Japan Semiconductor Market Size, Share, Trends and Forecast by Components, Material Used, End User, and Region, 2026-2034

Japan Semiconductor Market Summary:

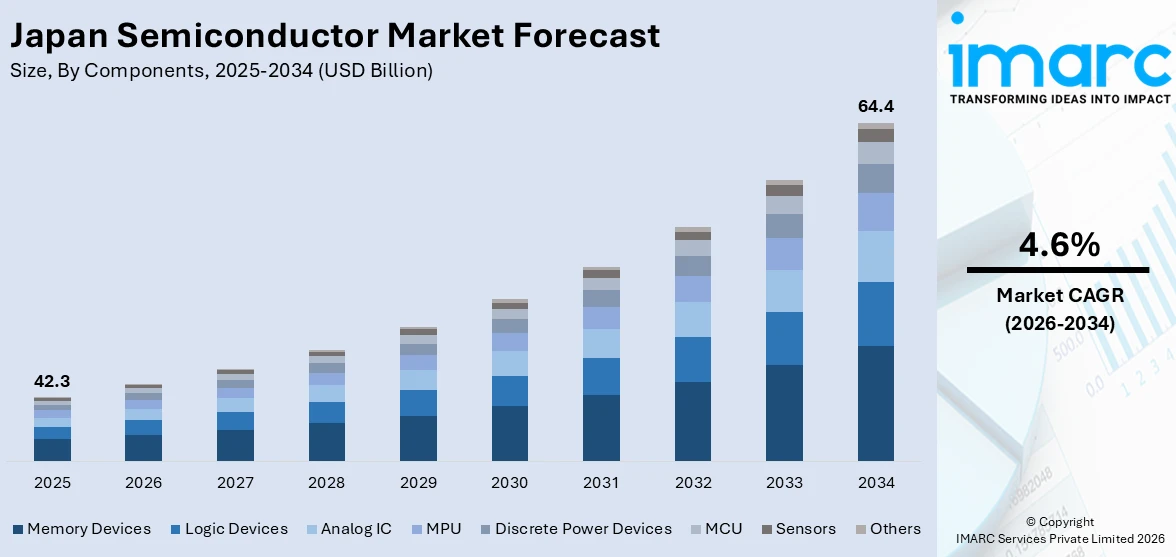

The Japan semiconductor market size was valued at USD 42.3 Billion in 2025 and is projected to reach USD 64.4 Billion by 2034, growing at a compound annual growth rate of 4.6% from 2026-2034.

The Japan semiconductor industry is undergoing a profound strategic transformation, driven by rising demand across artificial intelligence (AI) applications, electric mobility solutions, and next-generation communication networks. Sustained investments in advanced chip design, fabrication capabilities, and compound semiconductor materials, alongside robust government-backed supply chain resilience programs, are collectively reshaping the technology landscape. Additionally, global supply chain diversification is boosting semiconductor investments in Japan.

Key Takeaways and Insights:

- By Components: Memory devices dominate the market with a share of 31.8% in 2025, driven by accelerating demand for high-capacity storage solutions across AI workloads, expanding data center infrastructure, and the proliferation of advanced consumer electronics, which collectively reinforce Japan's strategic focus on strengthening domestic memory manufacturing capacity.

- By Material Used: Silicon carbide leads the market with a share of 28.6% in 2025, owing to its exceptional thermal conductivity and high-voltage resistance, which render it indispensable for electric vehicle (EV) powertrains, industrial automation systems, renewable energy infrastructure, and energy-efficient power conversion applications, thereby driving widespread adoption across Japan's semiconductor technology landscape.

