Japan Smart Lock Market Size, Share, Trends and Forecast by Lock Type, Communication Protocol, End User, and Region 2026-2034

Japan Smart Lock Market Size & Forecast 2026-2034

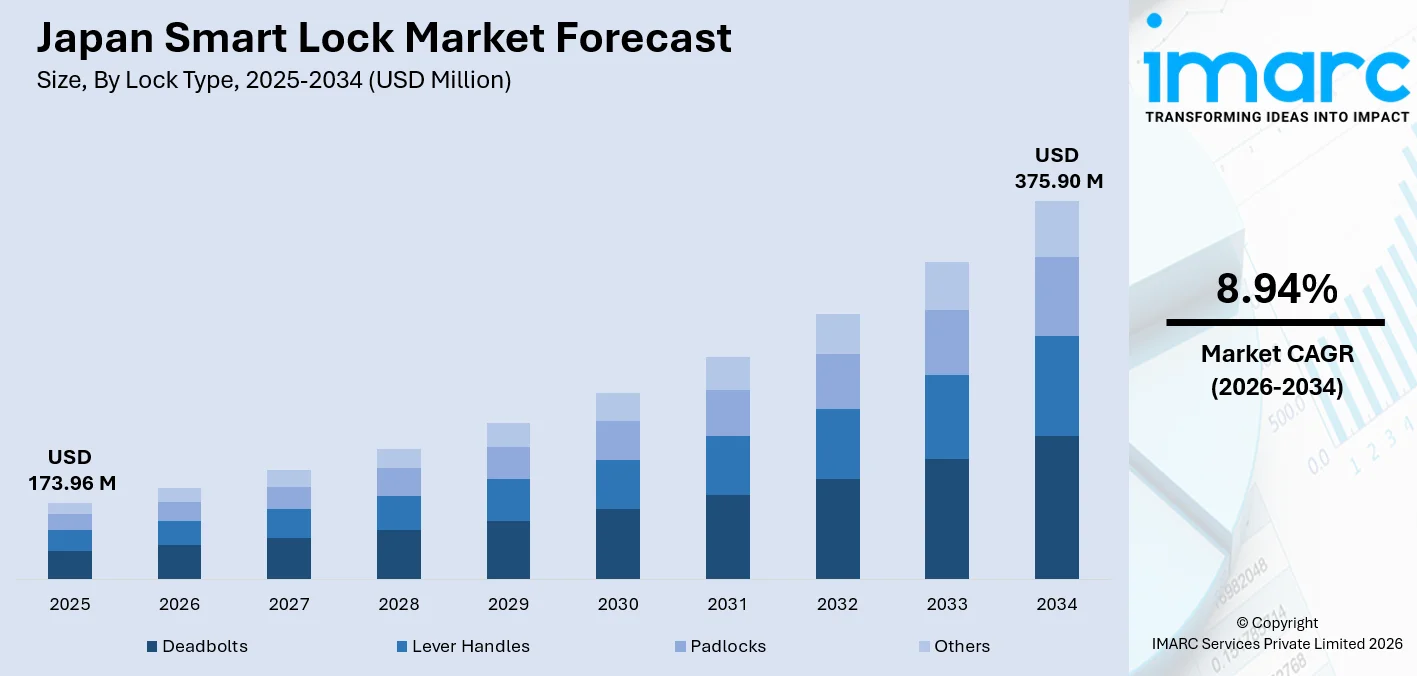

The Japan smart lock market size was valued at USD 173.96 Million in 2025, and is projected to reach USD 375.90 Million by 2034, growing at a CAGR of 8.94% from 2026-2034, driven by accelerating adoption of smart home ecosystems, rising demand for keyless access control in residential properties, and a rapidly aging population requiring convenient security solutions. Leopalace21 Corporation announced that approximately 550,000 rental housing units are managed by Leopalace21, accounting for about 10% of that total.

To get more information on this market Request Sample

Japan Smart Lock Industry Analysis - Key Insights

- Deadbolts command 42.3% of the market by lock type in 2025- Japan's residential door architecture overwhelmingly favours cylinder deadbolts, and smart variants slot directly into existing preparations.

