Japan Wax Market Size, Share, Trends and Forecast by Type, Form, Application, and Region 2026-2034

Japan Wax Market Size, Share, Trends & Forecast (2026-2034)

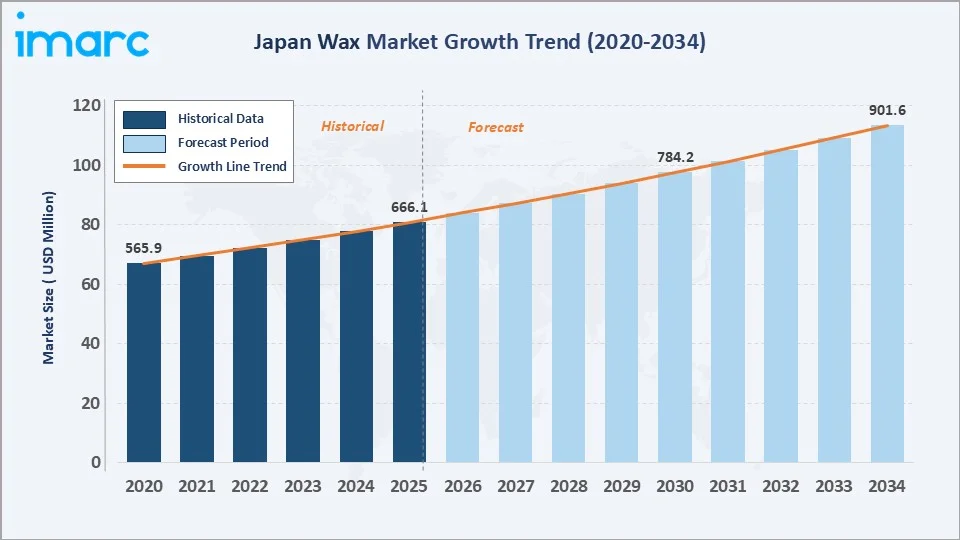

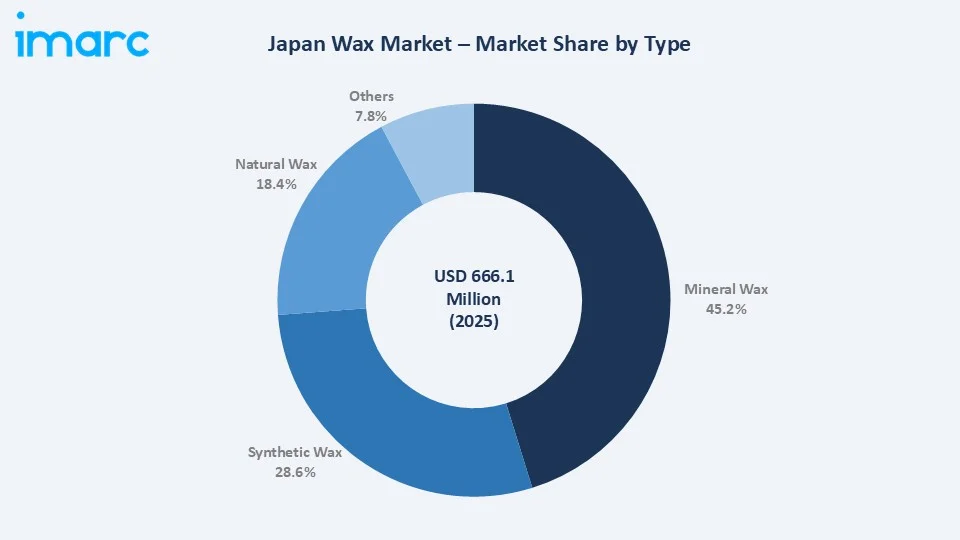

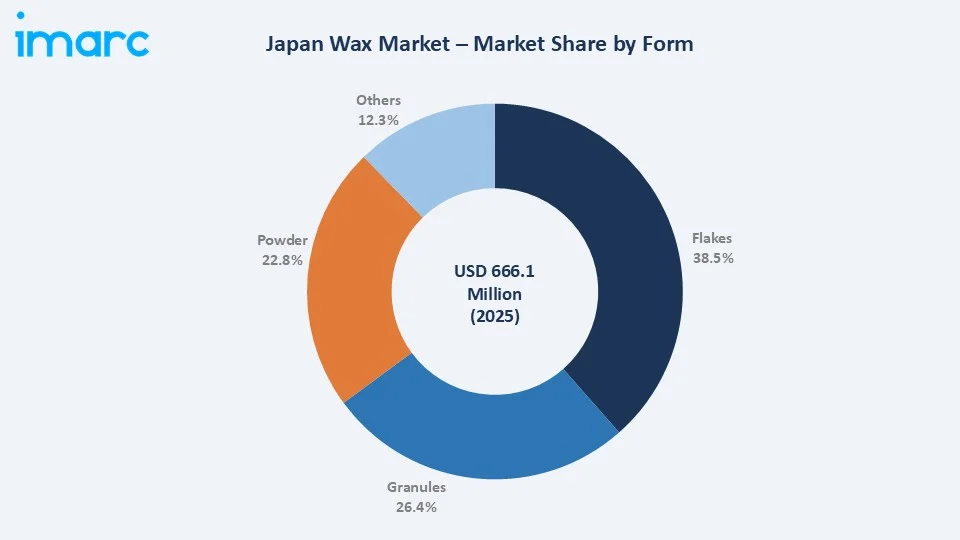

The Japan wax market size reached USD 666.1 Million in 2025 and is projected to reach USD 901.6 Million by 2034, exhibiting a CAGR of 3.32% during 2026-2034. Growing demand from cosmetics, packaging, and candle manufacturing sectors, rising preference for sustainable bio-based wax alternatives, and expanding industrial applications underpin the market's steady growth trajectory.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 666.1 Million |

|

Forecast Market Size (2034) |

USD 901.6 Million |

|

CAGR (2026-2034) |

3.32% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

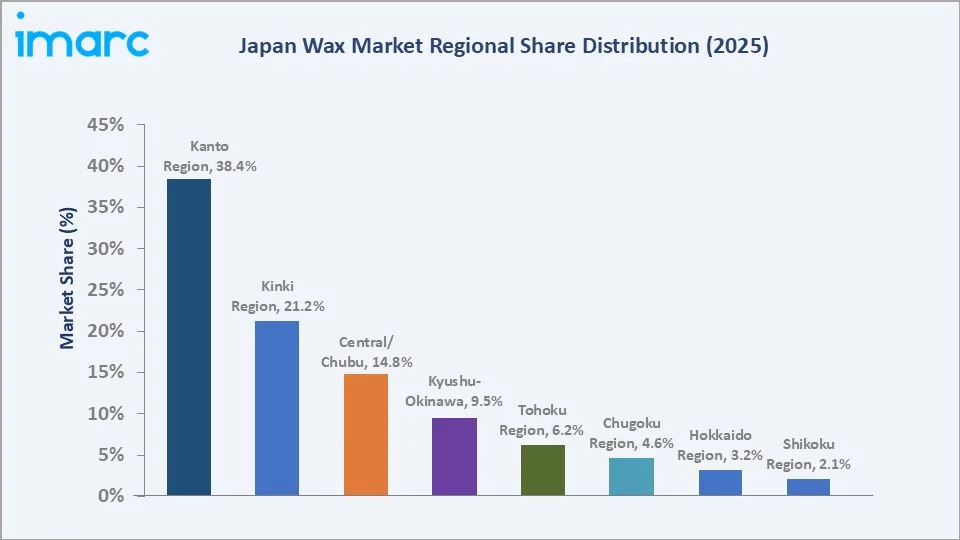

Kanto Region (38.4% share, 2025) |

|

Second Largest Region |

Kinki Region (21.2% share, 2025) |

|

Leading Type |

Mineral Wax (45.2%, 2025) |

|

Leading Form |

Flakes (38.5%, 2025) |

To get more information on this market, Request Sample

The Japan wax market growth trajectory from 2020 through 2034, with historical expansion to USD 666.1 Million in 2025, reflects consistent demand driven by cosmetics, packaging, and candle manufacturing industries. The forecast period projects sustained growth to USD 901.6 Million by 2034, supported by bio-based wax innovation and expanding industrial end uses.

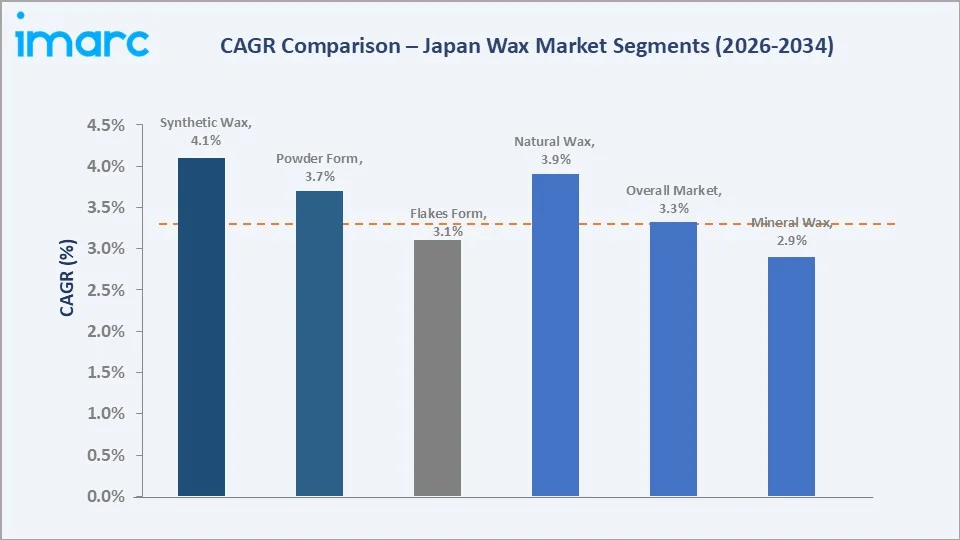

The CAGR trajectories across key type and form sub-segments, with synthetic wax at ~4.1% CAGR and powder form at ~3.7% CAGR, represent the fastest-growing sub-segments, driven by innovation in functional wax formulations and sustainable packaging applications across Japan's diversified chemical industry.

Executive Summary

The Japan wax market is on a sustained growth trajectory from USD 666.1 Million in 2025 to USD 901.6 Million by 2034. Wax, an essential material spanning cosmetics, packaging, candles, pharmaceuticals, and industrial coatings, benefits from Japan's highly developed chemical manufacturing base and premium quality standards.

