Joint Reconstruction Devices Market Size, Share, Trends and Forecast by Technique, Joint Type, End User, and Region, 2026-2034

Joint Reconstruction Devices Market Size and Share:

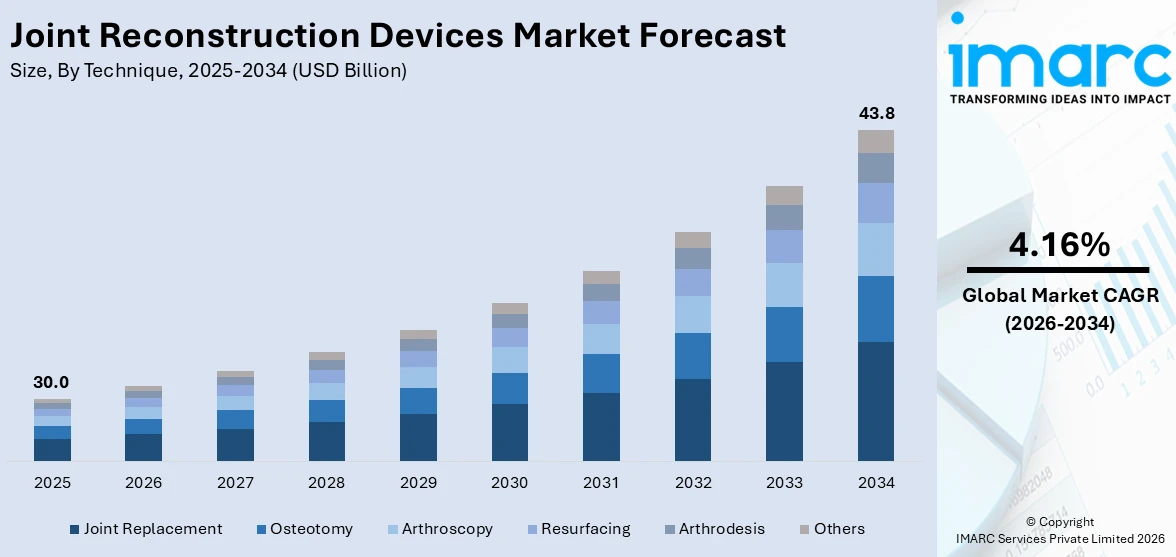

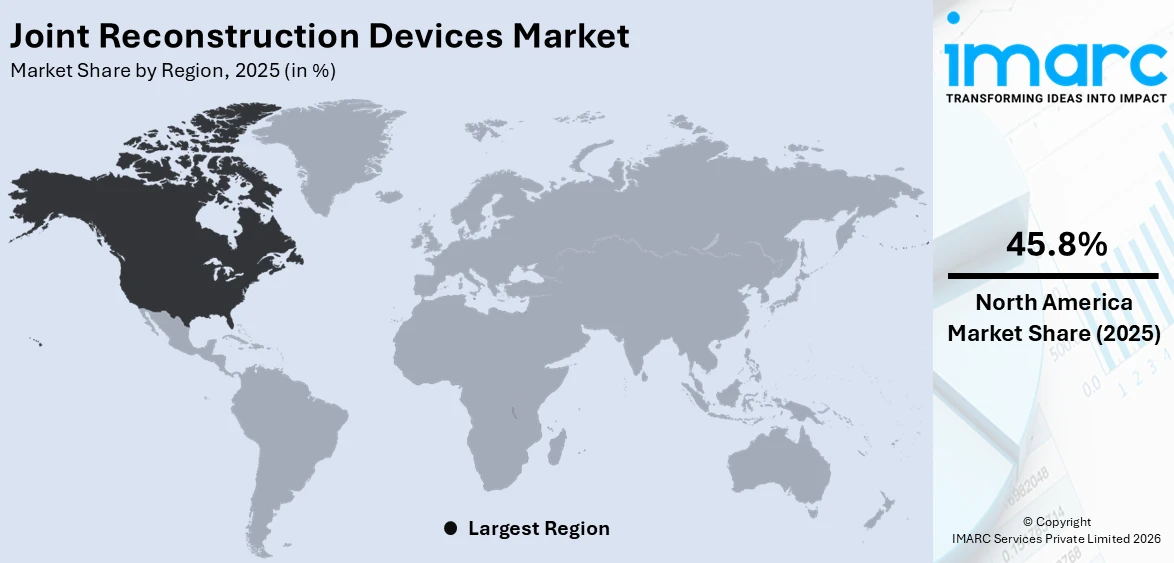

The global joint reconstruction devices market size was valued at USD 30.0 Billion in 2025. The market is projected to reach USD 43.8 Billion by 2034, exhibiting a CAGR of 4.16% from 2026-2034. North America currently dominates the market, holding a market share of over 45.8% in 2025. The market is witnessing consistent growth fueled by demographic changes, innovative technology, and increasing rates of joint injuries. Growing demand for minimal invasive procedures and innovative implants is transforming the treatment scenario, and improvements in healthcare infrastructure are making orthopedic care more accessible globally. The market is also boosted by improving patient awareness and focus on preservation of mobility. These factors combined make the environment conducive to growth, reinforcing the global outlook and driving the competitive positioning of the joint reconstruction devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 30.0 Billion |

|

Market Forecast in 2034

|

USD 43.8 Billion |

| Market Growth Rate 2026-2034 | 4.16% |

One of the key global drivers for the joint reconstruction devices market is the continuous enhancement of healthcare infrastructure and access to expert orthopedic treatment in both developed and emerging economies. As nations invest in developing surgical centers, resident training in orthopedic surgery, and the implementation of sophisticated medical technology, patients highly have access to advanced joint treatment. Increased insurance coverage, rising healthcare spending, and expanded emphasis on musculoskeletal well-being are all combining to make joint reconstruction more accessible. In addition, the international focus on developing post-surgical recovery and rehabilitation is spurring the use of devices that facilitate faster and more streamlined results. The adoption of global best practices for orthopedic treatment is also creating increased patient awareness, further fueling demand. Combined, these developments are creating a solid foundation for expansion, with the joint reconstruction devices market receiving a boost from enhanced international healthcare delivery systems.

To get more information on this market Request Sample

With a market share of 85.70% in 2024, the United States is a key driver of the joint reconstruction devices market growth, driven by an emphasis on active lifestyles and physical well-being. High levels of people participating in sports, fitness, and leisure activities have resulted in increased cases of joint-related injuries that are in need of surgical correction. As per sources, in November 2024, Johnson & Johnson MedTech launched advanced joint reconstruction devices, including VELYS™ Robotic-Assisted UKA and WATSON EXTRACTION SYSTEM™, enhancing surgical precision and efficiency in the United States joint reconstruction devices market. Moreover, the focus within the health system on maintaining mobility, independence, and overall quality of life has helped to increase the common acceptance of joint reconstruction procedures. The availability of cutting-edge medical facilities and surgical experience further guarantees access to innovative solutions for both common and challenging reconstructions. Furthermore, patient awareness programs and education initiatives further point to the long-term advantages of these procedures, leading to increased uptake. Together, these elements support the strong growth climate in the United States of the joint reconstruction devices market.

Joint Reconstruction Devices Market Trends:

Increasing Population of Geriatrics Spurring Joint Reconstruction Demand

The rise in geriatric populations across the globe is a significant driver of demand for joint reconstruction procedures. With advancing age, the incidence of degenerative diseases like osteoarthritis, osteoporosis, and other joint pathologies increases immensely, resulting in a tremendous rise in surgical procedures. The world population aged 65 years and above is projected to be 2.2 billion by the late 2070s, outnumbering the population of people under the age of 18 years. This population change is likely to redefine healthcare need, especially in orthopedic management. Older individuals usually need knee, hip, shoulder, and ankle joint replacements because of wear and tear on the bones and cartilage that occurs with aging. With the rise in life expectancy, the focus on enhancing the quality and mobility of the elderly also increases the demand for advanced surgical techniques. The amplifying demand thus reflects the importance of population changes in driving the market for joint reconstruction worldwide.

Technical Innovations Shaping Joint Reconstruction

Fast-paced technological innovations, including 3D printing, robotics, and augmented reality (AR), are transforming the joint reconstruction industry. 3D printing has become an innovation instrument for creating personalized biomodels and implants that mirror patient anatomy, enabling surgeons to prepare and rehearse complicated surgical operations with increased accuracy. This is especially useful for joint replacement for infections or failure of prior implants. In addition, robotic surgery is highly being adopted in hip and knee arthroplasty, providing greater precision in component alignment, intraoperative real-time feedback regarding soft tissue balance, and more reliable restoration of offset and hip length. With more than 6,700 robotic surgery platforms installed globally, their use is increasing steadily in healthcare institutions. These technologies enhance surgical results as well as minimize complications, rehabilitation periods, and revision rates, thus being the focus of joint reconstruction devices market trends development and playing an important role in market growth.

Increased Cases of Injuries and Ankle Disorders

In addition to conditions that accompany aging, injuries that result from accidents and sports are also playing a part in boosting the demand for joint reconstruction surgery. Bone fractures, dislocations, and ligament sprains typically need surgical procedures involving implants and reconstructive surgery to restore function. This is especially so in younger age groups participating in high-impact sports, where joint injuries are prevalent. Also contributing as a strong market driver is ankle pathology. Increasingly, more people are undergoing total ankle replacement (TAR) and tibiotalar arthrodesis (TTA) for the surgical treatment of advanced ankle arthritis, historically being tougher to treat than knee or hip problems. Heightened demand for the ankle-specific procedure highlights the expanding range of orthopedic interventions, not just addressing age-related decline, but also trauma and injury-induced conditions. These factors collectively continue to reinforce market growth by increasing the patient pool in need of advanced surgical intervention.

Joint Reconstruction Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global joint reconstruction devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on technique, joint type, and end user.

Analysis by Technique:

- Joint Replacement

- Implants

- Bone Graft

- Osteotomy

- Arthroscopy

- Resurfacing

- Arthrodesis

- Others

Joint replacement with 52.34% share in 2025 was the dominant category in the joint reconstruction devices market outlook, underpinned by its extensive use in many joints including hips, knees, shoulders, and ankles. The surgery is also well known for bringing back mobility and alleviating long-standing pain related to degenerative disease, trauma, or complicated musculoskeletal disorders. Joint replacement is also driven by the fact that there are sophisticated implants that are made for endurance and compatibility with the body, which can be used in patients of diverse groups. Increasing use of less invasive methods also helped in better outcomes in recovery time, prompting people to seek these operations more. Moreover, the rapid growth in the number of orthopedic care facilities around the world, along with added emphasis on patient-specific treatment planning, has made joint replacement the leading segment. Its leadership stems from its extensive clinical application and sustained adoption, which has contributed immensely to the overall joint reconstruction devices market growth.

Analysis by Joint Type:

- Knee

- Hip

- Shoulder

- Ankle

- Others

Knee reconstruction, which had 45.45% share in 2025, was at the forefront in the joint reconstruction devices market. The knee is still one of the most frequently treated joints because it is so prone to wear and tear, sports trauma, and degenerative diseases that weaken movement and stability. Improved implant design, navigation systems, and robotics are making knee reconstruction more accurate, enhancing long-term results for patients. The growing demand is also a result of the significance of knee function in preserving mobility, independence, and levels of daily activity, making it a high priority for orthopedic treatment. Patient demand fueled by awareness of surgical success rates and availability of specialized rehabilitation programs has also helped to fuel the high demand for knee devices. With healthcare systems allocating more importance to mobility-related interventions, knee reconstruction remains to play a leading role and reinforce its proportion and enhance its contribution to the global joint reconstruction devices market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers (ASCs)

- Others

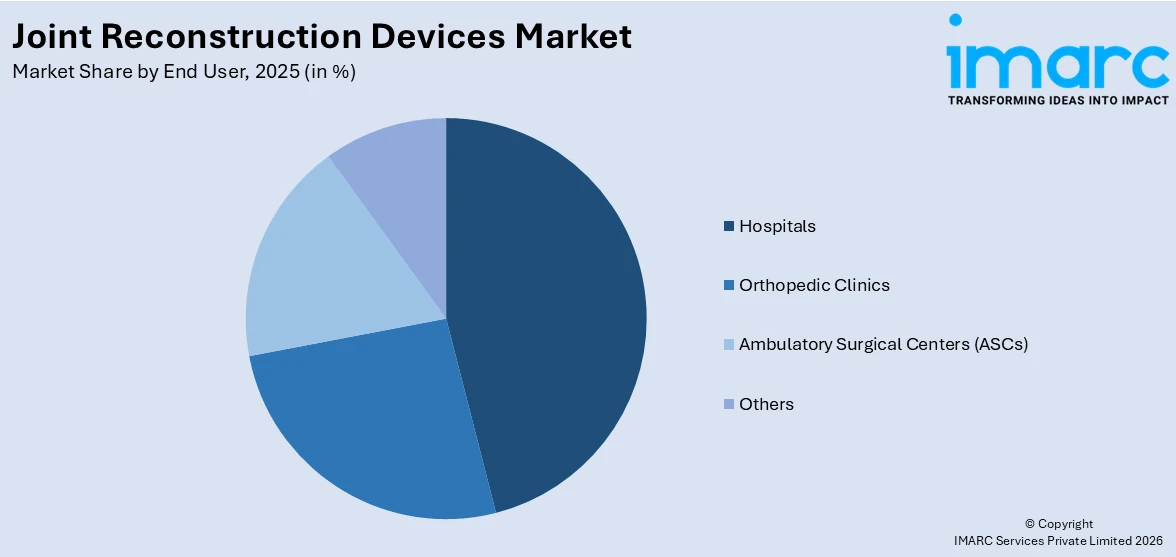

Hospitals are the largest end-user segment, with full-range orthopedic care backed by state-of-the-art facilities, experienced surgeons, and access to cutting-edge devices. They perform all kinds of joint reconstruction procedures, ranging from the complex to simple ones, and enjoy better patient flow, making them the focus of the joint reconstruction devices market.

Orthopedic clinics are instrumental in delivering specialized patient-centric care for joint disorders. Orthopedic clinics are going the extra mile to adopt cutting-edge diagnostic equipment and minimally invasive surgical procedures, delivering customized treatment plans that enhance patient results. Their emphasis on specialty orthopedic care makes them a prominent segment in the joint reconstruction devices market.

Ambulatory surgery centers are becoming more recognized because of their cost-effective, efficient, and outpatient-oriented services. They provide support to patients who are looking for faster procedures and quicker recovery, especially for minimally invasive joint reconstructions. ASCs are supported by increasing patient desire for convenient, affordable care, solidifying their role in the joint reconstruction devices market environment.

The others segment comprises rehabilitation facilities and specialty care centers offering post-surgical care and joint health solutions. These centers enable recovery and restoration of mobility, supplementing surgical procedures conducted in hospitals and clinics. By servicing post-operative requirements, this segment enhances the value proposition of the care continuum within the joint reconstruction devices market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Accounting for 45.8% share in 2025, North America dominated the worldwide joint reconstruction devices market, bolstered by its sophisticated healthcare infrastructure, high rate of technological uptake, and robust clinical experience in orthopedic procedures. The area is blessed with well-developed surgical centers, qualified orthopedic surgeons, and availability of advanced treatment technologies enhancing patient care. Quality of life, preservation of mobility, and quicker recovery rates are emphasized very heavily in leading demand for solutions in joint reconstruction on a regular basis. Moreover, population-friendly reimbursement models, insurance coverage, and widespread use of minimally invasive procedures keep the region at the leading edge. North America also witnesses heavy investment in research and development, further driving the rollout of next-generation devices enhancing precision and patient results. The amalgamation of these factors has guaranteed dominance of the region, positioning it as a focal point for innovation and demand in the joint reconstruction devices market, while establishing the yardsticks for global adoption trends.

Key Regional Takeaways:

United States Joint Reconstruction Devices Market Analysis

United States is witnessing strong demand for joint reconstruction devices adoption due to growing investment in robotic-assisted surgery, which is transforming orthopedic procedures. Increasing preference for minimally invasive techniques and precision-based treatments is driving hospitals and surgical centers to allocate higher budgets for advanced robotic platforms. This trend is encouraging greater use of implants and prosthetics in knee, hip, and shoulder reconstruction. Rising awareness of improved recovery outcomes and reduced complications further supports market expansion. Continuous investment in training and integration of robotics into orthopedic practices is also enhancing surgical accuracy. Surgeons are increasingly relying on these technologies to improve patient satisfaction and treatment efficiency. With ongoing advancements, robotic-assisted surgery is becoming a central factor for joint reconstruction devices adoption.

Asia Pacific Joint Reconstruction Devices Market Analysis

Asia-Pacific is experiencing rising joint reconstruction devices adoption due to growing investment in healthcare sector, which is enabling expansion of surgical infrastructure. According to India Brand Equity Foundation, the Indian government has allocated Rs. 99,858 crore (USD 11.50 Billion) to the healthcare sector in the Union Budget 2025-26 for the development, maintenance, and enhancement of the country's healthcare system. Rapid economic development has resulted in better funding for hospitals and medical centers, supporting access to advanced orthopedic solutions. Healthcare modernization initiatives are improving surgical capabilities, while growing demand for joint replacements is leading to wider availability of devices. The healthcare sector investment is encouraging companies to expand production and distribution, making devices more accessible. Rising patient awareness about effective treatment options is further accelerating adoption.

Europe Joint Reconstruction Devices Market Analysis

Europe shows increasing joint reconstruction devices adoption due to growing geriatric population, which is significantly impacting demand for knee, hip, and shoulder procedures. According to WHO, the population aged 60 and older is rapidly growing in the WHO European Region. In 2021, there were 215 Million by 2030, it is projected to be 247 Million, and by 2050, over 300 Million. An aging population is more prone to degenerative joint conditions, creating consistent need for advanced reconstruction solutions. Healthcare providers are addressing these needs by adopting innovative implants and surgical techniques that improve mobility and reduce recovery time. The growing geriatric population is also prompting higher demand for revision surgeries, further boosting device utilization. Hospitals and clinics are expanding their orthopedic services to handle rising patient volumes. As longevity continues to rise, the need for effective joint reconstruction options will intensify.

Latin America Joint Reconstruction Devices Market Analysis

Latin America is witnessing higher joint reconstruction devices adoption due to growing investment and government support in the healthcare sector. For instance, budget allocation for Brazil’s Unified Health System is expected to increase by 6.2% in 2025. Expanding healthcare budgets and favorable policies are driving the modernization of hospitals and surgical departments, improving access to advanced orthopedic devices. Increased emphasis on joint health is encouraging healthcare institutions to adopt innovative reconstruction solutions. Government support in funding infrastructure upgrades and promoting medical training is further enhancing surgical outcomes, contributing to steady adoption of devices across the region.

Middle East and Africa Joint Reconstruction Devices Market Analysis

Middle East and Africa are showing increased joint reconstruction devices adoption due to growing healthcare facilities and privatization in the healthcare sector. For instance, the Saudi healthcare sector is experiencing unprecedented privatization as part of Vision 2030, with over 290 hospitals and 2,300 health institutions transitioning into private operations. Expansion of private hospitals and clinics is improving access to advanced orthopedic care, while healthcare facilities are being upgraded with specialized surgical units. Privatization is attracting investment in high-quality implants and technologies, allowing more patients to benefit from reconstruction procedures.

Competitive Landscape:

The competitive market scenario of the joint reconstruction devices market is influenced by ongoing innovation, strategic alliances, and increased use of sophisticated surgical technology. The players in the market are actively investing in research and development to create implants and devices that provide enhanced biocompatibility, strength, and patient-specificity. The emphasis on minimally invasive procedures has also heightened competition as firms battle to provide solutions that cut down on recovery time while improving the accuracy of surgery. Global and regional firms are also consolidating their foothold by partnering with healthcare providers, building up distribution channels, and customizing products to suit varied patient demands in varying geographies. Moreover, the growing need for digital integration, including robotics and surgical navigation systems, is prompting companies to invest in incorporating innovative tools in their product portfolios. These forces indicate an emerging scenario where innovation, accessibility, and quality continue to play a pivotal role in determining the joint reconstruction devices market forecast in the next few years.

The report provides a comprehensive analysis of the competitive landscape in the joint reconstruction devices market with detailed profiles of all major companies, including:

- Allegra

- Conformis

- Conmed Corporation

- Enovis

- Exactech Inc.

- KYOCERA Medical Technologies, Inc.

- Medacta International SA

- Medical Device Business Services, Inc. (Johnson & Johnson)

- MicroPort Orthopedics, Inc.

- Smith & Nephew

- Zimmer Biomet

Latest News and Developments:

- July 2025: Care Hospitals, Hyderabad unveiled the AI-powered Stryker Mako Robotic System, which assisted in robotic-assisted joint reconstruction devices surgeries by combining 3D CT-based planning with real-time guidance to enhance precision, reduce post-operative pain, and enable faster recovery.

- July 2025: Sarvodaya Hospital in Greater Noida introduced a fully active Joint Replacement Robot, marking a significant advancement in joint reconstruction devices as it enhanced surgical precision with AI-powered 3D planning, minimized recovery time, and reflected the growing adoption of robotic-assisted technologies in orthopaedic care.

- June 2025: Johnson & Johnson MedTech announced the launch of its KINCISE™ 2 Surgical Automated System, a next-generation innovation in joint reconstruction devices that expanded surgical applications across primary and revision hip and knee procedures while aiming to improve efficiency, reduce surgeon fatigue, and streamline workflows compared to traditional methods.

- April 2025: OSSTEC, a London-based start-up, raised USD 3.23 Million to launch its 3D printed joint reconstruction devices, developed from a decade of research at Imperial College London, aiming to reduce implant failure risks and improve outcomes for knee replacement patients.

- January 2025: A J Hospital and Research Centre launched Smith+Nephew’s robotic joint reconstruction devices, marking a milestone in orthopaedic care with advanced 3D imaging and surgeon-driven robotics that enhanced precision in hip and knee replacement surgeries and promised faster recovery and improved patient outcomes.

Joint Reconstruction Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Techniques Covered | Joint Replacement (Implants, Bone Graft), Osteotomy, Arthroscopy, Resurfacing, Arthrodesis, Others |

| Joint Types Covered | Knee, Hip, Shoulder, Ankle, Others |

| End Users Covered | Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers (ASCs), Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allegra, Conformis, Conmed Corporation, Enovis, Exactech Inc., KYOCERA Medical Technologies, Inc., Medacta International SA, Medical Device Business Services, Inc. (Johnson & Johnson), MicroPort Orthopedics, Inc., Smith & Nephew, Zimmer Biomet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the joint reconstruction devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global joint reconstruction devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the joint reconstruction devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Joint Reconstruction Devices Market Report

The joint reconstruction devices market was valued at USD 30.0 Billion in 2025.

The joint reconstruction devices market is projected to exhibit a CAGR of 4.16% during 2026-2034, reaching a value of USD 43.8 Billion by 2034.

The joint reconstruction devices market is driven by the rising prevalence of joint disorders, growing geriatric populations, and increasing cases of sports-related injuries. Technological advancements, including robotics and personalized implants, are enhancing surgical precision and recovery outcomes. Expanding healthcare infrastructure, greater patient awareness, and the preference for minimally invasive procedures further accelerate adoption, strengthening overall market growth worldwide.

North America currently dominates the joint reconstruction devices market, accounting for a share of 45.8%, driven by its well-developed healthcare system, powerful clinical experience, and extensive adoption of advanced surgical technologies. Favorable reimbursement policies and insurance coverage also boost the adoption of joint reconstruction procedures. The region's patient outcome improvement focuses and investment in research are also supportive of its leadership globally.

Some of the major players in the joint reconstruction devices market include Allegra, Conformis, Conmed Corporation, Enovis, Exactech Inc., KYOCERA Medical Technologies, Inc., Medacta International SA, Medical Device Business Services, Inc. (Johnson & Johnson), MicroPort Orthopedics, Inc., Smith & Nephew, Zimmer Biomet, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)