- Bluetooth holds 44.6% of the communication protocol share in 2025- anchored by its low power draw, year-long battery life, and smartphone-only operation without a hub.

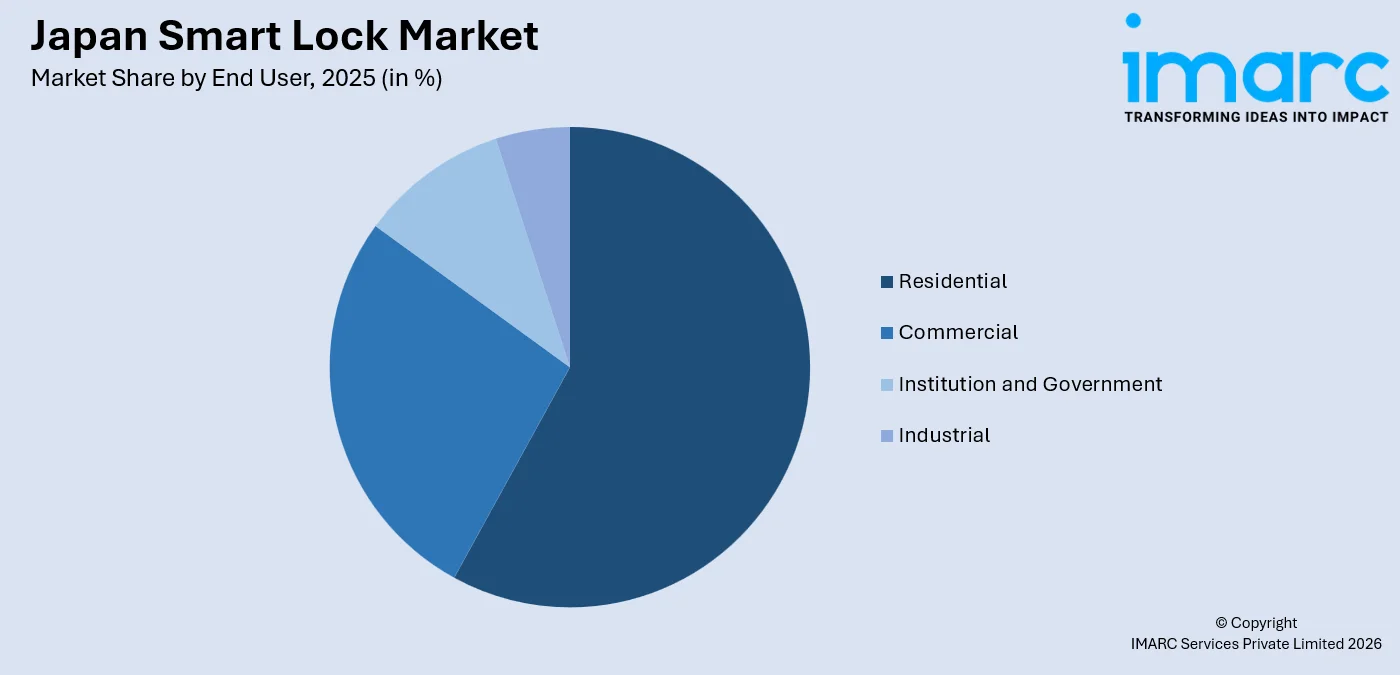

- Residential dominates end user demand at 58.2% in 2025- with high dwelling units across Japan and surging uptake in rental apartment complexes, the home segment is the market's undisputed volume engine.

- Kanto Region leads regionally with 40.7% share in 2025- Tokyo's concentration of high-income, tech-savvy households, active smart-city pilots in Yokohama and Kawasaki.

Japan Smart Lock Market Trends and Dynamics 2026

Market Trends

Matter Protocol Integration Is Reshaping Japan's Smart Lock Landscape

Japan's smart lock sector is undergoing a pivotal interoperability transition as domestic manufacturers adopt the universal Matter standard. In January 2025, SEALSQ Corp partnered with MIWA Lock Co., Ltd. to launch the PiACK HOME PG, Japan's first Matter-compatible smart lock, integrating quantum-resistant PKI security with Amazon Alexa, Apple Home, and Google Home ecosystems.

