Japan Robotics in Manufacturing Market Size, Share, Trends and Forecast by Component, Type, End User, and Region, 2026-2034

Japan Robotics in Manufacturing Market Size, Share, Trends & Forecast (2026-2034)

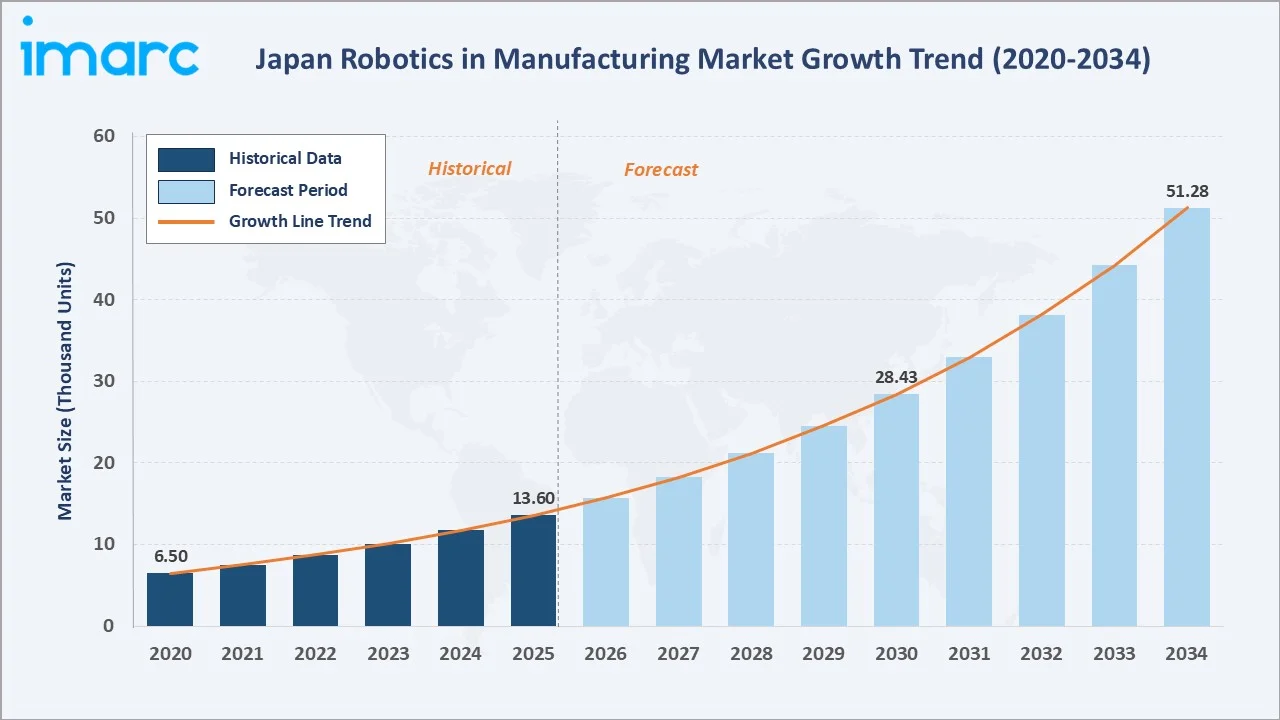

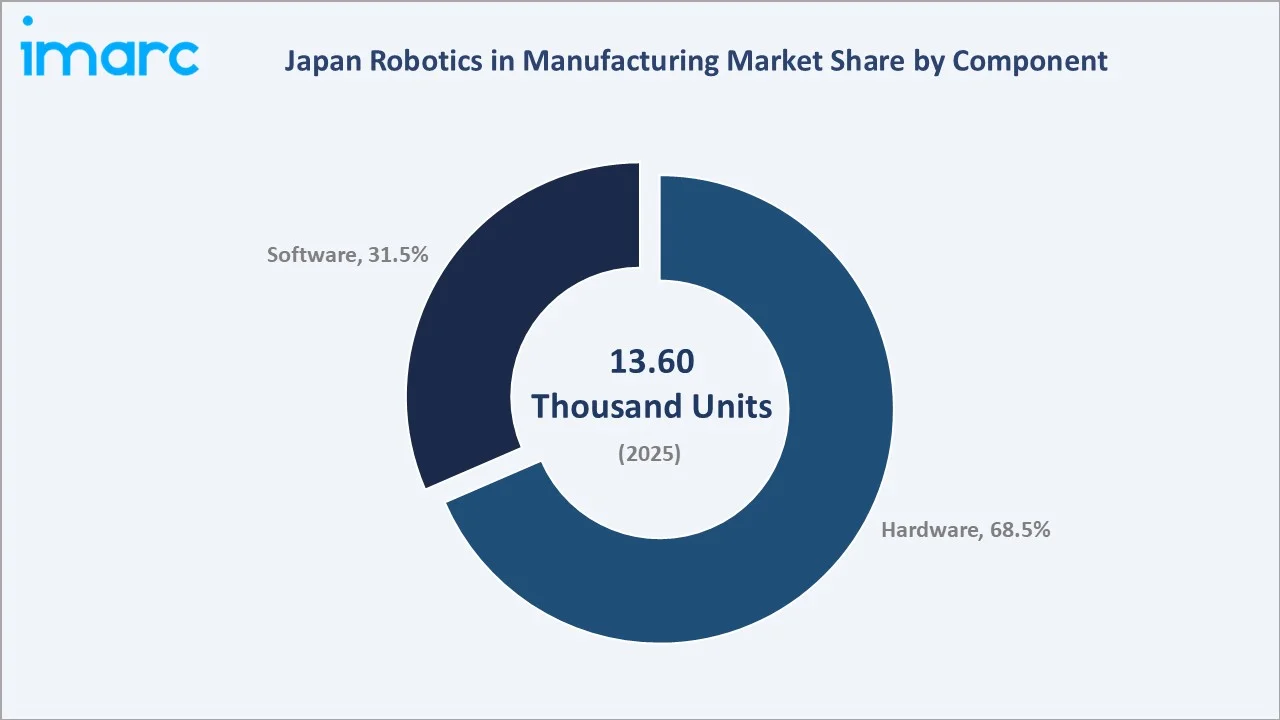

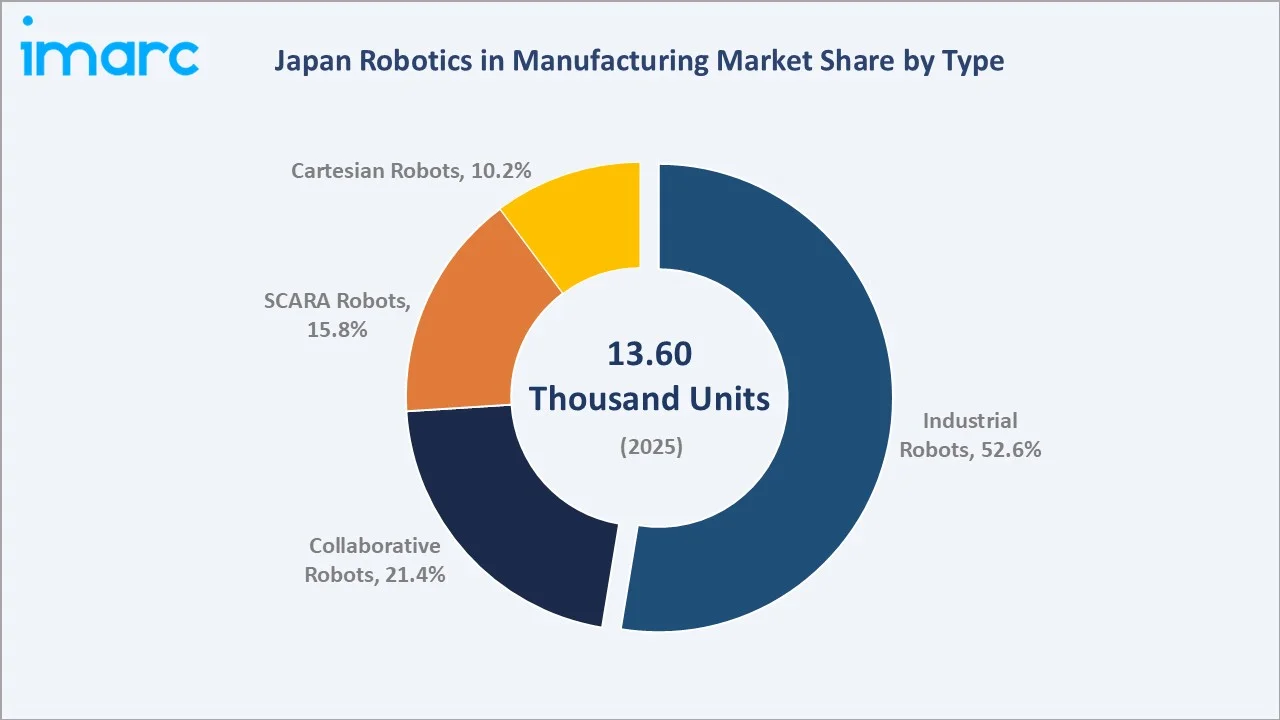

The Japan robotics in manufacturing market reached 13.60 Thousand Units in 2025 and is projected to reach 51.28 Thousand Units by 2034, growing at a CAGR of 15.89% during 2026-2034. Japan's structural demographic challenges, including a rapidly aging population and acute labor shortages, are the foundational drivers compelling manufacturers across automotive, electronics, food processing, and pharmaceuticals to accelerate robotic deployment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

13.60 Thousand Units |

|

Forecast Market Size (2034) |

51.28 Thousand Units |

|

CAGR (2026-2034) |

15.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

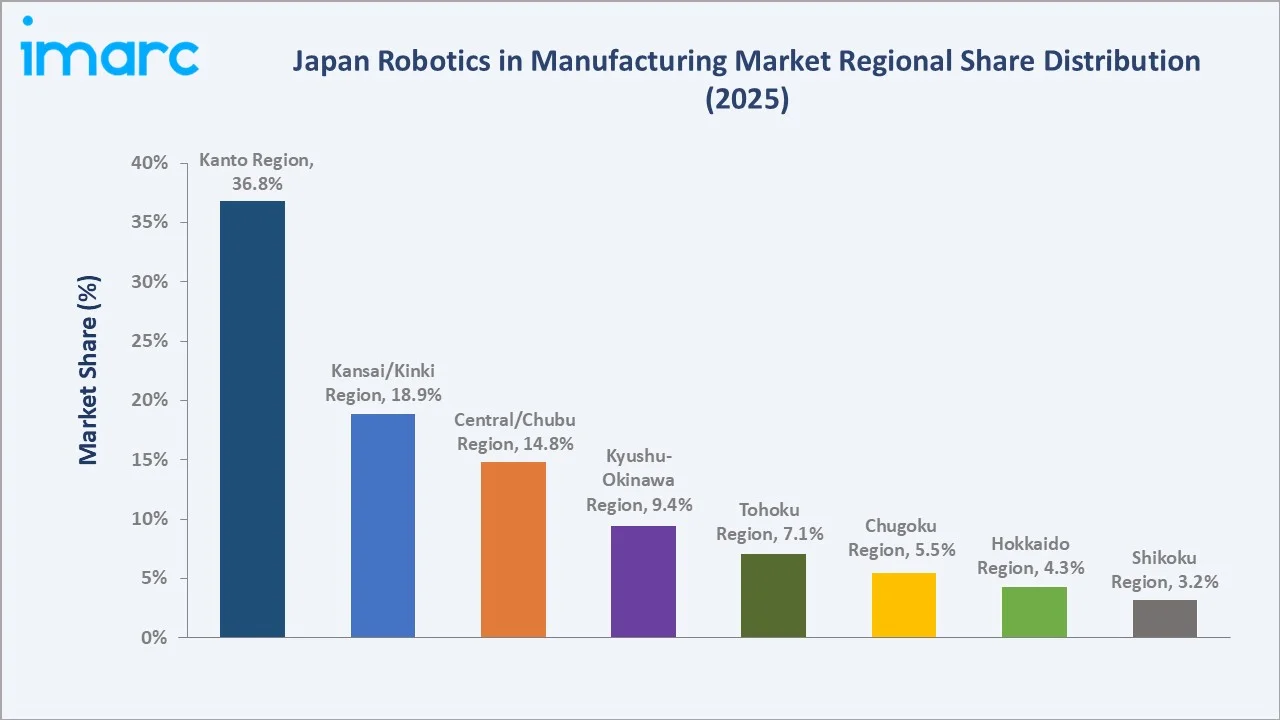

The Kanto region leads regionally, holding a 36.8% market share in 2025, anchored by Tokyo's dense concentration of automotive OEMs and tier-1 electronics manufacturers. Hardware commands a dominant 68.5% share of the component breakdown, while industrial robots retain the largest share among robot types at 52.6%.

