Lead Acid Battery Market Size, Share, Trends and Forecast by Product, Construction Method, Sales Channel, Application, and Region, 2026-2034

Lead Acid Battery Market Size, Share, Trends & Forecast (2020-2025)

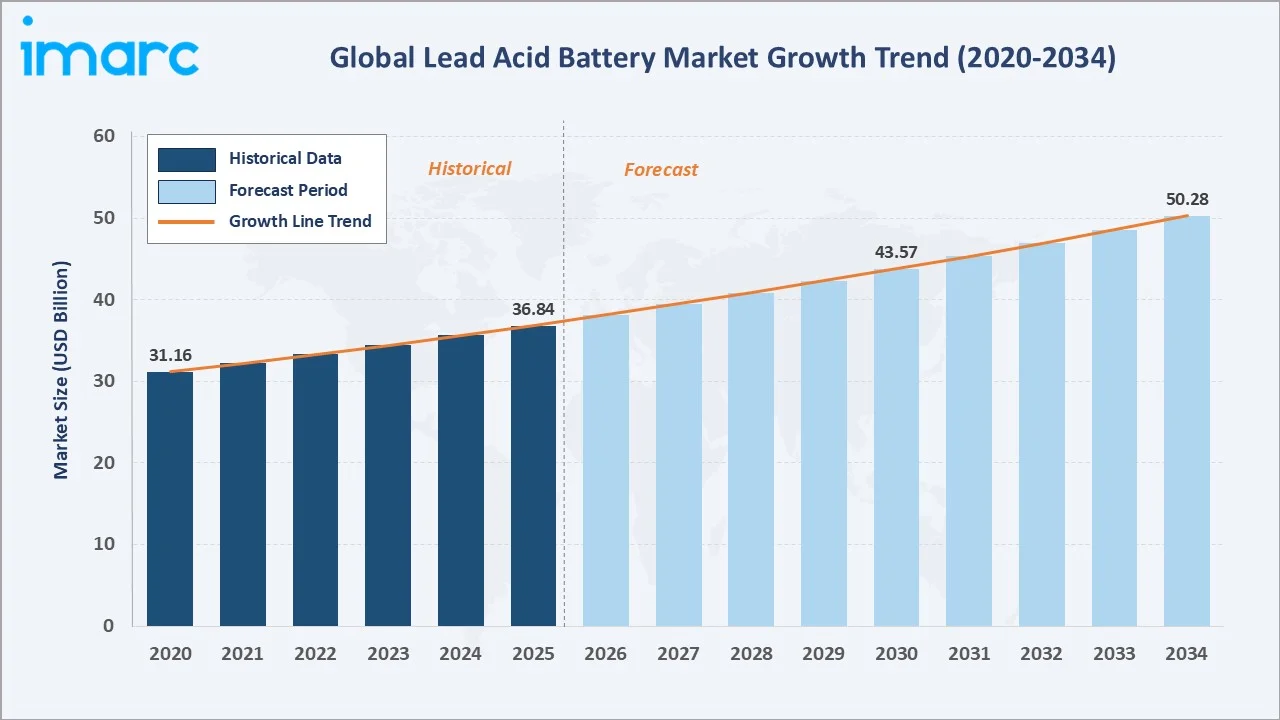

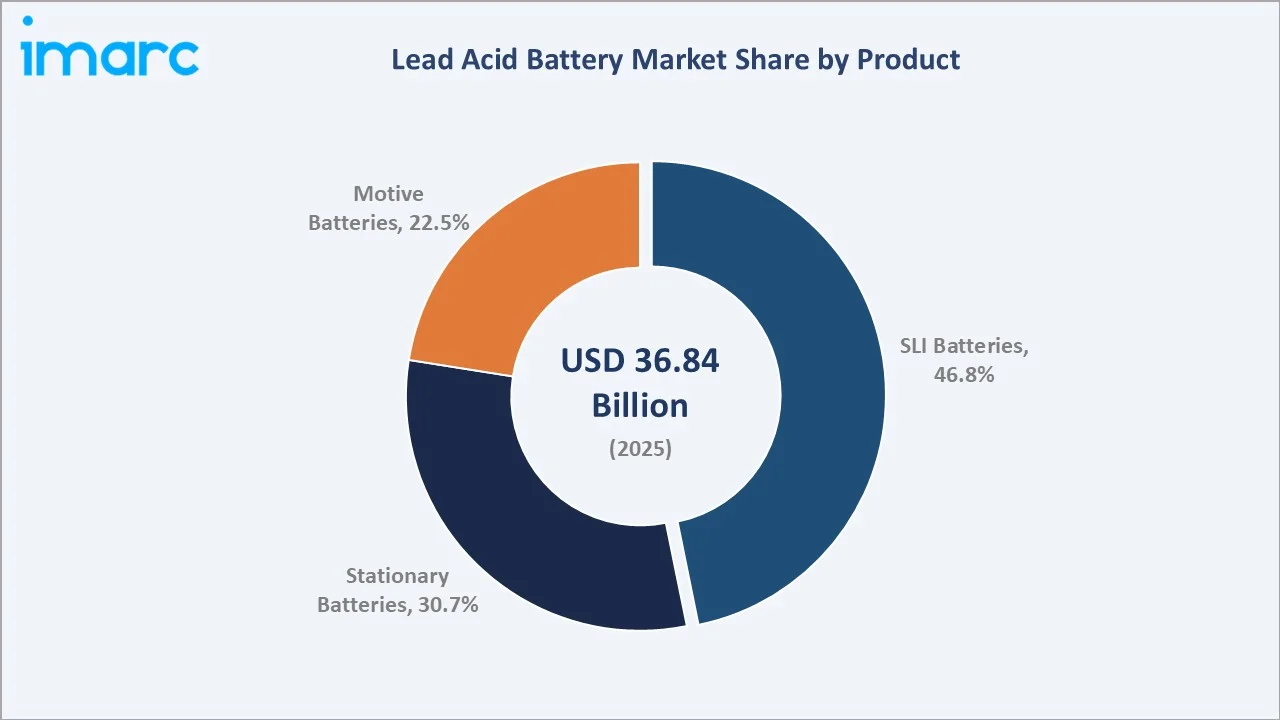

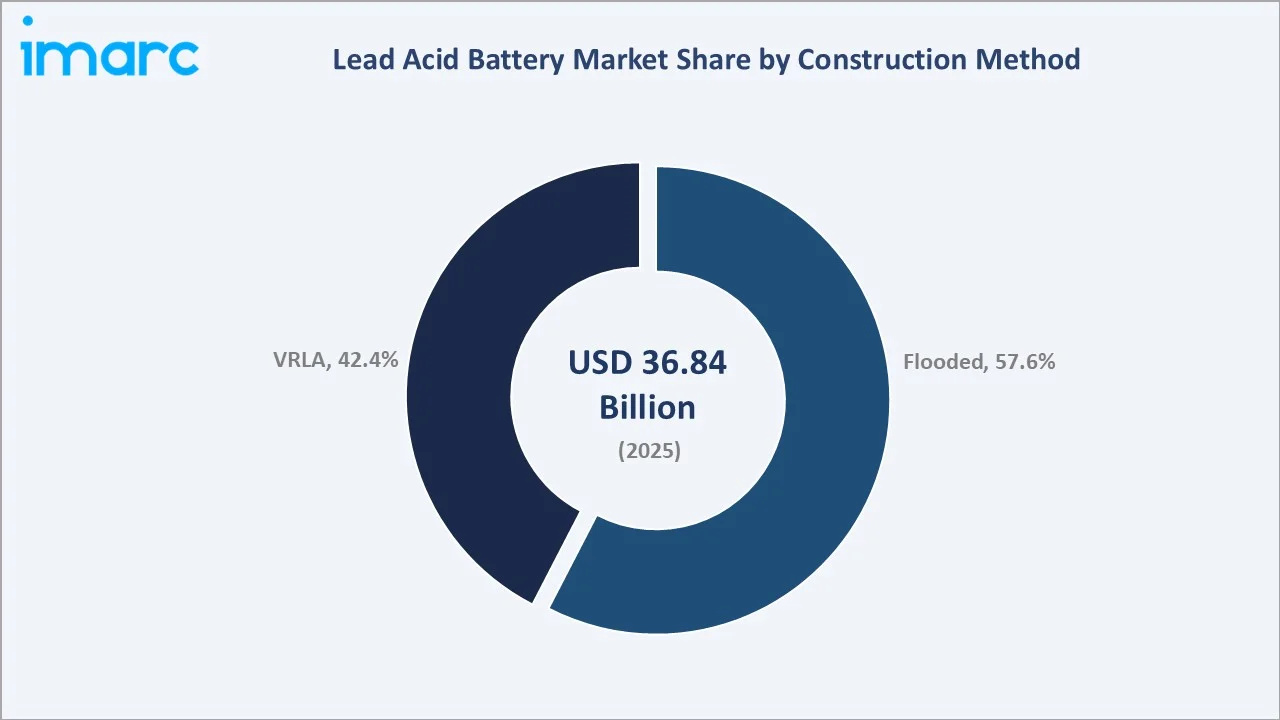

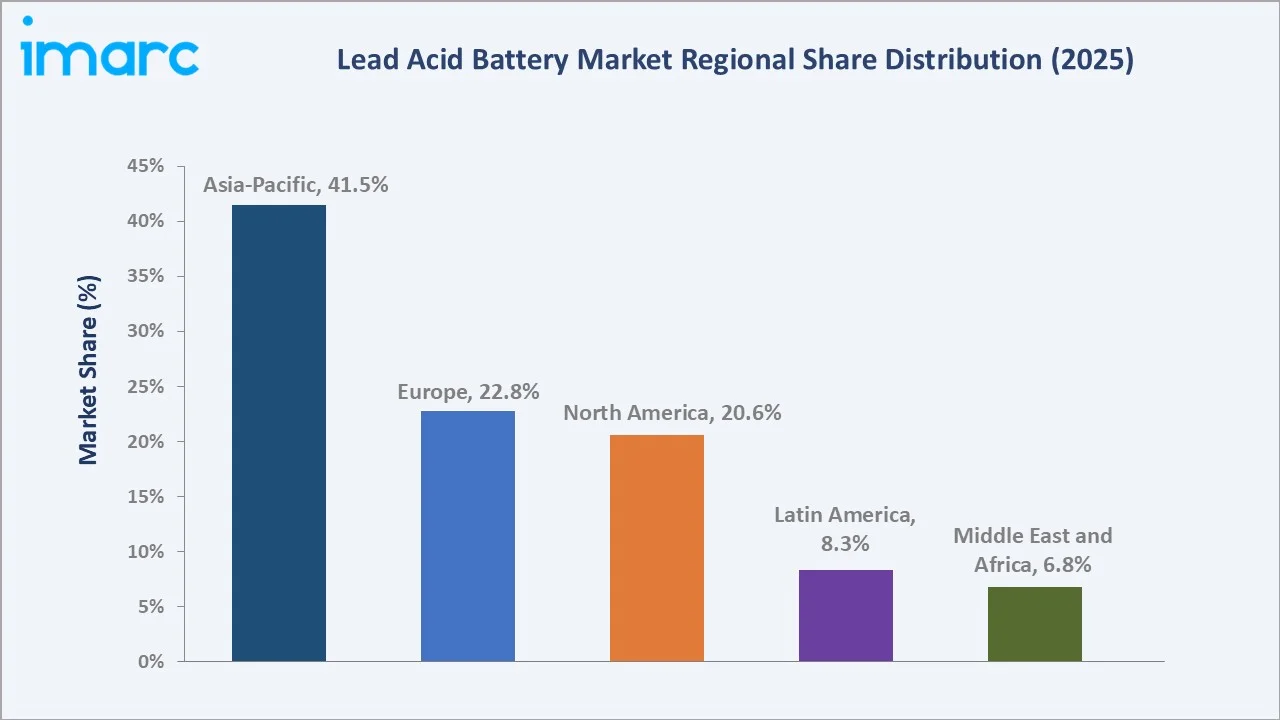

The global lead acid battery market reached USD 36.84 Billion in 2025 and is projected to reach USD 50.28 Billion by 2034, growing at a CAGR of 3.41% during 2026-2034. The market is driven by rising demand for reliable and cost-effective energy storage solutions across automotive, telecommunications, industrial backup power, and renewable energy applications. Global electric vehicle sales exceeded 17 million units in 2024, reflecting an increase of nearly 25% compared to 2023. This growth is driving the lead-acid battery market by increasing demand for auxiliary batteries used in electric vehicles for functions such as lighting, backup power, safety systems, and onboard electronics. SLI batteries dominate at 46.8%. Flooded leads construction at 57.6%. Asia-Pacific commands 41.5% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 36.84 Billion |

|

Forecast Market Size (2034) |

USD 50.28 Billion |

|

CAGR (2026-2034) |

3.41% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

SLI Batteries (46.8%, 2025) |

|

Dominant Construction |

Flooded (57.6%, 2025) |

|

Leading Region |

Asia-Pacific (41.5%, 2025) |

The market expanded from USD 31.16 Billion in 2020 to USD 36.84 Billion in 2025, anchored at USD 43.57 Billion in 2030, and forecast to reach USD 50.28 Billion by 2034. COVID-19 created a temporary automotive production disruption affecting SLI battery OEM demand, while simultaneously accelerating stationary battery demand as hospitals, telecommunications networks, and remote work infrastructure required enhanced UPS backup power. Post-pandemic automotive recovery restored SLI battery volume, while telecom 5G network infrastructure expansion and data center construction sustained stationary battery demand growth that has continued through 2025.