Rental Property Operators Accelerating Keyless Deployment at Scale

Japan's residential property management sector is embedding smart locks into standard lease infrastructure. Leopalace21 reported that 92% of new tenants signed leases at smart-lock-equipped units April 2024 to February 2025, eliminating leasing office key pickup and cutting lock-related operational labour.

AI-Enhanced Security Features Driving Premium Product Differentiation

Smart lock manufacturers operating in Japan are integrating AI-powered anomaly detection, facial recognition doorbell pairing, and predictive maintenance alerts to command premium price points. This health-security convergence is unlocking entirely new commercial use cases for the Japan Smart Lock market growth.

- Biometric Authentication Expansion: Fingerprint and NFC-card access modes are being added to mid-range smart deadbolts, broadening appeal beyond early-adopter segments.

- Short-Term Rental Adoption: Inbound tourism surging to record levels is driving vacation-rental operators to deploy time-limited code smart locks across Kyoto, Osaka, and Tokyo listings.

- Quantum-Resistant Cybersecurity Standards: Post-quantum PKI solutions are entering smart lock hardware, establishing Japan as an early adopter of future-proofed IoT access security.

- DX-Led Property Management Integration: Real estate tech platforms are linking smart lock APIs to property management systems for automated access provisioning at tenant onboarding.

Growth Drivers

Aging Population and Independent Living Demand

Japan's demographic structure is a foundational market driver. With over 36.2 million citizens aged 65 or above by September 2023, municipal governments and housing operators are subsidising smart locks, motion sensors, and fall-detection integrations to enable seniors to remain in their homes independently. Telecom operators including NTT have bundled smart lock hardware into 24-month subscription contracts that spread upfront costs, making adoption accessible for fixed-income elderly households who represent a structurally expanding user segment.

Smart City Infrastructure and Government Digitization Mandates

The Zero Energy House subsidy programme offers homeowners rebates on qualifying smart home installations, directly incentivising deadbolt and smart lock upgrades. Government digitization of real estate processes, including electronic tenancy contracts and digital move-in procedures, is further normalising smart lock adoption across the residential Japan smart lock market forecast.

Rising Security Awareness and Insurance Incentives

Heightened public anxiety following a rise in reported residential break-ins during 2024–2025 accelerated smart security device uptake.

- Smart Home Ecosystem Expansion: Growing penetration of voice assistants is pulling smart lock adoption as users build integrated home control environments.

- Urbanization and High-Density Living: With 92.13 % of Japan's population residing in urban areas (2024), compact apartment living makes keyless entry a practical necessity rather than a premium feature.

- Tourism-Driven Short-Term Rental Growth: Expanding inbound tourism and licensed short-term rental properties are generating demand for remotely programmable, time-coded smart locks across hospitality and vacation properties.

Market Restraints

High retrofit complexity in ageing housing stock: Japan's residential landscape includes a substantial share of older buildings and rental properties that lack standardized door preparations compatible with modern smart lock form factors. Retrofitting in such properties often requires structural modifications or landlord consent, creating installation barriers.

Cybersecurity and data privacy concerns: Consumer reluctance to entrust physical home access to networked devices remains a persistent demand-side moderator in Japan's privacy-conscious culture. Concerns about unauthorized remote access, firmware vulnerabilities, and cloud-server data retention practices create hesitation among technologically cautious buyer segments, particularly elderly demographics who represent a priority growth cohort for the market.

Fragmented interoperability and multi-protocol complexity: The coexistence of Bluetooth, Wi-Fi, Z-Wave, Zigbee, and Thread protocols across competing smart lock platforms creates integration challenges for consumers seeking unified home ecosystems. The absence of universally adopted standards, despite the emergence of Matter, means buyers risk vendor lock-in or device incompatibility when expanding their connected home environments, moderating upgrade and cross-selling opportunities for manufacturers.

Japan Smart Lock Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Lock Type |

Deadbolts |

42.3% |

2025 |

|

Communication Protocol |

Bluetooth |

44.6% |

2025 |

|

End User |

Residential |

58.2% |

2025 |

|

Region |

Kanto Region |

40.7% |

2025 |

Lock Type Insights

Deadbolts - 42.3% Market Share (2025) | Leading Lock Type

Deadbolts dominate Japan's smart lock market because the vast majority of residential and commercial doors across the country use cylinder deadbolt configurations that accept direct smart replacements. Their superior mechanical resistance to forced entry, combined with straightforward retrofit installation onto existing door preparations, makes them the default upgrade path for property managers and homeowners alike.

|

Segment Breakdown Deadbolts (42.3%) · Lever Handles · Padlocks · Others |

Communication Protocol Insights

Bluetooth - 44.6% Market Share (2025) | Leading Communication Protocol

Bluetooth's dominance in Japan's smart lock communication protocol segment reflects the practical realities of urban apartment living. Bluetooth-enabled locks operate without a home Wi-Fi hub or continuous internet connectivity, consume minimal power, enabling battery life exceeding twelve months, and connect directly to smartphones within proximity.

|

Segment Breakdown Bluetooth (44.6%) · Wi-Fi · Others |

End User Insights

Access the comprehensive market breakdown Request Sample

Residential - 58.2% Market Share (2025) | Leading End User

Japan's residential sector commands the dominant share of smart lock demand, driven by the country's vast housing stock and the accelerating integration of smart access into rental property management. The structural shift is demonstrated by Leopalace21's 300,000-unit smart lock rollout, where smart locks eliminated physical key handovers, automated one-time passcode issuance for viewing appointments, and reduced lock-related administrative workload. These operational benefits are prompting competing property management chains to implement equivalent programmes.

|

Segment Breakdown Residential (58.2%) · Commercial · Institution and Government · Industrial |

Regional Insights

Kanto Region - 40.7% Market Share (2025) | Leading Region

The Kanto Region commands Japan's smart lock market through Tokyo's exceptional concentration of high-income, technology-early-adopter households and the region's unmatched density of large-scale residential property managers. The region hosts the headquarters of major Japanese property management and lock manufacturers alike, creating a fully integrated supply-and-demand ecosystem that reinforces Kanto's structural market leadership.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 40.7% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | High disposable incomes, smart-city pilot programmes, dense managed-apartment ecosystem, tech-early-adopter demographics |

| Outlook | Sustained leadership with premium product growth |

|

Regional Breakdown Kanto Region (40.7%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

Kansai is Japan's second-largest smart lock market, anchored by Osaka's smart city development blueprint and the region's manufacturing base for lock hardware and IoT components. Osaka, Kyoto, and Kobe collectively host a high concentration of inbound international tourism, generating strong demand for vacation rental smart lock deployments.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga |

| Key Growth Drivers | Tourism-driven short-term rental adoption, Osaka smart city programme, manufacturing hub proximity |

| Outlook | Strong growth from tourism and smart city investments |

Central/Chubu Region:

Chubu's smart lock market is shaped by Nagoya's industrial base and Toyota's connected-home experiments, which are bringing smart access technology into company-affiliated housing estates and employee dormitories. The region's high proportion of factory worker dormitories and corporate housing is driving institutional and industrial end-user demand alongside residential adoption.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Corporate housing smart upgrades, Toyota connected-home programme, manufacturing-adjacent property demand |

| Outlook | Steady growth led by corporate and residential channels |

Kyushu-Okinawa Region:

Kyushu-Okinawa is emerging as one of the fastest-growing smart lock sub-markets, propelled by disaster-preparedness mandates following recent typhoon events and expanding renewable microgrid and zero-energy house programmes. Okinawa's thriving vacation and short-term rental ecosystem, driven by domestic and international beach tourism, is generating demand for remote-access Wi-Fi smart locks that allow property owners to manage access without physical presence.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto |

| Key Growth Drivers | Vacation rental proliferation, disaster-preparedness funding, zero-energy house subsidies, renewable energy housing integration |

| Outlook | Fastest-growing region through the forecast period |

Tohoku Region:

Tohoku's smart lock adoption is driven by reconstruction housing developments following the 2011 earthquake and subsequent regional rebuilding programmes that incorporated smart home infrastructure into new residential construction.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima |

| Key Growth Drivers | Reconstruction housing upgrades, elderly care subsidies, cold-climate remote access demand |

| Outlook | Moderate growth with elderly-care focus |

Market Outlook (2026-2034)

What is the future outlook of the Japan Smart Lock market?

The Japan Smart Lock market is expected to sustain steady revenue growth through 2034.

Japan's smart lock market is positioned for robust, sustained expansion through 2034, underpinned by the convergence of demographic-driven residential demand, policy-mandated smart housing targets, and continuous innovation in biometric and interoperable access technologies. The accelerating adoption of the Matter standard across domestic manufacturers will reduce integration friction, expand compatible device networks, and attract new buyer cohorts. Rising insurance incentives, expanding short-term rental infrastructure, and corporate housing smart upgrade programmes across industrial regions will collectively broaden the addressable market beyond the Kanto core, ensuring geographically distributed growth and reinforcing Japan's position as Asia's leading premium smart access market.

Japan Smart Lock Market - Leading Key Players

The Japan smart lock market is shaped by a competitive mix of established domestic lock manufacturers, global smart home technology companies, and specialized IoT security providers. Key players compete on integration depth, security certification, battery efficiency, and ecosystem compatibility, with domestic brands leveraging decades of lock engineering expertize while global players introduce Matter-certified interoperable platforms.

| Company | Leading Brands | Highlights |

|---|---|---|

|

MIWA Lock Co., Ltd. |

PiACK 2 Digital Lock, iEL Zero Smart Lock, OPJ Series |

One of Japan’s largest lock manufacturers with strong domestic market share; provides electronic and smart locking systems for residential, commercial, and hospitality sectors. |

|

LOCKMAN japan |

LC-105, ID-202TAB, ID-602Bhook |

Offers electronic door locks, digital security solutions, and access control products for residential and commercial buildings. |

|

Photosynth Inc. |

Akerun Access Control System, Akerun.M Keyless Rental System |

Developer of the Akerun smart lock platform enabling smartphone-based remote access and cloud-managed door control for homes and offices. |

Some of the other key market players in the Japan smart lock market are Leopalace21 Corporation, GOAL Co., Ltd., ALPHA Corporation, Panasonic Corporation (HomeX), Assa Abloy Japan, etc.

Latest Development & News

- In March 2025, Leopalace21 Corporation announced that more than 300,000 units in its managed apartments are now equipped with smart locks, marking the largest deployment in Japan’s rental housing management industry. The installation enhances customer convenience by eliminating the need for tenants to visit leasing offices to collect keys when moving in. It also helps the company improve operational efficiency and productivity.

- In January 2025, SEALSQ Corp announced a partnership with MIWA Lock Co., Ltd. to deliver the secure technology behind PiACK HOME PG, Japan’s first Matter-compatible smart lock. The product, now officially launched, marks the start of a strategic business collaboration between SEALSQ and MIWA Lock in the smart home security market.

Japan Smart Lock Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Lock Types Covered | Deadbolts, Lever Handles, Padlocks, Others |

| Communication Protocols Covered | Bluetooth, Wi-Fi, Others |

| End Users Covered | Commercial, Residential, Institution and Government, Industrial |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan smart lock market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan smart lock market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan smart lock industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Smart Lock Market Report

The Japan smart lock market reached a value of USD 173.96 Million in 2025.

The market is projected to grow at a CAGR of 8.94% during 2026-2034, reaching USD 375.90 Million by 2034.

Key growth drivers include the increasing adoption of smart home systems and IoT integration, rising demand for convenient keyless access control, growing security concerns, and expanding use of biometric authentication in residential and commercial sectors.

The report covers segmentation by lock type, communication protocol, end user, and region. Each segment includes detailed market size and forecast analysis.

Key trends include growing home automation adoption, expanding IoT ecosystem integration, rising consumer confidence in biometric and digital key technologies, and increasing compatibility of smart locks with diverse smart home platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade