Latin America Vegan Cosmetics Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Country, 2026-2034

Latin America Vegan Cosmetics Market Size, Share, Trends & Forecast (2026-2034)

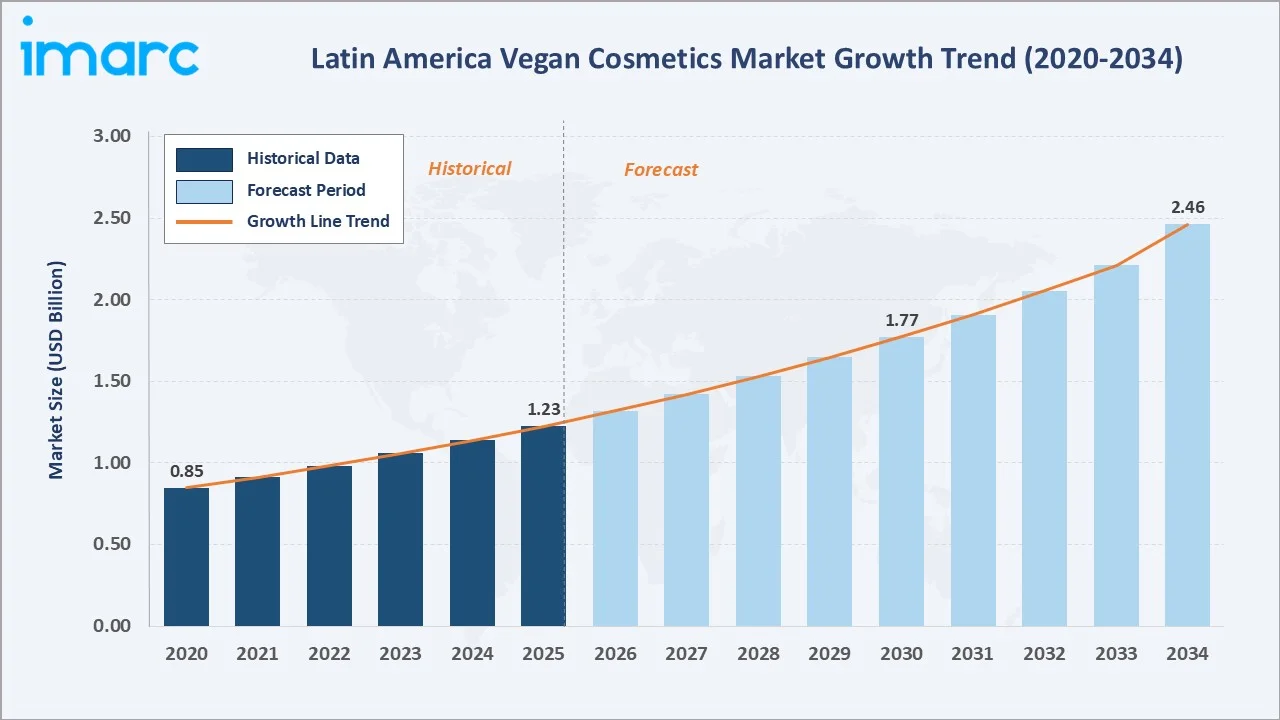

The Latin America vegan cosmetics market reached USD 1.23 Billion in 2025 and is projected to reach USD 2.46 Billion by 2034, growing at a CAGR of 7.66% during 2026-2034. Rising consumer awareness of animal welfare and ethical beauty standards, accelerating legislative bans on animal testing across key markets, and growing millennial and Gen Z demand for clean-label, plant-based personal care products are the primary forces driving robust growth throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 1.23 Billion |

|

Market Size (2034) |

USD 2.46 Billion |

|

CAGR (2026-2034) |

7.66% |

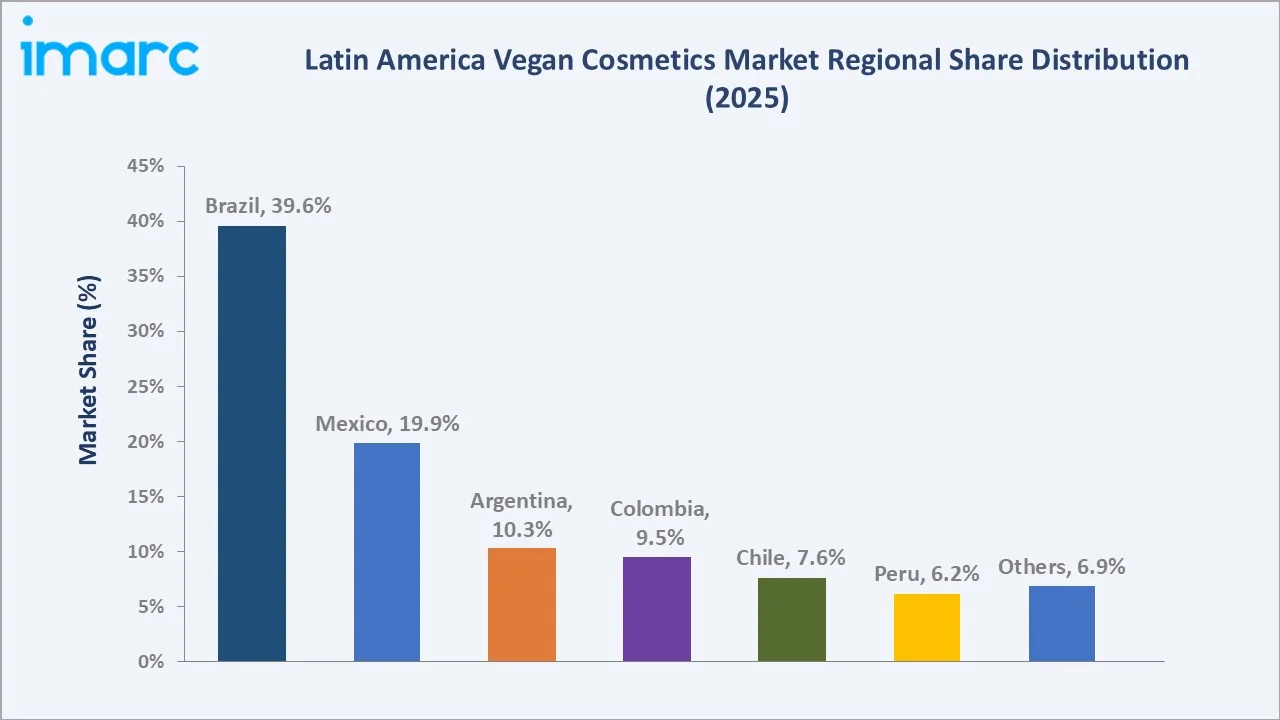

Brazil leads regionally with a 39.6% market share in 2025, anchored by its status as Latin America’s largest cosmetics producer and the presence of leading vegan-committed brands. Skin Care commands the largest product type share at 38.7%, while supermarkets and hypermarkets lead distribution at 36.5%. Online stores are the fastest-growing distribution channel at ~10.2% CAGR, driven by social commerce and direct-to-consumer brand expansion.

To get more information on this market, Request Sample

The market grew from USD 0.85 Billion in 2020 to USD 1.23 Billion in 2025, an increase of USD 0.38 Billion over five years, driven by post-pandemic clean beauty acceleration, expanding cruelty-free certification awareness, and the growth of local brands leveraging Amazonian and Andean botanical ingredients. The market is forecast to reach USD 2.46 Billion by 2034, reflecting the structural shift toward ethical beauty consumption across all income tiers and age groups in the region.

Executive Summary

The Latin America vegan cosmetics market is experiencing accelerating growth, driven by the convergence of ethical consumerism, regulatory advancement in animal testing bans, biodiversity-driven ingredient innovation, and the rapid digitalization of beauty retail. The market stood at USD 1.23 Billion in 2025 and is forecast to reach USD 2.46 Billion by 2034 at a CAGR of 7.66%.

Skin care dominates with a 38.7% product type share, driven by consumer demand for plant-derived moisturizers, serums, and sunscreens formulated without animal-derived ingredients. Hair care at 27.4% is the second-largest segment, expanding rapidly through innovation in Amazonian botanical actives including babassu oil, cupuassu butter, and murumuru butter. Makeup at 22.1% is growing at approximately 8.4% CAGR, supported by the expansion of vegan color cosmetics from both international and regional brands.

Supermarkets and hypermarkets lead distribution at 36.5%, leveraging the scale of regional grocery chains in Brazil, Mexico, and Argentina. Specialty stores at 24.8% serve premium and niche vegan beauty consumers in urban centers. Online stores at 18.6% is the fastest-growing channel at ~10.2% CAGR, fueled by social commerce on Instagram and TikTok, DTC brand subscription models, and platforms such as MercadoLibre and Magalu expanding their beauty categories.

Brazil leads regionally at 39.6%, reflecting its dual position as Latin America’s largest cosmetics market and the home of Natura and Grupo Boticário, two of the region’s most prominent vegan and cruelty-free beauty champions. Mexico at 19.9% benefits from a legislative ban on animal testing enacted in 2021, making it a regulatory bellwether for the region.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Skin Care – 38.7% share (2025) |

|

Fastest Growing Product Type |

Makeup – ~8.4% CAGR (2026-2034) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 36.5% share (2025) |

|

Fastest Growing Distribution Channel |

Online Stores – ~10.2% CAGR (2026-2034) |

|

Leading Country |

Brazil – 39.6% share (2025) |

|

Top Companies |

Natura, Grupo Boticário, L'Oréal S.A., Beiersdorf AG |

Key Analytical Observations Supporting The Above Data:

- Skin care at 38.7% (2025) reflects the segment’s role as Latin America’s primary vegan beauty entry point, anchored by consumer demand for moisturizers, facial serums, and sunscreens free of beeswax, lanolin, collagen, and other animal-derived actives.

- Supermarkets and hypermarkets at 36.5% (2025) reflect the mass-market accessibility of vegan cosmetics through Latin America’s large grocery retail chains, including Pão de Açúcar (Brazil), Walmart Mexico, and Cencosud (Chile, Colombia).

- Online Stores at ~10.2% CAGR is the fastest-growing distribution channel as MercadoLibre, Amazon Brasil, and brand DTC websites accelerate vegan beauty discovery and repurchase across the region. Natura’s integration with MercadoLibre’s fulfillment network and TikTok Shop’s expanding beauty category in Mexico are collectively reshaping channel dynamics.

- Brazil’s 39.6% (2025) market leadership reflects its position as the world’s fourth-largest beauty market, the home of globally recognized cruelty-free brand champions, and a consumer culture increasingly influenced by environmental consciousness, indigenous biodiversity pride, and social media-driven beauty trends.

Latin America Vegan Cosmetics Market Overview

The Latin America vegan cosmetics market encompasses skin care, hair care, color cosmetics, and body care products formulated without animal-derived ingredients and not tested on animals, typically certified by recognized bodies such as PETA, Leaping Bunny, or ABV (Associação Brasileira de Veganismo). The market serves a growing segment of ethically motivated consumers across Brazil, Mexico, Argentina, Colombia, Chile, Peru, and other regional markets.

Latin America’s vegan cosmetics value chain is distinguished by its access to one of the world’s richest biodiversity resources, the Amazon Basin, the Andes, and Atlantic Forest biomes, providing unique plant-derived actives unavailable elsewhere. Regional brands increasingly partner with indigenous communities for sustainable, fair-trade botanical sourcing, creating both supply chain resilience and authentic brand narratives that resonate with ethical consumers globally.

Market Dynamics

To evaluate market opportunities, Request Sample

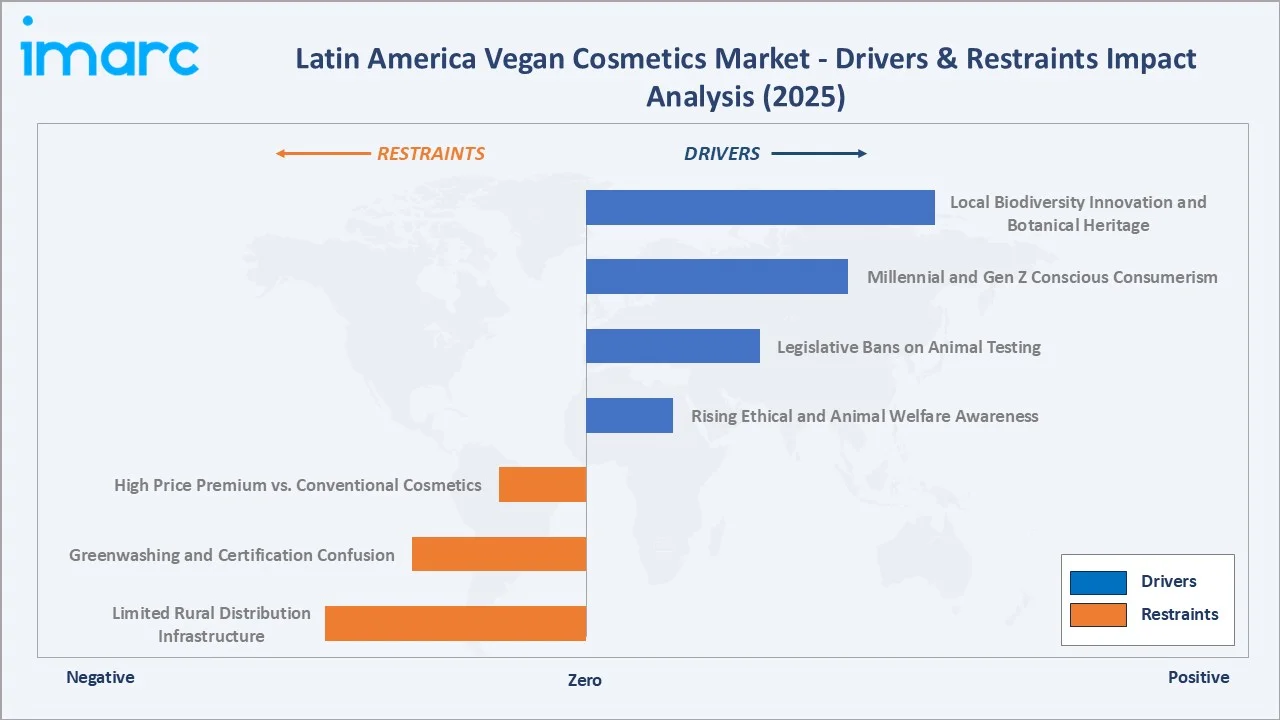

Market Drivers

- Rising Ethical and Animal Welfare Awareness: Consumer awareness of animal testing practices, supply chain transparency, and the environmental impact of cosmetics manufacturing is driving structural demand for certified vegan and cruelty-free beauty products across Latin America.

- Legislative Bans on Animal Testing: Mexico’s 2021 federal ban on cosmetic animal testing and Brazil’s Law No. 11794 (2008) and Law No. 6360 (1976) restricting animal testing for cosmetics have created a regulatory environment that accelerates the adoption of vegan-compliant formulations.

- Millennial and Gen Z Conscious Consumerism: Latin America and the Caribbean’s demographic profile, with over 25% of the population aged between 10 and 24, creates a structurally large and growing audience for ethical beauty consumption. This cohort is particularly receptive to social media-driven brand transparency, ingredient education, and the clean beauty narrative, making social commerce a critical acquisition channel for vegan cosmetics brands.

- Local Biodiversity Innovation and Botanical Heritage: The region’s unique botanical assets, including babassu oil, camu-camu, açaí, murumuru butter, buriti oil, and quinoa protein, enable Latin American brands to create distinctively positioned vegan formulations, differentiating them from European and North American competitors in domestic and export markets.

Market Restraints

- High Price Premium vs. Conventional Cosmetics: Certified vegan cosmetics in Latin America typically command a 20–45% price premium over equivalent non-vegan products, creating a significant affordability barrier in markets where mass-market beauty consumption dominates.

- Greenwashing and Certification Confusion: The proliferation of self-declared “natural,” “organic,” and “cruelty-free” labels without third-party certification is eroding consumer trust and creating confusion in the vegan cosmetics category. The absence of a single harmonized Latin America-wide vegan cosmetics certification standard makes it difficult to distinguish genuinely compliant products from opportunistic greenwashing.

- Limited Rural Distribution Infrastructure: Vegan cosmetics retail penetration is concentrated in urban metropolitan markets, with limited availability in secondary cities and rural areas where traditional direct selling channels remain the primary beauty retail touchpoints.

Market Opportunities

- Men’s Vegan Grooming and Personal Care: The men’s grooming segment within Latin America’s vegan cosmetics market is nascent but growing rapidly, with an estimated CAGR of 12–15% in 2022–2025. Brazil’s male grooming culture and Mexico’s growing metrosexual consumer segment are driving demand for vegan-certified face washes, moisturizers, beard oils, and hair care products specifically marketed to men.

- Export Opportunity from Regional Botanical Heritage: Latin American vegan cosmetics brands leveraging indigenous plant actives are gaining significant traction in North American, European, and Japanese premium beauty markets, where “sustainable sourcing from Amazonian biodiversity” commands strong consumer resonance and retail premiums.

Market Challenges

- Currency Volatility and Import Cost Exposure: Latin America’s endemic currency volatility creates significant cost uncertainty for brands that import vegan-certified specialty ingredients or sustainable packaging materials from Europe, North America, and Asia. Currency depreciation events can compress margins and force retail price increases that reduce category accessibility.

- Competition from Mainstream Brands Entering Vegan Claims: The entry of large multinational FMCG brands into the vegan cosmetics space through brand extensions and reformulations creates intensified competition for shelf space and consumer attention previously dominated by specialist vegan and natural beauty brands.

Emerging Market Trends

1. AI and Botanical Innovation Advance Longevity Skincare

In May 2026, Debut and Natura announced a partnership to develop and commercialize an AI-discovered skin longevity ingredient complex, combining Debut’s AI biotechnology platform with Natura’s Amazonian botanical expertise. Products using the complex could launch as early as 2027, after clinical validation, targeting longevity-focused skincare in Latin America.

2. Vegan Mass-Market Democratization

The Latin America vegan cosmetics market is witnessing wider mass-market adoption as affordable brands expand cruelty-free, plant-based, and clean-label product lines across skincare, haircare, color cosmetics, and personal care. Rising consumer awareness about animal welfare, sustainability, and ingredient safety is pushing vegan beauty beyond premium niches into supermarkets, pharmacies, e-commerce platforms, and direct-selling channels.

3. Social Commerce and Influencer-Driven Discovery

According to FastMoss data from April 2025, TikTok Shop Mexico’s beauty and personal care category sold more than 255,000 units in a single month, reflecting a strong 83.9% month-over-month increase. This enables vegan cosmetics brands to sell directly through viral video content. Micro-influencer campaigns featuring ingredient transparency and vegan certification “unboxing” content consistently outperform macro-influencer campaigns in driving trial.

4. Vegan Verification Supports Transparent Cosmetic Claims

Eurofins’ Vegan Verification Program for cosmetics and personal care helps manufacturers, brands, and retailers test products and support “100% vegan” labeling claims through scientific verification. The program includes supply-chain review, risk assessment, animal-origin testing, and use of the Eurofins Vegan Verified logo to strengthen consumer trust.

Industry Value Chain Analysis

Latin America’s vegan cosmetics value chain is distinguished by its exceptional raw material biodiversity advantage, the increasing role of indigenous community partnerships in sustainable botanical sourcing, and a growing ecosystem of vegan certification bodies, sustainable packaging suppliers, and ethical ingredient traceability platforms that collectively enable a transparent, ethically validated supply chain from field to shelf.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Sustainably sourced plant-based raw materials; eco-friendly primary and secondary packaging materials |

|

Formulation & R&D |

Specialist vegan and cruelty-free cosmetics contract formulators; in-house brand R&D teams; biotechnology-derived ingredient development laboratories |

|

Manufacturing & Packaging |

Regional and multinational cosmetics contract manufacturers operating under national regulatory compliance; sustainable and biodegradable packaging converters |

|

Certification & Compliance |

Third-party vegan and cruelty-free certification bodies; national cosmetics regulatory agencies; product safety assessment services |

|

Retail & Distribution |

Mass-market supermarket and hypermarket chains; specialty natural and vegan beauty retailers; pharmacy chains; online marketplaces and brand DTC e-commerce platforms |

|

End Consumers |

Ethically and environmentally motivated urban consumers; health-conscious and wellness-oriented shoppers; international premium export market consumers |

Technology Landscape in the Latin America Vegan Cosmetics Industry

Plant-Based and Biotechnology-Derived Ingredient Innovation

Latin American vegan cosmetics brands are investing in biotechnology-derived plant actives to overcome the supply variability of wild-harvested botanical ingredients. Natura’s partnership with biotech firms to develop lab-grown equivalents of rare Amazonian actives represents the frontier of sustainable vegan ingredient technology.

Ingredient Transparency Technology and QR-Code Traceability

Blockchain-enabled ingredient traceability, QR-code-linked supply chain transparency portals, and AI-powered ingredient safety analysis are increasingly adopted by Latin American vegan cosmetics brands to substantiate cruelty-free and vegan claims. Natura’s “Sociobiodiversidade” (Sociobiodiversity) program uses digital traceability tools, providing consumers with scannable proof-of-origin for key active ingredients.

Social Commerce Technology and AI-Personalization

AI-powered skin analysis applications, virtual shade-matching for vegan makeup, and personalized vegan product recommendation engines are scaling rapidly across Latin America’s digital beauty ecosystem. Grupo Boticário’s AI skin diagnostic tool and Natura’s digital consultant personalization platform enable vegan product discovery and trial conversion at significantly higher rates than traditional retail browsing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Skin Care |

38.7% |

2025 |

|

Distribution Channel |

Supermarkets & Hypermarkets |

36.5% |

2025 |

|

Country |

Brazil |

39.6% |

2025 |

By Product Type

Skin care dominates with a 38.7% share in 2025. This segment encompasses face cleansers, moisturizers, serums, eye creams, sunscreens, and body lotions formulated exclusively from plant-derived, mineral, and biotechnology-derived ingredients. Skin care’s leadership reflects Latin American consumers’ strong dermatological awareness, high UV exposure driving sunscreen demand, and the cultural centrality of facial skin care in personal care routines across all age demographics.

To access detailed market analysis, Request Sample

Hair care at 27.4% is growing strongly, driven by innovation in plant-derived conditioning actives uniquely accessible to Latin American formulators, including babassu oil for damaged hair repair, murumuru butter for frizz control, and quinoa protein for color-treated hair strengthening. Makeup at 22.1% is growing at ~8.4% CAGR as vegan color cosmetics transition from a premium niche to mainstream availability, supported by social media tutorials normalizing vegan beauty product usage.

By Distribution Channel

Supermarkets and hypermarkets lead with a 36.5% share in 2025. In Latin America’s largest markets, major grocery and hypermarket chains, including Carrefour Brasil, Walmart Mexico, and Grupo Pão de Açúcar, increasingly dedicate shelf space to vegan and natural beauty sub-categories, providing mass-market accessibility for vegan cosmetics brands.

Specialty stores at 24.8% serve the premium vegan beauty segment through natural and organic beauty retailers, pharmacy chains, and standalone vegan lifestyle stores in Latin America’s major urban markets. Online stores at 18.6% is the fastest-growing channel at ~10.2% CAGR, as social commerce and brand DTC websites collectively capture an increasing share of vegan beauty purchases, particularly among urban millennials.

Regional Market Insights

Brazil’s market leadership (39.6%, 2025) reflects its position as Latin America’s largest economy and a consumer culture deeply engaged with environmental sustainability and indigenous biodiversity heritage. Brazil’s cosmetics regulator ANVISA processes thousands of new cosmetic product registrations annually, creating a uniquely dynamic innovation environment, while the country’s over 3 million Natura beauty consultants form one of Latin America’s largest direct selling networks for vegan-committed beauty products.

Mexico, at 19.9%, has been energized by its landmark 2021 federal ban on cosmetic animal testing, positioning it as the region’s regulatory leader and attracting international vegan beauty brand investment. Argentina at 10.3% reflects Buenos Aires’ sophisticated premium beauty culture, while Colombia at 9.5% and Chile at 7.6% represent fast-growing secondary markets with above-average consumer openness to ethical beauty consumption.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Brazil |

39.6% |

Home of leading ethical beauty brand champions; rich botanical biodiversity heritage; large and sophisticated direct selling and e-commerce consumer base |

|

Mexico |

19.9% |

Legislative animal testing ban creating regulatory tailwind; rapidly growing urban millennial consumer base; expanding social commerce and online beauty retail; increasing multinational manufacturing investment |

|

Argentina |

10.3% |

Premium urban consumer market with high ethical beauty awareness; rising eco-consciousness and willingness to pay a sustainability premium; growing online and specialty retail channel accessibility |

|

Colombia |

9.5% |

Advancing cruelty-free and vegan cosmetics regulatory framework; expanding urban specialty retail; growing natural cosmetics export ecosystem; increasing consumer awareness of ethical beauty standards |

|

Chile |

7.6% |

Above-average household incomes and strong environmental regulation affinity; expanding supermarket vegan shelf space; well-developed specialty natural beauty retail in major urban centers |

|

Peru |

6.2% |

Access to unique Andean botanical sourcing traditions and indigenous ingredient heritage; growing urban ethical consumer market; regulatory alignment with regional cruelty-free and vegan standards |

|

Others |

6.9% |

Nascent but growing ethical beauty awareness; increasing online and cross-border e-commerce accessibility; gradual expansion of vegan cosmetics retail through supermarkets and pharmacy channels |

Competitive Landscape

Latin America’s vegan cosmetics market is moderately concentrated, with key players collectively controlling an estimated 45–55% of total organized market revenue. The remaining share is distributed across a vibrant ecosystem of regional indie vegan brands, local natural beauty companies, and international specialist vegan beauty brands entering Latin America through e-commerce and specialty retail.

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Natura |

Natura, Avon |

Market Leader |

Regional market leadership through an extensive direct selling network; strong ethical sourcing credentials and botanical biodiversity heritage; well-established vegan-certified portfolio across multiple price tiers |

|

Grupo Boticário |

O Boticário, Eudora, Quem Disse Berenice, Vult |

Market Leader |

Largest domestic franchise retail network providing mass-market accessibility; aggressive vegan portfolio expansion across mass and premium tiers; strong digital and AI-powered consumer engagement capabilities |

|

L'Oréal S.A. |

Garnier, L’Oréal Paris, Biolage |

Strong Challenger |

Global R&D capabilities enabling large-scale vegan reformulation; strong mass-market distribution across supermarket and hypermarket channels; broad international brand recognition supporting consumer trust |

|

Beiersdorf AG |

NIVEA, Eucerin |

Challenger |

Dermatologically validated product credentials supporting pharmacy and clinical channel presence; growing clean and vegan formulation pipeline; strong consumer trust in skin care safety and efficacy claims |

The Latin America vegan cosmetics market is gaining momentum as consumers increasingly prefer cruelty-free, plant-based, and clean-label beauty products across skincare, haircare, makeup, and personal care categories. Rising awareness of animal welfare, sustainability, ingredient safety, and ethical consumption is encouraging both global and regional brands to expand vegan product lines.

Key Company Profiles

Natura

Natura is one of Latin America’s largest cosmetics companies and the region’s most recognized champion of vegan, sustainable, and ethically sourced beauty. The company operates its Natura brand as the flagship business alongside Avon.

- Product Portfolio: Natura Ekos (Amazonian botanical vegan skin and body care), Natura Una (vegan makeup), Natura Plant (vegan hair care), Natura Chronos (anti-ageing vegan skin care), and Avon Planet Spa (vegan spa-inspired body care).

- Recent Developments: In May 2026, Natura reported Q1 2026 net revenue of BRL 4.7 billion, with revenue pressured by weaker conditions in Brazil and Argentina, while other Hispanic Latin American markets delivered solid performance. The company posted EBITDA of BRL 346 million with a 7.3% margin, gained market share in Brazil, recorded 23.6% YoY digital sales growth, and began the Avon relaunch in Brazil and Mexico in March.

- Strategic Focus: Amazonian sociobiodiversity sourcing expansion; digital-physical omnichannel model blending consultant selling with DTC e-commerce; export growth in US Hispanic, European, and Asian premium beauty markets.

Grupo Boticário

Grupo Boticário is one of Brazil’s largest beauty franchise networks and has growing international operations. The group manages a portfolio of brands spanning mass-market (O Boticário, Vult), premium (Eudora), and lifestyle (Quem Disse Berenice, Dr. Jones) categories.

- Product Portfolio: O Boticário Nativa SPA (vegan body care), Eudora Siàge (vegan hair care with Amazonian actives), Quem Disse Berenice vegan color cosmetics, and Vult affordable vegan makeup.

- Recent Developments: In April 2026, Grupo Boticário announced that it is prioritizing operational efficiency to sustain growth amid a slowdown in Brazil’s beauty market. The company reported 6.7% sales volume growth in 2025, reaching BRL 38.1 billion, while expanding market share to 15.5%.

- Strategic Focus: Vegan product portfolio democratization across mass-market price tiers; AI digital skin diagnostics expansion via Eudora Siàge; international market expansion in US Hispanic and Lusophone markets.

Market Concentration Analysis

Latin America’s vegan cosmetics market exhibits moderate concentration, with Natura and Grupo Boticário collectively dominating the Brazilian market through their combined franchise, direct selling, and digital retail networks. International players are steadily growing their vegan-certified product presence, but have not yet achieved the regional heritage and consumer trust credentials of the local incumbents in the ethical beauty space.

Market fragmentation is highest in the specialty and online channels, where hundreds of regional indie vegan brands compete effectively for premium consumer wallet share. Regional consolidation is expected to accelerate as leading players acquire successful indie vegan brands to expand their ethical beauty portfolio breadth.

Investment & Growth Opportunities

Fastest Growing Segments

Online stores (~10.2% CAGR), men’s vegan grooming (~12–15% CAGR), vegan makeup (~8.4% CAGR), and specialty stores (~8.8% CAGR) represent the primary high-growth investment vectors through 2034. The functional vegan beauty segment is growing at double-digit rates in urban Brazilian and Mexican markets, commanding 30–50% retail price premiums over standard vegan beauty products.

Emerging Market Expansion

Colombia, Chile, and Peru represent the most attractive near-term expansion markets, with growing urban middle classes, advancing legislative frameworks for cruelty-free cosmetics, and underserved specialty and online retail channels creating first-mover opportunities. Colombia’s emerging export ecosystem for natural cosmetics creates a regional export hub opportunity with investment potential.

Venture and Institutional Investment Trends

- Private equity and strategic investment in Latin American vegan beauty brands is accelerating, with international strategic buyers actively scouting Brazilian and Mexican indie vegan brands with proven DTC and social commerce scale for acquisition at Series A–B stages.

- Brazil’s SEBRAE (national SME support agency) and BNDES development bank are supporting sustainable cosmetics SME development through low-interest credit lines and innovation grants, with vegan and natural cosmetics identified as priority export sectors under Brazil’s bioeconomy strategy.

Future Market Outlook (2026-2034)

Latin America’s vegan cosmetics market is positioned for sustained, above-GDP growth through 2034. From a base of USD 1.23 Billion in 2025, the market is projected to reach USD 2.46 Billion by 2034 at a 7.66% CAGR. Brazil will retain absolute market leadership, but Mexico, Colombia, and Chile are projected to grow at above-average regional rates as animal testing legislation advances and specialty retail infrastructure matures.

Online stores’ channel share is forecast to expand from 18.6% in 2025 to approximately 28–30% by 2034, as social commerce, subscription beauty boxes, and D2C brand models capture an increasing share of vegan beauty purchasing. Skin care will maintain category leadership, but men’s grooming and functional beauty sub-categories will grow disproportionately, reflecting demographic and lifestyle trends that are structurally expanding the vegan cosmetics addressable market beyond its current female-skewed core consumer base.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry participants in 2024–2025, including vegan cosmetics brand managers, retail category buyers across Brazilian and Mexican supermarket chains, specialty natural beauty store operators, vegan certification body representatives (PETA Latin America, Leaping Bunny), industry association representatives from ABIHPEC (Brazil) and CANIPEC (Mexico), and independent cosmetics regulatory consultants.

Secondary Research

Secondary research encompassed annual reports; ABIHPEC Panorama do Setor 2025; CANIPEC Mexico industry data; ANVISA regulatory publications; Euromonitor and Statista Latin America beauty databases; IMARC primary expert panel review; and trade media, including Global Cosmetics News, Cosmética & Perfumaria, and Happi Magazine.

Forecasting Models

Market size estimations were derived using bottom-up country-level segment modelling incorporating per-capita beauty expenditure growth, vegan cosmetics penetration rate trajectories by income tier, channel shift dynamics from conventional to online retail, and demographic demand growth for ethical beauty consumption. A CAGR of 7.66% reflects consensus validated against ABIHPEC forward projections and IMARC’s primary expert panel review.

Latin America Vegan Cosmetics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Skin Care, Hair Care, Makeup, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Others |

| Countries Covered | Brazil, Mexico, Argentina, Colombia, Chile, Peru, Others |

| Companies Covered | Natura, Grupo Boticário, L'Oréal S.A., Beiersdorf AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Latin America vegan cosmetics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Latin America vegan cosmetics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Latin America vegan cosmetics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Latin America Vegan Cosmetics Market Report

The Latin America vegan cosmetics market reached USD 1.23 Billion in 2025 and is forecast to reach USD 2.46 Billion by 2034.

The market is expected to grow at a CAGR of 7.66% during 2026-2034, driven by ethical consumerism, legislative animal testing bans, local botanical innovation, and e-commerce expansion.

Brazil leads with a 39.6% share in 2025, anchored by Natura and Grupo Boticário’s market-leading vegan beauty portfolios and Brazil’s rich Amazonian botanical ingredient heritage.

Skin care dominates with a 38.7% share in 2025, driven by consumer demand for plant-derived moisturizers, serums, and sunscreens formulated without animal-derived ingredients.

Supermarkets and hypermarkets lead with a 36.5% share in 2025, reflecting their role as the primary mass-market accessibility point for vegan cosmetics across Brazil, Mexico, and other regional markets.

Some of the key players in the market include Natura, Grupo Boticário, L'Oréal S.A., and Beiersdorf AG.

Online stores are growing at approximately 10.2% CAGR because social commerce on TikTok and Instagram, DTC brand models, and Amazon Brasil’s expanding beauty categories are collectively shifting vegan cosmetics purchasing toward digital-first discovery and purchasing models among millennial and Gen Z consumers.

Key challenges include the high price premium of certified vegan cosmetics versus conventional alternatives, limiting mass-market accessibility, greenwashing and certification confusion eroding consumer trust, limited rural distribution infrastructure, and currency volatility creating cost unpredictability for brands relying on imported vegan-certified ingredients.

Men’s vegan grooming, functional vegan beauty formulations, social commerce and DTC digital platforms, Colombia and Chile market entry, and Amazonian botanical export brands targeting North American and European premium beauty markets represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)