Latin America Solar Panel Market Size, Share, Trends and Forecast by Type, End Use, and Country, 2026-2034

Latin America Solar Panel Market Size, Share, Trends & Forecast (2026-2034)

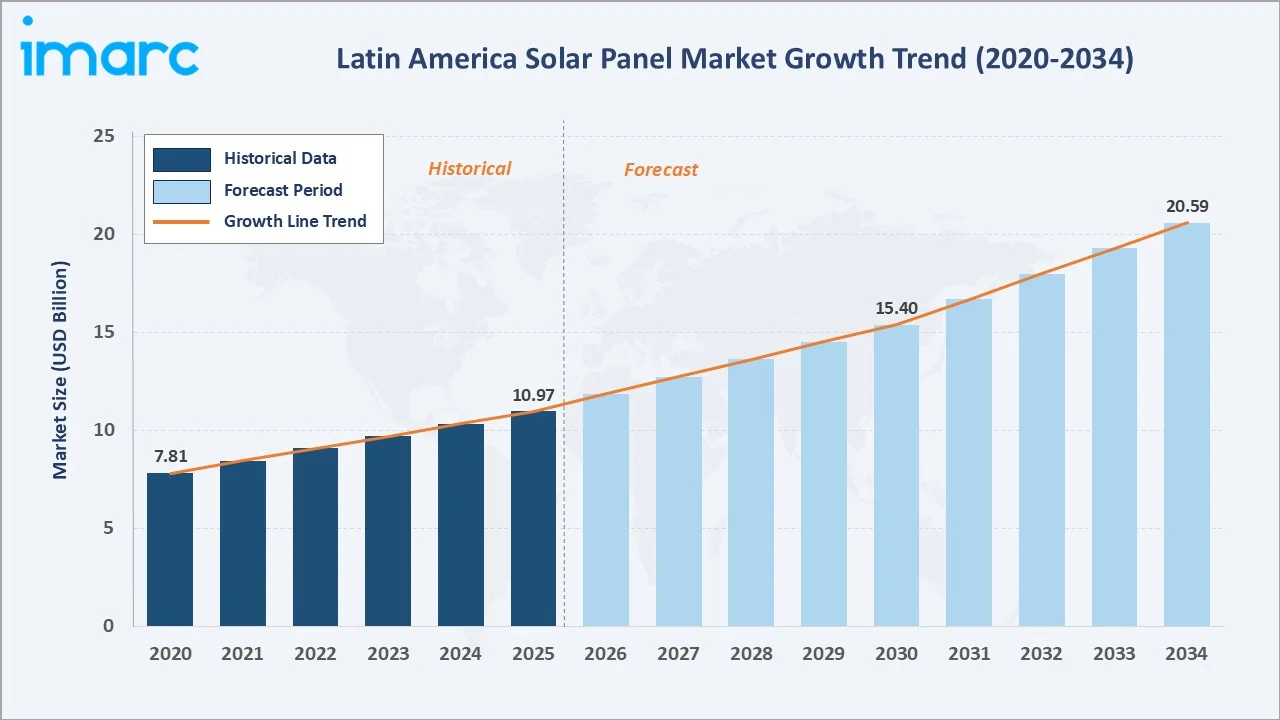

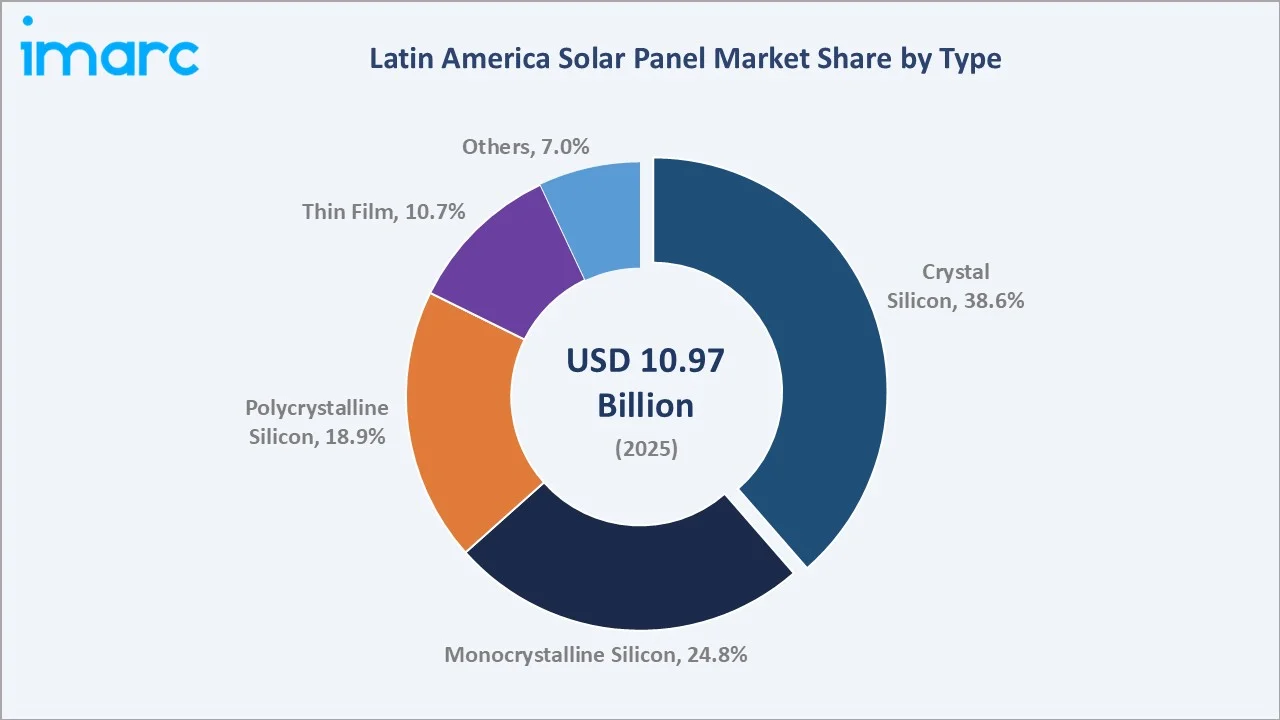

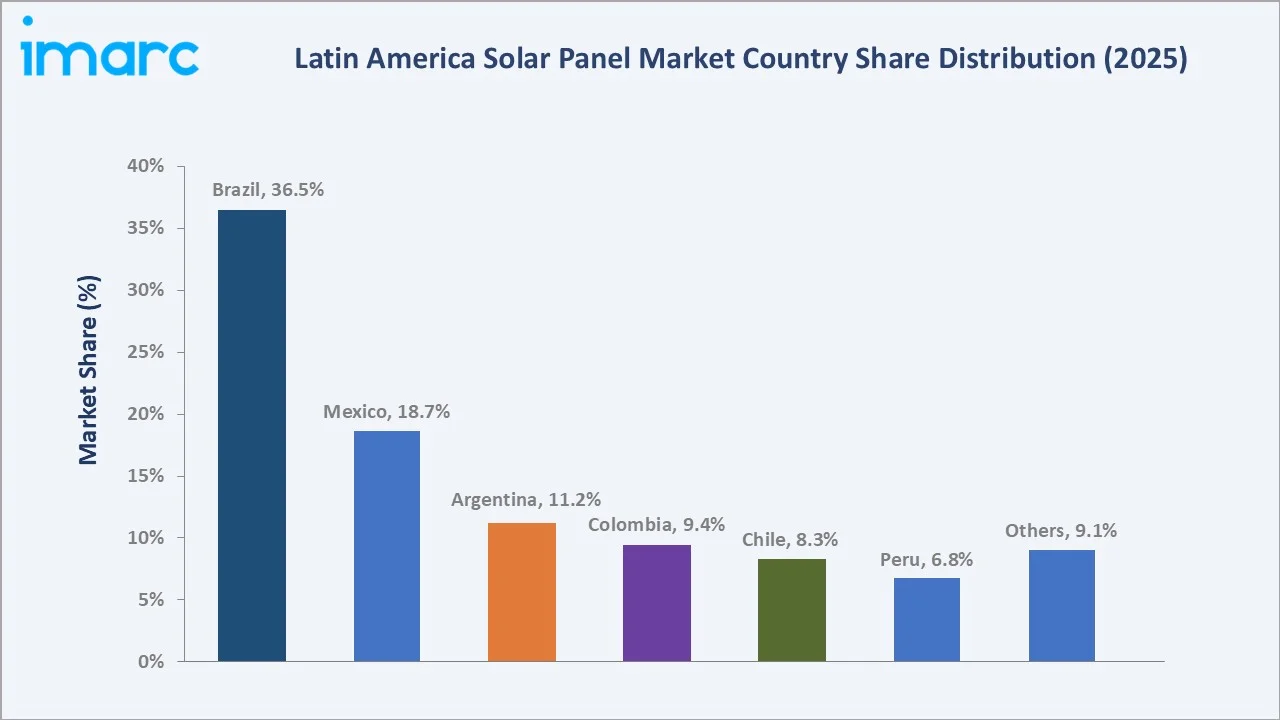

The Latin America solar panel market reached USD 10.97 Billion in 2025 and is projected to reach USD 20.59 Billion by 2034, growing at a CAGR of 7.03% during 2026-2034. Latin America is targeting to achieve 70% share of electricity generation from renewable sources by 2030, accelerating investments in clean energy infrastructure and energy transition initiatives. This is driving the Latin America solar panel market by increasing utility-scale solar projects, renewable capacity additions, and demand for photovoltaic installations across the region. Crystal silicon dominates at 38.6%. Commercial end-use leads at 41.9%. Brazil commands 36.5% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.97 Billion |

|

Forecast Market Size (2034) |

USD 20.59 Billion |

|

CAGR (2026-2034) |

7.03% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Crystal Silicon (38.6%, 2025) |

|

Dominant End-Use |

Commercial (41.9%, 2025) |

|

Leading Country |

Brazil (36.5%, 2025) |

The market expanded from USD 7.81 Billion in 2020 to USD 10.97 Billion in 2025, anchored at USD 15.40 Billion in 2030, and forecast to reach USD 20.59 Billion by 2034. COVID-19 temporarily disrupted project supply chains before the post-pandemic acceleration from 2022, driven by Brazil's residential solar boom, Chile's Atacama utility-scale expansion, and Mexico's C&I self-supply growth despite reduced government renewable support.

To get more information on this market, Request Sample

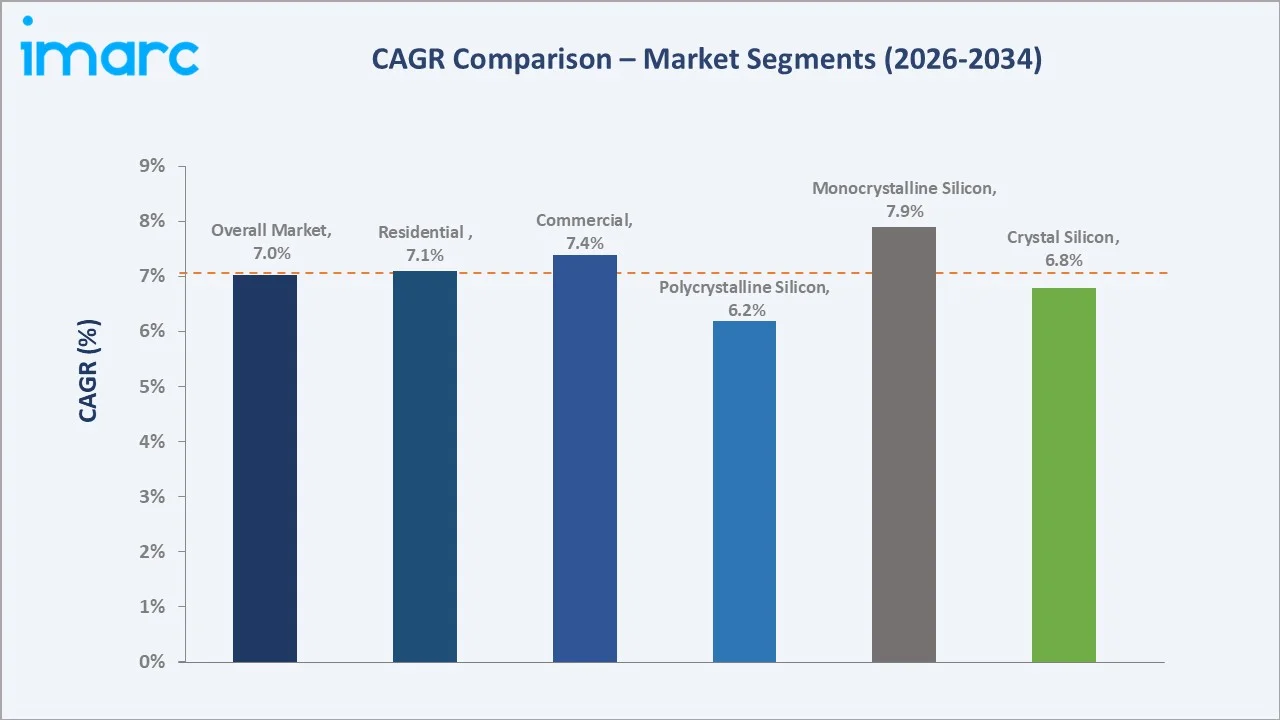

Monocrystalline silicon grows fastest at ~7.9% CAGR as technology modules achieve efficiency levels and cost points that are displacing polycrystalline silicon in virtually all new project specifications. Commercial end-use grows fastest at ~7.4% CAGR driven by Latin American commercial real estate, retail chains, hotel and hospitality, and agri-industry adopting on-site solar for electricity cost reduction, carbon neutrality targets, and energy security.

Executive Summary

The Latin America solar panel market reached USD 10.97 Billion in 2025, positioning the region as one of the world's largest solar energy markets by new installations. Latin America's solar energy transformation is among the most commercially compelling in the world, creating solar payback periods of 2-5 years that represent the strongest solar investment economics globally for C&I customers. The market is projected to reach USD 20.59 Billion by 2034.

Crystal silicon at 38.6% leads as the combined category encompassing Brazil's dominant residential and small commercial rooftop solar segment, where standard crystalline silicon modules are the default product. Commercial end-use at 41.9% dominates as corporate energy sustainability commitments, high industrial electricity tariffs, and favorable solar PPA structures drive commercial and industrial solar adoption across the region's manufacturing, retail, agriculture, and services sectors. Brazil, at 36.5%, is the market's undisputed leader, with installed solar capacity reached 50 GW in 2024 and annual additions placing it among one of the world's top annual solar installation markets.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Crystal Silicon - 38.6% share (2025) |

|

Dominant End-Use |

Commercial - 41.9% market share (2025) |

|

Leading Country |

Brazil - 36.5% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Crystal Silicon at 38.6% reflecting Brazil's mass-market residential solar market where standard crystalline PERC technology modules at USD 0.18-0.25/W retail pricing dominate by volume: Crystal Silicon's market leadership encompasses the full range of crystalline silicon technology, both standard PERC (passivated emitter and rear cell) and the transitioning n-type TOPCon (tunnel oxide passivated contact) technology, as the dominant technology for Brazil's installed rooftop solar systems.

- Commercial at 41.9% reflecting Latin American corporate electricity cost driver and corporate ESG commitment, creating the region's most commercially active solar end-use segment: Commercial solar's 41.9% dominance reflects the convergence of Latin America's highest industrial and commercial electricity tariffs globally with corporate ESG commitments and favorable C&I solar financing.

- Brazil at 36.5%: Brazil dominates the market due to its large-scale solar capacity additions, supportive renewable energy policies, and rising investments in utility-scale and distributed solar projects. The country’s abundant solar resources and growing electricity demand are further accelerating solar panel adoption.

Latin America Solar Panel Market Overview

Latin America's solar panel market encompasses the production, import, distribution, installation, and servicing of photovoltaic (PV) solar panels across utility-scale power plants, commercial and industrial (C&I) rooftop and ground-mounted systems, and residential rooftop microgeneration across national markets from Mexico to Argentina. The market includes crystalline silicon panels, thin-film panels, bifacial modules, and high-concentration photovoltaics.

The ecosystem integrates polysilicon and wafer manufacturers, solar cell and module manufacturers, import logistics and in-country distribution networks, EPC (Engineering, Procurement, Construction) contractors for project execution, inverter manufacturers, mounting system suppliers, grid connection infrastructure, national energy regulators, and end users across commercial, residential, and industrial segments.

Market Dynamics

To evaluate market opportunities, Request Sample

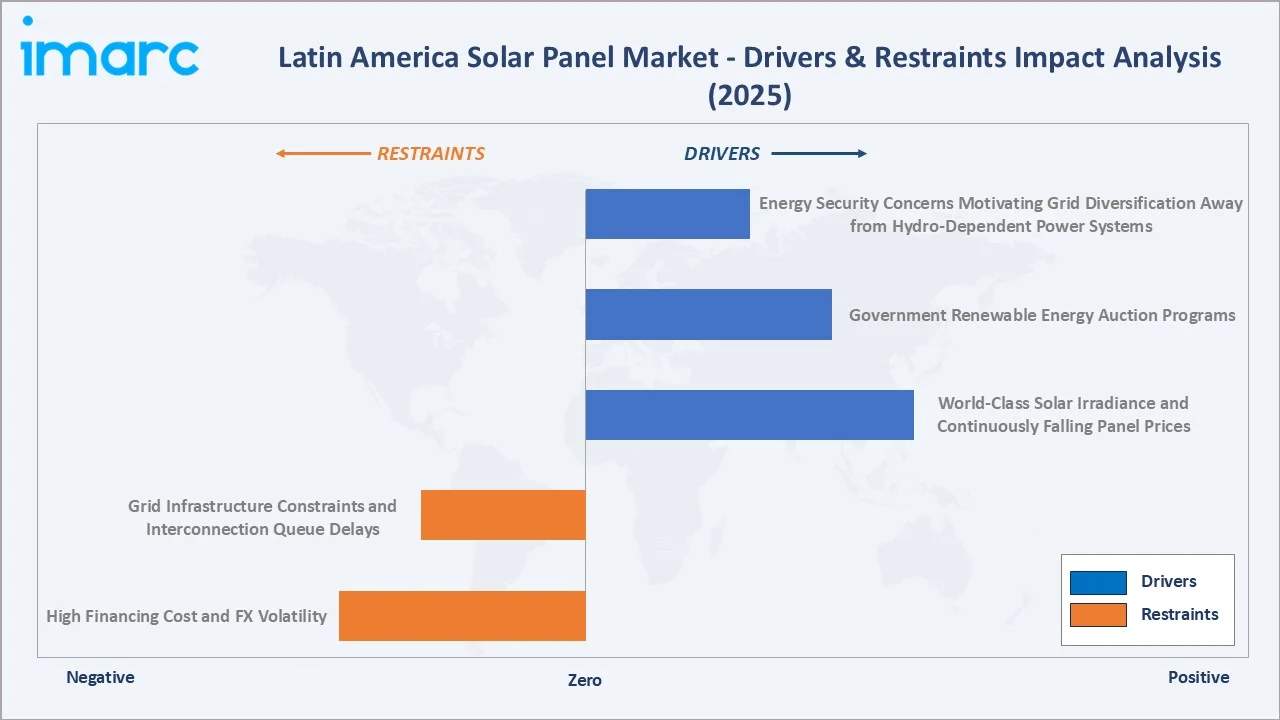

Market Drivers

- World-Class Solar Irradiance and Continuously Falling Panel Prices: Latin America and the Caribbean generated 65% of their electricity from clean energy sources in 2025, surpassing the global average, with hydropower (40%) remaining the primary source while solar and wind (19%) recorded the fastest growth, more than doubling over the past five years and expanding faster than regional electricity demand. With the region’s high solar resource availability, combined with declining solar module costs, solar deployment is accelerating and increasing the adoption of solar panels across residential, commercial, and utility-scale projects.

- Government Renewable Energy Auction Programs: Latin American government renewable energy auction programs create the revenue certainty that enables international project finance for utility-scale solar.

- Energy Security Concerns Motivating Grid Diversification Away from Hydro-Dependent Power Systems: Latin America's electricity systems are historically hydro-dominant. Solar generation's climate-resilience and complementary seasonal profile to hydro make solar-plus-hydro grid combinations more resilient than pure-hydro systems, creating national energy security policy motivation for solar expansion beyond pure economics.

.webp)

Market Restraints

- High Financing Cost and FX Volatility: Latin American project finance costs are among the highest globally due to sovereign credit risk premiums, currency devaluation risk, and limited domestic capital market depth for long-term renewable energy project bonds. Solar projects financed in local currency face tariff mismatch risk when module procurement is USD-denominated, but PPA revenue is local currency.

- Grid Infrastructure Constraints and Interconnection Queue Delays: Transmission grid infrastructure inadequacy is creating solar deployment bottlenecks in multiple LATAM markets. Limited grid capacity and delays in transmission expansion, particularly in high renewable-growth regions, are restricting large-scale solar deployment despite rising investments.

Market Opportunities

- Green Hydrogen Production Creating Large-Scale Solar Demand: Green hydrogen is emerging as Latin America's most commercially exciting new solar application because the region's exceptional solar resource creates hydrogen production costs below European and North American equivalents, creating potential for LATAM green hydrogen export competitiveness. Each 1 GW of electrolysis capacity requires approximately 1.5-2.5 GW of dedicated solar PV, creating a solar module demand multiplier from green hydrogen.

- BESS Integration with Solar Creating Enhanced Value Proposition: Battery Energy Storage Systems (BESS) integration with solar improves energy storage, grid stability, and the reliability of intermittent solar generation. The combination enables better peak demand management, higher renewable energy utilization, and supports the expansion of utility-scale and distributed solar projects across the region.

Market Challenges

- Chinese Module Import Dependence Creating Supply Chain Vulnerability and Domestic Industry Development Challenges: Latin America's dependence on Chinese solar module imports creates supply chain concentration risk. COVID-19 supply chain disruptions demonstrated this vulnerability when Brazilian solar installer order books were disrupted by module availability uncertainty.

- Skilled Workforce Shortage for Large-Scale Solar Installation and O&M Driving Project Execution Delays: Latin America's solar installation workforce development has not kept pace with industry growth, creating systemic performance risk from poor-quality installation at scale. Training institutions are scaling solar installation certification programs, but the 7.03% annual market growth creates training program enrollment demand that consistently outpaces certificate issuance capacity.

Emerging Market Trends

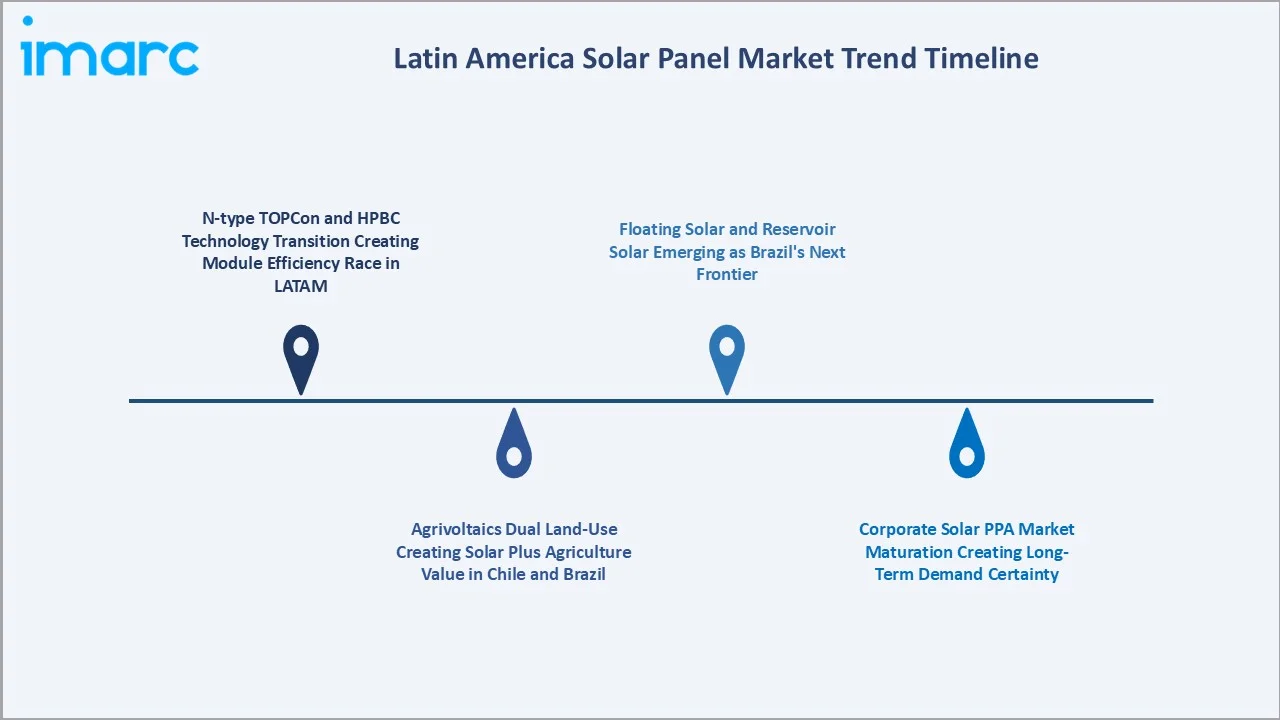

1. N-type TOPCon and HPBC Technology Transition Creating Module Efficiency Race in LATAM

The transition toward N-type TOPCon and HPBC technologies is emerging as developers increasingly prioritize high-efficiency modules to maximize energy output and project returns. In August 2025, LONGi launched HPBC 2.0 photovoltaic modules in Brazil, designed to deliver superior results in any type of system: from residential rooftops to large ground-mounted solar plants. These advanced technologies offer improved conversion efficiency, lower degradation rates, and better performance under high-temperature conditions, making them well-suited to Latin America’s strong solar irradiation environment. Their adoption is intensifying competition among manufacturers to deliver higher-performance solar modules.

2. Agrivoltaics Dual Land-Use Creating Solar Plus Agriculture Value in Chile and Brazil

Agrivoltaics dual land-use systems are emerging, particularly in Chile and Brazil, by combining solar power generation with agricultural activities on the same land. This approach improves land-use efficiency, supports crop cultivation through partial shading and water conservation benefits, and creates additional revenue streams for farmers. The model is gaining attention as countries seek to expand solar capacity without increasing land-use conflicts.

3. Corporate Solar PPA Market Maturation Creating Long-Term Demand Certainty

Latin America's corporate solar PPA (Power Purchase Agreement) market has matured from early-stage bilateral negotiations into standardized commercial structures that multinational and domestic corporations deploy as systematic energy procurement instruments. Corporate PPAs provide stable revenue visibility for solar developers, reduce project financing risks, and create long-term demand certainty, supporting continued solar capacity expansion across the region.

4. Floating Solar and Reservoir Solar Emerging as Brazil's Next Frontier

Floating solar and reservoir-based solar projects are emerging, particularly in Brazil, by utilizing water bodies and hydropower reservoirs for solar installations. This approach helps optimize land use, reduces water evaporation, and enables hybrid hydro-solar generation systems. The trend is gaining traction as Brazil seeks to expand renewable capacity while leveraging its extensive reservoir infrastructure.

Industry Value Chain Analysis

Latin America's solar panel value chain integrates polysilicon and wafer production, solar cell and module manufacturing, import logistics and in-country distribution, EPC and project development, grid connection and commissioning, and ongoing O&M and asset management. Brazil's upstream value chain is the weakest segment.

|

Stage |

Key Participants |

|

Polysilicon & Wafer Production |

Raw material suppliers and wafer manufacturers supplying polysilicon feedstock, wafers, and ingots. |

|

Cell & Module Manufacture & Testing |

Solar cell and module manufacturers involved in cell processing, module assembly, efficiency testing, quality inspection, and certification activities. |

|

Import, Logistics & Distribution |

Importers, shipping providers, distributors, and warehousing companies managing module transportation, customs clearance, and distribution. |

|

EPC & Project Development |

EPC contractors, project developers, and engineering firms responsible for utility-scale, commercial, and distributed solar project planning, procurement, and execution. |

|

Grid Connection, Installation & Commissioning |

Inverter suppliers, electrical contractors, installers, and grid integration service providers. |

|

O&M, Asset Management & Recycling |

Operations and maintenance providers, asset managers, monitoring companies, and recycling firms. |

The O&M, asset management, and recycling tier is growing in commercial importance as Latin America's installed solar base matures. Solar module end-of-life management creates an emerging circular economy opportunity that Brazil's framework is progressively addressing through extended producer responsibility requirements on module importers.

Technology Landscape in the Latin America Solar Panel Industry

Bifacial Module Technology

Bifacial module technology enables solar panels to capture sunlight from both front and rear surfaces, improving overall energy yield and project efficiency. The technology is gaining traction in utility-scale projects across high-irradiance regions due to its ability to enhance power generation and lower the levelized cost of electricity (LCOE). Its adoption is further supported by Latin America’s favorable solar conditions and expanding large-scale solar installations. São Gonçalo is the largest solar facility currently in operation in Latin America and the first Enel plant in Brazil to use bifacial solar modules, which capture solar energy from both sides.

High-Concentration Photovoltaics and Perovskite-Silicon Tandem Development

High-concentration photovoltaics (HCPV) and perovskite-silicon tandem developments are advancing module efficiency and improving power output under high solar irradiation conditions. These technologies support higher energy generation with reduced land requirements, making them attractive for utility-scale projects. Their development is strengthening the industry’s focus on next-generation, high-efficiency solar solutions across the region.

Floating Solar and Agrivoltaic Mounting Systems

Floating solar and agrivoltaic mounting systems are expanding solar deployment beyond conventional land-based installations. Floating solar systems utilize reservoirs and water bodies to optimize space and support hybrid renewable projects, while agrivoltaic systems enable simultaneous agricultural activity and solar power generation. These technologies are improving land-use efficiency and supporting sustainable solar expansion across the region.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Crystal Silicon |

38.6% |

2025 |

|

End Use |

Commercial |

41.9% |

2025 |

|

Country |

Brazil |

36.5% |

2025 |

By Type

Crystal silicon leads at 38.6% market share (2025). Crystal silicon in the Latin American context primarily encompasses the standard PERC monocrystalline modules that constitute the backbone of Brazil's residential and small commercial rooftop solar market. These standard-format modules are the most widely stocked in Brazil, Mexico, and Colombia's solar distribution networks, and the most installed by Brazil's solar installer companies.

To access detailed market analysis, Request Sample

Monocrystalline silicon at 24.8% grows fastest at ~7.9% CAGR through the n-type TOPCon technology adoption for utility-scale and premium C&I applications. Polycrystalline silicon at 18.9% is declining in relative share. Thin film at 10.7% serves first solar's niche in high-temperature LATAM utility applications. Others at 7.0% encompasses CIGS thin film, OPV (organic), and emerging perovskite-silicon research modules.

By End-Use

Commercial leads at 41.9% market share (2025). Commercial solar encompasses office buildings, retail centers, hotels, restaurants, supermarkets, schools, hospitals, and commercial warehouse solar installations from 50 kW to 10 MW scale. Brazil's commercial solar market has been driven by shopping mall owners, supermarket chains, and corporate office buildings seeking green building certification and electricity cost reduction.

Residential at 33.6% reflects Brazil's extraordinary residential solar adoption. Industrial at 24.5% covers manufacturing, mining, agribusiness, and logistics solar installations from 500 kW to 100 MW scale across Brazil's industrial heartland and Chile's mining regions.

Regional Market Insights

|

Country |

Share (2025) |

Key Solar Panel Market Drivers & Characteristics |

|

Brazil |

36.5% |

Supported by strong utility-scale developments, expanding distributed generation, and favorable renewable energy investments. |

|

Mexico |

18.7% |

Driven by abundant solar resources, growing industrial power demand, and increasing adoption of commercial and utility-scale solar projects. |

|

Argentina |

11.2% |

Supported by high solar irradiation potential, renewable energy expansion initiatives, and rising investments in clean energy infrastructure. |

|

Colombia |

9.4% |

Developing steadily with increasing renewable energy deployment, supportive policy measures, and improving investment activity. |

|

Chile |

8.3% |

Benefits from strong solar resources and growing solar installations, supported by the country’s focus on renewable energy transition. |

|

Peru |

6.8% |

Expanding through increasing renewable capacity additions and the utilization of favorable solar conditions in various regions. |

|

Others |

9.1% |

The others are gradually increasing renewable energy investments and solar deployment activities across the region. |

Brazil's 36.5% market leadership is built on the combination of distributed generation policy, rising electricity tariffs creating compelling solar economics, and financing accessibility. Brazil's annual solar additions are projected to grow as remaining urban rooftop market penetration expands, and greenfield utility-scale auctions continue delivering 2-3 GW annually.

Mexico's 18.7% is recovering from political uncertainty, with C&I self-supply solar sustaining growth independently of government auctions. Argentina's 11.2% combines world-class solar resource with macroeconomic instability. Colombia's 9.4% reflects accelerating corporate and C&I adoption supported by net metering and auction programs. Chile's 8.3% is driven by utility-scale solar and mining sector demand. Peru's 6.8% reflects growing rural electrification and mining sector solar self-supply. Others at 9.1% encompasses Ecuador, Uruguay, Bolivia, Central America, and the Caribbean, growing from smaller bases.

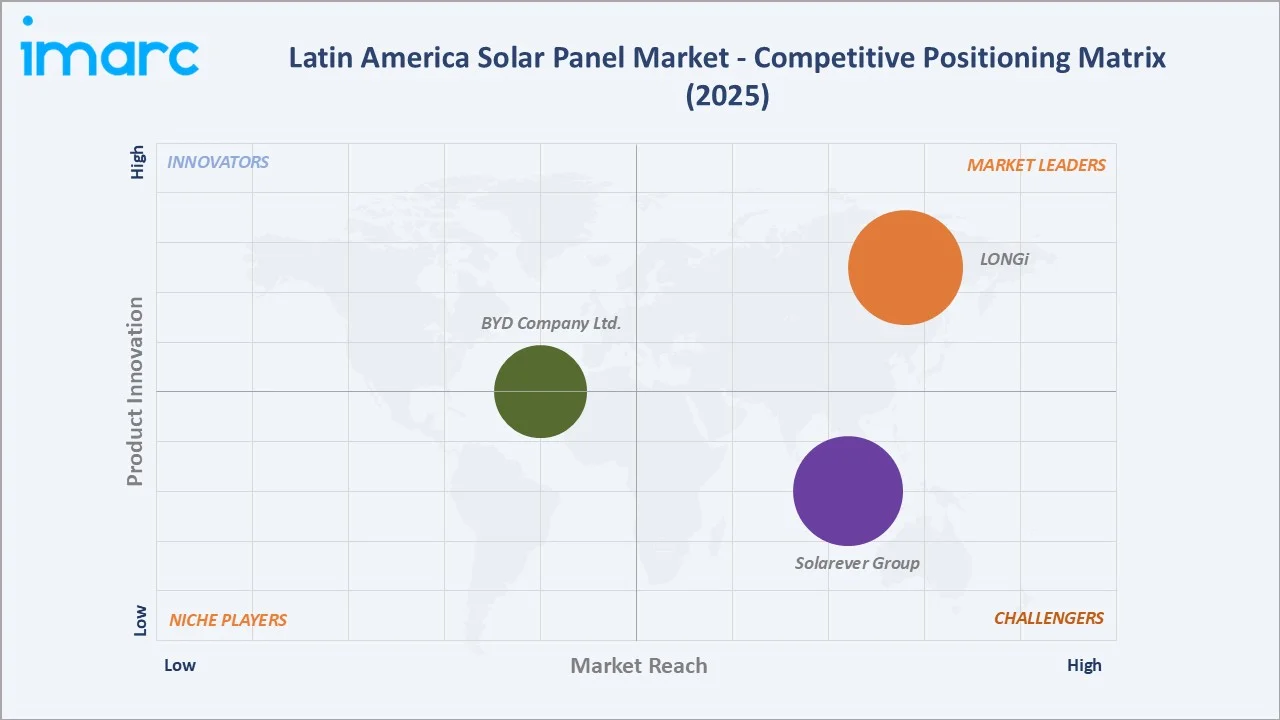

Competitive Landscape

The Latin America solar panel competitive landscape is structurally dominated by Chinese module manufacturers. This Chinese manufacturer's dominance reflects their structural cost advantages that enable module pricing at USD 0.12-0.16/W - below the production cost threshold for most non-Chinese manufacturers.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

LONGi |

Hi-MO X10, Hi-MO 9, Hi-MO 7, Hi-MO X6 Max |

Market Leader |

LONGi supplies its reliable, high-quality, high-performance solar modules to help propel the world towards a low-carbon future. |

|

Solarever Group |

640W/645W/650 BC ANTIDUST, Solarever 110W, Solarever 410W All Black, Solarever 555W PERC, Solarever 615W |

Challenger |

Solarever has the highest ratings and certifications in the manufacturing of solar panels. |

|

BYD Company Ltd. |

HALO, AURO N series, AURO P series |

Established Player |

As the pioneer of global new energy solutions, BYD is committed to building a sustainable new energy ecosystem |

The competitive landscape is being reshaped by the n-type TOPCon technology transition. The competitive differentiation for the LATAM market success increasingly centers on module certification for Brazilian and Mexican market compliance, LATAM regional technical support and logistics, project finance pre-approval with commercial banks, and warranty backstop financial strength that project financiers require.

Key Company Profiles

LONGi

LONGi is the world's largest solar module manufacturer by annual shipment and the global benchmark for the solar panel market.

- Key Products: Hi-MO X10, Hi-MO 9, Hi-MO 7, Hi-MO X6 Max.

- Recent Developments: In August 2025, LONGi launched HPBC 2.0 photovoltaic modules (Hi-MO 9) in Brazil, designed to deliver superior results in any type of system: from residential rooftops to large ground-mounted solar plants, whether DG (distributed generation) or GC (centralized).

- Strategic Focus: Expanding high-efficiency module adoption through advanced technologies such as HPBC and N-type products while strengthening its presence in utility-scale and distributed solar projects across the region.

BYD Company Ltd.

BYD Company Ltd. is a global renewable energy and technology company with a strong presence in photovoltaic modules, energy storage systems, and integrated clean energy solutions for the solar market.

- Key Products: HALO, AURO N series, AURO P series.

- Strategic Focus: Strengthening integrated solar ecosystems by expanding high-efficiency TOPCon module adoption while leveraging solar, energy storage, and EV charging solutions across utility-scale and distributed solar projects.

Market Concentration Analysis

The Latin America solar panel market is highly concentrated at the manufacturer level. LONGi and BYD Company Ltd. together supply an estimated 55-65% of LATAM module imports by volume, reflecting the structural advantages of integrated manufacturers that sustain Chinese manufacturer price leadership. National market concentration varies significantly by country: Brazil's fragmented 80,000+ installer market prevents any single module brand from dominating retail distribution, with LONGi holding an estimated 15-20% share of Brazilian module imports. Chile's utility-scale market is more concentrated among premium brands specified in large project tenders, while Mexico's C&I market has stronger positions versus Brazil's LONGi dominance due to Mexican industrial buyer preference for non-Chinese supply chain diversification.

Investment & Growth Opportunities

Highest Growth Segments

Monocrystalline silicon type (~7.9% CAGR), commercial end-use (~7.4% CAGR), residential end-use (~7.1% CAGR), Brazil's MMGD distributed generation market (~8-10% national CAGR), Chile's Atacama mining sector utility-scale (~7-9% CAGR), and the green hydrogen-adjacent solar demand (~25-30% CAGR for green hydrogen-dedicated solar from near-zero 2025 base) represent the region's highest-growth solar panel investment vectors.

Emerging Investment Opportunities

The LATAM C&I solar financing market represents one of Latin America's most commercially attractive clean energy investment themes. C&I solar system models are growing rapidly in Brazil, Mexico, and Colombia. Each 1 MW of C&I solar installation requires USD 500,000-800,000 in project financing, generating USD 50,000-100,000 annual EBITDA through the electricity service agreement, creating USD 8-12 return on invested capital over 15-year contract terms.

Investment Themes

- Green hydrogen solar anchor development positioning for Chile, Brazil, and Colombia: Each 1 GW of planned electrolysis capacity for green hydrogen export projects requires 1.5-2.5 GW of dedicated solar PV as anchor generation. Investors and developers positioning early in green hydrogen solar supply chains create competitive advantages when green hydrogen project financial close timelines materialize.

- Chile and Peru lithium and copper mine solar self-supply creating long-term industrial PPA demand: Latin America's lithium triangle and Peruvian copper mining industry each face energy transition requirements that make solar self-supply at mine sites commercially compelling. Each new large-scale copper mine energy PPA contract at USD 25-35/MWh creates USD 150-400 Million in annual PPA revenue for LATAM solar developers.

Future Market Outlook (2026-2034)

The Latin America solar panel market is projected to grow from USD 10.97 Billion in 2025 to USD 20.59 Billion by 2034, delivering a 7.03% CAGR over the forecast period. The market's anchor value of USD 15.40 Billion in 2030 represents a Latin American solar industry where Brazil has crossed 50 GW of cumulative installed solar capacity, Chile's Atacama Desert has emerged as a global green hydrogen production hub requiring 5+ GW of dedicated solar, and the regional C&I solar market has matured into a structured, financeable asset class with institutional capital from pension funds and infrastructure investors providing long-term financing. Three structural forces define Latin America's solar market growth through 2034 with high confidence. First, Brazil's policy irreversibility. Second, the electricity tariff trajectory. Third, module price reduction continuation.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Country Managers and Regional Directors; EPC project directors; solar project finance officers; ANEEL grid connection and MMGD regulation officers; CNE Chile renewable energy auction team; Brazilian solar distributor executives; and Brazilian and Chilean solar project developers.

Secondary Research

Secondary research encompassed ABSOLAR (Associacao Brasileira de Energia Solar Fotovoltaica); ANEEL SIGA generation database; IEA Renewables 2025 report, Latin America section; IRENA Renewable Energy Statistics 2025; individual company annual reports; Latin America Solar Market Update. Over 70 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up country and end-use models calibrated against ABSOLAR Brazil annual installation data (GW), ANEEL SIGA cumulative capacity database, Chile CNE installed capacity statistics, and national energy regulator annual reports for Mexico, Colombia, Peru, and Argentina. Module revenue modeled from GW installation and average module ASP (USD/W) by country and segment, calibrated against BNEF module price index and LONGi public pricing disclosures. Key inputs include MMGD Brazil annual installation trajectory, Chile Atacama utility-scale auction tender pipeline, Mexico C&I self-supply growth, and Colombia/Peru renewable auction award timeline from national regulator public procurement schedules.

Latin America Solar Panel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Crystal Silicon, Monocrystalline Silicon, Polycrystalline Silicon, Thin Film, Others |

| End Uses Covered | Commercial, Residential, Industrial |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | LONGi, Solarever Group, BYD Company Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America solar panel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America solar panel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America solar panel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Solar Panel Market Report

The Latin America solar panel market reached USD 10.97 Billion in 2025, driven by Brazil's solar cumulative installed base and annual additions under the distributed generation framework, Chile's utility-scale solar expansion, Mexico's C&I self-supply growth, Colombia's corporate PPA market, Peru's mining sector solar adoption, and Argentina's auction pipeline.

The market grows at 7.03% CAGR during 2026-2034, reaching USD 20.59 Billion by 2034, driven by Brazil's residential market expansion to tier-3 and tier-4 cities, Chile's green hydrogen solar demand, Mexico's renewable policy normalization, n-type TOPCon module efficiency enabling greater kWp per hectare at equivalent cost, and BESS integration creating solar-plus-storage value propositions beyond energy-only generation.

Crystal silicon leads at 38.6% through Brazil's mass-market residential and C&I monocrystalline panel segment.

Commercial leads at 41.9% through Latin American C&I electricity tariffs, creating 2-3 year solar payback periods for commercial buyers, corporate ESG commitments driving multinational subsidiary solar adoption, and the maturing LATAM C&I ESCO and PPA market enabling zero-CapEx solar access for commercial consumers.

Brazil leads at 36.5% through net metering policy, electricity tariff increases creating compelling solar ROI and consumer credit financing, installed rooftop systems, and utility-scale auction programs delivering 2-3 GW annually.

Leading companies include LONGi, Solarever Group, and BYD Company Ltd., among others.

The market is projected to reach approximately USD 15.40 Billion by 2030, with Brazil crossing 50 GW cumulative installed capacity, Chile's green hydrogen first commercial projects anchoring 2-4 GW dedicated solar, Mexico's auction tender relaunch, n-type TOPCon modules reaching 24%+ standard efficiency, and the LATAM C&I ESCO solar market attracting institutional infrastructure investor capital.

Green hydrogen requires 1.5-2.5 GW of dedicated solar per 1 GW of electrolysis capacity. Chile's National Green Hydrogen Strategy requires a high amount of dedicated solar, driving the demand.

Three primary challenges: high financing costs and FX volatility, grid infrastructure constraints, and Chinese module import dependence.

Three priority opportunities: green hydrogen solar anchor projects in Chile, Brazil C&I ESCO solar financing, and Brazil solar cooperative remote self-generation financing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)