Japan Used Car Market Size, Share, Trends and Forecast by Vehicle Type, Vendor Type, Fuel Type, Sales Channel, and Region, 2026-2034

Japan Used Car Market Size, Share, Trends & Forecast (2026-2034)

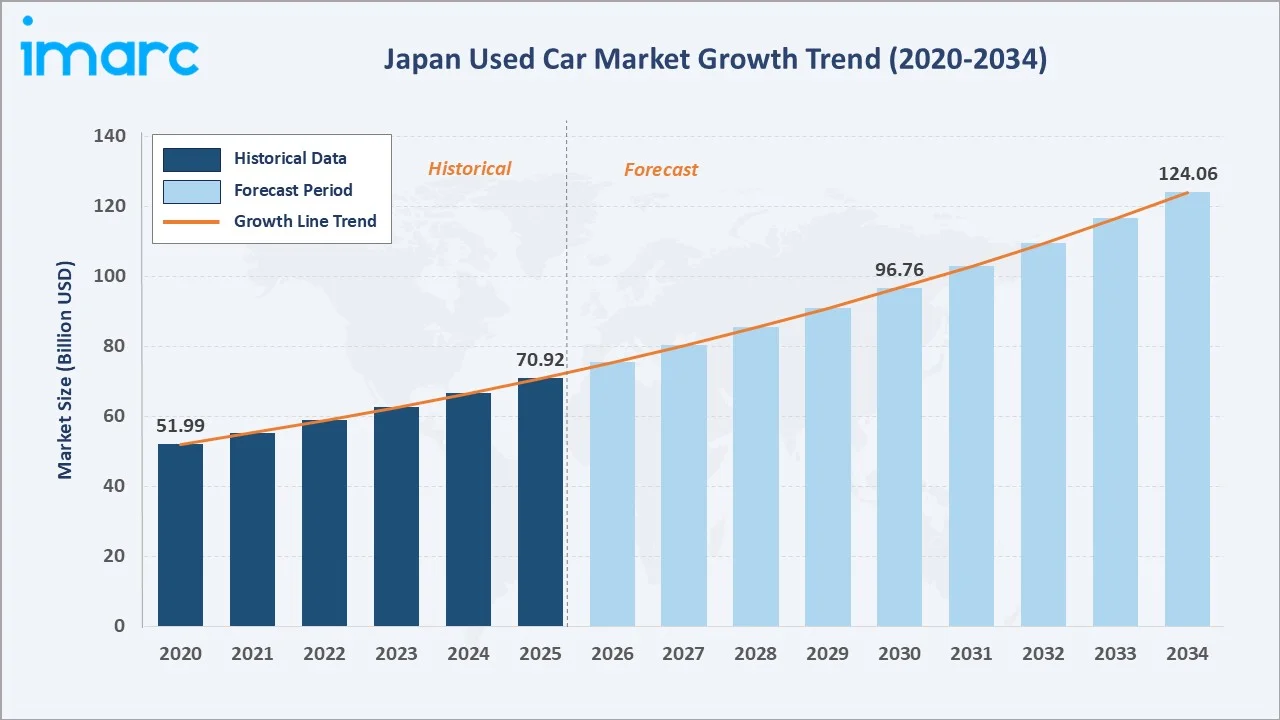

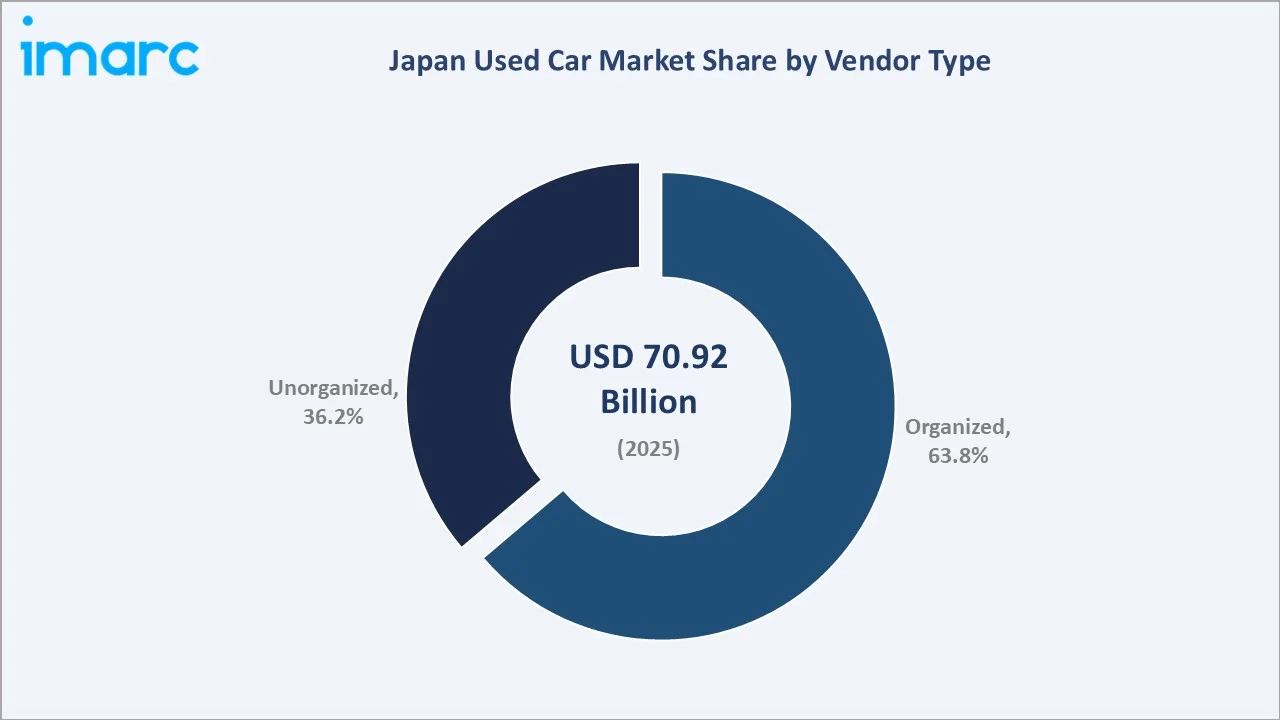

The Japan used car market reached USD 70.92 Billion in 2025 and is projected to reach USD 124.06 Billion by 2034, growing at a CAGR of 6.41% during 2026-2034. Prolonged new vehicle shortages from semiconductor supply disruptions driving consumers to the used market, Japan's globally trusted Shaken vehicle inspection system underpinning used car quality confidence, surging export demand from Africa, South Asia, and the Middle East, and the rapid growth of AI-powered digital auction and retail platforms are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 70.92 Billion |

