Latin America Hypodermic Syringes and Needles Market Size, Share, Trends and Forecast by Product, End Use, and Country, 2026-2034

Latin America Hypodermic Syringes and Needles Market Size, Share, Trends & Forecast (2026-2034)

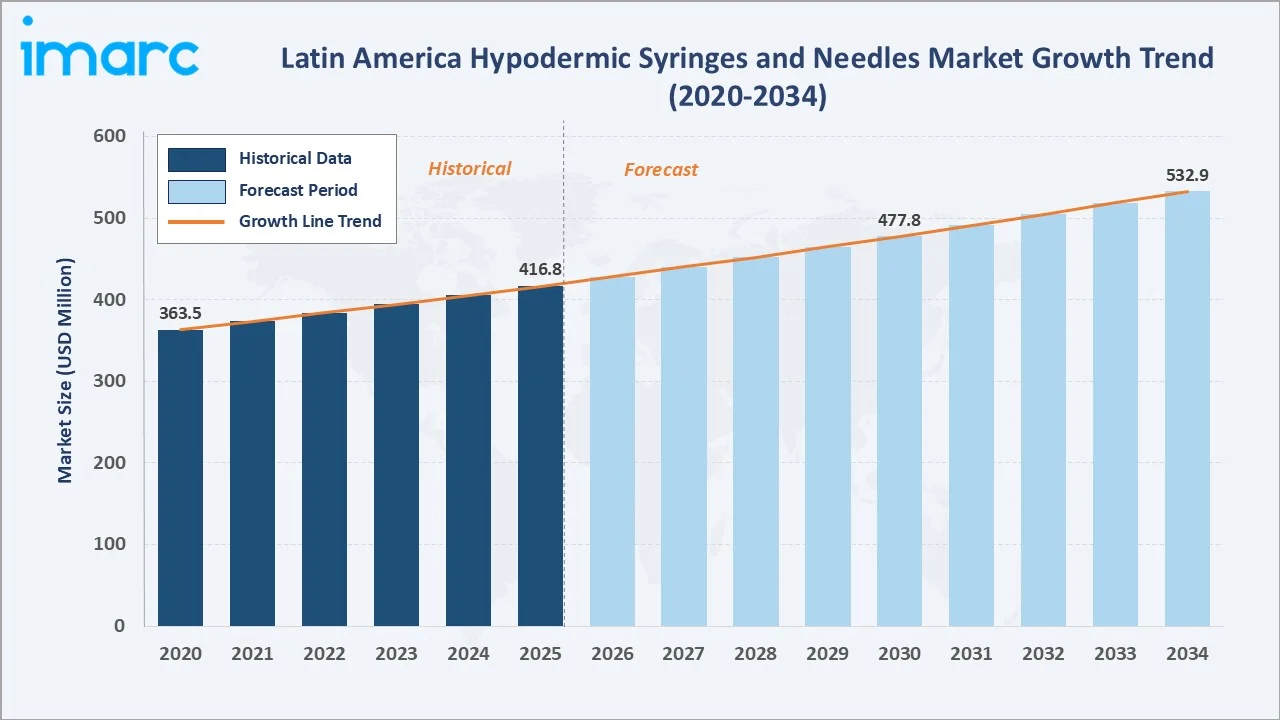

The Latin America hypodermic syringes and needles market reached USD 416.8 Million in 2025 and is projected to reach USD 532.9 Million by 2034, growing at a CAGR of 2.77% during 2026-2034. Increasing chronic disease burden, expanding vaccination programs, growing surgical procedure volumes, and mandates for safety-engineered devices are key growth drivers.

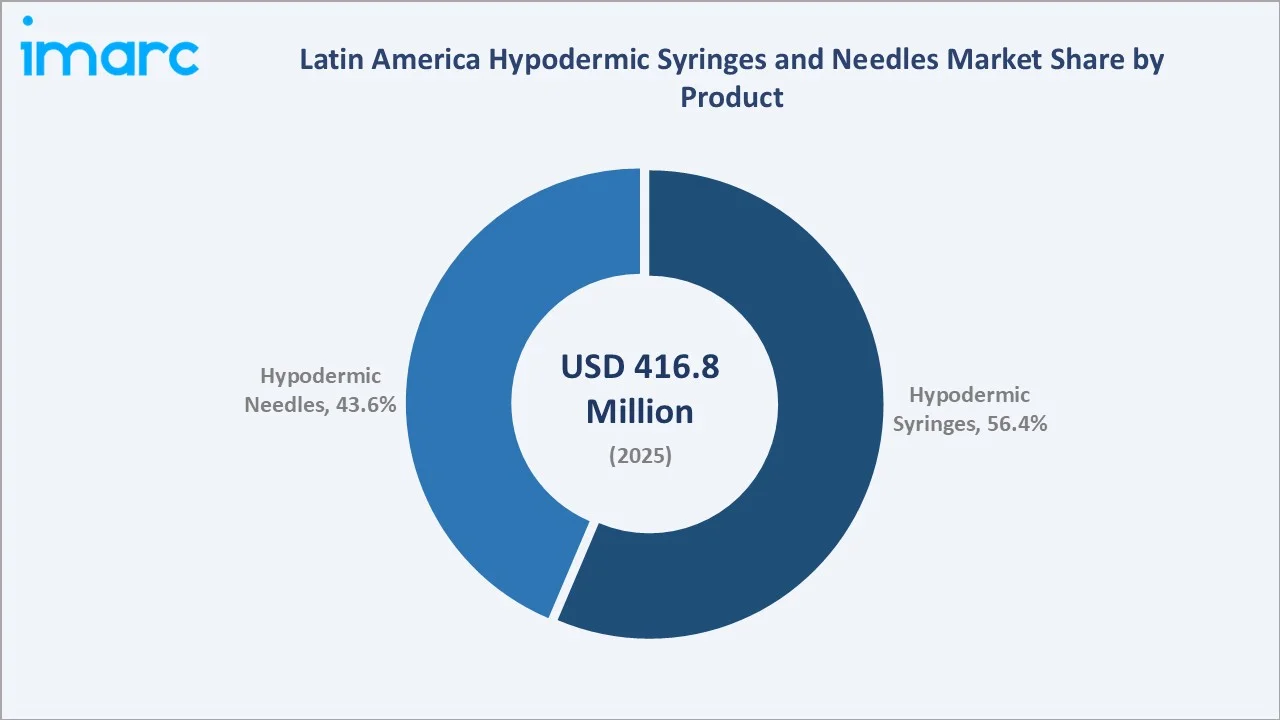

Hypodermic Syringes dominate at 56.4% of product share. Hospitals lead end use at 39.7%. Brazil commands 40.8% of the regional share in 2025, anchored by government immunization programs, a large patient base, and established medical device manufacturing infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 416.8 Million |

|

Forecast Market Size (2034) |

USD 532.9 Million |

|

CAGR (2026-2034) |

2.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Hypodermic Syringes (56.4%, 2025) |

|

Dominant End Use |

Hospitals (39.7%, 2025) |

|

Leading Region |

Brazil (40.8%, 2025) |

The market expanded steadily from its 2020 base to USD 416.8 Million in 2025, supported by post-pandemic healthcare investment and vaccination rollouts. The forecast trajectory to USD 532.9 Million by 2034 reflects consistent demand from chronic disease management, biosimilar injectables, and home-care injection growth across Brazil, Mexico, and Argentina.

To get more information on this market, Request Sample

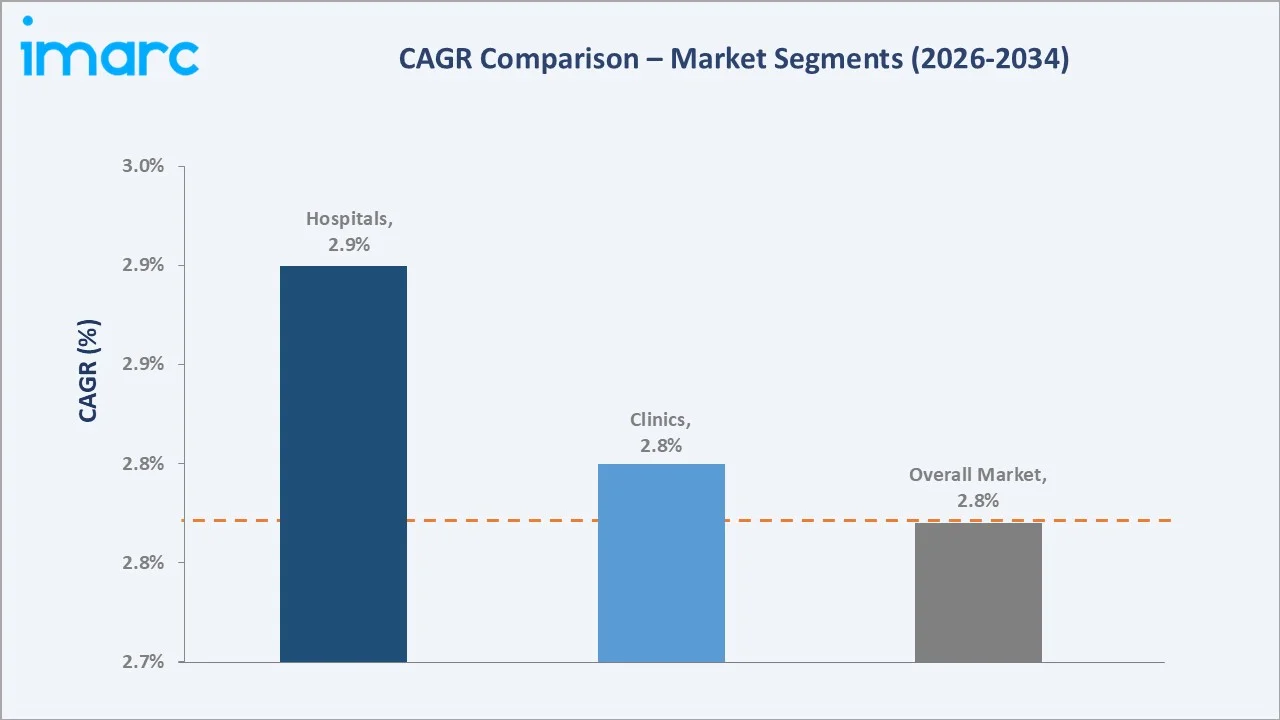

Hypodermic Syringes grow at ~3.0% CAGR as safety syringe adoption and auto-disable mandates expand across hospital and vaccination programs. Hospitals at ~2.9% CAGR reflect sustained procedure volume growth. The overall market CAGR of 2.77% during 2026–2034 represents steady structural demand across all product and end-use segments.

Executive Summary

The Latin America hypodermic syringes and needles market reached USD 416.8 Million in 2025, serving as an essential component of regional healthcare delivery across hospitals, clinics, home care, and veterinary settings. Hypodermic syringes and needles are critical for drug delivery, vaccination, blood sampling, and insulin administration.

The market is projected to reach USD 532.9 Million by 2034. Hypodermic Syringes lead at 56.4%, Hospitals dominate end use at 39.7%, and Brazil holds 40.8% regional share.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Hypodermic Syringes – 56.4% share (2025) |

|

Dominant End Use |

Hospitals – 39.7% market share (2025) |

|

Leading Region |

Brazil – 40.8% market share (2025) |

|

Market Opportunity |

Safety syringe mandates; biosimilar injectables; home-care growth; vaccination programs |

Key Analytical Observations Supporting The Above Data:

- Hypodermic Syringes at 56.4%: Leads through universal use across drug delivery, vaccination, and blood sampling. Safety syringe mandates by PAHO and national health ministries are expanding premium product revenue within the segment.

- Hospitals at 39.7%: Dominates end-use through high volumes of surgical procedures, in-patient medication administration, and government-funded immunization programs operating through hospital infrastructure.

- Brazil at 40.8%: Commands regional leadership through the largest patient base in Latin America, established medical device manufacturing, strong public procurement, and robust national vaccination program infrastructure.

Latin America Hypodermic Syringes and Needles Market Overview

The Latin America hypodermic syringes and needles market encompasses the design, manufacture, and distribution of hypodermic syringes, conventional needles, and safety needles for use in drug delivery, vaccination, blood sampling, and chronic disease management across all healthcare settings.

The ecosystem integrates polymer and steel raw material suppliers, medical device manufacturers, sterilization service providers, regulatory bodies including ANVISA and COFEPRIS, distributors, group purchasing organizations, and end-use healthcare facilities. Macroeconomic factors include rising healthcare expenditure, government health initiatives, and growing chronic disease prevalence.

Market Dynamics

To evaluate market opportunities, Request Sample

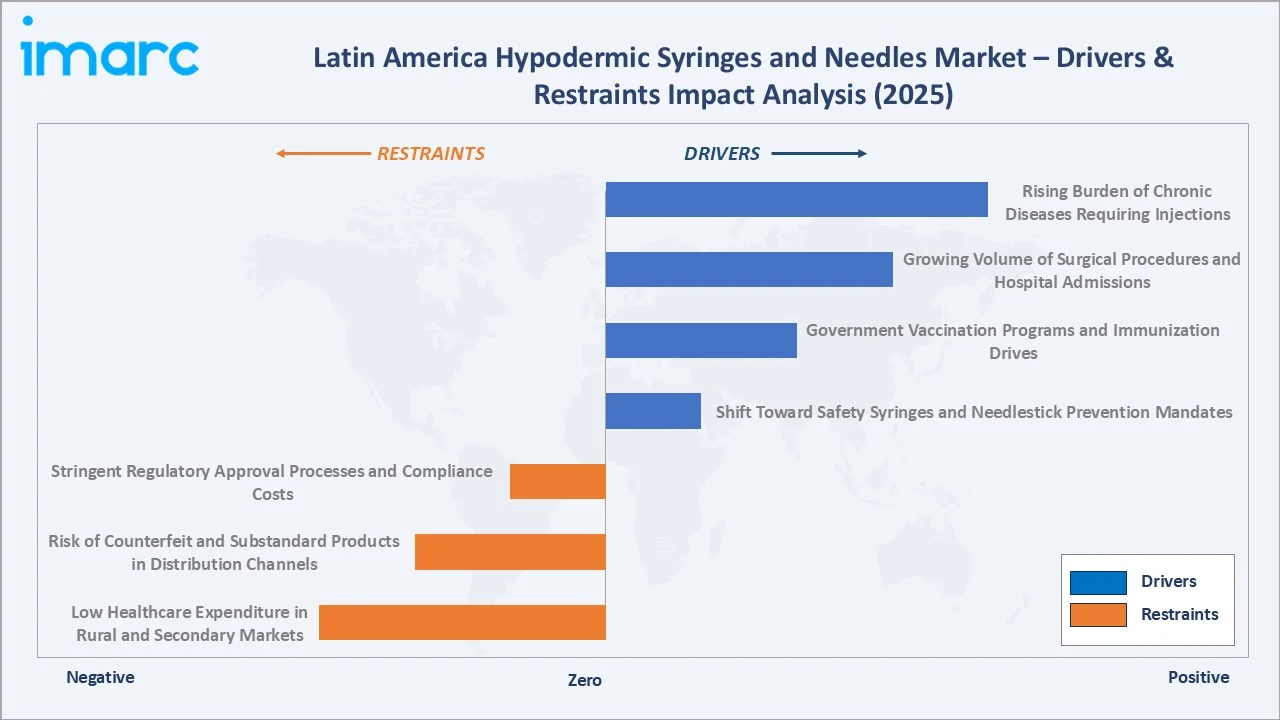

Market Drivers

- Rising Burden of Chronic Diseases Requiring Injections: The growing prevalence of diabetes, cancer, and cardiovascular diseases across Latin America is driving sustained demand for hypodermic syringes and needles. Insulin-dependent diabetics and oncology patients require frequent injections, creating recurring high-volume procurement needs across hospitals, clinics, and home-care settings.

- Government Vaccination Programs and Immunization Drives: Nationally funded immunization programs across Brazil, Mexico, and Colombia are among the world's largest by volume, requiring massive quantities of hypodermic syringes and needles. PAHO and WHO-supported vaccination drives, including COVID-19 booster programs and childhood immunization schedules, sustain high baseline procurement volumes.

- Growing Volume of Surgical Procedures and Hospital Admissions: Rising surgical procedure volumes, hospital admissions, and outpatient visits driven by aging populations and healthcare capacity expansion in Brazil and Mexico are increasing in-hospital syringe and needle demand. Greater access to healthcare services in secondary and tertiary cities further expands the addressable volume base.

- Shift Toward Safety Syringes and Needlestick Prevention Mandates: Regulatory mandates by national health authorities and PAHO guidelines requiring auto-disable and safety-engineered syringes for public health programs are driving product category upgrades. Safety syringe adoption commands higher average selling prices, expanding market revenue beyond unit volume growth alone.

Market Restraints

- Low Healthcare Expenditure in Rural and Secondary Markets: Significant disparities in healthcare access and expenditure between urban and rural areas across Latin America limit penetration of premium safety syringe products. Budget-constrained rural health facilities rely on lower-cost conventional devices, limiting average revenue per unit in secondary markets.

- Risk of Counterfeit and Substandard Products in Distribution Channels: The presence of counterfeit and substandard hypodermic syringes and needles in informal distribution channels undermines market integrity and creates pricing pressure on legitimate manufacturers. These products present patient safety risks and create compliance challenges for healthcare procurement managers.

- Stringent Regulatory Approval Processes and Compliance Costs: Registering medical devices with ANVISA in Brazil, COFEPRIS in Mexico, and equivalent authorities in other markets involves lengthy timelines and significant compliance investment. For smaller and mid-tier manufacturers, regulatory costs create barriers to market entry and limit portfolio expansion in the region.

Market Opportunities

- Biosimilar and Injectable Drug Expansion: Growth of biosimilar injectable drugs and biologic therapies in Latin America is creating new demand for compatible high-precision syringes and needles, offering premium product growth opportunities for compliant manufacturers.

- Home-Care Injection Market Development: Rising adoption of self-injection therapies for diabetes, rheumatoid arthritis, and multiple sclerosis is expanding the home-care syringe and needle market, representing a high-growth premium segment distinct from institutional procurement.

Market Challenges

- Single-Use Plastic Waste and Environmental Regulations: Growing regulatory and social pressure around single-use plastic medical device waste is driving demand for eco-friendly and recyclable syringe alternatives, requiring manufacturers to invest in sustainable product development.

- Price Sensitivity and Public Procurement Tendering Dynamics: Government and institutional procurement through competitive tender processes creates significant pricing pressure, compressing margins for medical device manufacturers competing for large national immunization program supply contracts.

Emerging Market Trends

1. Auto-Disable Syringe Adoption Driven by WHO and PAHO Mandates

Auto-disable syringes that automatically lock after single use are being mandated by the WHO and PAHO guidelines for all immunization programs. Latin American governments are progressively implementing these requirements, accelerating product category transitions from conventional to safety-engineered syringes across national vaccination infrastructure.

2. Smart Syringe Technology and Digital Drug Delivery Integration

Digitally integrated syringes with dose-tracking and connectivity capability are emerging for clinical trial applications and chronic therapy management. These smart devices support medication adherence monitoring and pharmacovigilance programs, representing an emerging premium segment within the broader hypodermic syringe market.

3. Biosimilar Injectable Therapies Expanding Precision Syringe Demand

The Latin American biosimilar market is expanding rapidly as patent expiries create opportunities for lower-cost biologic therapies. Growing biosimilar administration volumes require compatible precision syringes and ultra-fine needles, creating a distinct high-value product demand stream separate from conventional injection applications.

4. Eco-Friendly and Biodegradable Syringe Development

Environmental sustainability mandates and growing healthcare green procurement programs are driving the development of biodegradable and recyclable syringe alternatives. Manufacturers are investing in plant-based polymers and recyclable component designs to address single-use plastic waste concerns and align with regional environmental regulations.

Industry Value Chain Analysis

The hypodermic syringes and needles value chain integrates raw material procurement, manufacturing and assembly, sterilization and quality testing, packaging and regulatory compliance, distribution logistics, and end-use healthcare delivery. The commercial architecture has progressively consolidated toward safety-engineered product supply as the primary format for institutional and government procurement.

|

Stage |

Key Participants |

|

Raw Material & Component Procurement |

Sourcing of raw materials and components from global and regional suppliers to support manufacturing requirements |

|

Syringe & Needle Manufacturing & Assembly |

Core product manufacturing, component assembly, and integration of functional mechanisms by specialized medical device manufacturers |

|

Sterilization & Quality Testing |

Product sterilization, quality testing, dimensional validation, and sterility assurance in compliance with applicable medical device standards |

|

Packaging & Regulatory Compliance |

Product packaging, labeling, regulatory registration, and quality management system compliance for target markets |

|

Distribution & Logistics Networks |

Distribution through national and regional networks, including wholesalers, group purchasing organizations, and government tender fulfillment channels |

|

End-Use Delivery & Aftersales |

End-use delivery to healthcare facilities and patients, waste disposal management, and post-market surveillance activities |

The raw material procurement tier is most sensitive to polypropylene and stainless-steel price volatility, while the regulatory compliance stage creates the highest barriers to market entry for new manufacturers. The distribution tier is experiencing consolidation as group purchasing organizations gain influence over pricing and supplier selection across Latin American institutional markets.

Technology Landscape in the Latin America Hypodermic Syringes and Needles Industry

Retractable and Auto-Disable Safety Syringe Technology

Retractable and auto-disable safety syringe technology provides needle-stick injury protection by automatically retracting or locking the needle after injection. These devices are mandated by WHO for immunization programs and are increasingly adopted by hospital procurement across Brazil and Mexico, commanding premium pricing over conventional syringes.

Ultra-Fine and Thin-Wall Needle Technology

Ultra-fine needle technology with thin-wall precision engineering reduces patient pain during injection while maintaining precise fluid flow characteristics for insulin, biologic therapies, and vaccines. Nipro Corporation and Terumo Corporation are leading developers of thin-wall needle technology, addressing growing patient comfort requirements in diabetes management and self-injection therapy markets.

Pre-filled Syringe and Integrated Drug Delivery Technology

Pre-filled syringe technology integrates drug storage and delivery into a single-use device, eliminating preparation error risks and improving dose accuracy.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Hypodermic Syringes |

56.4% |

2025 |

|

End Use |

Hospitals |

39.7% |

2025 |

|

Region |

Brazil |

40.8% |

2025 |

By Product

Hypodermic Syringes lead at 56.4% in 2025, capturing the majority market share through universal application across drug delivery, vaccination, blood sampling, and insulin administration. Safety syringe mandates and auto-disable adoption are expanding the segment's average selling price and revenue share through the forecast period.

To access detailed market analysis, Request Sample

Hypodermic Needles at 43.6% represent a substantial complementary segment driven by demand for standalone needles for IV-line administration, blood collection, and veterinary applications. The segment benefits from consistent institutional procurement volumes and growing safety needle adoption in line with hospital needlestick prevention programs.

By End Use

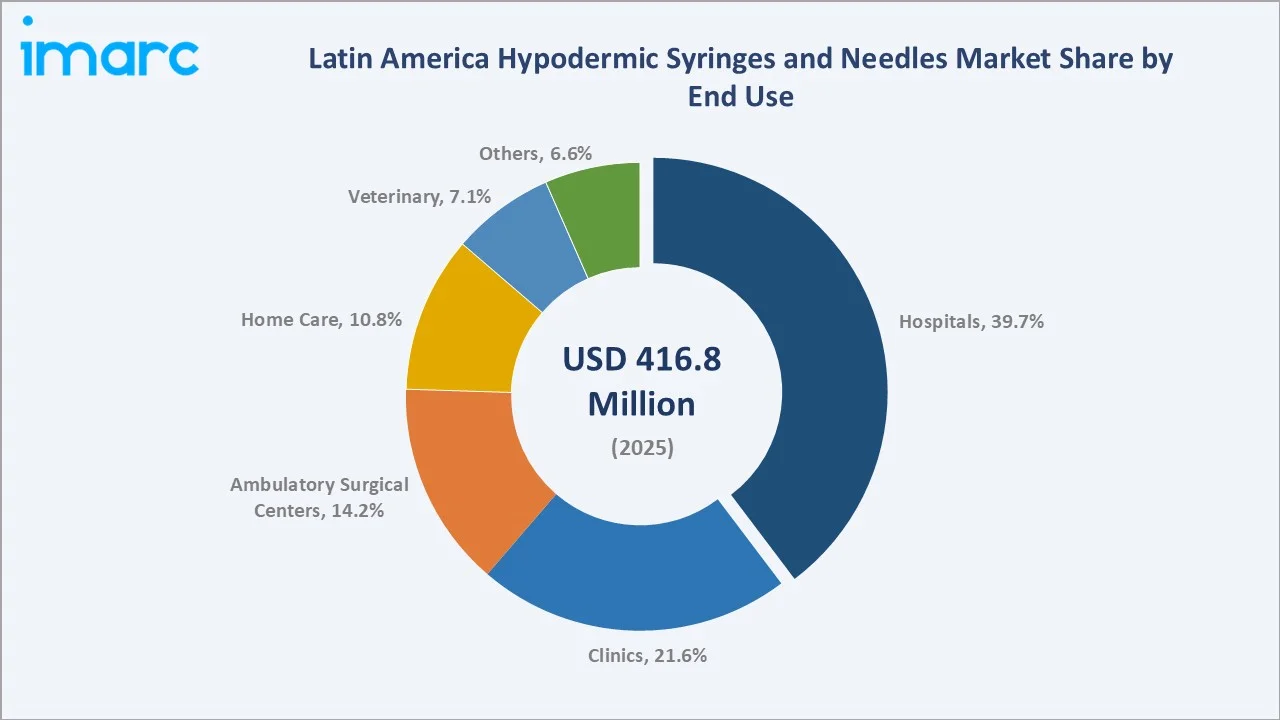

Hospitals lead at 39.7% in 2025, driven by the highest per-facility volume of syringe and needle consumption for in-patient medication, surgical procedures, blood sampling, and vaccination programs. Government hospital procurement programs and universal health coverage expansion in Brazil and Mexico sustain strong institutional demand.

Clinics at 21.6% represent the second-largest end-use segment through primary care and specialist clinic growth. Ambulatory Surgical Centers at 14.2% are growing above market average as outpatient surgical volume rises. Home Care at 10.8% is the fastest-growing segment driven by self-injection therapy expansion. Veterinary at 7.1% and Others at 6.6% complete the end-use distribution.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Brazil |

40.8% |

Leading healthcare market in the region; strong public procurement infrastructure; established regulatory framework supporting domestic and imported product supply |

|

Mexico |

19.5% |

Growing hospital and clinic network; national health system procurement supporting institutional demand; regulatory compliance framework for medical device imports |

|

Argentina |

10.2% |

Expanding healthcare access and rising disease management requirements supporting procurement growth; growing hospital and outpatient network |

|

Colombia |

9.3% |

Health coverage expansion driving institutional procurement growth; increasing outpatient care volumes and public health program requirements |

|

Chile |

7.4% |

Higher per-capita healthcare investment supporting advanced product adoption; mature hospital procurement practices and strong regulatory compliance standards |

|

Peru |

6.1% |

Expanding public health investment and primary care network development supporting increased procurement volumes across healthcare settings |

|

Others |

6.7% |

Diverse smaller markets at varying stages of healthcare infrastructure development; growth supported by public health funding and institutional capacity building |

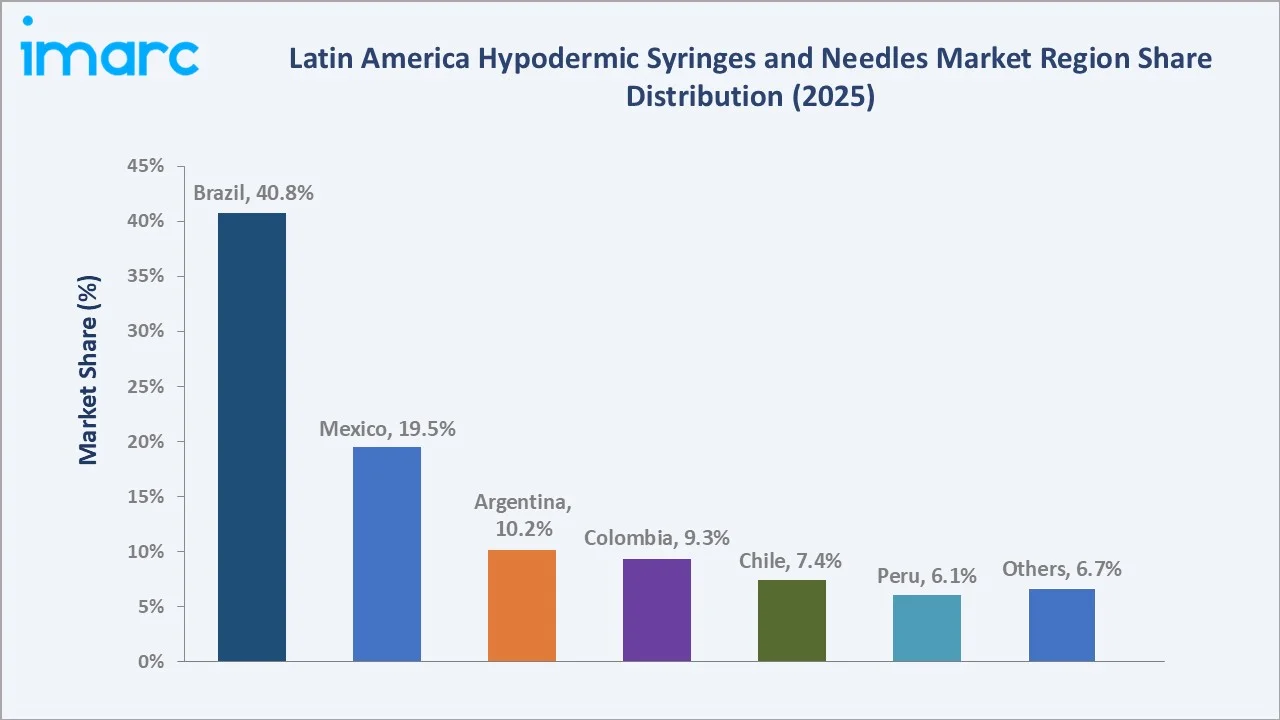

Brazil at 40.8% leads through its national immunization infrastructure and domestic manufacturing. Mexico at 19.5% reflects large-scale public health system procurement. Chile at 7.4% demonstrates the highest premium product penetration, with advanced safety device adoption across its developed hospital network.

Argentina at 10.2% and Colombia at 9.3% represent growing sub-markets supported by expanding universal health coverage. Peru at 6.1% and Others at 6.7% are early stage but growing markets, driven by public health investment and primary care infrastructure expansion across smaller Latin American nations.

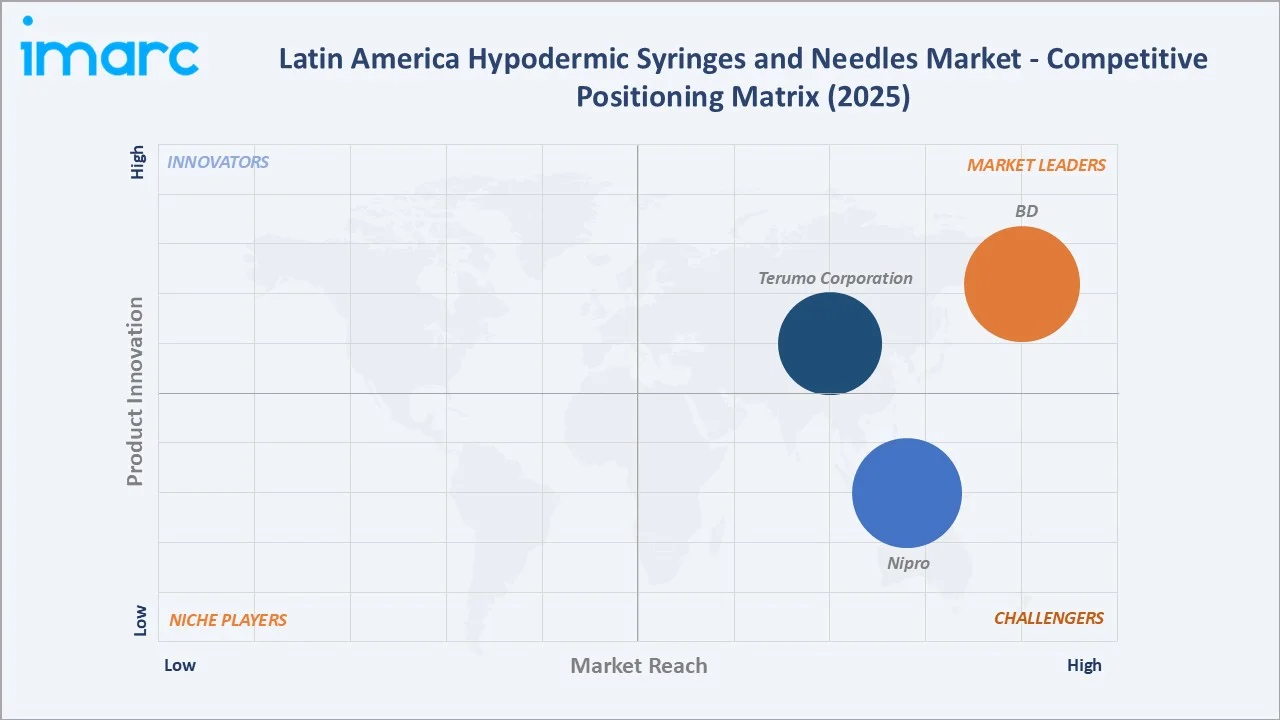

Competitive Landscape

The Latin America hypodermic syringes and needles market is moderately concentrated, with global medical device leaders dominating institutional and government procurement through established regulatory compliance, broad product portfolios, and regional distribution infrastructure across Brazil, Mexico, and Argentina.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

BD |

BD SafetyGlide Syringes and Needles, BD Eclipse Syringes and Needles, BD Blunt Fill/Filter Needles, BD PrecisionGlide Needles, BD Syringes, BD Syringe/Needle Combination, BD Allergy Syringes, BD Tuberculin Syringes |

Market Leader |

Dominant Latin American market position with local manufacturing in Brazil; deep integration with national immunization programs and hospital procurement systems |

|

Terumo Corporation |

Terumo Hypodermic Needle, Terumo Hypodermic Syringes with Needle |

Market Leader |

Strong safety needle and syringe portfolio; established regional supply agreements with Mexican and Colombian hospital networks and vaccination programs |

|

Nipro |

Standard Hypodermic Needles, SafeTouch hypodermic needles |

Strong Challenger |

Cost-competitive high-volume syringe and needle supply with strong distribution networks in Brazil and Mexico; leading insulin syringe supplier |

Key players include BD, Terumo Corporation, and Nipro among others.

Key Company Profiles

BD

BD is a United States-based global medical technology company and the dominant player in the Latin America hypodermic syringes and needles market, with local manufacturing in Brazil and deep integration into national immunization programs and institutional hospital supply across the region.

- Key Products: BD SafetyGlide Syringes and Needles, BD Eclipse Syringes and Needles, BD Blunt Fill/Filter Needles, BD PrecisionGlide Needles, BD Syringes, BD Syringe/Needle Combination, BD Allergy Syringes, BD Tuberculin Syringes

- Strategic Focus: Expanding safety-engineered syringe and needle portfolio across Latin America while deepening government immunization program supply relationships and growing pre-filled syringe manufacturing capacity for biologic drug delivery.

Terumo Corporation

Terumo Corporation is a Japan-based global medical device company with a significant presence in the Latin America hypodermic syringes and needles market, offering a comprehensive range of precision syringes, ultra-fine needles, and safety-engineered injection devices to hospitals, clinics, and vaccination programs.

- Key Products: Terumo Hypodermic Needle, Terumo Hypodermic Syringes with Needle

- Strategic Focus: Advancing ultra-fine and thin-wall needle technology for patient comfort in chronic disease management, expanding safety syringe adoption in Latin American hospital procurement, and growing biosimilar-compatible syringe product lines.

Market Concentration Analysis

The Latin America hypodermic syringes and needles market is moderately concentrated, the top 4-5 key players collectively accounting for an estimated 55–65% of regional market revenue.

Market concentration is gradually decreasing as regional distributors gain procurement influence and local manufacturers in Brazil expand capacity to serve government tender requirements. The safety syringe and pre-filled syringe segments attract specialized competitors, further diversifying the competitive landscape beyond conventional syringe supply.

Investment & Growth Opportunities

Highest Growth Segments

Home Care self-injection segment (~3.5% CAGR), Ambulatory Surgical Centers (~3.2% CAGR), Hypodermic Syringes through safety device mandates (~3.0% CAGR), and pre-filled syringe systems for biosimilar administration represent the highest-growth investment vectors through 2034. Brazil and Mexico government procurement programs sustain the highest absolute volume growth.

Emerging Investment Opportunities

Latin America's expanding biosimilar injectable market represents the highest per-unit value emerging opportunity for precision syringe and needle investment. Pre-filled syringe systems for biologic drug delivery command 3–5x the per-unit revenue of conventional hypodermic syringes, with biosimilar adoption growth creating structurally expanding demand through 2034.

Investment Themes

- Local manufacturing establishment in Brazil: Leveraging Brazil's domestic manufacturing incentives and proximity to national immunization program procurement to reduce import costs and achieve competitive pricing advantages in government tender processes.

- Safety syringe portfolio expansion: Investing in auto-disable, retractable, and safety-engineered syringe product lines to align with WHO and PAHO mandates, capturing premium pricing growth above conventional device procurement.

- Home-care and self-injection market development: Developing patient-friendly ultra-fine needle and insulin syringe products for the rapidly growing self-injection therapy market driven by diabetes, rheumatoid arthritis, and biologic treatment expansion.

Future Market Outlook (2026-2034)

The Latin America hypodermic syringes and needles market is projected to grow from USD 416.8 Million in 2025 to USD 532.9 Million by 2034, delivering a 2.77% CAGR. Brazil's vaccination program scale, Mexico's hospital network expansion, and the region-wide shift to safety-engineered devices collectively define the structural demand trajectory through 2034.

Three structural forces define market growth through 2034: regulatory-driven product upgrades from conventional to safety-engineered syringes; chronic disease burden expansion creating recurring injection demand; and biosimilar injectable market growth creating a distinct high-value precision syringe demand stream above baseline volume growth.

The market's anchor value of approximately USD 474.5 Million in 2030 represents the inflection toward premium safety and pre-filled syringe architecture mainstream adoption, when safety-engineered device mandates will have achieved broad national compliance across major Latin American markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including hospital procurement managers, medical device distributor leads, regulatory affairs specialists, and national health ministry procurement officials across Brazil, Mexico, Argentina, and Colombia.

Secondary Research

Secondary research encompassed ANVISA and COFEPRIS registration databases, PAHO vaccination program reports, national health expenditure data, company annual reports and investor presentations, WHO medical device safety guidelines, and IMARC Group market databases. Over 50 secondary sources were reviewed and cross-validated.

Forecasting Models

Market revenue forecasts developed using a bottom-up healthcare volume model: (i) country-level vaccination program syringe volume requirements; (ii) chronic disease patient population requiring injection therapy by condition; (iii) surgical procedure volume by country and procedure type; (iv) average selling price by product type with safety device premium adjustment.

Latin America Hypodermic Syringes and Needles Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| End Uses Covered | Hospitals, Clinics, Ambulatory Surgical Centers, Veterinary, Home Care, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | BD, Terumo Corporation, Nipro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America hypodermic syringes and needles market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America hypodermic syringes and needles market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America hypodermic syringes and needles industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Hypodermic Syringes and Needles Market Report

The market reached USD 416.8 Million in 2025, with Brazil leading at 40.8% regional share, Hypodermic Syringes dominating at 56.4%, and Hospitals representing 39.7% of end-use demand.

The market grows at 2.77% CAGR during 2026-2034, reaching USD 532.9 Million by 2034, driven by chronic disease management, vaccination programs, safety syringe mandates, and biosimilar injectables growth.

Hypodermic Syringes lead at 56.4% in 2025, capturing the majority share through universal application across drug delivery, vaccination, blood sampling, and insulin administration in all healthcare settings.

Hospitals lead at 39.7% through the highest per-facility consumption volume for inpatient medication, surgical procedures, and vaccination administration. Home Care at 10.8% is the fastest-growing segment.

Brazil leads at 40.8% through its national vaccination infrastructure, large chronic disease patient base, ANVISA-regulated domestic manufacturing, and large-scale government syringe procurement programs.

Leading companies include BD, Terumo Corporation, and Nipro among others.

The market is projected to reach approximately USD 474.5 Million by 2030, driven by safety syringe mandate compliance, biosimilar injectable volume growth, and home-care self-injection therapy expansion.

Key opportunities include local manufacturing in Brazil, safety syringe portfolio development aligned to WHO mandates, pre-filled syringe systems for biosimilar drug delivery, and home-care self-injection product development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)