To get more information on this market, Request Sample

Japan's robotics in the manufacturing market is underpinned by three structural forces: acute labor shortages driven by demographic aging, the Society 5.0 smart manufacturing initiative, and the government's strategic investments in robotics R&D through NEDO and METI. Each force independently raises demand density and technical sophistication, collectively sustaining an above-average CAGR through 2034.

Executive Summary

The Japan robotics in manufacturing market is experiencing accelerated expansion, driven by the convergence of demographic labor constraints, industrial digitalization under Society 5.0, and rising cobot adoption among small-to-medium enterprises (SMEs). The market reached 13.60 Thousand Units in 2025 and is forecast to reach 51.28 Thousand Units by 2034, growing at a CAGR of 15.89%.

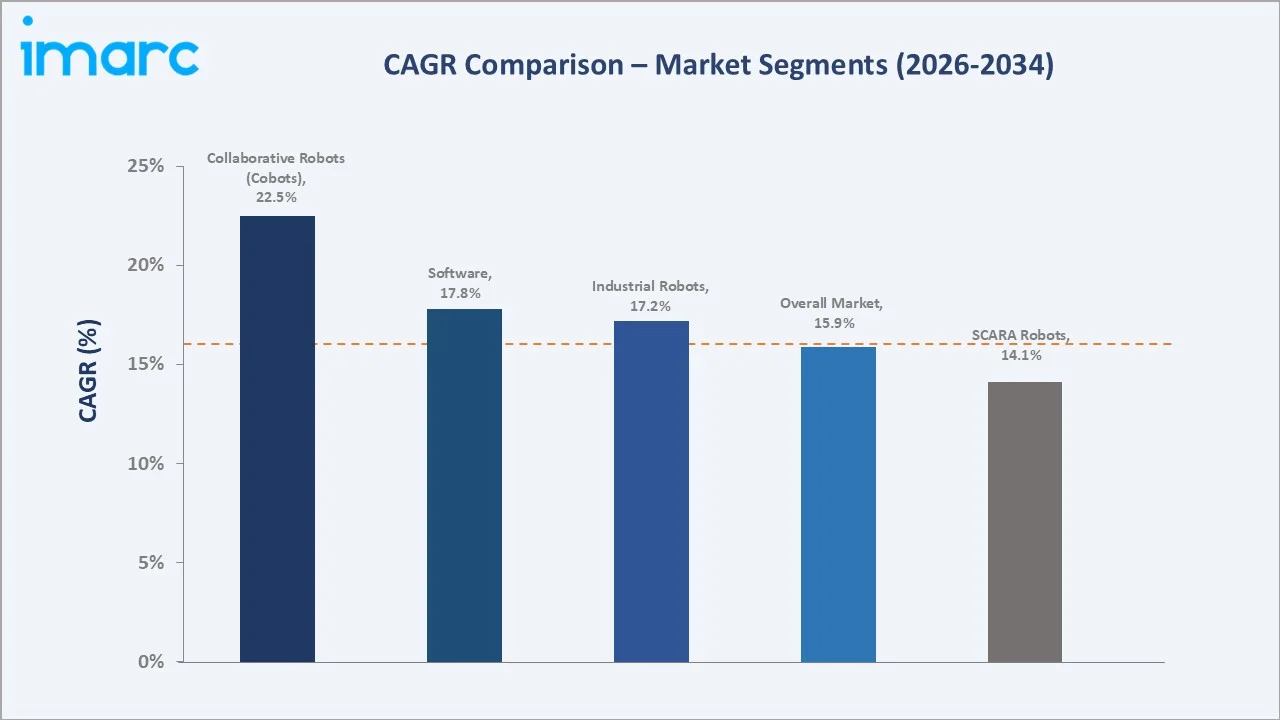

Hardware-based robot systems dominate the component segment with a 68.5% share in 2025, encompassing industrial robot arms, end effectors, servo motors, controllers, and sensing subsystems. Industrial robots lead the type segment at 52.6%, though collaborative robots (cobots) are growing fastest at an estimated 22.5% CAGR, driven by SME adoption for flexible assembly tasks where human-robot co-operation is operationally essential.

The Kanto region at 36.8% leads regionally, followed by Kansai/Kinki (18.9%), driven by Osaka's precision machinery and electronics manufacturing base. Leading global and domestic vendors, including FANUC CORPORATION, YASKAWA Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, and DENSO Corporation, dominate the market, supplemented by emerging cobot specialists.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Hardware – 68.5% share (2025) |

|

Fastest Growing Component |

Software – ~17.8% CAGR (2026-2034) |

|

Largest Robot Type |

Industrial Robots – 52.6% share (2025) |

|

Fastest Growing Type |

Collaborative Robots (Cobots) – ~22.5% CAGR (2026-2034) |

|

Leading Region |

Kanto Region – 36.8% share (2025) |

|

Top Companies |

FANUC CORPORATION, YASKAWA Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, and DENSO Corporation |

Key Analytical Observations Supporting the Above Data:

- Hardware products account for 68.5% of Japan's robotics in the manufacturing market in 2025. This dominance reflects the capital-intensive nature of robot cell installations, where articulated arms, SCARA units, delta robots, and their mechanical subsystems represent the primary CAPEX category for automotive OEMs and precision electronics manufacturers.

- Industrial robots at 52.6% (2025) remain dominant due to their six-axis multi-directional reach capability and compatibility with Japan's mature automotive production infrastructure. Japanese automotive OEMs mandate digital twin validation for all new robot cells, ensuring continued preference for proven industrial robot platforms.

- Collaborative robots' ~22.5% CAGR (2026-2034) is the fastest growing software segment as Japan's SMEs in electronics assembly, food processing, and pharmaceutical packaging adopt lightweight cobots that require no safety guarding infrastructure, reducing integration costs by 40–60% versus traditional industrial robot installations.

- The Kanto region's 36.8% share reflects Tokyo's concentration of Japan's largest automotive OEMs, Toyota's technical center, Honda's Sayama plant, and Nissan's Oppama facility, alongside a dense electronics manufacturing cluster in Kanagawa and Saitama prefectures.

Japan Robotics in Manufacturing Market Overview

Robotics in manufacturing encompasses industrial robots, collaborative robots, SCARA robots, and Cartesian robots deployed across automated production cells for tasks including welding, assembly, material handling, painting, inspection, and packaging. Japan's robotics market spans hardware components and software platforms, including robot operating systems, simulation tools, and manufacturing execution system (MES) integration middleware.

Macroeconomic drivers include Japan's working-age population expected to fall by 5.8% between 2020 and 2030, equivalent to an annual decline of 0.6%, government METI subsidies for smart factory investments under the Connected Industries initiative, and allocation of more than JPY 32 billion by Ministry of Economy, Trade and Industry (METI) under the fiscal 2024 supplementary budget to support AI robot R&D and strengthen Japan’s industrial ecosystem.

Market Dynamics

To evaluate market opportunities, Request Sample

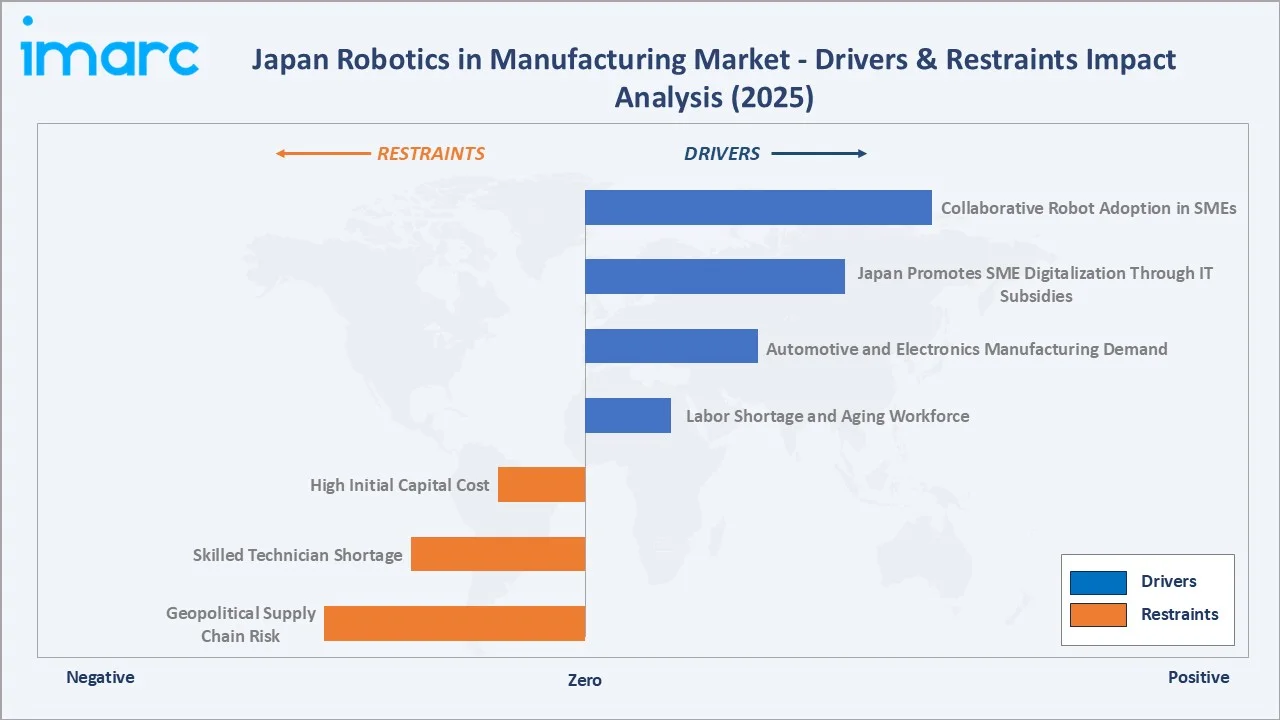

Market Drivers

- Labor Shortage and Aging Workforce: In 2024, Japan's working-age population (15–64 years) declined to just 59% of the total population, significantly below the global average of 65%, according to the Organisation for Economic Co-operation and Development (OECD). Moreover, according to the 2025 Manufacturing White Paper, over 60% of manufacturing establishments are facing workforce development challenges.

- Automotive and Electronics Manufacturing Demand: Japan's automotive sector, responsible for one-fifth of total manufacturing output, mandates robotic automation at every production stage from stamping to final assembly. Japan’s automotive industry installed around 13,000 industrial robots in 2024, marking an 11% increase from the previous year and the highest level recorded since 2020.

- Japan Promotes SME Digitalization Through IT Subsidies: Japan’s IT Introduction Subsidies support SMEs in adopting IT systems and digital tools to automate operations, improve workflow efficiency, and strengthen competitiveness. Under the scheme, eligible projects can run for up to 18 months, with grants covering 50–75% of eligible costs.

- Collaborative Robot Adoption in SMEs: Japan's 380,000 manufacturing SMEs represent an underpenetrated market, with cobot installations growing at ~22.5% annually as vendors introduce sub-JPY 2 million systems from Universal Robots and FANUC's CRX series that require no safety cage infrastructure, enabling deployment in existing facilities without major floor layout modifications.

Market Restraints

- High Initial Capital Cost: A complete industrial robot cell, including robot arm, end effector, safety fencing, programming, and integration, costs JPY 5–30 million for SME-scale deployments, representing 18–36 months of payback at current labor cost differentials. This capital requirement remains prohibitive for micro-enterprises with fewer than 10 production workers.

- Skilled Technician Shortage: Advanced robotic systems, particularly those incorporating vision guidance, force-torque sensing, and AI-based task adaptation, require specialized programming and maintenance expertise. Japan's certified robot engineer pool is estimated at 47,000 professionals as of 2024, creating integration bottlenecks and extended commissioning timelines.

- Geopolitical Supply Chain Risk: Semiconductor shortages in 2021–2023 disrupted robot production lines globally, with FANUC and Yaskawa both reporting 25–35% order backlogs at peak. Ongoing US-China technology restrictions on advanced semiconductors used in robot controllers create supply uncertainty for robot manufacturers sourcing components from Taiwan and South Korea.

Market Opportunities

- AI-Integrated Cobots for Flexible Manufacturing: Force-torque sensors and AI vision systems enabling compliant assembly operations are transforming cobot applicability in Japan's electronics and pharmaceutical sectors. FANUC's CRX Series demonstrates sub-5-minute safety certification for new tasks, reducing changeover costs and enabling SME adoption for small-batch, high-mix production.

- Expansion into Food and Pharmaceutical Manufacturing: Japan's food processing industry, which recorded a 3.9% rise in the value of food produced, reaching USD 174 billion in 2024, is shifting from manual to robotic handling for hygienic packaging, where stainless-steel SCARA and delta robots rated IP69K are replacing labor in chilled environments.

