Japan Spout Pouch Market Size, Share, Trends and Forecast by Component, Material, Pouch Size, Closure Type, End User, and Region, 2026-2034

Japan Spout Pouch Market Summary:

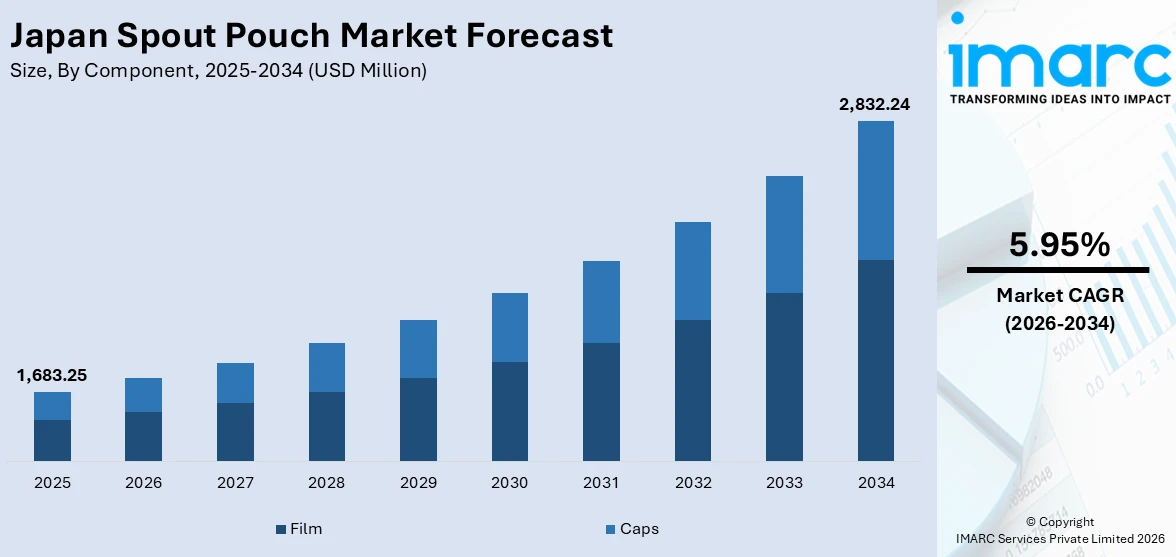

The Japan spout pouch market size was valued at USD 1,683.25 Million in 2025 and is projected to reach USD 2,832.24 Million by 2034, growing at a compound annual growth rate of 5.95% from 2026-2034.

The Japan spout pouch market is experiencing sustained expansion driven by evolving consumer preferences for convenient, lightweight, and resealable packaging formats. Rapid urbanization, an aging population, and growing single-person households are accelerating demand across food, beverage, personal care, and pharmaceutical applications. The increasing adoption of sustainable packaging solutions aligned with national environmental policies further strengthens market momentum. Technological advancements in barrier properties and material innovation continue to enhance product functionality, reinforcing the integral role of spout pouches across diverse end-use industries.

Key Takeaways and Insights:

- By Component: Film dominates the market with a share of 62.4% in 2025, owing to its superior barrier properties, flexibility in lamination processes, and compatibility with high-speed filling operations. Growing preference for lightweight packaging structures accelerates film adoption across multiple end-use applications.

- By Material: Plastic leads the market with a share of 71.9% in 2025. This dominance is driven by the versatility of polyethylene and polypropylene resins that deliver excellent moisture resistance, heat-seal performance, and cost-effective manufacturing capabilities essential for large-scale commercial packaging.

- By Pouch Size: 200 to 500 ML dominates the market with a share of 33.7% in 2025, owing to its alignment with single-serve beverage consumption patterns, on-the-go meal solutions, and personal care refill applications that resonate with Japan’s convenience-oriented consumer culture.

- By Closure Type: Screw cap exhibits a clear dominance in the market with 68.5% share in 2025, reflecting consumer preference for secure, resealable closure mechanisms that prevent spillage, maintain product freshness, and enable controlled dispensing across liquid food and household applications.

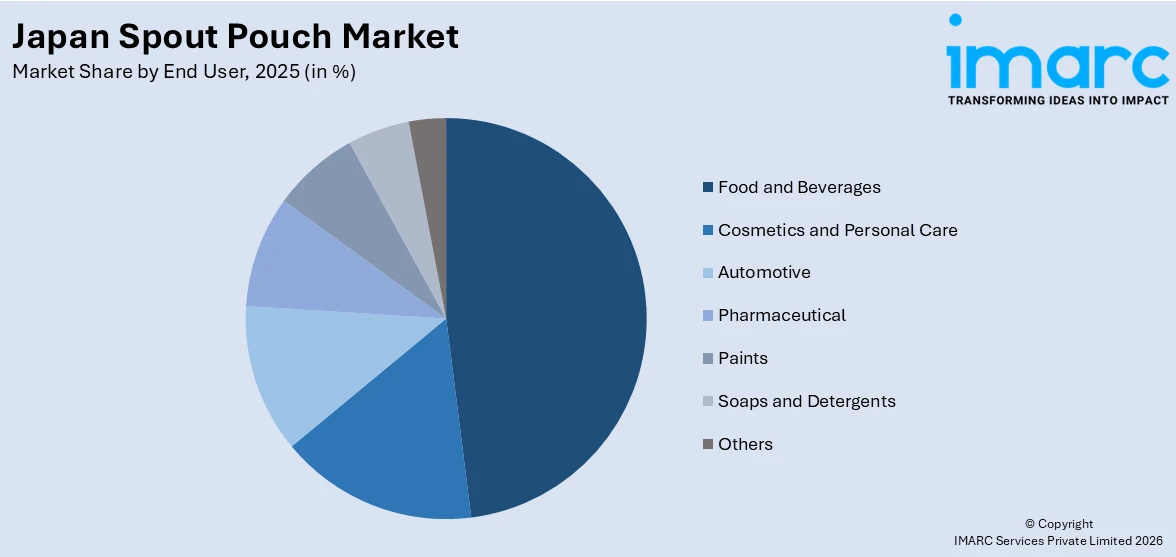

- By End User: Food and beverages hold the largest segment with a market share of 48.2% in 2025, driven by Japan’s robust convenience food culture, expanding ready-to-eat product offerings, and increasing demand for shelf-stable beverages packaged in lightweight, portable, and resealable formats.

- By Region: Kanto Region represents the leading region with 36.1% share in 2025, driven by the concentration of metropolitan populations in Tokyo and Yokohama, extensive retail infrastructure, high consumer spending, and the presence of major food processing and packaging manufacturing facilities.

- Key Players: Key players drive the Japan spout pouch market by investing in sustainable material innovation, expanding production capacities, and strengthening partnerships with food processors and consumer goods manufacturers. Their focus on mono-material recyclable structures, advanced barrier technologies, and automated filling systems accelerates market penetration and ensures consistent product availability across diverse distribution channels.

To get more information on this market Request Sample

The Japan spout pouch market is propelled by a convergence of demographic shifts, regulatory mandates, and technological innovation that collectively reinforce sustained demand for flexible packaging solutions. The country’s rapidly aging population and expanding base of single-person households create persistent demand for portion-controlled, easy-to-dispense, and resealable packaging formats that optimize convenience in compact living environments. The government’s Plastic Resource Circulation Strategy mandates that all plastic packaging achieve reusable or recyclable status, compelling manufacturers to invest in mono-material laminates, bio-based polymers, and paper-based barrier substrates. Simultaneously, the proliferation of convenience stores and expanding e-commerce channels demand lightweight, durable packaging that minimizes transportation costs while preserving product integrity. These interconnected forces position the spout pouch as an indispensable packaging format across Japan’s evolving consumer landscape, driving consistent growth throughout the forecast period.

Japan Spout Pouch Market Trends:

Accelerated Shift Toward Mono-Material Recyclable Structures

Japanese spout pouch manufacturers are increasingly transitioning from traditional multi-layer laminates to mono-material structures designed for mechanical recycling compatibility. This transformation is driven by the Plastic Resource Circulation Strategy, which mandates that all plastic packaging achieve reusable or recyclable status. Converters are developing retort-capable polypropylene and polyethylene mono-material pouches that maintain high heat resistance and barrier performance while enabling single-polymer recoverability through existing municipal waste streams. The shift extends to barrier-coated kraft substrates incorporating nanocellulose coatings that deliver oxygen transmission rates previously achievable only with aluminum foil, enabling food and beverage brands to replace metalized laminates without compromising product shelf life or freshness preservation requirements.

Integration of Smart Packaging Technologies

The convergence of digital innovation and packaging design is reshaping the Japan spout pouch landscape as manufacturers embed interactive technologies directly into flexible packaging formats. Smart pouches integrated with near-field communication tags, quick response codes, and radio-frequency identification markers enable real-time product authentication, supply chain traceability, and enhanced consumer engagement. These digital features align with Japan’s technology-driven consumer culture, where shoppers increasingly expect packaging to deliver informational value beyond basic containment. The digitalization trend extends to automated quality inspection systems and digital inkjet printing capabilities that enable short-run customization, rapid design iteration, and cost-effective production of limited-edition packaging variations.

Expansion of Refill-Based Consumption Models

The growing environmental consciousness among Japanese consumers is driving rapid expansion of refill-based packaging systems that leverage spout pouches as primary delivery mechanisms. Household care brands are transitioning concentrated detergents, hand soaps, and cleaning solutions into spouted refill pouches that reduce overall plastic consumption by enabling multiple reuses of rigid dispensing containers. This model resonates strongly with Japan’s waste-conscious consumer base, where municipal waste sorting requirements and limited storage space incentivize compact, collapsible packaging formats. Skincare companies provide moisturizers, cleansers, and shampoos in spouted pouches that are easy to transfer into reusable containers, demonstrating how the refill trend has spread beyond home goods into personal care categories.

Market Outlook 2026-2034:

The Japan spout pouch market is poised for consistent expansion throughout the forecast period, underpinned by strengthening demand from convenience-driven consumer segments and escalating regulatory emphasis on sustainable packaging transitions. Continued investment in mono-material recyclable structures and bio-based polymer alternatives will reshape the material composition landscape, enabling compliance with increasingly stringent environmental regulations while maintaining functional performance. The proliferation of e-commerce channels and expanding direct-to-consumer delivery models will sustain demand for lightweight, tamper-evident, and durable packaging formats optimized for logistics efficiency. Technological advancements in barrier coatings, digital printing capabilities, and automated filling systems will further enhance production efficiency and product differentiation opportunities across diverse application segments. The market generated a revenue of USD 1,683.25 Million in 2025 and is projected to reach a revenue of USD 2,832.24 Million by 2034, growing at a compound annual growth rate of 5.95% from 2026-2034.

Japan Spout Pouch Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Film |

62.4% |

|

Material |

Plastic |

71.9% |

|

Pouch Size |

200 to 500 ML |

33.7% |

|

Closure Type |

Screw Cap |

68.5% |

|

End User |

Food and Beverages |

48.2% |

|

Region |

Kanto Region |

36.1% |

Component Insights:

- Caps

- Film

Film dominates with a share of 62.4% of the total Japan spout pouch market in 2025.

Film maintains its commanding position in the Japan spout pouch market due to its unmatched versatility in accommodating diverse product viscosities, temperature requirements, and shelf-life specifications across multiple end-use categories. The segment benefits from continuous advancements in multilayer lamination technologies that enable precise calibration of barrier properties, including oxygen transmission rates, moisture vapor permeability, and light protection characteristics. Growing demand for lightweight, high-performance packaging structures further accelerates film adoption across food, beverage, pharmaceutical, and personal care applications nationwide.

The growing emphasis on recyclability is driving significant innovation within the film segment as converters develop mono-material polyethylene and polypropylene film structures capable of replacing traditional multi-layer laminates without compromising functional performance. These advances enable spout pouch films to meet stringent municipal recycling requirements while maintaining the heat resistance, puncture strength, and seal integrity demanded by high-speed automated filling operations. The expansion of retort-capable mono-material films further broadens application possibilities, allowing shelf-stable food products previously dependent on aluminum-containing structures to transition into fully recyclable packaging formats compatible with established mechanical recycling infrastructure.

.webp)

Material Insights:

- Plastic

- Aluminium

- Paper

- Others

Plastic leads with a share of 71.9% of the total Japan spout pouch market in 2025.

Plastic dominates the material landscape of Japan’s spout pouch market owing to the exceptional processing versatility, barrier customization capabilities, and cost efficiency that polyethylene, polypropylene, and polyethylene terephthalate resins deliver across diverse packaging applications. The material’s inherent adaptability enables manufacturers to engineer spout pouches with precisely tailored moisture resistance, oxygen barrier properties, and heat-seal performance characteristics essential for preserving product integrity in food, beverage, pharmaceutical, and personal care segments.

The plastic segment is undergoing transformative innovation as Japanese manufacturers respond to intensifying regulatory pressure and consumer demand for environmentally responsible packaging materials. The development of mono-material polypropylene retort pouches that withstand high-temperature sterilization while remaining fully compatible with mechanical recycling streams represents a significant technological breakthrough. Converters are simultaneously investing in bio-based polyethylene derived from sugarcane feedstock and recycled post-consumer resin content to reduce virgin plastic dependency. These sustainability-oriented innovations enable spout pouch producers to maintain the functional advantages of plastic while progressively aligning with circular economy mandates established under Japan’s Plastic Resource Circulation Strategy.

Pouch Size Insights:

- Less than 200 ML

- 200 to 500 ML

- 500 to 1,000 ML

- More than 1,000 ML

200 to 500 ML exhibits a clear dominance with a 33.7% share of the total Japan spout pouch market in 2025.

200 to 500 ML maintains its leading position in the Japan spout pouch market by aligning perfectly with the nation’s deeply embedded single-serve consumption patterns and on-the-go lifestyle preferences. This size range accommodates the most commercially significant product categories including ready-to-drink beverages, fruit juices, yogurt drinks, liquid soups, and personal care refills that constitute daily purchasing habits across Japanese convenience stores and supermarkets. The segment benefits from Japan’s extensive convenience store network, which comprises outlets nationwide providing accessible retail touchpoints where single-serve spouted pouches occupy prominent shelf positions alongside traditional rigid packaging alternatives.

The sustained growth of this size segment reflects broader demographic trends reshaping Japanese consumer behavior, particularly the expansion of single-person households and the increasing workforce participation among women, both of which drive demand for portable, pre-portioned packaging solutions. Manufacturers are responding by developing ergonomically optimized pouch designs within this capacity range that feature improved grip surfaces, controlled-pour spout mechanisms, and visually appealing graphics that differentiate products in crowded retail environments. The versatility of the size range also positions it as the preferred format for household product refills, where concentrated detergents and cleaning solutions in spouted pouches enable consumers to replenish rigid dispensers efficiently.

Closure Type Insights:

- Screw Cap

- Flip Top Cap

Screw cap holds the largest share at 68.5% of the total Japan spout pouch market in 2025.

Screw cap maintains its overwhelming dominance in the Japan spout pouch closure segment due to its proven reliability in delivering leak-proof sealing, controlled dispensing, and secure resealability that Japanese consumers prioritize across food, beverage, and household product categories. The closure mechanism’s universal familiarity among end users reduces the learning curve for new product adoption while ensuring consistent performance throughout the product consumption cycle. According to industry data, the beverage segment alone accounts for a significant portion of spouted pouch applications in Japan, where screw cap closures facilitate hygienic, spill-free consumption patterns among commuters and outdoor consumers.

The screw cap segment continues to evolve through material optimization and design innovation aimed at enhancing both functional performance and sustainability credentials. Manufacturers are developing lightweight polypropylene and polyethylene screw caps that reduce overall material usage while maintaining the torque resistance and tamper-evidence features demanded by regulatory agencies and quality-conscious consumers. The emergence of tethered cap designs, aligned with global anti-litter legislation trends, represents the latest evolution in closure engineering. These innovations ensure that screw caps remain physically attached to the pouch after opening, preventing environmental contamination and facilitating proper disposal through municipal waste sorting systems.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverages

- Cosmetics and Personal Care

- Automotive

- Pharmaceutical

- Paints

- Soaps and Detergents

- Others

Food and beverages dominate with a share of 48.2% of the total Japan spout pouch market in 2025.

Food and beverages command the largest share of the Japan spout pouch market, reflecting the sector’s deep reliance on flexible packaging formats that deliver superior product preservation, portability, and consumer convenience. Japan’s robust convenience food culture, characterized by an extensive network of over 56,000 convenience stores and widespread adoption of ready-to-eat meal solutions, generates persistent demand for spouted pouches capable of containing liquid soups, sauces, beverages, and semi-viscous food products. The United States Department of Agriculture reported that Japan’s food processing industry production encompasses substantial output in dairy products, processed meats, and frozen foods, all of which increasingly utilize spout pouch formats for retail distribution.

The expansion of functional and health-oriented beverage categories further reinforces the segment’s growth trajectory as Japanese consumers increasingly seek convenient packaging for protein drinks, vitamin-enriched waters, and fermented dairy beverages. Spout pouches offer distinct advantages for these applications through controlled dispensing, oxygen-barrier protection that preserves nutritional content, and lightweight portability that accommodates active lifestyle consumption patterns. The segment also benefits from the growing meal kit delivery market, where pre-measured sauce and condiment pouches with spout closures enable precise ingredient dispensing while minimizing food waste and packaging volume in urban households.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represents the leading region with a 36.1% share of the total Japan spout pouch market in 2025.

Kanto Region commands the largest share of the Japan spout pouch market, driven by the extraordinary concentration of metropolitan populations, commercial infrastructure, and industrial manufacturing capabilities centered around Tokyo and Yokohama. The region’s dense retail landscape, encompassing supermarket chains, convenience store networks, and rapidly expanding e-commerce fulfilment operations, generates substantial demand for lightweight, space-efficient packaging formats that optimize shelf utilization and logistics efficiency. Japan’s urban population reached approximately 92% in 2023, with the Kanto metropolitan area housing a significant proportion of this urbanized population, creating an exceptionally concentrated consumer base with high per capita packaging consumption rates.

The region’s position as Japan’s primary economic and innovation hub ensures that emerging packaging trends gain earliest traction within the Kanto market before diffusing to other regions. Major food processing companies, cosmetics manufacturers, and pharmaceutical firms headquartered in the greater Tokyo area maintain close operational relationships with packaging converters, facilitating rapid adoption of advanced spout pouch technologies including smart packaging integration, sustainable material transitions, and customized design solutions. The concentration of research institutions and packaging technology development centers within the Kanto corridor further accelerates innovation cycles that continually expand the application scope and performance capabilities of spout pouch packaging.

Market Dynamics:

Growth Drivers:

Why is the Japan Spout Pouch Market Growing?

Escalating Demand for Convenience-Oriented Packaging Across Aging and Urbanizing Demographics

Japan’s demographic transformation is fundamentally reshaping packaging requirements across all consumer product categories, creating powerful structural demand for spout pouch formats that deliver intuitive dispensing, lightweight portability, and effortless resealability. The nation’s rapidly aging population increasingly requires packaging solutions with ergonomic features that accommodate reduced grip strength and dexterity, making the controlled-pour functionality of spout closures an essential design attribute for food, beverage, and pharmaceutical products targeting elderly consumers. Simultaneously, the expanding proportion of single-person households drives demand for individually portioned packaging sizes that minimize food waste while providing convenient storage in compact urban living spaces. The proliferation of convenience stores and their integration into daily commuting patterns further accelerates adoption of spouted pouches as preferred formats for on-the-go meal solutions, ready-to-drink beverages, and functional health products. Japanese consumers’ heightened expectations for packaging that combines practical convenience with aesthetic sophistication compel manufacturers to continuously refine spout pouch designs, incorporating features such as easy-tear notches, transparent windows for content visibility, and textured grip surfaces that enhance the overall user experience throughout the product consumption journey.

Regulatory Mandates Driving Sustainable Material Innovation and Circular Economy Transitions

Japan’s comprehensive regulatory framework governing packaging sustainability is creating transformative momentum within the spout pouch market by compelling manufacturers to invest in recyclable material systems, bio-based polymer alternatives, and reduced-plastic packaging architectures. The Plastic Resource Circulation Strategy establishes binding targets requiring all plastic packaging to achieve reusable or recyclable status, while the Containers and Packaging Recycling Law impose specific obligations on brand owners and converters regarding material reduction roadmaps and end-of-life management responsibilities. These regulatory mandates intersect with municipal fee structures that penalize hard-to-recycle multi-material laminates, creating direct economic incentives for transitioning to mono-material spout pouch constructions compatible with established mechanical recycling infrastructure. The Ministry of Economy, Trade and Industry’s newly announced packaging certification criteria, effective from January 2026, introducing additional requirements for recycled content minimums and material simplification across beverage, cosmetics, and household product packaging categories. This escalating regulatory environment stimulates capital investment in advanced coating technologies, bio-based film development, and paper-plastic hybrid structures that enable spout pouches to maintain functional performance while achieving full compliance with increasingly stringent environmental standards governing the Japanese packaging sector.

Expanding E-Commerce Channels and Direct-to-Consumer Distribution Models

The rapid expansion of Japan’s e-commerce ecosystem is generating significant incremental demand for spout pouch packaging formats that combine lightweight construction with superior transit durability and tamper-evidence capabilities essential for online fulfilment operations. The acceleration of direct-to-consumer delivery services, subscription-based meal kit platforms, and online grocery shopping creates requirements for packaging that minimizes dimensional weight while maximizing product protection throughout increasingly complex last-mile delivery networks. Spout pouches offer distinct logistical advantages over rigid packaging alternatives through their ability to reduce shipping volume, eliminate breakage risks associated with glass containers, and provide space-efficient storage at both fulfilment center and consumer household levels. The integration of spouted pouches into automated warehouse picking systems further enhances operational efficiency as e-commerce retailers prioritize packaging formats compatible with robotic handling equipment and high-throughput sortation processes. The growing penetration of online platforms in personal care, household chemical, and specialty food categories expands the addressable market for spout pouches beyond traditional brick-and-mortar retail channels. This digital commerce transformation creates sustained demand growth as brands increasingly develop e-commerce-optimized packaging designs that leverage the inherent flexibility, customizability, and cost advantages of spouted pouch formats.

Market Restraints:

What Challenges the Japan Spout Pouch Market is Facing?

Recycling Infrastructure Limitations for Multi-Layer Laminate Structures

Despite significant progress in mono-material development, a substantial portion of existing spout pouch production continues to rely on multi-layer laminated structures combining different polymer types, aluminum foil layers, and adhesive systems that complicate end-of-life recycling processes. Japan’s municipal waste management infrastructure, while sophisticated in sorting capabilities, faces technical challenges in efficiently separating and recovering individual material components from complex multi-layer pouches, resulting in diversion to thermal recovery rather than mechanical recycling pathways. This recycling complexity creates regulatory compliance risks for manufacturers as environmental standards progressively tighten.

Higher Unit Production Costs Compared to Conventional Rigid Packaging Formats

The specialized manufacturing processes required for spout pouch production, including precision spout insertion, multi-station sealing, and automated quality inspection systems, generate higher per-unit production costs compared to established rigid packaging alternatives such as bottles and cans. Small and medium-sized food and beverage processors face particular challenges in justifying the capital investment required for dedicated spouted pouch filling lines, limiting conversion rates among cost-sensitive segments of the market that prioritize immediate production economics over long-term sustainability and convenience benefits.

Consumer Perception Barriers Regarding Product Premium Quality

Certain consumer segments in Japan maintain established preferences for glass bottles, metal cans, and rigid plastic containers that convey perceptions of premium quality, product safety, and brand prestige that flexible spout pouches struggle to replicate. The tactile and visual associations between rigid packaging and product value remain deeply ingrained in Japanese consumer psychology, particularly within premium beverage, gourmet food, and luxury personal care categories where packaging presentation significantly influences purchasing decisions and brand loyalty formation.

Competitive Landscape:

The Japan spout pouch market features a moderately consolidated competitive structure characterized by the coexistence of established domestic packaging conglomerates and multinational flexible packaging specialists competing across technology innovation, sustainability credentials, and customer relationship depth. Leading participants leverage extensive research and development capabilities to advance mono-material recyclable structures, high-barrier film technologies, and smart packaging integration systems that differentiate their product portfolios. Strategic acquisitions and partnership formations accelerate capability expansion, enabling market leaders to offer comprehensive packaging solutions spanning material development, pouch converting, closure engineering, and automated filling line integration. The competitive intensity is amplified by escalating regulatory requirements that favor technologically advanced manufacturers capable of delivering compliant, recyclable, and performance-optimized packaging solutions. Regional production footprint optimization and supply chain efficiency improvements remain critical competitive differentiators as customers demand shorter lead times, customization flexibility, and consistent quality delivery across diverse application requirements spanning food, beverage, pharmaceutical, and industrial end-use segments.

Japan Spout Pouch Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Caps, Film |

|

Materials Covered |

Plastic, Aluminium, Paper, Others |

|

Pouch Sizes Covered |

Less than 200 ML, 200 to 500 ML, 500 to 1,000 ML, More than 1,000 ML |

|

Closure Types Covered |

Screw Cap, Flip Top Cap |

|

End Users Covered |

Food and Beverages, Cosmetics and Personal Care, Automotive, Pharmaceutical, Paints, Soaps and Detergents, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Spout Pouch Market Report

The Japan spout pouch market size was valued at USD 1,683.25 Million in 2025.

The Japan spout pouch market is expected to grow at a compound annual growth rate of 5.95% from 2026-2034 to reach USD 2,832.24 Million by 2034.

Food and beverages dominated the market with a share of 48.2%, driven by Japan’s extensive convenience food culture, expanding ready-to-eat product offerings, and increasing demand for portable, resealable beverage packaging formats.

Key factors driving the Japan spout pouch market include escalating consumer demand for convenient and portable packaging, regulatory mandates promoting sustainable material transitions, expanding e-commerce distribution channels, and continuous technological innovation.

Major challenges include recycling infrastructure limitations for multi-layer laminate structures, higher unit production costs compared to rigid packaging alternatives, consumer perception barriers regarding premium quality associations, supply chain constraints affecting raw material availability, and the technical complexity of achieving barrier performance parity in mono-material recyclable designs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)