To get more information on this market, Request Sample

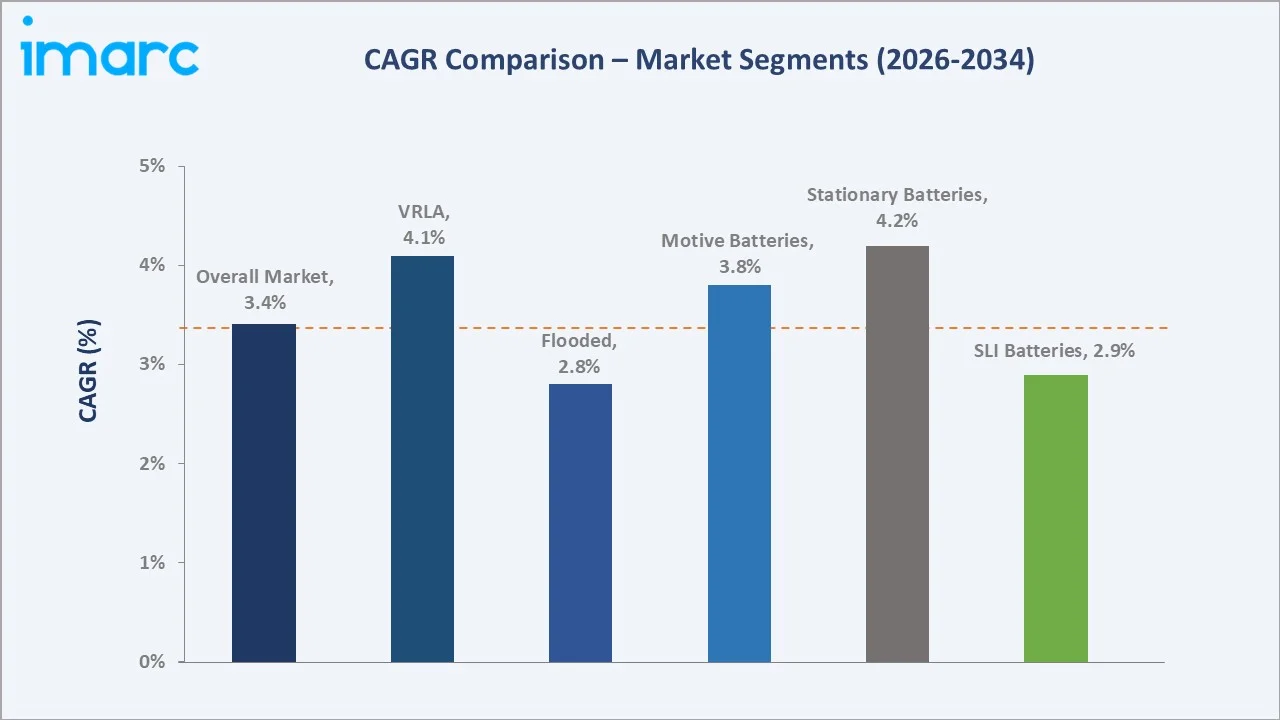

Stationary batteries grow fastest at ~4.2% CAGR driven by 5G telecom tower deployment, hyperscale data center construction in North America and Europe, and off-grid solar energy systems in the Asia Pacific, Africa, and Latin America. VRLA construction grows at ~4.1% CAGR as maintenance-free sealed battery technology gains adoption in telecommunications, UPS, and solar applications, where electrolyte maintenance is impractical.

Executive Summary

The global lead acid battery market reached USD 36.84 Billion in 2025, a figure that understates lead acid technology's true economic significance, 150-year-old lead acid batteries power more of the world's vehicle fleets, backup power infrastructure, and industrial operations than any other electrochemical energy storage technology combined, and despite persistent predictions of obsolescence from lithium-ion competition, the market continues growing at a healthy 3.41% CAGR through superior recyclability, low cost, safety, and unmatched reliability in float standby applications. The market is projected to reach USD 50.28 Billion by 2034.

SLI batteries at 46.8% dominate through the global ICE and mild-hybrid vehicle fleet's universal requirement for 12V starting power, which lead acid provides at a lower cost than lithium-ion equivalents at equivalent starting capability. The flooded segment dominates the construction method at 57.6%. Asia-Pacific at 41.5% leads through China's manufacturing scale dominance, India's growing automotive and telecom markets, and Southeast Asia's off-grid solar storage demand.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

SLI - 46.8% share (2025) |

|

Dominant Construction Method |

Flooded - 57.6% market share (2025) |

|

Leading Region |

Asia-Pacific - 41.5% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- SLI at 46.8% reflecting the global ICE vehicle fleet's structural dependence on lead acid starting batteries and the growing stop-start vehicle AGM upgrade cycle: SLI batteries' market dominance is structurally sustained by the global ICE vehicle fleet, every internal combustion engine vehicle requires a 12V lead acid SLI battery.

- Flooded at 57.6% maintaining majority through cost advantage for agricultural, industrial, and emerging market applications, where electrolyte maintenance is feasible: Flooded lead acid batteries' 57.6% majority reflects the fundamental economics of electrochemical energy storage, flooded batteries produce equivalent electrochemical performance at lower manufacturing cost than VRLA alternatives, making them the commercial choice wherever regular maintenance is operationally feasible, and ventilation requirements are manageable.

- Asia-Pacific at 41.5% through China's manufacturing dominance, India's growth, and Southeast Asia's solar storage and motorcycle SLI demand: Asia-Pacific's 41.5% market share reflects the region's structural role as both the world's largest lead acid battery manufacturer and the world's largest consumer, driven by the densest concentration of motorcycle and light vehicle fleets, telecom towers, and off-grid solar storage demand.

Lead Acid Battery Market Overview

The global lead acid battery market encompasses the design, manufacture, distribution, and servicing of electrochemical energy storage cells and batteries based on the lead-sulfuric acid electrochemical couple, across three primary product categories and two principal construction methodologies. Lead-acid batteries span an enormous capacity and application range.

The ecosystem integrates lead ore miners and secondary lead smelters, sulfuric acid manufacturers, separator and grid component suppliers, battery OEMs, automotive and industrial OEM buyers purchasing original equipment batteries, aftermarket distribution networks for replacement batteries, end users across automotive, telecom, UPS, industrial, and solar segments, and the critical battery collection and recycling infrastructure that closes the lead supply loop with 85%+ material recovery. Macroeconomic factors include industrialization, rapid urbanization, rising vehicle ownership, and increasing investments in power infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

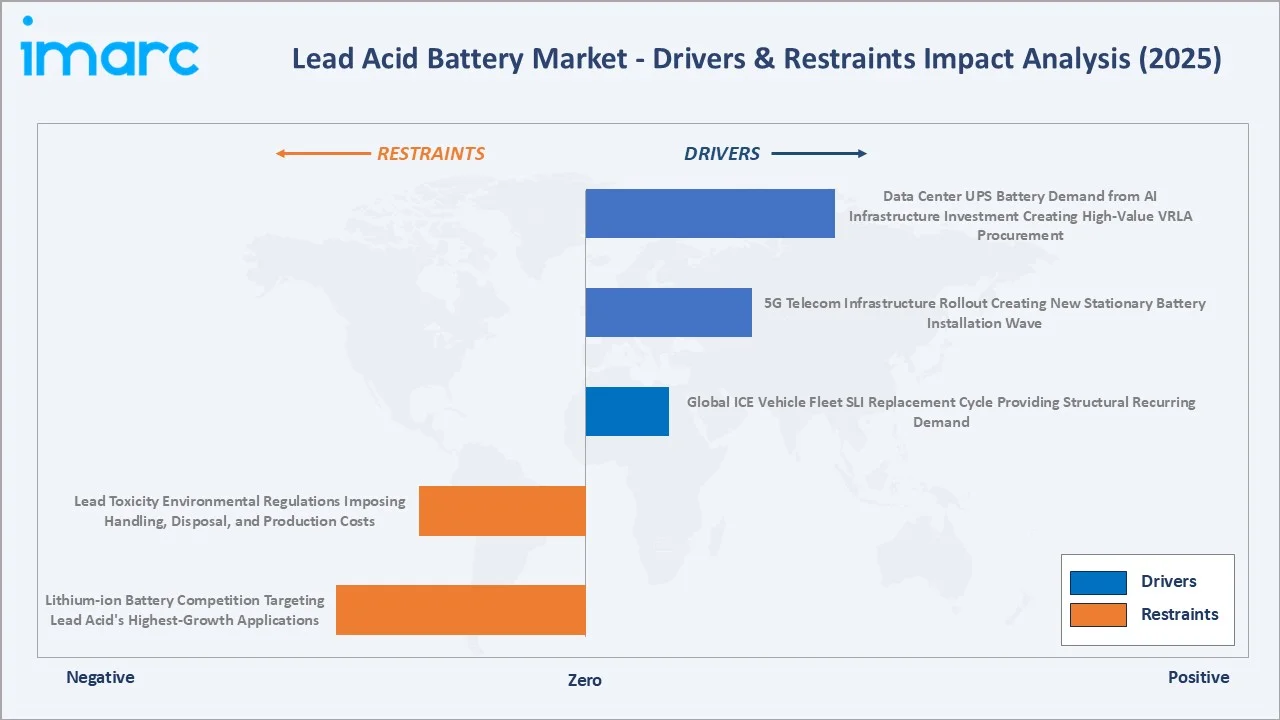

Market Drivers

- Global ICE Vehicle Fleet SLI Replacement Cycle Providing Structural Recurring Demand: The global passenger vehicle fleet rising from 1.4 billion today to 2.3 billion by 2050, creates an annual SLI battery replacement market that operates as a recurring demand base driven by fleet size, average battery life, and climate stress factors. In severe climate markets, SLI battery life is 3-4 years, creating a higher replacement frequency. In temperate markets, SLI battery life extends to 5-6 years.

- 5G Telecom Infrastructure Rollout Creating New Stationary Battery Installation Wave: Global 5G network deployment is the single most commercially significant new demand driver for stationary VRLA batteries since the 2000s-era 2G telecom tower expansion. 5G coverage reached 55% of the world’s population in 2025, up from 39% in 2022, requiring a high number of 5G base stations globally. Each 5G base station requires 48V VRLA backup battery systems of 100-400 Ah capacity, representing a high VRLA battery system value per site.

- Data Center UPS Battery Demand from AI Infrastructure Investment Creating High-Value VRLA Procurement: The artificial intelligence computing buildout (generative AI training infrastructure from OpenAI, Google, Meta AI, Microsoft Azure, requiring specialized GPU cluster data centers) is driving unprecedented data center construction investment. Global data center installed capacity growth, creating a VRLA UPS battery market growth of USD 1-2 Billion annually.

Market Restraints

- Lithium-ion Battery Competition Targeting Lead Acid's Highest-Growth Applications: The most commercially significant competitive threat to lead acid batteries is lithium iron phosphate (LiFePO4) batteries' ongoing cost reduction and performance improvement, making lithium competitive in the stationary backup power and motive (forklift) segments that represent lead acid's fastest-growing and highest-margin applications.

- Lead Toxicity Environmental Regulations Imposing Handling, Disposal, and Production Costs: Lead is classified as a hazardous substance under multiple international regulatory frameworks, creating a comprehensive regulatory burden on lead acid battery manufacturing, handling, and disposal. Secondary lead smelter compliance adds USD 50-200 per tonne in environmental compliance cost versus unregulated primary lead smelting in developing countries.

Market Opportunities

- Advanced Lead Carbon (PbC) Batteries Extending Lead Acid Performance into Partial State of Charge Applications: Advanced carbon-enhanced lead acid technologies represent the lead acid industry's most commercially significant technology innovation. PbC batteries provide 2-4x better partial state of charge (PSoC) cycling performance versus standard flooded lead acid and dramatically reduced sulfation at partial charge states, which is the primary failure mechanism for standard lead acid in solar applications.

- Solar Energy Storage in Emerging Markets Sustaining Deep-Cycle Lead Acid Demand Despite Lithium Competition: Africa's energy access challenge creates a structurally growing deep-cycle lead acid battery market for solar home systems, community microgrids, and agricultural pumping. India's rural household solar program similarly creates deep-cycle lead acid demand where VRLA deep-cycle batteries serve the cost-sensitive rural energy access segment.

Market Challenges

- Global EV Fleet Growth Progressively Displacing SLI Battery Demand Over the Long Term: While battery electric vehicles (BEVs) do not use 12V SLI lead acid batteries, eliminating the primary recurring revenue driver for SLI battery manufacturers in those vehicle categories, the pace of BEV adoption is creating a manageable transition challenge rather than an immediate existential threat.

- Chinese Manufacturing Over-Capacity Creating Global Market Price Competition: China's lead acid battery manufacturing overcapacity creates persistent pricing pressure in international markets as Chinese exporters compete for global share to absorb capacity beyond domestic consumption.

Emerging Market Trends

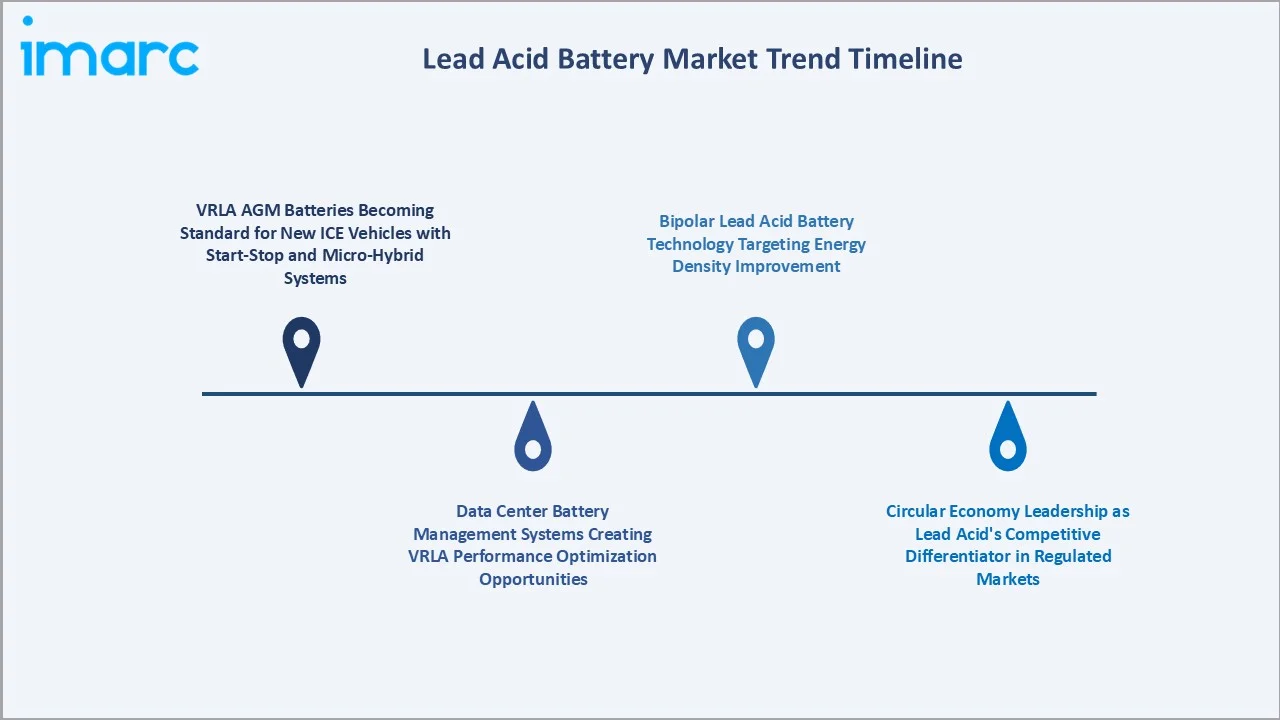

1. VRLA AGM Batteries Becoming Standard for New ICE Vehicles with Start-Stop and Micro-Hybrid Systems

The adoption of VRLA AGM batteries is emerging as automakers increasingly integrate start-stop and micro-hybrid technologies into internal combustion engine (ICE) vehicles. These batteries offer higher cycling performance, faster recharge capability, improved durability, and enhanced power support for advanced onboard electronics. In April 2026, Stryten Energy launched a new range of multi-terminal AGM batteries aimed at enhancing reliability across telecommunications and electric utility infrastructure applications. The E-Series AGM160 and AGM190 VRLA batteries are engineered to provide stable backup power, support extended discharge cycles, enable rapid charging, and maintain dependable performance even at high depths of discharge in demanding operating environments.

2. Data Center Battery Management Systems Creating VRLA Performance Optimization Opportunities

The increasing deployment of battery management systems in data centers is improving the performance, reliability, and lifespan of VRLA batteries used in backup power applications. Advanced monitoring technologies enable real-time tracking of battery health, temperature, charge cycles, and energy efficiency, helping operators reduce downtime and maintenance costs. This trend is driving demand for intelligent VRLA battery solutions that can support the growing power reliability requirements of hyperscale and enterprise data centers.

3. Circular Economy Leadership as Lead Acid's Competitive Differentiator in Regulated Markets

The strong recyclability of lead-acid batteries in regulated markets, where sustainability, waste management, and circular economy practices are becoming increasingly important. Manufacturers are emphasizing closed-loop recycling systems that recover and reuse lead, plastic, and electrolyte materials, helping reduce raw material dependency and environmental impact. This trend is strengthening the position of lead-acid batteries in automotive, industrial, and backup power applications where regulatory compliance and cost-efficient recycling infrastructure are critical factors.

4. Bipolar Lead Acid Battery Technology Targeting Energy Density Improvement

The development of bipolar lead-acid battery technology is emerging as manufacturers seek to improve energy density, charging efficiency, and overall battery performance. In February 2024, Terra Supreme Battery began production of its Group 31 battery at its manufacturing facility in the United States. The battery is based on the company’s composite grid bipolar AGM lead-acid technology, which is designed to enhance performance and efficiency in advanced energy storage applications. These advancements are expanding the potential use of lead-acid batteries in automotive, renewable energy storage, and industrial power applications.

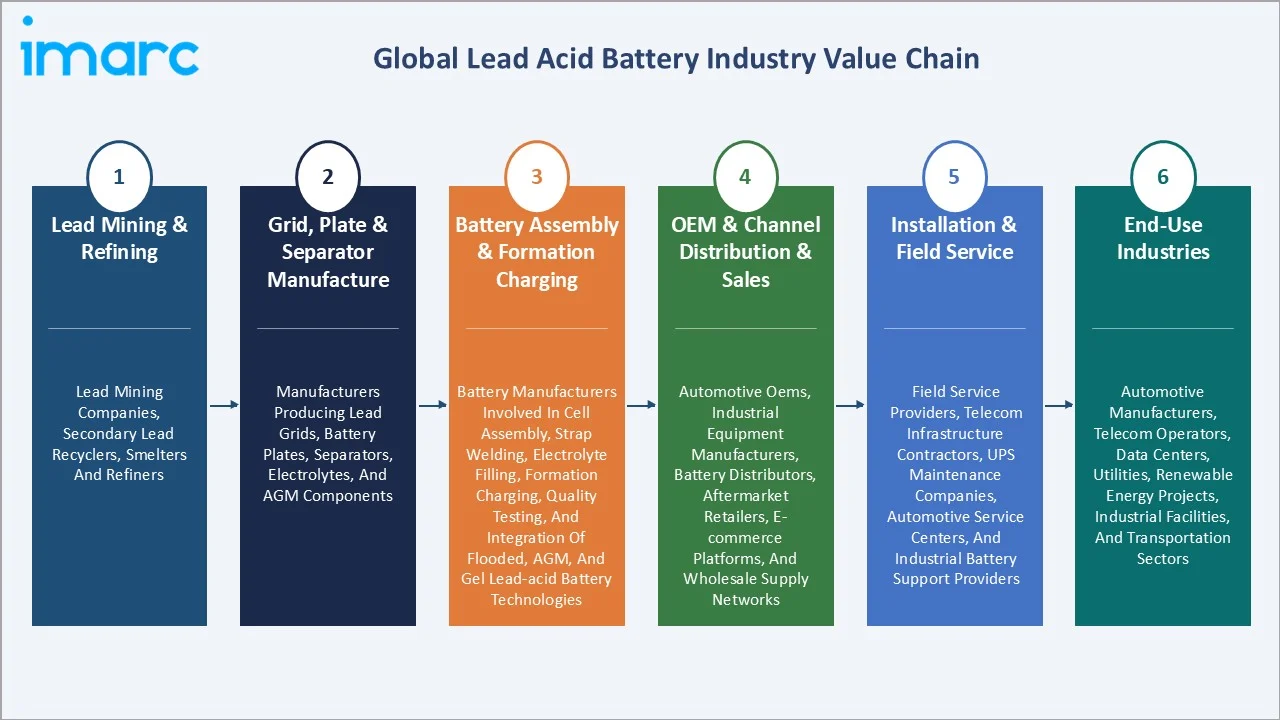

Industry Value Chain Analysis

The global lead acid battery value chain integrates lead mining and secondary smelting, grid and plate manufacturing, battery assembly and formation charging, OEM and channel distribution, installation and field service, and collection and recycling. Lead is the dominant raw material, making the lead supply chain the most strategically important value chain element for battery manufacturers. The secondary lead supply chain creates a closed-loop material cycle that provides cost stability, environmental compliance, and supply chain resilience relative to primary mined lead dependence.

|

Stage |

Key Participants |

|

Lead Mining & Refining |

Lead mining companies, secondary lead recyclers, smelters and refiners. |

|

Grid, Plate & Separator Manufacture |

Manufacturers producing lead grids, battery plates, separators, electrolytes, and AGM components. |

|

Battery Assembly & Formation Charging |

Battery manufacturers involved in cell assembly, strap welding, electrolyte filling, formation charging, quality testing, and integration of flooded, AGM, and gel lead-acid battery technologies. |

|

OEM & Channel Distribution & Sales |

Automotive OEMs, industrial equipment manufacturers, battery distributors, aftermarket retailers, e-commerce platforms, and wholesale supply networks. |

|

Installation & Field Service |

Field service providers, telecom infrastructure contractors, UPS maintenance companies, automotive service centers, and industrial battery support providers. |

|

End-Use Industries |

Automotive manufacturers, telecom operators, data centers, utilities, renewable energy projects, industrial facilities, and transportation sectors. |

The collection and recycling tier is uniquely important in the lead acid value chain, unlike most manufacturing industries where product end-of-life management is a cost center, lead acid battery recycling generates positive economic returns from recovered lead, recovered polypropylene, and recovered sulfuric acid. This positive recycling economics creates natural market incentives for battery collection even without regulatory mandates, explaining the industry's historically high collection rates that predated environmental regulation.

Technology Landscape in the Lead Acid Battery Industry

Advanced Plate and Grid Technology

Advanced plate and grid technologies are improving battery durability, conductivity, energy efficiency, and charge acceptance performance. Innovations such as thin plate pure lead designs, corrosion-resistant alloys, carbon-enhanced negative plates, and advanced AGM grid structures are enabling longer battery life and better cycling capability. These technologies are also supporting high-performance applications in automotive start-stop systems, industrial backup power, telecom infrastructure, and renewable energy storage.

VRLA Separator and Electrolyte Technology

Advancements in VRLA separator and electrolyte technologies are enhancing battery safety, efficiency, and maintenance-free operation. Improved absorbent glass mat (AGM) separators, gel electrolytes, and optimized electrolyte distribution systems are increasing charge retention, thermal stability, and deep-cycle performance. These innovations are supporting wider adoption of VRLA batteries in automotive start-stop vehicles, telecom backup systems, UPS applications, and renewable energy storage solutions.

Battery Management and Monitoring Technology

Battery management and monitoring technologies are enabling real-time tracking of battery health, charge levels, temperature, and performance efficiency. Advanced monitoring systems, IoT-enabled sensors, and predictive analytics are helping operators reduce downtime, optimize charging cycles, and extend battery lifespan across automotive, telecom, UPS, and data center applications. These technologies are also improving reliability, maintenance planning, and energy management in critical backup power systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

SLI |

46.8% |

2025 |

|

Construction Method |

Flooded |

57.6% |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

41.5% |

2025 |

By Product

SLI batteries lead at 46.8% market share (2025). SLI batteries provide starting current, lighting, and ignition power for ICE vehicles. The SLI market is structured across standard flooded, EFB Enhanced Flooded Battery, and AGM segments. Premium AGM and EFB are growing fastest within SLI as European and Japanese stop-start vehicle fleets age into first and second battery replacement cycles.

To access detailed market analysis, Request Sample

Stationary batteries at 30.7% grow fastest at ~4.2% CAGR through 5G telecom, data center, and solar storage demand. Stationary batteries provide uninterruptible power supply (UPS) backup for telecommunications, data centers, industrial controls, emergency lighting, and alarm systems. Motive batteries at 22.5% power electric forklifts, airport ground support equipment, electric golf carts, floor cleaning machines, and utility vehicles requiring deep-cycle energy delivery over 6-8 hour shift periods.

By Construction Method

Flooded batteries lead at 57.6% market share (2025). Flooded lead acid batteries use liquid sulfuric acid electrolyte in open or semi-sealed cells, requiring periodic distilled water addition to replace electrolyte lost through hydrogen and oxygen gas evolution during charging. Flooded batteries' manufacturing cost advantage, superior high-temperature performance for automotive SLI in tropical markets, and suitability for deep-discharge industrial motive applications sustain their majority share.

Valve Regulated Sealed Lead–acid Battery (VRLA) at 42.4% grows fastest at ~4.1% CAGR as telecom, UPS, and premium automotive applications expand. VRLA encompasses AGM (Absorbent Glass Mat: electrolyte absorbed in glass fiber mat, no free liquid, recombination valve maintains sealed operation) and Gel (silica gel electrolyte: no free liquid, better high-temperature and deep-cycle performance than AGM). VRLA's non-spillable classification under transport regulations, elimination of hydrogen gas evolution in normal operation, and complete maintenance-free operation sustain its growth relative to flooded construction.

Regional Market Insights

|

Region |

Share (2025) |

Key Lead Acid Battery Market Drivers & Characteristics |

|

Asia-Pacific |

41.5% |

Supported by strong automotive production, expanding telecommunications infrastructure, industrialization, and rising demand for backup power and energy storage solutions. |

|

Europe |

22.8% |

Characterized by advanced recycling infrastructure, stringent environmental regulations, strong adoption of start-stop vehicle technologies, and growing demand for industrial backup power systems. |

|

North America |

20.6% |

Driven by automotive aftermarket demand, data center expansion, telecom infrastructure growth, and widespread deployment of UPS and energy backup systems. |

|

Latin America |

8.3% |

Supported by rising vehicle ownership, increasing industrial activities, telecom network expansion, and growing demand for affordable energy storage and backup power solutions. |

|

Middle East and Africa |

6.8% |

Witnessing growth due to expanding power infrastructure, rising telecommunications investments, increasing automotive demand, and the need for reliable backup power systems in underserved regions. |

Asia-Pacific's 41.5% market leadership reflects China's dual role as the world's largest battery manufacturer and consumer, amplified by India's rapidly growing automotive and telecom markets, and Southeast Asia's motorcycle and off-grid solar storage demand. The region's competitive landscape is intensely price-driven in mass-market segments while simultaneously featuring the world's fastest-growing premium segments.

Europe, at 22.8%, is the regulatory sophistication leader, with the EU Battery Regulation creating compliance requirements that favor well-invested manufacturers with recycling programs. North America, at 20.6%, is characterized by the highest average selling price globally and world-leading collection infrastructure. Latin America, at 8.3%, is driven by Brazil and Mexico's automotive fleets and growing telecom infrastructure. Middle East and Africa, at 6.8%, is the fastest-growing region from a smaller base, driven by GCC standby power and Africa's solar energy access programs.

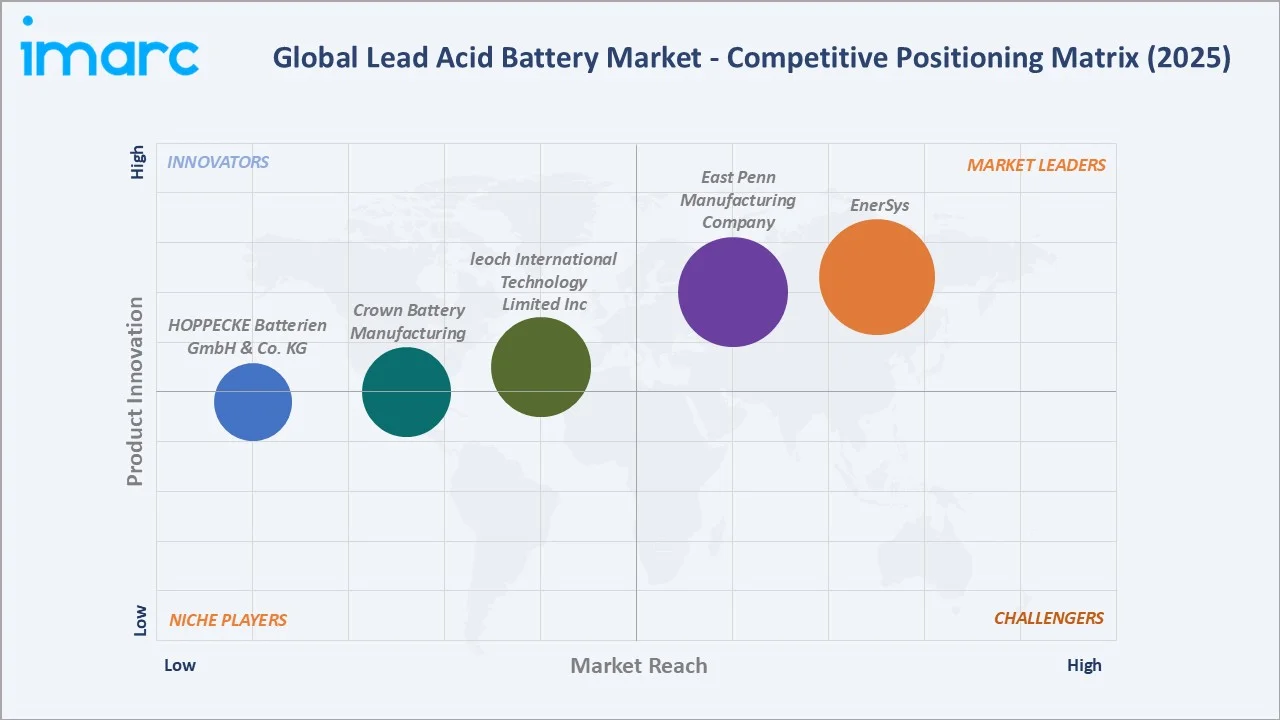

Competitive Landscape

The global lead acid battery competitive landscape is regionally segmented by application focus and geographic market orientation. North American and European premium manufacturers compete on technology differentiation, brand value, after-sales service, and recycling compliance in premium industrial and automotive markets. Asian manufacturers compete on volume, cost, and emerging market penetration. Indian manufacturers represent the growing premium domestic market challenge.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

EnerSys |

ODYSSEY Extreme Batteries, CYCLON Batteries, IRONCLAD Batteries |

Market Leader |

EnerSys is an industrial technology leader serving the global community with mission-critical stored energy solutions that meet the growing demand for energy efficiency, reliability and sustainability. |

|

East Penn Manufacturing Company |

INTIMIDATOR AGM, INTIMIDATOR AGM with EHP, DEKA ULTIMATE, GOLD and STANDARD, DEKA ULTIMATE EFB, Deka HRC |

Market Leader |

East Penn's lead-acid batteries are one of the most recyclable products on the planet. |

|

leoch International Technology Limited Inc |

VRLA-AGM Battery for Telecom, Pure Lead Battery for Telecom, VRLA-AGM Battery for UPS, Pure Lead Battery for UPS |

Established Player |

Network energy solutions from Leoch are widely used in communication networks and data centers at all levels to provide a key guarantee for the normal operation of communication networks. |

|

Crown Battery Manufacturing |

Boltage Series Industrial Lead Acid Battery |

Established Player |

Unlike most bolt-on battery terminal connectors that rely on a rubber grommet compression seal, Boltage features a permanent lead weld and seal from post to floating bushing. |

|

HOPPECKE Batterien GmbH & Co. KG |

grid | Xtreme VR (pure lead), grid | Xtreme VR (green series) |

Established Player |

HOPPECKE grid | Xtreme VR pure lead batteries have similar lifetime projections to comparable LFP solutions. |

The competitive pressure from lithium-ion substitution is creating strategic divergence among lead acid manufacturers: some are investing in lithium-ion capacity alongside lead acid, while others are doubling down on lead acid technology advancement as their strategic focus.

Key Company Profiles

EnerSys

EnerSys is one of the world's largest industrial battery manufacturers. EnerSys is a leading industrial technology company that provides mission-critical stored energy solutions to support rising global needs for energy efficiency, reliability, and sustainability.

- Key Products: ODYSSEY Extreme Batteries, CYCLON Batteries, IRONCLAD Batteries.

- Recent Developments: In November 2024, EnerSys presented its advanced floor care power solutions portfolio at ISSA Show North America 2024, including the iQ Mini battery monitoring device and its maintenance-free NexSys TPPL (Thin Plate Pure Lead) battery range. The showcase highlights the company’s focus on intelligent battery monitoring and high-performance energy storage solutions for industrial applications.

- Strategic Focus: Focused on expanding advanced lead-acid energy storage solutions, intelligent battery monitoring technologies, and maintenance-free industrial power systems for telecom, data center, material handling, and backup power applications.

East Penn Manufacturing Company

East Penn Manufacturing is the largest privately-held and employee-owned battery manufacturer in the United States.

- Key Products: INTIMIDATOR AGM, INTIMIDATOR AGM with EHP, DEKA ULTIMATE, GOLD and STANDARD, DEKA ULTIMATE EFB, Deka HRC.

- Recent Developments: In October 2025, East Penn Manufacturing introduced its Armor Alloy Technology range to strengthen its presence in the expanding data center market. The technology enhances the company’s Deka HRC lead battery portfolio by combining pure lead grids with a proprietary engineered alloy blend designed to improve durability, conductivity, and overall battery performance for hyperscale data center applications.

- Strategic Focus: Strengthening its lead-acid battery portfolio through advanced alloy technologies, improved energy reliability, and expansion into high-demand sectors such as hyperscale data centers and industrial backup power systems.

Market Concentration Analysis

The global lead acid battery market exhibits moderate concentration at the premium segment level and high fragmentation at the total market level. The top 5 global manufacturers collectively account for approximately 35-40% of global market revenues. This moderate concentration reflects the market's geographic and application segmentation. At the high-volume Asian manufacturing level, Chinese manufacturers collectively produce 60%+ of global battery units but generate a disproportionately smaller share of global market revenues due to e-bike and motorcycle SLI battery average selling prices.

Market concentration at the premium VRLA segment level is higher. The competitive landscape is expected to gradually consolidate through 2034 as lithium-ion substitution pressure reduces the number of viable stand-alone lead acid manufacturers, and the EU Battery Regulation's recycling compliance costs create barriers for smaller manufacturers without closed-loop lead supply chains.

Investment & Growth Opportunities

Highest Growth Segments

Stationary VRLA batteries (~4.2% CAGR driven by 5G, data center, solar), motive VRLA/AGM batteries (~3.8% CAGR for electric forklift applications), advanced carbon-enhanced lead acid for solar and grid applications (~10-15% CAGR from small base), VRLA construction method (~4.1% CAGR across applications), and AGM/EFB stop-start automotive battery replacement segment (~6-8% CAGR as European and Japanese stop-start fleets age into replacement cycles) represent the global lead acid battery market's highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The circular economy infrastructure investment represents the lead acid industry's most financially attractive emerging opportunity. Each 100,000-tonne annual capacity secondary lead smelter represents high capital investment generating 20-25% ROI from lead recovery value at USD 2,000-2,500 per tonne, regulatory compliance benefit, and competitive battery manufacturing cost advantage.

Investment Themes

- 5G telecom battery replacement wave as recurring VRLA procurement cycle: The global 5G base stations being deployed 2022-2030 each require VRLA battery replacement every 3-5 years, creating an annual replacement market of USD 3-8 Billion at peak replacement cycle.

- Data center AGM/VRLA premium market development driven by AI infrastructure build-out: Each MW of AI computing infrastructure requires USD 200,000-1,000,000 in VRLA UPS battery backup, and the USD 200+ Billion committed data center capex for 2024-2026 creates a USD 2-4 Billion VRLA battery procurement opportunity concentrated in a relatively small number of hyperscale customers and co-location operators.

Future Market Outlook (2026-2034)

The global lead acid battery market is projected to grow from USD 36.84 Billion in 2025 to USD 50.28 Billion by 2034, delivering a 3.41% CAGR over the forecast period. The market's anchor value of USD 43.57 Billion in 2030 represents a global lead acid battery industry where 5G telecom tower battery replacement cycles are adding USD 500 Million-1 Billion annually in VRLA replacement demand, North American and European stop-start vehicle AGM replacement cycles are generating USD 3-5 Billion in premium SLI battery aftermarket revenue, and the circular economy profile of lead acid has become a EU battery regulation compliance advantage that differentiates established lead acid manufacturers from lithium-ion competitors struggling with nascent end-of-life recycling infrastructure.

Three structural forces define global lead acid battery market growth through 2034 with high confidence: the global ICE vehicle fleet's replacement cycle is irreversible in the forecast period; the global data center and telecommunications infrastructure is committed to lead acid VRLA as the standard battery chemistry for standby power backup based on proven float service life, installation density, and total cost of ownership that lithium-ion cannot yet match in pure standby applications at competitive cost; and lead acid battery technology advancement is demonstrating that the 150-year-old electrochemistry has fundamental improvement headroom that will periodically extend its competitive position in applications where lithium-ion advocates prematurely declared victory.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Directors of Sales and Product Management; battery procurement managers, UPS and data center infrastructure managers; automotive battery engineering managers; battery recycling operations managers; and national policy representatives.

Secondary Research

Secondary research encompassed Battery Council International (BCI) Annual Report 2025; International Lead Association (ILA) Lead Facts report 2025; individual company annual reports; EUROBAT European Battery Association statistics; ITU (International Telecommunication Union) 5G infrastructure statistics; IEA World Energy Outlook 2025 for off-grid solar storage data; and US National Emissions Inventory for secondary lead smelting. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up product type and construction method models calibrated against BCI battery shipment data, Chinese MIIT battery production statistics, individual company revenue disclosures, and automotive fleet registration data. Key forecast inputs include global ICE vehicle fleet size projections, BEV adoption S-curve by country, 5G base station deployment timeline by region, data center construction pipeline, off-grid solar system deployment in emerging markets, and lead metal price forecasts.

Lead Acid Battery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Lead Acid Battery Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | SLI, Stationary, Motive |

| Construction Methods Covered | Flooded, Valve Regulated Sealed Lead–acid Battery (VRLA) |

| Sales Channels Covered | OEM, Aftermarket |

| Applications Covered | Automotive, UPS, Telecom, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | EnerSys, East Penn Manufacturing Company, leoch International Technology Limited Inc, Crown Battery Manufacturing, HOPPECKE Batterien GmbH & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the lead acid battery market from 2020-2034.

- The research report study provides the latest information on the market drivers, challenges, and opportunities in the global lead acid battery market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the lead acid battery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Lead Acid Battery Market Report

The global lead acid battery market reached USD 36.84 Billion in 2025, driven by the global ICE vehicle fleet SLI replacement cycle, 5G telecom tower VRLA backup expansion, data center UPS battery demand from AI infrastructure investment, solar energy storage in emerging markets, and stop-start AGM automotive battery adoption in Europe, Japan, and China.

The market grows at 3.41% CAGR during 2026-2034, reaching USD 50.28 Billion by 2034, driven by stationary VRLA battery growth, VRLA construction method growth, motive battery expansion, and the premium SLI replacement cycle in European and Japanese stop-start vehicle fleets.

SLI batteries lead at 46.8% through the global ICE and hybrid vehicle fleet's universal 12V starting power requirement at a cost-effective battery.

Flooded leads at 57.6% through cost advantage for automotive SLI, industrial motive, and telecom central office stationary applications.

Asia-Pacific leads at 41.5% through China's manufacturing dominance, India's rapidly growing automotive and telecom markets, and Southeast Asia's motorcycle SLI and off-grid solar demand. China's e-bike battery market alone represents USD 3-5 Billion within the Asia Pacific's regional total.

Leading companies include EnerSys, East Penn Manufacturing Company, leoch International Technology Limited Inc, Crown Battery Manufacturing, and HOPPECKE Batterien GmbH & Co. KG, among others.

The market is projected to reach approximately USD 43.57 Billion by 2030, with 5G telecom tower battery replacement cycles annual VRLA demand, data center AI infrastructure creating annual VRLA UPS procurement, European and Japanese stop-start AGM replacement reaching peak volume, and carbon-enhanced batteries entering commercial scale for solar and grid applications.

5G network deployment is the most significant new demand driver for stationary VRLA batteries since the 2G network expansion in the 2000s. Each 5G base station requires 2-4x more backup capacity than its 4G predecessor, and the global 5G base station deployment creates high cumulative VRLA battery installation value per site.

Three priority opportunities: 5G telecom VRLA replacement cycle investment positioning; data center premium VRLA market development for AI infrastructure; and secondary lead recycling infrastructure in South/Southeast Asia.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)