Market Challenges

- Workforce Retraining and Social Acceptance: Japan's manufacturing unions have historically opposed rapid automation at certain facilities, requiring manufacturers to negotiate deployment timelines and invest in worker retraining programs costing JPY 500,000–1,500,000 per employee for robot operation certifications.

- Interoperability Standards Fragmentation: Competing robot communication standards and vendor-proprietary protocols from Yaskawa's YRC1000 create integration complexity when combining robots from multiple vendors within a single production cell, increasing system integration costs and limiting plug-and-play adoption.

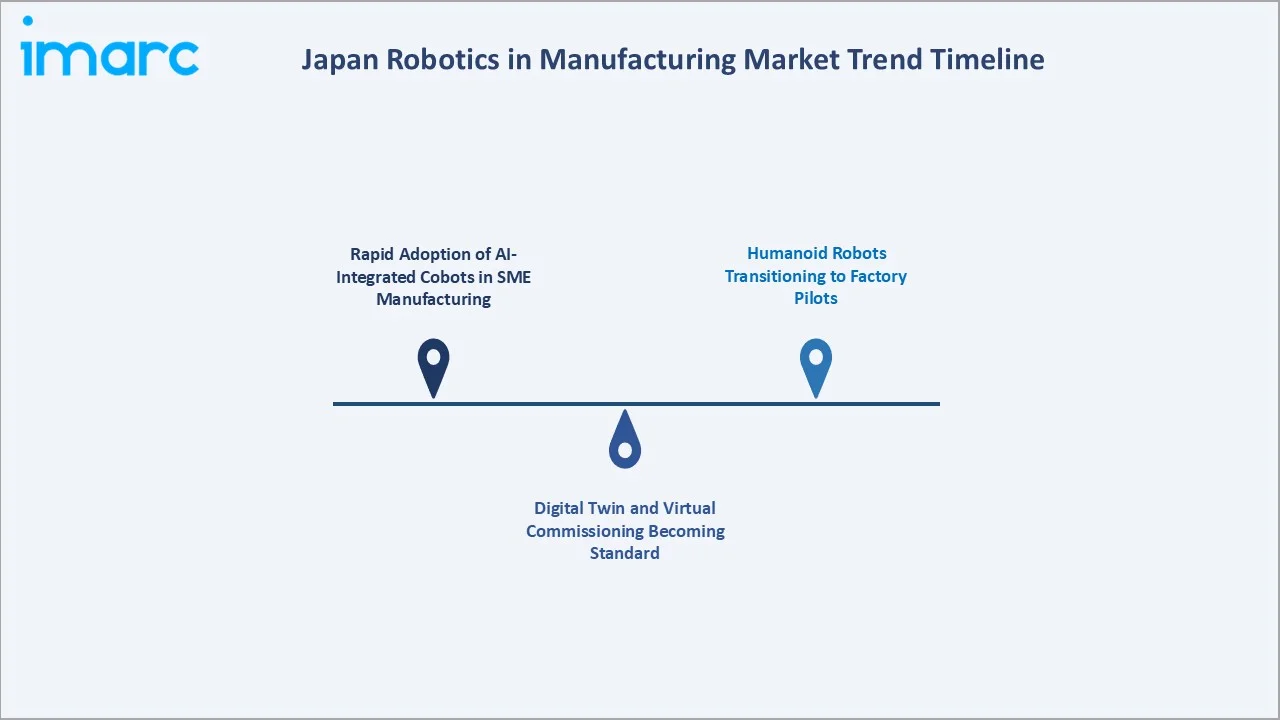

Emerging Market Trends

1. Rapid Adoption of AI-Integrated Cobots in SME Manufacturing

One-third of Japanese companies are already using or considering AI-powered robots, with transportation equipment manufacturers leading adoption. The trend reflects Japan’s push to address labor shortages and strengthen its robotics competitiveness, though only 4% of surveyed firms currently use AI robots. Kawasaki's duAro dual-arm SCARA collaborative robot and Universal Robots' UR series have achieved penetration in more than 12,000 Japanese SME facilities as of 2025, predominantly in electronics assembly and consumer goods packaging, where flexible, safe human-robot collaboration is operationally critical.

2. Digital Twin and Virtual Commissioning Becoming Standard

In March 2026, Mitsubishi Electric Corporation developed edge digital twin technology with RWTH Aachen University to correct CNC machine-tool errors in real time, reducing machining errors by up to 50%. The technology improves productivity by lowering defective parts and stabilizing surface quality, while also helping reduce environmental impact in precision manufacturing.

3. Humanoid Robots Transitioning to Factory Pilots

In March 2025, Toyota Research Institute highlighted its humanoid robotics work under the Global AI Accelerator (GAIA) program, focusing on robots powered by Large Behavior Models. TRI said these systems can learn from demonstrations and combine sensor inputs to handle new situations without hand-coded instructions. Toyota positioned the technology as a way to amplify human capabilities and support workers.

