Japan Printed Circuit Board Market Size, Share, Trends and Forecast by Type, Substrate, End-Use Industry, and Region, 2026-2034

Japan Printed Circuit Board Market Summary:

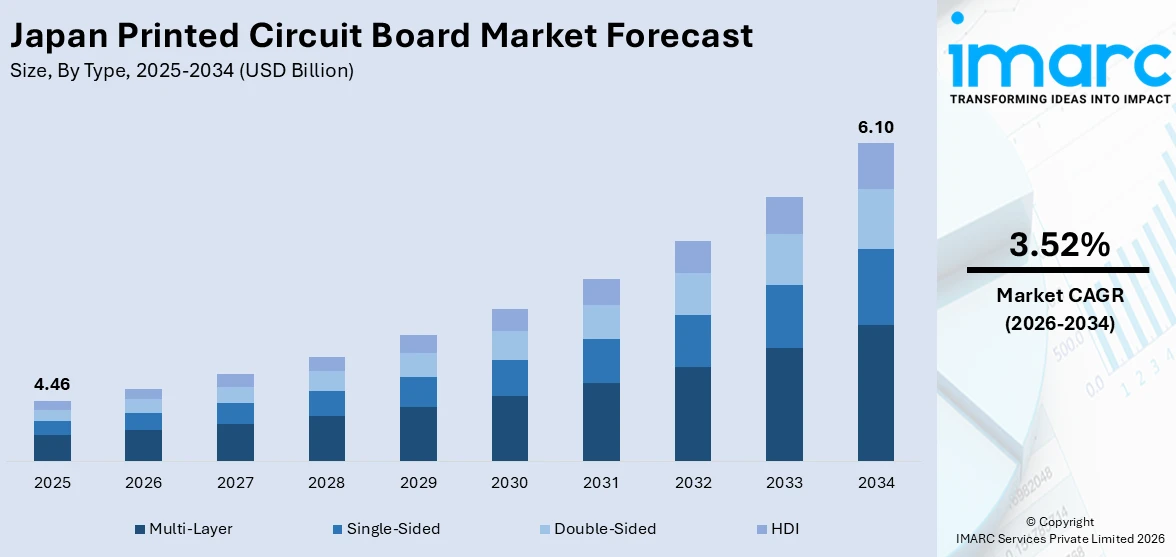

The Japan printed circuit board market size was valued at USD 4.46 Billion in 2025 and is projected to reach USD 6.10 Billion by 2034, growing at a compound annual growth rate of 3.52% from 2026-2034.

The Japan printed circuit board market is fueled by a convergence of expanding automotive electrification, accelerating 5G network deployments, and sustained consumer electronics innovation. Increasing demand for advanced driver-assistance systems and electric vehicle (EV) power electronics is reshaping board design requirements, while government investments in semiconductor self-sufficiency are reinforcing domestic supply chains, collectively elevating the market share.

Key Takeaways and Insights:

- By Type: Multi-layer dominates the market with a share of 38.4% in 2025, driven by its ability to support complex circuitry and higher component densities essential for automotive, telecommunications, and high-performance computing applications across Japan.

- By Substrate: Rigid leads the market with a share of 52.3% in 2025, owing to superior mechanical stability, widespread suitability across end-use industries, including industrial electronics and automotive systems, and established large-scale manufacturing infrastructure in Japan.

