Japan Unified Communications Market Size, Share, Trends and Forecast by Component, Product, Organization Size, End User, and Region, 2026-2034

Japan Unified Communications Market Size & Forecast 2026-2034

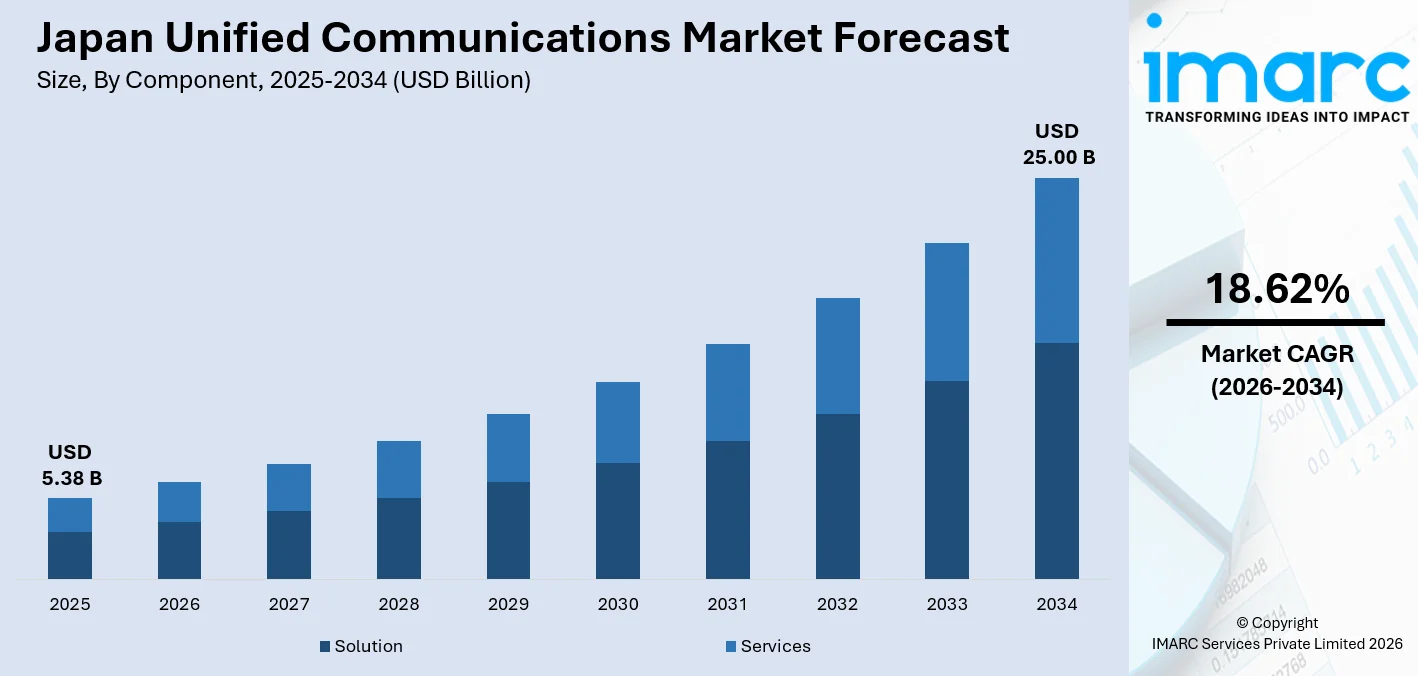

The Japan unified communications market size, valued at USD 5.38 Billion in 2025, is projected to reach USD 25.00 Billion by 2034, growing at a CAGR of 18.62% from 2026-2034, driven by Japan's accelerating shift from legacy on-premises telephony to cloud-hosted UCaaS platforms. For instance, AWS services are used by over half of the Japanese companies utilizing both PaaS and IaaS services, according to a MM Research Institute survey. This is directly propelling Japan unified communications market share.

To get more information on this market Request Sample

Japan Unified Communications Industry Analysis - Key Insights

- Solution owns 62.0% of the component in 2025- the single largest sub-segment within solutions. The explosion of hybrid work and Japan's massive MICE sector has permanently elevated real-time video as the primary enterprise communication modality.

- Hosted commands 55.0% of the market by product in 2025- the majority deployment mode, and is climbing. Cloud economics, near-universal 5G coverage, and Japan's Digital Agency Cloud-First Principle are collectively dismantling the last structural arguments for on-premises infrastructure.

- Large enterprises drive 62.0% of the market by organization size in 2025- reflecting the capital-intensive nature of enterprise-wide UC rollouts and the outsized IT transformation budgets that Japan's largest corporations are committing to digital workplace programs.

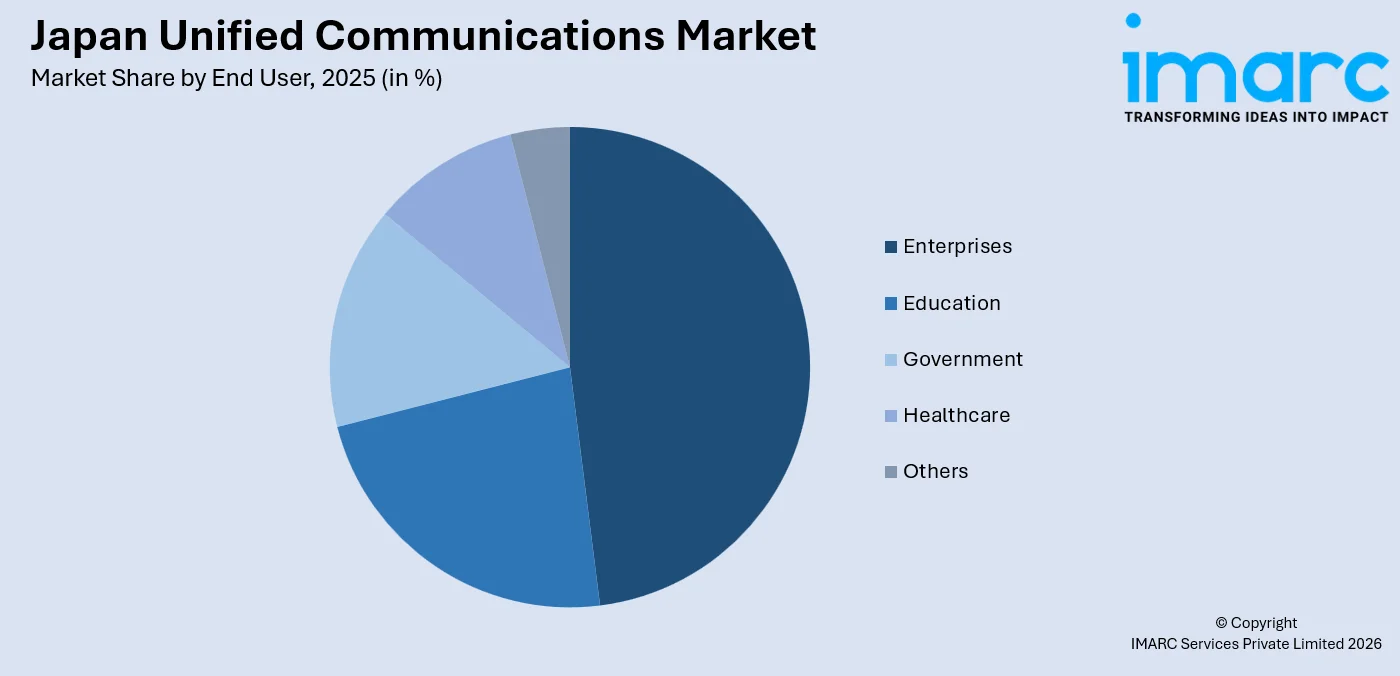

- Enterprises account for 48.0% of end user share in 2025- the dominant vertical, anchored by Japan's large corporate sector and its accelerating migration away from fragmented PBX and email-based workflows toward integrated omni-channel communication platforms.

- Kanto Region leads regionally with 44.0% of the market in 2025- a commanding share driven by Tokyo's concentration of multinational headquarters, major financial institutions, and the highest density of enterprise IT buyers in the country, all at the forefront of UC adoption.

Japan Unified Communications Market Trends and Dynamics 2026

Market Trends

AI-native features are reshaping audio and video conferencing as the enterprise productivity layer

AI capabilities embedded directly into UC platforms are transforming audio and video conferencing from a communication tool into an intelligent productivity layer. Cisco was named a Leader in the 2025 Gartner Magic Quadrant for UCaaS for the 7th consecutive year, with its Webex AI Assistant delivering automated meeting summaries, real-time transcription, live translation, and sentiment analysis natively across the platform.

Cloud-first government mandates accelerating hosted UC adoption across the public sector

Serving as the central authority for Japan’s digital transformation, the Digital Agency initiated the development of a government cloud platform in 2021. The initiative aims to establish a secure, flexible, fast, and cost-efficient cloud infrastructure to support 12 central ministries, 1,788 local government bodies, and various semi-public organizations. In line with government guidelines for the proper use of cloud services in public information systems, the agency is advancing a comprehensive modernization and reform of government cloud utilization across the public sector. This policy-driven shift is one of the most significant structural drivers shaping Japan unified communications market trends as public-sector deployments increasingly convert to cloud-native communication architectures.

Hybrid work institutionalisation is permanently elevating demand for cloud UC infrastructure

Hybrid work has become a permanent organisational structure in Japan: according to the Ministry of Internal Affairs and Communications, as of August 2023, approximately 49.9% of Japanese companies with 100 or more employees adopted telework practices, excluding the public sector.

- UCaaS Platform Consolidation: Enterprises are consolidating fragmented communication tools onto single-vendor UCaaS platforms, reducing integration complexity and driving higher per-seat spending on feature-rich cloud plans.

- 5G-Enabled Edge UC Deployments: Japan's near-universal 5G coverage, with 90% population coverage by 2025, is enabling low-latency edge computing use cases, including real-time AR collaboration and 4K mobile video conferencing.

- Contact Centre-UC Convergence: The boundary between UCaaS and CCaaS is dissolving as vendors integrate customer engagement capabilities directly into unified collaboration suites, driven by enterprise demand for seamless internal and external communication workflows.

- Security and Data Sovereignty Focus: Japan's APPI amendments and Economic Security Promotion Act are compelling enterprises to evaluate UC vendors on in-country data residency, sovereign cloud capability, and ISO/IEC 27001 certification as primary procurement criteria.

Growth Drivers

Hyperscaler investment wave is building cloud infrastructure for enterprise UC workloads

Massive foreign technology investment is underpinning Japan unified communications market growth by building the cloud infrastructure on which hosted UC platforms depend. In April 2024, Microsoft announced a USD 2.9 billion investment in AI and cloud infrastructure in Japan, including training 3 million people in AI skills.

"2025 Digital Cliff" urgency is forcing enterprise legacy system replacements

Japan's Ministry of Economy, Trade and Industry identified that if enterprises fail to modernise legacy IT systems, technical-debt costs could reach JPY 12 trillion annually. This urgency is catalysing large-scale enterprise IT replacements, including legacy PBX and fragmented communication infrastructure, with integrated UC platforms. Large enterprises are committing the largest share of transformation budgets to hosted UC deployments.

Labour shortage driving automation and AI-embedded UC adoption across industries

Japan's structural labour shortage is a powerful systemic driver of UC adoption. With more than 70% of Japanese organisations reporting understaffing in cloud and digital disciplines, enterprises are deploying AI-assisted UC tools, automated call routing, AI-generated meeting summaries, and intelligent transcription to compress communication overhead and maintain productivity without proportional headcount growth. This is accelerating paid seat expansion on feature-rich UCaaS tiers.

- Government Digital Transformation Mandates: METI's financial support for telework tool adoption and the Digital Agency's cloud certification ecosystem are directly subsidising enterprise UC migration costs.

- Expanding SME Cloud Adoption: Japan's SME segment is growing at the fastest pace within UC, driven by affordable subscription-based hosted solutions that eliminate capital infrastructure requirements.

- Healthcare Telemedicine UC Expansion: Rising adoption of telemedicine and virtual consultations is driving healthcare sector investment in HIPAA-compliant, secure UC platforms that integrate voice, video, and patient data systems.

- Microsoft Teams Platform Dominance: Microsoft Teams Phone surpassed 15 million monthly active users, representing a 40% year-over-year growth, and its deep integration with Japan's pervasive Microsoft 365 deployments is driving enterprise-wide UC consolidation onto cloud calling platforms.

Market Restraints

Deep-rooted legacy system entrenchment and organisational resistance to change: Many large Japanese enterprises and government agencies operate entrenched on-premises telephony and communication infrastructure with complex dependencies across internal workflows. Risk-averse organisational cultures and cross-departmental integration challenges create prolonged migration timelines, slowing the velocity of UC adoption even where digital transformation intent is clearly present.

Acute shortage of qualified cloud and UC implementation talent: Japan faces a structural deficit of professionals with the skills to deploy, integrate, and manage complex cloud UC environments. This talent gap extends implementation cycles, raises consultancy costs, and forces organisations to delay or scale back UC rollouts, constraining market growth even among enterprises with committed transformation budgets and clear business cases.

Stringent data sovereignty and regulatory compliance requirements: Japan's evolving data protection framework, including APPI amendments and the Economic Security Promotion Act, imposes strict requirements on where and how communication data is stored and processed. Global UC vendors must invest substantially in local data residency and sovereign cloud capabilities, adding complexity to deployments and narrowing the field of fully compliant platform options available to regulated industries.

Japan Unified Communications Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Component |

Solution |

62.0% |

2025 |

|

Product |

Hosted |

55.0% |

2025 |

|

Organization Size |

Large Enterprises |

62.0% |

2025 |

|

End User |

Enterprises |

48.0% |

2025 |

|

Region |

Kanto Region |

44.0% |

2025 |

Component Insights

Solution - 62.0% Market Share (2025) | Leading Component

Audio and video conferencing is the dominant subsegment of Japan's unified communications solutions landscape, a position cemented by the hybrid work revolution that has made video calls the default mode of enterprise collaboration. Japan's MICE sector, meetings, incentives, conferences, and exhibitions, represents one of Asia's largest concentrated demand pools for enterprise video infrastructure, with major corporations in Tokyo, Osaka, and Nagoya running continuous virtual and hybrid event formats.

|

Segment Breakdown Solution – (Audio and Video Conferencing, Instant and Unified Messaging, IP Telephony, and Others) (62.0%) · Services – (Professional Services and Managed Services) |

Product Insights

Hosted - 55.0% Market Share (2025) | Leading Product

Hosted UC decisively overtaken on-premises deployment in Japan, driven by the convergence of government cloud mandates, hyperscaler infrastructure investment, and the accelerating exit of legacy on-premises vendors. Microsoft Azure, AWS, Google Cloud, Oracle, and Sakura Internet are some of the government cloud-certified vendors, and all their enterprise communication workloads run on hosted architectures.

|

Segment Breakdown Hosted (55.0%) · On-premises |

Organization Size Insights

Large Enterprises - 62.0% Market Share (2025) | Leading Organization Size

Large enterprises command the Japan unified communications market through their ability to deploy enterprise-wide UC transformation programs at scale. Mizuho Financial Group, one of Japan's major banking institutions, earmarked JPY 100 billion for a multi-cloud marketing and communications engine in 2025, illustrating the magnitude of enterprise-grade UC investments flowing through Japan's corporate sector. Japan's "2025 Digital Cliff" urgency is producing a distinctive pattern in large enterprise UC procurement: organisations are not simply migrating existing telephony to cloud equivalents, but deploying fully integrated UC suites that converge voice, video, messaging, and contact centre capabilities on a single platform.

|

Segment Breakdown Large Enterprises (62.0%) · Small and Medium-sized Enterprises |

End User Insights

Access the comprehensive market breakdown Request Sample

Enterprises - 48.0% Market Share (2025) | Leading End User

Enterprises are the primary engine of Japan's unified communications market, spanning financial services, manufacturing, retail, IT services, and logistics, all sectors with complex, multi-site communication infrastructure requirements that UC platforms are purpose-built to address. Large enterprises with over 1,000 employees are deploying an average of 177 SaaS applications, each requiring integration with centralised communication platforms.

|

Segment Breakdown Enterprises (48.0%) · Education · Government · Healthcare · Others |

Regional Insights

Kanto Region - 44.0% Market Share (2025) | Leading Region

Kanto's dominance in Japan's unified communications market is structurally anchored by Tokyo's role as the headquarters city for virtually every major Japanese corporation. Japan's Digital Agency is headquartered in Tokyo at the Kioicho district in Chiyoda Ward, and its Government Cloud procurement framework directly shapes public-sector UC adoption across ministries headquartered in the region. In April 2024, Microsoft's USD 2.9 billion Japan investment, which includes training 3 million people in AI skills and building new research infrastructure, was centred on its Tokyo operations, reinforcing Kanto's position as Japan's deepest enterprise UC market.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 44.0% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | Government digital agency mandates, corporate headquarters concentration, hyperscaler data centre investment, financial sector UC transformation |

| Outlook | Dominant region, deepening AI-embedded UC penetration |

|

Regional Breakdown Kanto Region (44.0%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai/Kinki Region, centred on Osaka and Kyoto, is Japan's second-largest UC market, driven by the strong presence of manufacturing conglomerates, pharmaceutical companies, and a growing startup technology ecosystem. Osaka was also the site of the 2025 World Expo, which attracted major technology deployments and international business activity, directly stimulating enterprise communications upgrades across the region.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga prefectures |

| Key Growth Drivers | Manufacturing sector digital transformation, Osaka Expo 2025 enterprise activity, pharmaceutical and biotech UC adoption |

| Outlook | Strong second region, industrial-digital UC convergence |

Central/Chubu Region:

The Central/Chubu Region, centred on Nagoya, Japan's automotive and advanced manufacturing heartland, is emerging as a high-growth UC market driven by Industry 4.0 transformation programs. The Japan SaaS market projects Nagoya as the fastest-growing regional market through 2035, driven by the automotive sector's electric vehicle and IoT convergence programs.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Automotive sector Industry 4.0 programs, EV and IoT convergence, manufacturing AI platform deployments |

| Outlook | Fastest-growing region through industrial digitalisation |

Kyushu-Okinawa Region:

Kyushu-Okinawa is expanding its UC footprint through semiconductor and semiconductor-adjacent manufacturing investments that have made the region, particularly Kumamoto, a major new industrial cluster. TSMC's Kumamoto fab, which began operations in 2024, catalysed supplier ecosystem buildout across the region, creating a concentrated new corporate user base for enterprise UC platforms as hundreds of associated manufacturers upgrade communication infrastructure to support expanded operations and international supply chain coordination.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto prefectures |

| Key Growth Drivers | Semiconductor cluster development, new manufacturing enterprise UC buildouts, Fukuoka tech startup ecosystem |

| Outlook | Growing industrial cluster driving UC infrastructure investment |

Tohoku Region:

Tohoku's UC market is expanding as rural broadband infrastructure improvements and government-backed telework promotion programs bring cloud communication tools to manufacturers, municipalities, and healthcare providers outside major urban centres. Hybrid-friendly co-working spaces are opening across Sendai, and broadband expansion programs are raising baseline connectivity quality to levels that support hosted video conferencing and VoIP, broadening the addressable enterprise and government UC market across the region.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima prefectures |

| Key Growth Drivers | Rural broadband expansion, government telework promotion, municipal digital transformation programs |

| Outlook | Government-led broadband enabling gradual hosted UC uptake |

Market Outlook (2026-2034)

What is the future outlook of the Japan unified communications market?

The Japan unified communications market is expected to sustain steady revenue growth through 2034.

The convergence of AI embedding across UC platforms, Japan's structural labour shortage driving automation-first communication strategies, and the government's unwavering commitment to cloud-first infrastructure will sustain the market's strong CAGR through the forecast period. As SME cloud adoption accelerates, Japan's SME segment cloud adoption is advancing, and the addressable UC market will broaden substantially beyond large enterprises, creating a second growth wave that extends the market expansion trajectory well into the early 2030s.

Japan Unified Communications Market - Leading Key Players

The Japan unified communications market is served by a mix of global platform vendors with deep Japan enterprise penetration and domestic technology champions with strong government and public-sector relationships.

| Company | Leading Products | Highlights |

|---|---|---|

|

Avaya LLC |

Avaya Aura, Avaya Cloud Office, Avaya Aura Private Cloud, Avaya IP Office | Navigating strategic transition from bankruptcy, AI-agnostic orchestration allows enterprise clients to integrate custom AI models into Aura/Aura Elite voice environments |

|

Cisco Systems Inc. |

Cisco Business Edition 7000, Cisco Hosted Collaboration Solution (HCS), Webex for Cisco BroadWorks | Named Gartner UCaaS Magic Quadrant Leader for 7th consecutive year in 2025. |

|

NEC Corporation |

UNIVERGE BLUE UCaaS, UNIVERGE CONNECT, NEC BLUE AI ASSISTANT | Launched UNIVERGE BLUE AI ASSISTANT with generative AI, transcription, and sentiment analysis |

Some of the key market players in the Japan unified communications market are Microsoft, Fujitsu, Mitel, Vonage (Telefonaktiebolaget LM Ericsson), etc.

Latest Development & News

- In October 2025, NEC Corporation announced the acquisition of CSG International for USD 2.9 billion or JPY438.5 billion, including debt, a major move to expand NEC's enterprise software portfolio as it pivots away from legacy on-premises UC toward cloud-native business systems. The acquisition reflects NEC's broader strategic repositioning toward managed services and cloud software.

- In April 2024, Microsoft announced a USD 2.9 billion investment to expand AI and cloud infrastructure in Japan, inclusive of plans to train 3 million people in AI skills, open a new research laboratory, and boost cybersecurity capabilities in partnership with the Japanese government. The investment directly supports Microsoft Teams and Azure Communications Services deployments, reinforcing Microsoft's position as the dominant productivity and unified communications platform across Japan's enterprise and public-sector organisations and accelerating the hosted UC market's growth trajectory.

Japan Unified Communications Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Products Covered | On-premises, Hosted |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| End Users Covered | Enterprises, Education, Government, Healthcare, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Avaya LLC, Cisco Systems Inc., NEC Corporation (AT&T Inc.), Vonage (Telefonaktiebolaget LM Ericsson), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan unified communications market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan unified communications market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan unified communications industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Unified Communications Market Report

The Japan unified communications market reached a value of USD 5.38 Billion in 2025.

The market is projected to grow at a CAGR of 18.62% during 2026-2034, reaching USD 25.00 Billion by 2034.

Key growth drivers include the accelerating shift to remote and hybrid work, rising demand for seamless multi-channel collaboration tools, rapid 5G network proliferation, growing need for cost-efficient integrated communication platforms, and increasing integration of UC with CRM systems and data analytics to enhance customer service delivery.

The report covers segmentation by component, product, organization size, end user, and region. Each segment includes detailed market size and forecast analysis.

Major players in the Japan unified communications market include Avaya LLC, Cisco Systems Inc., NEC Corporation (AT&T Inc.), Vonage (Telefonaktiebolaget LM Ericsson), etc.

Key trends include rapid adoption of hosted and cloud-based UC platforms, growing integration of 5G-enabled real-time communication capabilities, increasing convergence of UC with CRM and business analytics tools, and rising demand for unified messaging and video conferencing across enterprise, healthcare, and government sectors in Japan.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)