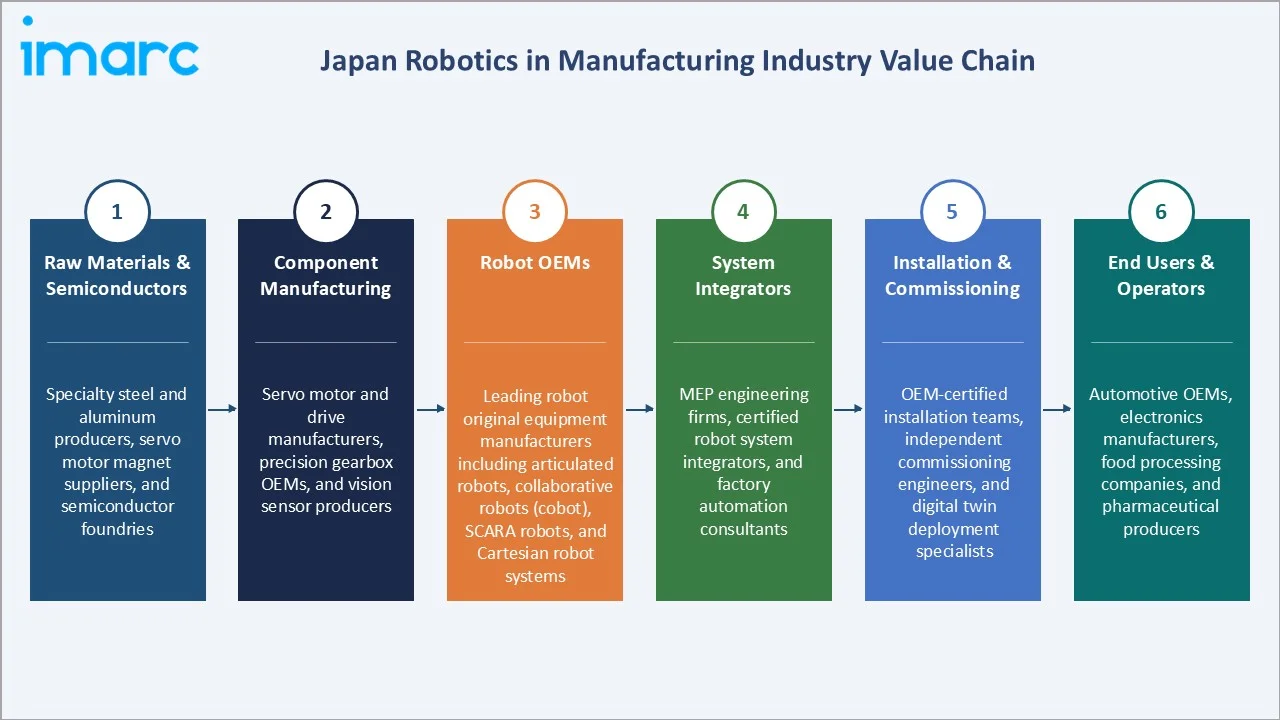

Industry Value Chain Analysis

Japan's robotics in the manufacturing value chain spans raw material and semiconductor supply through end-user factory deployment, with each stage occupied by specialized manufacturers, integrators, and service providers whose performance directly influences robot performance, delivery lead times, and total cost of ownership.

|

Stage |

Key Players / Examples |

|

Raw Materials & Semiconductors |

Specialty steel and aluminum producers, servo motor magnet suppliers, and semiconductor foundries |

|

Component Manufacturing |

Servo motor and drive manufacturers, precision gearbox OEMs, and vision sensor producers |

|

Robot OEMs |

Leading robot original equipment manufacturers including articulated robots, collaborative robots (cobot), SCARA robots, and Cartesian robot systems |

|

System Integrators |

MEP engineering firms, certified robot system integrators, and factory automation consultants |

|

Installation & Commissioning |

OEM-certified installation teams, independent commissioning engineers, and digital twin deployment specialists |

|

End Users & Operators |

Automotive OEMs, electronics manufacturers, food processing companies, and pharmaceutical producers |

Technology Landscape in the Japan Robotics in Manufacturing Industry

Articulated Industrial Robots – Six-Axis Platforms

Six-axis articulated robots form the backbone of Japan's automotive and electronics manufacturing automation. These robots handle payloads from 3 kg to 1,500 kg with positional repeatability of ±0.01–0.02 mm, making them the standard solution for welding, painting, and precision assembly applications requiring multi-directional reach across complex part geometries.

Collaborative Robots (Cobots) – Force-Limited Safety Platforms

Japan's cobot market is growing at ~22.5% annually. Force-torque sensors integrated into cobot wrist designs enable compliant assembly operations without safety guarding, enabling deployment in existing facilities with minimal infrastructure modification. Sub-5-minute task reprogramming through tablet-based teach pendants is accelerating adoption in Japan's high-mix electronics assembly and consumer goods packaging operations.

SCARA and Cartesian Robots – Precision Assembly Platforms

SCARA robots from Epson, Mitsubishi Electric Corporation, and DENSO Corporation dominate Japan's electronics component assembly, PCB handling, and pharmaceutical dispensing segments, offering throughputs of 120–180 picks per minute with ±0.005 mm repeatability. Cartesian gantry robots serve material handling, part transfer, and palletizing applications requiring a large workspace, linear-axis precision at a lower total system cost than articulated alternatives.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

68.5% |

2025 |

|

Type |

Industrial Robots |

52.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

36.8% |

2025 |

By Component

The hardware segment dominates with a 68.5% share in 2025. This segment encompasses all physical robot systems, including articulated arms, delta/parallel robots, end effectors, servo drives, robot controllers, and safety systems.

To access detailed market analysis, Request Sample

Hardware's dominance reflects the capital-intensive robot cell procurement cycle underway across Japan's automotive and electronics manufacturing expansion programs, where new model launches require complete robot cell upgrades every 4–7 years.

Software represents 31.5% of the market, encompassing robot operating systems, simulation and offline programming tools, MES integration middleware, vision software, AI-powered task planning platforms, and robot fleet management systems. The software segment is growing fastest (~17.8% CAGR) as hyperscale automotive manufacturers shift toward continuous software-defined robot reconfiguration that enables production line changeovers within hours rather than days.

By Type

Industrial robots command a 52.6% share in 2025. This segment includes six-axis articulated robots, the workhorse of Japan's automotive assembly and welding operations. Industrial robots' dominance reflects Japan's mature automotive manufacturing base, where six-axis articulated platforms are irreplaceable for arc welding, spot welding, painting, and heavy-payload handling tasks.

Collaborative robots represent 21.4% share (2025), growing fastest as Japan's SME manufacturers adopt force-limited cobots for flexible assembly, kitting, and machine tending operations where human-robot co-existence is operationally necessary. SCARA robots at 15.8% serve Japan's precision electronics assembly and pharmaceutical dispensing segments.

Regional Market Insights

The Kanto region's market leadership (36.8%, 2025) reflects Tokyo's established status as Japan's primary industrial automation hub, anchored by automotive OEM headquarters, precision electronics manufacturing in Kanagawa and Saitama, and the concentration of tier-1 robot OEM sales and service networks.

