Japan Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034

Japan Real Estate Market Size, Share, Trends & Forecast (2026-2034)

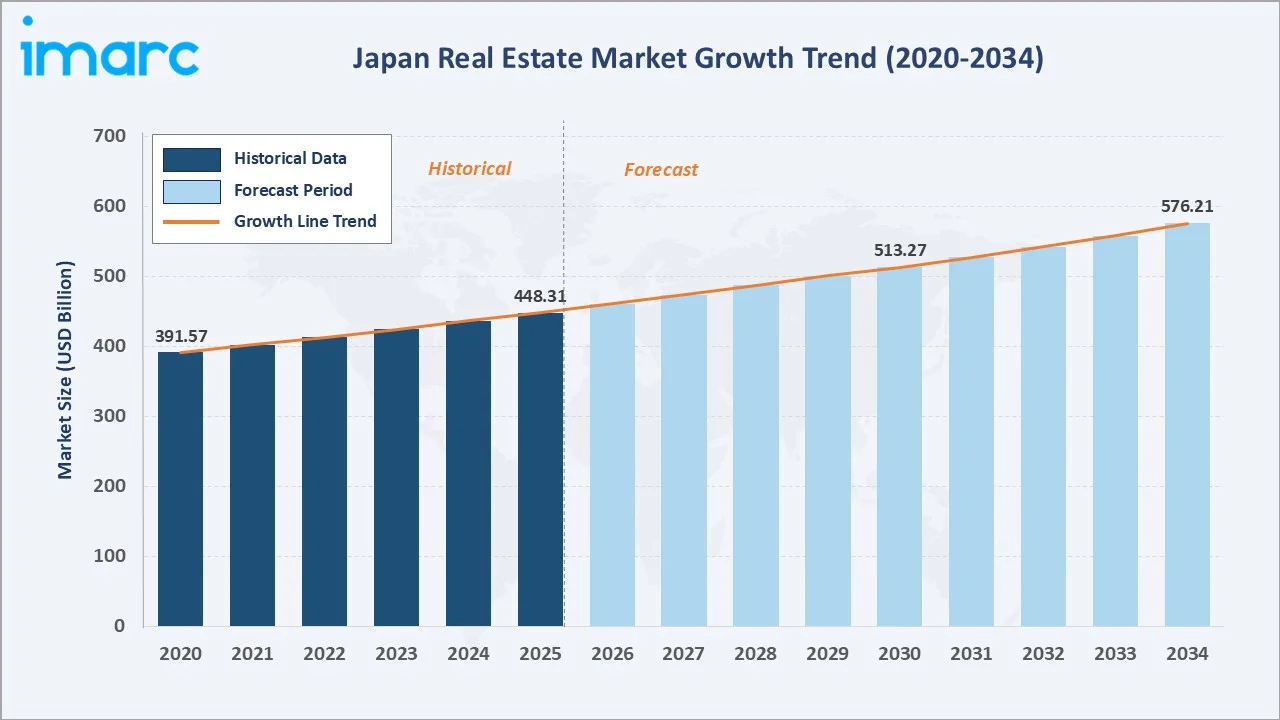

Japan real estate market reached USD 448.31 Billion in 2025 and is projected to reach USD 576.21 Billion by 2034, growing at a CAGR of 2.74% during 2026-2034. Rising demand for senior-adapted housing, rapid urban development, growing international investment trends, and the widespread adoption of smart building technologies are key growth drivers propelling the Japan real estate market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 448.31 Billion |

|

Forecast Market Size (2034) |

USD 576.21 Billion |

|

CAGR (2026-2034) |

2.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

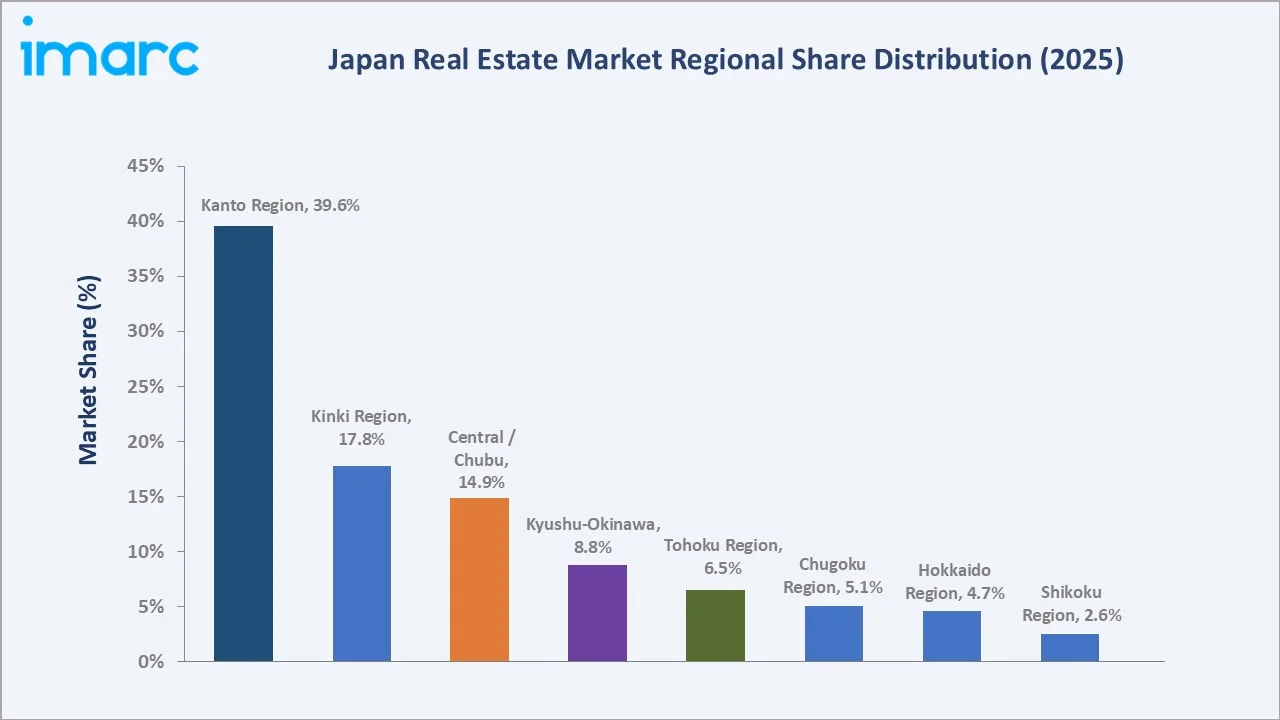

Largest Region |

Kanto Region (39.6% share, 2025) |

|

Fastest Growing Region |

Kinki Region |

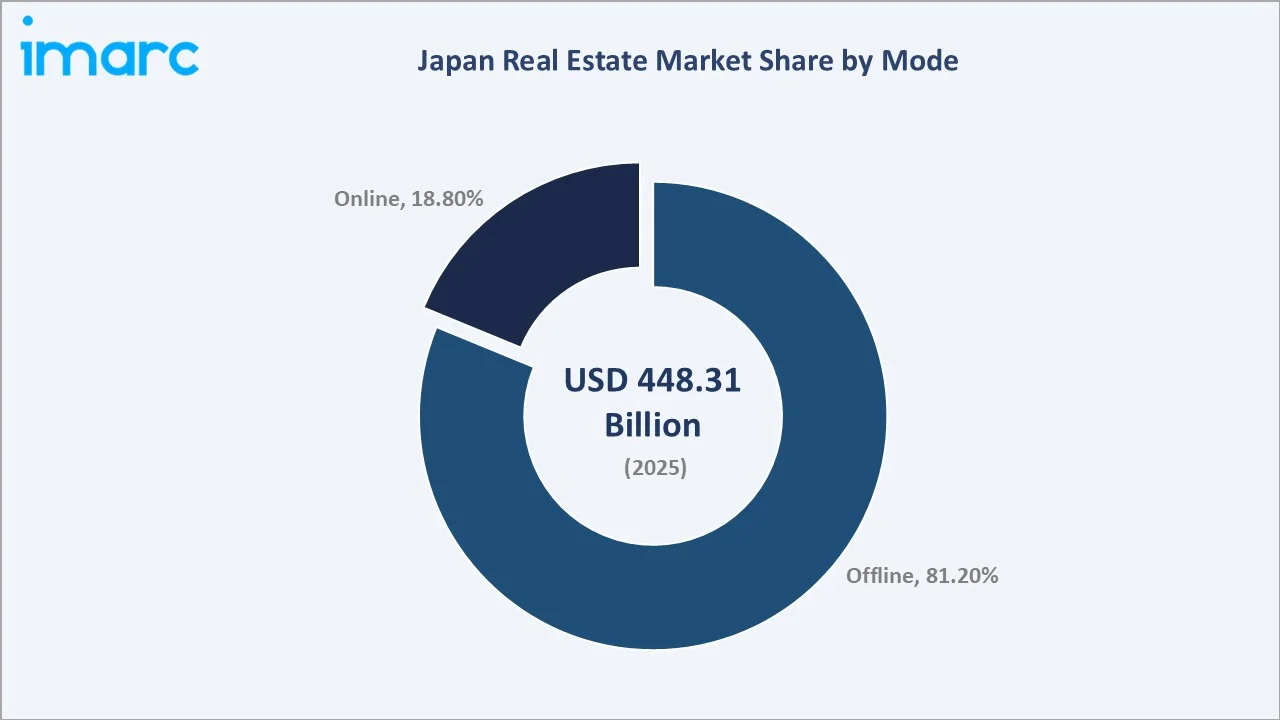

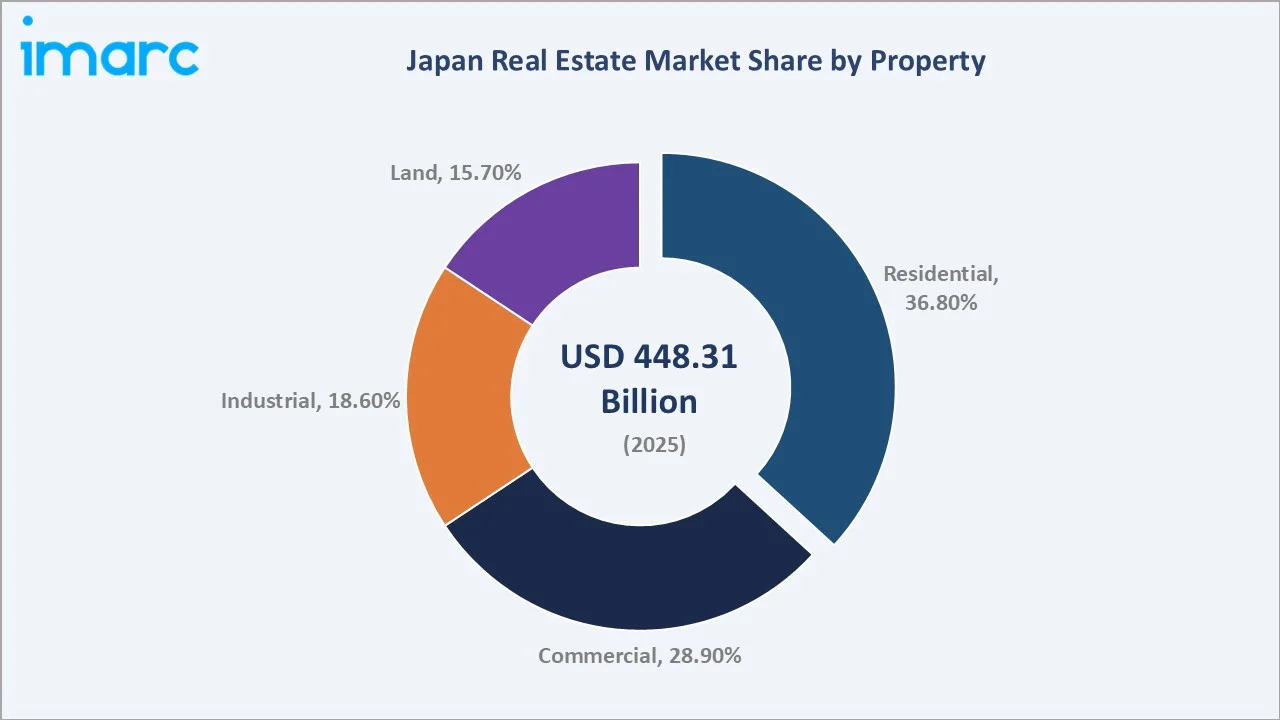

The Kanto region dominates, holding a 39.6% market share in 2025, while the residential segment leads property demand at 36.8%. The offline mode remains the primary transaction channel at 81.2%. Japan's real estate sector offers stable returns, transparent legal frameworks, and well-developed infrastructure, making it one of Asia's most attractive investment destinations.

To get more information on this market, Request Sample

With activity spanning residential, commercial, industrial, and land segments, the market is expected to continue expanding through 2034, supported by government urban revitalization programs, rising PropTech adoption, inbound tourism-linked hospitality real estate, and a sustained influx of foreign institutional capital. The Japan real estate market forecast points to a structurally sound expansion path across all property types and regions.

Executive Summary

The Japan real estate market is on a sustained growth path, underpinned by accelerating urban development, rising international investment inflows, and structural shifts in housing demand driven by Japan's aging demographic profile. The market reached USD 448.31 Billion in 2025 and is forecast to surpass USD 576.21 Billion by 2034, reflecting a CAGR of 2.74% over the forecast period.

The Kanto region leads nationally with a 39.6% revenue share in 2025, driven by Tokyo's position as a global financial and commercial hub and its deep pool of institutional real estate investment. The Kinki region, at 17.8%, represents the second-largest and fastest-growing sub-market, buoyed by Osaka's Expo 2025 legacy development and Kyoto's thriving hospitality real estate sector. The residential property type commands the largest segment share at 36.8%, followed by commercial at 28.9%.

The offline transaction mode holds an 81.2% share in 2025, reflecting the continued dominance of traditional brokerage networks across Japan's property market. However, the online channel at 18.8% is the fastest-growing mode, as PropTech platforms gain adoption among younger buyers and digital-first investors. Key players continue to drive market consolidation, innovation in mixed-use development, and expansion into senior housing and smart community formats.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Property) |

Residential – 36.8% share (2025) |

|

Dominant Mode |

Offline – 81.2% share (2025) |

|

Leading Region |

Kanto Region – 39.6% revenue share (2025) |

|

Fastest Growing Region |

Kinki Region (Osaka Expo legacy + tourism) |

|

Top Companies |

Mitsui Fudosan Co., Ltd., Mitsubishi Estate Co., Ltd., Sumitomo Realty & Development Co., Ltd., Daiwa House Industry Co., Ltd., Tokyu Fudosan Holdings., Nomura Real Estate Holdings, Inc., Sekisui House, Ltd. |

|

Market Opportunity |

Senior housing and PropTech platforms projected for above-average growth through 2034 |

Key Analytical Observations Supporting The Above Data:

- Residential property leads the Japan real estate market at 36.8% (2025), supported by urban in-migration, government first-home buyer incentives, and an accelerating pipeline of senior-adapted housing across metropolitan prefectures.

- Commercial real estate accounts for 28.9% of the market in 2025, driven by strong demand for premium Grade A office space in Tokyo, Osaka, and Nagoya, where vacancy rates for high-spec assets remain at multi-year lows.

- The offline mode commands 81.2% of market share in 2025, reflecting a deeply embedded brokerage culture, preference for in-person site visits, and the legal complexity of Japanese property transactions that necessitate professional intermediaries.

- The Kanto region holds 39.6% of national market activity in 2025, anchored by Tokyo's unrivaled concentration of commercial assets, multinational tenants, and global institutional capital targeting core Japanese real estate.

- Online real estate platforms are growing rapidly, currently representing 18.8% of the market in 2025. PropTech adoption is accelerating as virtual tour technology, AI-based listing tools, and e-signature capabilities become mainstream in residential and light-commercial segments.

Japan Real Estate Market Overview

Japan's real estate market encompasses a broad spectrum of property types – residential, commercial, industrial, and land – transacted through both traditional offline brokerage channels and a rapidly expanding set of digital platforms. The market ecosystem spans property developers, construction firms, financial institutions, REITs, property management companies, government housing agencies, and international capital allocators.

As one of Asia's largest and most mature real estate markets, Japan offers stable long-term returns, transparent legal frameworks for property ownership and leasing, and a well-functioning regulatory environment. The Japan real estate market trends reflect the confluence of demographic shifts, technology-led smart city development, and sustained foreign institutional interest.

Macroeconomic factors, including Japan's accommodative monetary policy stance, high urban concentration, government-backed revitalization programs, and the country's positioning as a safe-haven asset destination, are primary growth catalysts.

Market Dynamics

To evaluate market opportunities, Request Sample

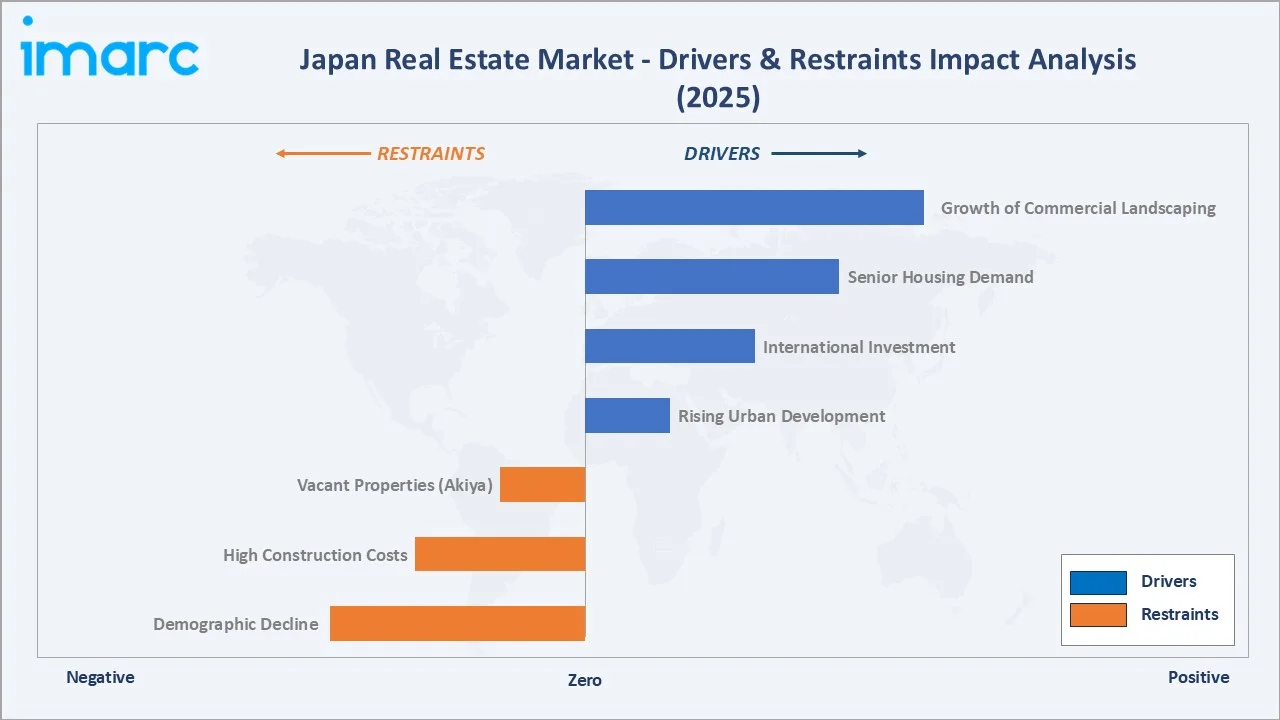

Market Drivers

- Rising Urban Development and Government Revitalization Programs: National and prefectural governments are channeling significant resources into urban densification, transit-oriented development, and the regeneration of underutilized urban land.

- Increasing International Investment Inflows: Japan’s stable regulatory environment, transparent property market, and attractive capitalization rates are reflected in rising foreign participation, which increased from 18% in 2024 to 27% in 2025.

- Expanding Senior Housing Demand: With citizens aged over 65 expected to constitute 34.8% of Japan's population by 2040, according to the National Institute of Population and Social Security Research, the need for senior-adapted residential formats is growing rapidly across all major urban prefectures.

- Smart City and Technology-Integrated Development: Large-scale smart city projects, including Toyota's Woven City hydrogen-powered community near Mount Fuji and the Smart City Takeshiba initiative in Tokyo, are driving investment into technologically enhanced mixed-use developments.

These drivers reinforce a self-sustaining growth cycle, government urban programs stimulate new property supply, foreign capital inflows improve price discovery and market depth, and demographic-driven demand creates durable absorption across residential and senior housing sub-segments, collectively elevating the Japan real estate market outlook through 2034.

Market Restraints

- Elevated Number of Vacant Properties (Akiya): Japan faces a structural challenge with approximately 9 million vacant homes, known locally as akiya, predominantly concentrated in rural and regional areas. These properties depress peripheral land values and complicate urban planning objectives, creating a persistent structural overhang that dampens investment sentiment outside major metropolitan zones.

- Demographic Headwinds and Shrinking Population: Japan's declining birth rate and aging population create structural demand constraints in secondary and tertiary cities, where net outmigration toward metropolitan centers is intensifying.

- Rising Construction and Compliance Costs: Material cost inflation, escalating labor shortages in the construction sector, and increasingly stringent energy efficiency certification requirements are raising the viability threshold for new development projects, particularly in the mid-market residential and small-scale commercial segments.

Market Opportunities

- PropTech and Online Platform Expansion: The digitization of property search, transaction processing, and asset management functions represents a fast-growing and under-monetized opportunity. Online channels currently represent 18.8% of real estate mode share in 2025, with significant room for expansion as younger demographic cohorts increasingly prefer digital-first property engagement tools.

- Logistics and Industrial Real Estate Demand: The sustained rise of e-commerce penetration and supply chain resilience strategies is generating strong demand for Class A logistics facilities and last-mile distribution centers, particularly in corridors connecting the Kanto, Kinki, and Central/Chubu regions, where freight infrastructure is concentrated.

- Tourism-Linked and Hospitality Real Estate: Japan's recovery as a premier global tourism destination is creating new development opportunities in branded hotel assets, serviced apartments, and resort real estate.

Market Challenges

- Urban-Rural Market Bifurcation: The concentration of real estate demand and investment in a small number of metropolitan areas creates a two-speed market that challenges developers, investors, and policymakers seeking to deliver balanced, nationwide growth.

- Regulatory Complexity and Compliance Burden: Japan's layered property ownership laws, complex zoning regulations, and evolving building code requirements create high compliance costs for international entrants and smaller domestic developers, limiting competitive market participation and slowing development timelines in some regions.

Emerging Market Trends

1. Demand for Senior and Age-Adapted Housing

The Ministry of Land's subsidy programs for private-sector senior housing construction have been instrumental in bridging viability gaps for smaller developers. Private equity investment in senior living assets reached a post-pandemic high in 2024, with AXA IM Alts acquiring a portfolio of two nursing homes in Japan with over 170 purpose-built assisted living units in Kyoto and Nishinomiya, strengthening its healthcare presence in the Greater Osaka region.

2. Smart City Initiatives and Technology-Integrated Real Estate

Toyota's Woven City project, a 175-acre hydrogen-powered smart community near Mount Fuji incorporating autonomous systems, robotic services, and AI-driven infrastructure, represents a landmark in technology-integrated real estate in Japan. Joint initiatives such as the Smart City Takeshiba project in Tokyo, developed collaboratively by TOKYU LAND CORPORATION and SoftBank Corp., are deploying data exchange platforms to optimize urban operations and enhance property asset quality.

3. Growth of Online Real Estate Platforms and PropTech Adoption

Online real estate platforms now represent 18.8% of transaction mode share in 2025, driven by younger buyers and renters who prefer virtual property tours. Major platforms, including LIFULL HOME'S, Athome, and SUUMO, are attracting growing user bases through real-time listings data, satellite imagery integration, and neighborhood analytics tools.

4. Sustainable and Green Building Adoption

Developers are embedding green roofs, solar panel integration, energy-efficient HVAC systems, and BELS (Building Energy-efficiency Labeling System) certifications into new projects to meet rising institutional ESG standards. Tokyo's land prices increased by 2.7% as of January 2025, partly reflecting premium valuations attached to carbon-compliant assets in core districts.

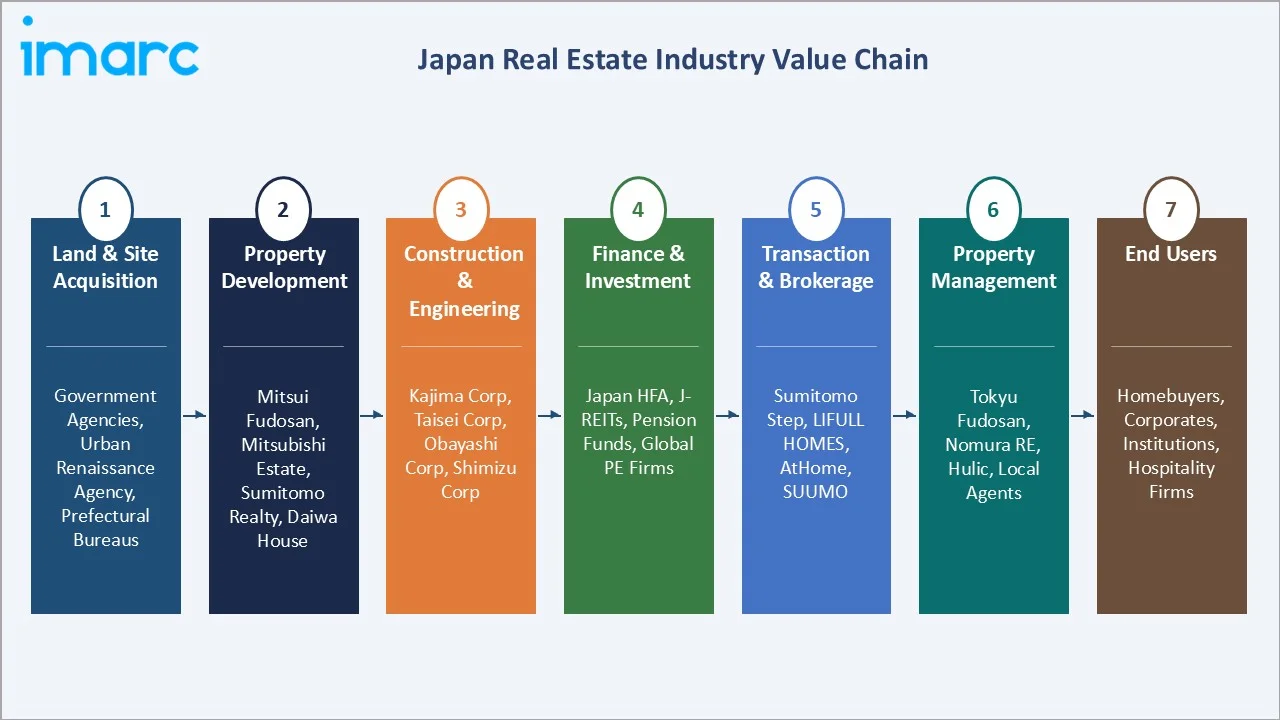

Industry Value Chain Analysis

The Japan real estate value chain spans land acquisition, property development, construction, financing, transaction execution, and long-term asset management, with each stage populated by specialized participants whose performance directly influences market efficiency, pricing accuracy, and investment returns.

|

Stage |

Key Participants / Examples |

|

Land & Site Acquisition |

Urban Renaissance Agency, prefectural land bureaus, government housing programs, and private landowners |

|

Property Development |

Mitsui Fudosan Co., Ltd., Mitsubishi Estate Co., Ltd., Sumitomo Realty & Development Co., Ltd., Nomura Real Estate Holdings, Inc., Sekisui House, Ltd. |

|

Construction & Engineering |

Kajima Corporation, Taisei Corporation, Obayashi Corporation, Shimizu Corporation, Takenaka Corporation |

|

Finance & Investment |

Japan Housing Finance Agency, domestic J-REITs, pension funds, global private equity, and sovereign wealth funds |

|

Transaction & Brokerage |

Traditional agents, Sumitomo Fudosan Step, ERA Japan, LIFULL HOME'S, At home, SUUMO (online platforms) |

|

Property Management |

Tokyu Fudosan Holdings, Nomura Real Estate Holdings, local managing agents, and FM firms |

|

End Users |

Individual homebuyers, corporate office tenants, logistics operators, hospitality groups, and institutional investors |

Technology Landscape in the Japan Real Estate Industry

PropTech and Digital Transaction Platforms

Major platforms, including LIFULL HOME'S and Athome, have integrated AI-powered recommendation engines, virtual reality property tours, and automated valuation models (AVMs) to enhance buyer decision-making. Government-backed digital property registration reforms introduced in 2024 are further removing friction from online transactions, enabling paperless closings and e-signature adoption across residential and small commercial deal workflows.

Smart Building and IoT Integration

Smart building certification schemes, including CASBEE and the BELS energy labeling program, are increasingly mandated by institutional landlords to attract premium tenants and maintain competitive rental positioning. The Toyota Woven City project exemplifies next-generation smart community design, incorporating hydrogen fuel cells, autonomous vehicle integration, and AI-driven urban management systems in a purpose-built real estate development.

Carbon Measurement and Green Technology

Gold Standard launched a pilot program to integrate digital Measurement, Reporting, and Verification (dMRV) solutions, aiming to improve the accuracy, transparency, and efficiency of monitoring carbon credits and sustainability impacts through digital technologies. Running until October 2026, the initiative tests how automated data collection and digital tools can streamline emissions reporting, reduce burdens on project developers, and support faster, more reliable impact verification.

AI-Driven Property Analytics and Valuation

Major developers and institutional investors are deploying machine learning-based market forecasting tools that analyze macroeconomic indicators and historical transaction records to generate granular sub-market valuation models. Real-time data exchange platforms in smart city environments, such as those deployed in Tokyo's Takeshiba district, are enabling property managers to optimize occupancy, maintenance scheduling, and tenant mix decisions using AI-derived analytics dashboards.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Property |

Residential |

36.8% |

2025 |

|

Business |

🔒 |

🔒 |

2025 |

|

Mode |

Offline |

81.2% |

2025 |

|

Region |

Kanto Region |

39.6% |

2025 |

By Mode

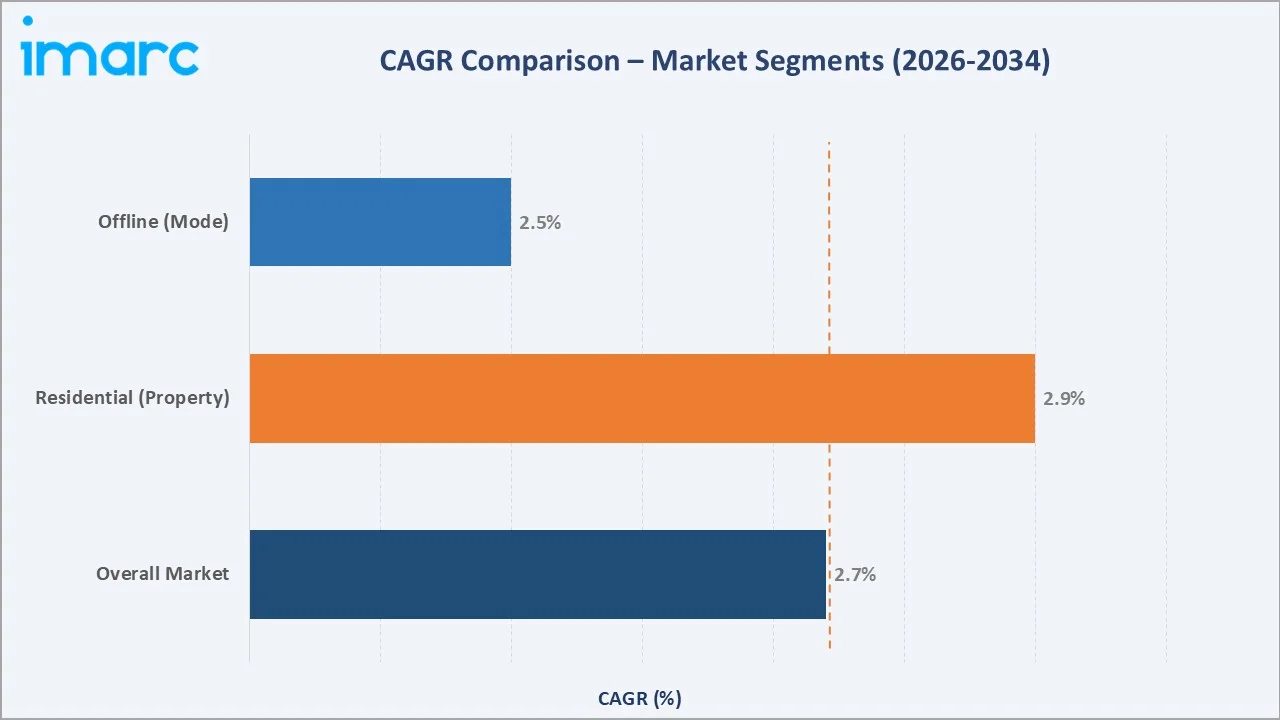

The offline mode dominates the Japan real estate market with a 81.2% share in 2025 (equivalent to approximately USD 364.2 Billion). Its dominance reflects the deeply embedded role of traditional real estate agencies, in-person site evaluations, and broker-facilitated negotiations in Japanese property culture, where trust, legal due diligence, and physical inspection remain essential elements of both residential and commercial transactions.

To access detailed market analysis, Request Sample

The online mode represents 18.8% of the market in 2025 and is the fastest-growing transaction channel, driven by PropTech platforms such as LIFULL HOME'S, Athome, and SUUMO that offer real-time listings, virtual tours, AI-based property matching, and digital contract workflows. Government digital transformation initiatives supporting e-signature adoption and paperless property registration are accelerating online channel penetration.

By Property

The residential segment holds the largest property share at 36.8% in 2025 (approximately USD 164.9 Billion). Its dominance is driven by sustained urban in-migration to major prefectures, government-backed first-home buyer incentives, historically low mortgage rates maintained under the Bank of Japan's accommodative policy, and accelerating demand for senior-adapted housing formats.

The commercial segment accounts for 28.9% of the market in 2025, underpinned by robust Grade A office demand in Tokyo, Osaka, and Nagoya, where vacancy rates for premium assets are at multi-year lows. The industrial segment represents 18.6%, benefiting from the rapid expansion of e-commerce and supply chain nearshoring trends, driving demand for Class A logistics and warehouse facilities.

Regional Market Insights

The Kanto region's market leadership at 39.6% in 2025 reflects Tokyo's status as Asia's premier commercial real estate market, where, in 2025, the average land price growth rate across all land uses in Tokyo rose to 7.7%, up from 6.0% in 2024. Record net office absorption volumes in Tokyo in early 2025 validate continued institutional appetite for high-spec, ESG-compliant commercial assets within the Japan real estate market trends landscape.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

Kanto |

39.6% |

Tokyo commercial hub; Grade A office demand; global institutional investment |

Seismic safety standards; green building mandates |

|

Kinki |

17.8% |

Osaka Expo legacy; Kyoto tourism; urban renewal programs |

Osaka casino resort regulatory framework |

|

Central/Chubu |

14.9% |

Automotive industry real estate; Nagoya logistics; Shinkansen corridor |

Industrial zone expansion policies |

|

Kyushu-Okinawa |

8.8% |

IT offshoring in Fukuoka; Okinawa tourism; decentralization programs |

Government decentralization incentives |

|

Tohoku |

6.5% |

Post-disaster reconstruction; renewable energy; Sendai downtown renewal |

Reconstruction special measures |

|

Chugoku |

5.1% |

Manufacturing clusters; port logistics, and industrial zone development |

Industrial expansion support policies |

|

Hokkaido |

4.7% |

Ski and resort real estate; inbound tourism; winter sports infrastructure |

Tourism zone development incentives |

|

Shikoku |

2.6% |

Agricultural real estate; rural revitalization; modest urban development |

Regional revitalization programs |

The Kinki region is the highest-growth regional market, with Osaka's commercial land values posting a 6.7% annual appreciation in 2025 per official surveys, driven by the Expo 2025 Osaka legacy investment pipeline and a sustained hotel and serviced apartment development boom. The Central/Chubu Region benefits from automotive and aerospace industry real estate demand, with Nagoya's all-grade vacancy falling to 2.3% in Q4 2025, its lowest level in four years.

Competitive Landscape

The Japan real estate market exhibits a moderately consolidated structure. The top five developers – Mitsui Fudosan Co., Ltd., Mitsubishi Estate Co., Ltd., Sumitomo Realty & Development Co., Ltd., Daiwa House Industry Co., Ltd., and Sekisui House, Ltd.– collectively account for a significant share of national real estate development revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Mitsui Fudosan Co., Ltd. |

Park Homes, Park Court |

Market Leader |

Japan's largest developer; diversified mixed-use portfolio; 140+ project pipeline |

|

Mitsubishi Estate Co., Ltd. |

The Parkhouse |

Market Leader |

Iconic Marunouchi district ownership; ESG-aligned commercial development; global footprint |

|

Sumitomo Realty & Development Co., Ltd. |

City House, La Tour, DEUX TOUR |

Major Player |

Strong domestic focus; large office leasing portfolio; active residential development |

|

Daiwa House Industry Co., Ltd. |

Premist, D-Room, Graca, Xevoσ, The Stately |

Major Player |

Leading logistics real estate developer; prefabricated housing; strong industrial segment presence |

|

Tokyu Fudosan Holdings. |

Branz |

Challenger |

Smart city leadership (Takeshiba); resort and lifestyle real estate; station-adjacent development |

|

Nomura Real Estate Holdings, Inc. |

Proud |

Challenger |

Premium residential brand; active urban redevelopment; strong Kanto market presence |

|

Sekisui House, Ltd. |

Shawood; Grande Maison |

Major Player |

Net-zero housing technology leader; large residential portfolio; growing global operations |

Key Company Profiles

Mitsui Fudosan Co., Ltd.

Mitsui Fudosan, headquartered in Tokyo and established in 1941, is Japan's largest real estate company by total assets and revenue. The firm operates a fully integrated real estate platform spanning office, retail, residential, logistics, and hotel segments, with a growing international presence in the United States, Europe, and Asia.

- Product Portfolio: Diversified mixed-use developments (Toyosu, LaLaport retail centers); residential condominiums; office towers; logistics parks; hotel assets.

- Recent Developments: In August 2025, Mitsui Fudosan announced plans to invest a cumulative investment of JPY 1.3 trillion (approximately USD 8.5 billion) across 78 facilities in Japan and overseas.

- Strategic Focus: Vertical integration across development, leasing, and management; expansion into senior housing and PropTech partnerships; growing international portfolio.

Mitsubishi Estate Co., Ltd.

MITSUBISHI ESTATE CO., LTD., founded in 1937 and headquartered in Tokyo, is renowned for its ownership and management of the Marunouchi district. The company is one of Japan's most prestigious commercial real estate owners, with a significant international portfolio spanning Europe, the US, and Southeast Asia.

- Product Portfolio: Marunouchi office portfolio; Torch Tower mixed-use development; international commercial assets; residential units.

- Recent Developments: Confirmed that the Torch Tower project, set to be Japan's tallest building upon completion in 2028, will include approximately 50 ultra-luxury rental apartments.

- Strategic Focus: Premium commercial real estate leadership; sustainable and ESG-certified building development; international expansion and luxury residential positioning.

Sumitomo Realty & Development Co., Ltd.

Sumitomo Realty & Development Co., Ltd., a member of the historic Sumitomo Group established in 1949, is heavily involved in office development and leasing, housing sales, and home renovations. The company maintains one of Tokyo's largest private office building portfolios, with consistently high occupancy rates in prime locations.

- Product Portfolio: Office buildings across central Tokyo; residential developments; home renovation services (Shinchiku Sokkurisan; Mumbai premium office buildings.

- Recent Developments: In June 2025, Sumitomo Realty's Mumbai project in Bandra Kurla Complex, featuring pillar-less wide-plate office floors, signed JPMorgan as an anchor tenant, commanding a 30–40% rental premium over local market rates.

- Strategic Focus: Domestic office leasing leadership; residential mid-to-high-end market focus; selective international expansion in high-growth emerging markets.

Daiwa House Industry Co., Ltd.

Daiwa House Industry Co., Ltd., established in 1955, is one of Japan's leading prefabricated and logistics real estate developers. The company is the dominant player in Japan's industrial and logistics real estate segment, with a fast-growing pipeline of Class A warehouse and distribution center developments.

- Product Portfolio: Prefabricated residential housing; D-Project Logistics; commercial and retail developments; overseas housing projects.

- Recent Developments: In 2025, Daiwa House DPL Vietnam Minh Quang (February 2025, Hung Yen Province, Vietnam, 37,500 sqm leasable area), an overseas facility.

- Strategic Focus: Logistics real estate leadership; net-zero carbon building programs; overseas market expansion in Australia, Vietnam, and the U.S.

Market Concentration Analysis

The Japan real estate market exhibits moderate concentration at the development and investment levels, with the top five integrated developers collectively commanding a significant share of national real estate activity in 2025. However, a broad ecosystem of regional specialists, construction firms, PropTech platforms, and smaller residential developers ensures substantial market fragmentation below the top tier, particularly in Hokkaido, Shikoku, Chugoku, and the Kyushu-Okinawa region.

Consolidation activity is gradually increasing, driven by scale economies in logistics real estate, ESG compliance investment requirements, and the capital intensity of smart city and mixed-use development formats. Between 2020 and 2025, several significant mergers and joint venture structures reshaped sub-segment competitive dynamics, particularly in the senior housing, industrial logistics, and PropTech platform segments.

Private equity interest in Japanese real estate assets remains elevated, targeting mid-tier commercial assets in secondary cities with value-add repositioning potential and senior housing development platforms with institutional-grade management infrastructure.

Investment & Growth Opportunities

Fastest Growing Segments

Senior housing and care-integrated residential formats, logistics and industrial real estate adjacent to major e-commerce corridors, and PropTech-enabled online transaction platforms represent the three highest-growth investment vectors through 2034. Online channels are expected to grow from 18.8% of market share in 2025 toward 28–32% by 2034, driven by generational change in buyer preferences and government digital transaction reforms.

Emerging Regional Opportunities

The Kinki Region, particularly Osaka and its surrounding metropolitan area, offers the strongest near-term growth potential among Japan's regional markets, supported by the 2025 Osaka Kansai Expo, which is expected to rise to 839 billion yen ($5.8 billion). The Hokkaido resort real estate segment is also emerging as a high-growth niche, driven by inbound luxury tourism and international second-home buyer demand from Hong Kong, Singapore, and Australia.

Venture and Institutional Investment Trends

- Key investment themes include senior housing development platforms, PropTech infrastructure (AI valuation tools, virtual tour technology, e-signature systems), green building retrofit programs, and Class A logistics park development in Kanto-Kinki corridor locations.

- Institutional capital from North American, European, and Southeast Asian sovereign wealth funds and pension managers continues to increase Japan allocation targets, attracted by the market's defensive characteristics, strong rule of law, and relatively attractive yields versus other Asia-Pacific gateway cities.

- Japan Housing Finance Agency programs supporting digitized mortgage applications and government-guaranteed home loan products are improving residential market access for first-time buyers, stimulating volume growth in the USD 391–448 billion market band established during the 2020–2025 historical period.

Future Market Outlook (2026-2034)

The Japan real estate market is positioned for sustained, broad-based growth through 2034. From a base of USD 448.31 Billion in 2025, the market is projected to reach USD 576.21 Billion by 2034, representing total incremental value creation of approximately USD 127.9 Billion over the forecast decade at a CAGR of 2.74%.

Regulatory evolution, particularly Japan's evolving green building certification standards, tightening seismic compliance requirements for older commercial stock, and digital property transaction reforms, will drive meaningful asset repositioning and redevelopment activity across the forecast period. Developers that establish certified, ESG-aligned product portfolios and technology-integrated property management platforms by 2027 are positioned to capture a disproportionate share of institutional procurement budgets as foreign capital inflows intensify.

Long-term, the Japan real estate market outlook is tied to three structural macro-themes: urbanization concentration in Kanto and Kinki (sustaining commercial and high-density residential demand), demographic aging (creating durable senior housing and healthcare real estate pipelines), and digital transformation (enabling PropTech-led transaction efficiency gains and smart building premium valuations).

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including residential and commercial property developers, institutional investors, real estate agents, PropTech platform executives, REIT portfolio managers, and government housing authority representatives across Japan's major prefectures.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, Ministry of Land, Infrastructure, Transport and Tourism (MLIT) data releases, Bank of Japan monetary policy statements, National Institute of Population and Social Security Research demographic projections, industry databases, trade publications, and publicly available J-REIT financial disclosures. Over 200 secondary sources were reviewed and cross-validated.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting methodologies, incorporating macroeconomic indicators, urbanization and population data, historical transaction volumes, segment-level growth rates, and validated against reported developer revenue trends. The base-case CAGR of 2.74% reflects consensus analyst estimates adjusted for Japan's structural demographic constraints and upside potential from foreign investment inflow acceleration.

Japan Real Estate Market Report:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Properties Covered | Residential, Commercial, Industrial, Land |

| Businesses Covered | Sales, Rental |

| Modes Covered | Online, Offline |

| Regions Covered | Kanto, Kinki, Central/ Chubu, Kyushu-Okinawa, Tohoku, Chugoku, Hokkaido, Shikoku |

| Companies Covered | Mitsui Fudosan Co., Ltd., Mitsubishi Estate Co., Ltd., Sumitomo Realty & Development Co., Ltd., Daiwa House Industry Co., Ltd., Tokyu Fudosan Holdings., Nomura Real Estate Holdings, Inc., Sekisui House, Ltd., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan real estate market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan real estate market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan real estate industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Real Estate Market Report

The Japan real estate market reached USD 448.31 Billion in 2025. It is projected to reach USD 576.21 Billion by 2034, growing at a CAGR of 2.74%.

The Japan real estate market is expected to grow at a CAGR of 2.74% during the forecast period from 2026-2034, supported by consistent demand from residential, commercial, and industrial property segments, accelerating foreign institutional investment, and government-led urban revitalization programs.

The Kanto region leads the market with a 39.6% revenue share in 2025, driven by Tokyo's status as Asia's premier commercial real estate market, a large base of Grade A commercial assets, and deep global institutional investment activity concentrated in central Tokyo and its surrounding metropolitan corridors.

Residential property is the largest segment with a 36.8% share in 2025, valued at approximately USD 164.9 Billion. Its dominance is driven by sustained urban in-migration, government homeownership incentives, historically low mortgage rates, and accelerating demand for senior-adapted residential formats across Japan's major metropolitan prefectures.

The offline mode commands the largest share at 81.2% in 2025, reflecting the entrenched role of traditional real estate agents and broker-facilitated transactions in Japanese property culture. However, the Online mode at 18.8% is growing rapidly, driven by PropTech platform adoption and government digital transaction reforms.

Key players include Mitsui Fudosan Co., Ltd., Mitsubishi Estate Co., Ltd., Sumitomo Realty & Development Co., Ltd., Daiwa House Industry Co., Ltd., Tokyu Fudosan Holdings, Nomura Real Estate Holdings, Inc., and Sekisui House, Ltd., among others.

PropTech platforms are increasingly reshaping Japan's traditionally broker-centric real estate market. Digital platforms, including LIFULL HOME'S, Athome, and SUUMO, are driving Online mode channel growth from 18.8% in 2025 toward an estimated 28–32% by 2034, as AI-powered matching, virtual tours, and paperless transaction capabilities attract younger buyer demographics.

Key challenges include the structural vacancy problem posed by approximately 9 million akiya (vacant homes), depressing regional land values, Japan's declining and aging population creating demand imbalances between urban and rural markets, and rising construction costs limiting new development viability in cost-sensitive residential segments outside core metropolitan areas.

Significant opportunities exist in senior housing and care-integrated residential platforms, Class A logistics real estate along the Kanto-Kinki e-commerce corridor, Osaka's post-Expo 2025 commercial and hospitality development pipeline, Hokkaido resort real estate, and PropTech infrastructure investment targeting Japan's rapidly growing online transaction channel.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)