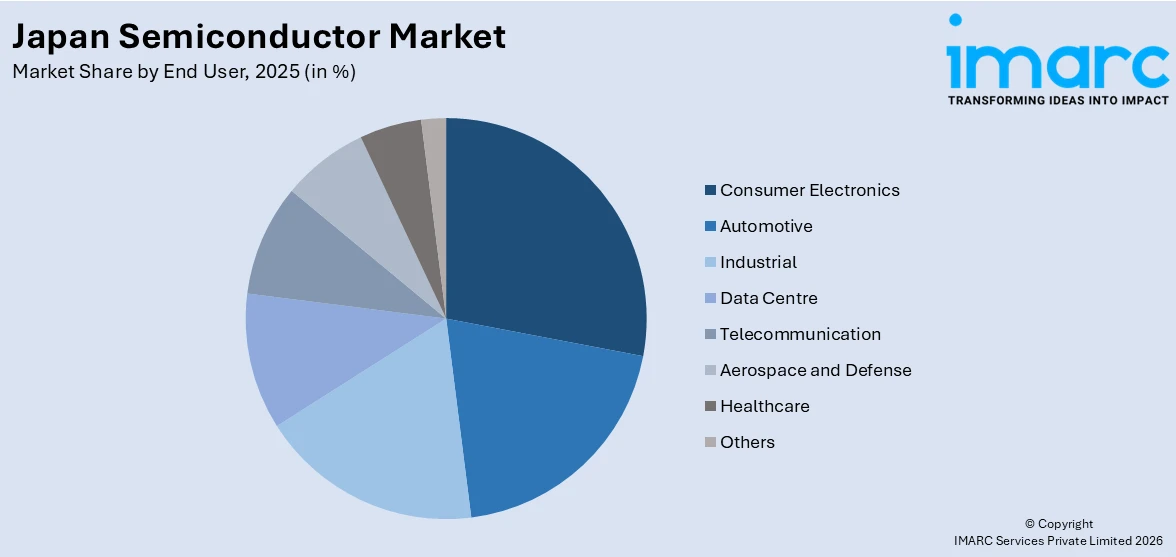

- By End User: Consumer electronics represent the largest segment with a market share of 26.9% in 2025, reflecting the sustained consumer demand for smartphones, wearable technology, gaming consoles, and connected home devices, which require increasingly sophisticated semiconductor components to deliver enhanced performance, energy efficiency, and seamless connectivity in Japan's technology-driven marketplace.

- By Region: Kanto Region comprises the largest region with 34.7% share in 2025, driven by the deep concentration of Japan's leading technology firms and research institutions across the Tokyo metropolitan area, enabling continuous innovation in AI-powered semiconductors, advanced integrated circuit design, and precision semiconductor equipment manufacturing.

- Key Players: Leading companies in the Japan semiconductor market drive innovation through advanced chip design, compound material research and development (R&D), and strategic manufacturing alliances. Their targeted investments in domestic fabrication capacity and supply chain resilience bolster Japan's competitiveness across automotive, AI, and consumer electronics segments.

To get more information on this market Request Sample

The Japan semiconductor market is experiencing robust expansion, driven by macroeconomic, technological, and policy forces reshaping the industry's competitive landscape. Japan's strategic specialization across semiconductor equipment, advanced materials, and power devices is gaining renewed momentum. The government's commitment to revitalizing domestic chip manufacturing has catalyzed significant capital inflows. Data provided by a subcommittee of Japan's Ministry of Finance's Fiscal System Council indicated that Japan planned to invest JPY 3.9 Trillion (around USD 25.7 Billion) in the semiconductor industry from 2025 to 2027, which represented 0.71% of its GDP. The sustained government support is attracting leading international chip manufacturers to establish operations in Japan, reinforcing supply chain security and technological self-sufficiency. The growing deployment of EVs, industrial automation systems, and AI-powered applications is simultaneously driving demand for sophisticated semiconductors across diverse end user segments.

Japan Semiconductor Market Trends:

Rise of AI-Driven Semiconductor Demand

The Japan semiconductor sector is increasingly shaped by the rapid proliferation of AI applications across data center infrastructure, industrial robotics, and autonomous vehicle systems. As AI inference and training workloads intensify, demand for high-bandwidth memory solutions, specialized logic devices, and energy-efficient processor architectures continues to accelerate. Japan's established expertise in precision manufacturing, advanced compound materials, and optical sensing technologies positions it as a critical supplier in the global AI chip ecosystem, reinforcing the country's strategic relevance in next-generation computing platforms.

Accelerating Integration of Silicon Carbide in Power Electronics

Silicon carbide is emerging as a defining material in Japan's semiconductor landscape, driven by the accelerating electrification of transportation and the expansion of industrial power systems. Its superior thermal conductivity, high breakdown voltage, and low switching losses make it the material of choice for power conversion in EV inverters, renewable energy systems, and high-voltage industrial applications. Japan's manufacturers are channeling substantial resources into expanding silicon carbide production capabilities, positioning the country to capture growing global demand for next-generation power electronics.

Expansion of Government-Led Semiconductor Ecosystem Initiatives

Japan is actively pursuing a comprehensive policy framework to revitalize its domestic semiconductor industry, underpinned by substantial government investments in advanced chip manufacturing, research infrastructure, and industry partnerships. National initiatives are fostering closer collaboration between public institutions, private manufacturers, and international technology leaders, creating an enabling environment for cutting-edge chip development. This ecosystem approach is attracting significant foreign direct investment (FDI) and establishing Japan as a strategically important node in the global semiconductor supply chain for advanced logic, memory, and power devices.

Market Outlook {Forecastperiod}:

The Japan semiconductor market is positioned for steady and sustained expansion across the forecast period, driven by the convergence of next-generation communication technologies, EV proliferation, and AI infrastructure buildout. Government-backed domestic manufacturing initiatives, combined with expanding international partnerships in chip fabrication and materials development, are expected to reinforce Japan's competitiveness and supply chain resilience. The market generated a revenue of USD 42.3 Billion in 2025 and is projected to reach a revenue of USD 64.4 Billion by 2034, growing at a compound annual growth rate of 4.6% from 2026-2034. Key growth catalysts include expanding end user applications in consumer electronics, automotive systems, and industrial automation. Japan's continued emphasis on compound semiconductor materials, such as silicon carbide, is expected to unlock new revenue streams, particularly in power electronics and clean energy applications.

Japan Semiconductor Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Components |

Memory Devices |

31.8% |

|

Material Used |

Silicon Carbide |

28.6% |

|

End User |

Consumer Electronics |

26.9% |

|

Region |

Kanto Region |

34.7% |

Components Insights:

- Memory Devices

- Logic Devices

- Analog IC

- MPU

- Discrete Power Devices

- MCU

- Sensors

- Others

Memory devices dominate the market with a share of 31.8% of the total Japan semiconductor market in 2025.

Memory devices represent the largest and most strategically significant component within the Japan semiconductor industry, reflecting the explosive growth of data-intensive applications, including AI workloads, cloud computing platforms, and autonomous vehicle systems. Japan's memory manufacturing ecosystem encompasses a wide range of NAND flash, DRAM, and high-bandwidth memory solutions that are integral to next-generation data processing architectures. In May 2024, Micron Technology intended to establish a new facility in Hiroshima Prefecture, Japan, for manufacturing DRAM chips, with operations expected to commence by the end of 2027, underscoring the strategic confidence placed in Japan as a high-value memory production hub for future semiconductor demand.

The market is seeing an increase in demand for a variety of memory devices, due to the steady growth of data center infrastructure and the emergence of edge computing architectures. Memory chips are being incorporated into a wider variety of end use applications, such as industrial sensors, medical diagnostic systems, wearable devices, and gaming platforms. With the industry concentrating on increased storage density, lower power consumption, and faster data access speeds to meet the increasingly demanding needs of contemporary computing ecosystems across both consumer and enterprise-grade markets, Japan's memory production capabilities are evolving in response to changing performance benchmarks.

.webp)

Material Used Insights:

- Silicon Carbide

- Gallium Manganese Arsenide

- Copper Indium Gallium Selenide

- Molybdenum Disulfide

- Others

Silicon carbide leads with a share of 28.6% of the total Japan semiconductor market in 2025.

Silicon carbide is firmly established as the leading material in the Japan semiconductor sector, owing to its unmatched combination of high thermal conductivity, superior electrical breakdown strength, and low power loss characteristics that make it indispensable for high-voltage and high-temperature power electronics applications. The material is central to Japan's automotive semiconductor strategy, where its properties directly support the performance requirements of EV traction inverters, onboard chargers, and fast-charging infrastructure.

Beyond automotive applications, silicon carbide is gaining traction across a broadening range of end-use sectors in Japan, including industrial motor drives, renewable energy inverters, and data center power supplies, where energy efficiency is a central design priority. The Japan semiconductor industry is investing in expanding silicon carbide wafer production and refining fabrication processes to meet the growing global demand driven by decarbonization commitments and electrification trends. The material's unique properties are enabling the development of more compact, reliable, and thermally stable power modules, reinforcing silicon carbide's critical long-term role within Japan's semiconductor industrial ecosystem and supply chain.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Industrial

- Data Centre

- Telecommunication

- Consumer Electronics

- Aerospace and Defense

- Healthcare

- Others

Consumer electronics comprise the largest segment with a 26.9% share of the total Japan semiconductor market in 2025.

Consumer electronics constitute the dominant end-user segment for semiconductors in Japan, driven by the country's position as a global leader in technology-driven consumer product innovation, encompassing smartphones, gaming consoles, wearable devices, and smart home appliances. The demand for high-performance chips in consumer products continues to grow as device specifications rise and new form factors emerge, requiring advanced memory, sensors, and processing components. Rapid product refresh cycles in consumer electronics further sustain consistent semiconductor demand.