The Kansai/Kinki region at 18.9% represents Japan's second-largest robotics market, driven by Osaka's deep precision machinery manufacturing base and the Kyoto-Osaka-Kobe corridor's pharmaceutical and electronics industries.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

36.8% |

Automotive OEM concentration, precision electronics manufacturing in Kanagawa/Saitama, tier-1 robot OEM headquarters, and strong government smart factory subsidy uptake |

|

Kansai/Kinki Region |

18.9% |

Osaka precision machinery, pharmaceutical automation in Kyoto, and a strong research robotics program |

|

Central/Chubu Region |

14.8% |

Toyota City automotive cluster, adjacent tier-1 supplier base, and DENSO Corporation headquarters |

|

Kyushu-Okinawa Region |

9.4% |

Semiconductor fabs, expanding automotive tier-2 suppliers, and growing food processing automation in Kyushu's agri-industrial corridor |

|

Tohoku Region |

7.1% |

Auto parts manufacturing reconstruction, an emerging electronics cluster in Miyagi, and government robotics subsidies for regional economic development |

|

Chugoku Region |

5.5% |

Mazda automotive manufacturing in Hiroshima, precision machinery in Okayama, and shipbuilding automation |

|

Hokkaido Region |

4.3% |

Expanding food processing automation for dairy, seafood, and vegetable packaging |

|

Shikoku Region |

3.2% |

Chemical and paper manufacturing automation, expanding medical device production in Tokushima, and SME cobot adoption in local manufacturing clusters |

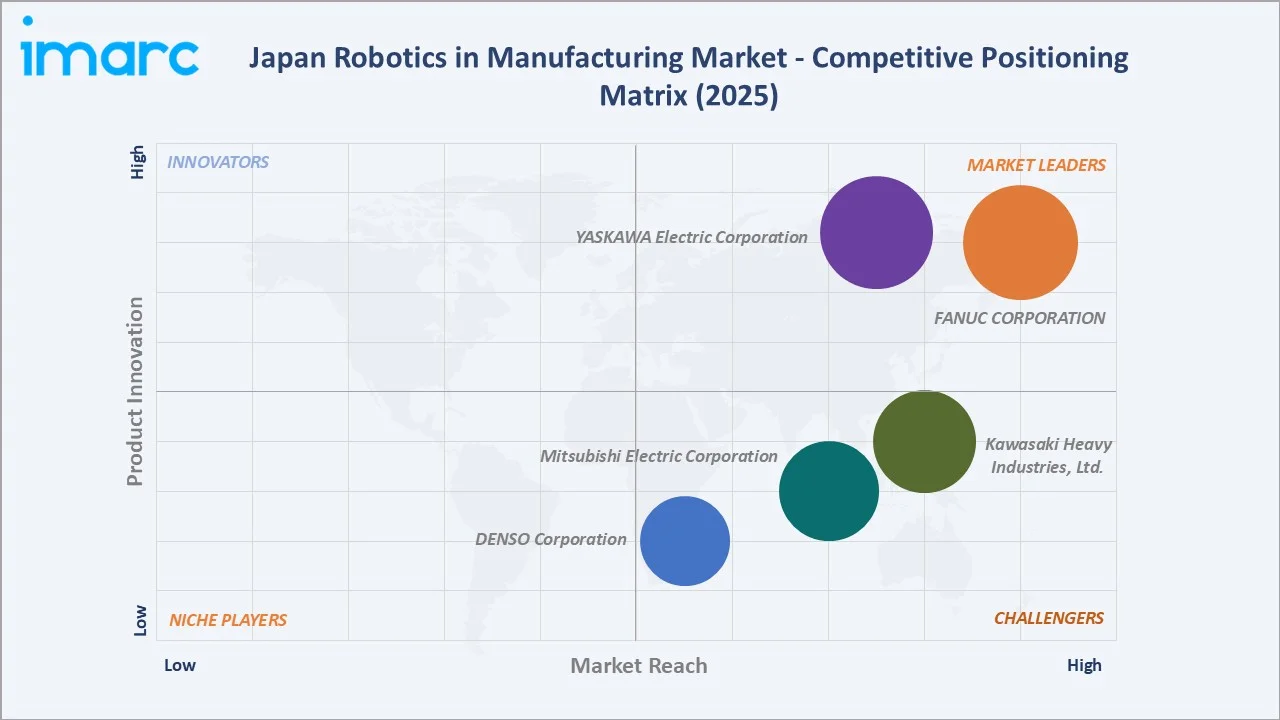

Competitive Landscape

Japan's robotics in the manufacturing market exhibits high concentration among domestic OEMs, with top players collectively holding approximately 58–65% of domestic market unit volume in 2025.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

FANUC CORPORATION |

Collaborative Robot CRX series, Collaborative Robot CR, SCARA Robot, Delta Robot, Among Others |

Market Leader |

Broad industrial and collaborative robot portfolio; strong presence across automotive and electronics manufacturing verticals |

|

YASKAWA Electric Corporation |

Arc Welding Robot, Spot Welding Robot, Handling/Assembling Robot, Collaborative Robot, Biomedical Robot, Palletizing Robot, Among Others |

Market Leader |

Comprehensive motion control and industrial automation expertise; wide payload range addressing diverse manufacturing applications |

|

Kawasaki Heavy Industries, Ltd. |

Small-medium Payload Robots, Welding - Spot Robots, Painting Robots, Palletizing Robots, Clean Robots, Medical and Pharmaceutical Robots, and Pick & Place Robots |

Strong Challenger |

Versatile robot applications across heavy industrial and precision manufacturing sectors; established presence in regulated industries |

|

Mitsubishi Electric Corporation |

MELFA FR Series, MELFA CR Series, MELFA ASSISTA, RV-FR Series, RV-CR Series, RH-FRH Series, RH-CRH Series, MELFA FR PLUS |

Strong Challenger |

Integrated factory automation ecosystem spanning articulated and SCARA robots; strong SME and large enterprise manufacturing customer base |

|

DENSO Corporation |

4-axis (SCARA) Robots, 5- and 6-axis Robots, Collaborative Robots, Pharma/Medical Robots, Integrated Robots, Built-in Robots |

Challenger |

High-speed precision assembly and compact robot expertise; deep automotive tier-1 supply chain integration |

International challengers, including ABB, KUKA, and Universal Robots, compete primarily in the cobot and collaborative automation segment, where Japanese incumbents have been slower to deploy entry-level platforms.

Key Company Profiles

FANUC CORPORATION

FANUC CORPORATION is one of Japan's largest industrial robot manufacturers and the global leader in CNC systems. The company offers a broad robot portfolio covering compact collaborative models, high-payload industrial robots, and heavy-duty automation systems, supported by a large global installed base across diverse end-use industries.

- Product Portfolio: Collaborative Robot CRX series, Collaborative Robot CR, SCARA Robot, Delta Robot, Small/Medium Size Robot, Large Size Robot, Large-size Palletizing Robot, Arc Welding Robot, and Paint Robot.

- Recent Developments: In May 2026, FANUC CORPORATION announced a strategic collaboration with Google to enhance its Physical AI Robot System using Google Cloud technologies, including Gemini Enterprise and Intrinsic’s Flowstate platform. The system enables AI agents to understand natural-language instructions, recognize objects, and autonomously operate FANUC robots.

- Strategic Focus: AI-powered cobot expansion; ROBOGUIDE digital twin SaaS growth; Green Factory initiative targeting 30% energy consumption reduction per robot cycle.

YASKAWA Electric Corporation

YASKAWA Electric Corporation is one of the global leaders in motion control and industrial automation. The company offers advanced robotics and automation solutions used across manufacturing, automotive, electronics, logistics, and other industrial sectors.

- Product Portfolio: Arc welding robot, spot welding robot, handling/assembling robot, collaborative robot, biomedical robot, palletizing robot, press handling robot, sealing/cutting/laser machining robot, deburring robot, painting robot, glass substrates transfer robot, and semiconductor wafer transfer robot.

- Recent Developments: In May 2024, YASKAWA Electric Corporation signed an MOU with Astellas Pharma to explore a cell therapy platform using the Maholo dual-arm robot. The partnership aims to automate and stabilize cell therapy manufacturing, shorten R&D timelines, and support commercialization.

- Strategic Focus: i3-Mechatronics platform subscription revenue growth; HC series expansion in SME manufacturing; North Asia cross-border robot service network development.

Market Concentration Analysis

Japan's robotics in manufacturing market exhibits high concentration, with the top five domestic OEMs holding approximately 58–65% of domestic unit volume in 2025. Below the top tier, a competitive mid-market of 10–15 specialized vendors serves precision electronics, food processing, and semiconductor logistics segments with application-specific platforms.

Consolidation is occurring primarily through capability expansion in collaborative and AI-integrated robotics. This incumbent-versus-specialist dynamic is driving price compression in the entry-level cobot segment while accelerating software and services revenue growth as OEMs seek to extend customer lifetime value beyond initial hardware sales.

Investment & Growth Opportunities

Fastest Growing Segments

Collaborative robots (~22.5% CAGR), AI-integrated robot software platforms (~20% CAGR), SCARA robots for pharmaceutical automation (~16% CAGR), and humanoid robot development (~30%+ CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined incremental market opportunity exceeding 25,000 additional units annually in Japan by 2030.

Emerging Market Expansion

Kyushu's semiconductor manufacturing cluster represents an incremental 2,000+ industrial robot installation opportunity by 2030, beyond traditional automotive and electronics centers. Entry strategies for robot vendors targeting Kyushu include local application engineering teams specializing in cleanroom semiconductor logistics robots and proximity to TSMC's supplier qualification processes.

Venture and Institutional Investment Trends

- Japan’s New Robot Strategy aims to position the country as the world’s leading robot innovation hub, with continued focus on key sectors such as manufacturing, nursing and medical care, and agriculture.

- Robot-as-a-Service (RaaS) business models are emerging, where system integrators provide turnkey robotic cell operation on a per-part-produced fee basis, eliminating CAPEX barriers for SMEs. This OpEx model potentially commands 40–60% lifetime revenue premiums over traditional hardware sales, creating new investor-attractive recurring revenue streams within Japan's robotics ecosystem.

Future Market Outlook (2026-2034)

Japan's robotics in manufacturing market is positioned for sustained, high-growth expansion through 2034. From a base of 13.60 Thousand Units in 2025, the market is projected to reach 51.28 Thousand Units by 2034, representing total incremental unit growth of 37.68 Thousand Units at a CAGR of 15.89%. This growth is underpinned by Japan's demographic imperative, the government's Society 5.0 commitment, and the irreversible shift toward software-defined, AI-integrated manufacturing systems.

The technology transition from traditional industrial robots to AI-augmented collaborative systems will define the market's composition by 2034. Industrial robots' share is projected to decline from 52.6% in 2025 to approximately 43% by 2034 as cobots grow from 21.4% to 32%+. This technology shift creates hardware replacement demand opportunities for incumbent OEMs and software revenue growth opportunities for AI platform developers building on top of Japan's installed robot base of 500,000+ units.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including robot OEM executives, manufacturing automation engineers, system integrators, industrial equipment distributors, and institutional investors across Japan, Germany, and the United States. Expert input validated market sizing, technology adoption rates, and regional deployment trends.

Secondary Research

Secondary research encompassed vendor annual reports, International Federation of Robotics (IFR) World Robotics reports, METI smart factory survey data, NEDO robotics technology roadmaps, Japan Robot Association (JARA) industry statistics, and industry publications (Robot Report, Robotics Business Review, Asia Robot Review).

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating robot installation data (units/year), average selling price trends, software attachment rates, and vendor revenue disclosures. A base-case CAGR of 15.89% reflects consensus estimates validated against Japan Robot Association installation data, METI subsidy uptake statistics, and vendor order backlog disclosures from FY2020 to FY2025.

Japan Robotics in Manufacturing Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Units |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software |

| Types Covered | Industrial Robots, Collaborative Robots (Cobots), SCARA Robots, Cartesian Robots |

| End Users Covered | Automotive, Electronics, Aerospace, Food and Beverage |

| Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Comapnies Covered | FANUC CORPORATION, YASKAWA Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, DENSO Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan robotics in manufacturing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan robotics in manufacturing market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan robotics in manufacturing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Robotics in Manufacturing Market Report

The Japan robotics in manufacturing market reached 13.60 Thousand Units in 2025 and is projected to reach 51.28 Thousand Units by 2034.

The market is expected to grow at a CAGR of 15.89% during 2026-2034, driven by labor shortages, Society 5.0 digitalization, and cobot adoption among SMEs.

The Kanto Region leads with a 36.8% share in 2025, anchored by Tokyo's automotive OEM concentration and Kanagawa's precision electronics manufacturing cluster.

Hardware dominates with a 68.5% share in 2025, encompassing articulated robot arms, SCARA units, controllers, servo drives, and safety systems.

Industrial robots hold the largest share at 52.6%, driven by Japan's mature automotive and electronics manufacturing base, deploying six-axis articulated platforms for welding, painting, and assembly.

Some of the key players in the market include FANUC CORPORATION, YASKAWA Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, and DENSO Corporation.

Cobots are growing at ~22.5% CAGR because Japan's SME manufacturers are adopting force-limited collaborative robots for flexible assembly and machine tending that require no safety cage infrastructure, reducing total installation cost by 40–60%.

Key challenges include high initial capital costs, skilled technician shortages, geopolitical supply chain risks affecting semiconductor availability, and legacy line integration complexity.

AI-integrated cobots, robot simulation software, humanoid robot development, RaaS business models, and Kyushu semiconductor automation represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade