Japan Vacuum Gas Oil Market Size, Share, Trends and Forecast by Type, Sulfur Content, Application, and Region, 2026-2034

Japan Vacuum Gas Oil Market Overview:

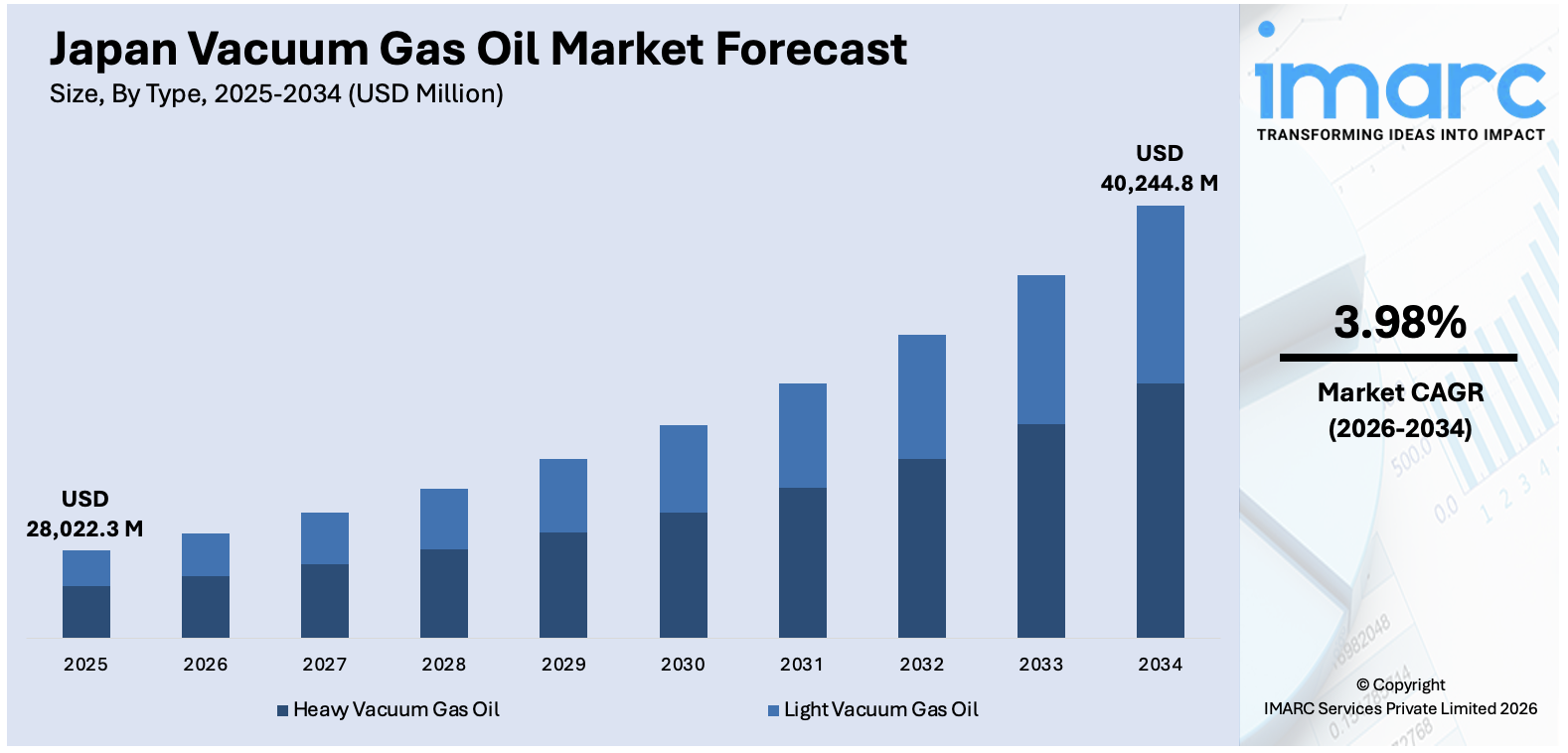

The Japan vacuum gas oil market size reached USD 28,022.3 Million in 2025. The market is projected to reach USD 40,244.8 Million by 2034, exhibiting a growth rate (CAGR) of 3.98% during 2026-2034. The market is driven by refinery rationalization in response to declining domestic petroleum consumption, stringent environmental regulations requiring low-sulfur fuel compliance, and strategic investments in sustainable refining technologies including carbon capture and storage infrastructure. These combined factors are expanding the Japan vacuum gas oil market share amid the nation's evolving energy landscape.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 28,022.3 Million |

| Market Forecast in 2034 | USD 40,244.8 Million |

| Market Growth Rate 2026-2034 | 3.98% |

Japan Vacuum Gas Oil Market Trends:

Refinery Rationalization Driven by Declining Domestic Petroleum Demand

Japan's refining industry is undergoing significant structural transformation as operators rationalize capacity in response to persistently declining domestic petroleum consumption. The country's aging and shrinking population, combined with improved vehicle fuel efficiency and gradual adoption of electric vehicles, is leading to reduced demand for transportation fuels. This demographic and technological shift has made many older, less complex refineries economically unviable, forcing operators to consolidate operations and permanently close facilities. Japanese refineries have been historically built to serve domestic needs but struggle to compete internationally due to their smaller scale and lower complexity. The closures represent strategic decisions by major operators to optimize their refinery portfolios and focus resources on more profitable, technologically advanced facilities capable of processing heavier crude grades and producing higher-value products. These strategic capacity reductions are reshaping the vacuum gas oil market as remaining refineries adjust their feedstock strategies and processing configurations to maintain profitability in a contracting domestic market environment.

To get more information on this market Request Sample

Stringent Environmental Regulations and Low-Sulfur Fuel Compliance

Environmental regulations have emerged as a critical driver reshaping vacuum gas oil processing in Japanese refineries, with the International Maritime Organization's sulfur regulations fundamentally altering refining operations and product specifications. Japanese refiners responded proactively to these requirements, investing in hydrotreating and hydrocracking units to reduce sulfur content in vacuum gas oil-derived products. This regulatory compliance necessitated capital expenditures for equipment upgrades and operational adjustments to produce very low-sulfur fuel oil while maintaining profitability. The sulfur regulations also created new market dynamics, with low-sulfur vacuum gas oil commanding premium prices due to its suitability for producing compliant marine fuels and ultra-low-sulfur diesel. Japanese refineries, began supplying sulfur bunker fuel oil from multiple refineries starting. This early compliance demonstrated the industry's commitment to meeting environmental standards while positioning Japanese refiners to serve both domestic and international marine fuel markets. The emphasis on sulfur reduction continues to influence vacuum gas oil trading patterns, refinery configurations, and product slate optimization across Japan's refining sector, supporting the Japan vacuum gas oil market growth through enhanced product value.

Investment in Sustainable Refining Technologies and Energy Transition

Japanese refineries are strategically investing in sustainable technologies and low-carbon initiatives as part of the nation's broader commitment to achieving net-zero emissions by 2050, fundamentally reshaping the role of vacuum gas oil in the refining value chain. Major operators are evaluating and implementing carbon capture and storage infrastructure, sustainable aviation fuel production facilities, and renewable feedstock processing capabilities to reduce their carbon footprint while maintaining operational viability. These investments reflect the industry's recognition that long-term survival requires transitioning from traditional petroleum refining toward more sustainable energy production models. The integration of advanced technologies into existing refinery assets aims to extend facility lifespans and create new revenue streams from low-carbon products while optimizing vacuum gas oil utilization for maximum economic and environmental benefit. Refiners are also exploring opportunities to co-process renewable feedstocks alongside conventional crude oil fractions, enabling gradual decarbonization of product portfolios without requiring complete facility replacements. In November 2024, Cosmo Oil contracted Chiyoda Corporation to conduct a feasibility study for implementing carbon capture and storage infrastructure at its 177,000-barrel-per-day Chiba refinery in Ichihara, Chiba Prefecture, examining designs for installations aimed at separating and capturing carbon dioxide emissions as part of Japan Organization for Metals and Energy Security's program to advance commercialization of a Japanese CCS value chain. These sustainability initiatives represent a fundamental shift in how Japanese refineries view vacuum gas oil processing, moving from purely volume-driven operations toward value-optimized, environmentally responsible production systems that balance commercial imperatives with climate commitments and regulatory requirements.

Japan Vacuum Gas Oil Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type, sulfur content, and application.

Type Insights:

- Heavy Vacuum Gas Oil

- Light Vacuum Gas Oil

The report has provided a detailed breakup and analysis of the market based on the type. This includes heavy vacuum gas oil and light vacuum gas oil.

Sulfur Content Insights:

- Low Sulfur VGO

- High Sulfur VGO

A detailed breakup and analysis of the market based on the sulfur content have also been provided in the report. This includes low sulfur VGO and high sulfur VGO.

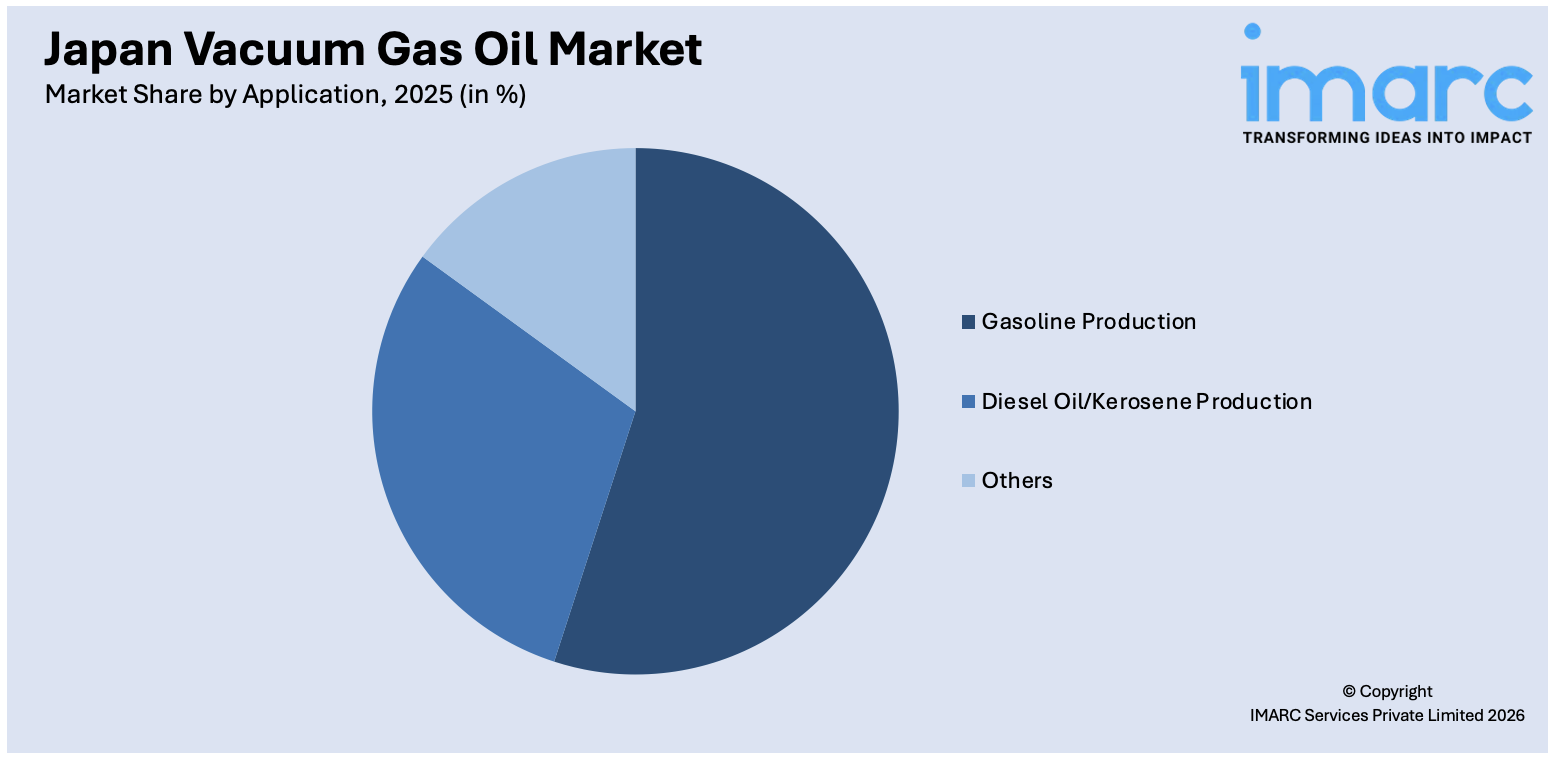

Application Insights:

Access the comprehensive market breakdown Request Sample

- Gasoline Production

- Diesel Oil/Kerosene Production

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes gasoline production, diesel oil/kerosene production, and others.

Regional Insights:

- Kanto Region

- Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The report has also provided a comprehensive analysis of all the major regional markets, which include Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, and Shikoku Region.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Japan Vacuum Gas Oil Market News:

- February 2025: ENEOS Corporation and Mitsubishi Corporation announced they would proceed with front-end engineering design for sustainable aviation fuel production at the Wakayama plant. The facility is expected to produce approximately 300,000 metric tonnes per year of SAF annually, along with naphtha and light oil fractions, beginning in fiscal year 2028, with feedstock primarily consisting of waste products and byproducts such as used cooking oil and tallow.

Japan Vacuum Gas Oil Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Heavy Vacuum Gas Oil, Light Vacuum Gas Oil |

| Sulfur Contents Covered | Low Sulfur VGO, High Sulfur VGO |

| Application Covered | Gasoline Production, Diesel Oil/Kerosene Production, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Japan vacuum gas oil market performed so far and how will it perform in the coming years?

- What is the breakup of the Japan vacuum gas oil market on the basis of type?

- What is the breakup of the Japan vacuum gas oil market on the basis of sulfur content?

- What is the breakup of the Japan vacuum gas oil market on the basis of application?

- What is the breakup of the Japan vacuum gas oil market on the basis of region?

- What are the various stages in the value chain of the Japan vacuum gas oil market?

- What are the key driving factors and challenges in the Japan vacuum gas oil market?

- What is the structure of the Japan vacuum gas oil market and who are the key players?

- What is the degree of competition in the Japan vacuum gas oil market?

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan vacuum gas oil market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan vacuum gas oil market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan vacuum gas oil industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)