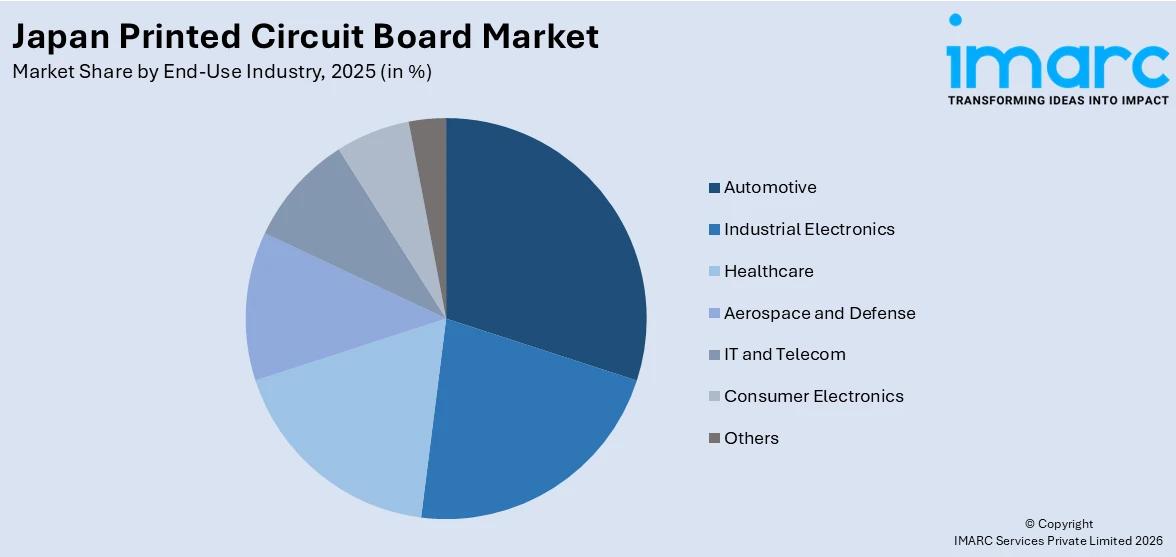

- By End-Use Industry: Automotive represents the largest segment with a market share of 28.5% in 2025, reflecting Japan's globally recognized automotive manufacturing heritage, strong demand for in-vehicle electronics, and rapidly expanding EV platforms.

- By Region: Kanto Region comprises the largest region with 35.2% share in 2025, driven by the concentration of Japan's leading electronics corporations, semiconductor research institutions, and advanced technology infrastructure across Tokyo and neighboring prefectures.

- Key Players: Key players in the Japan printed circuit board market drive growth through continuous investments in high-layer-count and high-density interconnect technologies, expanding manufacturing capacity, fostering strategic partnerships, and innovating eco-friendly substrates to serve diverse industrial applications.

To get more information on this market Request Sample

The Japan printed circuit board market occupies a pivotal position in the country's broader electronics ecosystem, underpinned by decades of manufacturing expertise and a relentless commitment to technological precision. The market serves as the foundational infrastructure for an expansive range of industries, from automotive and consumer electronics to aerospace and healthcare, reflecting Japan's stature as a global leader in electronics manufacturing. Domestic producers have consistently differentiated themselves through superior engineering capabilities, particularly in the development of high-density interconnect and flexible boards that effectively meet the evolving miniaturization requirements of modern devices. Government-backed semiconductor strategies have further catalyzed domestic capacity expansion, creating a robust and innovation-centric environment for advanced board development. Notably, around USD 101.96 Billion worth of electrical and electronic equipment was exported from Japan in 2025, underscoring the scale and global relevance of the country's electronics manufacturing sector and the central role that printed circuit boards continue to play in sustaining and amplifying this remarkable output.

Japan Printed Circuit Board Market Trends:

Growing Adoption of Flexible and High-Density Interconnect Boards

The Japan printed circuit board market is experiencing accelerating demand for flexible and high-density interconnect boards, driven by the miniaturization trend across consumer electronics, wearables, and connected automotive modules. These advanced board types offer superior design freedom, weight reduction, and thermal efficiency, making them indispensable in compact, high-performance devices. Rising investments in advanced manufacturing technologies and precision engineering are further enabling the production of more complex, multi-layer printed circuit board architectures to meet evolving industry requirements.

5G Infrastructure Rollout Reshaping Printed Circuit Board Specifications

The nationwide rollout of 5G networks across Japan is fundamentally reshaping printed circuit board specifications, with boards required to support high-frequency, low-dielectric-loss performance for base stations and connected devices. As per IMARC Group, the Japan 5G infrastructure market size reached USD 5.7 Billion in 2025 and is set to reach USD 65.8 Billion by 2034. Japanese manufacturers are increasingly investing in multi-layer and high-frequency substrates to meet these advanced signal integrity requirements.

Sustainability-Driven Innovations in Printed Circuit Board Manufacturing

Environmental sustainability has become a defining competitive priority for Japan's printed circuit board manufacturers, with a strong emphasis on reducing electronic waste and adopting circular economy practices. Companies are innovating with lead-free solder, halogen-free laminates, and closed-loop material recovery systems to align with evolving regulatory frameworks and corporate responsibility commitments. Additionally, manufacturers are increasingly optimizing energy consumption and water usage across production processes to further minimize their overall environmental footprint.

.webp)

Market Outlook 2026-2034:

The Japan printed circuit board market is positioned for sustained and progressive growth through the forecast period, driven by structural demand across the automotive, consumer electronics, telecommunications, and industrial electronics sectors. The transition towards EVs, deployment of advanced driver-assistance systems, and widespread adoption of 5G-capable devices are expected to maintain strong volume and value growth across multiple board categories. The market generated a revenue of USD 4.46 Billion in 2025 and is projected to reach a revenue of USD 6.10 Billion by 2034, growing at a compound annual growth rate of 3.52% from 2026-2034. As application complexity increases across all end-use industries, the demand for higher-layer-count boards, flexible substrates, and specialized high-frequency materials is expected to accelerate.

Japan Printed Circuit Board Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Multi-Layer |

38.4% |

|

Substrate |

Rigid |

52.3% |

|

End-Use Industry |

Automotive |

28.5% |

|

Region |

Kanto Region |

35.2% |

Type Insights:

- Single-Sided

- Double-Sided

- Multi-Layer

- HDI

Multi-layer dominates with a market share of 38.4% of the total Japan printed circuit board in 2025.

Multi-Layer has established clear dominance in the market, owing to its unmatched capacity to integrate complex circuitry within compact form factors—a quality essential across the country's most dynamic demand segments. The growing deployment of artificial intelligence (AI) computing infrastructure, automotive electronic control units, and high-performance communication equipment has elevated the requirement for boards with several functional layers. This capability also supports higher signal integrity and improved performance in densely packed electronic systems.

The deepening penetration of multi-layer printed circuit boards across industrial electronics, information technology, and telecommunications has further consolidated their commanding market position. Japanese manufacturers, leveraging their engineering heritage in precision fabrication, continue to push boundaries in high-layer-count and fine-line geometries, enabling ultra-compact board designs that fulfill the demands of next-generation consumer gadgets and autonomous vehicle systems. The alignment between domestic semiconductor ecosystems and printed circuit board producers creates a virtuous cycle of innovation, where chip-scale packaging advances simultaneously drive increases in board complexity and expand the overall addressable market for multi-layer configurations in Japan.

Substrate Insights:

- Rigid

- Flexible

- Rigid-Flex

Rigid leads with a share of 52.3% of the total Japan printed circuit board market in 2025.

Rigid maintains a commanding position in the market, due to its exceptional structural integrity, cost efficiency, and suitability across the full range of industrial, automotive, consumer, and telecommunications applications. Rigid printed circuit boards provide the mechanical support and thermal management performance required by densely populated electronic assemblies, making them the default choice for Japanese manufacturers producing everything from household appliances to precision medical instruments. Their compatibility with standardized mass production processes further enhances scalability and consistent product quality.

The continued prevalence of rigid printed circuit boards across Japan's industrial electronics and automotive sectors reflects entrenched design preferences and established supply chain efficiencies that alternative substrates have yet to fully overcome. Japanese original equipment manufacturers (OEMs) have refined their production processes around rigid board specifications over decades, creating significant switching costs that reinforce substrate loyalty. While flexible and rigid-flex variants are gaining traction in niche applications, the sheer volume of standard electronic products, ranging from power supplies and control modules to server hardware, ensures that rigid boards retain their leading position throughout the forecast horizon.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Industrial Electronics

- Healthcare

- Aerospace and Defense

- Automotive

- IT and Telecom

- Consumer Electronics

- Others

Automotive exhibits a clear dominance with a 28.5% share of the total Japan printed circuit board market in 2025.

Automotive remains the leading end-use industry in the market, driven by the country's global leadership in vehicle manufacturing and the rapid electronic content intensification across modern vehicle platforms. As per automotive industry reports, 4.56 Million vehicles were sold in 2025, representing surge of 3.2% from 2024. Advanced driver-assistance systems, battery management systems for EVs, infotainment architectures, and connectivity modules depend critically on sophisticated multi-layer and high-frequency boards.

The electrification of Japan's automotive fleet is driving a structural shift in printed circuit board demand toward thermally resilient, high-reliability configurations capable of withstanding the demanding operating conditions of electric drivetrains and power electronics. Lightweight yet structurally durable boards are increasingly specified for battery monitoring and charging interface applications, where compactness and energy efficiency are non-negotiable design priorities. Japan's major automakers have maintained close supplier relationships with domestic printed circuit board producers, ensuring that design iteration cycles remain short and that board specifications continue to evolve in lockstep with the advancement of next-generation vehicle platforms.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represents the leading segment with a 35.2% share of the total Japan printed circuit board market in 2025.

The Kanto Region commands the largest share of the market, anchored by Tokyo's status as the nation's foremost hub for semiconductor research, high-technology manufacturing, and corporate headquarters of leading electronics firms. The region's dense concentration of printed circuit board producers, downstream electronics assemblers, and specialized material suppliers creates a deeply integrated supply chain ecosystem that consistently attracts investment and talent. This concentration also enables faster collaboration, shorter development cycles, and efficient scaling of advanced printed circuit board production.

Beyond its manufacturing concentration, the Kanto Region benefits from proximity to world-class universities, government research institutions, and national technology accelerators that continuously seed innovation in board materials, fabrication processes, and design methodologies. The presence of automotive electronics firms and consumer technology companies in Tokyo and its surrounding prefectures ensures diversified demand streams that buffer the region from sector-specific volatility. As Japan's 5G rollout, AI infrastructure investment, and EV adoption accelerate, the region is positioned to expand its commanding market share.

Market Dynamics:

Growth Drivers:

Why is the Japan Printed Circuit Board Market Growing?

Automotive Electrification and Advanced Driver-Assistance System Integration

Japan's automotive industry represents one of the most significant structural drivers of printed circuit board demand, with vehicle electrification and advanced driver-assistance system adoption fundamentally transforming the nature and volume of board requirements. As OEMs accelerate the development of EV platforms, the need for specialized boards capable of managing high-voltage power electronics, battery thermal regulation, and bidirectional charging communication has surged considerably. Each modern EV platform requires multiple categories of printed circuit boards, ranging from high-layer-count multi-layer boards in electronic control unit clusters to thermally managed rigid-flex boards in battery management systems, creating unprecedented complexity in automotive electronics supply chains. Japan's battery manufacturers and automotive suppliers have developed deep collaborative ties with domestic board producers to ensure that specification advancement occurs in lockstep with vehicle platform evolution.

Government-Led Semiconductor Policy and Domestic Capacity Investment

Japan's national semiconductor strategy has emerged as a formidable structural driver of the printed circuit board market, creating a policy-backed investment environment that is systematically reshaping domestic supply chain capabilities. The Ministry of Economy, Trade and Industry's coordinated approach to re-shoring high-value electronics manufacturing encompasses significant subsidies, tax incentives, and public-private partnerships designed to attract global technology firms and expand indigenous production capacity simultaneously. This policy momentum has catalyzed a series of landmark investments in semiconductor fabrication, advanced packaging, and downstream components, including printed circuit boards, effectively anchoring demand that might otherwise migrate to competing regional suppliers. In February 2024, TSMC inaugurated its first Japan fabrication facility, Japan Advanced Semiconductor Manufacturing, Inc. (JASM), in Kumamoto, an event that brought together a network of domestic suppliers and partners and anchored sustained localized demand for substrates and specialty printed circuit boards tied to advanced logic and automotive semiconductor nodes, meaningfully strengthening Japan's interconnect ecosystem.

Expanding Consumer Electronics Innovations and Export Competitiveness

Japan's consumer electronics sector remains a foundational demand driver for the printed circuit board market, sustained by the country's globally recognized strength in device innovation, manufacturing quality, and export competitiveness. The transition towards increasingly miniaturized, multifunctional devices, spanning smartphones, advanced gaming hardware, wearable health monitors, and next-generation display technologies, has elevated the specifications required of printed circuit boards, with a particular emphasis on high-density interconnect configurations and flexible substrates that can accommodate ever-tighter component pitches. The penetration of smart home ecosystems, connected appliances, and industrial Internet of Things (IoT) devices further diversifies and sustains board demand beyond traditional consumer gadget categories. As per IMARC Group, the Japan smart homes market is set to reach USD 22.7 Billion by 2034.

Market Restraints:

What Challenges the Japan Printed Circuit Board Market is Facing?

Raw Material Price Volatility and Supply Chain Dependency

The Japan printed circuit board market faces significant headwinds from fluctuating prices of key raw materials, including copper foil, epoxy resin, and specialty laminates. Periodic supply disruptions and commodity price spikes directly compress manufacturer margins, complicate production planning, and can delay delivery timelines for downstream customers. Japan's reliance on imported raw materials exposes the industry to exchange rate volatility and geopolitical supply risks that are difficult to fully mitigate through domestic sourcing or long-term supply contracts, creating persistent operational uncertainty for board producers of all sizes.

Skilled Labor Shortages and an Aging Technical Workforce

Japan's aging population is creating persistent challenges for the printed circuit board manufacturing sector, where skilled technical labor, particularly engineers proficient in precision fabrication, inspection, and quality assurance, is increasingly scarce. The declining enrollment in electronics and engineering vocational programs compounds this structural issue, constraining the industry's capacity to scale production and adopt advanced automation technologies. Higher wage pressures resulting from labor market tightening are incrementally increasing production costs, particularly for smaller manufacturers with limited capital for automation investment, threatening the competitiveness of Japan's mid-tier printed circuit board producers.

Intensifying Competition from Lower-Cost Regional Manufacturers

The Japan printed circuit board market faces escalating competitive pressure from regional manufacturers in China and South Korea, where lower energy costs, substantial government subsidies, and extensive labor cost advantages create significant structural pricing differentials. Japanese producers, though recognized for superior quality and engineering precision, must continuously invest in process innovation and technology differentiation to justify premium pricing in standard board categories. Failure to differentiate sufficiently risks accelerating market share erosion as cost-sensitive customers in industrial and consumer electronics segments opt for functionally equivalent boards available at lower price points from regional competitors.

Competitive Landscape:

The Japan printed circuit board market is characterized by a competitive landscape where leading domestic players differentiate through specialized capabilities, long-standing relationships with major automotive and consumer electronics OEMs, and sustained investments in advanced fabrication technologies. Market participants are increasingly focusing on high-layer-count multi-layer boards, flexible circuits, high-density interconnect configurations, and IC substrates, which command premium pricing and align with the fastest-growing end use segments. Consolidation activity is actively shaping the competitive environment, with strategic acquisitions and partnerships enabling players to expand technology portfolios and geographic reach simultaneously. Competitive differentiation is also being achieved through commitment to eco-friendly manufacturing processes, as customers across the automotive, healthcare, and consumer electronics sectors increasingly mandate lead-free, halogen-free, and recyclable board specifications.

Japan Printed Circuit Board Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Single-Sided, Double-Sided, Multi-Layer, HDI |

| Substrates Covered | Rigid, Flexible, Rigid-Flex |

| End Use Industries Covered | Industrial Electronics, Healthcare, Aerospace and Defense, Automotive, IT and Telecom, Consumer Electronics, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Printed Circuit Board Market Report

The Japan printed circuit board market reached a value of USD 4.46 Billion in 2025.

The market is projected to grow at a CAGR of 3.52% during 2026-2034, reaching USD 6.10 Billion by 2034.

Key growth drivers include rising demand for automotive electronics, 5G and data center buildouts, domestic semiconductor investment, and flexible PCB adoption.

The report covers segmentation by type, substrate, end use industry, and region. Each segment includes detailed market size and forecast analysis.

Key trends include growing adoption of flexible and high-density interconnect PCBs, eco-friendly manufacturing innovations, accelerating 5G and data center deployment, automotive electrification, and expansion of IoT-enabled smart electronics applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade