Latin America Food Enzymes Market Size, Share, Trends and Forecast by Type, Source, Formulation, Application, and Country, 2026-2034

Latin America Food Enzymes Market Size, Share, Trends & Forecast (2026-2034)

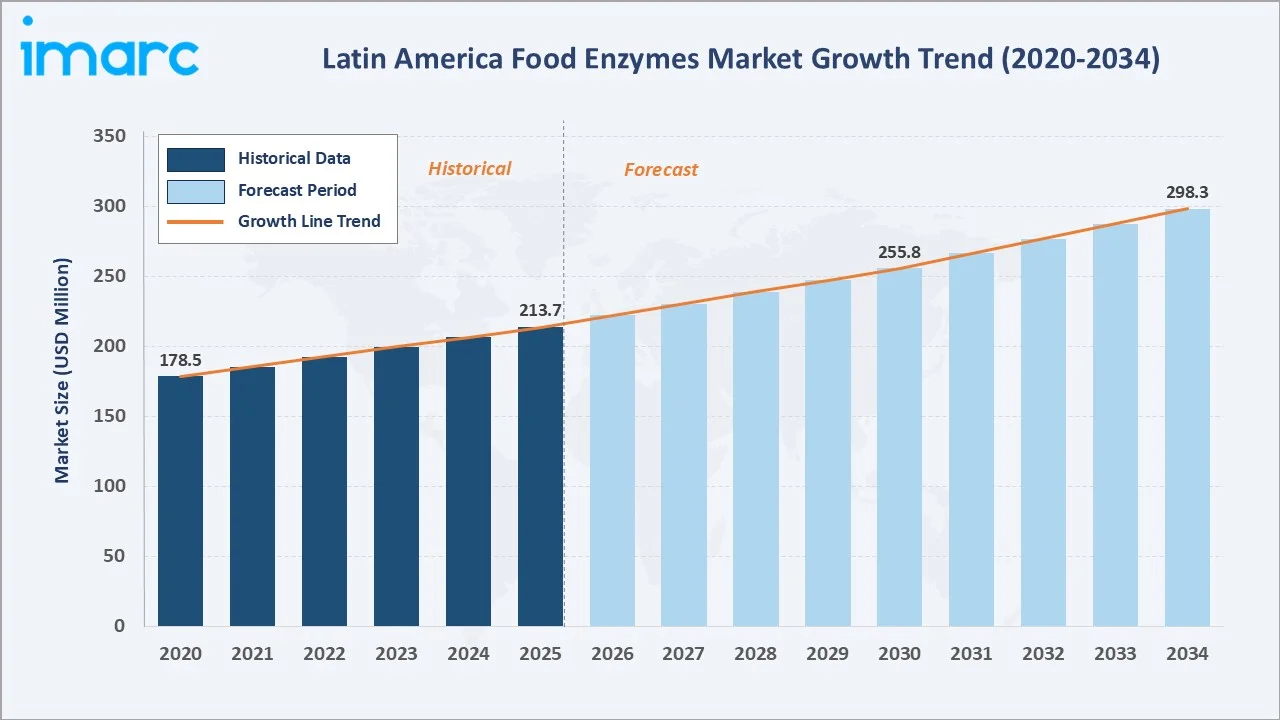

The Latin America food enzymes market reached USD 213.7 Million in 2025 and is projected to reach USD 298.3 Million by 2034, growing at a CAGR of 3.66% during 2026-2034. Continued expansion of the region's food and beverage processing industry, growing clean-label ingredient demand, modernization of bakery and dairy sectors, rising consumer awareness of enzyme-processed natural foods, and the scale-up of Brazilian bioethanol and starch processing collectively anchor the market's growth. Brazil’s agricultural exports reached a record US$16.6 billion in April 2026, reflecting the country’s strong agribusiness performance and expanding role in global food and commodity trade. This is driving the Latin America food enzymes market by increasing demand for enzyme-based processing solutions in grains, dairy, bakery, beverages, and animal-derived food products. Carbohydrase dominates at 39.7%. Powder formulation leads at 48.9%. Brazil commands 34.8% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 213.7 Million |

|

Forecast Market Size (2034) |

USD 298.3 Million |

|

CAGR (2026-2034) |

3.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Carbohydrase (39.7%, 2025) |

|

Dominant Formulation |

Powder (48.9%, 2025) |

|

Leading Country |

Brazil (34.8%, 2025) |

The market expanded from USD 178.5 Million in 2020 to USD 213.7 Million in 2025, anchored at USD 255.8 Million in 2030, and forecast to reach USD 298.3 Million by 2034. COVID-19's impact on the food enzymes market was mixed; hospitality sector closure reduced food service enzyme demand while retail food manufacturing remained stable, and the pandemic's long-term legacy of heightened consumer interest in gut health, probiotic foods, and minimally processed ingredients has structurally increased demand for enzyme-based clean-label processing across LATAM's food industry. Post-pandemic recovery has been supported by modernization investment in food processing facilities that are upgrading from chemical processing aids to enzyme-based natural alternatives.

To get more information on this market, Request Sample

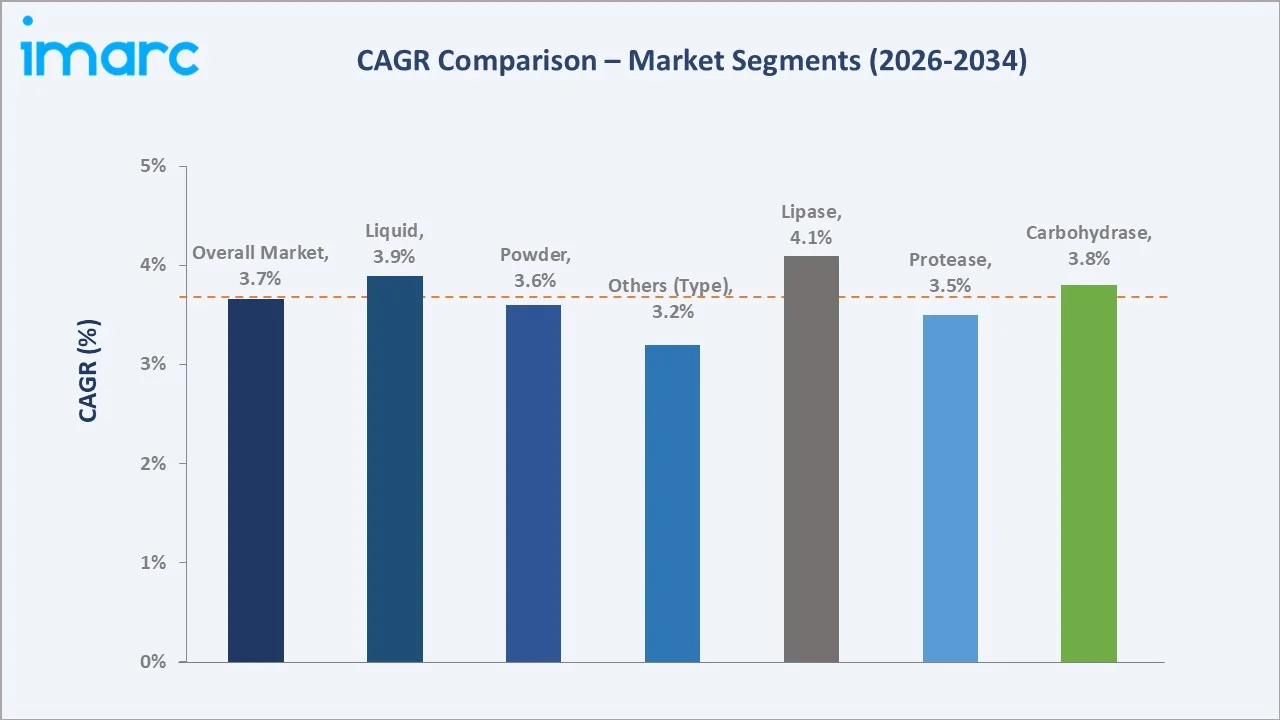

Lipase grows fastest at ~4.1% CAGR through expanding specialty fat modification, cheese flavor development, and the emerging plant-based food sector, requiring lipase-mediated flavor and texture development. Liquid formulation grows at ~3.9% CAGR as dairy, brewing, and beverage manufacturers specify liquid enzyme concentrates for continuous process dosing systems that provide more precise enzyme addition control than manual powder weighing, particularly relevant for LATAM's growing large-scale industrial food processing operations.

Executive Summary

The Latin America food enzymes market reached USD 213.7 Million in 2025, representing a technically specialized segment of the broader food ingredient market where biological catalysts provide food manufacturers with processing advantages that chemical alternatives cannot equally deliver. Food enzymes are biocatalysts derived from microbial fermentation that catalyze specific biochemical reactions in food substrates under mild temperature and pH conditions, enabling food manufacturers to process raw materials more efficiently, improve finished product properties, and replace synthetic chemical processing aids with natural biological alternatives. The market is projected to reach USD 298.3 Million by 2034.

Carbohydrase at 39.7% leads through its broadest application spectrum. Powder formulation at 48.9% leads through the bakery industry's preference for dry powder enzyme blends that can be metered by weight alongside flour in continuous mixing systems, the stability advantage of powder form in LATAM's warm and humid tropical climate storage conditions, and the established industrial bakery enzyme specification format across Brazil's and Mexico's large-scale bread, biscuit, and pastry manufacturing sectors. Brazil region dominates the market at 34.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Carbohydrase - 39.7% share (2025) |

|

Dominant Formulation |

Powder - 48.9% market share (2025) |

|

Leading Country |

Brazil - 34.8% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Carbohydrase at 39.7%: Carbohydrase dominates the market due to its wide use in bakery, brewing, dairy, starch processing, and beverage applications. It helps improve texture, sweetness, fermentation efficiency, and overall processing yield, making it highly preferred by food manufacturers.

- Powder formulation at 48.9%: Powder formulation dominates the market due to its longer shelf life, easier storage, better stability, and cost-effective transportation. It is widely preferred by food processors for bakery, dairy, brewing, and starch processing applications because it enables accurate dosing and convenient handling.

- Brazil at 34.8%: Brazil dominates the market due to its large food and beverage processing industry, strong bakery, dairy, brewing, and meat sectors, and abundant agricultural raw material base. Rising food exports and demand for efficient processing solutions further support enzyme adoption across the country.

Latin America Food Enzymes Market Overview

The Latin America food enzymes market encompasses the procurement, importation, distribution, and application of food-grade enzyme preparations across major enzyme type categories and multiple formulation formats for use in food and beverage processing application sectors across major national markets.

The ecosystem integrates microbial fermentation specialists, downstream purification and standardization plants, formulation facilities, import logistics and customs clearance, in-country distributors, food manufacturer technical service teams, and national food safety regulatory bodies. Macroeconomic factors include expanding food and beverage processing, rising agricultural output, growing packaged food consumption, and increasing demand for cost-efficient production technologies.

Market Dynamics

To evaluate market opportunities, Request Sample

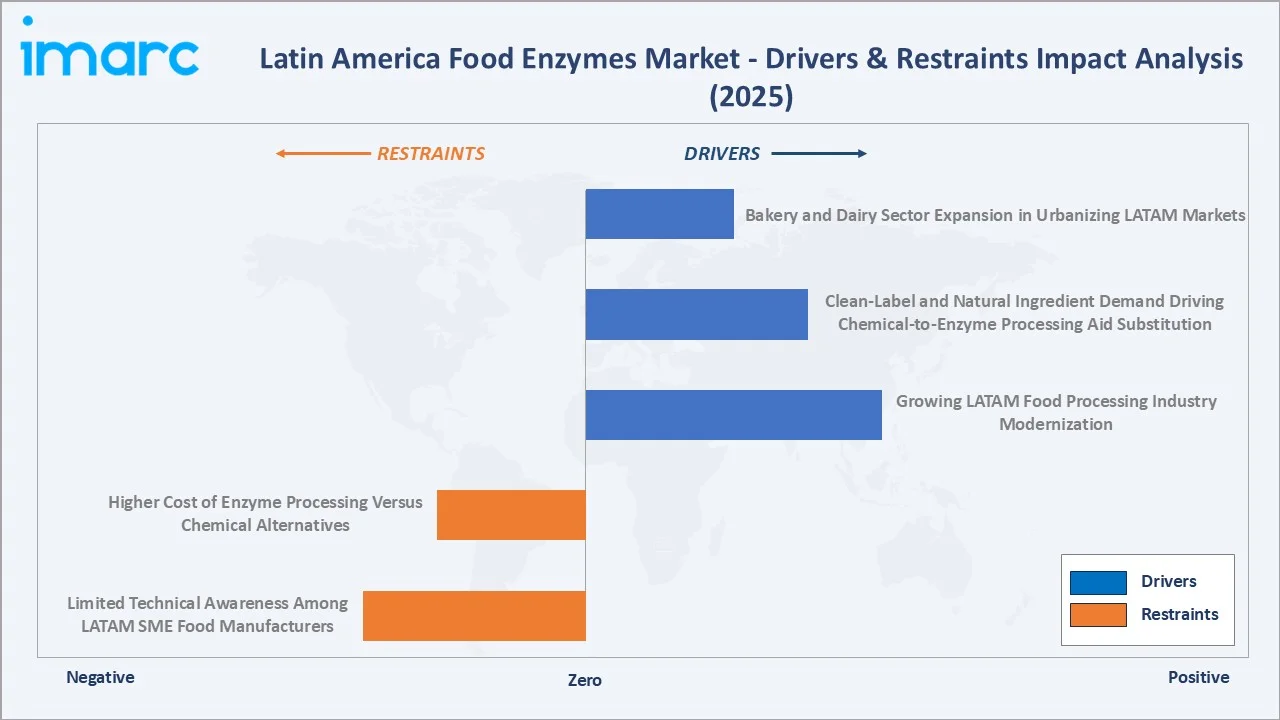

Market Drivers

- Growing LATAM Food Processing Industry Modernization: Latin America's food processing industry is in the most dynamic modernization phase of its history, the simultaneous growth of modern retail (hypermarket, supermarket, and convenience store channels replacing traditional wholesale and informal markets), rising urbanization with Latin America’s 82% urban, and expanding middle-class disposable income are driving food manufacturers to invest in industrial processing technology that enables greater production scale, better product consistency, longer shelf life, and higher value-added products. Enzyme technology is central to this modernization. Artisan bakers transitioning to industrial bakeries need enzyme-based bread improver systems for consistent daily production quality; small dairy processors expanding to regional distribution need rennet and ripening enzyme systems for consistent cheese maturation; craft breweries scaling to regional distribution need glucoamylase and amylase enzyme systems for consistent fermentation yield.

- Clean-Label and Natural Ingredient Demand Driving Chemical-to-Enzyme Processing Aid Substitution: Consumer demand for clean-label food products is creating the most commercially important structural shift in LATAM food enzyme demand since the early industrial bakery enzyme adoption of the 1990s. Each clean-label reformulation substituting chemical processing aids with enzyme-based alternatives creates new food enzyme procurement without necessarily eliminating the original application.

- Bakery and Dairy Sector Expansion in Urbanizing LATAM Markets: The bakery and dairy sectors collectively represent high LATAM food enzyme demand, and both sectors are growing through urbanization-driven food consumption pattern shifts. Per-capita bread consumption in Brazil is growing as urban Brazilians increasingly consume sliced pan bread that requires industrial bakery enzyme systems for consistent texture and extended shelf life.

.webp)

Market Restraints

- Higher Cost of Enzyme Processing Versus Chemical Alternatives: Food enzyme preparations carry significant cost premiums versus chemical processing alternatives. For large-scale industrial food processors, these cost premiums are justified by yield improvement and quality advantages. For LATAM's small and medium food manufacturers, the enzyme cost relative to financial scale creates adoption barriers.

- Limited Technical Awareness Among LATAM SME Food Manufacturers: The food enzyme market's growth in LATAM is constrained by the gap between enzyme technology performance potential and food manufacturer awareness and technical capability to implement enzyme programs effectively. A Brazilian artisan baker who has never used xylanase needs to understand optimal dosage, mixing protocol adjustments, and expected bread quality outcomes before committing to enzyme purchase, and this knowledge is not intuitively obvious. Food enzyme distributors and enzyme manufacturers' technical service teams must invest in training seminars, application laboratory demonstrations, and on-site trials before SME food manufacturers develop confidence to adopt enzyme programs commercially. This education investment creates a long sales cycle and high technical service cost, which makes the SME segment enzyme market development challenging.

Market Opportunities

- Lactose-Free Dairy Product Growth: Lactose intolerance affects Latin American adults, creating one of the world's most commercially significant markets for lactose-free dairy products, where lactase enzyme is the enabling processing technology. Brazil's lactose-free dairy market is the fastest-growing dairy sub-segment, growing 15-20% annually and representing an estimated 10-15% of Brazilian fresh milk retail sales.

- Plant-Based Protein and Alternative Fermented Food: Latin America's emerging plant-based food sector, driven by Brazilian soybean production creating the world's most cost-competitive plant protein feedstock, and by growing LATAM consumer interest in flexitarian and vegetarian diets, is creating enzyme application demand categories that did not exist at a commercial scale 5 years ago. Soy protein texturization, oat beta-glucan hydrolysis, and pea protein solubilization collectively represent new enzyme categories growing at 15-25% CAGR from a small base, contributing incrementally to total LATAM food enzyme market growth through 2034.

Market Challenges

- Enzyme Cold Chain Logistics Requirements Creating Cost and Access Challenges in Remote LATAM Markets: Many commercial food enzyme preparations require refrigerated storage and transport to maintain enzymatic activity during distribution, a requirement that creates significant logistics cost and product quality risk in LATAM's infrastructure-challenged interior markets.

- Brazilian Real and Argentine Peso FX Volatility Creating Pricing Instability for USD-Denominated Enzyme Imports: LATAM food enzyme market pricing is primarily USD-denominated at the import/distribution level, creating structural FX risk for LATAM food manufacturers whose revenues are local currency but enzyme input costs track USD.

Emerging Market Trends

1. Clean-Label Bread Improver Systems Replacing Chemical Dough Conditioners in LATAM Industrial Bakery

Clean-label bread improver systems are emerging as industrial bakeries replace chemical dough conditioners with enzyme-based solutions. Enzymes such as amylases, xylanases, and lipases help improve dough handling, volume, softness, and shelf life while supporting cleaner ingredient labels. This trend is gaining traction as bakery manufacturers respond to consumer demand for natural, minimally processed, and label-friendly baked goods.

2. Craft Brewing Expansion Driving Specialty Enzyme Adoption Across LATAM

Craft brewing expansion is emerging as small and mid-sized breweries adopt specialty enzymes to improve fermentation efficiency, flavor consistency, and raw material utilization. Enzymes such as amylases, beta-glucanases, and proteases help optimize mash performance, enhance beer clarity, and support the production of diverse craft beer styles. Rising demand for premium and locally brewed beverages is further encouraging enzyme use across LATAM breweries.

3. Precision Enzyme Dosing Technology Enabling Consistent Quality in LATAM Automated Food Processing

Precision enzyme dosing technology is emerging as automated food processing plants seek consistent product quality and reduced formulation errors. Accurate dosing helps optimize enzyme performance in bakery, dairy, brewing, starch, and beverage applications while minimizing waste and batch variability. This supports higher production efficiency, better texture, flavor, and shelf-life control across industrial food processing operations.

4. Fermented Foods Renaissance Creating Endogenous Enzyme Awareness and Market Development

The fermented foods renaissance is emerging as rising interest in yogurt, kefir, sourdough, kombucha, cheese, and traditional fermented foods increases awareness of natural enzyme activity. This is encouraging manufacturers to use enzymes for improving fermentation control, flavor development, texture, and product consistency. The trend is also supporting innovation in clean-label, probiotic, and functional food categories across the region.

Industry Value Chain Analysis

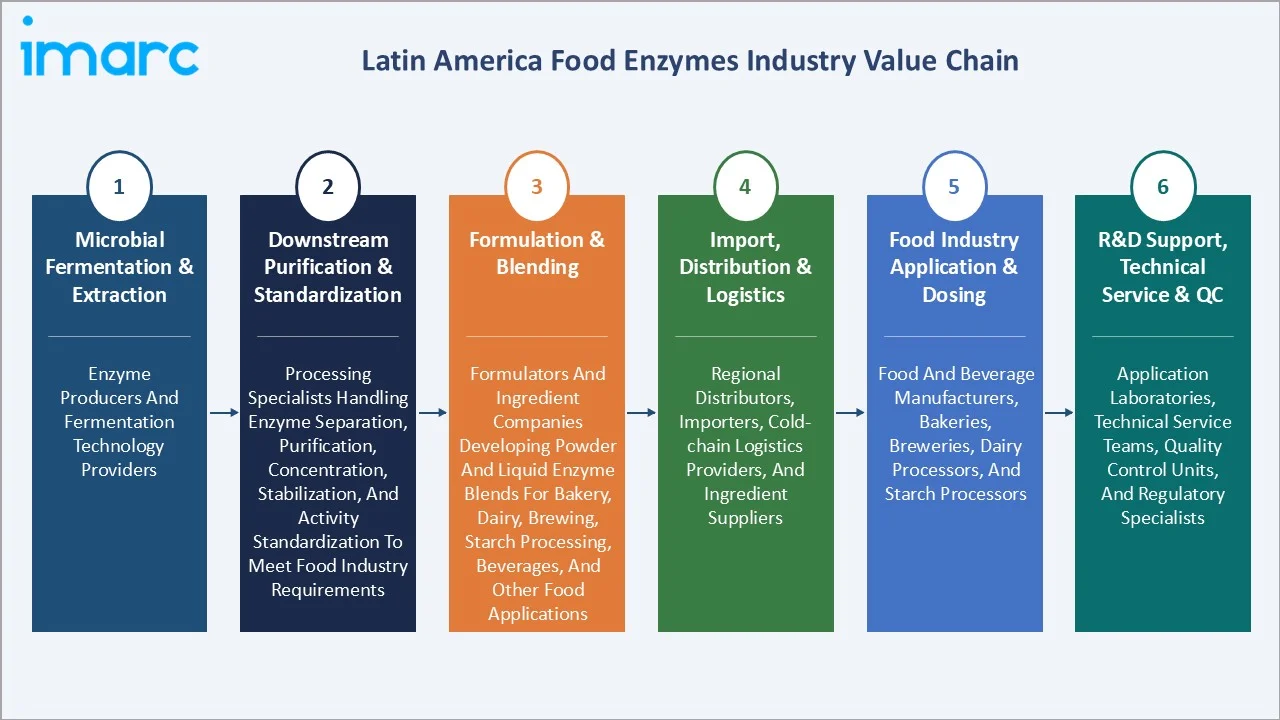

The Latin America food enzymes value chain integrates microbial fermentation and extraction at production sites, downstream purification and standardization, formulation into commercial food enzyme products, importation through LATAM customs, distribution by in-country specialty ingredient distributors, and technical application service supporting food manufacturer enzyme adoption.

|

Stage |

Key Participants |

|

Microbial Fermentation & Extraction |

Enzyme producers and fermentation technology providers. |

|

Downstream Purification & Standardization |

Processing specialists handling enzyme separation, purification, concentration, stabilization, and activity standardization to meet food industry requirements. |

|

Formulation & Blending |

Formulators and ingredient companies developing powder and liquid enzyme blends for bakery, dairy, brewing, starch processing, beverages, and other food applications. |

|

Import, Distribution & Logistics |

Regional distributors, importers, cold-chain logistics providers, and ingredient suppliers. |

|

Food Industry Application & Dosing |

Food and beverage manufacturers, bakeries, breweries, dairy processors, and starch processors. |

|

R&D Support, Technical Service & QC |

Application laboratories, technical service teams, quality control units, and regulatory specialists. |

The R&D support, technical service, and quality control tier provides the value chain's highest commercial leverage. Technical service investment translates directly to customer specification wins that generate 3-7 year recurring enzyme supply revenue from food manufacturer production commitments. The quality control function is also commercially critical because food-grade enzyme preparations require demonstration of activity level, purity, and safety certifications that LATAM food safety regulators require for food additive approval documentation.

Technology Landscape in the Latin America Food Enzymes Industry

Microbial Fermentation Enzyme Production Technology

Microbial fermentation enzyme production technology enables scalable, controlled, and cost-efficient production of food-grade enzymes. It supports consistent enzyme activity, purity, and functionality for bakery, dairy, brewing, starch processing, and beverage applications. In March 2026, IFF strengthened its production and innovation capabilities in Latin America to support the rapid growth of its Health & Biosciences business in the region. The initiative includes converting its Arroyito site in Argentina into the company’s first regional fermentation-based enzyme production hub and opening a household care application laboratory in Brazil, helping improve supply reliability, speed to market, and locally tailored solutions for brewing, animal nutrition, biofuels, and home care. As regional fermentation capabilities and R&D facilities expand, the technology is improving local innovation, faster product development, and customized enzyme solutions for LATAM food processors.

Enzyme Immobilization Technology for Continuous Processing

Enzyme immobilization technology enables enzymes to be fixed onto solid supports and reused in continuous food processing systems. This improves enzyme stability, reduces processing costs, and supports consistent product quality in applications such as dairy, beverages, starch conversion, and specialty ingredient production. As LATAM food processors modernize operations, immobilized enzymes are gaining relevance for efficient, scalable, and waste-reducing production.

Enzyme Engineering and Protein Design

Enzyme engineering and protein design enable the development of enzymes with improved stability, specificity, and performance under varied processing conditions. These technologies help food manufacturers customize enzyme functions for bakery, dairy, brewing, starch processing, and beverage applications. They also support cleaner labels, higher yields, reduced processing time, and more consistent product quality across modernized LATAM food production systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Carbohydrase |

39.7% |

2025 |

|

Source |

🔒 |

🔒 |

2025 |

|

Formulation |

Powder |

48.9% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Country |

Brazil |

34.8% |

2025 |

By Type

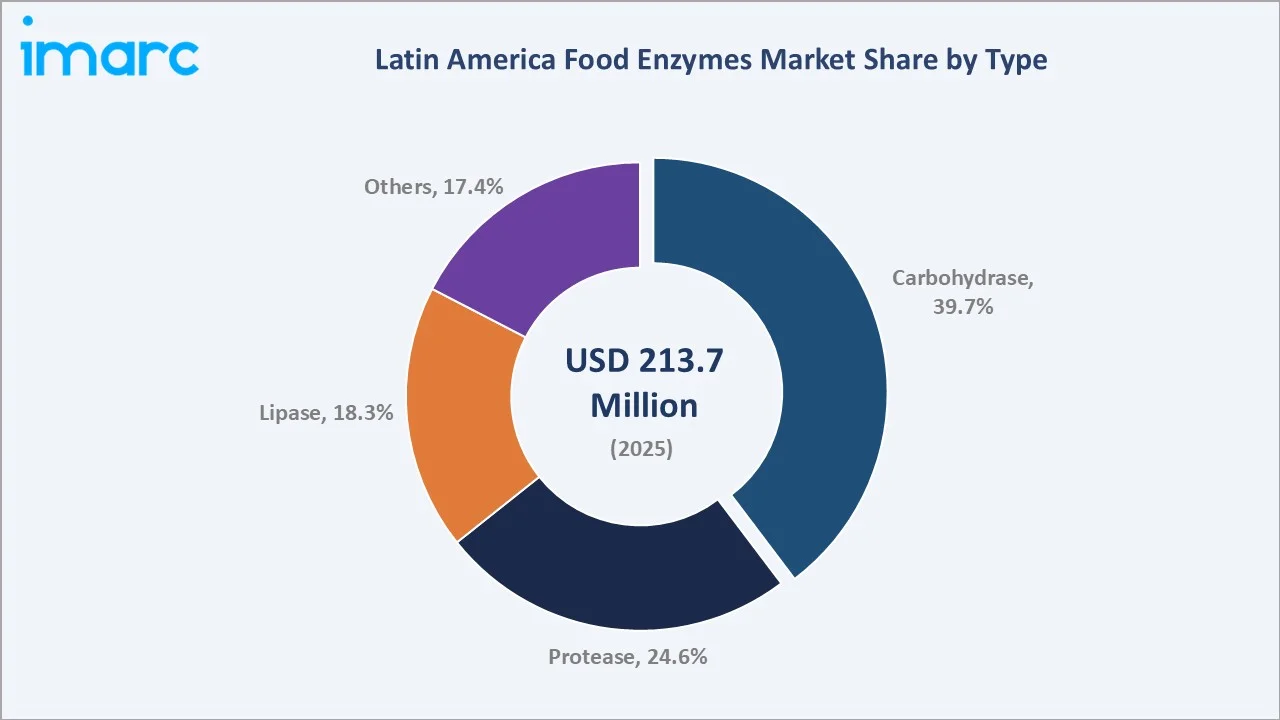

Carbohydrase leads at 39.7% market share (2025). Carbohydrase encompasses alpha-amylase (liquefaction and baking freshness), beta-amylase (malting and fermentation), glucoamylase (saccharification to glucose), xylanase (arabinoxylan hydrolysis for dough improvement), pectinase (fruit juice clarification and wine processing), lactase (lactose hydrolysis for lactose-free dairy), beta-glucanase (brewing and oat milk processing), and cellulase (fiber hydrolysis and plant-based food processing).

To access detailed market analysis, Request Sample

Protease at 24.6% covers rennet/chymosin for dairy, meat tenderization enzymes, and protein hydrolysate production enzymes. Lipase at 18.3% grows fastest at ~4.1% CAGR through specialty fat modification, cheese flavor development, and clean-label emulsifier replacement. Others at 17.4% encompasses glucose oxidase, lipoxygenase, phytase, transglutaminase, laccase, and specialty oxidoreductase enzymes.

By Formulation

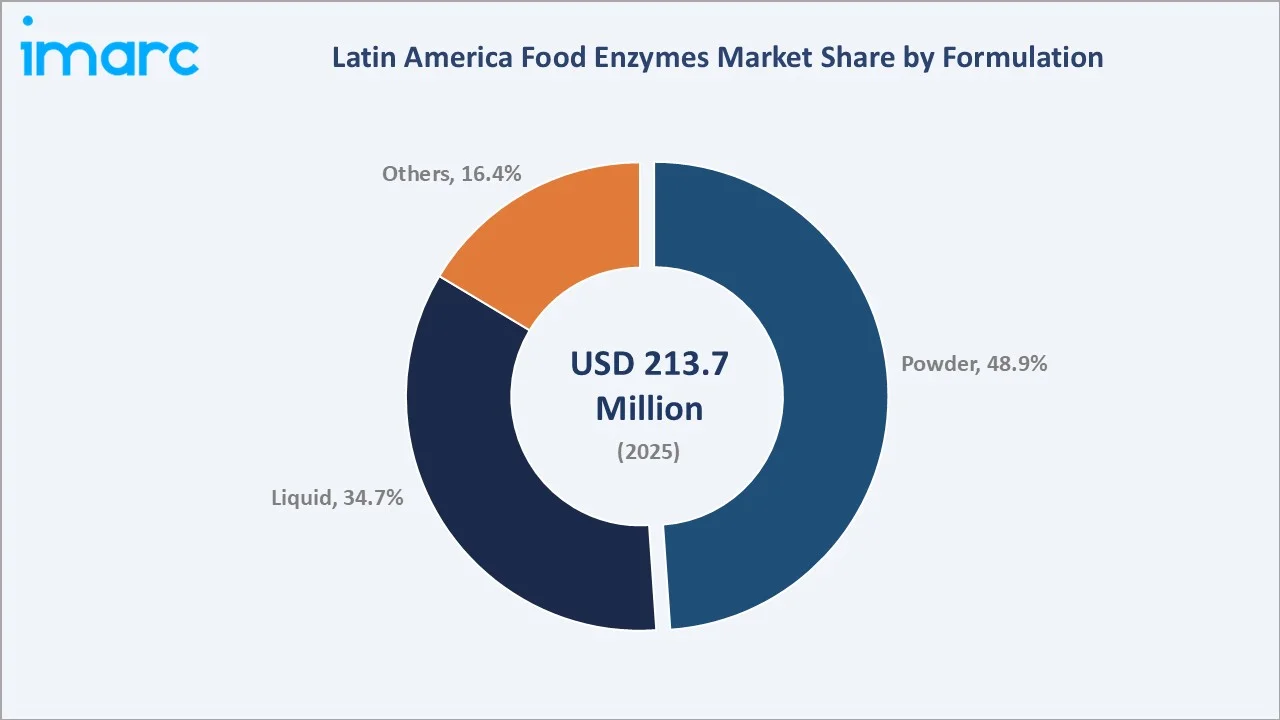

Powder formulation leads at 48.9% market share (2025). Powder enzyme preparations serve the bakery industry's mixing system compatibility requirements, provide superior ambient temperature stability in tropical LATAM climates, and enable precise dry ingredient dosing in automated flour handling systems. Standard powder activity specifications and dust-free granular formats have established powder as the industrial bakery standard enzyme format.

Liquid formulation at 34.7% grows fastest at ~3.9% CAGR through dairy, brewing, and juice processing sectors requiring automated liquid dosing precision. Liquid enzyme concentrates serve rennet dosing in cheese vats, glucoamylase in brewery fermentation tanks, and pectinase in fruit juice macerators, where continuous in-line dosing is technically essential. Others at 16.4% includes immobilized enzyme preparations, coated granules, and tablet enzyme formats for specialty applications.

Regional Market Insights

|

Country |

Share (2025) |

Key Food Enzymes Market Drivers & Characteristics |

|

Brazil |

34.8% |

Supported by its large food processing base, strong bakery, dairy, brewing, meat, and agricultural processing industries. |

|

Mexico |

18.9% |

Driven by expanding packaged food production, bakery and beverage processing, and rising demand for enzyme-based clean-label and efficiency-enhancing solutions. |

|

Argentina |

11.6% |

Supported by its strong agricultural and grain processing sector, along with the growing use of enzymes in bakery, dairy, and beverage applications. |

|

Colombia |

9.3% |

Developing through rising processed food consumption, growing bakery and beverage sectors, and increasing adoption of enzyme solutions for quality and yield improvement. |

|

Chile |

8.2% |

Benefits from its export-oriented food and beverage industry, where enzymes are used to improve processing efficiency, product consistency, and shelf-life performance. |

|

Peru |

6.9% |

Expanding gradually with growth in food processing, bakery, dairy, and fruit-based beverage applications. |

|

Others |

10.3% |

The others include smaller Latin American markets where enzyme adoption is increasing through packaged food growth, industrial bakery expansion, and modernization of food processing operations. |

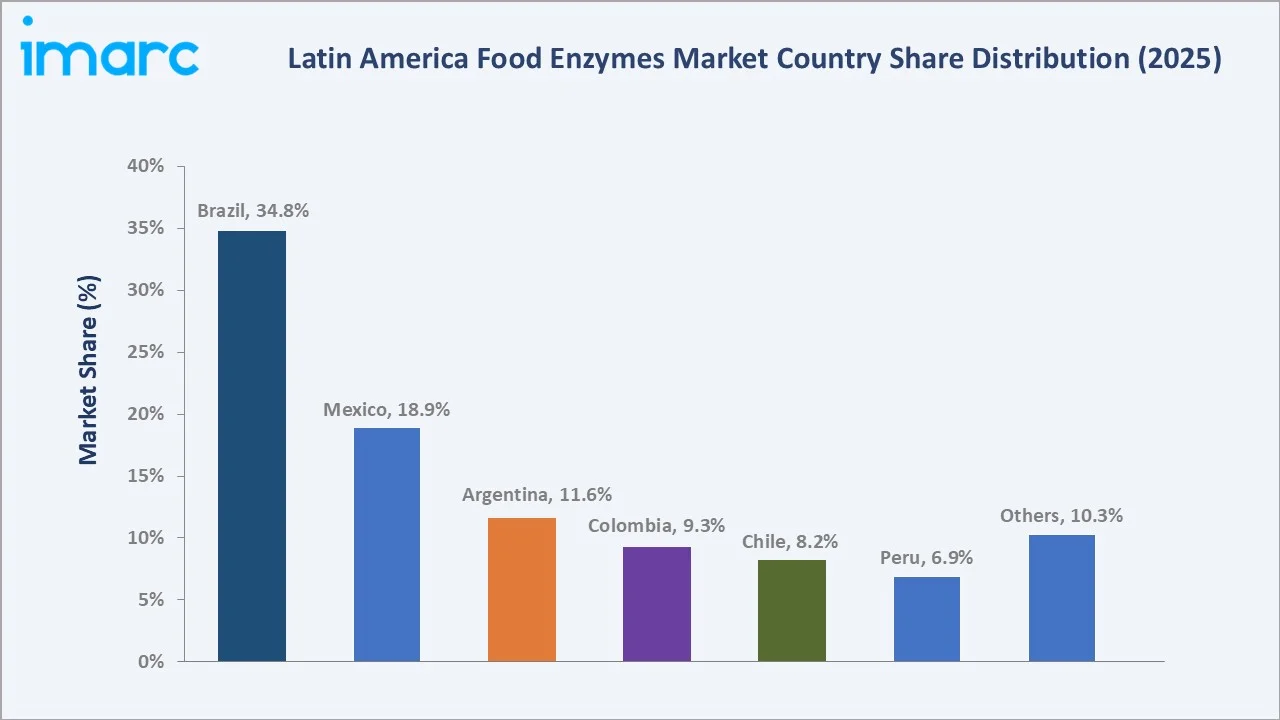

Brazil's 34.8% market leadership reflects the combination of the region's largest food processing sector, world-leading sugar-ethanol biorefinery creating industrial enzyme infrastructure, sophisticated beer industry driving carbohydrase demand, and Brazil's regulatory framework that, despite its rigor, provides clear approval pathways for international enzyme suppliers willing to invest in Brazilian market regulatory compliance.

Mexico's 18.9% reflects the corn-based food industry's structural carbohydrase demand, modern brewery enzyme systems, and proximity to North American enzyme supply chains. Argentina's 11.6% is driven by the world-leading soybean processing industry and dairy sector. Colombia's 9.3% features the growing dairy sector and coffee/cocoa processing enzyme demand. Chile's 8.2% is anchored by the wine and salmon aquaculture enzyme applications. Peru's 6.9% encompasses the world's leading fishmeal protease demand. Others at 10.3% spans Ecuador, Uruguay, Central America, and the Caribbean with diverse specialty applications.

Competitive Landscape

The Latin America food enzymes competitive landscape is highly concentrated among three to four global leaders, with a long tail of specialty suppliers serving niche applications. The concentration reflects the high barriers to food enzyme market competition, industrial fermentation infrastructure, protein engineering R&D capability, global quality management and regulatory affairs, and LATAM-specific technical service infrastructure that Japanese, Indian, and Chinese enzyme suppliers are challenged to replicate at competitive investment levels.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

International Flavors & Fragrances Inc. |

AMYLEX, LAMINEX, ALPHALASE, DIAZYME, BCLEAR, TEXSTAR, ENOVERA |

Market Leader |

IFF enzymes are working tirelessly to optimize processes, boost sustainability, and minimize waste. |

|

Amano Enzyme Inc. |

Amano PG500, CheeseMax PB, Umamizyme Pulse |

Niche Player |

Amano’s comprehensive portfolio of food-grade enzymes supports applications across baking, brewing, plant-based foods, protein processing, and specialty food production. |

|

Advanced Enzyme Technologies |

SEBake Fresh 10P Ultra, SEBake Pro, SEBMalt STP L, SEBCheese Pro, Hydrolact W |

Challenger |

Advanced Enzymes is a research-driven company with global leadership in the manufacturing of enzymes and probiotics. |

|

Enzyme Development Corporation |

ENZECO FICIN 50K, ENZECO BROMELAIN, THISTLEZYME, ENZECO BACTERIAL ALPHA AMYLASE, ENZECO BACTERIAL AMYLASE BL, ENZECO BACTERIAL AMYLASE 25LN |

Established Player |

Enzyme Development Corporation offers experience in enzyme applications and formulations, high standards of quality to ensure consistent results, an extensive enzyme product line, custom blending and packaging, and prompt attention to customer requirements. |

The competitive landscape's most significant structural change is the Novozymes-Chr. Hansen merger creating Novonesis, a combined enzyme + microbial culture + probiotic company that can sell integrated biotechnology solutions to LATAM food manufacturers through a single commercial relationship.

Key Company Profiles

International Flavors & Fragrances Inc.

International Flavors and Fragrances (IFF) merged with DuPont Nutrition and Biosciences in 2021, inheriting DuPont's Danisco food enzyme business, one of the global top food enzyme portfolios with LATAM market presence.

- Key Products: AMYLEX, LAMINEX, ALPHALASE, DIAZYME, BCLEAR, TEXSTAR, ENOVERA.

- Strategic Focus: Centered on expanding regional fermentation-based enzyme production and application innovation to deliver faster, reliable, and locally tailored solutions for brewing, food processing, and related bioscience applications.

Amano Enzyme Inc.

Amano Enzyme is a Japanese specialty enzyme manufacturer. Amano Enzyme's competitive positioning in LATAM food enzymes is differentiated by its specialty enzyme precision, Japanese manufacturing quality standards, and the unique enzyme activity profiles of Amano's proprietary enzyme preparations that serve applications requiring specific substrate selectivity not achievable with large-scale enzyme products.

- Key Products: Amano PG500, CheeseMax PB, Umamizyme Pulse.

- Strategic Focus: Centered on supplying high-quality specialty enzymes for bakery, dairy, beverages, and protein processing while supporting clean-label formulation and process efficiency for regional food manufacturers.

Market Concentration Analysis

The Latin America food enzymes market is highly concentrated at the supplier level. International Flavors & Fragrances Inc., Amano Enzyme Inc., Advanced Enzyme Technologies, and Enzyme Development Corporation together account for approximately 70-85% of the LATAM food enzyme market value, reflecting the high technical and regulatory barriers to food enzyme market competition. The concentration is reinforced by the Novonesis merger, which combined Novozymes' approximately 40-45% market share with Chr. Hansen's approximately 5-8% share in a single entity that may face merger control scrutiny in some jurisdictions.

Investment & Growth Opportunities

Highest Growth Segments

Lipase type (~4.1% CAGR), liquid formulation (~3.9% CAGR), protease for plant-based protein (15-20% CAGR from small base), lactase for lactose-free dairy (15-20% CAGR from growing base), craft brewing specialty enzymes (~10-15% CAGR in craft segment), and clean-label bakery enzyme systems (~5-6% CAGR in industrial bakery clean-label conversion segment) represent the highest-growth investment vectors within the LATAM food enzyme market through 2034.

Emerging Investment Opportunities

LATAM domestic food enzyme production represents the market's most strategically significant long-term opportunity. Brazil's infrastructure advantages for enzyme production create conditions favorable to domestic food enzyme production investment. A 500-1,000 tonne/year food enzyme production facility in Brazil (USD 30-80 Million investment) producing xylanase, amylase, and pectinase at 20-30% below import cost would create material LATAM market competitive advantage and supply chain security.

Investment Themes

- Lactose-free dairy enzyme systems for Brazil and Mexico's high-lactase-demand market: Brazil's lactose-free dairy market is growing at 15-20% annually, with lactase as the enabling enzyme, creating a USD 5-10 Million annual recurring revenue opportunity for lactase suppliers that is expanding proportionally with lactose-free dairy category growth.

- Plant-based protein processing enzyme development for LATAM's emerging alternative protein sector: Brazilian soybean and pea protein processing for plant-based food applications creates protease and enzyme demand growing at 15-25% annually from a small base. Each new LATAM plant-based food manufacturer requires protease and transglutaminase enzyme solutions for protein texturization, meat analogue gel formation, and plant-based egg replacement applications.

Future Market Outlook (2026-2034)

The Latin America food enzymes market is projected to grow from USD 213.7 Million in 2025 to USD 298.3 Million by 2034, delivering a 3.66% CAGR over the forecast period. The market's anchor value of USD 255.8 Million in 2030 represents a LATAM food enzyme industry where clean-label bakery enzyme systems have been widely adopted by industrial bread and biscuit manufacturers across Brazil and Mexico, lactase enzyme is processing 20-25% of all LATAM fresh milk for lactose-free dairy products, and the first Brazilian domestic food enzyme production facility has commenced commercial production, reducing the import dependency that currently constrains LATAM food enzyme pricing and supply chain resilience.

Three structural forces sustain the LATAM food enzyme market growth through 2034 with confidence. First, the secular trend toward clean-label food processing is irreversible. Brazilian and Mexican consumers' growing preference for natural, minimally processed foods creates a permanent commercial incentive for food manufacturers to adopt enzyme-based natural processing alternatives to chemical additives, creating a continuously expanding addressable market for bakery, dairy, meat, and beverage food enzymes. Second, the food processing sector modernization across LATAM's tier-2 and tier-3 food manufacturers. Third, new application category emergence, each adding incremental enzyme demand categories to the established bakery, dairy, and brewing base.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including LATAM Regional Directors; National Sales Managers; technical service managers; food technology managers; and regulatory affairs specialists from Brazilian and Mexican food industry associations.

Secondary Research

Secondary research encompassed AMFEP (Association of Manufacturers and Formulators of Enzyme Products) annual industry statistics; food enzyme evaluation reports; Brazilian food industry annual reports; Mexico food industry reports. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up enzyme type and application sector models calibrated against (i) AMFEP food enzyme market statistics for global volumes with LATAM regional adjustment factors, (ii) food processing sector growth rates by country, (iii) enzyme price trend analysis, and (iv) application-specific adoption curve modeling. Key forecast inputs include merger commercial synergy realization timeline, LATAM domestic enzyme production investment feasibility, and LATAM food processing modernization investment cycle.

Latin America Food Enzymes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Sources Covered | Microorganisms, Bacteria, Fungi, Plants, Animals |

| Formulations Covered | Powder, Liquid, Others |

| Applications Covered | Beverages, Processed Foods, Dairy Products, Bakery Products, Confectionery Products, Others |

| Countries Covered | Argentina, Brazil, Mexico, Colombia, Chile, Peru, Others |

| Companies Covered | International Flavors & Fragrances Inc., Amano Enzyme Inc., Advanced Enzyme Technologies, Enzyme Development Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Latin America Food Enzymes Market Report

The Latin America food enzymes market reached USD 213.7 Million in 2025, driven by the expanding food processing sector modernization across Brazil, Mexico, Argentina, Colombia, Chile, and Peru; growing clean-label bakery enzyme adoption in industrial bread production; dairy sector growth creating rennet and lactase demand; brewing sector carbohydrase requirements; and the diversified food enzyme applications across fruit juice processing, meat tenderization, starch conversion, and specialty fat modification.

The market grows at 3.66% CAGR during 2026-2034, reaching USD 298.3 Million by 2034. The growth reflects clean-label processing trend acceleration, lactose-free dairy expansion requiring lactase, Brazilian and Mexican craft brewing specialty enzyme adoption, plant-based protein processing creating new protease demand categories, and the progressive modernization of LATAM's SME food processor segment adopting enzyme technology as technical awareness increases through distributor training programs.

Carbohydrase leads at 39.7% through amylase for bakery and brewing, glucoamylase for starch saccharification and bioethanol, xylanase for bread improvement, pectinase for fruit juice and wine, and lactase for lactose-free dairy - the broadest application spectrum of any enzyme category.

Powder formulation leads at 48.9% through the bakery industry's dry ingredient mixing system compatibility, tropical climate ambient temperature stability, and precision dosing by weight in automated flour handling.

Brazil leads at 34.8% through the region's largest food processing sector, world-leading bioethanol and starch processing creating industrial carbohydrase demand, LATAM brewing operations, sophisticated dairy sector requiring rennet and lactase, and a regulatory framework providing clear approval pathways for international enzyme suppliers.

Leading companies include International Flavors & Fragrances Inc., Amano Enzyme Inc., Advanced Enzyme Technologies, and Enzyme Development Corporation, among others.

The market is projected to reach approximately USD 255.8 Million by 2030, with Novonesis post-merger integration delivering integrated enzyme + culture + probiotic LATAM dairy and bakery solutions, Brazilian industrial bakery completing clean-label enzyme reformulation, lactase demand growing 15-20% annually with lactose-free dairy expansion, and specialty lipase growing for Brazil's premium cheese and Chile's wine enzyme applications.

Food enzymes are proteins produced by microbial fermentation that catalyze specific biochemical reactions in food substrates. Food enzymes are classified as processing aids in some jurisdictions or as food additives in others, with international standards providing the safety evaluation framework recognized by LATAM regulators.

The clean-label trend is the single most commercially significant driver of incremental food enzyme demand growth in LATAM. Each food manufacturer reformulating from chemical processing aids to enzyme-based alternatives creates new enzyme procurement where none existed.

Three priority opportunities: lactose-free dairy lactase supply agreements with Brazil's top-5 dairy companies, clean-label bakery enzyme system commercial development for LATAM industrial bakery clean-label conversion, and Brazilian domestic food enzyme production investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)