Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Global Logistics Market Size, Share, Trends & Forecast (2026-2034)

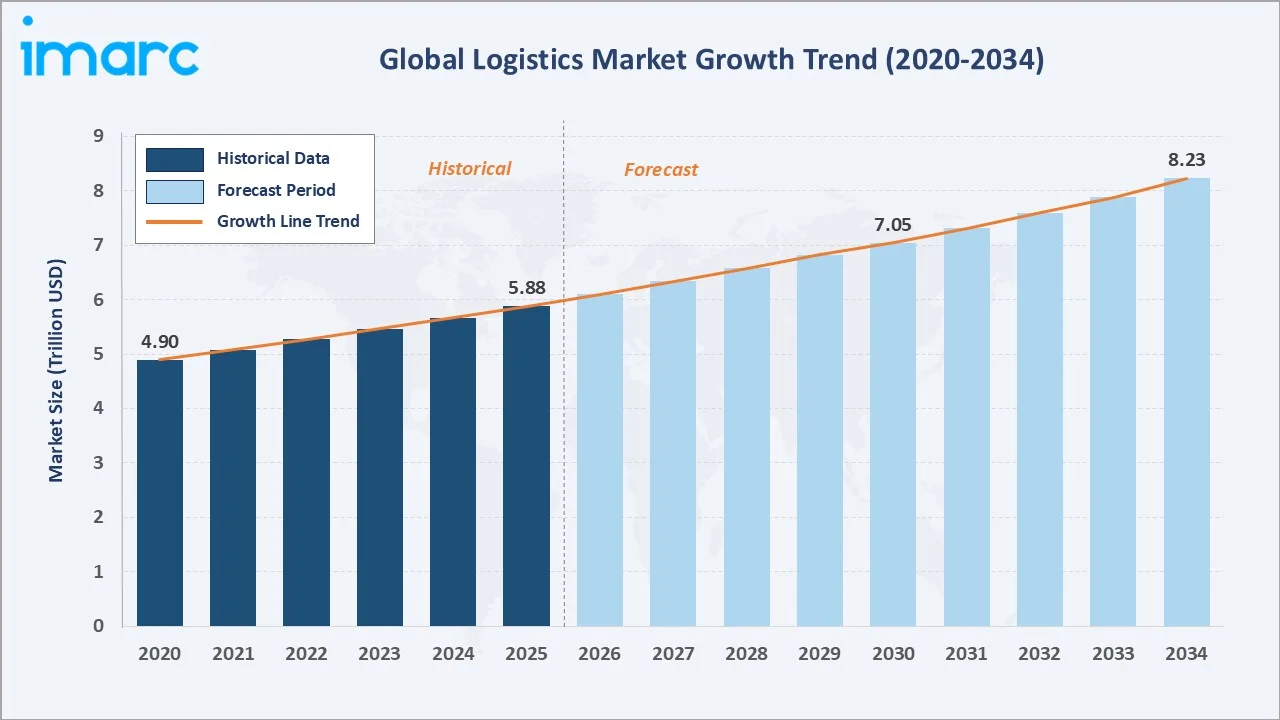

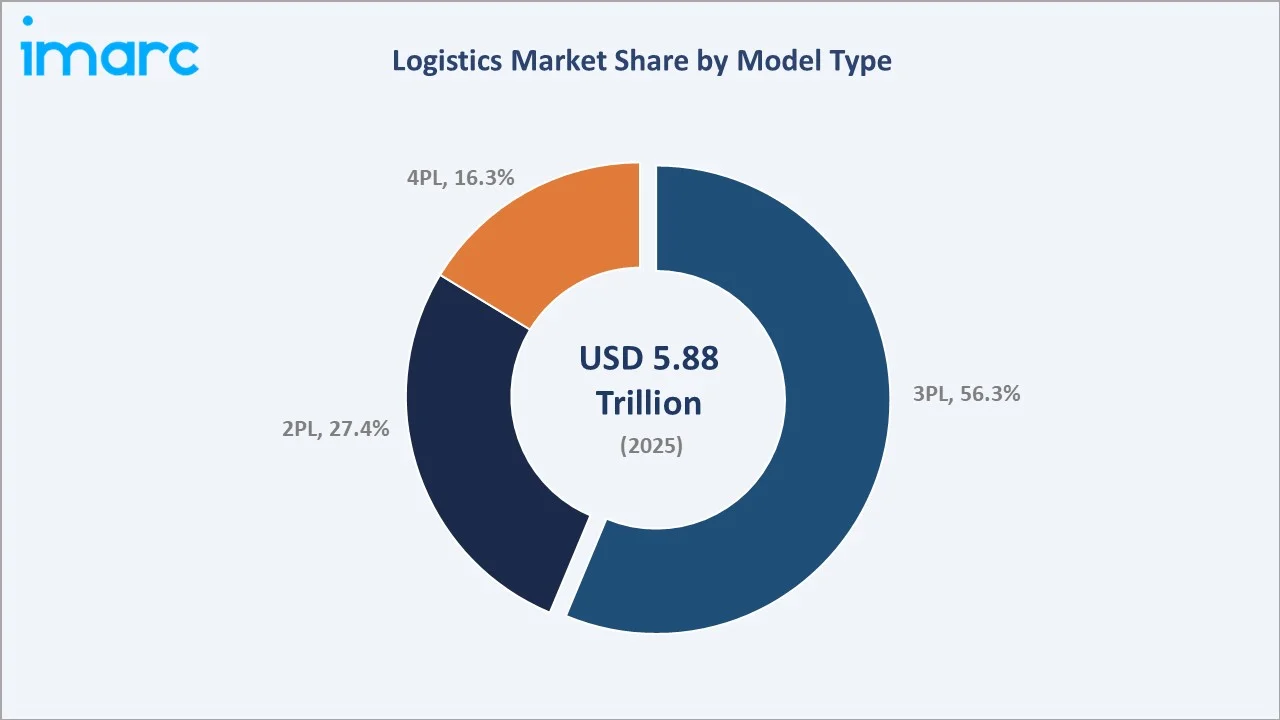

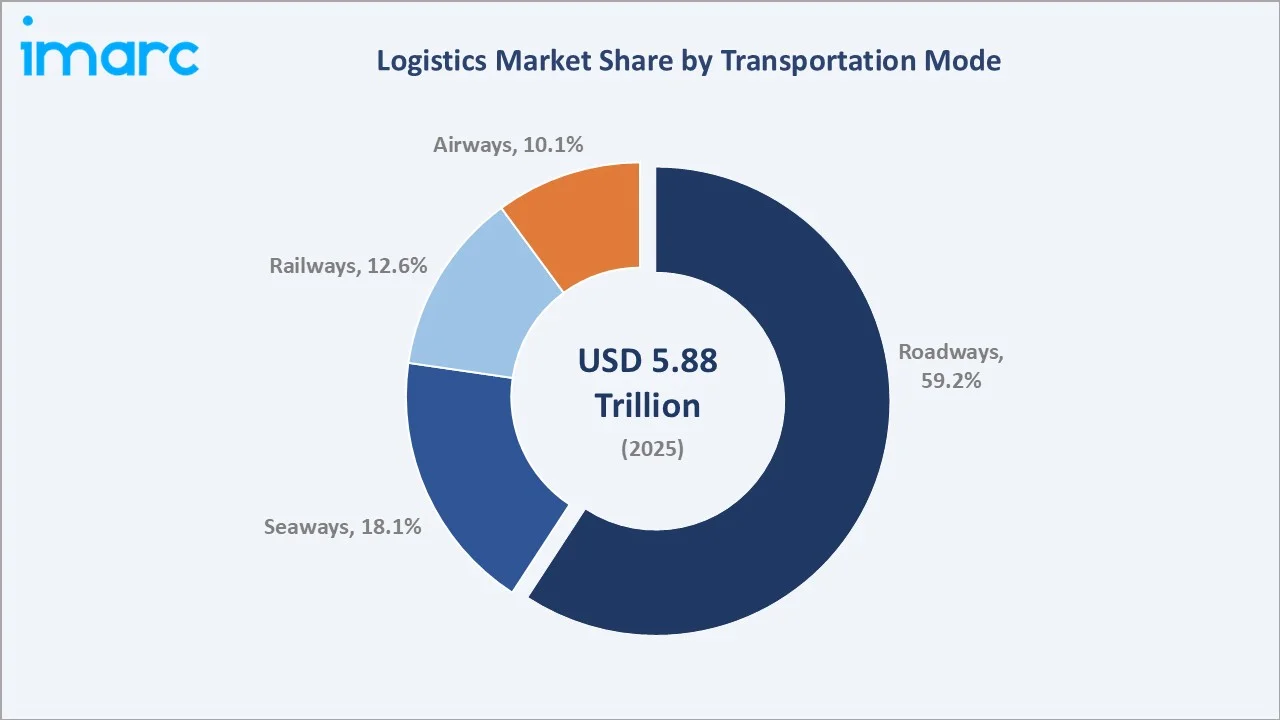

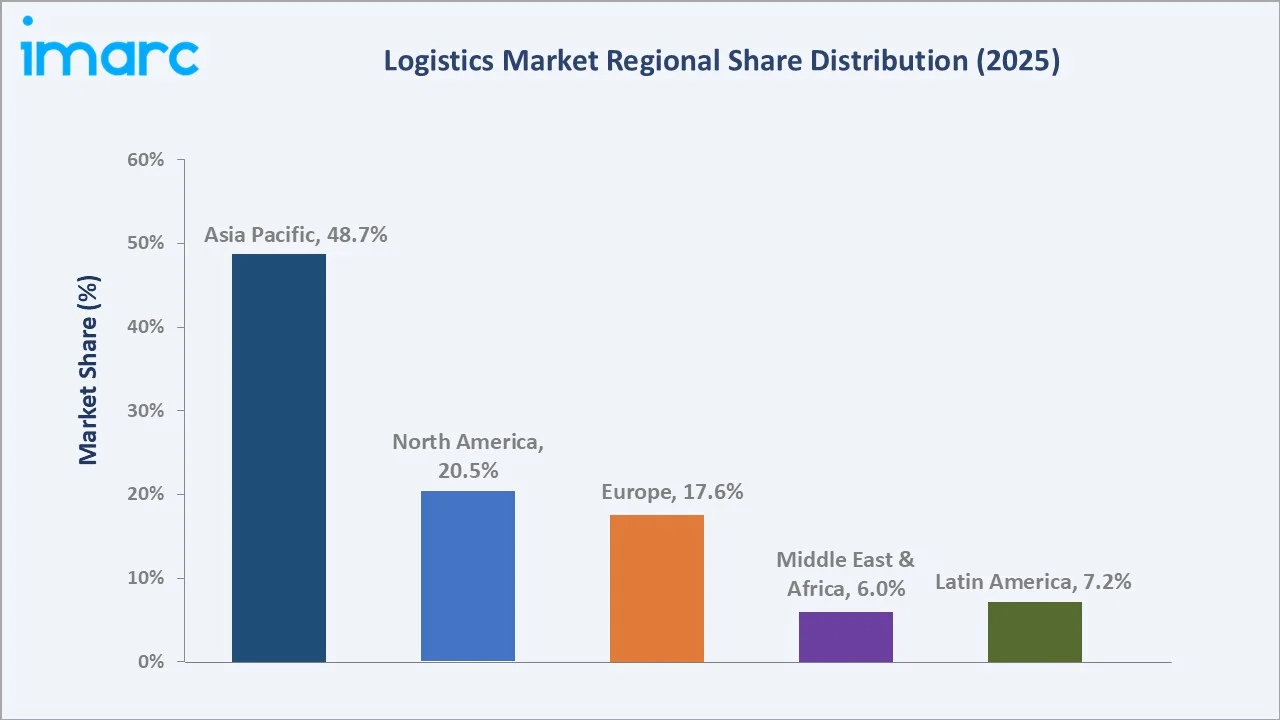

The global logistics market size was valued at USD 5.88 Trillion in 2025 and is projected to reach USD 8.23 Trillion by 2034, exhibiting a CAGR of 3.71% during the forecast period 2026-2034. Expanding global trade volumes, rising e-commerce penetration, and rapid digitization of supply chains are driving the logistics market growth. Third-party logistics (3PL) leads at 56.3% share in 2025, while roadways account for 59.2% of global transportation demand. Asia Pacific dominates with 48.7% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.88 Trillion |

|

Forecast Market Size (2034) |

USD 8.23 Trillion |

|

CAGR (2026-2034) |

3.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (48.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~4.3%) |

|

Leading Model Type |

3 PL (56.3%, 2025) |

|

Leading Transportation Mode |

Roadways (59.2%, 2025) |

The global logistics market growth trajectory from 2020 through 2034 reflects steady expansion powered by e-commerce maturity, manufacturing nearshoring, and accelerating supply-chain digitization across developed and emerging economies.

To get more information on this market, Request Sample

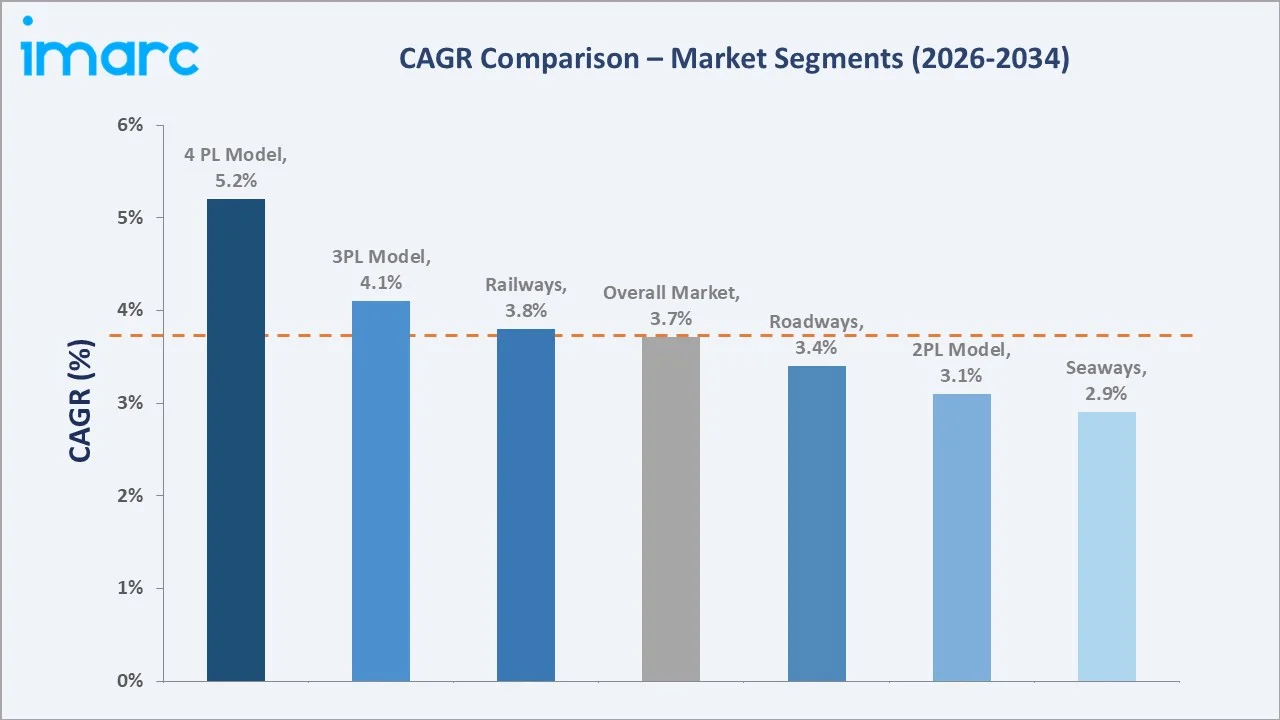

Segment-level CAGR comparisons highlight 4PL model expansion and airways modernization as the fastest-growing sub-categories within the global logistics market forecast through 2034.

Executive Summary

The global logistics market is undergoing structural transformation. It is driven by e-commerce scale, digital freight platforms, and tightening sustainability mandates. Valued at USD 5.88 Trillion in 2025, the market is forecast to reach USD 8.23 Trillion by 2034 at a CAGR of 3.71%.

The 3PL model commands 56.3% share in 2025, driven by shipper outsourcing and integrated warehouse-transport contracts. Roadways dominate transportation mode with 59.2% share, while airways is the fastest-growing transport mode at an estimated CAGR of 4.6% through 2030. 4PL services represent the premium growth tier, serving complex multinational supply chains.

Asia Pacific leads with 48.7% global revenue share in 2025. North America holds 20.5% and Europe 17.6%. The logistics market outlook remains positive as cross-border e-commerce, nearshoring, and green logistics converge across major trade corridors.

Key Market Insights

|

Insight |

Data |

|

Largest Model Type |

3 PL – 56.3% share (2025) |

|

Second Model Type |

2 PL – 27.4% share (2025) |

|

Largest Transportation Mode |

Roadways – 59.2% share (2025) |

|

Fastest Growing Transport Mode |

Airways – ~4.6% CAGR (2025-2030) |

|

Leading Region |

Asia Pacific – 48.7% revenue share (2025) |

|

Top Companies |

DHL, FedEx, UPS, DSV, Ceva, Expeditors, C.H. Robinson |

|

Leading End Use |

Manufacturing – 16.8% share (2025) |

Key Analytical Observations Supporting the Above Data:

- 3PL's 56.3% dominance in 2025 reflects structural shipper outsourcing, with global contract logistics spending exceeding USD 1.2 Trillion as manufacturers and retailers prioritize variable-cost transport and warehousing over owned assets.

- 2PL's 27.4% share remains anchored by traditional asset-heavy carriers and freight forwarders, particularly in ocean and rail, where dedicated capacity is critical for bulk commodity flows and long-haul corridors.

- Roadways' 59.2% majority is underpinned by global truck freight volumes exceeding 22 Trillion tonne-kilometers in 2024, with e-commerce last-mile delivery and regional manufacturing networks as the primary volume drivers.

- Asia Pacific's 48.7% global dominance reflects China's USD 2.5 Trillion domestic freight economy and India's National Logistics Policy targeting logistics cost reduction from 14% to 8% of GDP by 2030.

- Cross-border e-commerce parcel shipments reached approximately 125 Billion units in 2024, driven by marketplaces such as Amazon, Alibaba, Shein, and Temu, and they are projected to double by 2030.

- 4PL services represent the highest-growth model tier at an estimated 5.2% CAGR through 2030, driven by multinational shippers outsourcing end-to-end supply-chain orchestration to integrators like DHL and Ceva.

Global Logistics Market Overview

Logistics refers to the planning, execution, and control of the movement and storage of goods, services, and information across the supply chain. The global market spans freight transportation (road, rail, sea, air), warehousing, value-added services, customs brokerage, and end-to-end supply-chain management. Service delivery ranges from traditional asset-based 2PL carriers to integrated 3PL contract logistics and strategic 4PL orchestration.

The industry operates at the intersection of global trade flows, manufacturing localization, e-commerce expansion, and digital transformation. Growth is supported by macro drivers such as multi-trillion-dollar infrastructure programs, Free Trade Agreement (FTA) expansion, supply-chain diversification post-pandemic, and the rapid rollout of AI, IoT, and autonomous technologies across warehousing and transport.

Market Dynamics

To evaluate market opportunities, Request Sample

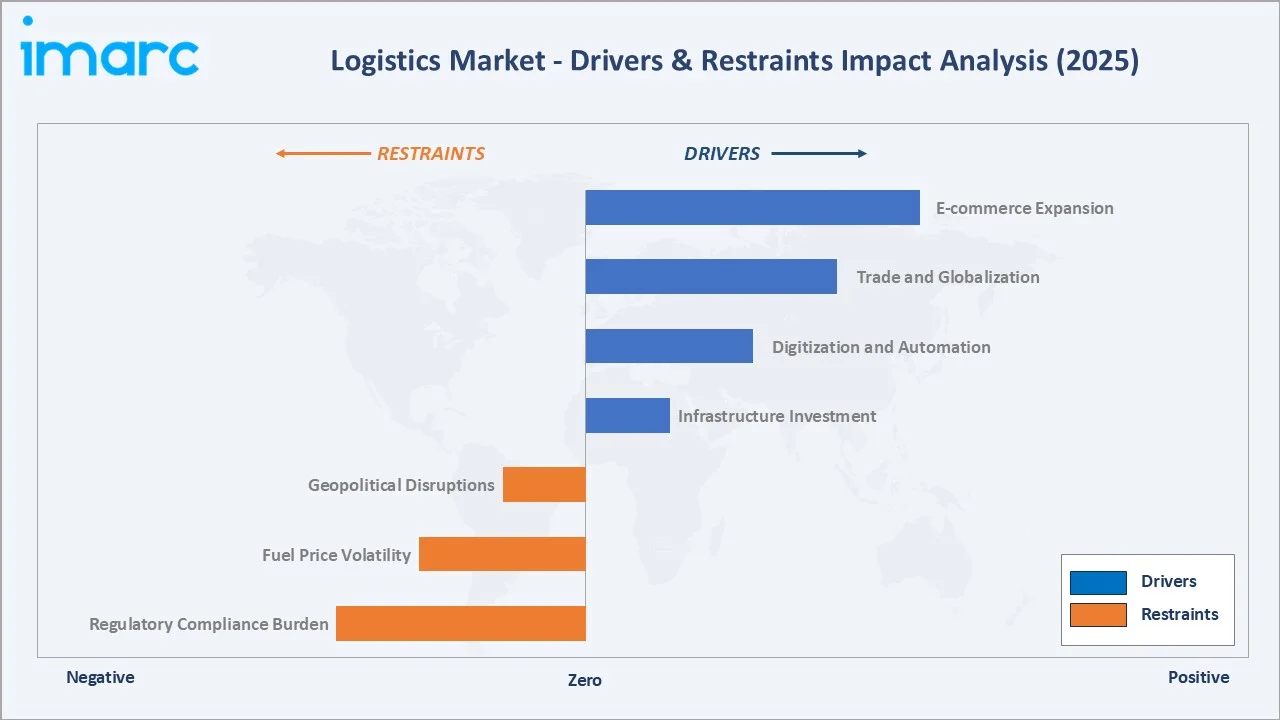

Market Drivers

- E-commerce Expansion: Global e-commerce sales crossed USD 4.4 Trillion in 2023 and are projected to exceed USD 6.8 Trillion by 2028. This is creating sustained demand for last-mile delivery, parcel networks, and fulfillment warehousing. Major retailers such as Amazon, JD.com, and Alibaba Cainiao continue to scale regional logistics capacity aggressively.

- Trade and Globalization: Global merchandise trade remained in the range of approximately USD 23–25 trillion in 2024, based on WTO trade statistics, supported by expanding regional trade integration such as RCEP and AfCFTA. These cross-border flows are directly lifting ocean, air, and cross-border road freight volumes.

- Digitization and Automation: Logistics technology investment reached USD 36 Billion in 2024, according to McKinsey. Digital freight matching platforms, transportation management systems (TMS), and warehouse robotics are reducing empty miles, accelerating throughput, and compressing logistics cost per shipment.

- Infrastructure Investment: Governments globally are scaling logistics infrastructure. India's PM Gati Shakti plan mobilized 15 Lakh Crore in multi-modal corridors. The U.S. Infrastructure Investment and Jobs Act allocated USD 550 Billion to ports, highways, and rail. The EU Connecting Europe Facility targets USD 30 Billion for trans-European transport networks through 2027.

Market Restraints

- Geopolitical Disruptions: Geopolitical disruptions such as Red Sea rerouting, U.S.–China tariff tensions, and the Russia–Ukraine conflict are forcing longer shipping routes, inflating insurance premiums, and significantly increasing transit times, with Asia–Europe routes experiencing delays of up to two weeks.

- Fuel Price Volatility: Diesel and jet fuel account for approximately 25–40% of operating costs across road and air freight, while Brent crude price fluctuations in the range of USD 65–95 per barrel in 2024 have contributed to significant margin pressure for asset-heavy carriers.

- Regulatory Compliance Burden: CBAM in Europe, ELD mandates in North America, and carbon disclosure requirements impose substantial compliance costs, particularly on small and mid-size carriers operating across multiple jurisdictions.

Market Opportunities

- Nearshoring and Supply-Chain Diversification: Mexico became the top U.S. trading partner in 2023, with cross-border freight volumes continuing to expand, supported by nearshoring trends and increased manufacturing integration across North America. This shift is creating sustained opportunities for 3PL and cross-border trucking operators across North America.

- Green Logistics and Electrification: Sustainable logistics investment is accelerating globally, driven by electrification of transport fleets, decarbonization initiatives, and regulatory pressures, with annual spending estimated in the tens of billions of dollars. Fleet electrification, SAF (sustainable aviation fuel) adoption, and green shipping corridors are opening new service-premium tiers for asset operators and 4PL providers.

Market Challenges

- Labor and Driver Shortage: The American Trucking Associations reported that the U.S. trucking industry experienced a driver shortage of around 80,000, reaching a historic high, highlighting persistent labor constraints despite rising wages and ongoing recruitment efforts.

- Cybersecurity Risks: Ransomware attacks on logistics IT systems, as seen in the 2023 DP World and Expeditors incidents, are disrupting port and freight operations and forcing material investment in OT security.

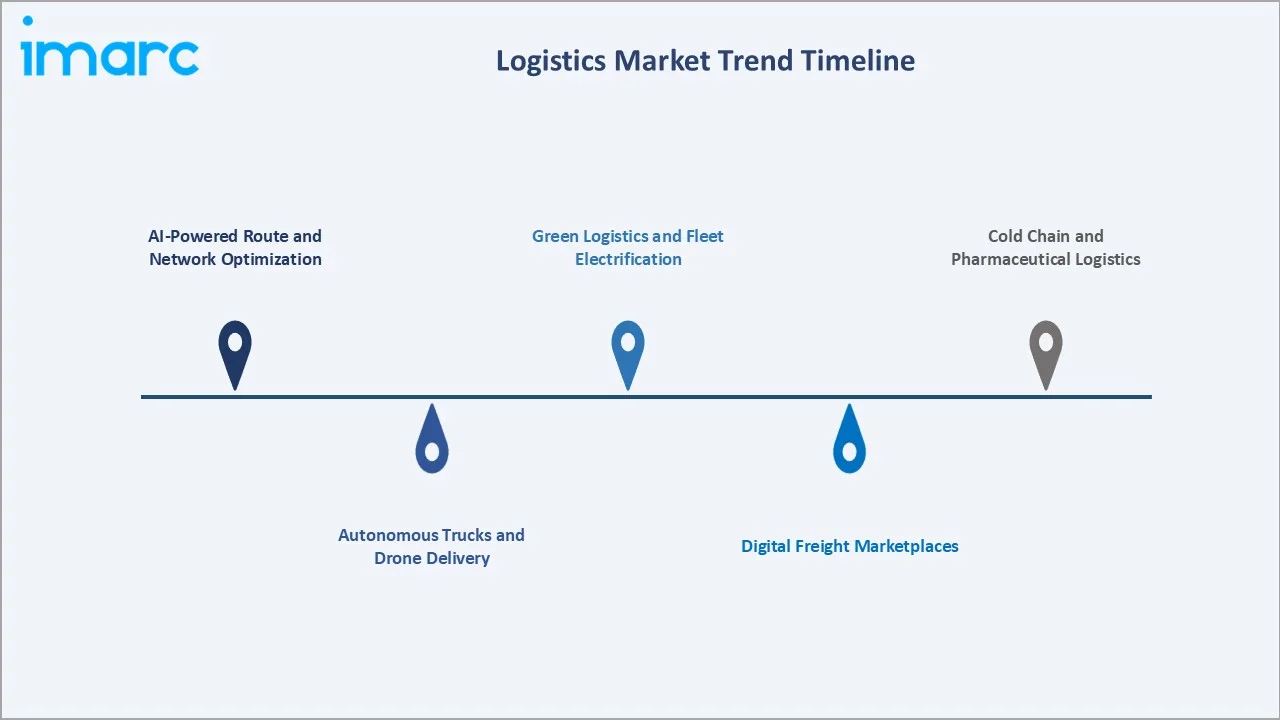

Emerging Market Trends

1. AI-Powered Route and Network Optimization

Artificial intelligence is reshaping freight network design, real-time routing, and load consolidation. Leading 3PLs report 6-12% reductions in transportation cost after AI deployment. Platforms such as Project44, FourKites, and FreightWaves are embedding predictive ETA and exception management into mainstream shipper workflows.

2. Autonomous Trucks and Drone Delivery

Level-4 autonomous trucking is entering commercial corridors in the U.S. Sun Belt through operators such as Aurora, Kodiak, and Gatik. Drone delivery is scaling in select Chinese, U.S., and GCC markets. These technologies are projected to unlock structural labor cost savings starting in 2026-2028.

3. Green Logistics and Fleet Electrification

Electrified last-mile vans, hydrogen-fuel-cell tractors, and sustainable aviation fuel (SAF) adoption are accelerating. Amazon’s partnership with Rivian includes a commitment to deploy 100,000 electric delivery vans by 2030 under its Climate Pledge, positioning fleet electrification as a core lever for reducing emissions in its logistics operations.

4. Digital Freight Marketplaces

Digital freight matching platforms such as Uber Freight, Convoy (pre-wind-down), and Manbang (Full Truck Alliance) are aggregating fragmented trucking capacity. The rapid growth of digital freight platforms is enhancing real-time pricing visibility and increasing spot-market participation, leading to margin compression for traditional brokers.

5. Cold Chain and Pharmaceutical Logistics

Biologics, vaccines, and temperature-sensitive food shipments are lifting demand for validated cold chain networks. Americold and Lineage Logistics are investing heavily in automated cold storage, while air cargo carriers are expanding CEIV Pharma-certified capacity across major gateways.

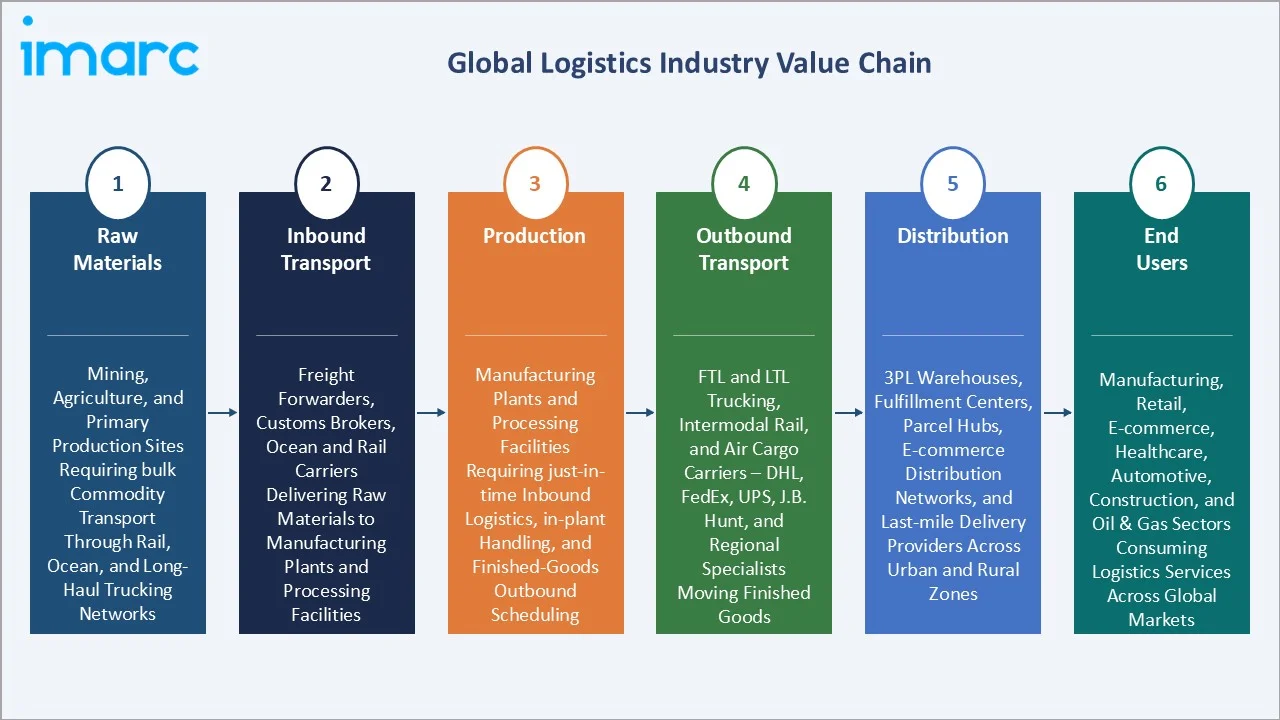

Industry Value Chain Analysis

The global logistics industry value chain spans six integrated stages from raw material sourcing through end-user consumption. Each stage presents distinct competitive dynamics, asset intensity, and digital investment requirements relevant to the overall logistics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Mining, agriculture, and primary production sites requiring bulk commodity transport through rail, ocean, and long-haul trucking networks |

|

Inbound Transport |

Freight forwarders, customs brokers, ocean and rail carriers delivering raw materials to manufacturing plants and processing facilities |

|

Production |

Manufacturing plants and processing facilities requiring just-in-time inbound logistics, in-plant handling, and finished-goods outbound scheduling |

|

Outbound Transport |

FTL and LTL trucking, intermodal rail, and air cargo carriers – DHL, FedEx, UPS, J.B. Hunt, and regional specialists moving finished goods |

|

Distribution |

3PL warehouses, fulfillment centers, parcel hubs, e-commerce distribution networks, and last-mile delivery providers across urban and rural zones |

|

End Users |

Manufacturing, retail, e-commerce, healthcare, automotive, construction, and oil & gas sectors consuming logistics services across global markets |

3PL and 4PL providers capture the highest strategic value by integrating transport, warehousing, technology, and analytics into turnkey supply-chain solutions. At the same time, digital freight platforms and direct-to-shipper e-commerce fulfillment are reshaping intermediation economics, allowing asset-light aggregators to capture margin traditionally held by traditional brokers and forwarders.

Technology Landscape in the Logistics Industry

Transportation Management Systems (TMS) and Visibility

Cloud-based TMS platforms from Oracle, SAP, Blue Yonder, and Manhattan Associates are standardizing shipment planning, carrier procurement, and freight audit. Real-time visibility solutions, including Project44 and FourKites, are becoming standard across large enterprise supply chains, enabling improved ETA accuracy, reduced dwell time, and enhanced on-time performance.

Warehouse Automation and Robotics

Warehouse automation is accelerating globally, led by providers such as AutoStore, Symbotic, and Geek+, while Amazon operates more than 750,000 robots across its fulfillment network. Automation technologies are reducing pick-and-pack labor requirements and improving SKU density and order accuracy across e-commerce and retail fulfillment operations.

AI, IoT, and Blockchain Integration

AI-powered route optimization, demand forecasting, and predictive maintenance are increasingly embedded across leading 3PL operations, while IoT-enabled sensors are expanding shipment visibility through real-time tracking of temperature, location, and handling conditions. Blockchain initiatives, including Maersk and IBM’s TradeLens (discontinued in 2023), have contributed to the development of more transparent and auditable supply chain documentation frameworks.

Autonomous Vehicles and Electrification

Level-4 autonomous trucks are running freight corridors between Dallas, Phoenix, and Houston. Battery electric trucks from Tesla Semi, Volvo VNR Electric, and BYD are scaling in port drayage and regional haul. Sustainable aviation fuel blends and methanol-powered ocean vessels are accelerating decarbonization commitments across leading carriers and shippers worldwide.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global logistics market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on model type and transportation mode.

By Model Type

3PL leads the global logistics market by model type with a 56.3% share in 2025. Demand is driven by structural shipper outsourcing, integrated contract logistics, and rising e-commerce fulfillment complexity. The global 3PL sub-segment was valued at approximately USD 3.31 Trillion in 2025 and is projected to grow at 4.1% CAGR through 2030. DHL Supply Chain, Ceva, and XPO dominate this tier, with regional specialists scaling fast across Asia Pacific.

2PL accounts for 27.4% of global model demand, anchored by asset-heavy carriers and traditional freight forwarders. This segment continues to serve bulk commodity flows and long-haul ocean and rail corridors. 4PL services represent 16.3% share and are the fastest-growing tier at approximately 5.2% CAGR, driven by multinational shippers outsourcing end-to-end supply-chain orchestration to integrators like DHL, Ceva, and Accenture Supply Chain.

By Transportation Mode

Roadways lead the global logistics market by transportation mode with a 59.2% share in 2025. Global road freight volumes account for a significant share of total freight activity, reaching tens of trillions of tonne-kilometers annually, supported by strong demand from manufacturing, retail, and e-commerce supply chains, driven by e-commerce last-mile delivery, regional manufacturing networks, and cross-border nearshoring activity between the U.S. and Mexico. Roadways remain the default short- and medium-haul mode due to door-to-door flexibility and capillary reach.

Seaways account for 18.1% of global transportation demand and remain the backbone of international trade, handling over 85% of global goods by weight. Railways represent 12.6% share, with particular strength in North American intermodal, European freight corridors, and China's Belt and Road rail network. Airways account for 10.1% but are the fastest-growing mode at approximately 4.6% CAGR through 2030, driven by cross-border e-commerce parcels, pharmaceuticals, and high-value electronics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

48.7% |

China trade scale, India Gati Shakti, ASEAN manufacturing, cross-border e-commerce |

|

North America |

20.5% |

U.S. nearshoring, Mexico cross-border freight, IIJA infrastructure funding, e-commerce scale |

|

Europe |

17.6% |

EU Green Deal, Connecting Europe Facility, CBAM implementation, multi-modal rail expansion |

|

Latin America |

7.2% |

Brazil agribusiness exports, Mexico manufacturing growth, Pacific Alliance trade corridors |

|

Middle East & Africa |

6.0% |

GCC logistics hubs, Saudi Vision 2030, AfCFTA rollout, Suez trade corridor |

Asia Pacific commands 48.7% global revenue share in 2025. China is the single largest national logistics market, combining massive manufacturing volumes with a USD 2.5 Trillion domestic freight economy. India's National Logistics Policy and the PM Gati Shakti multi-modal plan target structural cost reduction from 14% to 8% of GDP by 2030, creating a long runway for 3PL growth. Asia Pacific is also forecast to be the fastest-growing region, advancing at approximately 4.3% CAGR through 2034.

North America holds 20.5% of global revenue, anchored by U.S.-Mexico cross-border freight that exceeded USD 860 Billion in 2024. The U.S. is the world's largest 3PL market, with Amazon, FedEx, UPS, and DHL leading parcel and contract logistics volumes. The Infrastructure Investment and Jobs Act continues to channel USD 550 Billion into ports, highways, and rail corridors through 2030.

Europe holds 17.6%, characterized by tight CO2 regulations, multi-modal rail expansion, and robust contract logistics demand across Germany, France, and the Netherlands. The EU's Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase in January 2026, reshaping cross-border compliance flows. Latin America accounts for 7.2%, led by Brazilian agribusiness exports and Mexican manufacturing growth. The Middle East and Africa represent 6.0%, driven by GCC logistics hubs, Saudi Vision 2030 investments, and AfCFTA trade integration.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Deutsche Post AG |

DHL Group |

Leader |

Global integrated express, contract logistics scale |

|

FedEx |

FedEx |

Leader |

Global express network, e-commerce parcel leadership |

|

United Parcel Service of America |

UPS |

Leader |

North America parcel dominance, healthcare logistics |

|

DSV |

DSV, Schenker (acquired) |

Leader |

Freight forwarding scale, post-Schenker global reach |

|

CEVA Logistics |

CEVA Logistics |

Leader |

Contract logistics, automotive and e-commerce |

|

Expeditors International of Washington |

Expeditors |

Leader |

Freight forwarding, customs brokerage excellence |

|

C.H. Robinson Worldwide, Inc. |

C.H. Robinson |

Leader |

Non-asset 3PL, digital freight matching platform |

|

J.B. Hunt Transport |

J.B. Hunt Transport |

Challenger |

North American intermodal rail leadership |

|

XPO |

XPO |

Challenger |

Less-than-truckload North America leadership |

|

Americold |

Americold |

Challenger |

Temperature-controlled warehousing leadership |

The global logistics market's competitive landscape is moderately fragmented. Global integrators with deep multi-modal networks compete alongside specialist 3PLs and regional asset-heavy carriers. Leading players compete on network density, digital platform capability, vertical specialization, and sustainability credentials. Strategic acquisitions are a key tool - DSV acquired DB Schenker from Deutsche Bahn in 2024-2025 for approximately EUR 14.3 Billion, creating the world's largest freight forwarder.

Key Company Profiles

Deutsche Post DHL Group

Deutsche Post DHL Group, headquartered in Bonn, Germany, is the world's largest logistics company. The group operates across DHL Express, DHL Supply Chain, DHL Global Forwarding, DHL eCommerce, and Deutsche Post mail divisions, serving over 220 countries with approximately 600,000 employees.

- Product & Platform Portfolio: The group's portfolio spans international express parcels, contract logistics, freight forwarding (ocean and air), e-commerce fulfillment, and domestic German mail operations, with dedicated vertical practices for healthcare, automotive, and technology.

- Recent Developments: In 2024, DHL continued to invest in green logistics with the addition of SAF offtake agreements and electric delivery vehicles. Deutsche Bahn completed the sale of DB Schenker to DSV in 2024-2025, intensifying competition for DHL Global Forwarding.

- Strategic Focus: DHL's Strategy 2030 centers on Quality Leadership, digitization through MyDHL+ and supply-chain control towers, sustainable logistics leadership including fleet electrification, and disciplined capital return through share buybacks and dividends.

FedEx Corp.

FedEx Corporation, headquartered in Memphis, Tennessee, is a global leader in transportation, e-commerce, and business services. Founded in 1971, FedEx serves more than 220 countries and territories through FedEx Express, FedEx Ground, and FedEx Freight operating companies.

- Product & Platform Portfolio: FedEx's portfolio spans FedEx Express international air cargo, FedEx Ground parcel delivery, FedEx Freight LTL trucking, FedEx Logistics customs and forwarding, and the FedEx Dataworks analytics platform supporting enterprise shippers.

- Recent Developments: In 2024, FedEx announced the planned spin-off of FedEx Freight into an independent publicly traded company, expected to complete in 2026. The company also accelerated its DRIVE cost-transformation program, targeting USD 4 Billion in structural cost savings.

- Strategic Focus: FedEx's strategy focuses on Network 2.0 integration of Express and Ground, LTL value unlocking through the Freight spin-off, and scaling data-driven shipper services via Dataworks and SenseAware platforms.

United Parcel Service, Inc.

United Parcel Service, Inc. (UPS), headquartered in Atlanta, Georgia, is one of the world's largest integrated package delivery and supply-chain management companies. Founded in 1907, UPS serves more than 200 countries and territories through its global small-package, freight, and SCS operations.

- Product & Platform Portfolio: UPS's portfolio covers Worldwide Express and Ground parcel delivery, UPS Supply Chain Solutions for contract logistics and forwarding, UPS Healthcare for cold-chain pharmaceutical logistics, and the Ware2Go digital fulfillment platform.

- Recent Developments: In 2024, UPS completed its acquisition of MNX Global Logistics, strengthening UPS Healthcare's time-critical and temperature-controlled pharmaceutical capabilities. The company also executed network rationalization to align capacity with post-pandemic e-commerce volumes.

- Strategic Focus: UPS's strategy centers on UPS Healthcare scale-out, SMB e-commerce penetration through Digital Access Program, and margin recovery through Network of the Future automation across its North American parcel operations.

Market Concentration Analysis

The global logistics market exhibits moderate fragmentation. The top five players - DHL Group, FedEx, UPS, DSV (post-Schenker), and Ceva - collectively account for 18-22% of global market revenue in 2025. The remaining market share is distributed across Expeditors, C.H. Robinson, J.B. Hunt, XPO, Americold, and a very long tail of regional asset-based carriers, freight forwarders, and local 3PL operators.

The market is experiencing a bifurcated dynamic. At the global integrator tier, consolidation is occurring through mega-deals such as the DSV-DB Schenker combination and CMA CGM's acquisitions of Ceva and Bollore Logistics. Simultaneously, Asia Pacific regional logistics players including Cainiao, SF Express, and Maersk's regional arms are building scale that is expected to reshape global rankings through 2034. This dual dynamic is intensifying competition across asset-heavy and asset-light models.

Investment & Growth Opportunities

Fastest-Growing Segments

4PL services are the highest-growth model sub-segment at an estimated 5.2% CAGR through 2030. Airways are the fastest-growing transport mode at approximately 4.6% CAGR, fueled by cross-border e-commerce parcels and high-value pharmaceuticals. Warehouse automation and cold chain logistics represent the premium technology growth opportunities, with automation investment exceeding USD 38 Billion globally in 2024.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by the PM Gati Shakti plan's USD 1.3 Trillion in multi-modal infrastructure and the National Logistics Policy targeting cost reduction from 14% to 8% of GDP. Southeast Asia's manufacturing shift, Mexico nearshoring, GCC logistics hubs, and AfCFTA rollout collectively represent major volume-growth opportunities for global and regional logistics operators.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. DSV acquired DB Schenker in 2024-2025 for approximately EUR 14.3 Billion. CMA CGM's Ceva acquired Bollore Logistics for EUR 4.85 Billion in February 2024. Venture capital continues to flow into digital freight platforms, warehouse robotics, and autonomous trucking. These are the primary focus areas for corporate and venture investment in the logistics industry through 2034.

Future Market Outlook (2026-2034)

The global logistics market forecast projects steady value expansion from USD 5.88 Trillion in 2025 to USD 8.23 Trillion by 2034 at a CAGR of 3.71%. Asia Pacific will retain regional leadership while accelerating structurally. North America and Europe will sustain value growth through nearshoring, e-commerce scaling, and regulatory-driven sustainability compliance cycles.

Three shifts will reshape the logistics market through 2034. Autonomous trucking and drone delivery will begin compressing labor-intensive cost structures starting in 2026-2028. Green logistics (electric fleets, SAF, methanol shipping) will emerge as a competitive differentiator and access requirement for major corporate shippers. Meanwhile, Asia Pacific regional giants such as Cainiao and SF Express will intensify global competitive pressure across freight forwarding and cross-border e-commerce fulfillment.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with logistics industry stakeholders, including executives at 3PL and 4PL providers, procurement and supply-chain directors at enterprise shippers, freight forwarders, port and airport operators, and institutional investors in transportation infrastructure. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include WTO global trade data, UNCTAD Review of Maritime Transport, IATA air cargo statistics, IRU road transport data, company annual reports, industry publications including Journal of Commerce, FreightWaves, and Logistics Management, and regional transport and customs authority databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global trade volumes, GDP growth rates, e-commerce penetration curves, freight tonnage data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic, geopolitical, and regulatory uncertainty.

Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Companies Covered | Deutsche Post AG, FedEx, United Parcel Service of America, DSV, CEVA Logistics, Expeditors International of Washington, C.H. Robinson Worldwide, Inc., J.B. Hunt Transport, XPO, Americold, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the logistics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global logistics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Logistics Market Report

The global logistics market was valued at USD 5.88 Trillion in 2025, driven by trade expansion, e-commerce growth, and accelerating supply-chain digitization across manufacturing, retail, and healthcare verticals worldwide.

The market is projected to reach USD 8.23 Trillion by 2034, growing at a CAGR of 3.71% during 2026-2034, supported by infrastructure investment, e-commerce scale, nearshoring, and rapid technology adoption across transport and warehousing.

Third-party logistics (3PL) leads with a 56.3% share in 2025, driven by structural shipper outsourcing, integrated warehousing and transport contracts, and rising complexity in global e-commerce fulfillment networks.

Roadways dominate with a 59.2% share in 2025, underpinned by global truck freight volumes exceeding 22 Trillion tonne-kilometers, last-mile e-commerce delivery, and cross-border nearshoring activity between the U.S. and Mexico.

Asia Pacific dominates with a 48.7% share in 2025. China's USD 2.5 Trillion domestic freight economy, India's Gati Shakti plan, and ASEAN manufacturing growth underpin regional leadership globally.

Key drivers include e-commerce expansion exceeding USD 6.3 Trillion in 2024, global trade volume growth, digitization and automation investment, infrastructure mega-programs, and structural nearshoring across North America and Europe.

Major players include Deutsche Post AG, FedEx, United Parcel Service of America, DSV, CEVA Logistics, Expeditors International of Washington, C.H. Robinson Worldwide, Inc., J.B. Hunt Transport, XPO, Americold, among other regional and specialist operators.

Airways are the fastest-growing transport mode, advancing at approximately 4.6% CAGR from 2025 to 2030, driven by cross-border e-commerce parcels, time-critical pharmaceuticals, and high-value electronics shipments.

Key opportunities include warehouse automation, cold chain expansion, India and Southeast Asia market scaling, 4PL control-tower services, green logistics including fleet electrification, and digital freight matching platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)