Mineral wax dominates the type segment at 45.2% in 2025, owing to its cost-effectiveness, versatile processing characteristics, and broad applicability in packaging and candle manufacturing. Synthetic wax (28.6%) is the fastest-growing type, driven by demand for high-performance hot-melt adhesives and specialty coatings.

The Kanto Region commands 38.4% of the market in 2025, reflecting the concentration of Japan's chemical manufacturing, cosmetics production, and packaging industries in the Greater Tokyo industrial corridor. Kinki Region (21.2%) and Central/Chubu Region (14.8%) represent the second and third largest markets respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Mineral Wax – 45.2% share (2025) |

|

Fastest-Growing Type |

Synthetic Wax – ~4.1% CAGR (2026-2034) |

|

Leading Form |

Flakes – 38.5% share (2025) |

|

Leading Region |

Kanto Region – 38.4% revenue share (2025) |

|

Second Region |

Kinki Region – 21.2% revenue share (2025) |

|

Top Companies |

Nippon Seiro Co., Ltd., Mitsui Chemicals, Inc., Sasol, S. KATO & CO., TOA KASEI CO., LTD., artience Co., Ltd. |

Key Analytical Observations Supporting the Above Data:

- Mineral Wax Leadership: Mineral wax, with 45.2% in 2025, dominates because of its cost-competitive refining economics, wide melting-point range, and entrenched role in candle production, food-grade coatings, and corrugated board sizing applications.

- Synthetic Wax Growth: Synthetic wax, with 28.6% in 2025, is growing fast due to expanding demand in hot-melt adhesives, PVC lubricants, and specialty coatings that require precise molecular weight distributions unavailable in petroleum-derived waxes.

- Flakes Form Dominance: Flakes form at 38.5% leads because of ease of handling, precise dosing, and compatibility with automatic dispensing systems in cosmetics and hot-melt adhesive manufacturing facilities across Japan.

- Kanto Region Strength: Kanto region's 38.4% dominance reflects the concentration of Japan's cosmetics majors, packaging converters, and specialty chemical distributors in the Greater Tokyo industrial belt.

Japan Wax Market Overview

Wax is a broad category of hydrophobic organic substances covering petroleum-derived paraffin and microcrystalline waxes, synthetic polyethylene and Fischer-Tropsch waxes, and natural waxes including carnauba, beeswax, and rice bran wax. Japan's market is characterized by high purity standards and specialty application development.

The Japan wax ecosystem integrates petroleum refiners supplying paraffin and microcrystalline fractions, specialty chemical companies producing synthetic wax grades, natural wax importers and blenders, downstream formulators serving cosmetics and adhesives, and distribution channels serving industrial end users across Japan's eight major regions.

Market Dynamics

To evaluate market opportunities, Request Sample

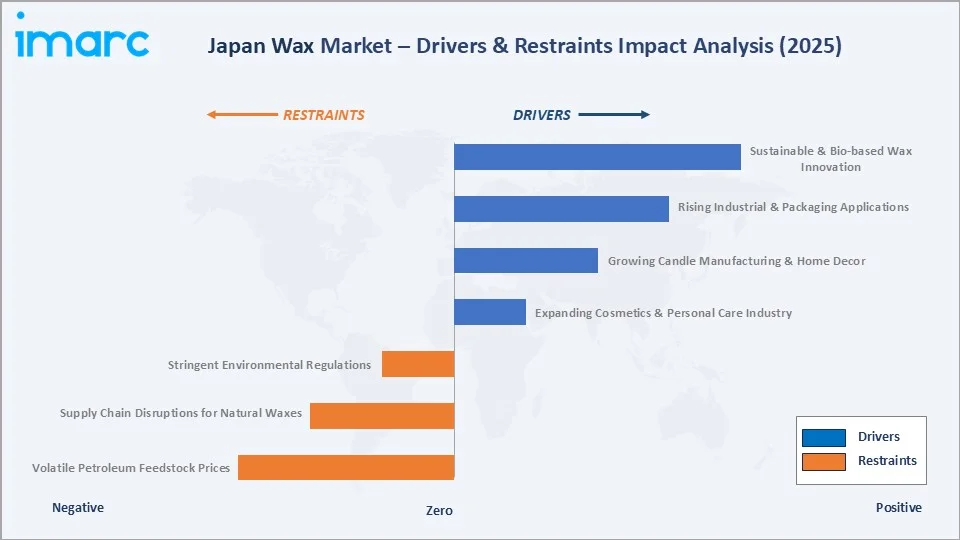

Market Drivers

- Expanding Cosmetics & Personal Care Industry: Japan's cosmetics and personal care sector, is a principal demand driver for specialty waxes. Japan is home to about 3,000 beauty care companies, including global brands of Shiseido, Kao, Kosé, and Pola Orbis. Lipstick, mascara, eyeliner, and skin-cream formulations require carnauba, beeswax, candelilla, and microcrystalline wax at high purity grades, sustaining premium wax demand from Japan's globally competitive beauty industry.

- Candle Manufacturing & Home Décor Trends: Growing cultural significance of scented and decorative candles in Japanese home décor, wellness, and gifting sectors has generated consistent volume demand for paraffin and natural waxes. E-commerce channels have accelerated candle retail growth, expanding the addressable wax consumption base significantly.