Japan's consumer electronics manufacturers continue to push the boundaries of product performance and miniaturization, necessitating the integration of increasingly sophisticated semiconductor components across all product categories. The transition towards smarter, more connected consumer devices, incorporating AI-driven features, biometric sensors, and advanced display technologies, is expanding the semiconductor content per device and creating new demand vectors across the value chain. Additionally, the rise of immersive gaming platforms, augmented reality (AR) applications, and health-monitoring wearables is broadening the scope of semiconductor applications within the consumer electronics segment, reinforcing its dominant position across Japan's semiconductor market share landscape.

Regional Insights:

- Kanto Region

- Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represents the leading segment with a 34.7% share of the total Japan semiconductor market in 2025.

Kanto Region, anchored by the Tokyo metropolitan area, stands as the primary hub of the Japan semiconductor industry, housing the headquarters and research centers of the country's leading technology companies, semiconductor design houses, and engineering institutions. Its deep concentration of engineering talent and established supply chain ecosystems reinforces its global prominence. The region also benefits from strong venture capital activity and a dense network of advanced electronics manufacturers supporting semiconductor innovation.

The Kanto Region's semiconductor ecosystem is evolving rapidly, with a growing emphasis on AI chip design, precision imaging semiconductors, and advanced power electronics. The area's proximity to major research universities, government technology agencies, and global equipment suppliers creates a fertile environment for collaborative innovation. Ongoing investments in next-generation chip development capabilities and expanding data center activity within the metropolitan region continue to strengthen Kanto Region's dominant position within Japan's semiconductor value chain.

Market Dynamics:

Growth Drivers:

Why is the Japan Semiconductor Market Growing?

Robust Government Support and Strategic Industrial Policy

An assertive and persistent government industrial strategy that views chip manufacturing as essential to Japan's economic security has a fundamental impact on the country’s semiconductor business. In order to draw advanced semiconductor investment and keep vital fabrication expertise inside Japanese borders, policy authorities have built a vast ecosystem of financial incentives, infrastructure assistance, and regulatory frameworks. The government has made Japan one of the most desirable sites in the world for semiconductor manufacturers looking to set up next-generation manufacturing capacity through direct subsidies, tax breaks, and land allocations. Significant foreign investment inflows from top global chip makers have been sparked by these favorable circumstances, resulting in semiconductor clusters that gain from proximity to supply chains, shared infrastructure, and labor pools.

Growing Adoption of EVs and Automotive Semiconductor Demand

The rapid electrification of Japan's automotive industry is creating substantial and sustained demand for advanced semiconductor technologies, fundamentally reshaping the composition of the Japan semiconductor market. As per the information released by the Japan Automobile Manufacturers Association, domestic EV sales increased by 1.6% in 2025 to reach 60,677 units. EVs require significantly higher semiconductor content than conventional internal combustion engine vehicles, incorporating power management chips, motor control systems, advanced driver assistance electronics, battery management units, and in-vehicle network controllers into their architectures. Japan's position as one of the world's leading automotive manufacturing nations places it at the forefront of this transition, as domestic vehicle manufacturers accelerate their electrification roadmaps and seek to secure reliable access to performance-grade semiconductors. Compound semiconductor materials, such as silicon carbide and gallium nitride, are particularly integral to EV applications, enabling higher power density, reduced thermal losses, and extended battery range in EV drivetrain systems.

Expansion of 5G Networks and Next-Generation Communication Infrastructure

The progressive deployment of fifth-generation wireless networks across Japan is generating significant and growing demand for the advanced semiconductor components that underpin modern telecommunications infrastructure. Network equipment for fifth-generation applications requires high-performance radio frequency chips, signal processing units, power amplifiers, and baseband processors that operate at higher frequencies and data throughput rates than earlier generations of wireless technology. Japan's strategic national goal of achieving widespread fifth-generation coverage, coupled with longer-term research into sixth-generation technology architectures, is creating a durable and expanding demand pipeline for cutting-edge communication semiconductors. The proliferation of connected devices enabled by fifth-generation infrastructure, spanning smart factories, autonomous vehicles, telemedicine platforms, and smart city systems, further amplifies semiconductor consumption across Japan's entire industrial and consumer ecosystem. Data center expansion is intrinsically linked to next-generation communication rollouts, as increased data flows generated by high-speed wireless networks require corresponding growth in cloud computing capacity, storage systems, and network switching infrastructure.

Market Restraints:

What Challenges the Japan Semiconductor Market is Facing?

High Manufacturing Costs and Capital Intensity

Building and operating advanced semiconductor fabrication facilities require enormous capital investments in equipment, real estate, and infrastructure, creating significant barriers for new entrants and limiting the pace of capacity expansion. Extreme ultraviolet (UV) lithography tools, precision chemical delivery systems, and cleanroom construction impose costs that are difficult to recover without sustained high-volume production. Japan's electricity costs, which are significantly higher than those in competing semiconductor manufacturing nations, further compound operational expenditure burdens. These cost dynamics create persistent competitive pressure on domestic manufacturers, particularly for advanced node production where margins are sensitive to yield rates and equipment amortization cycles, potentially constraining the overall expansion trajectory of the Japan semiconductor market.

Talent Shortages and Aging Workforce Demographics

The Japan semiconductor industry faces a structural talent gap driven by demographic shifts, including a declining birthrate and an aging engineering workforce. Many experienced semiconductor engineers have migrated to higher-paying markets, while domestic university enrollment in science, technology, engineering, and mathematics disciplines has not kept pace with industry demand. Training and onboarding new engineers for complex semiconductor fabrication and design roles requires substantial time and investment, limiting the industry's capacity to expand rapidly. The gap between available engineering talent and workforce requirements of new fabrication facilities represents a meaningful constraint on Japan's semiconductor production ambitions throughout the forecast period.

Geopolitical Risks and Supply Chain Dependencies

Japan's semiconductor supply chain faces meaningful exposure to geopolitical tensions, particularly given its significant dependence on imported critical materials and equipment components from regions subject to trade restrictions and diplomatic uncertainty. A substantial share of Japan's semiconductor imports originates from geographically concentrated sources, creating vulnerability to supply disruptions in the event of escalating trade disputes, export controls, or regional security instability. Dependence on external suppliers for essential raw materials, including gallium, germanium, and rare earth compounds, creates additional resilience risks for domestic chip production. These supply chain vulnerabilities necessitate costly diversification strategies and long-term procurement planning, adding complexity and cost pressure to semiconductor manufacturers operating within the market.

Competitive Landscape:

The Japan semiconductor market features a concentrated and highly capable competitive landscape, defined by the presence of globally recognized leaders across chip design, fabrication, materials, and equipment manufacturing. Domestic players maintain dominant positions in specialized high-value segments, including semiconductor manufacturing equipment, silicon wafer supply, photoresist materials, and compound power semiconductors, where Japan commands leading global market shares. Internationally, the market is further shaped by the presence of foreign chip manufacturers that have established or are expanding fabrication facilities in Japan, attracted by government incentives and strategic supply chain considerations. Competition within the market is intensifying across advanced logic, memory, and automotive semiconductor segments, as manufacturers accelerate investment in next-generation node development and advanced packaging technologies. Strategic alliances between domestic firms and global technology leaders are emerging as a key competitive dynamic, enabling knowledge transfer, shared R&D investment, and broader access to international customer bases.

Recent Developments:

-

In February 2026, TSMC disclosed intentions to manufacture cutting-edge 3-nanometer semiconductors in Japan. The 3-nanometer chips are anticipated to be utilized in high-demand sectors like AI data centers and autonomous vehicles.

Japan Semiconductor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others |

| Material Useds Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Others |

| End Users Covered | Automotive, Industrial, Data Centre, Telecommunication, Consumer Electronics, Aerospace and Defense, Healthcare, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Semiconductor Market Report

The Japan semiconductor market reached a value of USD 42.3 Billion in 2025.

The market is projected to grow at a CAGR of 4.6% during 2026-2034, reaching USD 64.4 Billion by 2034.

Key growth drivers include surging demand for automotive-grade chips, Japan's national semiconductor self-sufficiency strategy, rapid expansion of AI and IoT infrastructure, strong government subsidies attracting TSMC and Micron fabrication investments, and robust consumer electronics manufacturing base.

The report covers segmentation by components, material used, end user, and region. Each segment includes detailed market size and forecast analysis.

Key trends include accelerated domestic fab construction under the Semiconductor and Digital Industry Strategy, rising adoption of silicon carbide chips for EV powertrains, deepening US-Japan chip alliance, increased focus on edge AI processors, and growing investment in next-generation compound semiconductor R&D.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)