Lobster Market Size, Share, Trends and Forecast by Species, Weight, Product Type, Distribution Channel, and Region, 2026-2034

Global Lobster Market Size, Share, Trends & Forecast (2026-2034)

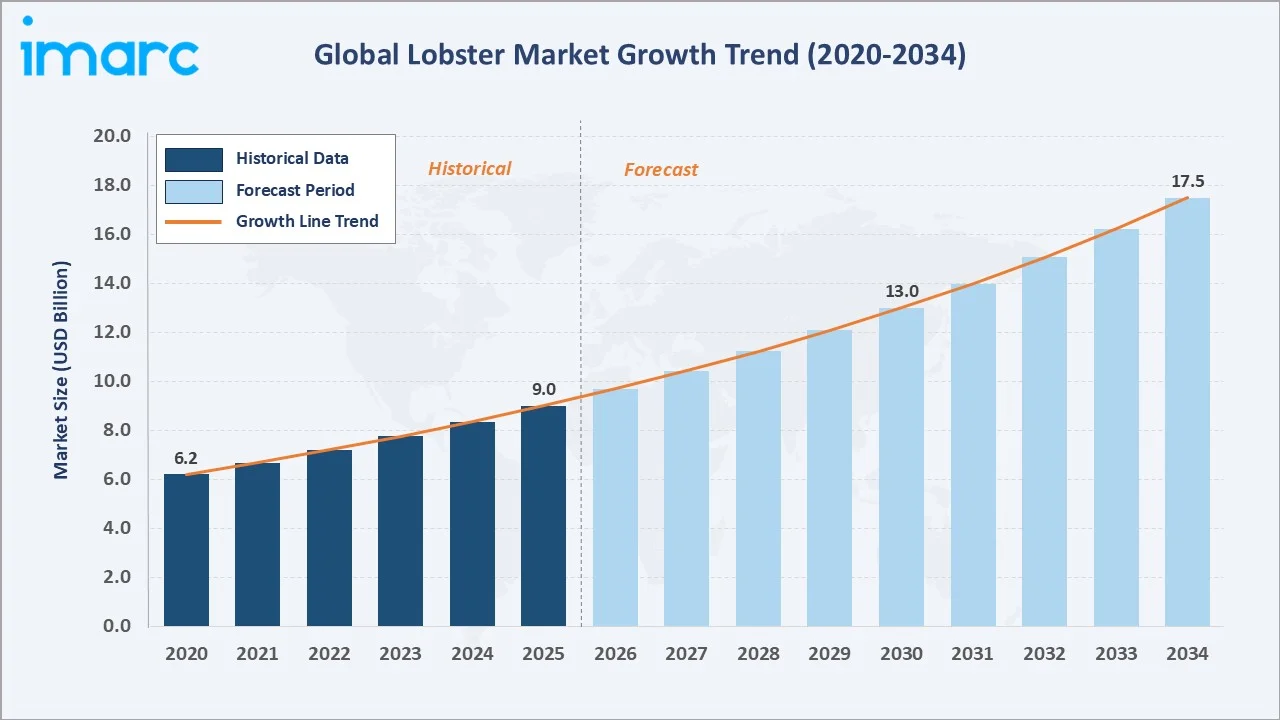

The global lobster market size reached USD 9.0 Billion in 2025 and is projected to reach USD 17.5 Billion by 2034, exhibiting a CAGR of 7.7% during 2026-2034. The market is propelled by rising global demand for premium seafood, the rapid expansion of the foodservice sector, growing consumer awareness of lobster's nutritional value.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.0 Billion |

|

Market Size (2020) |

USD 6.2 Billion |

|

Market Size (2030) |

USD 13.0 Billion |

|

Forecast Market Size (2034) |

USD 17.5 Billion |

|

CAGR (2026-2034) |

7.7% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

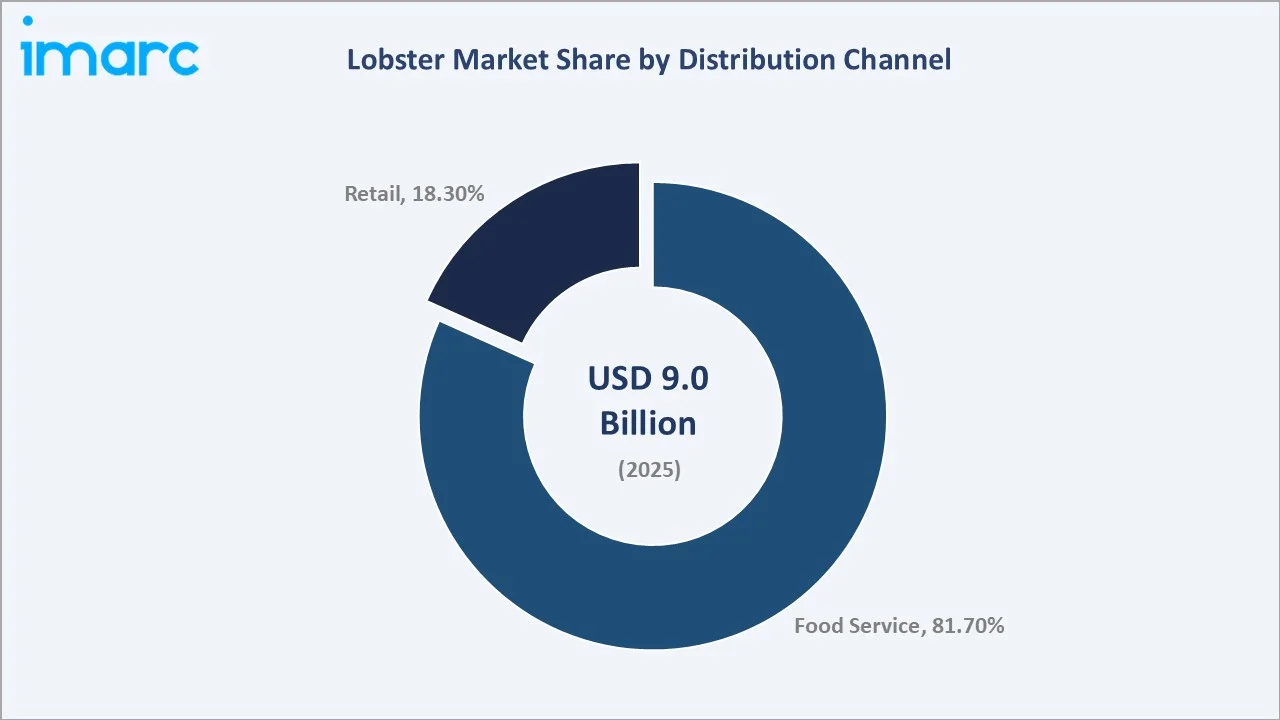

Largest Distribution Channel |

Food Service (81.7%, 2025) |

|

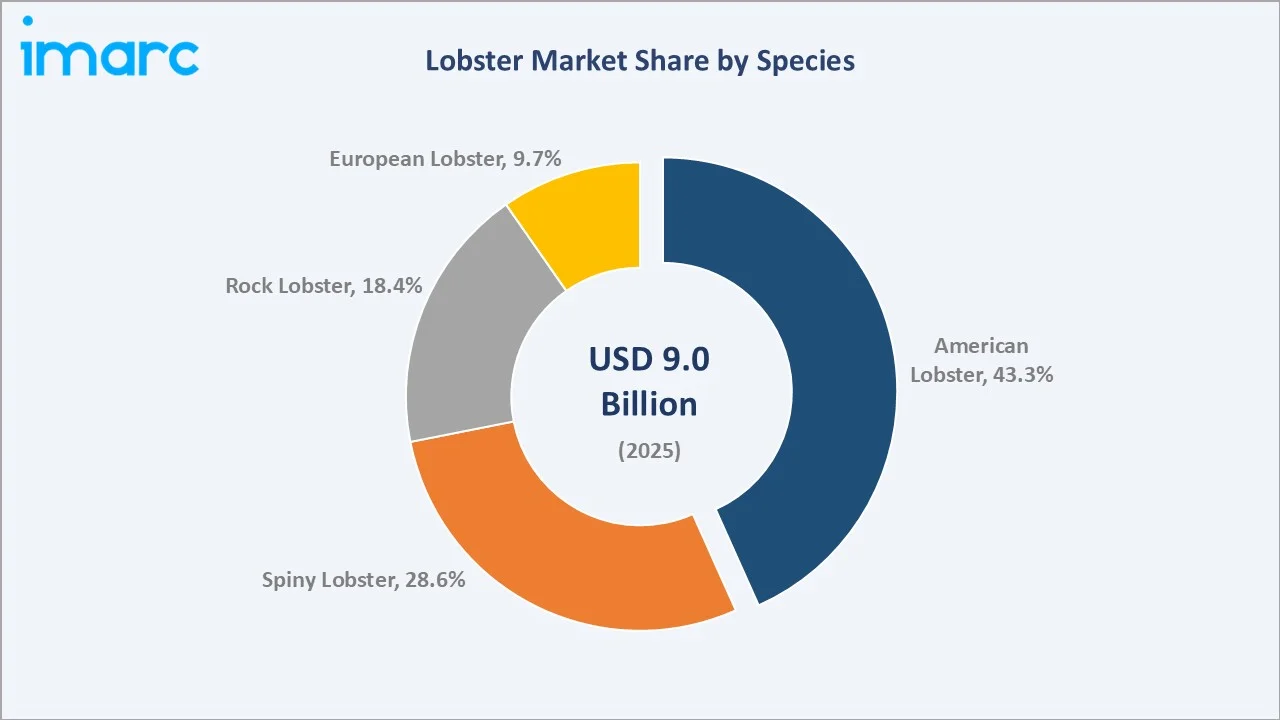

Leading Species |

American Lobster (43.3%, 2025) |

|

Largest Region |

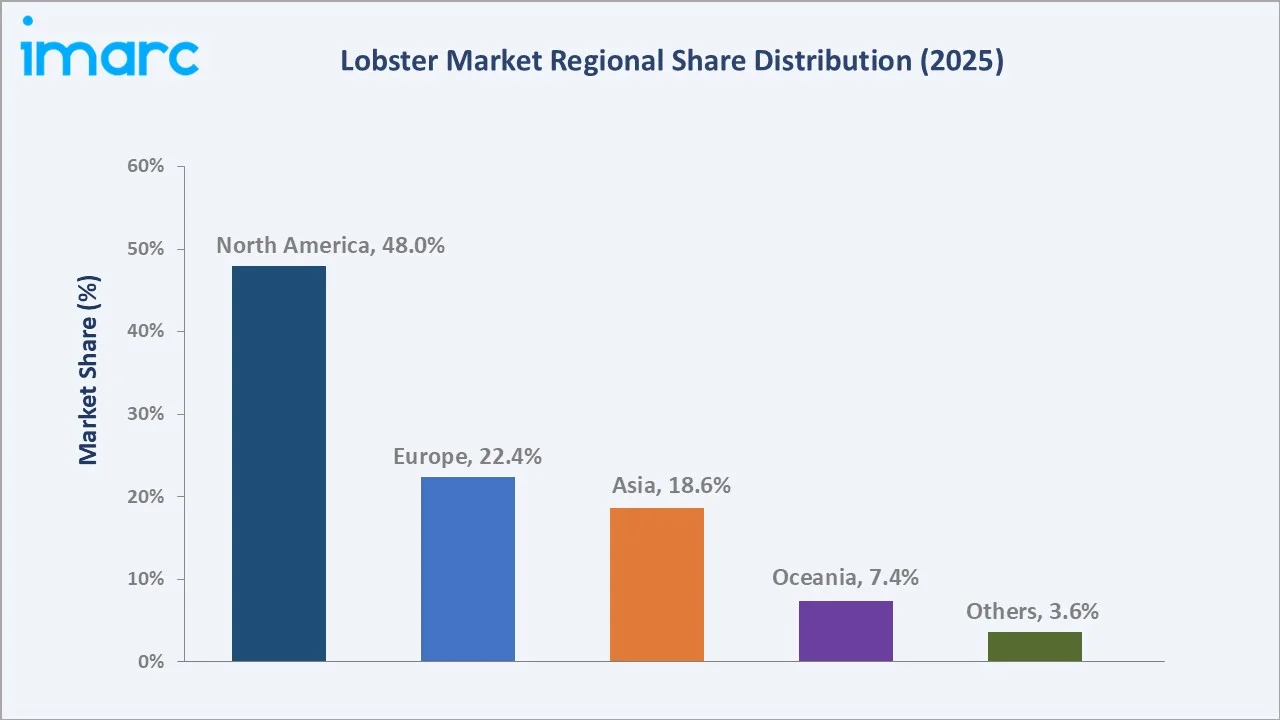

North America (~48.0% share, 2025) |

North America dominates the global lobster market, contributing 48.0% of revenues in 2025. Growth is supported by a well-established fishing heritage, strong institutional supply chains, and high consumer demand across restaurants, hotels, and retail channels.

To get more information on this market, Request Sample

Premium dining and retail consumption further drive market expansion, with American lobster as the most popular species. Technological advancements in aquaculture, processing, and cold-chain logistics enhance product quality, availability, and export potential, reinforcing North America’s leadership in the global lobster industry.

Executive Summary

The global lobster market demonstrates robust and sustained growth, underpinned by a structural shift in consumer preference toward premium, protein-rich seafood. Valued at USD 9.0 Billion in 2025, the market is forecast to reach USD 17.5 Billion by 2034 at a CAGR of 7.7% during 2026-2034.

The Food Service segment leads with an 81.7% distribution channel share, reflecting lobster's enduring position as a cornerstone ingredient in fine dining, hotel buffets, and casual seafood restaurants.

Asia is the fastest-emerging consumption frontier at 18.6%, powered by China's expanding middle-class appetite for luxury seafood. Looking ahead, the lobster market growth forecast through 2034 is anchored by sustainability-driven supply chain investments, aquaculture innovation, and the growing global appetite for traceable, responsibly sourced premium seafood.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel Segment |

Food Service– 81.7% share (2025) |

|

Second Distribution Channel Segment |

Retail – 18.3% share (2025) |

|

Largest Species Segment |

American Lobster – 43.3% share (2025) |

|

Second Species Segment |

Spiny Lobster– 28.6 % share (2025) |

|

Leading Region |

North America – 48.0% revenue share (2025) |

|

Top Companies |

Clearwater Seafoods, High Liner Foods, East Coast Seafood Group, Tangier Lobster Co. Ltd, Supreme Lobster & Seafood, Boston Lobster Company, Geraldton Fishermen's Co., Pescanova España, S.L.U, Thai Union Manufacturing Company Ltd. |

|

Market Opportunity |

Rising Premium Seafood Demand, and Expansion of Foodservice Industry |

Global Lobster Market Overview

The global lobster market size reached USD 9.0 Billion in 2025 and is projected to reach USD 17.5 Billion by 2034, exhibiting a CAGR of 7.7% during 2026-2034.

The global lobster market is experiencing robust growth, driven by rising seafood consumption, expanding aquaculture production, and increasing demand for premium, high-protein foods. North America dominates the market with a 48% share, followed by Europe (22.4%) and Asia (18.6%), while Oceania and other regions account for smaller portions.

Food service remains the primary distribution channel, capturing 81.7% of the market, compared with 18.3% through retail. Among species, American lobster leads with a 43.3% share, followed by spiny lobster (28.6%), rock lobster (18.4%), and European lobster (9.7%). Whole lobster products dominate the market at 72.8%, with the most common size range being 0.5–0.75 lbs, representing 42.4% of sales.

Market Dynamics

To evaluate market opportunities, Request Sample

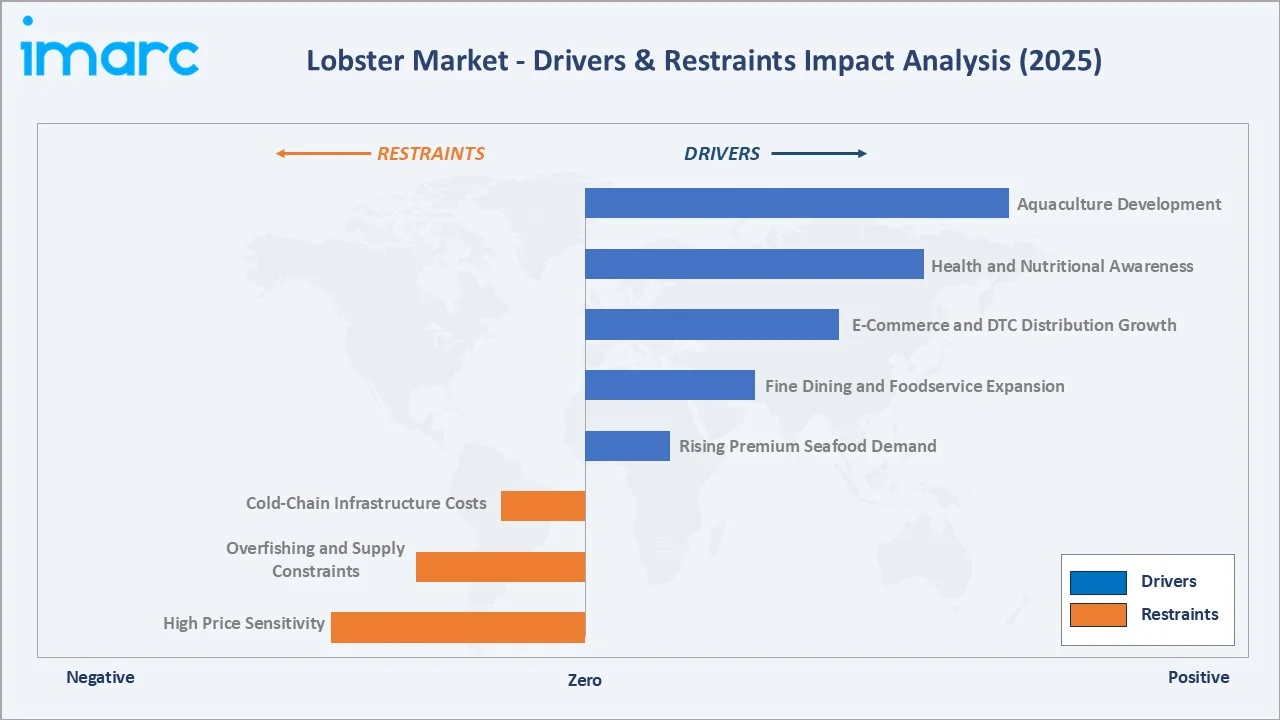

Market Drivers

- Rising Premium Seafood Demand: Growing global consumer aspiration for luxury protein has elevated lobster from a seasonal indulgence to a year-round premium staple across fine dining, hospitality, and retail channels globally.

- Fine Dining and Foodservice Expansion: The proliferation of upscale restaurant chains and hotel buffet culture - especially across Asia and the Middle East - is driving consistent institutional demand for live and processed lobster products.

- E-Commerce and DTC Distribution Growth: Advances in cold-chain logistics and overnight shipping capabilities have enabled direct-to-consumer seafood platforms to reach inland markets previously inaccessible to fresh lobster supply.

- Health and Nutritional Awareness: Lobster's profile as a high-protein, low-fat, omega-3-rich seafood aligns strongly with global health and wellness dietary trends, driving consumer preference particularly among affluent demographics.

Market Restraints

- High Price Sensitivity: Lobster's premium price point limits penetration in price-sensitive consumer segments and restricts broader retail adoption outside affluent consumer demographics.

- Overfishing and Supply Constraints: Regulatory quotas, seasonal restrictions, and sustainability-driven harvest limits constrain supply growth in key fishing regions including the Gulf of Maine and European waters.

- Cold-Chain Infrastructure Costs: Maintaining live lobster quality through extended logistics chains requires significant refrigeration investment, adding cost pressure that limits market expansion in underdeveloped logistics markets.

Market Opportunities

- Aquaculture Development: Advancements in closed-system hatchery technology and land-based aquaculture offer significant potential to supplement wild-catch supply, reduce seasonal volatility, and serve new markets year-round.

- Emerging Asian Market Expansion: China, India, and Southeast Asian nations represent high-growth import markets where rising middle-class incomes and a deepening premium food culture are creating rapidly expanding lobster demand.

- Product Innovation and Value-Added Formats: The development of pre-cooked, frozen, and ready-to-eat lobster products targeting convenience-driven consumers broadens addressable market segments beyond traditional live lobster buyers.

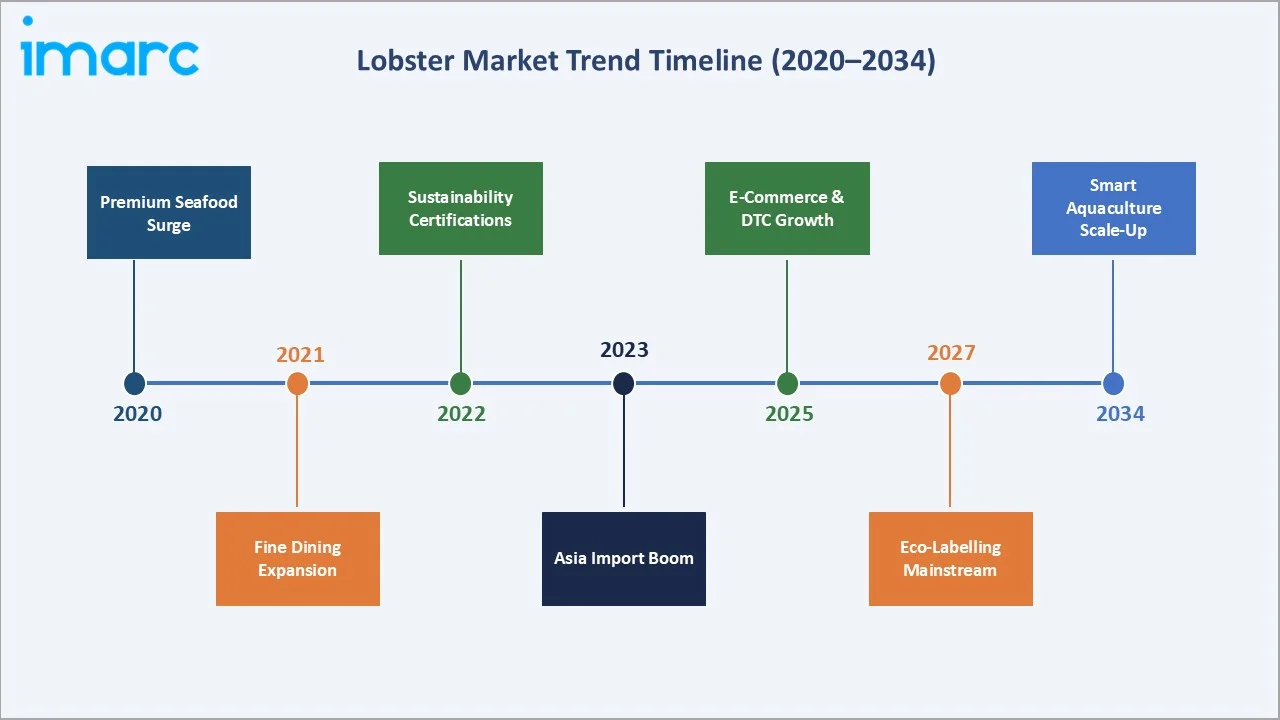

Emerging Market Trends

Premiumization and Fine Dining Expansion

The global appetite for premium dining experiences is reshaping the lobster industry at its core. Consumers across North America, Europe, and Asia are increasingly associating lobster with celebratory occasions, gourmet cuisine, and upscale hospitality experiences. This trend is fuelling sustained demand for live and whole lobster products at restaurants, luxury hotels, and high-end retail outlets.

Surge in E-Commerce and Online Seafood Delivery

The rapid expansion of digital commerce platforms is fundamentally transforming lobster distribution dynamics across major global markets. E-commerce channels offer consumers direct access to live, fresh, and processed lobster products with overnight shipping capabilities, dismantling traditional geographic barriers that previously confined premium seafood to coastal markets.

Sustainability Certifications and Responsible Sourcing

Consumer awareness of environmental responsibility is reshaping procurement strategies across the lobster supply chain, with sustainability credentials increasingly influencing purchasing decisions at both institutional and retail levels.

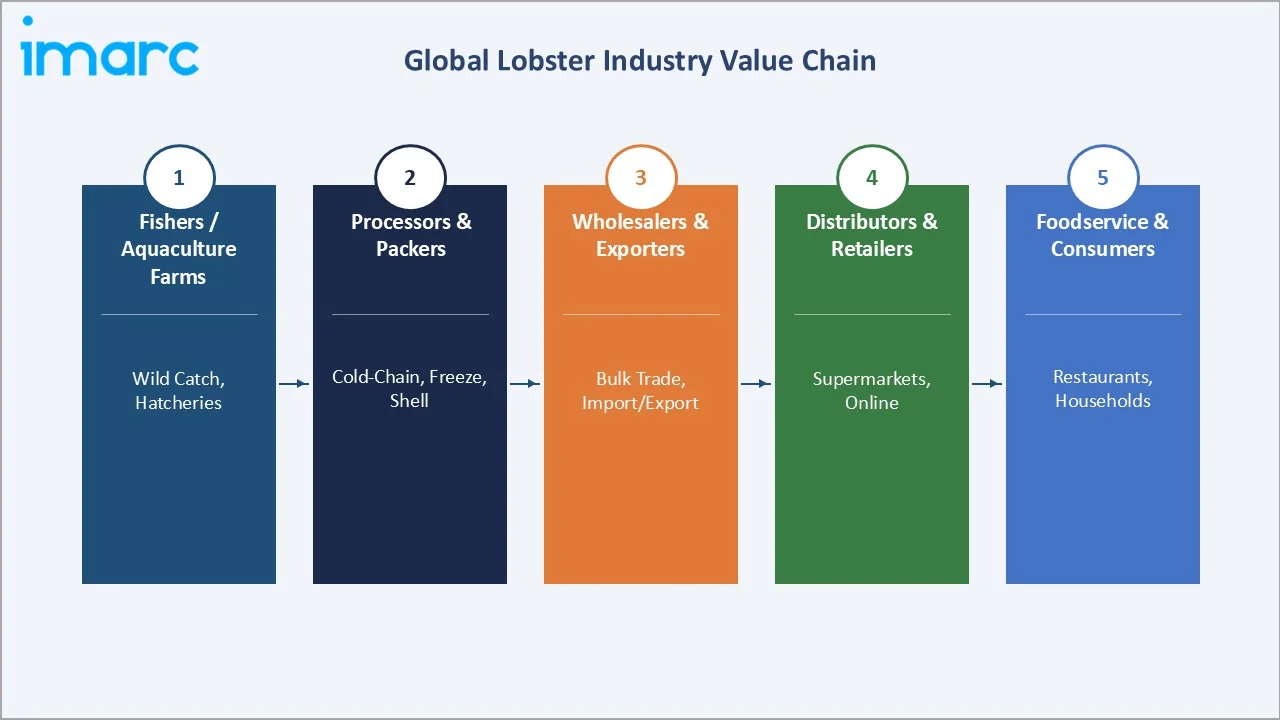

Lobster Industry Ecosystem & Value Chain

The global lobster industry operates through a sophisticated, geographically distributed value chain spanning primary harvesting operations, advanced cold-chain processing, international trade logistics, and multi-channel distribution to end consumers.

Technology Landscape in the Lobster Industry

- Aquaculture and Hatchery Innovations: Hatchery technology has advanced significantly to improve survival rates and growth performance of lobster larvae. Recirculating Aquaculture Systems (RAS) and biofloc systems provide controlled water quality and pathogen management. Selective breeding programs focus on disease resistance, rapid growth, and shell quality, while automated feeding systems optimize nutrition delivery, reduce feed waste, and enhance overall production efficiency.

- Sustainable Feed and Nutrition Technologies: Feed formulations are evolving to incorporate alternative proteins, algae, and krill-based ingredients, reducing environmental impact. Microencapsulated feeds improve nutrient absorption and minimize leaching into water. Feed management software monitors consumption patterns for improved feed conversion ratios, while functional additives, such as probiotics and immune boosters, support lobster health and disease resistance.

- Digital Monitoring and IoT Applications: IoT-enabled water sensors track temperature, salinity, oxygen, and pH in real time, while AI-based predictive analytics forecast growth rates, mortality, and optimal harvest timing. Remote monitoring platforms allow farm managers to adjust feeding and environmental controls from anywhere, and integrated dashboards consolidate water quality, feed, and growth metrics for optimized decision-making.

Global Lobster Market Industry Segmentation

The market has been categorized based on distribution channel and species.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Species |

American Lobster |

43.3% |

2025 |

|

Weight |

0.5-0.75lbs |

42.4% |

2025 |

|

Product Typ |

Whole lobster |

72.8% |

2025 |

|

Distribution Channel |

Food Service |

81.7% |

2025 |

|

Region |

North America |

48.0% |

2025 |

By Distribution Channel:

To access detailed market analysis, Request Sample

Food Service dominates the global lobster distribution channel landscape with an 81.7% market share in 2025, reflecting the enduring role of foodservice operators - including fine dining establishments, casual seafood restaurants, hotel chains, and institutional caterers - as the primary consumption channel for lobster globally.

In the U.S., food spending reached a high of $2.57 trillion in 2023, according to a new report from USDA’s Economic Research Service (ERS), validating the scale of opportunity for lobster within the foodservice ecosystem.

By Species:

American Lobster holds the largest species share at 43.3% in 2025, driven by its prolific supply from the Gulf of Maine and Canadian Maritime Provinces, its prized sweet and tender meat quality, and deep-rooted consumer familiarity in North American and European markets.

Regional Market Insights

The global lobster market forecast demonstrates differentiated growth patterns across regions, with established markets in North America and Europe maintaining volume leadership while Asia and Oceania emerge as high-growth frontiers. The following regional breakdown reflects 2025 revenue share data.

|

Region |

Market Share (2025) |

Key Growth Drivers |

|

North America |

48.0% |

Established fisheries, premium retail, export capacity |

|

Europe |

22.4% |

Fine dining culture, sustainability regulations, gourmet retail |

|

Asia |

18.6% |

Rising middle class, import growth, luxury dining |

|

Oceania |

7.4% |

Rock lobster exports, aquaculture investment, China trade |

|

Others |

3.6% |

Emerging markets, growing seafood consumption |

North America accounts for 48.0% of the global lobster market in 2025, representing the world's largest and most mature lobster production and consumption region. In November 2024, Sea Grant's American Lobster Initiative awarded USD 5.4 Million to fund 15 research and outreach projects focused on lobster growth, ecosystem impacts, and socioeconomic sustainability.

Asia represents 18.6% of the global lobster market in 2025and is positioned as the most dynamic growth region through the forecast period. China leads regional demand. In 2024, China's lobster imports from Vietnam surged 39%,

Competitive Landscape

The report provides a comprehensive analysis of the competitive landscape in the lobster market with detailed profiles of all major companies, including:

|

Company Name |

Brand / Division |

Market Position |

Core Strength |

|

Clearwater Seafoods |

Clearwater |

Market Leader |

Integrated operations, sustainability certifications, 40+ country exports |

|

High Liner Foods |

High Liner |

Leader |

Value-added frozen seafood, North American retail & food service reach |

|

East Coast Seafood Group |

East Coast Seafood |

Leader |

Full Maine supply chain integration, institutional food service supply |

|

Tangier Lobster Co. Ltd |

Tangier |

Challenger |

Atlantic Canada fisheries; significant US and Asian export operations |

|

Supreme Lobster & Seafood |

Supreme Lobster |

Challenger |

Midwest USA distribution leader; premium fresh and frozen lobster supply |

|

Boston Lobster Company |

Boston Lobster |

Challenger |

Live lobster wholesale; institutional food service and export distribution |

|

Geraldton Fishermen's Co. |

GFC |

Regional Leader |

Western Rock Lobster world-class export fishery; premium Asian market access |

|

Pescanova España, S.L.U. |

Pescanova |

Challenger |

European seafood processing; frozen lobster distribution across EU markets |

|

Thai Union Manufacturing Company Ltd. |

Chicken of the Sea / John West |

Emerging |

Asian seafood processing scale; growing shellfish and lobster integration |

The global lobster market exhibits a moderately concentrated competitive structure. A small group of large-scale processors and exporters dominate international trade flows particularly in North American supply chains and premium Asian export segments.

Competitive differentiation increasingly hinges on sustainability credentials, supply chain integration depth, cold-chain reliability, and strategic access to Asian growth markets. Consolidation is accelerating, with cross-industry M&A activity reflecting the premium lobster category's attractiveness to seafood companies seeking to diversify and access high-growth demand markets.

Key Company Profiles

Clearwater Seafoods

Clearwater Seafoods, headquartered in Halifax, Nova Scotia, is one of North America's largest vertically integrated seafood companies, with globally recognized lobster operations and a diversified shellfish license portfolio spanning Canadian Atlantic waters.

- Product Portfolio: Atlantic lobster (live, fresh, and frozen formats), sea scallops, surf clams, snow crab, and coldwater shrimp.

- Recent Developments: In May 2023, Clearwater filed for a 72-tonne annual quota increase in Nova Scotia's Lobster Fishing Area 41, reflecting active capacity expansion and growing demand from premium export markets.

- Strategic Focus: Sustainability certification leadership across its shellfish portfolio, premium positioning in Asian markets (particularly China and Japan), and continued investment in cold-chain logistics and traceability technology to support quality differentiation.

High Liner Foods

High Liner Foods, headquartered in Lunenburg, Nova Scotia, is a leading North American value-added frozen seafood manufacturer with established lobster processing and distribution capabilities serving retail and food service customers across the United States and Canada.

- Product Portfolio: Lobster-based frozen meals & entrées, breaded & battered seafood, and premium frozen shellfish products.

- Recent Developments: In June 2025, High Liner Foods announced its acquisition of the Mrs. Paul's and Van de Kamp's brands of frozen breaded and battered fish products from Conagra Brands, which closed on June 30 at the adjusted purchase price of USD $42.4 million.

- Strategic Focus: Premiumization of lobster-based frozen meal formats, leveraging its broad North American distribution network to capture at-home premium seafood consumption growth, and deepening food service channel penetration through value-added product innovation.

East Coast Seafood Group

East Coast Seafood Group (ECSG) is a Maine-based operator spanning the full lobster value chain from harvesting and processing through to wholesale and retail distribution with direct access to the world-renowned American Lobster fisheries of New England and long-standing relationships with regional fishing cooperatives.

- Product Portfolio: Live, fresh, and processed American lobster across wholesale, institutional food service, retail chain, and export formats, supported by a vertically integrated supply model that ensures consistent quality and year-round supply reliability.

- Recent Developments: ECSG has continued to deepen its cooperative relationships along the New England coast, strengthening supply chain resilience and positioning itself as a preferred supplier for institutional food service buyers and retail chains requiring consistent lobster volume and traceability.

- Strategic Focus: Vertical integration as a core competitive advantage enabling supply reliability, quality control, and margin capture across the value chain alongside expansion of export market access and institutional food service relationships in the US domestic lobster market.

Market Concentration Analysis

The global lobster market exhibits a moderately fragmented-to-concentrated competitive structure. While a small group of large-scale processors and distributors - particularly in North American supply chains - hold significant international trade market share, the broader production base encompasses thousands of independent fishermen, small-scale cooperatives, and regional processors across the Caribbean, Southeast Asia, and Oceanian markets.

|

Metric |

Assessment |

|

Top 5 Companies' Estimated Share |

~30-35% of global processing & distribution revenues (2025) |

|

Market Fragmentation Level |

Moderate - fragmented at production level, increasingly concentrated at processing/export |

|

Consolidation Trend |

Accelerating - cross-industry acquisitions and vertical integration activity rising |

|

Barriers to Entry |

High - fishing licenses, cold-chain infrastructure, sustainability certifications required |

|

Key Differentiator |

MSC certification, supply chain integration depth, Asian market access, brand equity |

Investment & Growth Opportunities

Fastest-Growing Segments

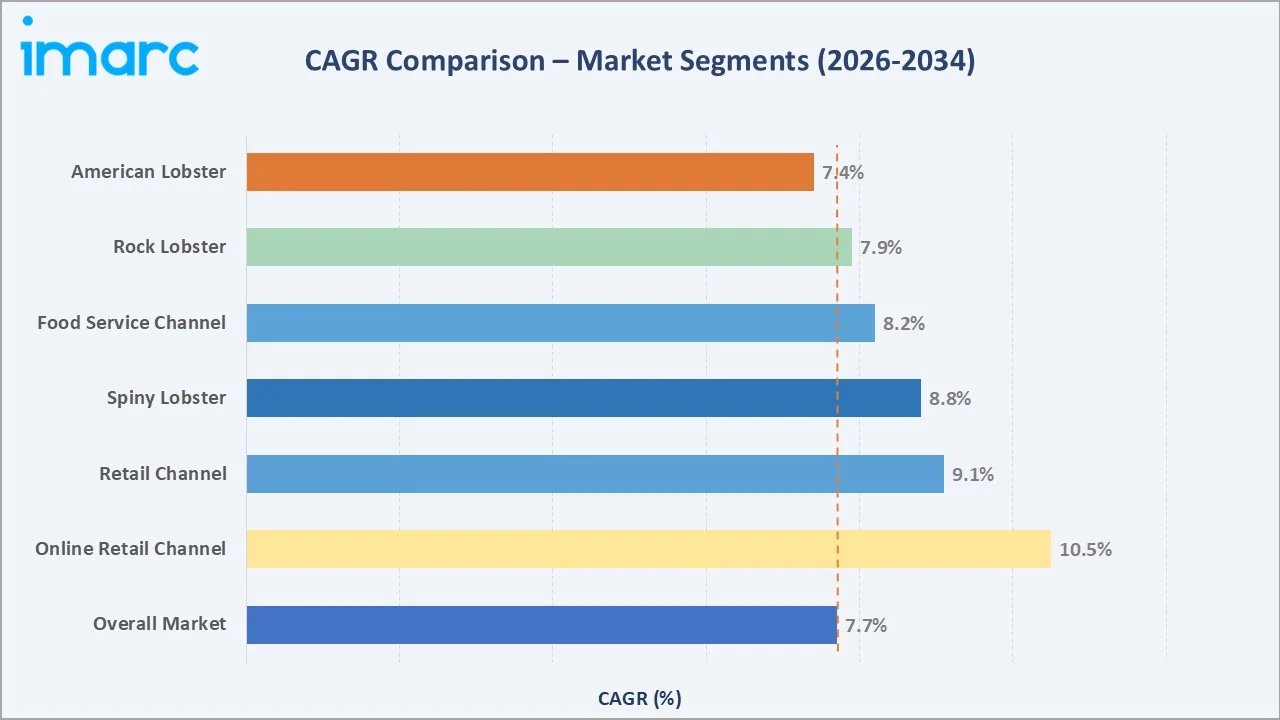

- Retail Distribution: The retail channel at 18.3% (2025) is the fastest-growing distribution category. E-commerce seafood delivery, supermarket premiumization, and gourmet home-dining trends are driving accelerating retail lobster demand. The frozen lobster sub-segment is forecast to grow at a CAGR of 8.0% through 2034, exceeding the overall market average.

- Asia-Pacific Species Demand: Spiny Lobster and Rock Lobster - catering to Asian culinary preferences - are recording the fastest species segment growth rates, supported by import volume surges in China, Japan, and South Korea, and active aquaculture investment in Vietnam, Australia, and India.

Emerging Markets with High Return Potential

- China: China’s lobster imports from Vietnam have seen strong growth, supported by rising consumption. As the middle class expands and premium dining continues to grow across Tier 1–3 cities, lobster demand is expected to increase at a robust pace through the late 2020s, making it one of the most attractive global markets for lobster demand growth.

- India: In FY 2023, Indian seafood industry aims for greater achievements by setting a target of reaching US$ 13.2 billion (Rs. 1 trillion) in exports.

- Middle East: Strong hospitality infrastructure, luxury hotel proliferation, and rising FMCG sector development in UAE, Saudi Arabia, and Qatar are creating incremental lobster demand. The region's rapidly expanding cruise and resort sector further amplifies food service lobster consumption.

Venture Investment and Strategic M&A Trends

- Aquaculture Technology Investment: Recirculating aquaculture systems, hatchery technology, and feed optimization are attracting growing venture capital.

- Digital Seafood Commerce: Investment in online seafood delivery infrastructure, DTC subscription platforms, and digital supply chain systems is accelerating, targeting the structural shift from traditional wholesale to e-commerce-enabled direct distribution channels in North America and Europe.

- Sustainable Fisheries and Certification Infrastructure: Impact investment in MSC certification support, traceability technology, and sustainable aquaculture infrastructure is growing, driven by the premium pricing power of certified product and increasing regulatory mandates for responsible sourcing across major import markets.

Future Market Outlook (2026-2034)

Growth Projections and Market Trajectory

The global lobster is projected to grow from USD 9.0 Billion in 2025 to USD 17.5 Billion by 2034, registering a CAGR of 7.7%. Over the same period (2025–2034), global consumption of aquatic animal foods is expected to rise, with Asia accounting for 75% of the growth, followed by Africa (15%), the Americas (11%), and Oceania (1%), while consumption in Europe is anticipated to decline marginally.

Technological Disruptions Shaping the Market

Commercial-scale lobster aquaculture, enabled by RAS technology and advances in larval rearing, is forecast to meaningfully supplement wild-catch supply by the late 2020s, supporting supply stabilization and enabling geographic expansion of lobster production to new regions.

Industry Transformation and Strategic Imperatives

The lobster industry will undergo significant structural transformation through 2034, characterized by consolidation at processing and distribution levels, increased vertical integration across the value chain, and the emergence of branded premium lobster products with explicit and verifiable sustainability credentials.

Research Methodology

Primary Research

IMARC Group's primary research involved structured interviews and consultations with industry stakeholders including seafood processors, fishing cooperative representatives, food service procurement managers, retail buyers, sustainability certification bodies (MSC), regulatory agency representatives, and aquaculture technology specialists. Primary data collection validated quantitative estimates derived from secondary sources and provided forward-looking qualitative intelligence on emerging trends, competitive dynamics, investment priorities, and technology adoption trajectories.

Secondary Research

Secondary research drew upon authoritative sources including government fisheries agencies (NOAA, FAO, DAWE Australia), regulatory bodies (MSC, EU Food Safety Authority), industry associations (VASEP, National Fisheries Institute, Marine Stewardship Council), trade publications, company annual reports, press releases, and verified third-party market intelligence databases. All statistics referenced in this report are sourced from 2024-2026 publications to ensure recency and analytical relevance.

Market Estimation and Forecasting Models

IMARC Group employed both bottom-up and top-down estimation methodologies. The bottom-up approach aggregated species-level production volumes, processing outputs, and trade flow data to estimate total market value by segment and region. The top-down approach utilized macroeconomic indicators, global seafood consumption trends, and regional income growth projections to validate overall market sizing. Forecasting models incorporate historical CAGR analysis, demand driver assessment, regulatory impact modelling, and scenario analysis across base, optimistic, and conservative cases for the 2026-2034 forecast period.

Lobster Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, ‘000 Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Covered | American Lobster, Spiny Lobster, Rock Lobster, European Lobster |

| Weights Covered | 0.5 - 0.75 lbs, 0.76 - 3.0 lbs, Over 3 lbs |

| Product Types Covered | Whole Lobster, Lobster Tail, Lobster Meat, Lobster Claw |

| Distribution Channels Covered | Food Service, Retail |

| Regions Covered | North America, Europe, Asia, Oceania, Others |

| Companies Covered | Clearwater Seafoods, High Liner Foods, East Coast Seafood Group, Tangier Lobster Co. Ltd, Supreme Lobster & Seafood, Boston Lobster Company, Geraldton Fishermen's Co., Pescanova España S.L.U., Thai Union Manufacturing Company Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the lobster market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global lobster market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the lobster industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Lobster Market Report

The global lobster market was valued at USD 9.0 Billion in 2025. The market grew from USD 6.2 Billion In 2020, reflecting a strong historical CAGR underpinned by premium seafood demand.

The lobster market is projected to exhibit a CAGR of 7.7% during 2026-2034, reaching USD 17.5 Billion by 2034, driven by Asia-Pacific expansion, aquaculture development, and sustained premium dining demand.

Key drivers include rising global premium seafood demand, sustainability certifications (MSC), e-commerce channel expansion, cold-chain logistics advances, aquaculture technology development, and rising middle-class incomes in Asia-Pacific, particularly China and India.

North America dominates with 48.0% of global revenues in 2025, supported by established Maine and Maritime Canada fisheries, high per-capita consumption, and strong institutional food service demand across premium restaurants and hotels.

Asia is the fastest-growing region, forecast to grow at approximately 9.4% CAGR through 2034.

American Lobster accounts for 43.3% of the global lobster market in 2025, driven by its premium culinary reputation, high meat yield, and certified sustainable supply from well-managed North Atlantic fisheries.

Food Service accounts for 81.7% of global lobster revenues in 2025, anchored by lobster's role as a centrepiece of fine dining menus, luxury hotel banquets, cruise ship operations, and premium catering services worldwide.

MSC certifications are increasingly mandated by major buyers. Consumers pay more for sustainably sourced seafood. The EU's 2025 approval of North American farmed lobster imports underscores the commercial importance of sustainability credentials.

Aquaculture is gaining strategic importance as a supplement to wild-catch supply. Developments such as Australia’s Toomulla Beach onshore facility and Lobster Harvest’s recent funding highlight the growing commercial viability of large-scale aquaculture.

Key challenges include climate change disrupting wild lobster habitats, overfishing risks requiring stringent regulation, trade policy exposure to tariff changes, high cold-chain logistics costs, and evolving traceability compliance requirements.

Major players include Clearwater Seafoods, High Liner Foods, East Coast Seafood Group, Tangier Lobster Co. Ltd, Supreme Lobster & Seafood, Boston Lobster Company, Geraldton Fishermen's Co., Pescanova España, S.L.U, Thai Union Manufacturing Company Ltd.

High-return opportunities include Asia-Pacific market entry, commercial-scale aquaculture development (RAS technology), e-commerce seafood platform investment, vertical supply chain integration, and value-added frozen and ready-to-eat lobster product development targeting retail premiumization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)