- Industrial & Packaging Applications: Japan's food packaging sector relies on food-grade paraffin wax coatings and wax emulsions for freshness preservation. Industrial demand from automotive detailing, electrical insulation, and rubber compounding adds further volume to Japan's wax consumption base. Japan is the highest per capita consumer of packaging materials in the world and there is a strong correlation between food and the packaging Industry in Japan.

Market Restraints

- Volatile Petroleum Feedstock Prices: Paraffin wax pricing in Japan is closely linked to crude oil refining dynamics, which introduces significant variability in procurement costs for downstream converters and formulators. Fluctuations in crude import costs make it difficult to maintain consistent formulation and pricing strategies. This volatility complicates long-term supply agreements and pricing negotiations across the value chain. It also pressures manufacturers to frequently adjust margins or absorb cost increases, impacting profitability. As a result, businesses often seek alternative sourcing strategies or substitute materials to manage risk.

- Supply Chain Disruptions for Natural Waxes: Carnauba wax (Brazil), rice bran wax, and specialty natural waxes depend on agricultural supply chains subject to weather, crop yield variability, and export regulation changes. Japan's reliance on natural wax imports creates supply-side exposure constraining volume planning for cosmetics formulators.

Market Opportunities

- Sustainable & Bio-based Wax Innovation: Japan's chemical industry R&D investment in bio-based Fischer-Tropsch wax alternatives, enzymatically modified natural waxes, and upcycled plant-derived wax fractions aligns with sustainability mandates from major cosmetics and packaging customers, opening new premium-priced product categories.

- Pharmaceutical Excipient Market Growth: The growth of Japan's pharmaceutical sector creates demand for pharmaceutical-grade microcrystalline wax in tablet coating, modified-release formulations, and ointment bases. PMDA's stringent purity specifications create a premium market segment with stable, specification-driven demand.

Market Challenges

- Stringent Environmental Regulations: The Ministry of the Environment's chemical substance management framework is progressively restricting aromatic and chlorinated processing aids used in certain wax formulations. Compliance investment and reformulation costs create barriers for smaller wax processors.

- Competition from Global Low-cost Suppliers: Chinese petrochemical producers and Southeast Asian natural wax suppliers offer commodity wax grades at significantly lower delivered costs, pressuring margins for Japanese wax processors in standard-specification applications and driving differentiation toward specialty grades.

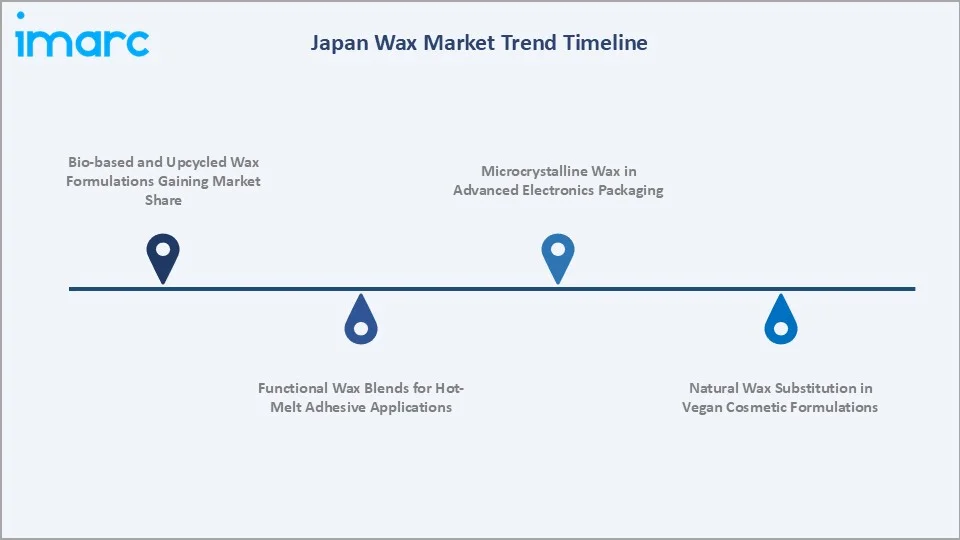

Emerging Market Trends

1. Bio-based and Upcycled Wax Formulations Gaining Market Share

Japanese cosmetics majors including Kao and Shiseido are committing to bio-derived and upcycled ingredient strategies, driving demand for rice bran wax, jojoba esters, and enzymatically modified carnauba waxes. MORESCO Corporation and Nippon Seiro have invested in green chemistry processes to address sustainability-mandated reformulation timelines.

2. Functional Wax Blends for Hot-Melt Adhesive Applications

The expansion of Japan's e-commerce packaging and automotive assembly industries is driving innovation in synthetic wax-modified hot-melt adhesive systems. Fischer-Tropsch and polyethylene wax blends engineered for specific open-time, crystallisation rate, and adhesion performance are displacing standard paraffin grades in premium assembly applications.

3. Microcrystalline Wax in Advanced Electronics Packaging

Japan's semiconductor and electronic components industry is consuming precision-grade microcrystalline wax for temporary bonding, dicing tape backcoating, and encapsulation masking applications. The METI semiconductor reinvestment roadmap is expected to expand this specialised demand segment at above-market CAGR.

4. Natural Wax Substitution in Vegan Cosmetic Formulations

The vegan and cruelty-free cosmetics movement is accelerating substitution of beeswax with plant-derived alternatives including carnauba, rice bran, and sunflower waxes in lipstick and foundation formulations. Japan's cosmetics certification bodies are formalising vegan ingredient standards, creating a structured market transition for natural wax suppliers.

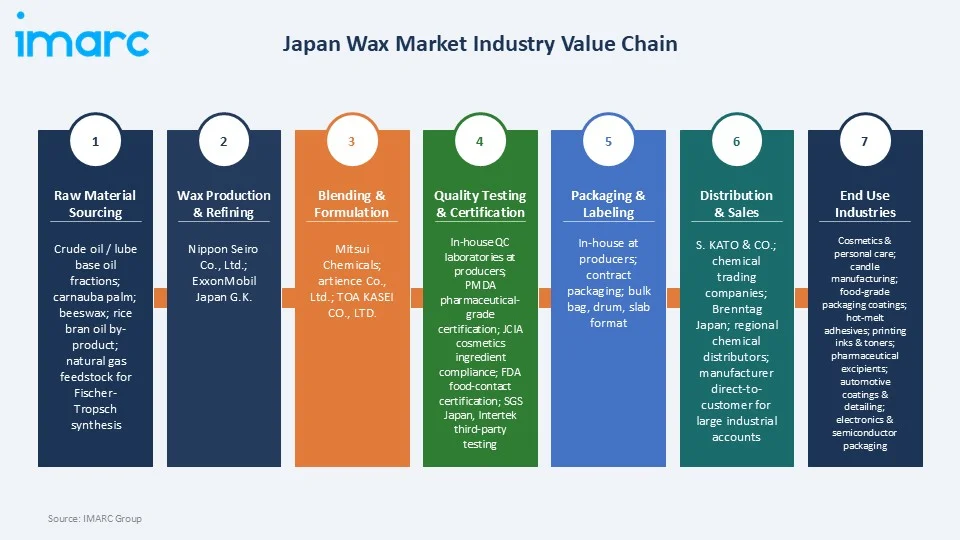

Industry Value Chain Analysis

The Japan wax value chain spans six stages from raw material sourcing through end-use distribution. Blending, formulation, and quality testing capture the highest value-add margins, while raw material procurement and distribution are characterised by competitive commodity economics and logistics efficiency requirements.

|

Stage |

Key Players/Examples |

|

Raw Material Sourcing |

Crude oil / lube base oil fractions; carnauba palm; beeswax; rice bran oil by-product; natural gas feedstock for Fischer-Tropsch synthesis |

|

Wax Production & Refining |

Nippon Seiro Co., Ltd.; ExxonMobil Japan G.K. |

|

Blending & Formulation |

Mitsui Chemicals, Inc.; artience Co., Ltd./Toyochem, TOA KASEI CO., LTD. |

|

Quality Testing & Certification |

In-house QC laboratories at producers; PMDA pharmaceutical-grade certification; JCIA cosmetics ingredient compliance; FDA food-contact certification; SGS Japan, Intertek third-party testing |

|

Packaging & Labeling |

In-house at producers; contract packaging for cosmetics-grade small-lot requirements; bulk bag, drum, and slab format conversion for industrial customers |

|

Distribution & Sales |

S. KATO & CO.; chemical trading companies; Brenntag Japan; regional chemical distributors; manufacturer direct-to-customer for large industrial accounts |

|

End Use Industries |

Cosmetics & personal care; candle manufacturing; food-grade packaging coatings; hot-melt adhesives; printing inks & toners; pharmaceutical excipients; automotive coatings & detailing; electronics & semiconductor packaging |

Vertically integrated wax producers, with captive petroleum fraction sourcing and in-house specialty formulation capabilities, achieve superior margin capture compared to pure-play distributors. Quality testing and regulatory compliance represent a growing cost centre for Japan market participants.

Technology Landscape in the Japan Wax Industry

Refining Technology: Solvent Dewaxing and Hydrotreating

Solvent dewaxing using methyl ethyl ketone (MEK) or propane dewaxing remains the dominant process for producing food- and cosmetics-grade paraffin wax from lube base oil fractions. Nippon Seiro and ExxonMobil Japan employ hydrofinishing to achieve colour stability and low polycyclic aromatic hydrocarbon levels required for pharmaceutical and food-contact certifications.

Synthetic Wax Production: Fischer-Tropsch and Metallocene

Fischer-Tropsch synthesis, pioneered by Sasol Japan KK, produces hard, high-melting-point waxes with narrow carbon number distributions ideal for printing inks, coatings, and hot-melt adhesives. Metallocene-catalysed polyethylene wax production by Mitsui Chemicals enables precise molecular weight control for specialty performance requirements.

Emulsification and Micro-encapsulation Technology

High-pressure homogenisation and microfluidic emulsification technologies are enabling Japan's wax formulators to produce sub-micron wax emulsions for waterborne coatings, textile finishing, and paper sizing applications. Micro-encapsulated wax for controlled-release cosmetic applications represents an emerging high-value technology frontier.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Mineral Wax |

45.2% |

2025 |

|

Form |

Flakes |

38.5% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

38.4% |

2025 |

By Type

To access detailed market analysis, Request Sample

Mineral wax commands a 45.2% majority share in 2025, underpinned by the cost-competitive economics of paraffin and microcrystalline production at Japanese refineries and strong demand from packaging, candle, and industrial coatings applications that do not require bio-based or synthetic specialty grades.

Synthetic wax at 28.6% in 2025, growing fastest at ~4.1% CAGR, is irreplaceable in high-performance applications where precise carbon chain length, melting point, and melt viscosity must be engineered. Fischer-Tropsch and polyethylene waxes enable hot-melt adhesive, printing ink, and specialty coatings performance unavailable from petroleum-derived grades.

By Form

Flakes form dominates at 38.5% in 2025, representing the most versatile, cleanly handled, and precisely dosed format for cosmetics compounding, hot-melt adhesive manufacturing, and candle production. Japanese cosmetics plants and adhesive compounders prefer flakes for automatic feeding, blending homogeneity, and reduced dust generation in factory environments.

Granules at 26.4% in 2025 are preferred in high-throughput industrial processes, including PVC compounding, rubber processing, and paper coating, where bulk conveying, pneumatic transfer, and continuous feed systems benefit from the uniform geometry and low dust characteristics of granular wax products.

Regional Market Insights

The Kanto region's 38.4% market dominance in 2025 is driven by Japan's highest concentration of cosmetics manufacturing, specialty chemical production, and packaging conversion facilities in the Greater Tokyo industrial corridor. Shiseido, Kao, Kosé, and Pola Orbis headquarters and major production sites are concentrated in this region.

Kinki region at 21.2% benefits from Osaka's established chemical manufacturing cluster, pharmaceutical production base, and food processing industries that collectively sustain diversified wax demand spanning mineral, synthetic, and specialty natural grades across multiple end-use sectors.

Central/Chubu region at 14.8% is driven by automotive component manufacturing, where wax-based release agents, protective coatings, and stamping lubricants generate consistent industrial consumption. Kyushu-Okinawa region at 9.5% is witnessing accelerating wax demand tied to semiconductor manufacturing expansion.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

38.4% |

Cosmetics majors, specialty chemicals, packaging converters, e-commerce hubs |

|

Kinki Region |

21.2% |

Osaka chemical industry cluster, pharmaceutical manufacturing, food processing |

|

Central/Chubu Region |

14.8% |

Automotive industry wax applications, industrial coatings, aerospace manufacturing |

|

Kyushu-Okinawa Region |

9.5% |

Semiconductor manufacturing growth, electronics packaging, agricultural applications |

|

Tohoku Region |

6.2% |

Food processing sector, candle manufacturing, paper and printing industries |

|

Chugoku Region |

4.6% |

Petroleum refining proximity, rubber industry, specialty chemical distribution |

|

Hokkaido Region |

3.2% |

Food-grade wax applications, agricultural produce coatings, printing & packaging |

|

Shikoku Region |

2.1% |

Paper manufacturing, food processing, marine industry applications |

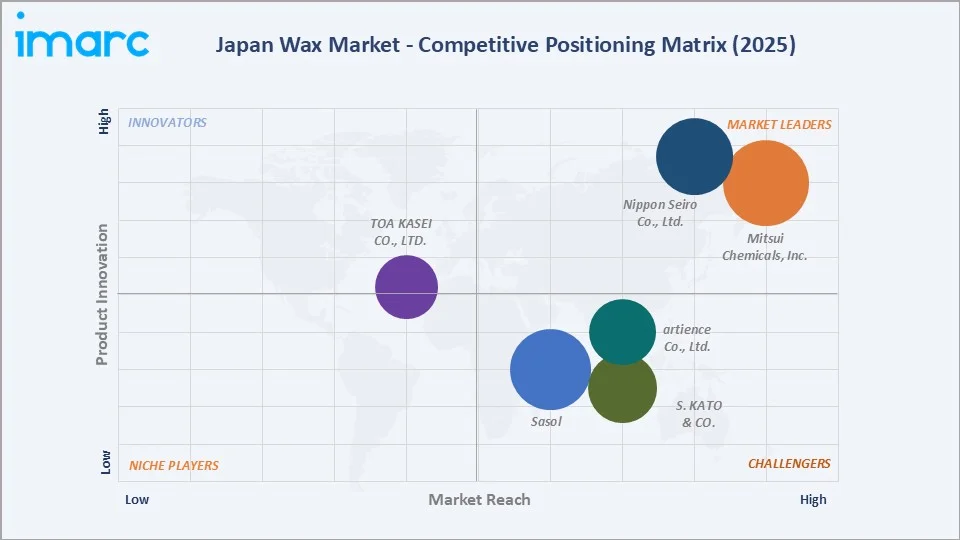

Competitive Landscape

The Japan wax market is moderately concentrated at the domestic level, with Nippon Seiro Co., Ltd. holding a leading position in petroleum-derived wax segments, while MORESCO Corporation and Fuji Wax Co., Ltd. compete in specialty and synthetic grades. Global majors including Sasol Japan KK, ExxonMobil Japan, and Mitsui Chemicals occupy significant positions in synthetic and specialty wax categories.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Nippon Seiro Co., Ltd. |

Paraffin Wax, Microcrystalline Wax |

Leader |

Domestic petroleum wax leader; food & cosmetics grades; refinery integration |

|

Mitsui Chemicals, Inc. |

Hi-WAX |

Leader |

Synthetic wax innovation; plastics & coatings; sustainability focus |

|

Sasol |

Fischer-Tropsch Hard Wax, Fischer-Tropsch Medium Wax, Hydrocarbon Wax, n-Paraffins, Synthetic Wax |

Challenger |

FT wax specialty; printing inks; hot-melt adhesive applications |

|

S. KATO & CO. |

Carnauba Wax, Beeswax, Casting Wax, Ceresin Wax, Montan Wax, Paraffin Wax |

Challenger |

Japan exclusive Sasol FT wax distributor; natural wax refining via Nippon Wax subsidiary; 100+ year legacy |

|

TOA KASEI CO., LTD. |

TOWAX-5F2, TOWAX-3F17, TOWAX-1F3, TOWAX-1F6, TOWAX-1F12 |

Emerging |

Osaka-based natural wax manufacturer & specialty trader; 110+ year heritage; Asia-focused distribution |

|

artience Co., Ltd. |

Plant-based wax (carnauba wax), Petroleum-based wax, Synthetic wax |

Challenger |

Handles ~40% of Japan's carnauba wax imports; NuCera Solutions synthetic wax distributor |

Key players include Nippon Seiro Co., Ltd., Mitsui Chemicals, Inc., Sasol, S. KATO & CO., TOA KASEI CO., LTD., artience Co., Ltd., and others.

Key Company Profiles

Mitsui Chemicals, Inc.

Mitsui Chemicals, Inc. is a major Japan-based diversified chemical company with a significant synthetic wax business including polyethylene wax and metallocene-catalysed wax production. The company's global R&D infrastructure enables continuous innovation in bio-based and high-performance synthetic wax alternatives.

- Product Portfolio: Polyethylene Wax (Hi-WAX series), Metallocene Wax, Fischer-Tropsch Wax, Functional Polymer Additives

- Recent Developments: In September 2025, Mitsui Chemicals, in collaboration with Asahi Kasei and Mitsubishi Chemical, announced the formation of a partnership aimed at advancing more sustainable ethylene production in western Japan. This development signaled a broader shift within the petrochemical value chain, which could influence the availability and cost structure of wax derived from refining processes.

- Strategic Focus: Mitsui Chemicals leverages integrated polymer chemistry R&D to develop next-generation synthetic wax grades for sustainability-driven reformulations in cosmetics, packaging, and adhesive markets, with global commercialisation reach.

Sasol

Sasol is a South Africa-headquartered integrated energy and chemical company and the world's pioneer in commercial Fischer-Tropsch wax production.

- Product Portfolio: Fischer-Tropsch Hard Wax, Fischer-Tropsch Medium Wax, Hydrocarbon Wax, n-Paraffins, Synthetic Wax

- Recent Developments: In August 2024, Sasol Chemicals launched SASOLWAX LC100, an industrial wax grade for the packaging adhesives sector delivering a 35% lower cradle-to-gate Carbon Footprint versus conventional alternatives.

- Strategic Focus: Sasol leverages its proprietary GTL Fischer-Tropsch technology to produce MOSH/MOAH-free and PFAS-free wax grades that align with tightening regulatory requirements in Japan and globally, targeting premium segments in cosmetics, pharmaceuticals, hot-melt adhesives, and packaging while expanding its lower-carbon wax portfolio to address customer sustainability commitments.

S. KATO & CO.

S. KATO & CO. is an Osaka-founded trading and wax manufacturing company established in 1901 with over 120 years of operational history. The company is engaged in natural wax refining, investment casting wax production, and synthetic wax processing.

- Product Portfolio: Carnauba Wax, Beeswax, Casting Wax, Ceresin Wax, Montan Wax, Paraffin Wax

- Strategic Focus: S. KATO & CO. operates a dual-pillar strategy combining exclusive Sasol FT wax distribution with proprietary natural wax refining through Nippon Wax, delivering a multi-wax portfolio that spans synthetic, natural, and mineral categories to cosmetics formulators, industrial manufacturers, and investment casting specialists, underpinned by a century-long tradition of safety-oriented raw material sourcing.

TOA KASEI CO., LTD.

TOA KASEI CO., LTD. is an Osaka-based specialty natural wax manufacturer and chemical trading company founded in 1913 with over 110 years of heritage in wax refining, purification, and distribution. The company operates manufacturing facilities including the Aikawa Factory, established in 2000, and serves customers across cosmetics, food, and industrial sectors in Japan and across Asia with its proprietary TOWAX series of purified natural waxes.

- Product Portfolio: TOWAX-5F2, TOWAX-3F17 (purified rice bran wax), TOWAX-1F3 (de-resin carnauba wax), TOWAX-1F6 (fine purified carnauba wax, Ecocert approved), TOWAX-1F12 (high-resin carnauba wax for mascara and eye liner)

- Recent Developments: In November 2024, TOA KASEI established a Seoul Office in South Korea, marking a strategic step in expanding its Asia-Pacific customer network and strengthening distribution of its natural wax portfolio to the Korean cosmetics manufacturing sector.

- Strategic Focus: TOA KASEI differentiates through its core competencies in natural wax separation, purification, and custom blending, directly sourcing raw materials from Brazil and India to ensure traceability and quality control from origin through to delivery. The company targets Japan's premium cosmetics industry with Ecocert-certified and vegan-compatible wax grades while expanding into ASEAN markets through its growing Asia-Pacific office network.

Market Concentration Analysis

The Japan wax market exhibits moderate concentration, with Nippon Seiro Co., Ltd. holding the leading position in petroleum-derived wax segments, while no single company commands more than 20% of the total market. The synthetic wax segment shows higher concentration, with MORESCO Corporation and Mitsui Chemicals jointly accounting for a majority of specialty synthetic grades.

Consolidation at the product category level is more advanced than overall market fragmentation suggests. Nippon Seiro's domination of domestic paraffin refining, and Mitsui Chemicals' leadership in polyethylene wax synthesis, create category-level concentration even within a moderately fragmented overall market structure.

Investment & Growth Opportunities

Fastest-Growing Segments

Synthetic wax at ~4.1% CAGR through 2034 is the highest-growth type segment, driven by hot-melt adhesive, electronics packaging, and specialty coating applications where engineered molecular performance commands significant price premiums over commodity petroleum wax grades in Japan's high-value manufacturing industries.

Emerging Markets

Kyushu-Okinawa Region at above-average CAGR is the fastest-growing region for wax in Japan through 2034. TSMC's Kumamoto semiconductor fab investments, Sony's image sensor expansion, and Daikin's industrial facilities are generating localised demand for electronics-grade specialty wax within this historically secondary market.

Venture & Investment Trends

Strategic investment in bio-wax R&D is intensifying among Japan's chemical majors, with NEDO-funded research programmes targeting enzymatic wax synthesis and catalytic plant-oil conversion. Private investment in specialty wax micro-emulsion technologies for personal care and pharmaceutical applications represents an emerging venture opportunity.

Future Market Outlook (2026-2034)

The Japan wax market is forecast to expand from USD 666.1 Million in 2025 to USD 901.6 Million by 2034 at a CAGR of 3.32%, adding approximately USD 235.5 Million in incremental annual market value. Japan's position as Asia's leading premium chemical and cosmetics producer underpins stable, quality-driven demand growth.

Three structural forces will most significantly shape the Japan wax market through 2034. Sustainability-driven bio-wax innovation will create premium product categories. Japan's semiconductor and electronics manufacturing reinvestment will expand specialty wax demand. The premium cosmetics export sector will sustain high-specification natural and synthetic wax consumption.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Japan wax industry stakeholders, including senior commercial managers at wax producers, procurement specialists at cosmetics and packaging converters, technical directors at adhesive and coating manufacturers, and regulatory affairs professionals across the wax supply chain.

Secondary Research

Key secondary sources include Japan Petroleum Energy Center statistical reports, METI chemical industry production data, Japan Cosmetic Industry Association market statistics, Ministry of Finance trade data for wax imports and exports, and published annual reports from leading Japan wax market participants.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating Japan GDP growth rates, industrial production indices, cosmetics and packaging output data, and sector-specific end-use demand modelling validated against primary research inputs and secondary data triangulation.

Japan Wax Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Mineral Wax, Synthetic Wax, Natural Wax, Others |

| Forms Covered | Flakes, Granules, Powder, Others |

| Applications Covered | Candles, Cosmetics, Packaging, Emulsions, Hot Melts, Floor Polishes, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu/Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region. |

| Companies Covered | Nippon Seiro Co., Ltd., Mitsui Chemicals, Inc., Sasol, S. KATO & CO., TOA KASEI CO., LTD., artience Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan wax market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan wax market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan wax industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Wax Market Report

The Japan wax market reached USD 666.1 Million in 2025, reflecting consistent demand from cosmetics, packaging, candle manufacturing, and industrial applications, underpinned by Japan's premium chemical manufacturing capabilities.

The market is projected to reach USD 901.6 Million by 2034, growing at a CAGR of 3.32% during 2026-2034, driven by bio-based wax innovation, synthetic wax demand growth, and expanding end-use applications.

Mineral wax leads with a 45.2% type share in 2025, valued for its cost-effectiveness and versatility across packaging, candle, and industrial applications that represent the largest volume consumption segments.

Flakes lead at 38.5% in 2025, representing the most versatile and precisely dosed format preferred by Japan's cosmetics manufacturers, hot-melt adhesive producers, and candle industry for clean handling and automatic dispensing.

Kanto Region commands a 38.4% market share in 2025, driven by Japan's highest concentration of cosmetics manufacturers, specialty chemical companies, and packaging converters concentrated in the Greater Tokyo industrial corridor.

Synthetic wax is the fastest-growing type at ~4.1% CAGR through 2034, driven by hot-melt adhesive, electronics packaging, printing inks, and specialty coating applications requiring engineered molecular performance.

Leading companies include Nippon Seiro Co., Ltd., Mitsui Chemicals, Inc., Sasol, S. KATO & CO., TOA KASEI CO., LTD., artience Co., Ltd., and others.

Key applications include cosmetics and personal care formulations, candle manufacturing, food-grade packaging coatings, hot-melt adhesives, printing inks, pharmaceutical excipients, automotive detailing, and electronics component manufacturing.

Sustainability mandates from cosmetics majors and packaging converters are driving adoption of bio-based, vegan-certified, and upcycled wax alternatives, generating new premium product categories and reformulation demand across the value chain.

Mineral wax is derived from petroleum refining with variable carbon chain distributions, while synthetic wax is produced by chemical synthesis enabling precise molecular weight, melting point, and performance characteristics unavailable in natural petroleum fractions.

Kinki Region's 21.2% share reflects Osaka's established chemical manufacturing cluster, major pharmaceutical production facilities, and food processing industry that generate diversified demand for specialty, food-grade, and industrial wax products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)