Laser Cladding Equipment Market Report by Power (High Power, Low Power), Application (Power Generation, Industrial, Mining, and Others), and Region 2026-2034

Market Overview:

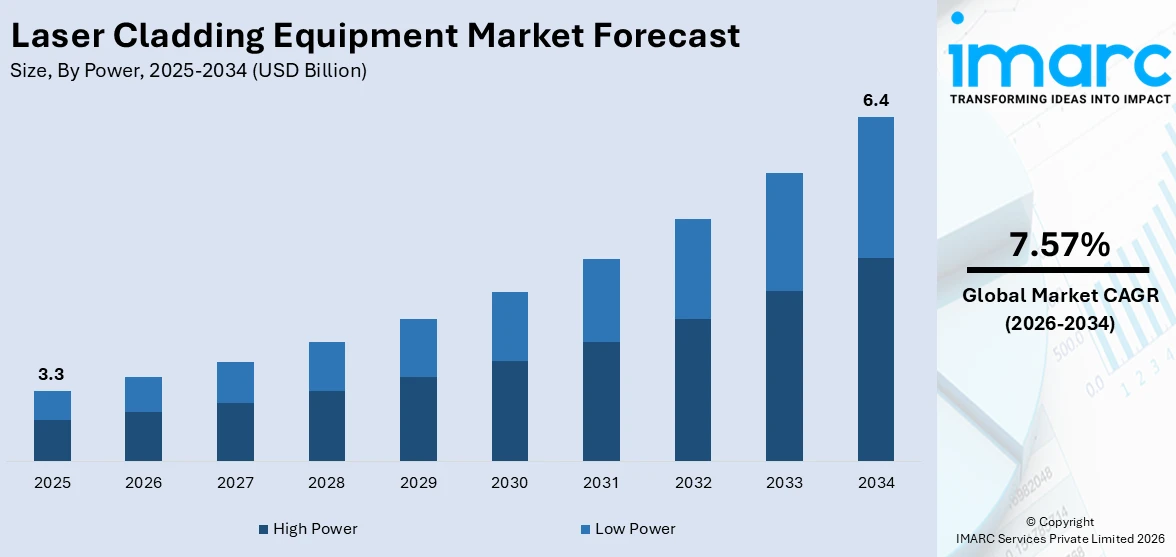

The global laser cladding equipment market size reached USD 3.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 6.4 Billion by 2034, exhibiting a growth rate (CAGR) of 7.57% during 2026-2034. The increasing need for improved wear and corrosion resistance in industrial machinery, the rising demand for resource optimization for extending the lifespan of costly industrial components, and rapid expansion of manufacturing sectors across emerging economies represent some of the factors that are propelling the market.

|

Report Attribute

|

Key Statistics |

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.3 Billion |

| Market Forecast in 2034 | USD 6.4 Billion |

| Market Growth Rate (2026-2034) | 7.57% |

Laser cladding equipment is an advanced technology that involves the use of lasers to deposit materials onto surfaces, typically to increase corrosion resistance, wear resistance, or dimensional restoration. This technique employs a focused laser beam to fuse powdered materials such as metal, ceramics, or polymers onto the host surface. The working mechanism involves directing a high-powered laser at the targeted surface while injecting a powdered cladding material into the beam's focal point, resulting in a localized melt pool that bonds the additive material to the surface. The characteristics of laser cladding include precise control, minimal distortion, and strong bonding between the cladding material and the substrate. This process also offers advantages such as the ability to create complex geometries, improved material properties, and the utilization of a broad range of cladding materials.

To get more information on this market Request Sample

The global market for laser cladding equipment is primarily driven by the increasing need for improved wear and corrosion resistance in industrial machinery. In line with this, the rising demand for resource optimization for extending the lifespan of costly industrial components is providing an impetus to the market. Moreover, the rapid expansion of manufacturing sectors across emerging economies and the need for precision in aerospace and automotive components are acting as significant growth-inducing factors for the market. In addition to this, the drive for technological innovation in materials science, leading to the development of advanced cladding materials, is resulting in higher investment in this technology. Apart from this, the rise in research and development activities to innovate and optimize laser cladding processes, and the integration of automation and Industry 4.0 principles into cladding operations, are propelling the market.

Laser Cladding Equipment Market Trends/Drivers:

An enhanced focus on enhancing manufacturing efficiency

In an era where the manufacturing landscape is constantly evolving, efficiency and precision stand at the core of success. Laser cladding technology emerges as a frontrunner in this regard. By offering precise control over the application of materials and facilitating faster production cycles, laser cladding significantly enhances manufacturing efficiency. The high precision ensures that the cladding process meets stringent quality standards, which is a critical requirement in industries such as aerospace and automotive. Furthermore, it allows manufacturers to maintain consistency across large production volumes, thereby assuring uniform quality. In addition, it contributes to a reduction in material waste, which is not only an economic advantage but also aligns with sustainable practices. This relentless focus on enhancing manufacturing efficiency while retaining or even improving quality standards is a vital factor in the proliferation of the laser cladding equipment market.

Global Emphasis on Sustainability

The growing global emphasis on sustainability is a guiding force that shapes various industrial practices, including laser cladding. With a world increasingly conscious of its ecological footprint, laser cladding's role in enabling the reuse and restoration of parts is being recognized. By allowing existing parts to be refurbished, it significantly reduces waste and conserves resources. The long-term implications are not just cost-saving but also a reduction in the environmental impact of manufacturing processes. The technology’s alignment with global sustainability goals makes it an attractive option for industries looking to enhance their green credentials. Additionally, as regulatory bodies around the world continue to tighten environmental compliance requirements, laser cladding emerges as a technology that aligns well with the evolving legal landscape. This commitment to sustainability and the alignment with broader global ecological goals contribute fundamentally to the market's growth.

Rising integration with industry 4.0 principles

Industry 4.0 represents the current trend of automation, data exchange, and the use of smart technology in manufacturing environments. Laser cladding, with its precision and adaptability, fits seamlessly into this paradigm. The ability of laser cladding equipment to communicate and function within a networked manufacturing environment provides substantial benefits. For instance, real-time monitoring and feedback can optimize the cladding process, reducing errors, and enhancing quality. Furthermore, the ability to automate the cladding process facilitates a more responsive manufacturing workflow. The customization that laser cladding equipment allows can be intelligently directed by integrating data analytics and machine learning algorithms, leading to innovative applications and higher efficiency. This synergy with Industry 4.0 principles makes laser cladding an essential component in modern, technologically advanced manufacturing processes. By aligning itself with the future of manufacturing, laser cladding ensures its relevance and importance, thereby fundamentally driving the market growth.

Laser Cladding Equipment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global laser cladding equipment market report, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on power and application.

Breakup by Power:

- High Power

- Low Power

The report has provided a detailed breakup and analysis of the market based on the power. This includes high power and low power.

The high power segment is propelled by the need for extensive surface treatment in industries such as aerospace, automotive, and energy. Handling large-scale components, enhancing surface properties, and delivering precision are significant factors. Continuous advancements in technology offering higher power outputs and efficiency are influential. The desire for rapid production and adherence to strict quality control standards further support this segment.

On the other hand, in the low power domain, applications requiring fine detailing and control such as electronics and medical devices drive demand. Increasing needs for cost-effective solutions offering quality results are significant. Miniaturization trends and the necessity for specific material properties influence this sector. A focus on energy consumption reduction and operational efficiency enhancement contributes to growth.

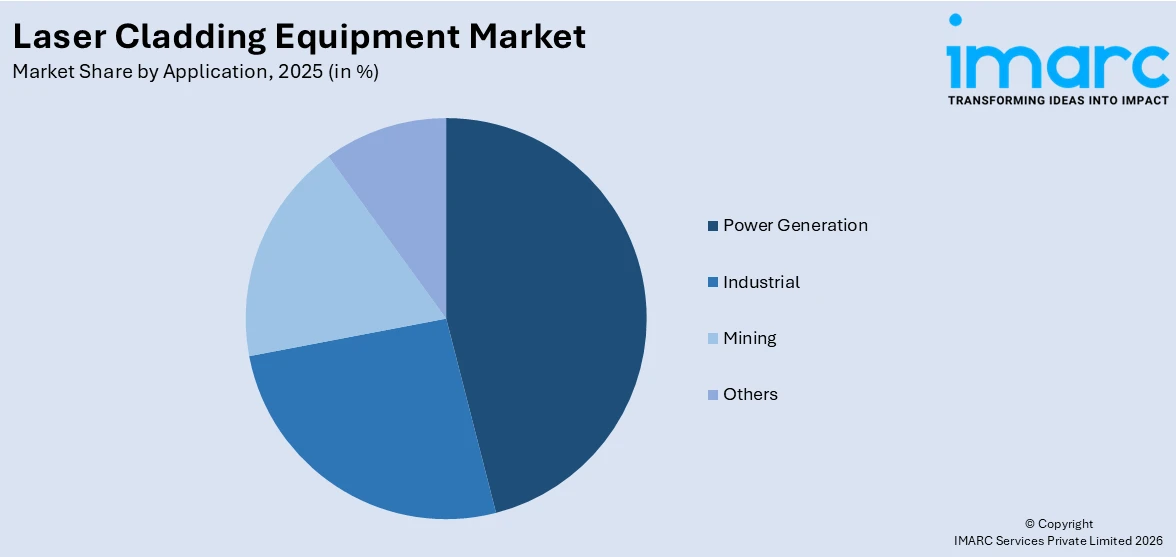

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Power Generation

- Industrial

- Mining

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes power generation, industrial, mining, and others.

The power generation segment is being influenced by the escalating need for wear and corrosion resistance in turbines and critical components. A focus on extending equipment lifespan and reducing maintenance costs significantly contributes to this growth. Enhanced efficiency coupled with the capability to restore and refurbish worn parts without major downtime further drives demand. The adherence to stringent environmental standards demanding reduced emissions also fuels the adoption of these advanced techniques in the sector.

On the other hand, in the industrial sphere, demand is motivated by the necessity for precision engineering and high-quality surface finishes. The growing need for customization in various applications and the emphasis on material property improvement are vital factors. Additionally, the shift towards automation and integration of Industry 4.0 principles supports the growth. Resource optimization and sustainable industrial processes further impact this segment positively.

Furthermore, for the mining sector, demand stems from the requirement for robust and wear-resistant tools that can endure harsh conditions. Extending the operational life of mining tools, reducing replacement costs, and utilizing advanced materials capable of handling specific applications are key drivers. The move towards environmentally responsible mining practices and relevant regulations also encourages the use of this technology.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Europe exhibits a clear dominance, accounting for the largest laser cladding equipment market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Afri)According to the report, Europe accounted for the largest market share.

The market in the Europe region is experiencing expansion due to a strong manufacturing sector, technological innovations, and sophisticated infrastructure. Key industry players and a robust focus on R&D shape the market dynamics.

In addition to this, investments in sectors like aerospace and automotive and a trend towards automation and digital integration in manufacturing are vital factors driving the market. Innovation, the need for tailored solutions, and extensive collaboration between academia and industry contribute to the region's dynamics.

Government support for advanced manufacturing, a skilled workforce, and an emphasis on quality and precision round out the driving factors. Compliance with environmental and safety standards and a regional focus on sustainability, resource optimization, and waste reduction further fuel growth.

Key Regional Takeaways:

United States Laser Cladding Equipment Market Analysis

The United States laser cladding equipment market is experiencing significant growth due to the country's strong industrial sector, technological innovation, and greater focus on high-precision manufacturing. The principal industries like aerospace, defense, automotive, energy, and oil & gas are the primary consumers of laser cladding, utilizing the technology for high-value component repair, surface property improvement, and increasing operating life of critical equipment. The increasing demand for efficient and cost-effective repair options is prompting industries to shift away from traditional welding or replacement practices towards next-generation cladding technologies that minimize downtime and maintenance expense. Additionally, the use of laser cladding in additive manufacturing processes and Industry 4.0 projects is enhancing efficiency, as organizations embrace automated, data-based platforms to deliver higher precision and productivity. The availability of pre-eminent technology suppliers, along with government support for advanced manufacturing, drives innovation and market growth. Moreover, uses in the oil and gas industries, especially corrosion-resistant coatings and refurbishment of costly components, are further driving adoption. Ongoing R&D and creation of high-performance materials put the U.S. at the forefront of the laser cladding equipment market globally.

Europe Laser Cladding Equipment Market Analysis

The market for European laser cladding equipment is witnessing a steady growth with the region's robust manufacturing base, technological advancement, and emphasis on high-precision production. Major sectors like aerospace, automotive, energy, and heavy machinery are increasingly adopting laser cladding for repair of components, surface treatment, and enhanced product longevity. Large nations such as Germany, France, and the UK have cornered the market with strong R&D capabilities, government-sponsored innovation initiatives, and a highly trained workforce. Europe's strict rules on sustainability, emissions cutting, and energy efficiency also help to drive the uptake of laser cladding as a green and cost-saving substitute for conventional part replacement or destruction. In addition to that, the adoption of laser cladding within additive manufacturing operations is broadening its applications and allowing industries to gain lightweight, robust, and personalized solutions. These combined with mounting pressures on operational efficiency and new production technologies make Europe a prime market for laser cladding machines.

Asia Pacific Laser Cladding Equipment Market Analysis

The laser cladding equipment market of Asia Pacific is growing at a fast pace, driven by faster-paced industrialization and growing manufacturing activity in the big economies of China, Japan, South Korea, and India. The automotive, shipbuilding, and energy sectors are heavily using laser cladding to extend the life of components, enhance wear resistance, and lower maintenance expenses. Government drives for advanced manufacturing solutions, combined with increases in foreign direct investments, are driving growth in the market even further. Further, the growing attention to cost-saving production processes and precision engineering in the region is propelling the adoption of laser cladding in repair and refurbishment activities, positioning Asia Pacific as a growth hotspot.

Latin America Laser Cladding Equipment Market Analysis

The market for laser cladding equipment in Latin America is increasing steadily, stimulated by demand from the oil & gas, mining, and energy sectors for inexpensive refurbishment of key equipment. Mexico and Brazil remain leading adopters, applying laser cladding to maximize equipment life and minimize maintenance costs. But economic uncertainties, inadequate technological infrastructure, and slower industrial modernization pose obstacles, impeding the rate of adoption across the region.

Middle East and Africa Laser Cladding Equipment Market Analysis

The Middle East and Africa laser cladding equipment market is growing, fuelled by rising adoption in oil & gas, petrochemical, and energy industries. GCC nations, especially Saudi Arabia and the UAE, are making significant investments in newer technologies in a bid to increase equipment life, boost efficiency, and reduce operational expenses. Continued industrial diversification efforts and infrastructural development further bolster the region's potential, with fresh opportunities for applications of laser cladding.

Competitive Landscape:

The key players in the market are strategically focusing on Research & Development (R&D) to enhance technological capabilities and drive innovation in laser cladding processes. Investments in automation, digital technologies, and Industry 4.0 integration form an integral part of their growth strategy. They are extending their geographical reach, targeting emerging economies, and diversifying their product lines to meet specific industrial demands. These industry leaders are investing in sustainability initiatives by developing energy-efficient equipment and adhering to environmental regulations. They are also compliant with international safety and quality standards, reflecting their commitment to excellence. Collaborations, partnerships, and acquisitions are tactics employed by them to strengthen their market position and share expertise. Furthermore, they are concentrating on optimizing supply chain management to ensure timely delivery and customer satisfaction.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ALPHA LASER GmbH

- Dura-Metal (S) Pte. Ltd.

- IPG Photonics Corp.

- Meera Lasers Solution Pvt. Ltd.

- Preco LLC

- SprayWerx Technologies Inc.

- TLM Laser Ltd.

- Trumpf Group

Latest News and Developments:

- In December 2024, The Australian Composites Manufacturing CRC, LaserBond, and The University of Sydney have partnered to develop a fully automated laser cladding system for creating multifunctional metal matrix composite (MMC) coatings. Targeting industries like marine, mining, and defense, the project aims to reduce reliance on overseas parts, minimize downtime through local repair of worn components, and boost Australia’s manufacturing efficiency by enabling cost-effective production of advanced, high-performance parts.

Laser Cladding Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Powers Covered | High Power, Low Power |

| Applications Covered | Power Generation, Industrial, Mining, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ALPHA LASER GmbH, Dura-Metal (S) Pte. Ltd., IPG Photonics Corp., Meera Lasers Solution Pvt. Ltd., Preco LLC, SprayWerx Technologies Inc., TLM Laser Ltd., Trumpf Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the laser cladding equipment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global laser cladding equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the laser cladding equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Laser Cladding Equipment Market Report

The laser cladding equipment market was valued at USD 3.3 Billion in 2025.

The laser cladding equipment market is projected to exhibit a CAGR of 7.57% during 2026-2034, reaching a value of USD 6.4 Billion by 2034.

Key factors driving the laser cladding equipment market include rising demand for cost-effective repair and refurbishment of high-value components, increasing adoption in aerospace, automotive, energy, and mining industries, advancements in automation and additive manufacturing, and the growing need for wear-resistant, corrosion-resistant coatings to extend equipment life and enhance performance.

Europe currently dominates the laser cladding equipment market, driven by advanced manufacturing capabilities, strong aerospace and automotive sectors, stringent sustainability regulations, and extensive R&D initiatives. The region’s focus on high-precision engineering, adoption of Industry 4.0 technologies, and demand for cost-effective, durable surface solutions further fuel market growth.

Some of the major players in the laser cladding equipment market include ALPHA LASER GmbH, Dura-Metal (S) Pte. Ltd., IPG Photonics Corp., Meera Lasers Solution Pvt. Ltd., Preco LLC, SprayWerx Technologies Inc., TLM Laser Ltd., Trumpf Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)