Language Services Market Size, Share, Trends and Forecast by Service, Component, Application, and Region, 2026-2034

Global Language Services Market Size, Share, Trends & Forecast (2026-2034)

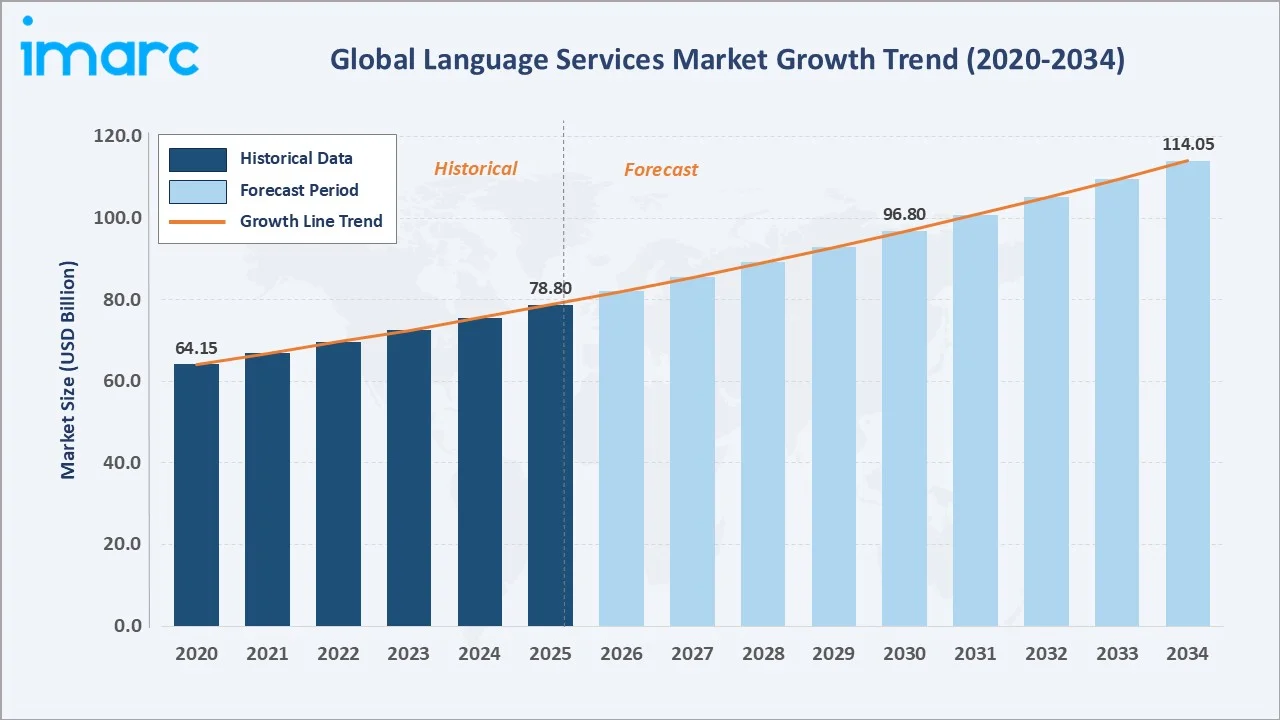

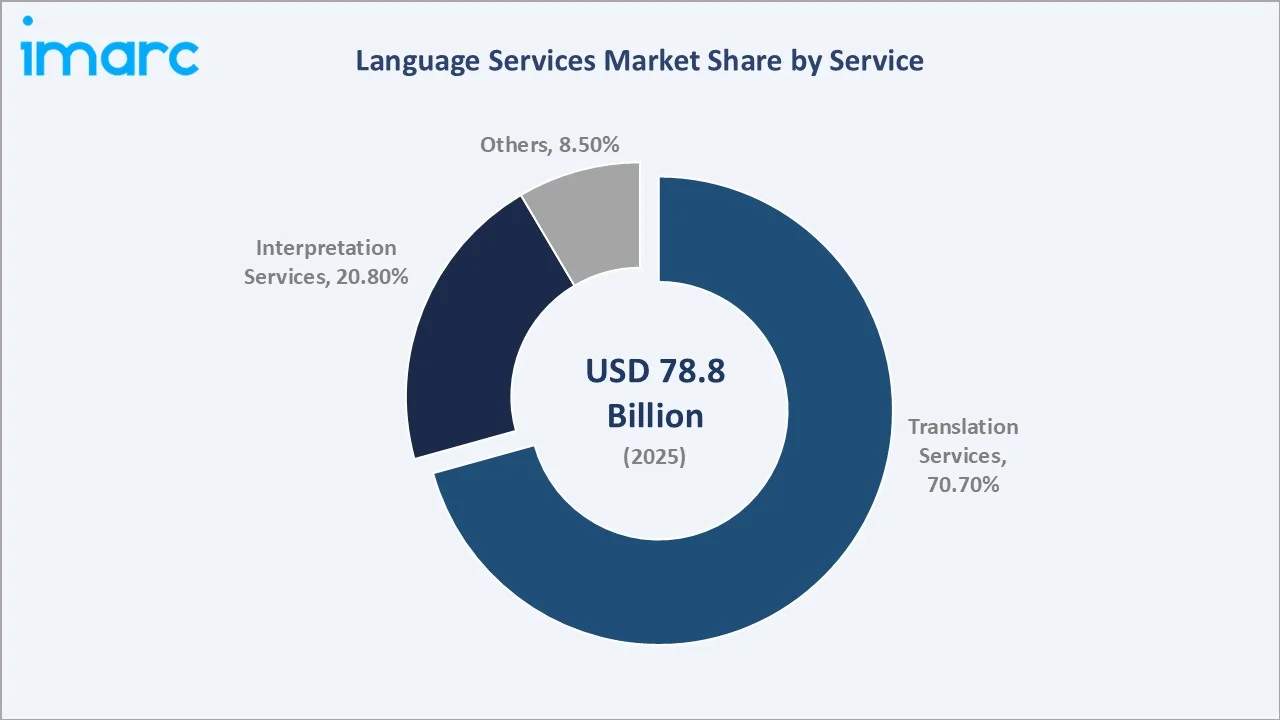

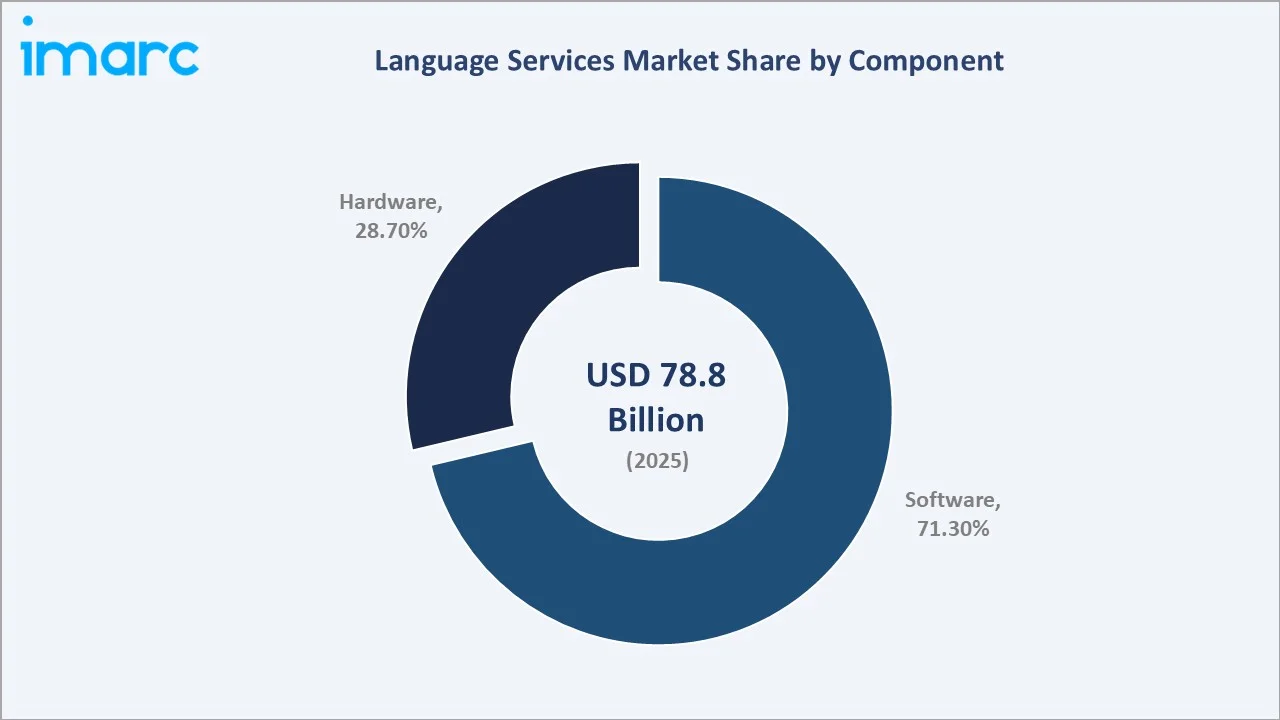

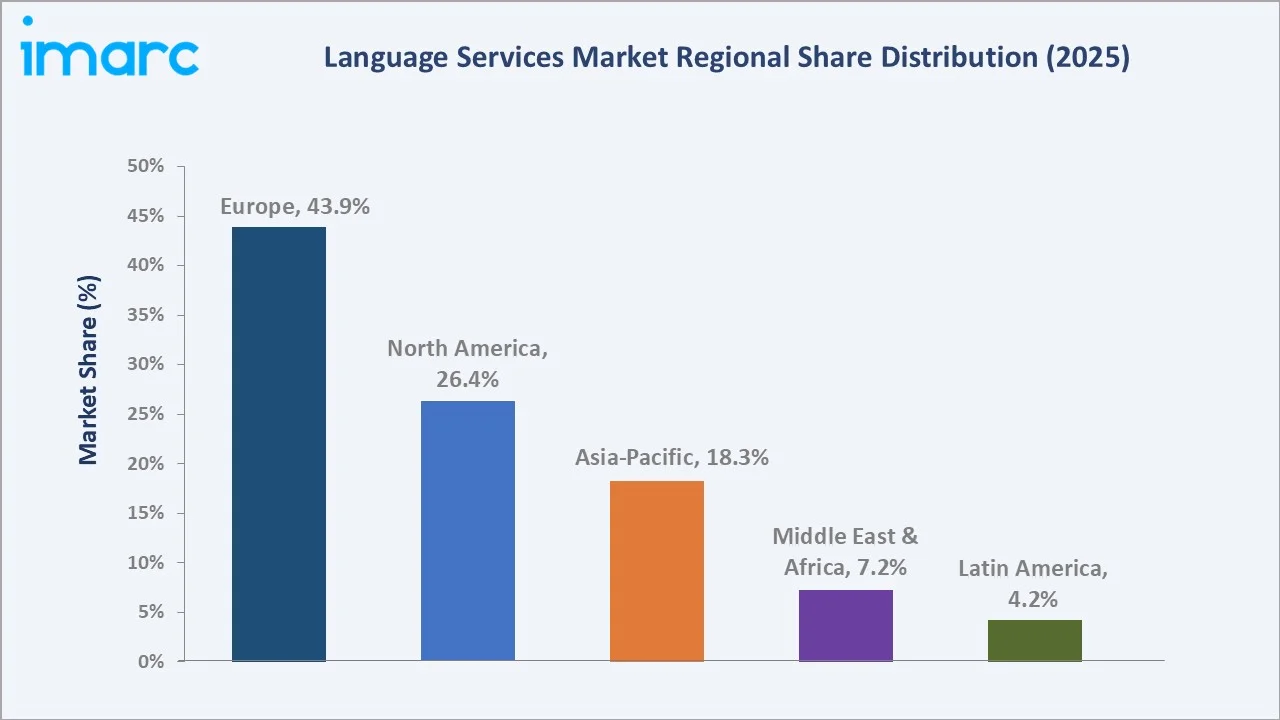

The global language services market size reached USD 78.8 Billion in 2025 and is projected to reach USD 114.1 Billion by 2034, exhibiting a CAGR of 4.20% during 2026-2034. Accelerating globalization, surging demand for multilingual content with more than 350 different languages spoken in the U.S. alone, and the increasing immigrant and international student population are the primary forces driving language services market growth. Translation services lead the service mix at 70.7% in 2025, while software components dominate the component split at 71.3%. Europe commands the largest regional share at 43.9% in 2025, underpinned by the EU's 24 official languages and stringent language access requirements across public institutions.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 78.8 Billion |

|

Forecast Market Size (2034) |

USD 114.1 Billion |

|

CAGR (2026-2034) |

4.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (43.9% share, 2025) |

|

Second Region |

North America (26.4% share, 2025) |

|

Leading Service |

Translation Services (70.7%, 2025) |

|

Leading Component |

Software (71.3%, 2025) |

The global language services market growth trajectory from 2020 through 2034, historical expansion from USD 64.1 Billion in 2020 to USD 78.8 Billion in 2025 reflects steady demand amplification, while the forecast trajectory toward USD 114.1 Billion captures the compounding effect of AI-augmented translation productivity, global enterprise content volume growth, and healthcare language access mandates.

To get more information on this market, Request Sample

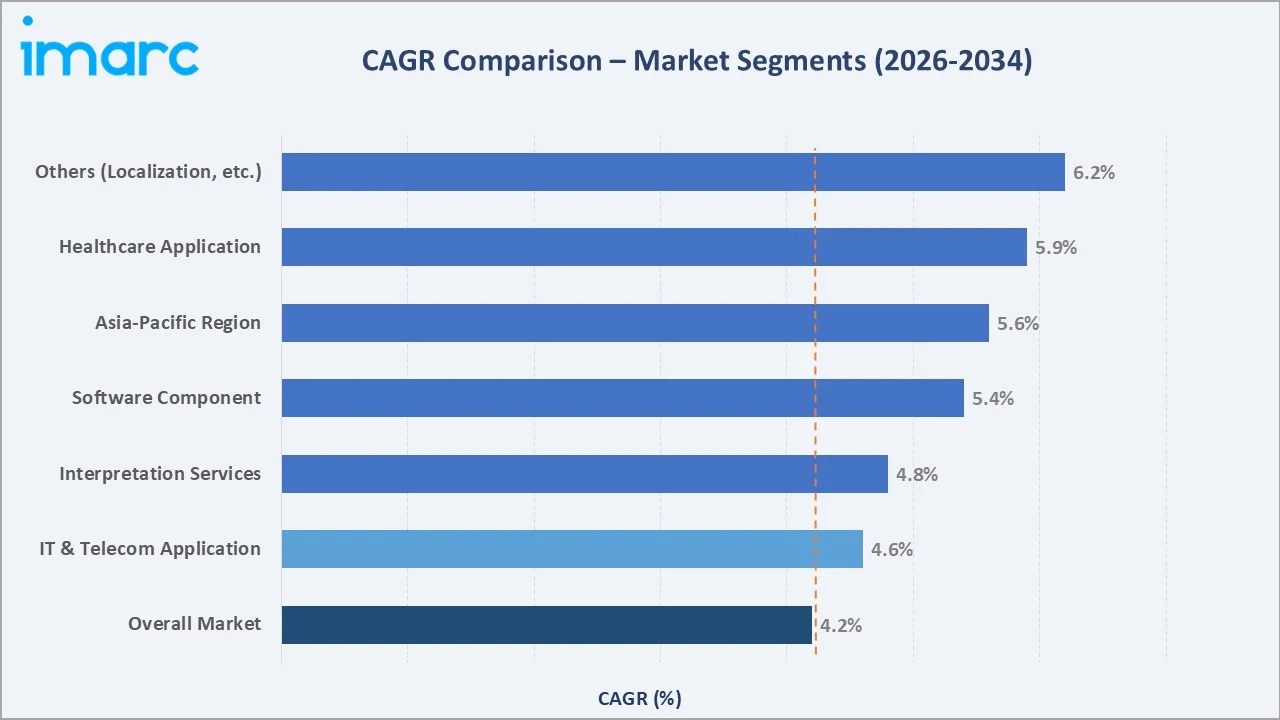

CAGR comparisons across key service, component, and regional sub-categories, healthcare application at ~5.9% CAGR and the software component at ~5.4% CAGR are the two fastest-growing sub-segments within the global language services industry analysis through 2034.

Executive Summary

The global language services market is experiencing steady, broad-based expansion from USD 78.8 Billion in 2025 to a projected USD 114.1 Billion by 2034. The EU alone operates in 24 official languages across its institutions, generating hundreds of millions of pages of translation annually.

Translation services dominate the service mix at 70.7% in 2025, anchored by document, legal, medical, technical, and website localization, the highest-volume content categories globally. Interpretation services at 20.8%, accelerated by the normalization of remote interpreting platforms (RSI/OPI) following the COVID-19 pandemic's elimination of on-site interpretation.

Software components lead at 71.3% in 2025, reflecting the industry's structural shift toward technology-mediated translation, translation management systems (TMS), computer-assisted translation (CAT) tools, machine translation post-editing (MTPE), and AI-powered quality assurance platforms now process the majority of translation volume. Europe leads at 43.9% in 2025, reflecting the EU's institutional language requirements. North America follows at 26.4%, driven by the more than 50.2 million immigrants lived in the United States in 2024.

Key Market Insights

|

Insight |

Data |

|

Largest Service |

Translation Services - 70.7% share (2025) |

|

Leading Component |

Software - 71.3% share (2025) |

|

Leading Region |

Europe - 43.9% revenue share (2025) |

|

Second Region |

North America - 26.4% revenue share (2025) |

|

Top Companies |

TransPerfect, Lionbridge, LanguageLine Solutions, RWS Holdings, Welocalize |

Key Analytical Observations Supporting the Above Data:

- Translation services, with 70.7% in 2025, dominate because written content translation, legal documents, medical records, software UIs, marketing materials, technical manuals, and websites represent the highest-volume output category across all language service segments.

- Software at 71.3% in 2025, reflects the industry's fundamental operational transformation. Translation management systems (TMS) from Phrase, Smartling, and Lionbridge's GlobalLink automate project routing, linguist assignment, and delivery workflows.

- Europe's 43.9% dominance in 2025 is structural. The EU institutions generate approximately 2.2 million pages of translated content annually across 24 official languages, representing the world's largest single institutional translation client.

Global Language Services Market Overview

The language services industry encompasses a broad spectrum of professional and technology-mediated services enabling communication across language barriers. Core service categories include translation, interpretation, localization, transcription, subtitling and captioning, desktop publishing, and language technology development.

With 67.3 million people in the U.S. speaking a non-English language at home, more than doubling over the past 30 years and over 25 million classified as Limited English Proficient (LEP), demand for translation, interpretation, and multilingual communication services is rapidly increasing, driving strong growth in the language services market.

Applications span corporate multilingual communications, regulatory compliance documentation, international legal proceedings, clinical trial documentation, e-commerce localization, multimedia subtitling, government public services, immigration and refugee support, and educational content.

Market Dynamics

To evaluate market opportunities, Request Sample

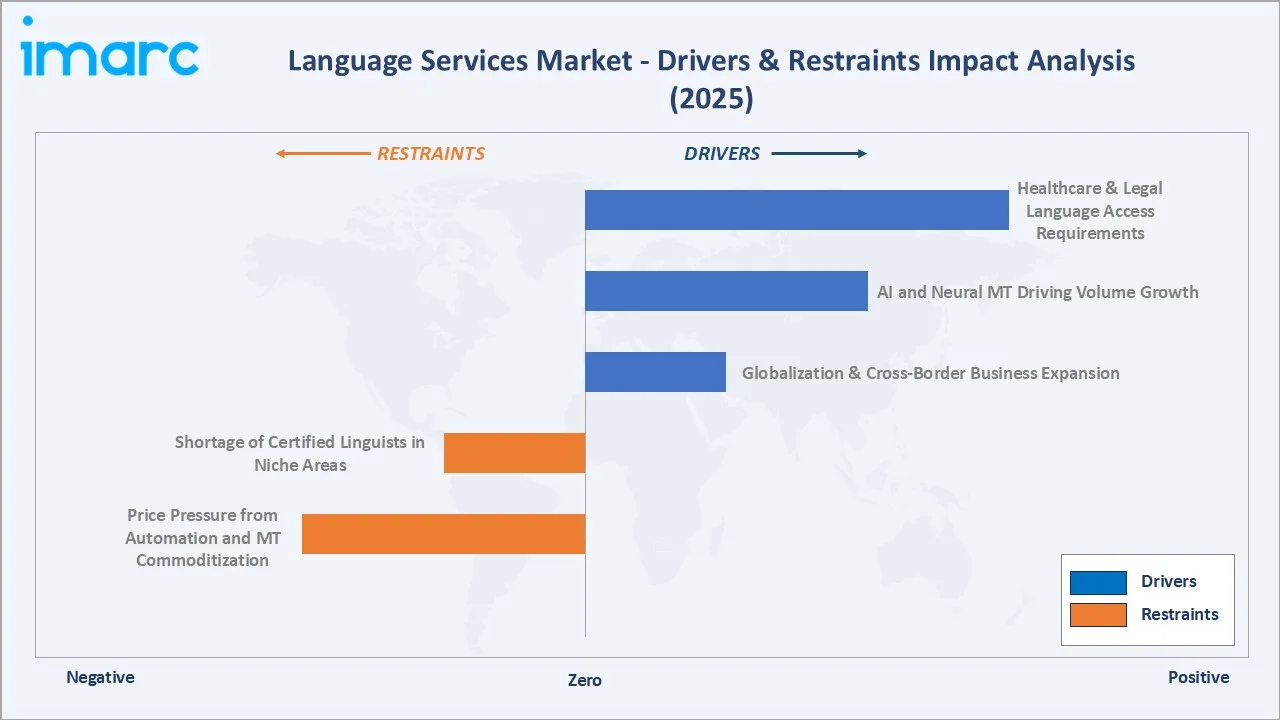

Market Drivers

- Globalization and Cross-Border Business Expansion: There are more than 40,000 multinational corporations (MNCs) with over 250,000 overseas affiliates, and the top 300 MNCs account for over 25% of the global economy, and each requires multilingual customer communication, regulatory compliance documentation, and product localization.

- AI and Neural Machine Translation Amplifying Service Volume: Neural machine translation (NMT) has not replaced human translators; it has dramatically amplified total translation volume by making previously uneconomical content types cost-effective to translate.

- Healthcare Language Access Legal Requirements: Under longstanding CMS policy, translation and interpretation services can be reimbursed at the standard 50% federal matching rate when classified as administrative expenses. This regulatory framework creates demand for healthcare language services market.

- Rising Immigration and International Student Populations: The immigrant population exceeded 50.2 million people in 2024, accounting for 14.8% of the US's 340.1 million residents, generating demand across legal, healthcare, social services, and educational language access.

Market Restraints

- Machine Translation Quality Limitations in Specialized Domains: Despite NMT's progress, machine translation quality in high-stakes specialized domains, legal, medical, patent, and financial, remains insufficient for unedited use in certified contexts. ISO 17100 certified translation requires human expertise for all certified translation workflows.

- Shortage of Qualified Linguists in Rare Language Pairs and Specialized Domains: Employment for interpreters and translators is expected to increase by 2% between 2024 and 2034, which is slower than the average growth rate across all occupations.

Market Opportunities

- Multimedia Localization and Streaming Content: The global OTT streaming market is growing, with Netflix, Disney+, Amazon Prime Video, and YouTube generating massive multilingual subtitling, dubbing, and captioning demand. Netflix localizes original content into 62 languages and has invested in proprietary dubbing quality standards.

- AI-Augmented Language Services for SMEs: Small and medium-sized enterprises historically under-invested in professional language services due to cost. SaaS-based localization platforms, including Phrase, Lokalise, and Smartling, combining MT, human review, and CMS integration are bringing enterprise-quality multilingual content capabilities to SMEs at accessible price points.

Market Challenges

- Generative AI Disruption Risk to Traditional LSP Business Models: ChatGPT's release in late 2022 triggered widespread industry debate about AI's impact on professional translation.

- Quality Consistency Across Distributed Freelance Networks: The language services industry relies heavily on freelance translators and interpreters globally. Maintaining quality consistency across diverse linguist pools with varying technical terminology expertise, subject matter knowledge, and localization style adherence is a persistent operational challenge.

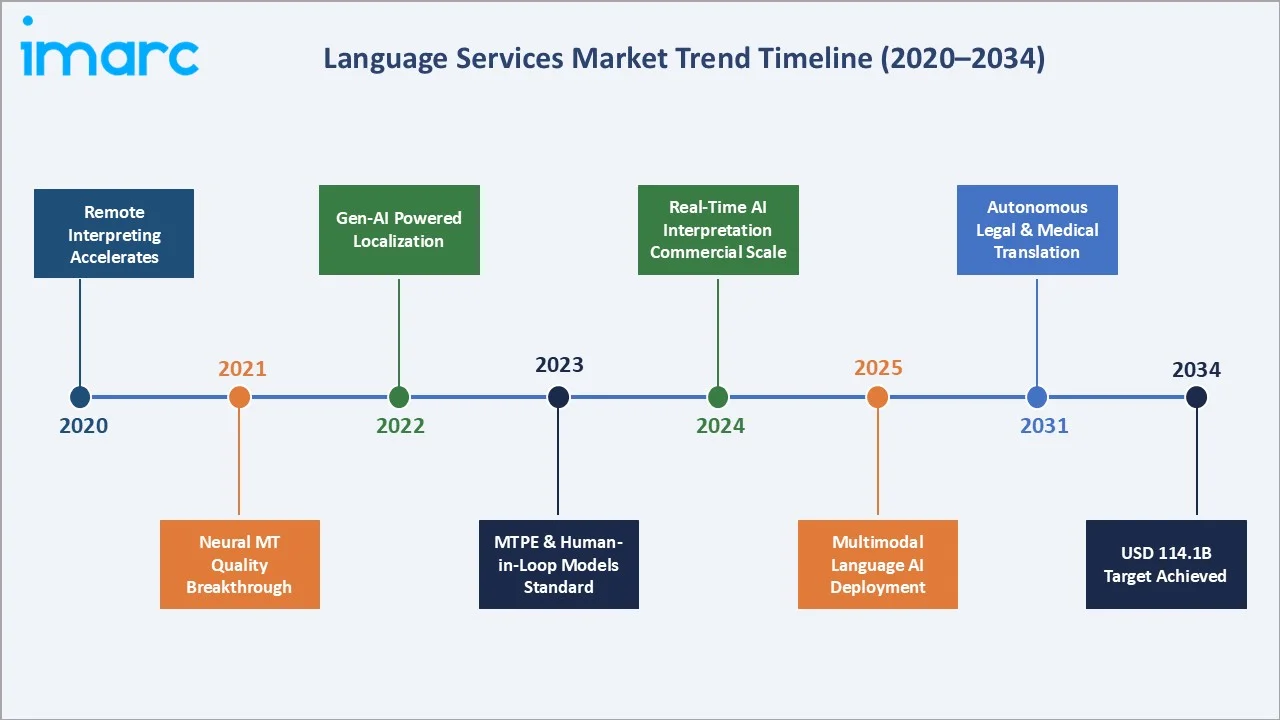

Emerging Market Trends

1. Generative AI and Large Language Models Transforming Translation Workflows

GPT-4-class large language models are being integrated into translation workflows by major LSPs, including Lionbridge (AI Translation Tier), transforming MTPE into AI-augmented translation where GenAI handles initial drafts that human linguists refine.

2. Remote Simultaneous Interpreting Becoming the Conference Standard

Remote simultaneous interpreting (RSI) platforms normalized during the COVID-19 pandemic are now the default format for multilingual conferences, international legal proceedings, and corporate events. The RSI market is growing, displacing portable booths and on-site interpreting logistics costs.

3. Real-Time AI Interpretation for Consumer and Healthcare Applications

Near-real-time AI interpretation, not yet certified for critical professional settings but commercially deployed in consumer contexts, is expanding language access dramatically. Google Translate Live in Google Meet, Microsoft Translator for Teams, and specialized medical AI interpreters from companies are enabling multilingual meetings without professional interpreters.

4. Multimedia and Audiovisual Localization Scaling with Streaming Growth

The explosion of video content from Netflix's 62-language localization requirement to YouTube's automatic caption translation to TikTok's multilingual content strategy is driving structural growth in audiovisual translation, subtitling, dubbing, and media localization.

5. Specialized AI Models for High-Stakes Domain Translation

Rather than general-purpose GenAI, specialized domain-trained NMT models are emerging as the quality solution for medical, legal, and technical translation. These specialized models command 2-3x premium pricing over generic MT outputs, preserving margin for LSPs with domain expertise.

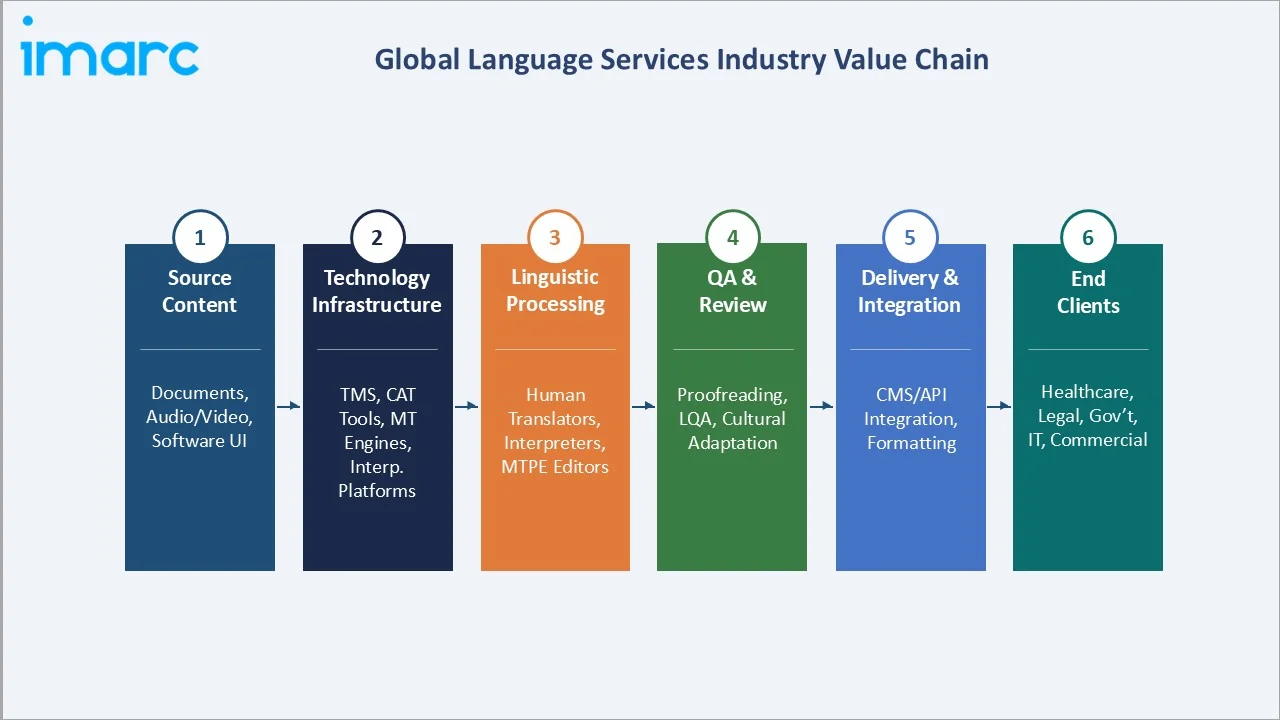

Industry Value Chain Analysis

The language services value chain spans six stages from source content preparation through end-client delivery. Technology infrastructure and linguistic processing represent the core value-add stages, while quality assurance and system integration are the premium differentiators commanding highest margins.

|

Stage |

Key Players / Examples |

|

Source Content |

Enterprise documents, legal filings, medical records, software strings, audio/video - all originating client content |

|

Technology Infrastructure |

TMS: Phrase, Smartling, GlobalLink (TransPerfect). CAT Tools: SDL Trados, memoQ. MT: DeepL, Google NMT, Microsoft Azure |

|

Linguistic Processing |

Freelance networks (ProZ, Translators Café), in-house linguists, MTPE editors, certified court interpreters, RSI professionals |

|

QA & Review |

SDL Language Weaver QE, Xbench, LanguageTool, ISO 17100 review workflows, LQA linguistic quality assessment |

|

Delivery & Integration |

CMS plugins (Drupal, WordPress), API integrations (Salesforce, Adobe), LocalizationEngine, Contentful multilingual |

|

End Clients |

Healthcare (Mayo Clinic, NHS), Legal (law firms, courts), IT (SAP, Microsoft), Government (EU, UN, federal agencies) |

Technology infrastructure vendors and specialized LSPs with domain-trained MT capture the highest margins in the language services value chain. TransPerfect's GlobalLink TMS platform generates significant recurring SaaS revenue independent of per-word transaction volume, a structural competitive advantage as translation per-word margins compress.

Technology Landscape in the Language Services Industry

Neural Machine Translation and Large Language Models

Neural machine translation has undergone a step-change transformation, culminating in the current generation of large language model-based translation. As of 2020, Google Translate supported over 100 languages and served more than 500 million users, translating over 100 billion words daily. It offers translation capabilities across 37 languages via images, 32 via voice (conversation mode), and 27 through real-time augmented reality video. This massive scale of multilingual usage highlights growing global communication needs, driving demand for advanced translation, localization, and AI-powered language services.

Translation Management Systems and CAT Tool Ecosystems

Translation management systems (TMS) are the operational backbone of enterprise language services workflows. Translation memory (TM) technology, storing previously translated segments for reuse, reduces redundant translation effort on repetitive content types including software UI strings, legal boilerplate, and technical manuals.

Remote Interpreting Platform Technology

Video remote interpreting (VRI) and over-the-phone interpreting (OPI) platforms have transformed the interpretation services delivery model. LanguageLine Solutions, the world's largest telephone interpreting service, processes over 76 million interpretation calls through its proprietary platform serving healthcare, legal, and government clients.

AI Quality Assurance and Linguistic Quality Management

Automated quality estimation (QE) technology, predicting translation quality without reference to the source text, using ML models trained on human quality assessments, is transforming how LSPs manage quality at scale. This automation enables quality management across millions of words per day, impossible with purely human review, while prioritizing linguist review effort toward the highest-risk segments and significantly reducing post-delivery revision rates.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Translation Services |

70.7% |

2025 |

|

Component |

Software |

71.3% |

2025 |

|

Application |

IT and Telecommunications |

24.0% |

2025 |

|

Region |

Europe |

43.9% |

2025 |

By Service

Translation services command the largest share at 70.7% in 2025, reflecting the enormous global volume of written content requiring language conversion across legal, medical, commercial, technical, and digital categories. The ISO 17100:2015 standard defines the professional requirements for translation service provision and has become the de facto quality benchmark for enterprise procurement.

To access detailed market analysis, Request Sample

Interpretation services at 20.8% in 2025, accelerated by remote interpreting platform adoption and healthcare language access mandates. LanguageLine Solutions alone processes over 76 million interpretation calls. The Others category (8.5%) encompasses localization, transcription, subtitling, desktop publishing, and language technology - each growing sub-segment at above-average rates driven by digital content proliferation and streaming media demand.

By Component

Software commands a 71.3% component share in 2025, the market's dominant technology category, the fastest-growing component. SaaS-based TMS and MT engine licensing generate recurring revenue less sensitive to per-word translation volume fluctuations than traditional project-based services billing.

Hardware at 28.7% in 2025 encompasses interpretation equipment (consoles, wireless receivers, booths), RSI hardware, assistive hearing devices, and voice recognition hardware. Professional interpretation equipment from Televic, Bosch, and Brahler remains essential for large-scale multilingual conferences, international organizations, and legal proceedings, particularly at the EU Parliament, UN system, and national court infrastructure globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

43.9% |

EU 24-language institutional demand; ISO-certified LSPs; multilingual healthcare and legal compliance |

|

North America |

26.4% |

US immigration (49M immigrants); federal language access mandates; tech sector content localization |

|

Asia-Pacific |

18.3% |

China/Japan enterprise localization; India BPO multilingual services; SEA e-commerce content growth |

|

Middle East & Africa |

7.2% |

Arabic language digital content; UAE multilingual business hub; Africa's 2,000+ language diversity |

|

Latin America |

4.2% |

Brazil Portuguese content; Spanish localization; LATAM e-commerce multilingual expansion |

Europe's 43.9% dominance in 2025 is a reflection of structural institutional language demand unmatched in any other global region. The EU's 24 official languages generate an estimated 2.2 million pages of translated content annually through the EU Directorate-General for Translation alone, the world's largest translation service. The European Union of Associations of Translation Companies is a collective body of national European associations, representing nearly 700 language service providers across the region.

North America (26.4%, 2025) is driven primarily by the US market. In 2024, about 77% (247.9 million) of the 321.7 million U.S. residents aged 5 and older reported speaking only English at home. Among the 73 million people who spoke another language, 61% reported speaking Spanish. The US is also the world's largest single-country technology sector, with Silicon Valley multinationals generating massive software localization and multilingual content demands.

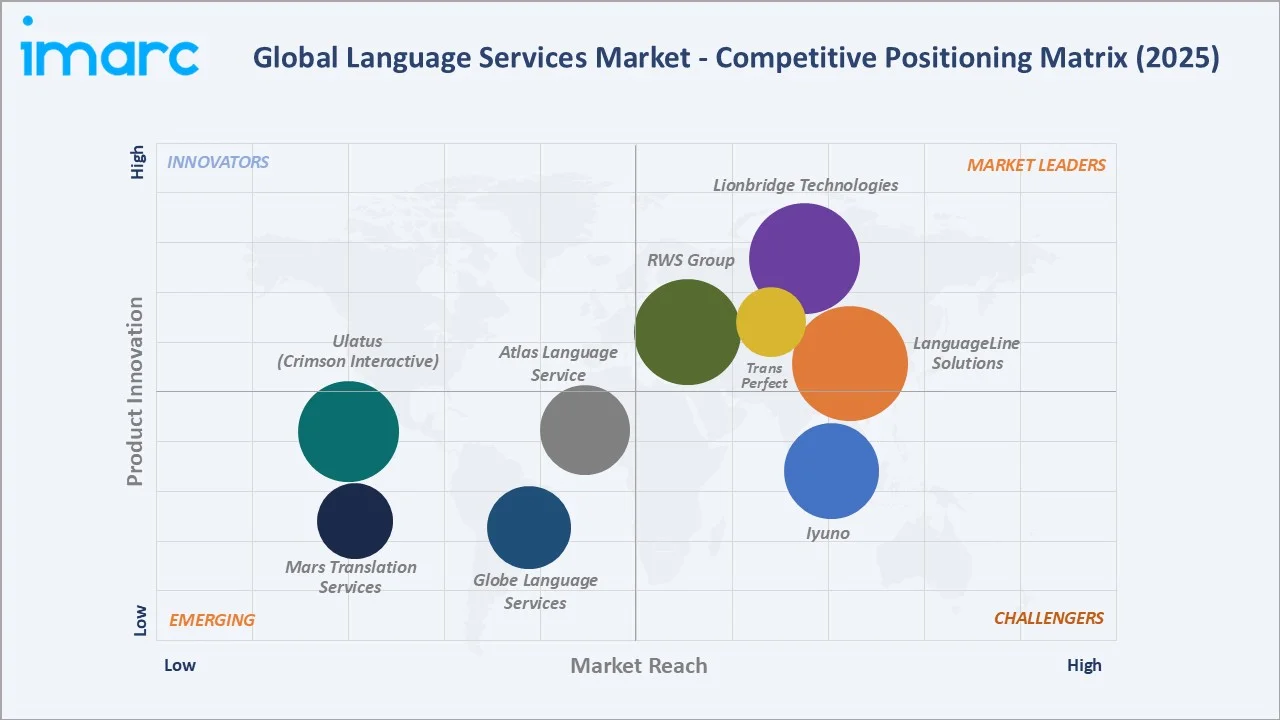

Competitive Landscape

The global language services market is moderately fragmented, with the top 5 LSPs collectively accounting for approximately 12-18% of global revenue. The remaining 82-88% is distributed across thousands of regional LSPs, boutique specialized agencies, and independent freelance professionals, reflecting the industry's structural diversity.

|

Company Name |

Key Brand/Platform |

Market Position |

Strategic Focus |

|

Atlas Language Service Inc. |

Atlas Language Services |

Emerging |

US legal and government interpretation; USCIS certified |

|

Globe Language Services Inc. |

Globe Language |

Emerging |

Healthcare and community interpretation; US regional |

|

Iyuno |

Iyuno Media Localization |

Challenger |

Media localization; Netflix/Amazon partner; 100+ languages |

|

LanguageLine Solutions (Teleperformance SE) |

LanguageLine Platform |

Leader |

OPI/VRI market leader; 35M+ sessions annually; healthcare |

|

Lionbridge Technologies LLC |

Lionbridge AI Translation |

Leader |

AI translation tier; game testing; global content solutions |

|

Mars Translation Services |

Mars Translation |

Emerging |

Chinese-English specialist; technical and legal translation |

|

RWS Group |

Trados |

Leader |

CAT tools + LSP; life sciences & IP translation specialist |

|

TransPerfect |

GlobalLink TMS Platform |

Leader |

Full-service LSP + TMS SaaS; legal, life sciences, finance |

|

Ulatus (Crimson Interactive Inc.) |

Ulatus Translation |

Emerging |

Academic and research translation; India-based; Asia focus |

The competitive positioning of key language services market participants across global market presence and strategic investment dimensions in 2025.

Key Company Profiles

TransPerfect Global Inc.

TransPerfect is the world's largest privately-held language services and technology solutions company. Founded in 1992 and headquartered in New York, TransPerfect serves clients across legal, life sciences, financial services, e-commerce, and technology sectors.

- Product Portfolio: GlobalLink TMS, TRANSPERFECT LEGAL, TransPerfect Life Sciences.

- Recent Developments: In June 2025, TransPerfect launched its TransPerfect Interpretation App, which allows users to instantly connect with professionally trained interpreters via video or phone.

- Strategic Focus: TransPerfect's strategy centers on expanding GlobalLink as a SaaS-revenue TMS platform independent of project-based translation billing, deepening AI integration to scale output per linguist, and building a comprehensive legal technology language services practice.

Lionbridge Technologies Inc.

Lionbridge is one of the world's largest language services companies, headquartered in Waltham, Massachusetts, owned by H.I.G. Capital since 2017.

- Product Portfolio: Lionbridge AI Translation, Lionbridge Smart Onboarding.

- Recent Developments: In December 2024, Lionbridge named the winner of the “Best Machine Translation Solution” at the seventh annual AI Breakthrough Awards. The recognition highlights its enterprise-level solution, Lionbridge Smart MT, along with its advanced post-editing technology powered by large language models to enhance translation quality and final output.

- Strategic Focus: Lionbridge's strategy focuses on three growth vectors: AI-augmented translation that increases linguist productivity and reduces per-word costs while maintaining quality, AI training data annotation as a high-growth revenue stream capitalizing on LLM development investment, and games and media localization as an entertainment industry growth market where Lionbridge's scale provides competitive advantage.

LanguageLine Solutions

LanguageLine Solutions is the world's largest telephone and video interpreting service, headquartered in Monterey, California. The company serves clients in healthcare, legal, financial services, government, and insurance.

- Product Portfolio: LanguageLine OPI, LanguageLine VRI, LanguageLine OnSite, LanguageLine Connect, and LanguageLine AI.

- Recent Developments: In June 2024, LanguageLine Solutions unveiled LanguageLine Analytics, a new tool integrated into the MyLanguageLine client portal. This tool enables organizations to make data-driven decisions and enhance their language access programs in an increasingly diverse environment.

- Strategic Focus: LanguageLine's strategy centers on maintaining dominance in healthcare interpreting, where Title VI, ADA, and ACA language access mandates create structural institutional demand - while expanding AI-assisted interpreting to cost-effectively serve routine language access needs, and growing its legal and government interpretation practices through federal agency contract expansion.

Iyuno

Iyuno is the world's largest dedicated media localization company, headquartered in Seoul, South Korea, with linguists and localization specialists serving the global streaming entertainment industry.

- Product Portfolio: Subtitling, dubbing, speech recognition.

- Recent Developments: In September 2025, Iyuno presented Sub.X at IBC 2025, a new AI-driven subtitling solution that combines automation with human expertise to produce studio-quality subtitles in near real-time. Unlike conventional AI translation tools, Sub.X utilizes Iyuno’s localization expertise to replicate a professional subtitling workflow, offering innovative features like context through multimodal prompting, precise speaker mapping, management of formality and style, and multiple levels of human review.

- Strategic Focus: Iyuno's strategy leverages its position as the world's largest AV localization network to capture the streaming media content globalization opportunity, deepening partnerships with major OTT platforms while expanding geographic studio capacity to serve underserved language markets in Africa, South Asia, and the Middle East.

Market Concentration Analysis

The global language services market is highly fragmented, with the top 5 players collectively accounting for approximately 12-18% of total market revenue. The remaining 82-88% is distributed across an estimated 25,000-30,000 active language service providers globally, ranging from mid-market regional LSPs to single-person freelance operators.

The language services market's extreme fragmentation reflects the market's 300+ active language combinations, 20+ specialized domain categories, and vast range of content types that create natural niches where boutique specialized agencies outcompete large LSPs on quality and turnaround. ISO 17100 quality certification creates a floor of standardization but not concentration.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare language services at ~5.7% CAGR through 2034 represent the highest-growth end-market. Investment in healthcare-specialized TMS with HIPAA compliance, EHR system integrations, and certified medical interpreter networks generates the highest sustainable revenue quality in the language services industry. The media localization category represents the highest absolute volume growth opportunity, with streaming platforms' content globalization investment sustaining double-digit AV localization market growth.

Emerging Markets

Africa represents the highest-upside emerging market opportunity in language services through 2034. Africa is home to approximately one-third of the world's languages, with anywhere between 1000 and 2000 languages. Early investment in African language technology, particularly NLP training data for low-resource African languages, positions language companies for first-mover advantage in a region where demand will grow faster than supply through the 2030s.

Venture & Investment Trends

Private equity interest in mid-tier LSPs, exemplified by H.I.G. Capital's Lionbridge ownership and CBPE Capital's investment in thebigword, reflects the language services industry's stable, recurring revenue characteristics and consolidation potential.

Future Market Outlook (2026-2034)

The global language services market is forecast to expand from USD 78.8 Billion in 2025 to USD 114.1 Billion by 2034 at a CAGR of 4.20%, adding USD 35.3 Billion in incremental market value. This consistent growth trajectory reflects the interplay of accelerating global content volume, expanding institutional language access mandates, and AI productivity tools amplifying total output capacity.

Three technology discontinuities will most significantly reshape the language services landscape through 2034. Multimodal AI translation, capable of translating not just text but image text, audio speech, and video captions simultaneously from a single model inference, will transform multimedia localization economics, collapsing production timescales and costs for AV content localization.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with language service industry stakeholders including LSP executives, enterprise language services buyers (healthcare systems, law firms, multinational technology companies), professional associations, TMS platform product managers, and equity analysts covering the language services and edtech sectors. Primary data validated market sizing, segmentation splits, regional demand characteristics, and technology adoption timelines.

Secondary Research

Key secondary sources include CSA Research Annual Language Services Market Report (2023-2024), Common Sense Advisory 'Can't Read, Won't Buy' studies, US BLS Occupational Outlook Handbook (translators and interpreters, 2022-2032), EU Directorate-General for Translation annual reports, UN Language Services department statistics, US Census Bureau American Community Survey (language at home data), ATA (American Translators Association) industry surveys, and trade publications including Multilingual Magazine, Slator, and The Linguist.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Language Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Translation Services, Interpretation Services, Others |

| Components Covered | Software, Hardware |

| Applications Covered | IT and Telecommunications, Commercial, Government, Automotive, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Sweden, Russia, Netherlands, China, Japan, India, South Korea, Australia, Turkey, Saudi Arabia, Iran, Brazil, Mexico |

| Companies Covered | Atlas Language Service Inc., Globe Language Services Inc., Iyuno, LanguageLine Solutions (Teleperformance SE), Lionbridge Technologies LLC, Mars Translation Services, RWS Group, TransPerfect, Ulatus (Crimson Interactive Inc.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the language services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global language services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the language services industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Language Services Market Report

The global language services market reached USD 78.8 Billion in 2025, driven by globalization, enterprise content growth, and institutional language access requirements globally.

The market is projected to reach USD 114.1 Billion by 2034, growing at a CAGR of 4.20% during 2026-2034, driven by AI-augmented translation productivity, healthcare mandates, and emerging market penetration.

Translation services lead with a 70.7% share in 2025, encompassing document, legal, medical, technical, website, and software localization across all industry verticals and geographic markets globally.

Software leads with a 71.3% share in 2025, the highest in the industry's history, reflecting the structural shift toward SaaS TMS platforms, AI translation engines, and CAT tool ecosystems that now mediate the majority of professional translation volume.

Europe leads with 43.9% market share in 2025, driven by the EU's 2.2 million translated pages annually across 24 official languages, national healthcare language access laws, and the continent's dense multilingual corporate base.

Primary drivers include globalization, AI-augmented translation expanding volume capacity, US Title VI healthcare language access mandates, and US immigrants generating sustained demand.

Key companies include Atlas Language Service, Inc., Globe Language Services Inc., Iyuno, LanguageLine Solutions (Teleperformance SE), Lionbridge Technologies, LLC, Mars Translation Services, RWS Group, TransPerfect, and Ulatus (Crimson Interactive Inc.).

Translation converts written text between languages (70.7% of market share in 2025); interpretation provides real-time oral communication across languages (20.8%). Both require certified professionals for healthcare, legal, and government applications.

GenAI workflows increased linguist productivity 40-65% per TransPerfect's 2024 data. MT engines process billions of words daily. AI training data annotation - creating multilingual NLP datasets - is growing at 20%+ annually as a new adjacent revenue stream.

Healthcare is the fastest-growing application at ~5.7% CAGR through 2034, driven by US Title VI mandates requiring federally-funded healthcare providers to offer qualified medical interpretation and translation to LEP patients at no cost.

Asia-Pacific (18.3%, 2025) is the fastest-growing region at ~5.4% CAGR, driven by Chinese enterprise localization, India's BPO multilingual services, Japan's technology documentation requirements, and Southeast Asian e-commerce demanding content in Thai, Indonesian, Vietnamese, Tagalog, and Malay.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade