Logistics Automation Market Size, Share, Trends and Forecast by Component, Function, Enterprise Size, Industry Vertical, and Region, 2026-2034

Global Logistics Automation Market Size, Share, Trends & Forecast (2026-2034)

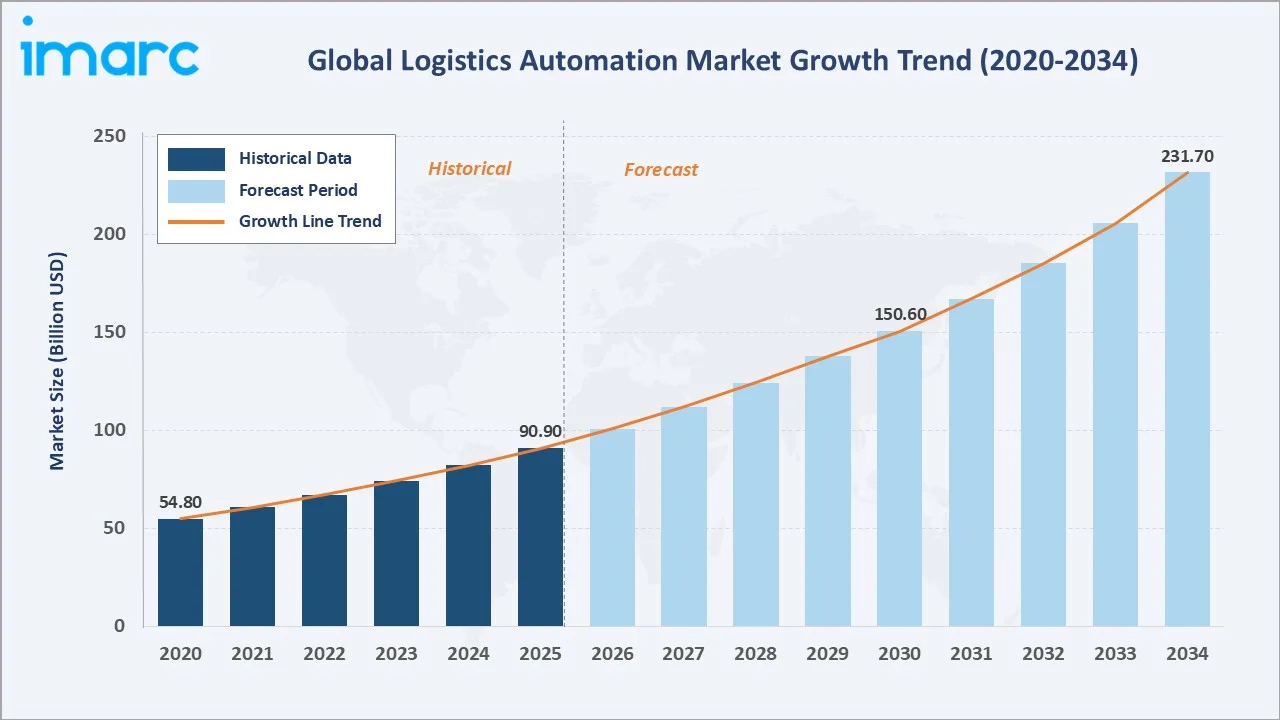

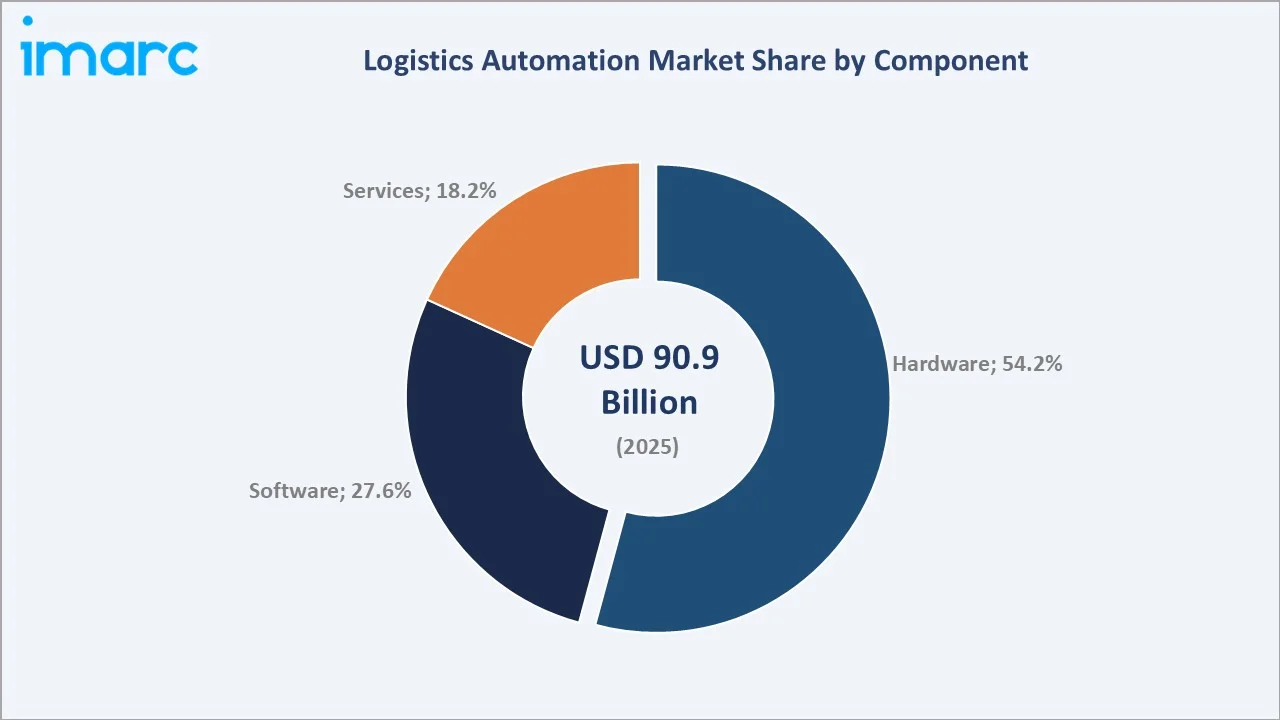

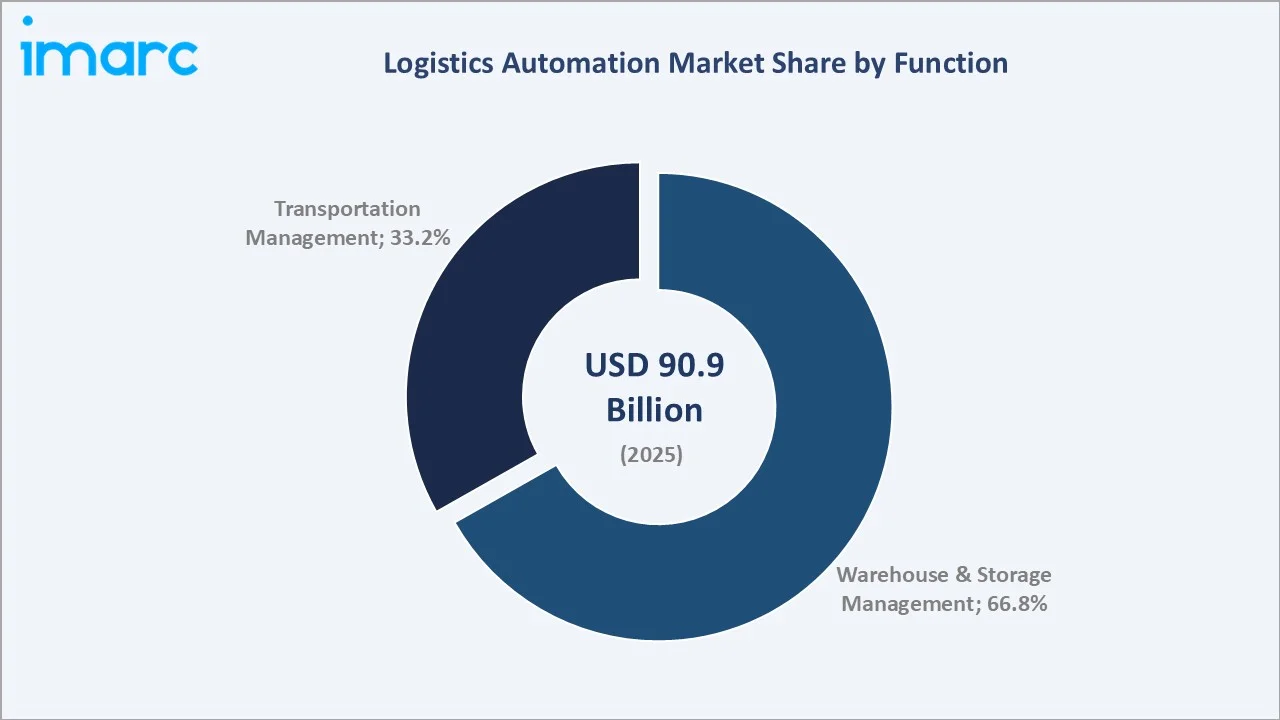

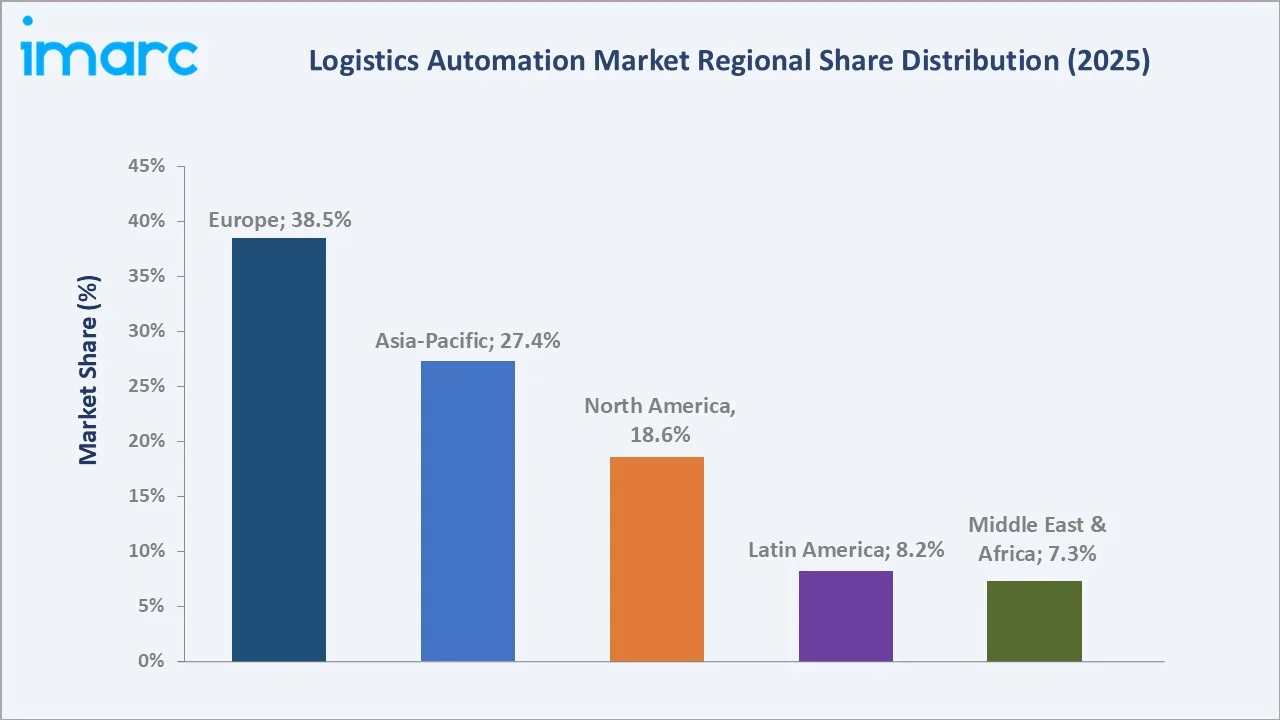

The global logistics automation market size was valued at USD 90.9 Billion in 2025 and is projected to reach USD 231.7 Billion by 2034, exhibiting a CAGR of 10.63% during the forecast period 2026-2034. The logistics automation market growth is propelled by rapid e-commerce expansion, rising labor costs, the adoption of AI-led robotics, and deep integration of warehouse management software across fulfillment networks. Hardware components lead with 54.2% share in 2025, while warehouse and storage management functions account for 66.8% of global demand. Europe dominates with 38.5% of global revenue in 2025, driven by strong manufacturing automation programs across Germany, France, and the UK.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 90.9 Billion |

|

Forecast Market Size (2034) |

USD 231.7 Billion |

|

CAGR (2026-2034) |

10.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (38.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~13.2%) |

|

Leading Component |

Hardware (54.2%, 2025) |

|

Leading Function |

Warehouse & Storage Management (66.8%, 2025) |

The global logistics automation market growth trajectory from 2020 through 2034 reflects a steady historical climb followed by a sharper forecast curve, supported by capex expansion in automated fulfillment centers, retail distribution, and third-party logistics operations worldwide.

To get more information on this market, Request Sample

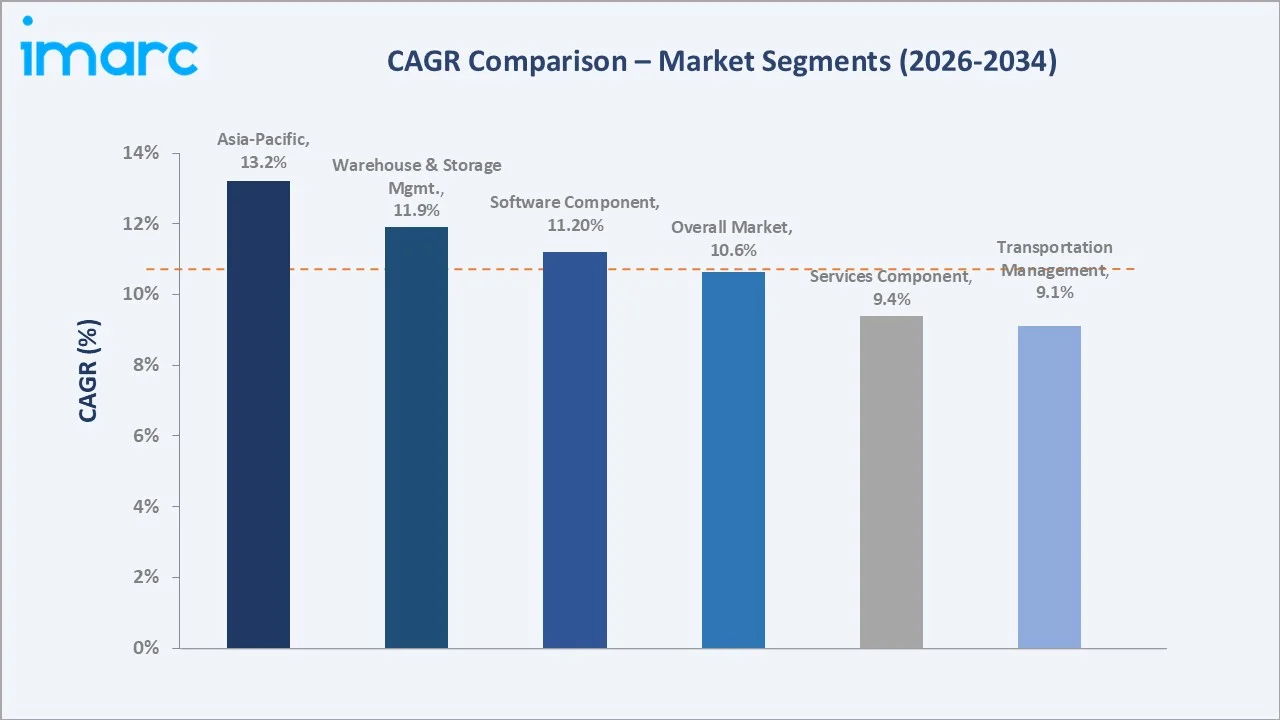

Segment-level CAGR benchmarks highlight Asia-Pacific and warehouse management as the fastest-growing categories within the global logistics automation market forecast through 2034, outpacing the blended 10.63% industry growth rate.

Executive Summary

The global logistics automation market is undergoing a structural transformation driven by e-commerce scale, labor cost inflation, and AI-led robotics adoption. Valued at USD 90.9 Billion in 2025, the market is forecast to reach USD 231.7 Billion by 2034 at a CAGR of 10.63%. Rising throughput demands at fulfillment centers and the global shortage of warehouse labor are forcing operators to scale automation investments at record levels.

Hardware components command 54.2% share in 2025, powered by surging AGV and AMR deployments, while software platforms grow faster on the back of cloud WMS and WES adoption. Warehouse and storage management represents 66.8% of global functional spend, supported by robotics-integrated distribution centers. Transportation management is scaling quickly on TMS modernization cycles among 3PLs and retailers.

Europe leads with 38.5% global revenue share in 2025, reflecting the region's Industry 4.0 investments and mature automotive and FMCG manufacturing base. Asia-Pacific holds 27.4% and is the fastest-growing region, expanding at an estimated 13.2% CAGR through 2034 on the back of Chinese e-commerce scale and India's warehousing boom. The logistics automation market outlook remains strongly positive through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Hardware - 54.2% share (2025) |

|

Leading Function |

Warehouse & Storage Management - 66.8% (2025) |

|

Fastest Growing Function |

Warehouse & Storage Management - ~11.9% CAGR (2026-2034) |

|

Leading Region |

Europe - 38.5% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - ~13.2% CAGR (2026-2034) |

|

Top Companies |

Daifuku Co. Ltd., KION Group AG, Honeywell International Inc., SAP SE, KUKA SE & Co. KGaA |

Key Analytical Observations Supporting the Above Data:

- Hardware's 54.2% dominance in 2025 reflects strong AGV, AMR, AS/RS, and conveyor demand across fulfillment centers. AMR deployments are estimated to exceed 0.8–1.0 million units globally in 2025, driven primarily by logistics automation (552,000 units) and manufacturing adoption (264,000 units).

- Software's 27.6% share is driven by cloud-based WMS and WES adoption. Cloud-based WMS and WES platforms are experiencing strong growth driven by subscription-based SaaS models, as vendors continue transitioning from legacy license deployments to recurring-revenue architectures, supported by rapid cloud adoption across logistics and fulfillment operations.

- Warehouse & storage management's 66.8% lead is underpinned by e-commerce fulfillment capex. Global warehouse construction starts exceeding 850 million sq. ft. in 2024 per JLL, with 30-35% designed for automation.

- Europe's 38.5% global dominance reflects Germany's Industrie 4.0 leadership, France's automated retail distribution scale-up, and EU-wide manufacturing modernization grants under Horizon Europe programs.

- Asia-Pacific's 13.2% forecast CAGR is propelled by China's JD Logistics and Cainiao network automation, India's national logistics policy launched in 2022, and Japan's chronic warehouse labor shortages.

- Top 5 OEM concentration (Daifuku, Kion, Honeywell, SAP, Kuka) is estimated at 32-38% of global revenue in 2025, indicating a moderately concentrated competitive structure.

Global Logistics Automation Market Overview

Logistics automation refers to the use of robotics, material-handling hardware, and intelligent software platforms to streamline goods movement across warehouses, distribution centers, and transportation networks. The global market spans AGVs, AMRs, automated storage and retrieval systems, sortation equipment, conveyors, AIDC technology, and WMS, WES, and TMS software solutions. Applications extend across manufacturing, retail, e-commerce, 3PL, healthcare, FMCG, aerospace, energy, and chemicals industries.

The industry operates at the convergence of e-commerce growth, labor economics, and digital transformation. Macroeconomic drivers include declining robotics costs, rising labor costs in developed markets, and sustained e-commerce penetration, which reached roughly one-fifth of global retail sales in 2024. Policy tailwinds such as the U.S. CHIPS and Science Act and the EU's Industry 5.0 framework are catalyzing long-horizon automation spending, reshaping how operators procure and deploy systems through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

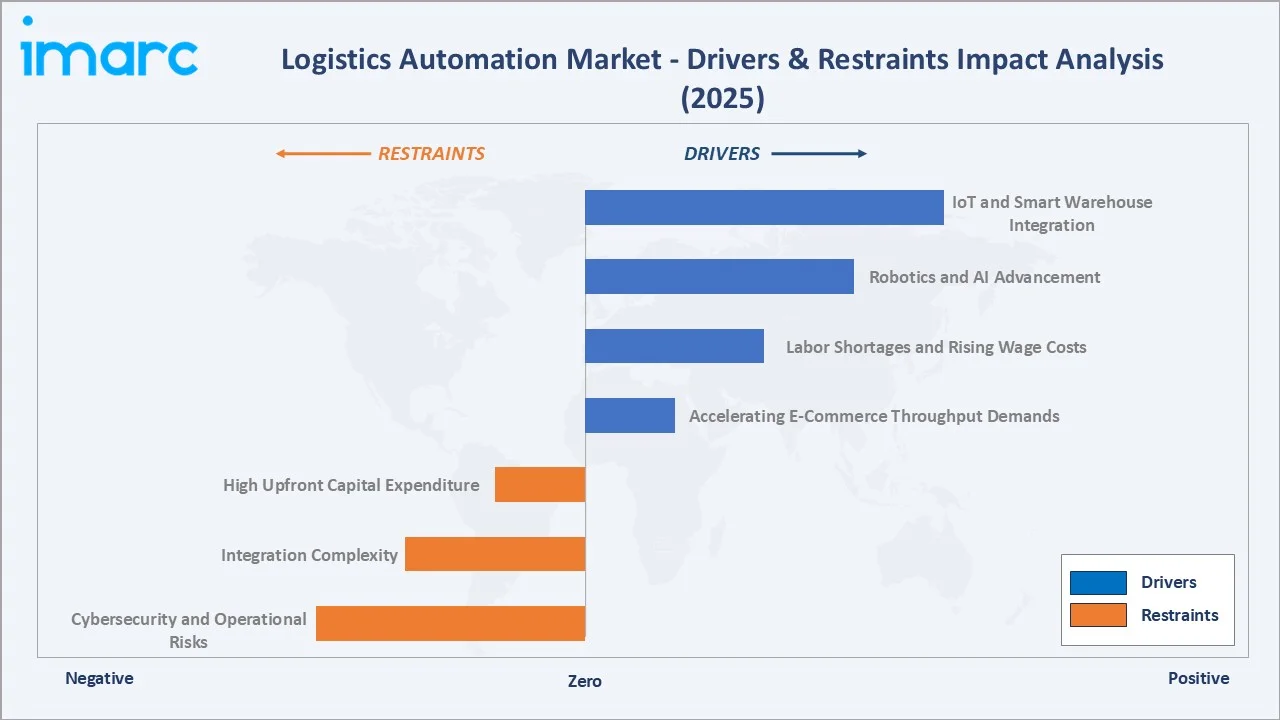

Market Drivers

- Accelerating E-Commerce Throughput Demands: Global e-commerce sales surpassed USD 6.3 trillion in 2024 per eMarketer, pushing retailers toward high-velocity automated fulfillment. Amazon alone operates more than 750,000 mobile drive units across its global network as of 2024, setting a benchmark for scaled robotics deployment.

- Labor Shortages and Rising Wage Costs: According to the U.S. Bureau of Labor Statistics, the transportation, warehousing, and utilities sector consistently recorded monthly separations in the hundreds of thousands, with separation rates in the high-single-digit annualized range, reflecting ongoing labor churn in logistics operations.

- Robotics and AI Advancement: Next-generation AMR fleets now operate at 99.8% navigation accuracy using SLAM and machine-vision systems. The price of industrial mobile robots has declined between 2020 and 2025, dramatically improving ROI for mid-market operators.

- IoT and Smart Warehouse Integration: Cloud-based WMS adoption is accelerating as enterprises shift toward scalable, subscription-driven platforms, enabling real-time visibility and seamless orchestration across automation systems, including robotics, conveyors, and labor operations. Digital twins and 5G connectivity are reducing downtime in early-adopter facilities, according to Deloitte industry surveys.

Urbanization and same-day delivery expectations further reinforce these drivers. Retailers and 3PLs are committing multi-year capex programs to retrofit legacy distribution centers with modular, software-defined automation stacks suited to peak-volume fluctuations.

Market Restraints

- High Upfront Capital Expenditure: A fully automated greenfield warehouse demands significant upfront investment in equipment and systems integration, which can create adoption barriers for small and mid-sized operators.

- Integration Complexity: Legacy ERP and WMS environments often require 12-18 month integration cycles, with project overruns common. This slows ROI realization in first-deployment sites.

- Cybersecurity and Operational Risks: The IBM 2024 Cost of a Data Breach Report placed average manufacturing and logistics sector breach costs at USD 5.56 million, amplifying buyer hesitancy around connected automation stacks.

Market Opportunities

- Automation-as-a-Service Models: S Subscription-based Robotics-as-a-Service (RaaS) models are expanding access to automation for small and mid-sized enterprises by eliminating upfront capital barriers and shifting robotics adoption to an operating expense model, supported by strong market growth and increasing demand across logistics and manufacturing sectors.

- Middle East Mega-Logistics Hubs: Ongoing logistics hub expansions in Dubai are driving sustained, multi-year investment in automation technologies, supported by government-led infrastructure development and increasing demand for advanced warehousing and supply chain solutions.

- Cold Chain Automation: Pharma and grocery cold-chain warehouse automation is growing at 14% annually, driven by biologics expansion and online grocery scaling across North America and Europe.

Market Challenges

- Workforce Reskilling Gap: The World Economic Forum estimates 50% of all logistics workers will need reskilling by 2027, creating a skills bottleneck for operators scaling automation across geographies.

- Supply Chain Component Constraints: Semiconductor and servo-motor lead times, still elevated at 20-40 weeks in early 2025 for certain components, continue to delay large automation projects.

- Standardization and Interoperability Gaps: Multi-vendor robotics fleets often struggle with orchestration layer fragmentation, limiting full-site throughput optimization in brownfield deployments.

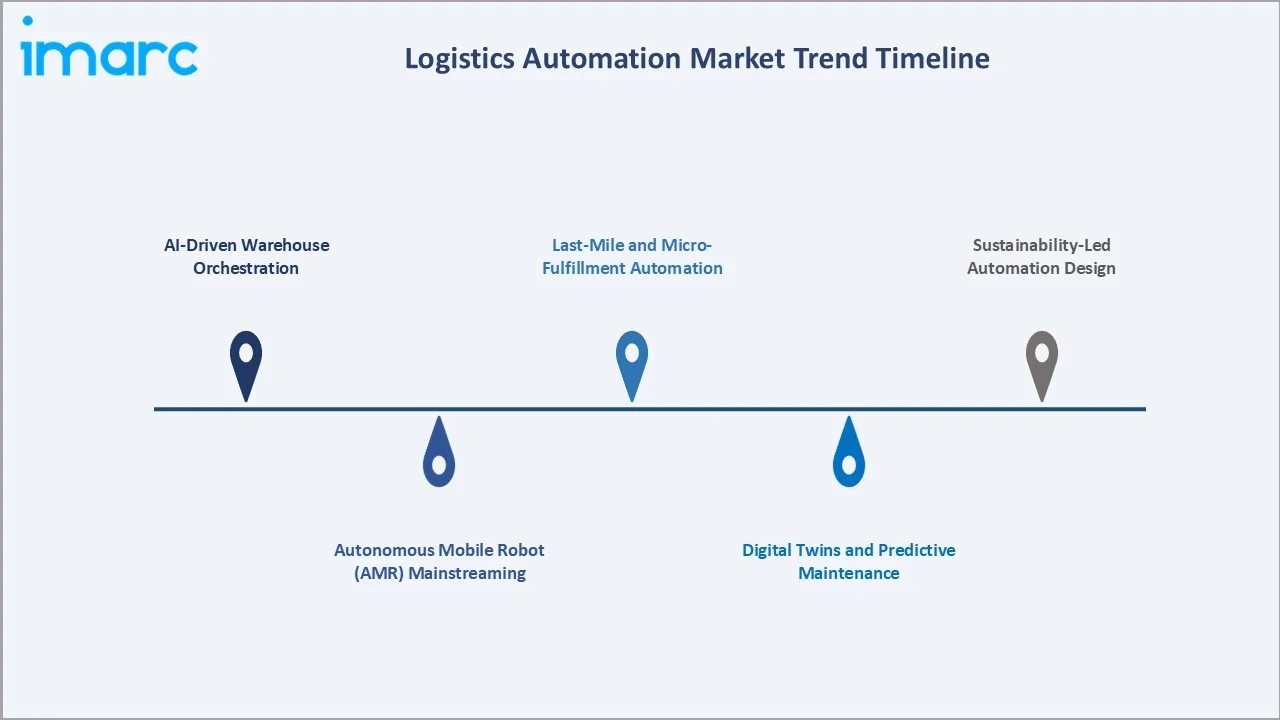

Emerging Market Trends

1. AI-Driven Warehouse Orchestration

AI-powered orchestration platforms are rapidly replacing rule-based control systems across large fulfillment operators. These platforms route tasks dynamically between human pickers, AMRs, and fixed automation in real time.

2. Autonomous Mobile Robot (AMR) Mainstreaming

AMR shipments exceeded 250,000 units globally in 2024, a 40% year-over-year increase per Interact Analysis. Unlike legacy AGVs, AMRs navigate via SLAM and operate without fixed infrastructure, making them attractive for mid-sized operators. Unit prices have dropped below USD 30,000 for standard form factors in 2025.

3. Digital Twins and Predictive Maintenance

Digital twin adoption in warehouse operations is accelerating, with the segment projected to reach USD 9.8 billion by 2028. Operators use virtual simulations to test layout changes, validate slotting strategies, and reduce downtime through predictive maintenance of critical hardware systems.

4. Last-Mile and Micro-Fulfillment Automation

Urban micro-fulfillment centers (MFCs) are spreading rapidly, with grocery and quick-commerce operators deploying modular automation in 2,000-10,000 sq. ft. formats. Ocado, Fabric, and AutoStore are driving sub-1-hour delivery economics across North America, Europe, and key Middle Eastern cities.

5. Sustainability-Led Automation Design

Energy-efficient drive systems, regenerative conveyors, and lightweight AMR designs are becoming standard. Leading operators report energy savings from modern automation versus legacy equipment, aligning with Scope 1 and Scope 2 emission reduction commitments through 2030.

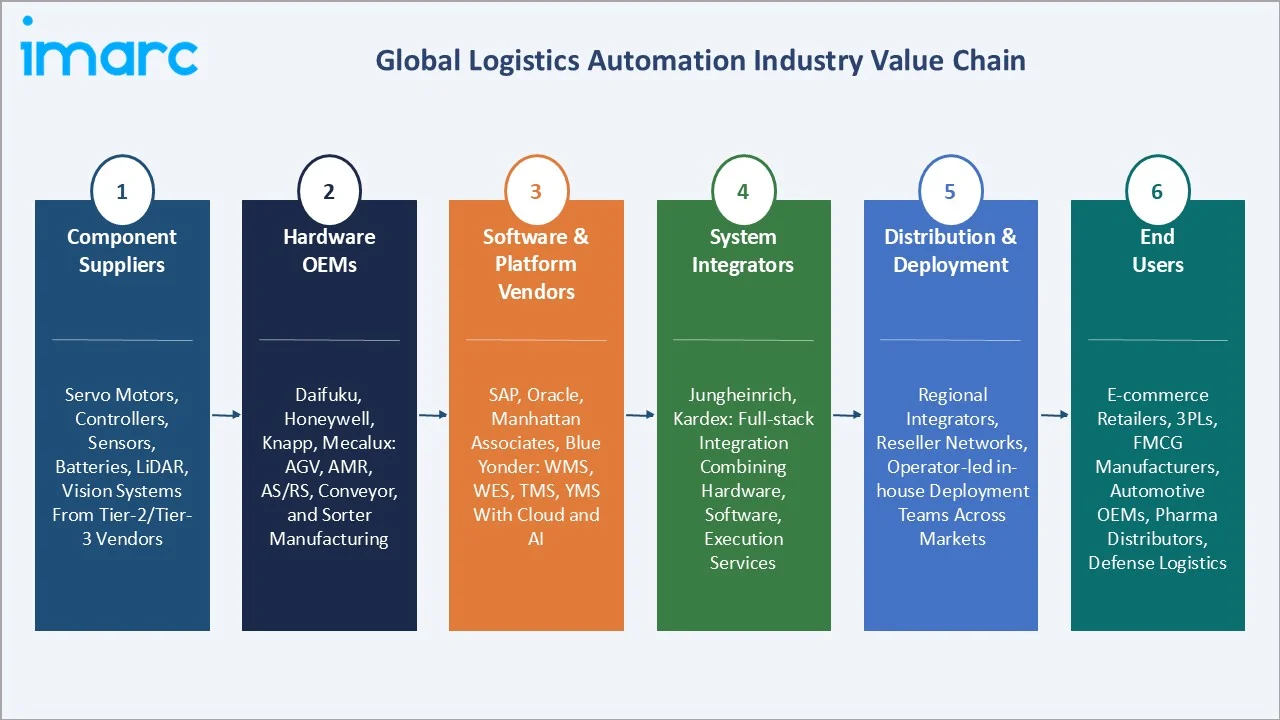

Industry Value Chain Analysis

The global logistics automation value chain spans six integrated stages from component supply through end-user operations. Each stage carries distinct competitive dynamics, margin profiles, and R&D intensity relevant to the overall logistics automation market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Component Suppliers |

Servo motors, controllers, sensors, batteries, LiDAR, vision systems supplied by Tier-2/Tier-3 vendors in Japan, Germany, and China |

|

Hardware OEMs |

Daifuku, Honeywell, Knapp, Mecalux- full AGV, AMR, AS/RS, conveyor, and sorter manufacturing |

|

Software & Platform Vendors |

SAP, Oracle, Manhattan Associates, Blue Yonder - WMS, WES, TMS, YMS solutions with cloud and AI capabilities |

|

System Integrators |

Jungheinrich, Kardex - full-stack integration combining hardware, software, and execution services |

|

Distribution & Deployment |

Regional integrators, reseller networks, and operator-led in-house deployment teams across mature and emerging markets |

|

End Users |

E-commerce retailers, 3PLs, FMCG manufacturers, automotive OEMs, pharma distributors, and defense logistics operators |

System integrators and OEMs hold the highest strategic value by bundling hardware, software, and long-tail services into turnkey solutions. Meanwhile, cloud-native software vendors are capturing expanding share of operator budgets, reshaping economics from pure capex-led toward recurring subscription revenues.

Technology Landscape in the Logistics Automation Industry

Robotics and Mobile Automation

AGVs, AMRs, and goods-to-person systems anchor the hardware layer. AMR fleet sizes at leading operators are scaling significantly, with AI-based fleet orchestration improving utilization compared to earlier AGV-based systems. Kiva-style goods-to-person robots remain dominant in high-SKU e-commerce fulfillment.

Automated Storage and Retrieval Systems (AS/RS)

Shuttle-based and mini-load AS/RS deployments are expanding rapidly across retail, pharma, and spare-parts distribution. Density gains of 3-5x compared with traditional racking are driving adoption, particularly in high-cost urban markets where real-estate economics favor verticalization.

Smart Software: WMS, WES, and TMS

Cloud-based warehouse management systems now account for the majority of new deployments. Embedded AI for slotting, wave-less order release, and dynamic labor allocation is becoming standard. TMS modernization among 3PLs is driving strong growth in software revenue for leading platforms.

AI, IoT, and Automation Intelligence

Computer vision for parcel dimensioning, machine-learning demand forecasting, and real-time IoT telemetry across conveyors and forklifts are converging into unified control towers.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global logistics automation market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on component and functions.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Component | Hardware | 54.2% |

2025 |

| Function | Warehouse and Storage Management | 66.8% |

2025 |

| Enterprise Size | Large Enterprises | 75.4% |

2025 |

| Industry Vertical | Retail and E-Commerce | 29.7% |

2025 |

| Region | Europe | 38.5% | 2025 |

By Component

Hardware leads the global logistics automation market component segment with a 54.2% share in 2025. AGVs, AMRs, automated storage and retrieval systems, sortation systems, palletizers, conveyors, and AIDC equipment make up the bulk of hardware revenue. Global AMR units reflected scaled adoption across Amazon, JD.com, Walmart, and Ocado fulfillment networks.

To access detailed market analysis, Request Sample

Software accounts for 27.6% of global component demand and is the fastest-growing component category. Warehouse management systems (WMS) and warehouse execution systems (WES) form the core of software revenue, with cloud-based deployments contributing the majority of new-license growth in 2024-2025. Services, at 18.2% share, include value-added services and maintenance contracts that are increasingly shifting toward multi-year subscription and SLA-based frameworks.

By Function

Warehouse and storage management dominates the functional segmentation at 66.8% of global revenue in 2025. Robotics-integrated distribution centers, goods-to-person fulfillment systems, and AI-led slotting optimization drive continued investment.

Transportation management accounts for 33.2% of global functional demand and is expanding steadily at an estimated 9.1% CAGR through 2034. Rising fuel costs, driver shortages, and shipper pressure for real-time visibility are driving TMS modernization. The 3PL segment is a primary buyer, with leading providers including DHL, DSV, and Kuehne+Nagel scaling AI-enabled TMS platforms across global networks.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

38.5% |

Germany Industrie 4.0, EU automotive & FMCG automation, Horizon Europe funding |

|

Asia-Pacific |

27.4% |

China e-commerce fulfillment scale, Japan labor shortage, India logistics policy |

|

North America |

18.6% |

U.S. e-commerce capex, Amazon-led robotics, 3PL modernization, USMCA nearshoring |

|

Latin America |

8.2% |

Brazil/Mexico distribution modernization, nearshoring from U.S. manufacturers |

|

Middle East & Africa |

7.3% |

Saudi Vision 2030 logistics hubs, Dubai Logistics City, GCC mega-projects |

Europe commands 38.5% global revenue share in 2025, the largest of any region. Germany anchors the market through Industrie 4.0 adoption across automotive, chemicals, and e-commerce fulfillment. France, the U.K., and the Netherlands add substantial volume driven by retail distribution automation and port modernization. The EU Horizon Europe programme continues to fund R&D automation, while the European Commission's 2024 Industry 5.0 framework encourages human-robot collaboration investments.

Asia-Pacific holds 27.4% of global revenue and is forecast to be the fastest-growing region, advancing at an estimated 13.2% CAGR through 2034. China dominates regional demand through JD Logistics, Cainiao, and SF Express automation programs. National Logistics Policy has accelerated warehousing investment in India, driving strong expansion in Grade-A logistics infrastructure and modern storage capacity. Japan and South Korea continue to scale automation to offset severe demographic labor constraints.

North America accounts for 18.6% of global revenue, anchored by U.S. e-commerce infrastructure. Amazon's logistics network alone operated more than 750,000 mobile drive units by end-2024, representing the world's largest single-operator robotics fleet. Nearshoring under the USMCA framework is spurring automation in Mexican distribution centers, while Canadian retailers are rapidly retrofitting legacy DCs.

Latin America represents 8.2% of global demand, led by Brazil and Mexico. Brazil's e-commerce market grew 16% in 2024, creating sustained pull for warehouse automation. Middle East and Africa accounts for 7.3%, driven by Saudi Arabia's Vision 2030 logistics hub program and the UAE's Dubai Logistics City expansion, which represent a multi-billion dollar automation procurement pipeline through 2030.

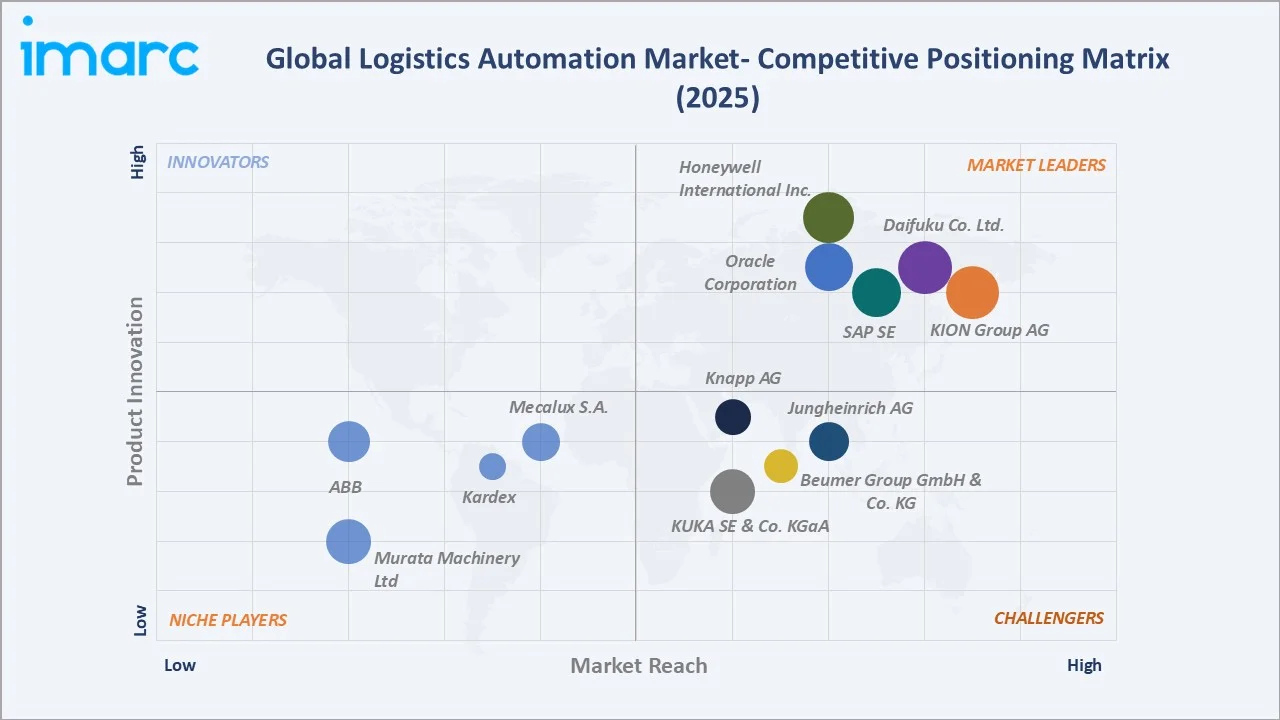

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Daifuku Co. Ltd. |

Daifuku |

Leader |

AS/RS leadership, airport & auto logistics scale |

|

KION Group AG |

Dematic |

Leader |

Full-stack integration, global fulfillment projects |

|

Honeywell International Inc. |

Honeywell |

Leader |

Sortation, voice automation, software scale |

|

SAP SE |

SAP Suite |

Leader |

Enterprise WMS/TMS, ERP-integrated platform |

|

Oracle Corporation |

Oracle Logistics |

Leader |

Cloud WMS/TMS, enterprise customer base |

|

KUKA SE & Co. KGaA |

Swisslog |

Challenger |

AutoStore systems, pharma & retail automation |

|

Knapp AG |

Knapp |

Challenger |

Pharma, fashion, and grocery automation expertise |

|

Jungheinrich AG |

Jungheinrich |

Challenger |

Intralogistics, forklift automation, European scale |

|

Beumer Group GmbH & Co. KG |

Beumer Group |

Challenger |

Airport & parcel sortation, high-speed systems |

|

Kardex |

Kardex Remstar |

Emerging |

Compact automation, mid-market reach |

|

Mecalux S.A. |

Mecalux International |

Emerging |

Iberia/Latin America strength, AS/RS expansion |

|

Murata Machinery Ltd |

Muratec |

Emerging |

Semiconductor fab automation, Japan/APAC base |

|

ABB |

ABB Robotics |

Emerging |

Industrial robotics, AMR integration |

The global logistics automation market's competitive landscape is moderately concentrated, with global powerhouses competing alongside regional specialists and software-led platform vendors. Leading players compete on integration breadth, AI and robotics IP, software scalability, and global deployment capability. Strategic partnerships are accelerating, with KION Group and Google Cloud announcing a generative AI supply-chain collaboration in April 2024 to enhance Dematic's orchestration capabilities.

Key Company Profiles

Daifuku Co. Ltd.

Daifuku Co. Ltd. is the world's largest material-handling systems provider, headquartered in Osaka, Japan. Founded in 1937, it operates across automotive, electronics, retail, airport, and semiconductor verticals with a presence in more than 26 countries.

- Product & Platform Portfolio: Daifuku's portfolio spans AS/RS, AGVs, sortation systems, airport baggage handling, and cleanroom automation. Key platforms include the Hikari AGV range, Shuttle Rack S mini-load systems, and the Sys-E software suite.

- Recent Developments: In 2025, Daifuku expanded its U.S. manufacturing footprint through the expansion of its Indiana-based Hobart facility, strengthening its ability to deliver intralogistics and distribution automation systems to North American customers, including e-commerce fulfillment applications.

- Strategic Focus: Daifuku's strategy centers on full-stack system delivery, global project execution, and deep vertical expertise across semiconductor fab logistics, airport baggage systems, and e-commerce fulfillment, with emphasis on India, Southeast Asia, and the Middle East.

KION Group AG

KION Group AG is a global provider of industrial trucks, warehouse automation, and supply chain solutions. Through its automation arm Dematic, the group delivers integrated intralogistics systems to customers across manufacturing, e-commerce, and retail. Dematic operates with a strong presence in North America, Europe, and Asia-Pacific, with its U.S. base in Atlanta, Georgia.

- Product & Platform Portfolio: Kion’s portfolio includes the Multishuttle AS/RS, Pouch Sorter, RapidPick goods-to-person systems, and the iQ software suite for orchestration and analytics. The company also integrates partner-provided AMR and conveyor technologies at scale.

- Recent Developments: In April 2024, KION Group and Google Cloud announced a partnership to embed generative AI into Dematic's warehouse orchestration platform.

- Strategic Focus: KION Group is focused on advancing software-driven automation, expanding its presence in warehouse automation, and strengthening digital capabilities across its portfolio. The company is positioning itself as an integrated solutions provider, combining industrial trucks, automation systems, and intelligent software to support increasingly complex global supply chains.

Honeywell International Inc.

Honeywell International Inc. is a diversified industrial technology company headquartered in Charlotte, North Carolina, USA. Its Intelligrated business is a leading provider of supply-chain automation solutions, serving retail, e-commerce, postal, parcel, and 3PL customers.

- Product & Platform Portfolio: Honeywell Intelligrated's portfolio includes high-speed sorters, conveyor systems, robotic palletizers, the Momentum warehouse execution software, and voice-directed picking solutions through Honeywell Vocollect.

- Recent Developments: In February 2025, Honeywell announced a strategic portfolio restructuring to separate its Automation, Aerospace, and Advanced Materials businesses into three independent companies, enabling each to pursue focused growth strategies and enhance shareholder value.

- Strategic Focus: Honeywell's focus centers on integrated robotics-software offerings, expanding the Momentum WES platform's install base, and capturing share in parcel-sortation and e-commerce fulfillment automation.

Market Concentration Analysis

The global logistics automation market exhibits moderate concentration. The top five players - Daifuku, Dematic, Honeywell, SAP, and Oracle - collectively account for an estimated 32-38% of global revenue in 2025. The remainder is distributed across Swisslog, Knapp, Jungheinrich, Beumer, Kardex, Mecalux, Muratec, and ABB, along with hundreds of specialized regional integrators and robotics startups.

The market is experiencing a dual-track dynamic. At the hardware OEM tier, consolidation continues as acquirers seek full-stack portfolios combining AS/RS, AMR, conveyor, and software capabilities. The KION-Google Cloud partnership, Honeywell's ongoing robotics acquisitions, and SAP/Oracle's software consolidation illustrate the race for end-to-end orchestration. Simultaneously, a rapidly growing cohort of AMR and orchestration-software startups is intensifying competition across mid-market customer segments through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia-Pacific is the highest-growth regional opportunity, expanding at approximately 13.2% CAGR through 2034. Warehouse and storage management functions represent the largest functional opportunity in absolute value terms, projected to grow at 11.9% CAGR. AMR hardware, cloud WMS, and RaaS (Robotics-as-a-Service) models represent the fastest-growing technology sub-segments through 2030.

Emerging Market Expansion

India represents the highest-potential emerging opportunity, driven by the 2022 National Logistics Policy, the PM Gati Shakti infrastructure program, and rapid e-commerce scaling via Amazon, Flipkart, and Meesho. GCC mega-projects, Southeast Asian e-commerce expansion, and Brazil's distribution network modernization collectively represent multi-billion-dollar procurement pipelines for OEMs with local deployment capacity.

Venture and Strategic Investment Trends

Strategic investment continues to flow into robotics, AI-orchestration, and cloud-WMS platforms. AMR and warehouse-robotics startups raised approximately USD 5.2 billion in venture funding between 2022 and 2024 per Pitchbook. Corporate M&A is also active: Fortna was acquired by Thomas H. Lee Partners and subsequently merged with MHS Global to create a fully integrated supply-chain automation platform in 2023.

Future Market Outlook (2026-2034)

The global logistics automation market forecast projects steady value expansion from USD 90.9 Billion in 2025 to USD 231.7 Billion by 2034 at a CAGR of 10.63%. Europe will maintain regional revenue leadership, while Asia-Pacific accelerates structurally. North America will continue to sustain premium growth through e-commerce infrastructure scaling and 3PL modernization cycles.

Three structural shifts will reshape the logistics automation market through 2034. First, AI-orchestration will become the dominant software paradigm, embedding machine-learning across slotting, routing, labor management, and predictive maintenance. Second, AMR and RaaS adoption will extend automation to mid-market operators previously priced out of legacy capex models. Third, sustainability-led automation design will become a procurement criterion, with energy-efficient drives and regenerative systems shifting from optional to standard across new deployments.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with logistics automation industry stakeholders, including product directors at OEM manufacturers, supply-chain VPs at Fortune 500 retailers and 3PLs, procurement managers at distribution operators, system integrators, and institutional investors active in industrial robotics. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include U.S. Bureau of Labor Statistics, Interact Analysis, LogisticsIQ, JLL warehouse research, CBRE industrial market reports, European Commission Industry 5.0 publications, IEA industrial automation data, company annual reports, Pitchbook venture data, and trade publications including Modern Materials Handling, Material Handling & Logistics, DC Velocity, and Supply Chain Dive.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, e-commerce penetration, warehousing stock expansion, labor cost inflation, and AMR adoption curves. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty through 2034.

Logistics Automation Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | USD Billion |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Functions Covered | Warehouse and Storage Management, Transportation Management |

| Enterprise Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Industry Verticals Covered | Manufacturing, Healthcare and Pharmaceuticals, Fast-Moving Consumer Goods (FMCG), Retail and E-Commerce, 3PL, Aerospace and Defense, Oil, Gas and Energy, Chemicals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Daifuku Co. Ltd., KION Group AG, Honeywell International Inc., SAP SE, Oracle Corporation, KUKA SE & Co. KGaA, Knapp AG, Jungheinrich AG, Beumer Group GmbH & Co. KG, Kardex, Mecalux S.A., Murata Machinery Ltd, ABB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the logistics automation market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global logistics automation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the logistics automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Logistics Automation Market Report

The global logistics automation market was valued at USD 90.9 Billion in 2025, driven by e-commerce expansion, labor shortages, AI-led robotics adoption, and accelerating warehouse modernization spending across retail, 3PL, and manufacturing operators.

The market is projected to reach USD 231.7 Billion by 2034, growing at a CAGR of 10.63% during 2026-2034, supported by warehouse capex expansion, AMR mainstreaming, cloud WMS adoption, and sustained automation demand across Europe, Asia-Pacific, and North America.

Hardware leads with a 54.2% share in 2025, driven by AGV, AMR, AS/RS, sortation, and conveyor system demand. Software follows at 27.6% and services at 18.2%, with software growing fastest on cloud WMS and WES adoption curves.

Warehouse and storage management dominated 66.8% of global revenue in 2025, supported by robotics-integrated distribution centers, goods-to-person systems, and AI-driven slotting. Transportation management accounts for the remaining 33.2% of demand.

Europe dominates with a 38.5% share in 2025, led by Germany's Industrie 4.0 adoption, strong French and U.K. retail automation, and broad EU-wide manufacturing modernization programs under Horizon Europe and Industry 5.0 frameworks.

Asia-Pacific is the fastest-growing region, advancing at an estimated 13.2% CAGR through 2034. Growth is powered by Chinese e-commerce giants, India's National Logistics Policy, Japan's demographic labor constraints, and rapid ASEAN fulfillment scaling.

Key drivers include e-commerce throughput demands, rising warehouse labor costs, AI-led robotics advances, cloud-based WMS adoption, falling AMR unit costs, smart-warehouse IoT integration, and macro tailwinds such as nearshoring and global supply-chain resilience investments.

Major players include Daifuku Co. Ltd., KION Group AG, Honeywell International Inc., SAP SE, Oracle Corporation, KUKA SE & Co. KGaA, Knapp AG, Jungheinrich AG, Beumer Group GmbH & Co. KG, Kardex, Mecalux S.A., Murata Machinery Ltd, ABB

Autonomous Mobile Robots (AMRs) are the fastest-growing hardware technology, with shipments exceeding 250,000 units globally in 2024. On the software side, cloud WMS and AI-driven orchestration platforms are the leading growth sub-segments through 2030.

Key opportunities include AMR hardware fleets, cloud-native WMS and WES platforms, Robotics-as-a-Service subscription models, cold-chain automation, Middle East logistics hubs, India warehousing expansion, and AI-orchestration software targeting mid-market operators.

Key challenges include high upfront capital expenditure, integration complexity with legacy systems, cybersecurity risks in connected environments, workforce reskilling gaps, and component lead-time volatility across sensors, motors, and semiconductor-dependent subsystems.

AI is enabling dynamic task orchestration, predictive maintenance, computer-vision parcel handling, and AI-native demand forecasting. Leading operators report 22-30% throughput gains and 15-20% labor productivity improvements from AI-augmented automation deployments in 2024-2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)