capacity by 2034, up from 327.73 GW in 2025, at a 1.07% CAGR. The growth trajectory is shaped by three converging forces: renewable energy expansion, nuclear capacity restoration, and demand-side electrification driven by EV adoption and industrial decarbonisation.

Thermal’s share is projected to decline from 48.3% in 2025 by 2034, as LNG-based generation is gradually replaced by offshore wind, solar, and the restart of nuclear power plants. The shift is supported by continued renewable capacity additions over the forecast period.

The Others segment—grouped at 6.7% in 2025—is expected to grow steadily by 2034, driven by the restart of NRA-approved reactors following municipal approvals. This shift supports Japan’s broader decarbonization strategy, with non-fossil fuel sources anticipated to account for a significantly larger share of total generation capacity by the end of the forecast period.

Research Methodology

|

Research Component |

Methodology Details |

|

Primary Research |

IDIs with utility executives, IPP developers, grid operators, regulators (METI, NRA), and investment analysts. Validation of quantitative data through expert networks. |

|

Secondary Research |

Analysis of METI energy statistics, OCCTO grid operation reports, IEA Japan energy profile, IRENA capacity data, company annual reports, and regulatory filings. |

|

Bottom-Up Modelling |

Installed capacity aggregated by generation type and region from plant-level datasets, cross-validated against METI published statistics. |

|

Top-Down Modelling |

Macro demand drivers (GDP growth, industrial output, EV adoption, population trends) used to project national capacity requirements through 2034. |

|

Forecasting Model |

Multi-variable regression integrating policy scenarios (GX Bill targets, nuclear restart schedule), technology cost curves (LCOE), and investment pipeline data. |

|

Data Triangulation |

Cross-validation of IMARC estimates against public utility disclosures, OCCTO annual reports, and IEA country-level projections. |

Japan Power Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Gigawatt |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Generation Sources Covered | Thermal, Hydro, Renewable, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Tokyo Electric Power Company (TEPCO), Kansai Electric Power Company (KEPCO), JERA Co., Inc., Chubu Electric Power Company, Kyushu Electric Power Company, Tohoku Electric Power Company, Toyota Tsusho Corporation (Acquired SB Energy), Enel X Japan K.K, etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan power market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan power market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan power industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Power Market Report

The Japan power market reached 327.73 GW of installed capacity in 2025, up from 310.80 GW in 2020, reflecting steady growth supported by renewable energy expansion and industrial demand.

The Japan power market is projected to reach 362.34 GW by 2034, growing at a CAGR of 1.07% during 2026-2034, driven by offshore wind, solar, and nuclear capacity restoration.

Key drivers include government carbon-neutrality targets, the GX Decarbonisation Power Supply Bill, hydrogen economy investments, smart grid modernisation, and accelerating EV-driven electricity demand.

Thermal power leads the market with a 48.3% share in 2025, largely driven by LNG-fired plants, while renewables, accounting for 28.6%, are expected to witness the fastest growth over the forecast period.

The Kanto Region leads with a 38.4% share in 2025, driven by Tokyo’s industrial, commercial, and residential energy demand served primarily by TEPCO and its subsidiaries.

Key players include Tokyo Electric Power Company (TEPCO), Kansai Electric Power Company (KEPCO), JERA Co., Inc., Chubu Electric Power Company, Kyushu Electric Power Company, Tohoku Electric Power Company, Enel X Japan K.K, and Toyota Tsusho Corporation.

Renewables held a 28.6% capacity share in 2025 and are the market’s fastest-growing segment at a 3.8% CAGR. Solar PV and offshore wind are the primary drivers, supported by FIP policy.

Key challenges include high energy transition and grid modernization costs, dependence on imported fossil fuels, limited interconnection between 50 Hz and 60 Hz grids, and public resistance to nuclear restarts.

Key opportunities include offshore wind (30–45 GW by 2040), grid-scale BESS deployment, hydrogen supply chain infrastructure, and EV charging and V2G platform development.

Japan’s 6th Strategic Energy Plan targets 36–38% renewable electricity by 2030, driven by expansion in solar, wind, hydropower, biomass, and geothermal to support decarbonization goals.

Japan’s Hydrogen Basic Strategy targets 3 million tonnes of supply by 2030. Hydrogen and ammonia co-firing at thermal plants, and dedicated hydrogen turbines, will progressively decarbonise the generation fleet through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)