Kitchen Sinks Market Size, Share, Trends and Forecast by Installation, Number of Bowl, Material, End User, and Region, 2026-2034

Kitchen Sinks Market Size and Share:

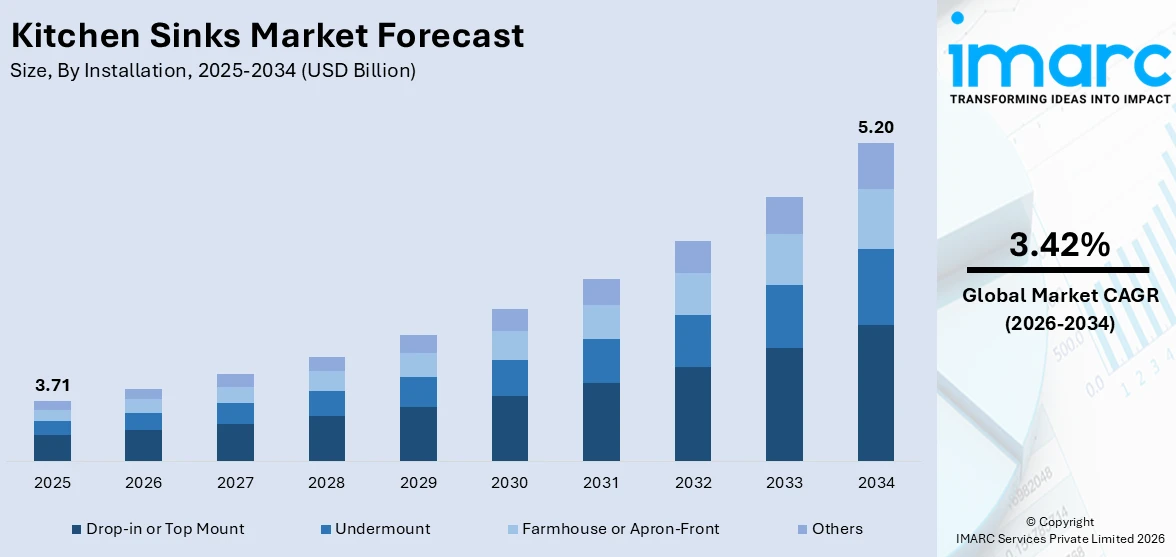

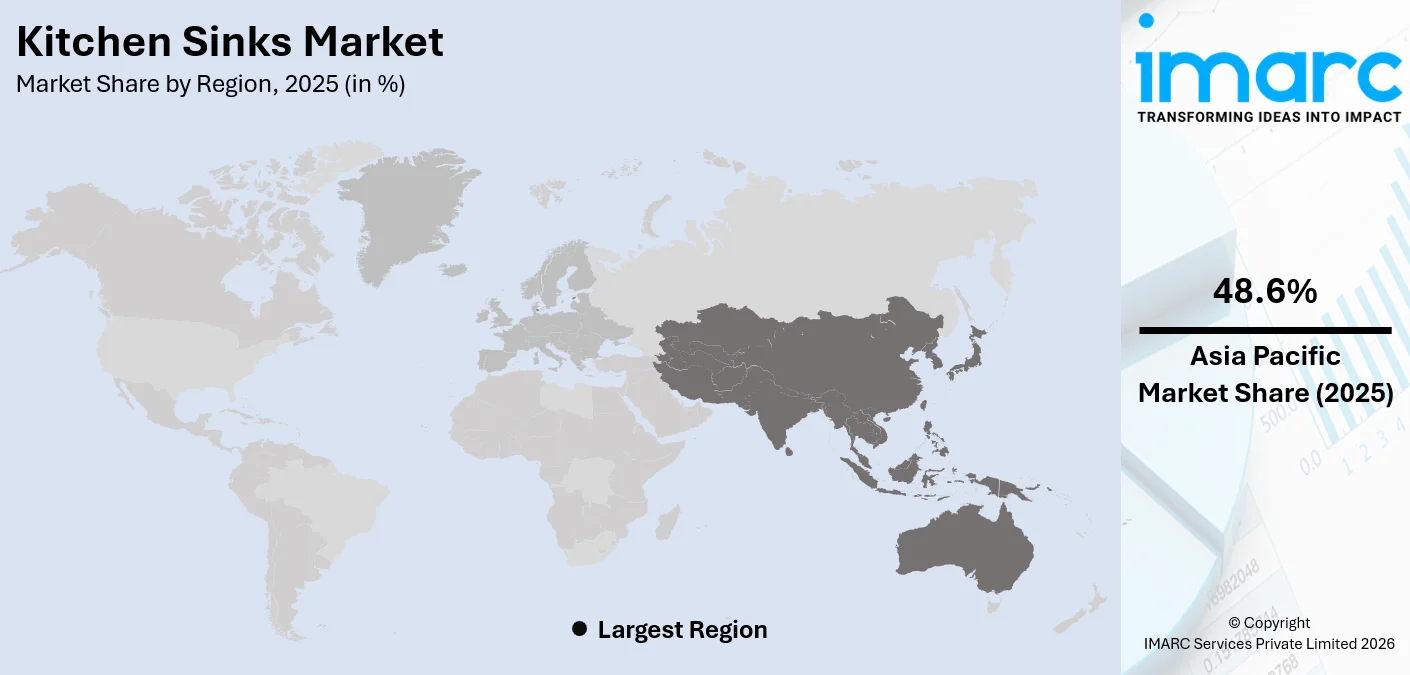

The global kitchen sinks market size was valued at USD 3.71 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 5.20 Billion by 2034, exhibiting a CAGR of 3.42% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 48.6% in 2025. The region's dominance is underpinned by rapid urbanization, robust residential and commercial construction activity, and rising consumer spending on modern kitchen upgrades, particularly across high-growth economies, collectively bolstering the kitchen sinks market share.

The global kitchen sinks market is driven by several interconnected forces shaping demand across residential and commercial sectors worldwide. Rising urbanization continues to catalyze new housing construction, directly increasing the installation of modern kitchen fixtures including sinks. The growing preference for premium, aesthetically sophisticated kitchen designs has elevated consumer expectations, prompting homeowners and commercial operators to invest in high-quality, multifunctional sink solutions. Increasing awareness of water conservation and sustainability has accelerated demand for eco-friendly sink materials such as recycled stainless steel and granite composite, which align with green building standards promoted by governments and regulatory agencies globally. The ongoing proliferation of modular kitchen concepts, particularly among urban middle-class households in emerging economies, further amplifies demand. Additionally, the expansion of the foodservice and hospitality sectors contributes significantly to kitchen sinks market growth, as restaurants, hotels, and catering facilities consistently require high-capacity, hygienic stainless-steel sinks to meet operational standards.

The United States has emerged as a major region in the kitchen sinks market owing to many factors. A deeply embedded culture of home improvement drives sustained investment in kitchen remodeling and renovation, making the US one of the most robust markets for premium kitchen fixtures. A broad network of specialty retailers, home improvement chains, and online platforms provides consumers with extensive product access, fueling competitive innovation across installation types, materials, and configurations. The preference for contemporary, open-concept kitchen designs has increased the uptake of undermount and workstation sink styles, which offer clean aesthetic integration and improved functionality. Favorable trends in homeownership among younger demographics, combined with rising home equity, support higher renovation expenditure.

To get more information on this market Request Sample

Kitchen Sinks Market Trends:

Growing Smart Sink Adoption

The integration of smart technology into kitchen sinks represents one of the most transformative developments in the global market. Modern consumers increasingly seek fixtures that offer connectivity, convenience, and hygiene benefits that traditional sinks cannot deliver. Smart sinks equipped with touchless faucets, voice-activated water controls, integrated sensors for leak detection, real-time water temperature monitoring, and built-in water quality filtration systems are rapidly transitioning from niche luxury items to mainstream residential and commercial fixtures. This shift is particularly pronounced in high-income urban segments where smart home ecosystems are already established. Demand from tech-savvy homeowners, upscale hospitality venues, and commercial kitchens seeking operational efficiency and hygiene compliance has become a consistent market driver. In February 2025, Delta Faucet Company introduced the Clarifi Under Sink Water Filtration System at the Kitchen and Bath Industry Show in Las Vegas, offering certified filtration that reduces chlorine and microplastics from in-home water supplies, with the product available for commercial shipment from October 2025 onward. The growing integration of smart features into sink design is reshaping product development priorities across manufacturers, driving investment in advanced materials, electronic components, and IoT-compatible infrastructure.

Surge in Workstation and Multifunctional Sink Designs

A pronounced shift toward workstation sinks is redefining kitchen sink market trends, as consumers and commercial operators prioritize efficiency, space optimization, and versatility in kitchen workflows. Workstation sinks feature integrated tracks along the rim that accommodate built-in accessories such as sliding cutting boards, colanders, drying racks, and mixing bowls, effectively transforming the sink basin into a centralized food preparation zone. This design philosophy has been particularly well received in urban households with limited counter space and in commercial kitchens where workflow efficiency is a critical operational requirement. The concept appeals to a growing demographic of home chefs and culinary professionals who demand more than a basic washing utility from their kitchen fixtures. Farmhouse and apron-front styles have also experienced renewed consumer interest, as homeowners pursue rustic aesthetics blended with modern functional capabilities.

Rising Preference for Sustainable Sink Materials

The sustainability imperative is substantially influencing consumer product choices in the kitchen sinks market forecast period, as environmental awareness grows among both residential buyers and commercial procurement teams. Demand for sinks manufactured from eco-certified materials, including recycled stainless steel, quartz composite, and fireclay, has increased noticeably as buyers seek products that minimize carbon footprint and align with green building certifications such as LEED. Stainless steel's inherent recyclability and durability make it a preferred eco-conscious choice, while quartz composite sinks offer scratch resistance and long product lifespans that reduce replacement frequency and associated environmental waste. Manufacturers are responding by expanding sustainable product lines and securing third-party environmental certifications to validate product claims. Government incentives promoting green building standards across North America, Europe, and parts of Asia Pacific have further elevated the strategic importance of sustainable design in the kitchen fixture category.

Kitchen Sinks Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global kitchen sinks market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on installation, number of bowl, material, and end user.

Analysis by Installation:

- Drop-in or Top Mount

- Undermount

- Farmhouse or Apron-Front

- Others

Drop-in or top mount holds 46.5% of the market share. Drop-in or top mount sinks represent the most widely adopted installation type globally due to their ease of installation, broad compatibility with existing countertops, and cost-effective replacement potential. These sinks are designed to rest on top of the countertop surface, with the rim overlapping the counter edge, making them suitable for virtually any countertop material including laminate, tile, and granite without the need for specialized cutting or adhesive systems. The simplicity of installation appeals to both professional contractors and do-it-yourself homeowners undertaking kitchen renovations on moderate budgets. Their widespread availability across diverse price points and material categories, including stainless steel, porcelain, and composite options, makes drop-in sinks a versatile choice for residential kitchens, commercial food preparation areas, and institutional settings. The accessibility of this installation format further supports its dominance in replacement markets where minimal countertop modification is preferred. Retailers and online platforms carry extensive assortments of top mount sinks, amplifying their availability and consumer reach globally.

Analysis by Number of Bowl:

- Single

- Double

- Multiple

Single leads the market with a share of 49.6%. The single-bowl configuration commands the largest share of the global kitchen sinks market, driven by its versatility, clean aesthetic, and practical utility across residential and commercial applications. Single-bowl sinks feature one large, uninterrupted basin that accommodates oversized cookware, baking trays, and large pots with greater ease than divided configurations, making them particularly popular among frequent home cooks and professional culinary operators. The spacious basin design also supports the workstation sink trend, as the unobstructed interior provides an ideal foundation for sliding accessories and integrated prep tools. In modern kitchen designs characterized by minimalist aesthetics and open layouts, the single-bowl sink's clean profile integrates seamlessly, enhancing spatial coherence. Additionally, single-bowl configurations are available across all primary material categories, stainless steel, fireclay, quartz composite, and copper, providing consumers with maximum customization flexibility regardless of design preference or budget tier. Commercial kitchens and foodservice facilities also favor single-bowl configurations for high-volume dishwashing and food preparation workflows.

Analysis by Material:

- Non-metal

- Granite

- Fireclay

- Quartz

- Others

- Metal

- Stainless Steel

- Copper

- Others

Metal dominates the market, with a share of 52.2%. The metal segment, led by stainless steel as the dominant subsegment, maintains its commanding position in the global kitchen sinks market due to the unmatched combination of durability, hygienic properties, corrosion resistance, and design adaptability that metallic materials provide. Stainless steel in particular is highly favored across residential, commercial, and institutional applications because it is non-porous, easy to clean, resistant to heat and chemical exposure, and inherently recyclable, aligning with growing sustainability mandates in both consumer and regulatory contexts. Copper sinks occupy a premium niche within the metal segment, prized for their natural antimicrobial properties and distinctive aesthetic appeal in high-end residential kitchens. The broad compatibility of metal sinks with all installation types, like drop-in, undermount, and farmhouse and their availability across a wide price range further reinforce segment dominance. Technological advancements in metal finishing, including nano-coatings that reduce fingerprint visibility and advanced noise-dampening pad systems, have further enhanced the appeal of metal sinks in modern kitchen designs, supporting sustained segment leadership.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

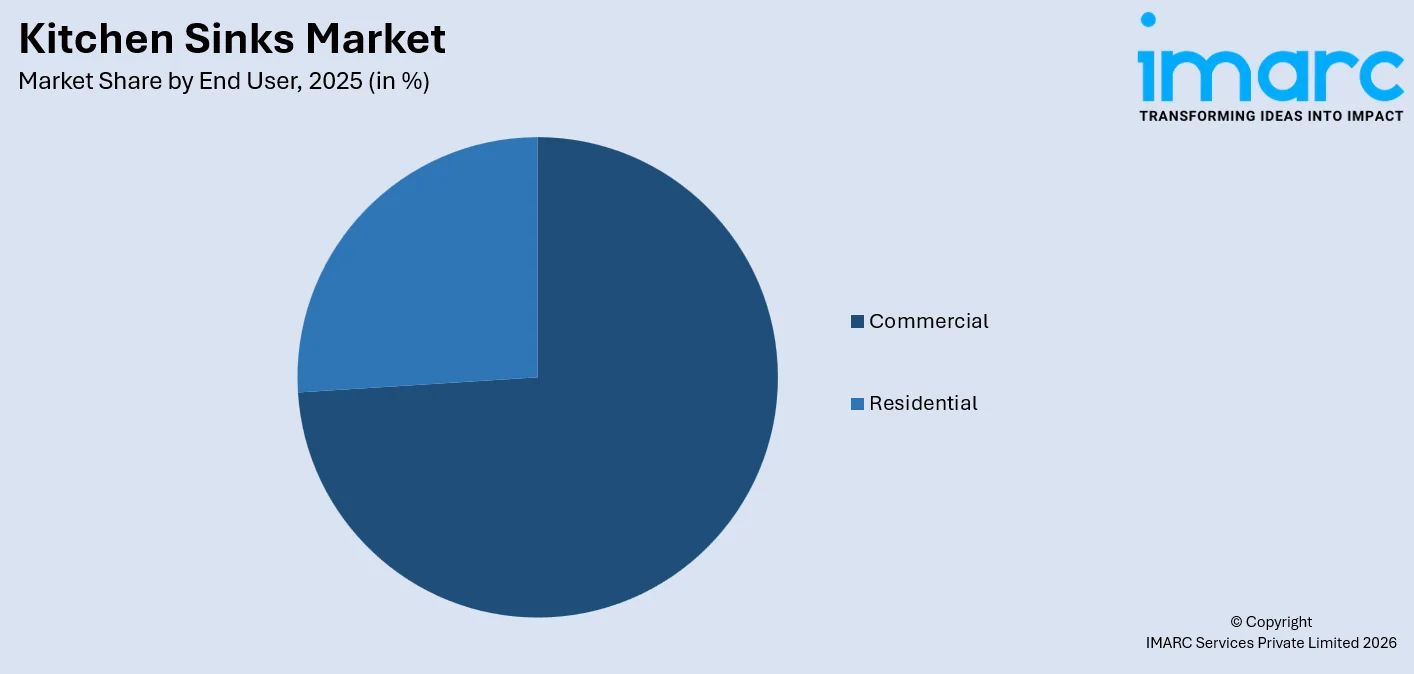

Commercial represents the leading segment, with a market share of 73.7%. The commercial end-user segment holds the dominant position in the global kitchen sinks market, driven by the extensive and continuous demand from restaurants, hotels, hospitals, institutional catering facilities, and other high-footfall food service environments. Commercial kitchens require specialized, high-capacity sink configurations built to withstand intensive daily use, strict hygiene regulations, and frequent sanitation protocols, making durable stainless steel multi-compartment sinks the standard fixture across this segment. The global expansion of the hospitality, quick-service restaurant, and healthcare sectors has created sustained procurement volumes for commercial-grade kitchen sinks, with new establishment openings and renovations of existing facilities contributing to consistent replacement demand. Regulatory frameworks governing food safety and sanitation in commercial kitchens, administered by health departments, food safety authorities, and building codes across major markets, mandate the installation of compliant sink configurations, creating non-discretionary demand that is largely insulated from residential market cycles. The institutional procurement scale of commercial buyers also supports large-volume, standardized supply agreements with manufacturers.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific, accounting for 48.6% of the share, holds the leading position in the market. The region's dominant position is driven by its extraordinary scale of residential and commercial construction activity, particularly across China, India, South Korea, and emerging Southeast Asian economies. Rapid urbanization has generated massive and sustained demand for new housing units, each requiring kitchen fixtures including sinks. The expansion of the hospitality and quick-service restaurant sectors across major Asia Pacific tourism hubs further amplifies commercial kitchen sink demand. Rising household incomes have enabled growing segments of the middle class to invest in premium modular kitchen designs that incorporate modern, aesthetically appealing sink configurations. Government-backed affordable housing initiatives in India and China have also contributed significant volumes of kitchen sink installations at the entry and mid-market price tiers. Strong domestic manufacturing capacity, particularly in China, supports competitive pricing that reinforces Asia Pacific's capacity to serve both internal demand and global export markets.

Key Regional Takeaways:

North America Kitchen Sinks Market Analysis

North America represents a significant and mature market for kitchen sinks, underpinned by the region's well-established home improvement culture, high homeownership rates, and sustained investment in kitchen remodeling and renovation. The United States dominates regional demand, supported by a wide retail infrastructure spanning specialty kitchen showrooms, national home improvement chains, and rapidly growing e-commerce platforms that provide consumers with extensive product selection across all price points and material categories. Canada contributes a meaningful share of regional demand, driven by strong residential construction activity in major metropolitan centers including Toronto, Vancouver, and Calgary, where new apartment and condominium developments consistently drive kitchen fixture procurement. The region's preference for premium materials such as stainless steel and quartz composite, combined with growing interest in workstation and undermount sink designs, supports consistently above-average per-unit spending. Demand from the commercial foodservice sector in North America, encompassing an extensive network of restaurants, institutional cafeterias, and healthcare facilities, provides a stable, non-discretionary demand base that is relatively insulated from residential market fluctuations.

United States Kitchen Sinks Market Analysis

The United States holds 80.70% of the market share in North America. The US kitchen sinks market benefits from one of the world's most active and well-funded home renovation ecosystems, where kitchen remodeling consistently ranks among the highest-priority and highest-budget projects undertaken by homeowners. Rising home equity levels, with homeowners gaining an average of approximately USD 30,000 annually in equity gains over the past five years, have provided substantial capital for renovation investment, directly supporting premium kitchen sink purchases. Consumer preference in the US has increasingly shifted toward undermount and workstation sink designs that offer cleaner aesthetics and enhanced functional utility, while stainless steel retains its dominant material share due to its durability and alignment with contemporary design trends. The commercial foodservice sector, comprising hundreds of thousands of restaurants, hotels, schools, and healthcare facilities, generates continuous and substantial replacement demand for high-specification stainless steel sinks. According to the 2025 US Houzz and Home Study surveying nearly 22,000 respondents, more than half of US homeowners undertook a remodeling project in 2024, with major kitchen renovations sustaining median spending levels of USD 55,000 for large-format kitchens, reflecting robust and ongoing demand for premium kitchen fixtures including sinks across residential segments.

Europe Kitchen Sinks Market Analysis

Europe maintains a substantial share of the global kitchen sinks market outlook, characterized by strong consumer demand for premium, design-forward, and sustainable kitchen fixtures that reflect the region's emphasis on quality craftsmanship and environmental responsibility. Germany leads European consumption, supported by a robust economy, high household income levels, and a strong domestic manufacturing ecosystem that includes internationally recognized premium brands producing innovative composite and stainless-steel sinks. France, the United Kingdom, Italy, and Spain represent significant individual country markets, with Italy contributing particularly strong demand from its heritage of artisan kitchen design and high-end residential construction. The European Green Deal has accelerated regulatory pressures favoring environmentally responsible materials in building products, supporting growth in composite and recycled-material sink categories. Stringent European Union standards governing material safety, water efficiency, and plumbing fixture performance shape product specifications across the market. The renovation and retrofitting of existing residential housing stock, driven by energy efficiency imperatives and changing household demographics, sustains a steady pipeline of kitchen sink replacement demand throughout Western Europe.

Asia-Pacific Kitchen Sinks Market Analysis

Asia Pacific commands the largest regional share of the global kitchen sinks market, driven by a unique convergence of population scale, urbanization velocity, and accelerating economic development across multiple high-growth markets. China is the region's dominant contributor, with extensive residential construction activity, a significant domestic manufacturing base, and rising middle-class household investments in premium kitchen modernization. India is the region's fastest-expanding market, propelled by government-backed affordable housing programs and rapid urban population growth that have generated substantial kitchen fixture demand across newly constructed residential units in cities and semi-urban areas. Southeast Asian economies including Indonesia, Vietnam, and the Philippines are experiencing accelerating construction pipelines supported by infrastructure investment and demographic expansion, creating growing addressable markets for both entry-level and mid-tier kitchen sink products. Rising household incomes across the region have enabled broader consumer segments to invest in modular kitchen designs that incorporate aesthetically appealing, functional sink configurations. The hospitality and quick-service restaurant sectors across major Asia Pacific tourism hubs further amplify commercial kitchen sink procurement volumes, as the region's expanding travel and foodservice industries require continuous fixture installations and replacements to meet operational and hygiene compliance requirements.

Latin America Kitchen Sinks Market Analysis

Latin America is an emerging growth market for kitchen sinks, driven by urbanization, rising disposable incomes, and expanding middle-class investment in modern kitchen upgrades across Brazil, Mexico, and other developing economies. Brazil accounts for the largest share of regional demand, supported by an active real estate development sector and a consumer base increasingly oriented toward contemporary kitchen fixtures. Mexico's growing foodservice and hospitality sectors, particularly in major tourism hubs and industrial cities, contribute consistent commercial kitchen sink procurement volumes. Government housing programs and private sector real estate development initiatives across the region continue to generate new residential construction activity, providing a reliable demand base for entry- and mid-market kitchen sink installations.

Middle East and Africa Kitchen Sinks Market Analysis

The Middle East and Africa market for kitchen sinks is growing steadily, supported by ambitious government-led infrastructure and real estate development programs, particularly in the Gulf Cooperation Council countries where Vision 2030 initiatives in Saudi Arabia are fueling substantial residential and commercial construction pipelines. The UAE and Saudi Arabia represent the region's most significant individual markets, with high-end residential projects, luxury hospitality developments, and large-scale institutional facilities generating demand for premium commercial and residential kitchen sink solutions. Africa's growing urban population and expanding middle class across economies such as South Africa, Nigeria, and Kenya are gradually building a foundation for broader kitchen fixture market development, particularly in the residential and institutional sectors.

Competitive Landscape:

The global kitchen sinks market features a moderately consolidated competitive landscape, with a mix of established international manufacturers and regional specialists vying for market share through product innovation, design differentiation, and strategic distribution partnerships. Leading players invest heavily in materials research to develop advanced composite formulations, nano-coating technologies, and sustainable material certifications that differentiate their product portfolios. Manufacturers have increasingly adopted digital marketing strategies and influencer-led campaigns to engage renovation-active consumer segments, while simultaneously deepening trade channel relationships with architects, interior designers, and commercial contractors who influence specification decisions. The market has seen growing interest in smart sink integration as a premium category differentiator, with brands competing to offer the most comprehensive IoT-compatible product ecosystems. Expansion into high-growth emerging markets, particularly across Asia Pacific and the Middle East, represents a key strategic priority for global players seeking to offset maturation pressures in established North American and European markets. Some manufacturers face input cost pressures from fluctuating raw material prices for stainless steel and composite materials, necessitating supply chain optimization to protect margin structures.

The report provides a comprehensive analysis of the competitive landscape in the kitchen sinks market with detailed profiles of all major companies, including:

- BLANCO GmbH + Co KG

- Carysil Limited

- Crown Sink

- Delta Faucet Company (Masco Corporation)

- Dornbracht AG & Co. KG

- Elkay Manufacturing Company (Zurn Elkay Water Solutions)

- House of Rohl (Fortune Brands Home & Security Inc.)

- Julien Inc.

- Kohler Co.

- Oliveri Solutions Pty Ltd (Fletcher Building Limited)

- Roca Sanitario S.A.

- Ruvati USA

- Zuhne

Kitchen Sinks Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Installations Covered | Drop-In Or Top Mount, Undermount, Farmhouse or Apron-Front, Others |

| Number of Bowls Covered | Single, Double, Multiple |

| Materials Covered | Non-Metal, Metal |

| End Users Covered | Residential, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BLANCO GmbH + Co KG, Carysil Limited, Crown Sink, Delta Faucet Company (Masco Corporation), Dornbracht AG & Co. KG, Elkay Manufacturing Company (Zurn Elkay Water Solutions), House of Rohl (Fortune Brands Home & Security Inc.), Julien Inc., Kohler Co., Oliveri Solutions Pty Ltd (Fletcher Building Limited), Roca Sanitario S.A., Ruvati USA, Zuhne, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the kitchen sinks market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global kitchen sinks market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the kitchen sinks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Kitchen Sinks Market Report

The kitchen sinks market was valued at USD 3.71 Billion in 2025.

The kitchen sinks market is projected to exhibit a CAGR of 3.42% during 2026-2034, reaching a value of USD 5.20 Billion by 2034.

The kitchen sinks market is propelled by rising residential construction and home renovation activity globally, growing demand for premium and smart kitchen fixtures, rapid urbanization in emerging economies, and increasing adoption of modular kitchen designs. The expansion of the commercial foodservice and hospitality sectors, combined with regulatory mandates for hygienic kitchen equipment standards, further sustains robust demand.

Asia Pacific currently dominates the kitchen sinks market, accounting for a share of 48.6%. The region benefits from extensive residential and commercial construction activity, rapid urbanization across China, India, and Southeast Asia, rising middle-class household incomes, and strong government-supported housing programs that sustain high volumes of kitchen fixture installations across entry, mid, and premium market tiers.

Some of the major players in the kitchen sinks market include BLANCO GmbH + Co KG, Carysil Limited, Crown Sink, Delta Faucet Company (Masco Corporation), Dornbracht AG & Co. KG, Elkay Manufacturing Company (Zurn Elkay Water Solutions), House of Rohl (Fortune Brands Home & Security Inc.), Julien Inc., Kohler Co., Oliveri Solutions Pty Ltd (Fletcher Building Limited), Roca Sanitario S.A., Ruvati USA, Zuhne, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)