|

Forecast Market Size (2034) |

USD 124.06 Billion |

|

CAGR (2026-2034) |

6.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

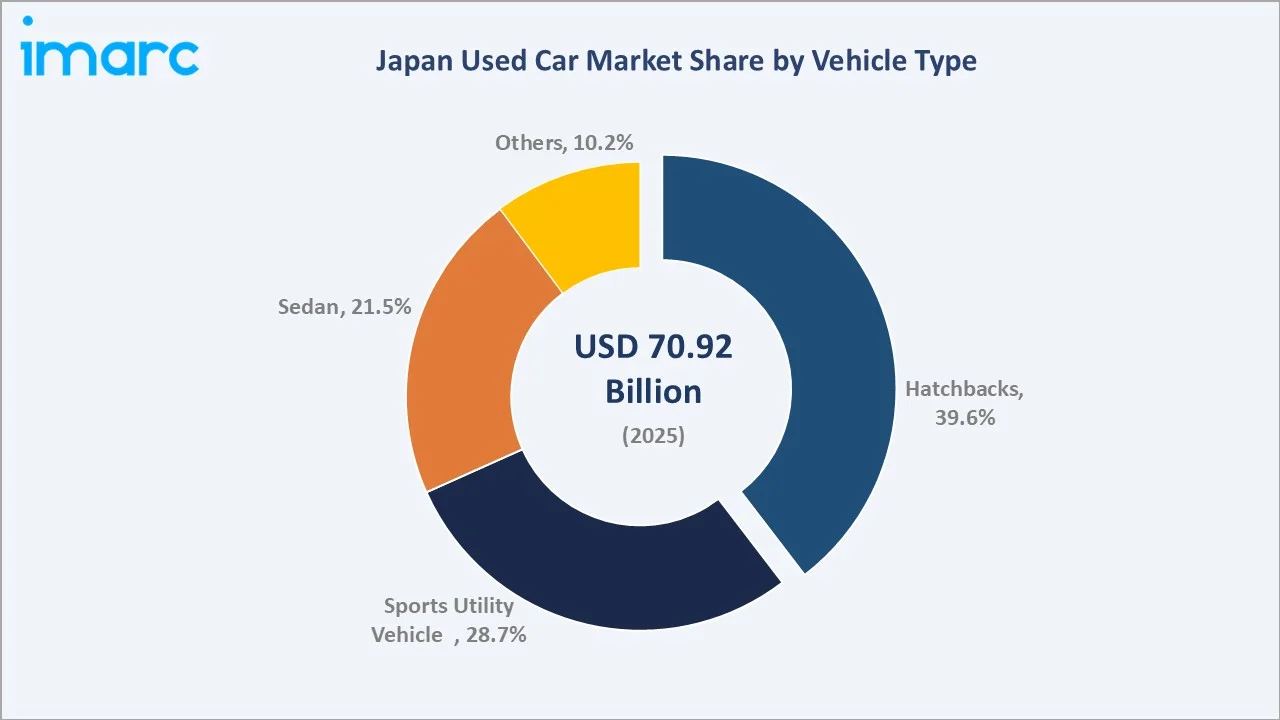

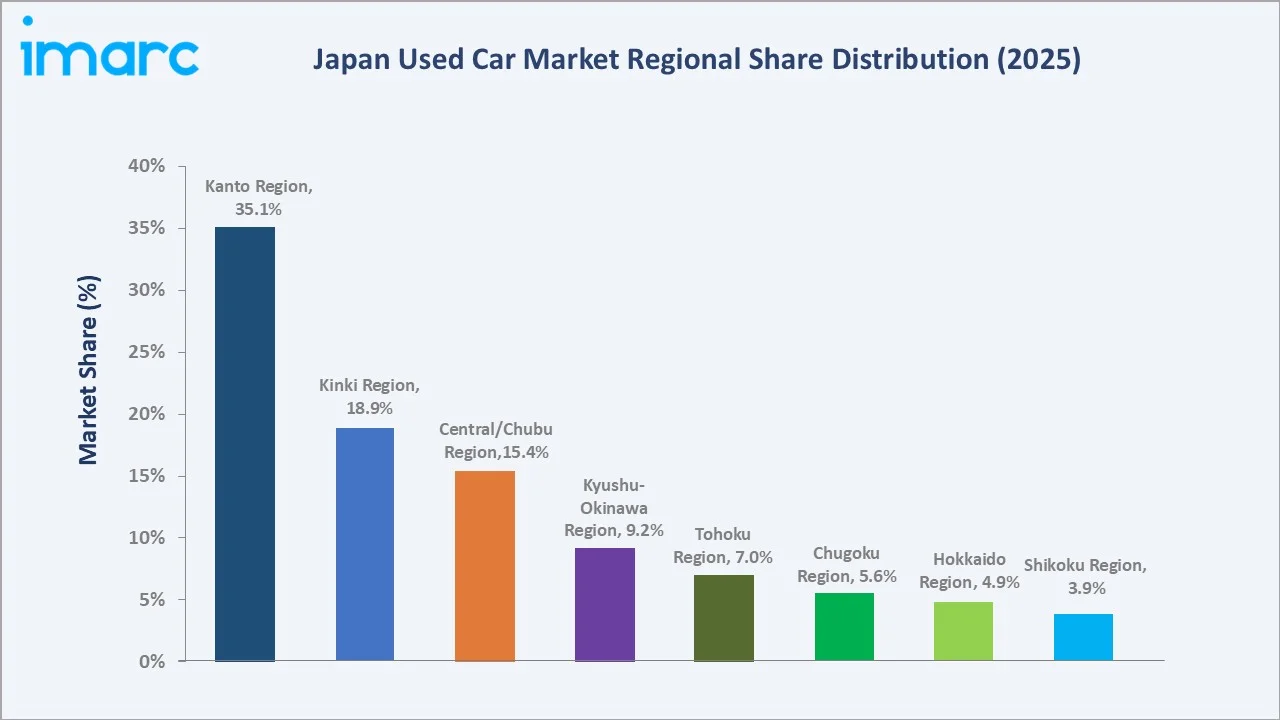

The Kanto Region leads nationally with a 35.1% share in 2025, anchored by Greater Tokyo's massive dealer concentration and the USS auction network's dominant Kanto facilities. Organized vendors command 63.8% of the market, while hatchbacks are the leading vehicle type at 39.6%, reflecting Japan's strong preference for compact, fuel-efficient city cars in a densely urbanized market where narrow roads and high parking costs favor smaller body styles.

To get more information on this market, Request Sample

The Japan used car market is underpinned by three structural forces: the unique quality certification infrastructure of the Shaken inspection system that maintains used vehicle standards well above global comparators, creating deep domestic and international buyer trust; the persistent affordability gap between new and used vehicles directing budget-sensitive buyers to the pre-owned market; and Japan's position as the world's premier source of right-hand-drive quality used vehicles for export markets across Asia, Africa, and Oceania.

Executive Summary

The Japan used car market is experiencing sustained growth, driven by structural affordability pressures, global export demand for Japanese quality vehicles, and the digital transformation of vehicle sourcing and retailing. The market was valued at USD 70.92 Billion in 2025 and is forecast to reach USD 124.06 Billion by 2034 at a CAGR of 6.41%.

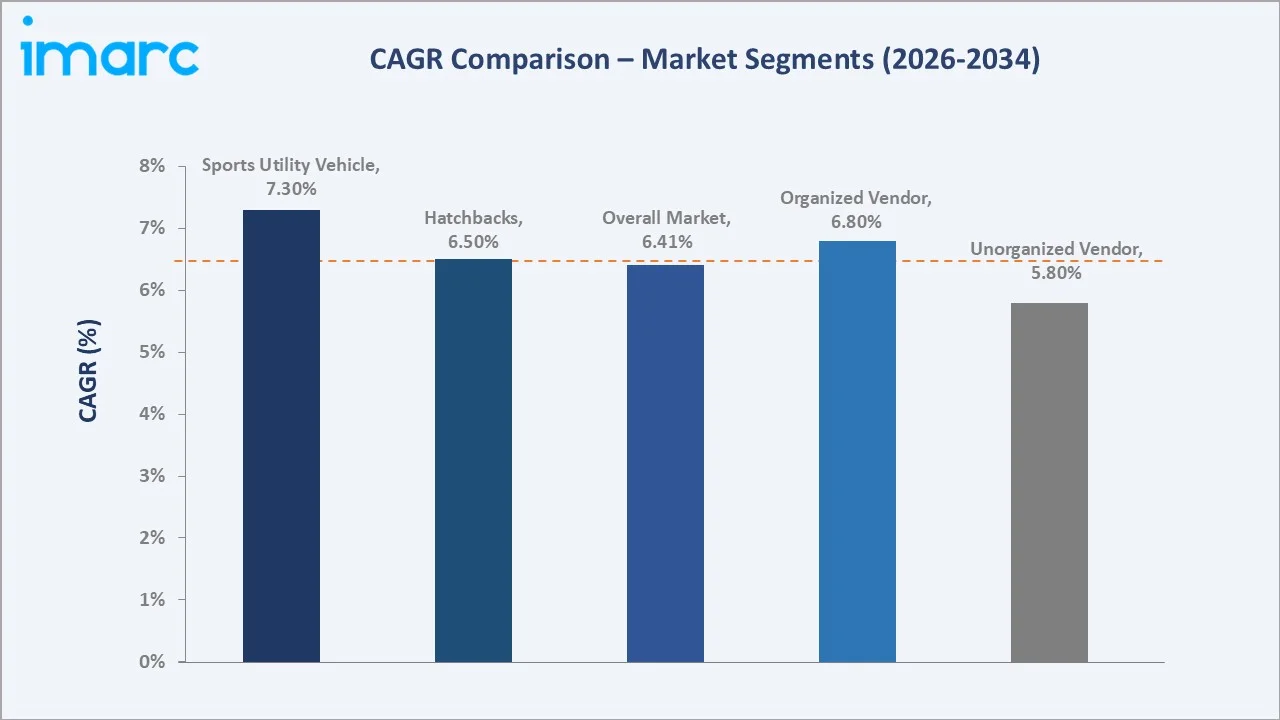

Organized vendors dominate at 63.8% of market share in 2025, reflecting Japan's progressive regulatory environment requiring certified dealer licensing, consumer protection guarantees, and Shaken compliance documentation, standards that unorganized vendors struggle to meet consistently. Unorganized vendors at 36.2% serve price-sensitive consumers through private-party transactions, kei-car local dealers, and smaller regional auction operators.

Hatchbacks lead vehicle type at 39.6%, driven by Japan's urban demographics where compact body styles navigate narrow city streets, fit standard parking spaces, and achieve superior fuel economy. Sports Utility Vehicles at 28.7% are the fastest-growing vehicle type, reflecting Japan's lifestyle shift toward larger family vehicles and the growing popularity of premium used SUVs from Toyota, Honda, and Nissan in suburban and rural regions.

Key Market Insights

|

Insight |

Data |

| Largest Vendor Type |

Organized – 63.8% share (2025) |

| Fastest Growing Vendor Type |

Organized – ~6.8% CAGR (2026-2034) |

| Largest Vehicle Type |

Hatchbacks – 39.6% share (2025) |

| Fastest Growing Vehicle Type |

Sports Utility Vehicle – ~7.3% CAGR (2026-2034) |

| Leading Region |

Kanto Region – 35.1% share (2025) |

| Top Companies |

USS Co., Ltd., IDOM Inc., ORIX Corporation, SBT CO., LTD. |

Key Analytical Observations Supporting The Above Data:

- Organized vendors account for 63.8% of Japan's used car market in 2025, reflecting the progressive consolidation of the Japanese used car retail landscape around certified dealership chains and digital auction platforms.

- Hatchbacks dominate vehicle type at 39.6% (2025), encompassing both conventional hatchbacks and the uniquely Japanese kei-car category. Honda N-BOX and Suzuki Spacia consistently top Japan's monthly registration charts, generating a continuous supply of trade-in and lease-return hatchbacks into the used market at price points of JPY 500,000–1,500,000 that serve Japan's large cost-conscious consumer base.

- Kanto Region's 35.1% national leadership (2025) reflects Greater Tokyo's position as Japan's largest population center, highest average vehicle ownership per household, and the concentration of Japan's largest used car auction facilities. Tokyo's active lease-return and corporate fleet turnover creates a continuous supply of high-quality 3–5 year-old used vehicles that sustain the Kanto region's dominant auction and retail volumes.

Japan Used Car Market Overview

Japan's used car market is the world's most structured and quality-assured pre-owned vehicle ecosystem, underpinned by the mandatory Shaken vehicle inspection system that requires all vehicles to pass rigorous safety and emissions testing every two years. The Shaken system creates a uniquely transparent and quality-standardized used vehicle supply that builds exceptional buyer confidence in Japanese used vehicles both domestically and internationally.

The market spans domestic retail through organized dealer networks, peer-to-peer private transactions, and physical and digital auction platforms, with the auction channel being particularly distinctive to Japan's used car ecosystem. Japan's vehicle auction network processes millions of used vehicles annually, providing price discovery and liquidity that underpins both domestic retail and export market supply chains.

Market Dynamics

To evaluate market opportunities, Request Sample

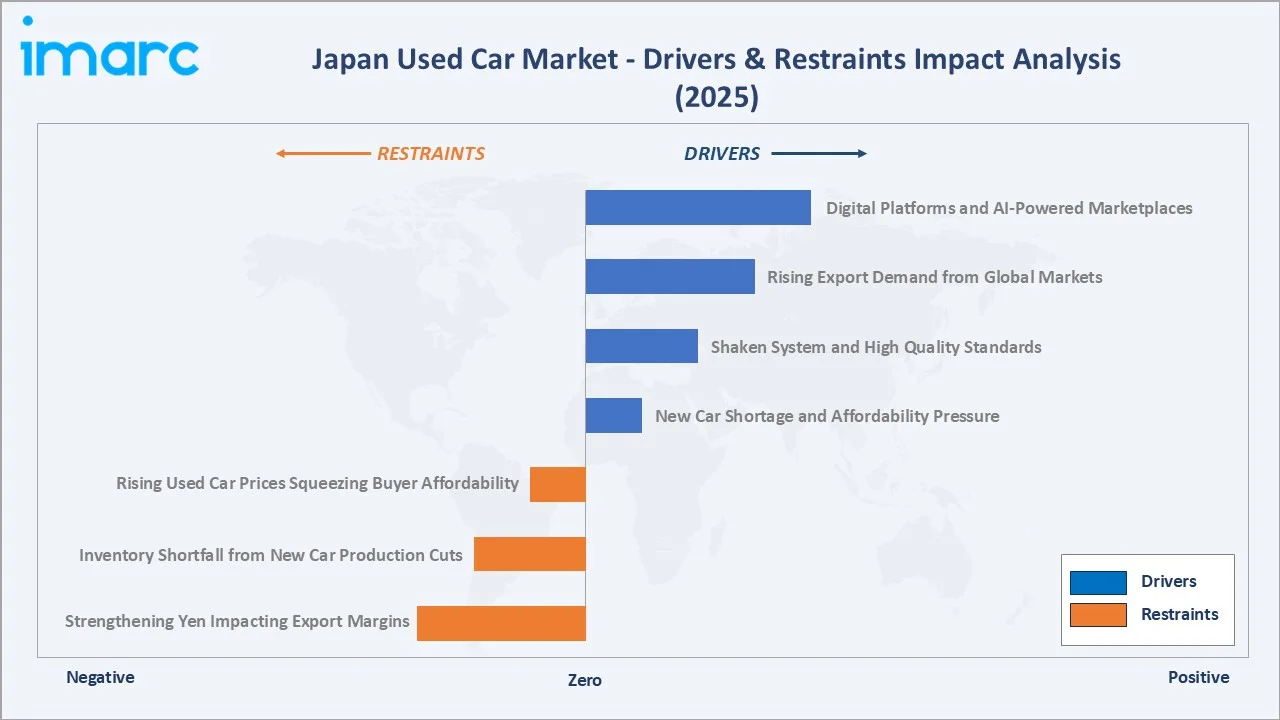

Market Drivers

- New Car Shortage and Affordability Pressure: Semiconductor supply chain disruptions are creating extended new car delivery timelines of 6–18 months across popular models, driving consumers who need immediate vehicle access toward used alternatives. USS Co. Ltd. noted March 2025 average auction prices exceeding JPY 1.26 millionas demand pressure from consumers avoiding long new car waits elevated used car prices.

- Shaken System and High Quality Standards: Japan's mandatory biennial vehicle inspection, the Shaken system, is the market's most powerful structural driver, creating a quality-standardized supply of used vehicles that commands buyer premiums globally. From April 2025, inspection periods were extended to two months before expiry, reducing administrative burden while maintaining compliance standards.

- Rising Export Demand from Global Markets: Japan is one of the world's largest exporters of right-hand-drive quality used vehicles, with export destinations spanning Africa, South Asia, Southeast Asia, and Oceania. In 2025–2026, USS auction data showed sustained international buyer participation maintaining sell-through rates above 70%, reflecting export market demand growing at pace with domestic supply expansion.

- Digital Platforms and AI-Powered Marketplaces: Japan's used car digital platforms are rapidly expanding the market's reach and efficiency. AI-driven vehicle inspection systems using deep learning algorithms identify scratches, dents, and wear patterns through image analysis, cutting inspection time while improving accuracy. Predictive pricing models processing auction data, specifications, and condition reports generate transparent fair market valuations that reduce information asymmetry between buyers and sellers.

Market Restraints

- Rising Used Car Prices Squeezing Buyer Affordability: The same semiconductor-driven new car shortage that redirected buyers to the used market also elevated used car prices substantially, with USS auction average winning prices reaching JPY 1.23 million in 2025, a significant increase from pre-shortage levels. While this price inflation benefits vendors and auction operators, it erodes the affordability advantage that the used market holds over new vehicles for budget-sensitive buyers.

- Inventory Shortfall from New Car Production Cuts: Japan produced 7.84 million motor vehicles in 2021, marking the third consecutive year of production decline. This shortfall of vehicles produced during that period is now creating a gap in the 3–5 year-old used car cohort. With fewer trade-ins and lease returns entering the auction pipeline from the 2021 production trough, wholesale price pressures are sustained even as dealer networks seek to maintain inventory levels.

- Strengthening Yen Impacting Export Margins: Japan's used car export market is sensitive to the USD/JPY exchange rate, as export buyers' purchasing power in yen-denominated Japanese auctions fluctuates with currency movements. Periods of yen appreciation reduce the affordability of Japanese used vehicles for African, Asian, and Pacific export buyers who operate in USD or local currencies pegged to the dollar.

Market Opportunities

- Electric Vehicle Used Car Market Development: Japan's growing EV fleet is creating an emerging used EV segment that is projected to grow at 14%+ CAGR through 2031. Battery health certification standards, government subsidy-informed used EV pricing benchmarks, and growing consumer familiarity with EV ownership are progressively building the infrastructure for a vibrant used EV market.

- OEM Certified Pre-Owned Program Expansion: Toyota Certified Used Cars, Honda Auto Terrace, Nissan Intelligent Choice, and Mazda's certified pre-owned program are expanding their inspection standards, warranty coverage, and retail network footprint, creating a premium organized segment within used car retail that captures quality-conscious buyers willing to pay 10–20% premiums for OEM certification.

Market Challenges

- Regulatory Compliance and Documentation Burden: Japan's Used Motor Vehicle Dealer Act requires comprehensive transaction documentation, consumer protection guarantees, and Shaken compliance tracking that creates significant administrative overhead for dealer operations. The Act's mandatory disclosure requirements for vehicle defect history, accident records, and odometer readings require dealer investment in inspection technology and documentation systems that constrain the speed and cost-efficiency of high-volume used car retail operations, particularly for smaller regional dealers.

- Consumer Trust Deficit from BIGMOTOR Scandal: The BIGMOTOR insurance fraud scandal damaged consumer trust in the used car industry broadly and created regulatory scrutiny that increased compliance requirements and consumer due diligence expectations across the sector. While BIGMOTOR's business was restructured as WECARS Co. Ltd. in May 2024 under ITOCHU Corporation and ITOCHU ENEX Co. Ltd. ownership (partnership with J-Will Partners Co. Ltd.), rebuilding industry-wide consumer trust requires sustained investment in transparent inspection practices and customer protection programs across the entire organized dealer sector.

Emerging Market Trends

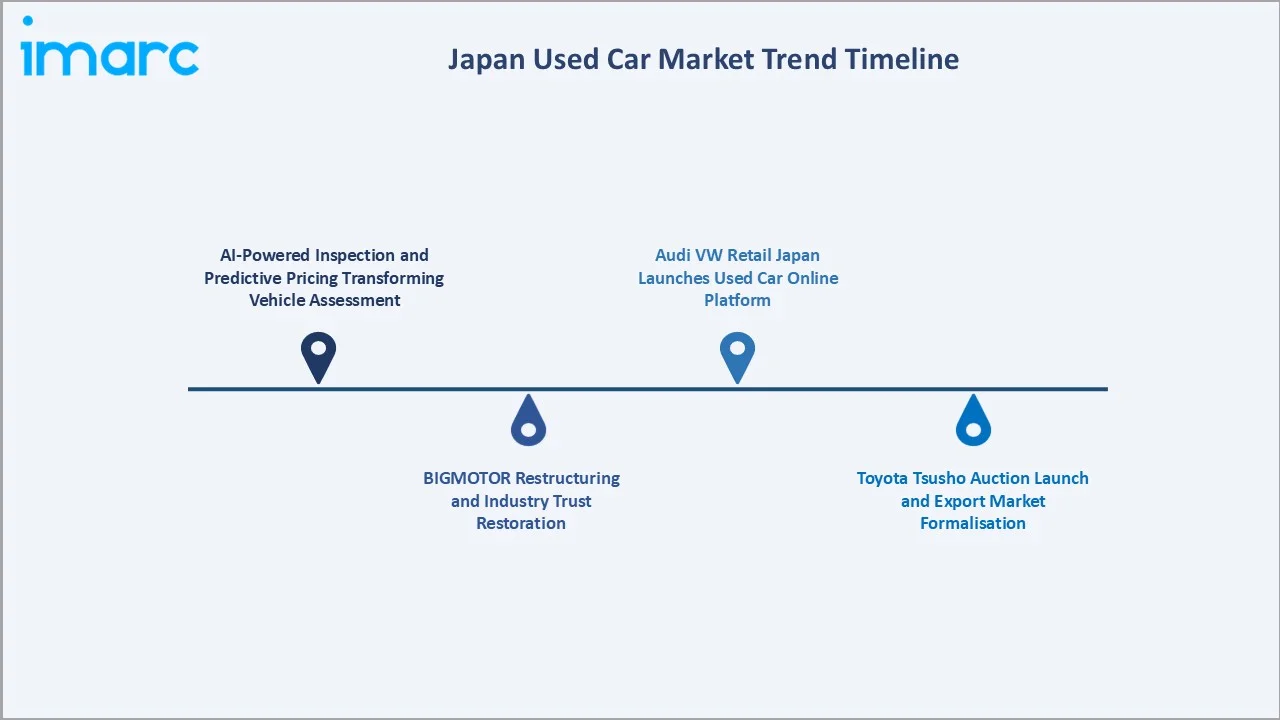

1. AI-Powered Inspection and Predictive Pricing Transforming Vehicle Assessment

AI and computer vision are rapidly transforming vehicle inspection and pricing across Japan's used car market. Ravin AI's DeepDetect technology is now operational at Japanese dealerships and auction houses, using deep learning algorithms to identify scratches, dents, and wear patterns through image analysis, cutting inspection time from 30–45 minutes to 5–10 minutes while improving condition grading consistency.

2. BIGMOTOR Restructuring and Industry Trust Restoration

In May 2024, ITOCHU Corporation and ITOCHU ENEX Co. Ltd. established WECARS Co. Ltd. through the acquisition of all BIGMOTOR businesses and subsidiaries, in partnership with J-Will Partners Co. Ltd. The restructuring under established corporate governance represents the industry's most significant consolidation event of the decade. WECARS has implemented comprehensive vehicle inspection transparency, mandatory disclosure of all inspection results, and customer complaint management systems, setting new standards for organized dealer compliance that are influencing industry-wide practice.

3. Toyota Tsusho Auction Launch and Export Market Formalization

In October 2024, Toyota Tsusho Corporation unveiled plans to launch Toyota Tsusho Auction (TTA), a new service specifically aimed at providing insights into used car auctions for export market purposes. TTA's launch signals the formalization of export market demand as a strategic priority for Japan's automotive trading companies, with structured data services, export market intelligence, and sourcing facilitation being offered alongside traditional vehicle trading.

4. Audi VW Retail Japan Launches Used Car Online Platform

In March 2025, Audi VW Retail Japan (AVRJ) unveiled 'Outlet Cars', a dedicated online platform for used vehicles traded at AVRJ dealerships. The service focuses on vehicles traded in at AVRJ's network, bringing premium European brand certified pre-owned vehicles into Japan's digital retail ecosystem with OEM-certified quality standards, transparent pricing, and online purchase capability.

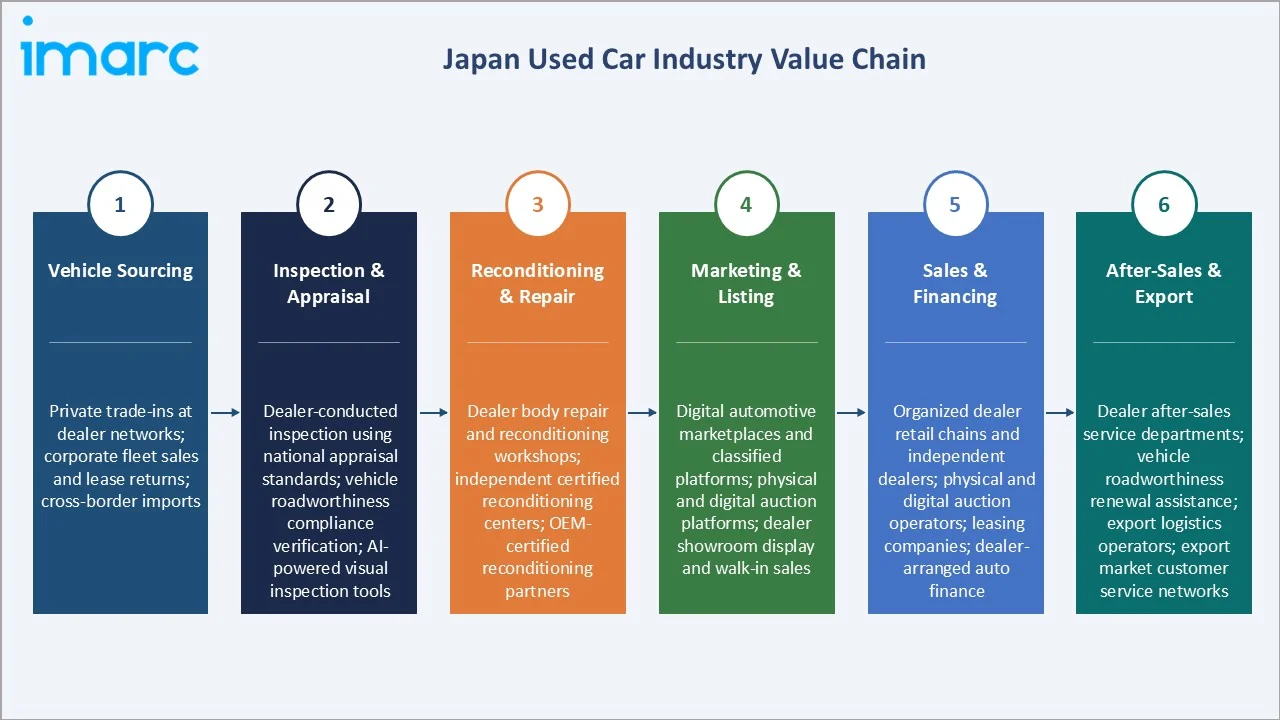

Industry Value Chain Analysis

Japan's used car value chain spans vehicle sourcing from domestic trade-ins, lease returns, and imports through final retail sale or export, with the auction platform playing a distinctive intermediary role unique to the Japanese market structure.

|

Stage |

Key Players / Examples |

| Vehicle Sourcing |

Private trade-ins at dealer networks; corporate fleet sales and lease returns; cross-border imports |

| Inspection & Appraisal |

Dealer-conducted inspection using national appraisal standards; vehicle roadworthiness compliance verification; AI-powered visual inspection tools |

|

Reconditioning & Repair |

Dealer body repair and reconditioning workshops; independent certified reconditioning centers; OEM-certified reconditioning partners |

| Marketing & Listing |

Digital automotive marketplaces and classified platforms; physical and digital auction platforms; dealer showroom display and walk-in sales |

| Sales & Financing |

Organized dealer retail chains and independent dealers; physical and digital auction operators; leasing companies; dealer-arranged auto finance |

| After-Sales & Export |

Dealer after-sales service departments for domestic retail buyers; vehicle roadworthiness renewal assistance; export logistics operators; export market customer service networks |

Technology Landscape in the Japan Used Car Industry

AI-Powered Vehicle Inspection and Condition Grading

Artificial intelligence is transforming the vehicle inspection and grading process that underpins Japan's used car market quality infrastructure. Ravin AI's DeepDetect platform, now deployed at Japanese dealerships, auctions, and fleet operations, uses computer vision models trained on millions of vehicle images to detect exterior damage. This technology is being integrated with Japan's established auction grade reporting system to provide standardized, AI-verified grade reports that reduce subjective variation between human appraisers and create more reliable price benchmarks across the auction ecosystem.

Digital Auction Platforms and Online Retail Marketplaces

USS Co. Ltd.'s digital auction system enables registered dealers across Japan and internationally to bid on vehicles remotely without physical attendance at USS's nationwide auction facilities, dramatically expanding the buyer base and liquidity of Japan's auction ecosystem. On the retail side, PROTO Corporation's Goo-net and Recruit Holdings' Car Sensor platform collectively aggregate hundreds of thousands of used vehicle listings, reducing geographic constraints on used car purchasing and enabling price comparison across the organized dealer network.

OBD Diagnostics and Shaken System Modernisation

October 2024's introduction of On-Board Diagnostics (OBD) testing as a component of the Shaken inspection process represents the system's most significant technical upgrade in decades. OBD testing electronically reads vehicles' onboard diagnostic systems, adding a standardized digital verification layer to the inspection process. This modernization reduces the risk of vehicles with concealed electronic defects passing visual inspection and has elevated the technical threshold for used vehicles to meet Shaken compliance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Vendor Type | Organized |

63.8% |

2025 |

|

Vehicle Type |

Hatchbacks |

39.6% |

2025 |

| Fuel Type |

🔒 |

🔒 |

2025 |

| Sales Channel |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

35.1% |

2025 |

By Vendor Type

The vendor type segment is analyzed across organized (63.8%) and unorganized (36.2%). Organized vendors dominate, reflecting Japan's progressive regulatory environment favoring licensed dealers with consumer protection guarantees, transparent pricing, and documented Shaken compliance, standards that are progressively consolidating market share away from unorganized operators who cannot match these compliance capabilities at scale.

To access detailed market analysis, Request Sample

Unorganized vendors at 36.2% comprise private-party transactions, small local kei-car dealers, regional independent dealers without national certification, and smaller auction operators outside the USS/Aucnet ecosystem, serving price-sensitive buyers who accept reduced documentation and consumer protection in exchange for lower transaction prices.

By Vehicle Type

The vehicle type segment is led by hatchbacks (39.6%), followed by sports utility vehicle (28.7%), sedans (21.5%), and others (10.2%). Hatchbacks' dominance encompasses both conventional hatchbacks and Japan's unique kei-car category, with kei-cars individually representing the top-selling individual models in Japan's monthly used car registration data.

Sports Utility Vehicle encompasses everything from compact crossovers to premium mid-size SUVs, with growing affluence and lifestyle shift toward outdoor recreation driving above-average SUV demand in Japan's used market. Sedans predominantly serve corporate buyers, older demographic segments, and export markets where sedan body styles remain highly popular.

Regional Market Insights

Kanto Region's 35.1% national leadership in 2025 reflects Greater Tokyo's position as Japan's largest and most active used car market, hosting the highest concentration of licensed dealers, the most active auction facilities, and the largest single concentration of lease-returning and fleet-turnover vehicles in Japan.

Japan's second-largest used car market, Kinki Region, is anchored by Osaka's commercial and industrial base, Kobe's port access for export, and the region's industrial base that generates substantial corporate fleet vehicle turnover that enters the used market through dealer buy-back programs and auctions.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

35.1% |

Corporate fleet and lease-return vehicle supply; highest household vehicle ownership turnover; international export buyer access through Yokohama port |

|

Kinki Region |

18.9% |

Osaka-Kyoto-Kobe dealer networks; Osaka port export logistics; corporate fleet vehicle supply; affluent Kobe and Kyoto consumer demographic; USS Osaka auction facility |

|

Central/Chubu Region |

15.4% |

Nagoya automotive manufacturing corporate fleet turnover; Toyota Group employee vehicle supply; active domestic demand driven by industrial worker income levels |

|

Kyushu-Okinawa Region |

9.2% |

Fukuoka used car retail hub; Hakata port export access; Okinawa unique vehicle demand from US base proximity; growing domestic consumption as semiconductor and automotive investment elevates regional incomes |

|

Tohoku Region |

7.0% |

Post-disaster recovery vehicle replacement demand; Sendai used car hub; growing agricultural and construction sector vehicle demand; value-oriented consumer base favoring affordability of used alternatives |

|

Chugoku Region |

5.6% |

Hiroshima Mazda corporate fleet vehicle supply; Hiroshima port export access; regional industrial consumption; balanced urban-rural demand profile |

|

Hokkaido Region |

4.9% |

Cold climate vehicle requirements driving 4WD and AWD used car demand; Sapporo urban dealer concentration; agricultural sector vehicle demand; Tomakomai port used car export activity |

|

Shikoku Region |

3.9% |

Mature automotive consumer base; limited new car dealership density driving used alternatives; agricultural and fisheries sector vehicle demand; ferry-linked logistics with Honshu dealer networks |

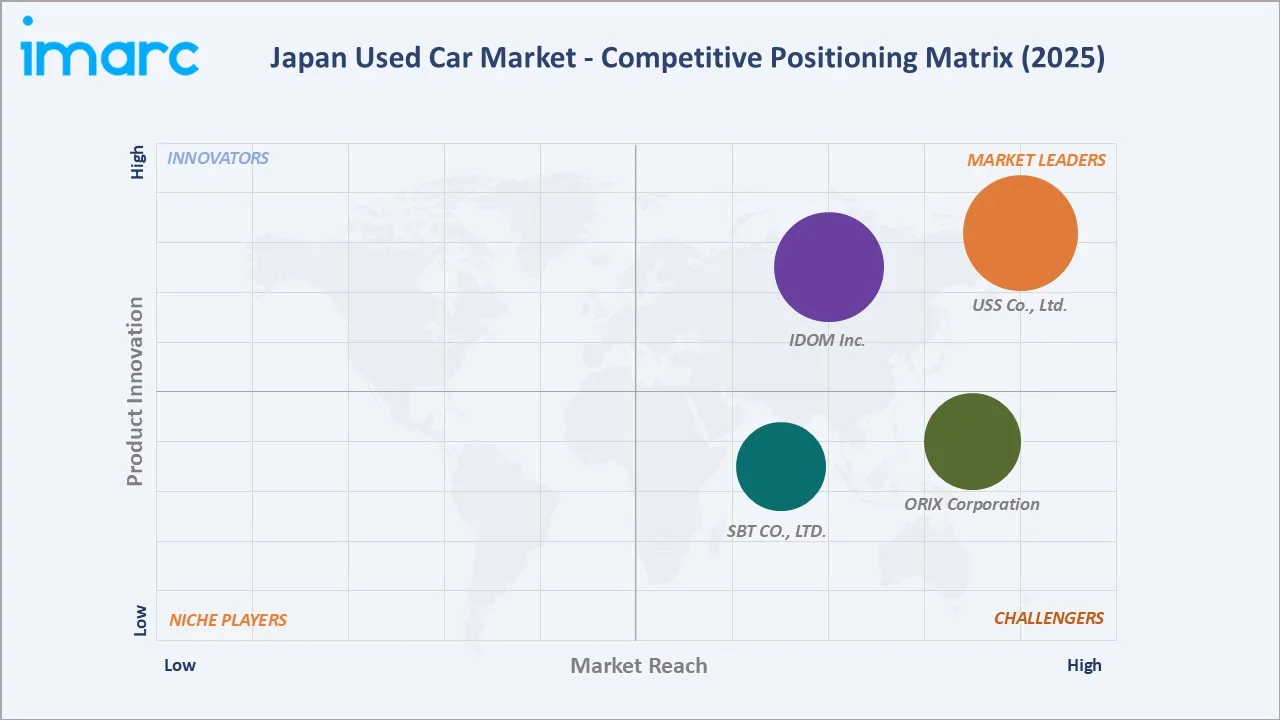

Competitive Landscape

Japan's used car market is moderately concentrated in the organized segment, with key players and leading multi-channel retailers commanding digital marketplace leadership. The unorganized segment remains highly fragmented across thousands of independent regional dealers and private sellers.

|

Company Name |

Services |

Market Position |

Core Strength |

| USS Co., Ltd. |

On-Site Auctions "USS Auto Auctions", Dedicated Terminal Auctions "USS JAPAN", Internet Auctions "CIS Information Service" |

Market Leader |

Japan's largest used car auction operator; USS Tokyo and USS Shonan flagship sites; digital remote bidding platform; export buyer network |

| IDOM Inc. |

Purchasing Business, Sales Business |

Market Leader |

Multi-channel retail (buy, sell, auction, export); Gulliver International export division; strong domestic retail brand recognition; online and offline integration |

| ORIX Corporation |

Used Vehicle Leasing and Sales, Vehicle Purchasing and Sales Agency |

Strong Challenger |

Corporate fleet vehicle remarketing leadership; certified pre-owned programs; financial services integration; nationwide dealer network; strong B2B fleet sales expertise |

| SBT CO., LTD. |

Used vehicle export, global auction facilitation, international shipping and documentation, right-hand-drive vehicle sourcing |

Challenger |

Leading used car export specialist; comprehensive export logistics and documentation; international auction buyer facilitation; right-hand-drive specialist for global markets |

Market competition is bifurcated: auction platform competition focuses on listing volume, price efficiency, and buyer network breadth; retail platform competition focuses on consumer experience, vehicle quality guarantees, and pricing transparency; and digital marketplace competition focuses on inventory depth, search functionality, and consumer protection features.

Key Company Profiles

USS Co., Ltd.

USS Co., Ltd. is one of the country's largest used car auction operators and the primary price discovery mechanism for Japan's used car wholesale market. The company operates a network of major auction sites, processing millions of vehicles annually through physical and digital auction formats.

- Service Portfolio: Physical and digital used car auction services; export market buyer facilitation; post-auction logistics and transport coordination; price analytics and market data services; digital remote bidding platform enabling nationwide and international buyer participation.

- Recent Developments: In July 2026, USS Co., Ltd preliminary used-car auction data for April–June 2026 showed 950,380 consigned vehicles, up 4.7% year over year, and 619,002 contracted vehicles, up 8.4%. The contract completion rate improved to 65.1% from 62.9%, reflecting stronger auction conversion during the quarter.

- Strategic Focus: Digital auction platform enhancement for remote domestic and international buyer access; AI-powered pricing assistance integration; export market buyer network development; data analytics services commercialization for dealer and fleet operator customers.

IDOM Inc.

IDOM Inc. operates the Gulliver brand with multiple directly managed and franchised stores nationwide. The company pioneered the 'buy only' store format in Japan, building consumer awareness of Gulliver as the primary destination for selling used cars before expanding into retail and international export operations.

- Service Portfolio: Used car retail sales (domestic); vehicle purchasing from private sellers (Gulliver buy-only store format); Gulliver International export division for right-hand-drive vehicle export to Africa, Southeast Asia, and Pacific markets; online vehicle listing and transaction platform; vehicle inspection and valuation services.

- Recent Developments: IDOM Inc. reported FY02/26 consolidated net sales of JPY 562.8 billion, up 13.3% year over year, while operating income rose 1.6% to JPY 20.2 billion and attributable profit declined 11.4% to JPY 11.9 billion. For FY02/27, the company forecasts JPY 629.0 billion in sales, JPY 24.0 billion in operating income, and total vehicle sales of approximately 352,000 units.

- Strategic Focus: Omnichannel integration of physical stores with digital booking and appraisal; export market expansion in Africa and Southeast Asia; AI appraisal tool rollout across the franchise network; used EV handling capability development as Japan's EV fleet grows into the secondary market.

Market Concentration Analysis

Japan's used car market is moderately concentrated at the auction infrastructure and organized retail tiers, commanding an estimated 35–40% of Japan's used car auction volume. At the overall market level, the top organized operators collectively represent an estimated 40–50% of the organized segment, which itself commands 63.8% of total market value.

Market consolidation in the organized segment is being driven by regulatory requirements for licensed dealer compliance, consumer protection standards that disadvantage smaller unorganized operators, and the investment required for digital platform development and AI-powered inspection tools that are becoming competitive necessities.

Investment & Growth Opportunities

Fastest Growing Segments

Used EV and hybrid vehicle segment (~14%+ CAGR within used car market), SUV vehicle type (~7.3% CAGR), organized vendor digital platform expansion (~8%+ CAGR for digital marketplace revenue), and export market facilitation services (~9%+ CAGR for specialist export operators) represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

The TSMC Kumamoto fab cluster and associated supply chain companies employing tens of thousands of workers in Kumamoto and Fukuoka prefectures are creating new demand for quality used vehicles in a region where used car dealer density has historically been below the national average relative to population growth trajectory.

Venture and Institutional Investment Trends

- Japan's used car digital marketplace sector is attracting venture capital and corporate investment, with AI-powered inspection technology companies, digital auction platforms, and consumer-facing used car retail technology platforms receiving growth investment as the market's digital transformation accelerates beyond the leading platform incumbents.

- Institutional investment in Japan's used car dealer networks is increasing following the WECARS restructuring model, demonstrating that professionally managed, compliance-focused used car retail can be operated at scale with acceptable governance standards, attracting private equity interest in regional dealer consolidation opportunities outside the major metropolitan auction markets.

Future Market Outlook (2026-2034)

The Japan used car market is positioned for sustained growth through 2034. From a base of USD 70.92 Billion in 2025, the market is projected to reach USD 124.06 Billion by 2034 at a CAGR of 6.41%, representing total incremental value creation of USD 53.14 Billion.

This growth is underpinned by the persistent affordability gap between new and used vehicles, growing global export demand for quality Japanese vehicles, and the progressive digitization of Japan's used car ecosystem that is expanding market participation and transaction efficiency.

AI-powered inspection, pricing, and matching technologies will become standard across all organized vendor operations, progressively eliminating the information asymmetry that currently constrains consumer confidence in unorganized vendor transactions, potentially accelerating the organized segment's share expansion by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry participants in 2024–2025, including used car dealer chain management, auction operator market analysts, export trader representatives, OEM certified pre-owned program managers, digital marketplace platform executives, and consumer finance specialists across Japan's Kanto, Kinki, and Chubu regions.

Secondary Research

Secondary research encompassed Japan Automobile Dealers Association (JADA) used car transaction volume statistics, USS Co. Ltd. monthly auction market reports, Japan Used Motor Vehicle Dealers Association compliance and licensing data, National Police Agency vehicle registration statistics by region, export customs statistics from Japan Customs for used vehicle exports by destination country, and financial disclosures.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating Japan Automobile Dealers Association historical used car transaction value data, consumer price index and affordability trend modelling for new-versus-used vehicle price gap dynamics, export market volume and price trend data from Japan Customs, regional economic activity indices by prefecture for regional market projections, and digital platform penetration rate modelling for organized segment share evolution.

Japan Used Car Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Hatchbacks, Sedan, Sports Utility Vehicle, Others |

| Vendor Types Covered | Organized, Unorganized |

| Fuel Types Covered | Gasoline, Diesel, Others |

| Sales Channels Covered | Online, Offline |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | USS Co., Ltd., IDOM Inc., ORIX Corporation, SBT CO., LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan used car market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan used car market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan used car industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Used Car Market Report

The Japan used car market reached USD 70.92 Billion in 2025 and is projected to reach USD 124.06 Billion by 2034.

The market is expected to grow at a CAGR of 6.41% during 2026-2034, driven by persistent new vehicle affordability pressures, digital platform expansion improving market access, and the progressive consolidation of organized dealer operations.

The Kanto Region leads with a 35.1% market share in 2025, driven by Greater Tokyo's dominant consumer base, Japan's largest auction facility concentration, and the highest volume of corporate fleet and lease-return vehicle supply entering the used market nationally.

Organized vendors dominate with a 63.8% share in 2025, reflecting Japan's regulatory environment requiring licensed dealer compliance, consumer protection standards, and Shaken documentation.

Hatchbacks hold the largest vehicle type share at 39.6%, driven by the popularity of Japan's unique kei-car category (Honda N-BOX, Suzuki Spacia) and conventional compact hatchbacks that dominate Japan's urban market due to their fuel efficiency, compact dimensions, and competitive price points in the JPY 500,000–1,500,000 range.

Some of the key players include USS Co., Ltd., IDOM Inc., ORIX Corporation, and SBT CO., LTD.

Key drivers include the persistent affordability gap between new and used vehicles, the Shaken inspection system maintaining high used vehicle quality standards, surging export demand from Africa, South Asia, and the Middle East, and AI-powered digital platforms expanding market access and transaction efficiency.

Key challenges include rising used car prices reducing the affordability advantage over new vehicles, inventory shortfall from 2021's low production creating a gap in the 3–5 year-old used vehicle supply pool, and the ongoing consumer trust restoration required following the BIGMOTOR fraud scandal.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)