Medical Cyclotron Market Size, Share, Trends and Forecast by Type, Product Type, End User, and Region, 2026-2034

Global Medical Cyclotron Market Size, Share, Trends & Forecast (2026-2034)

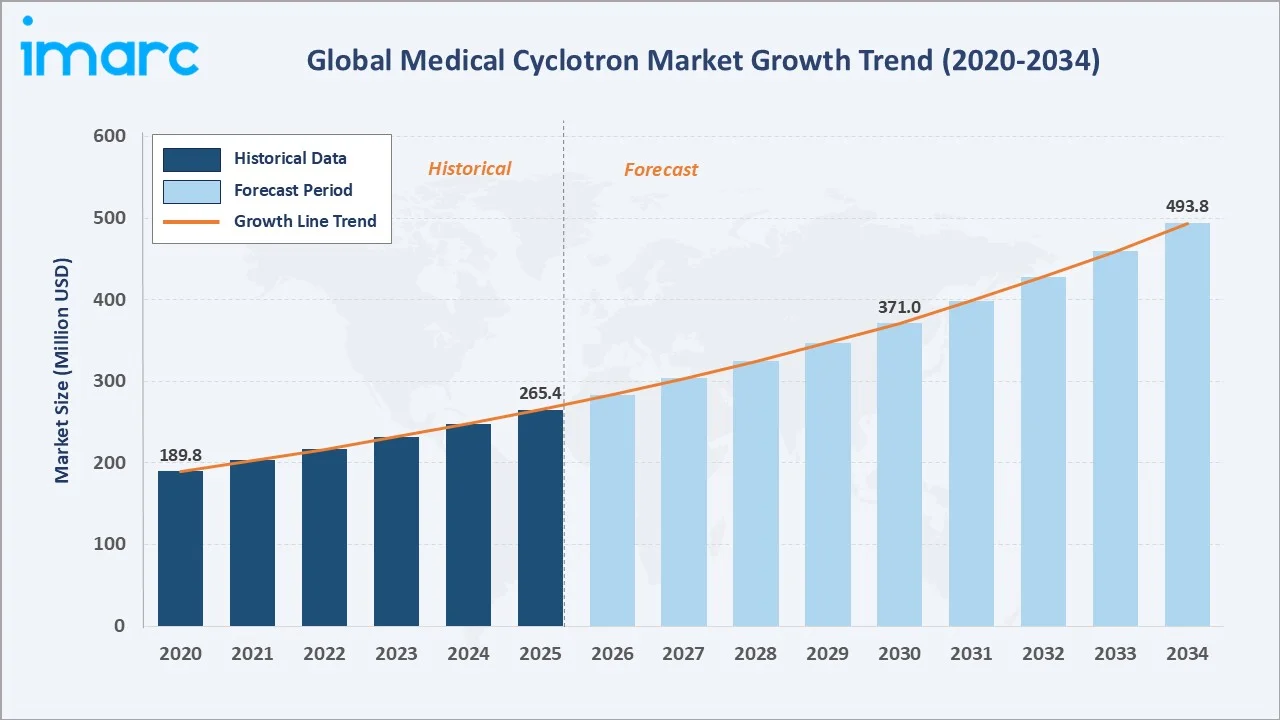

The global medical cyclotron market was valued at USD 265.4 Million in 2025 and is projected to reach USD 493.8 Million by 2034, exhibiting a CAGR of 6.93% during 2026-2034. Rising PET-CT procedure volumes, growing cancer burden, and expanding hospital-based radiopharmacy networks are the primary drivers shaping the market growth. In 2025, there are expected to be 2,041,910 new cases of cancer and 618,120 cancer-related deaths in the United States.

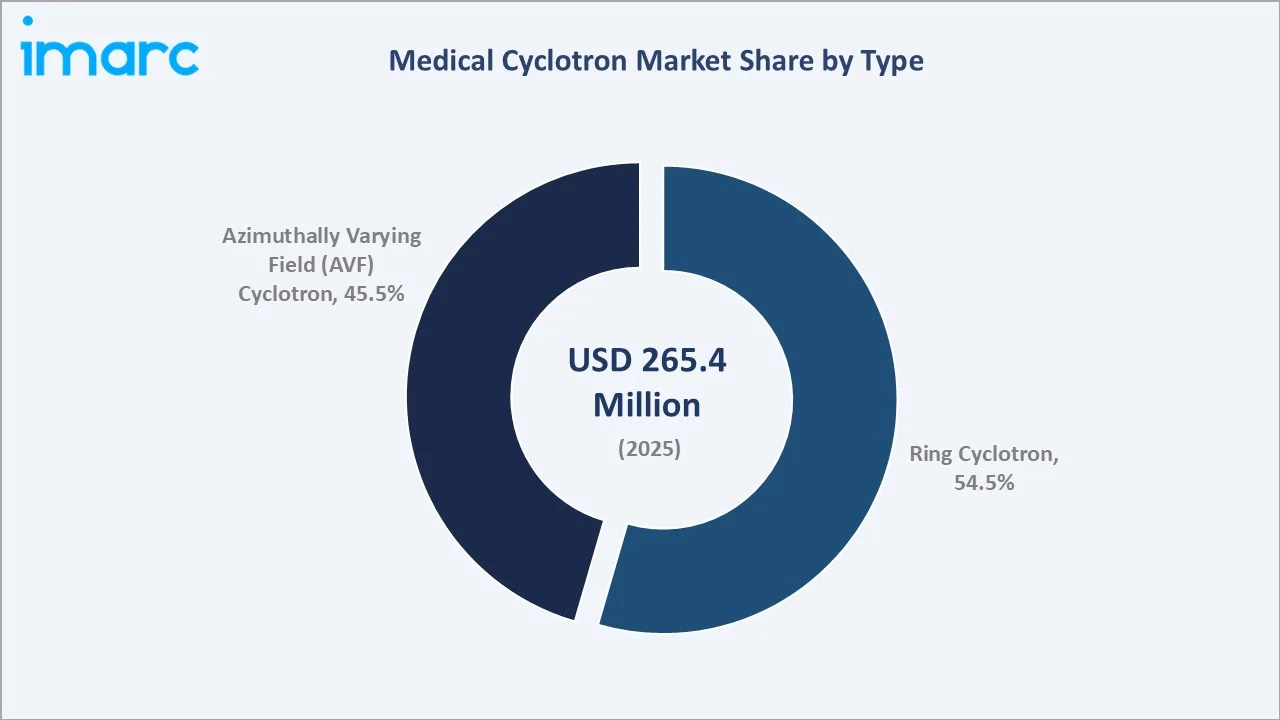

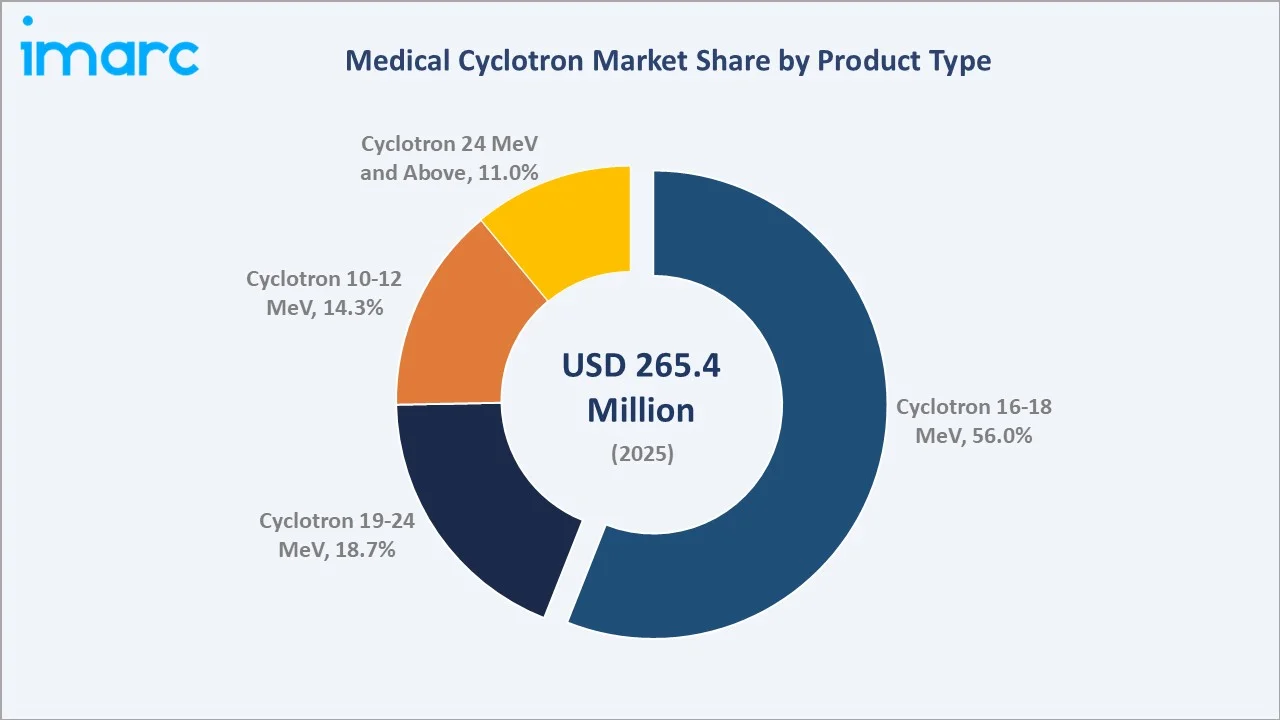

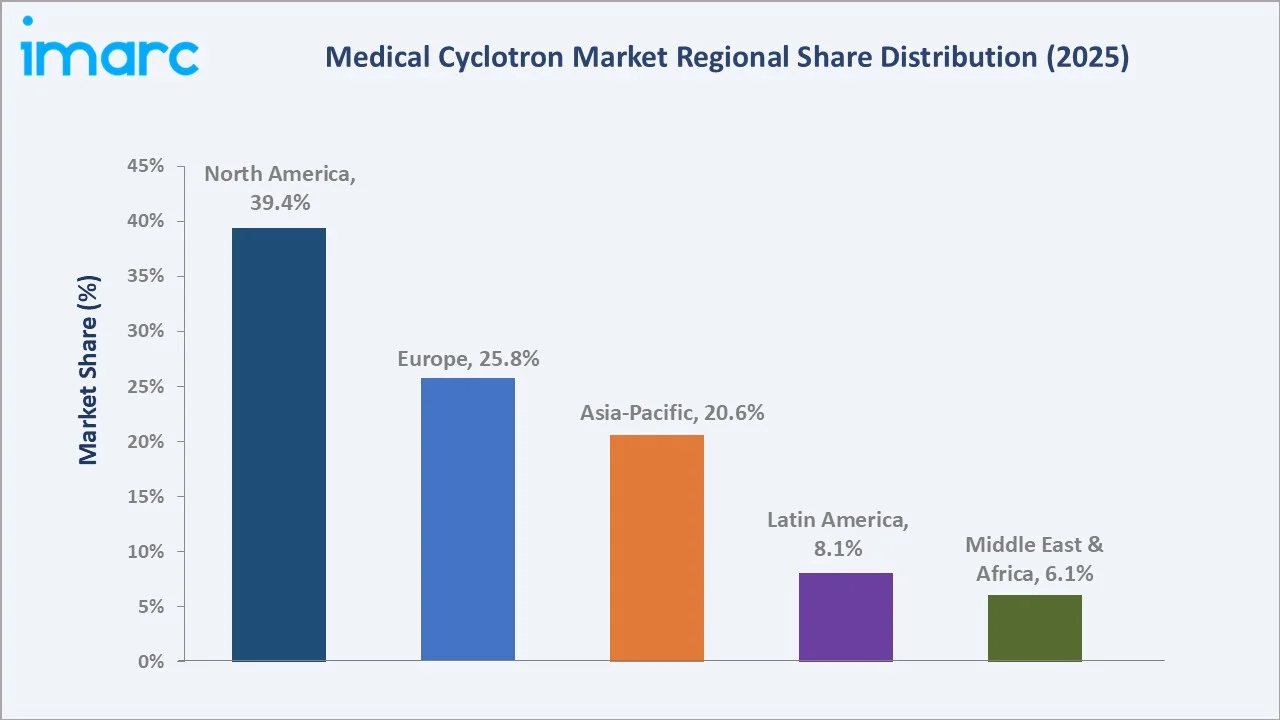

Ring cyclotron leads the type segment at 54.5%, cyclotron 16-18 MeV dominates the product type segment at 56.0%, and North America commands a 39.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 265.4 Million |

|

Forecast Market Size (2034) |

USD 493.8 Million |

|

CAGR (2026-2034) |

6.93% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.4%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (20.6%, 2025) |

|

Leading Type |

Ring Cyclotron (54.5%, 2025) |

|

Leading Product Type |

Cyclotron 16-18 MeV (56.0%, 2025) |

The global medical cyclotron market expanded from USD 189.8 Million in 2020 to USD 265.4 Million in 2025, supported by rising PET imaging adoption, expanding hospital-based radiopharmacy capacity, and steady reimbursement coverage. Anchored at USD 371.0 Million in 2030, the forecast to USD 493.8 Million by 2034 reflects accelerating theranostics demand and broader access to nuclear medicine across emerging healthcare systems.

To get more information on this market, Request Sample

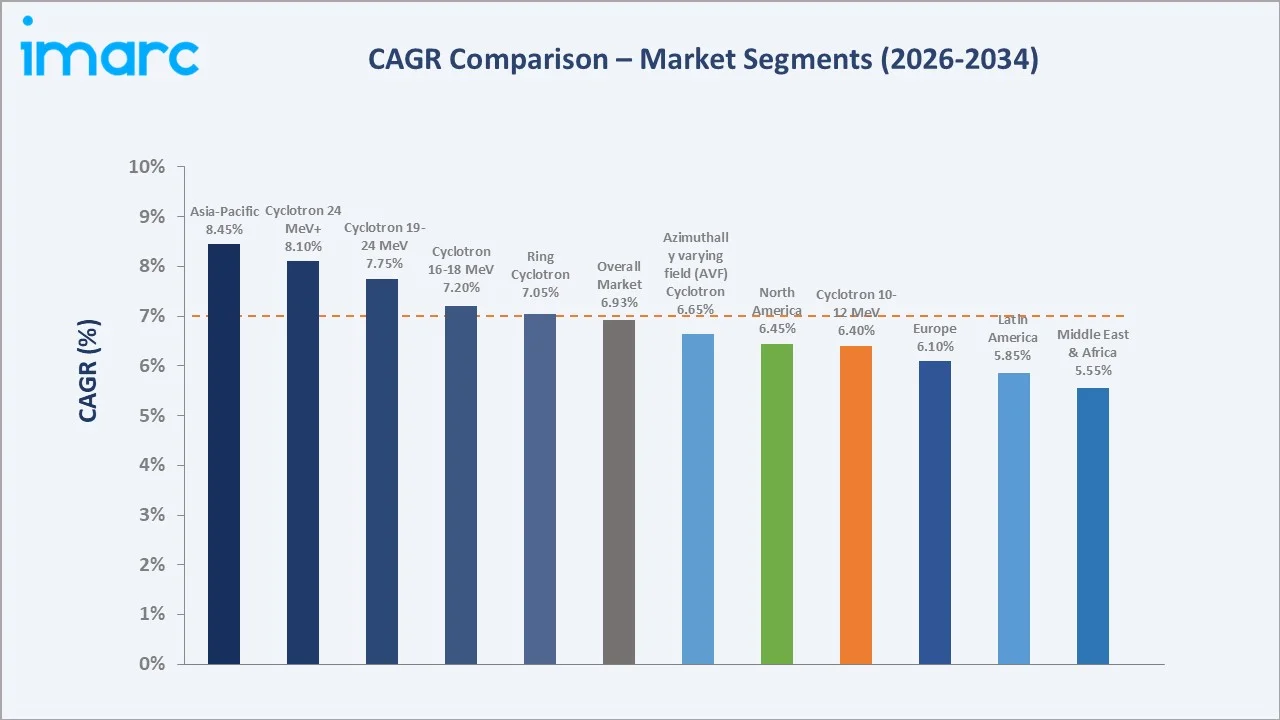

CAGR trajectories across type and product type sub-segments show high-energy cyclotrons and Asia-Pacific deployments expanding faster than the overall 6.93% market CAGR, driven by theranostics adoption and rising healthcare investment.

Executive Summary

The global medical cyclotron market is on a steady growth path from USD 189.8 Million in 2020 to USD 493.8 Million by 2034. Cyclotrons have moved from a research-only niche to a core hospital infrastructure asset for in-house production of short-lived PET radioisotopes. Rising PET-CT procedure volumes, growing oncology burden, and expanding theranostics pipelines are encouraging hospitals and radiopharmacies to invest in dedicated isotope production. Reimbursement coverage and supportive nuclear medicine policy frameworks are further reinforcing adoption.

Ring cyclotron dominates the type segment at 54.5% in 2025, supported by high beam-current capability, multi-isotope flexibility, and proven reliability for centralized PET radiopharmacy hubs. Cyclotron 16-18 MeV leads the product type segment at 56.0%, fueled by its versatile energy range that supports both fluorine-18 and a broader set of metallic radionuclides. North America commands 39.4%, anchored by the United States, where the FDA issued 15 approvals in oncology in the final three months of 2024, sustaining demand for diagnostic and theranostic isotopes across academic medical centers.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Ring Cyclotron - 54.5% share (2025) |

|

Second Type |

Azimuthally Varying Field (AVF) Cyclotron - 45.5% share (2025) |

|

Leading Product Type |

Cyclotron 16-18 MeV - 56.0% share (2025) |

|

Second Product Type |

Cyclotron 19-24 MeV - 18.7% share (2025) |

|

Leading Region |

North America - 39.4% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 20.6% share (2025) |

|

Top Companies |

IBA Worldwide, GE HealthCare, Sumitomo Heavy Industries, Ltd., Siemens, Mevion Medical Systems |

Key Analytical Observations Expanding on the Data Above:

- Ring cyclotron dominance at 54.5% is driven by its higher beam-current capability and ability to support multi-isotope production schedules in centralized radiopharmacy hubs. Reliability and proven service histories also reinforce its preference among large PET production facilities.

- Azimuthally Varying Field (AVF) cyclotron share at 45.5% is sustained by its compact footprint and lower siting cost, making it preferred for hospital-based PET centers and decentralized radiopharmacies. Improving compact-shielding designs are further expanding its addressable customer base.

- Cyclotron 16-18 MeV leadership at 56.0% reflects its versatility for routine fluorine-18 production while also supporting newer tracers, such as gallium-68 and copper-64. Operators value the balance between production yield and shielding requirements at this energy range.

- Cyclotron 19-24 MeV at 18.7% serves theranostics-focused centers requiring iodine-124, zirconium-89, and other metallic radionuclides for targeted alpha and beta therapies. Broader access to mid-energy cyclotrons also supports clinical research pipelines.

- North America at 39.4% leads through high PET-CT density, mature reimbursement coverage, and a strong base of academic medical centers running active radiopharmaceutical research programs. Robust public funding for cancer research further sustains regional investment. As per a national survey conducted by the American Association for Cancer Research (AACR) in 2025, 83% of participants supported boosting financial resources for cancer research.

Global Medical Cyclotron Market Overview

Medical cyclotrons are charged-particle accelerators, typically operating between 10 and 30 MeV, that produce short-lived radioisotopes used in PET imaging, single-photon imaging, and emerging theranostic therapies. They form the upstream backbone of nuclear medicine.

The global ecosystem integrates magnet and RF component suppliers, cyclotron OEMs, targetry and radiochemistry module providers, hospital radiopharmacies, regulatory authorities, and clinical end users, together enabling reliable, on-demand availability of diagnostic and therapeutic isotopes.

Market Dynamics

To evaluate market opportunities, Request Sample

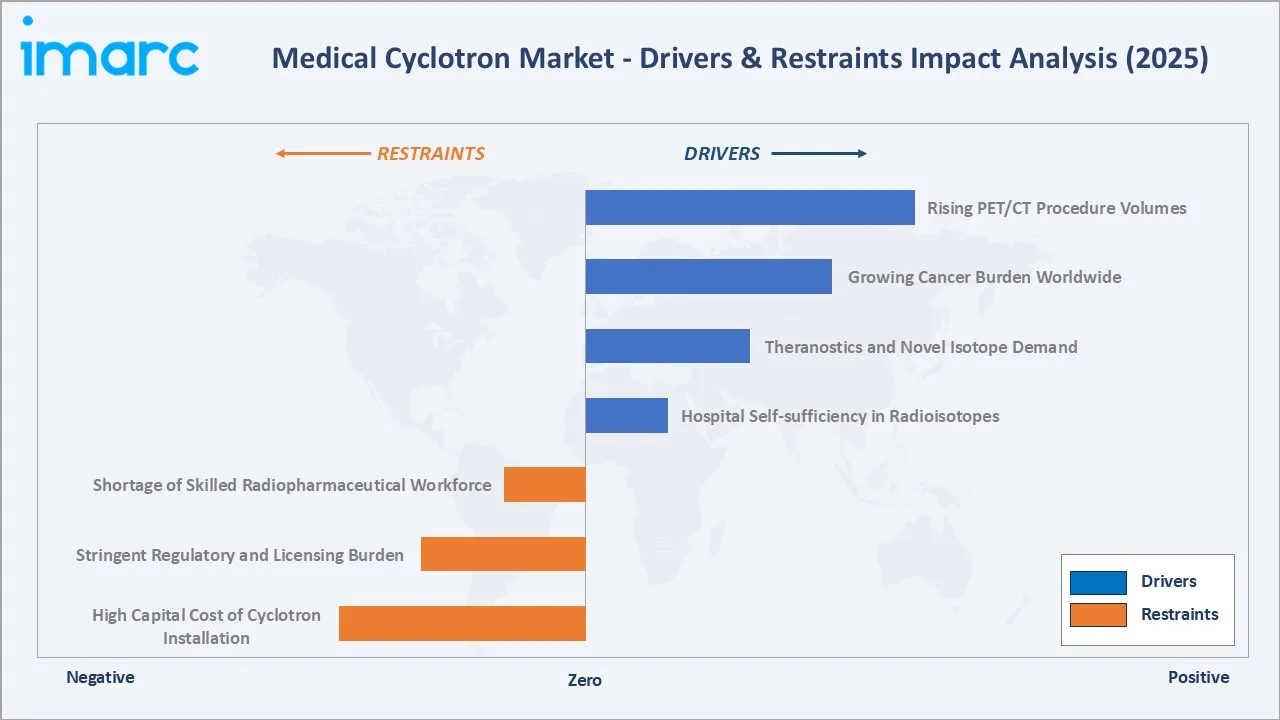

Market Drivers

- Rising PET/CT Procedure Volumes: Increasing utilization of PET-CT for oncology staging, neurology, and cardiology is driving sustained demand for short-lived radioisotopes, encouraging hospitals to invest in on-site cyclotron capacity. The newest PET/CT scanners are highly dependable and can detect cancer with an accuracy of up to 96.4%.

- Growing Cancer Burden Worldwide: Rising incidence of cancers requiring molecular imaging is expanding diagnostic and theranostic isotope demand. Higher case volumes are pushing healthcare systems to localize radioisotope production closer to clinical end users.

- Theranostics and Novel Isotope Demand: Growing clinical interest in theranostic pairs, such as gallium-68 / lutetium-177 and copper-64 / copper-67, is supporting demand for mid-energy cyclotrons capable of producing metallic radionuclides at clinical scale.

- Hospital Self-sufficiency in Radioisotopes: Supply disruptions of reactor-produced isotopes push hospitals to invest in cyclotron-based alternatives. In-house production also reduces reliance on long-distance distribution of short-lived tracers.

Market Restraints

- High Capital Cost of Cyclotron Installation: Total installed cost for a hospital cyclotron suite, including shielding, hot cells, and radiochemistry modules, can exceed several million US dollars, limiting adoption among smaller community hospitals. Per the IAEA, in 2022, only 10-12% of radiopharmaceuticals globally were produced via cyclotrons, with the majority of installed capacity concentrated in high-income markets and limited penetration across developing regions.

- Stringent Regulatory and Licensing Burden: Site licensing, radiation safety approvals, and radiopharmaceutical GMP compliance add multi-year timelines and recurring audit costs. Heterogeneous national regulations also complicate cross-border deployment for OEMs.

- Shortage of Skilled Radiopharmaceutical Workforce: Limited availability of trained nuclear pharmacists, cyclotron engineers, and radiochemistry technicians constrains capacity expansion. Long training cycles and specialized credentialing slow new facility ramp-ups in many regions.

Market Opportunities

- Theranostic Isotope Pipeline Expansion: Growing late-stage development of targeted radioligand therapies is opening recurring isotope-supply contracts for cyclotron operators. Multi-year supply agreements with pharma sponsors offer attractive utilization profiles for mid-energy systems.

- Compact and Self-shielded System Adoption: New compact, self-shielded cyclotron designs are reducing siting costs and enabling deployment in space-constrained hospital basements. This is unlocking a previously untapped mid-tier hospital segment across emerging markets.

Market Challenges

- Helium-3 and Critical Component Supply Volatility: Constrained supply of certain ion-source gases, RF amplifier tubes, and specialty target materials creates sourcing risks for OEMs and end users. Component lead times have lengthened across multiple geographies in recent years.

- Decommissioning and Radiation Waste Management: End-of-life decommissioning of activated cyclotron components and disposal of radioactive waste add lifecycle costs and regulatory complexity. Long-term liability frameworks remain inconsistent across jurisdictions.

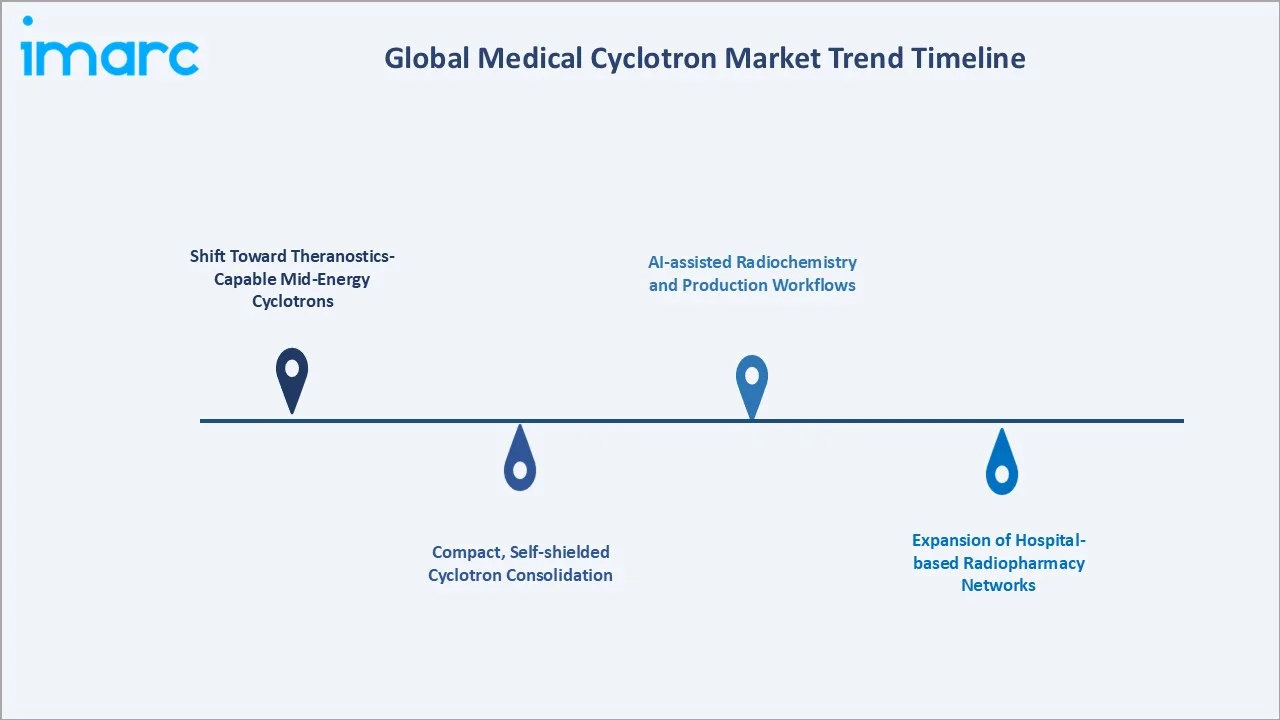

Emerging Market Trends

1. Shift Toward Theranostics-Capable Mid-Energy Cyclotrons

Cyclotrons in the 19-24 MeV range are gaining share as hospitals and radiopharmacies prepare for routine production of theranostic isotopes, such as zirconium-89, copper-64, and iodine-124. This shift is broadening the clinical role of cyclotrons beyond traditional fluorine-18 production.

2. Compact, Self-shielded Cyclotron Consolidation

Compact self-shielded systems integrating the accelerator, hot cells, and chemistry modules in a single vault are replacing traditional bunker-style installations. This trend is reducing civil construction costs and shortening commissioning timelines for new sites.

3. Artificial Intelligence (AI)-assisted Radiochemistry and Production Workflows

Operators are integrating digital twins, predictive maintenance, and AI-driven yield optimization into cyclotron operations, enabling automated batch scheduling, real-time quality control, and reduced unplanned downtime. As per the IMARC Group, the global AI in healthcare market reached USD 9.8 Billion in 2025, signaling broader adoption of AI tooling across nuclear medicine workflows.

4. Expansion of Hospital-based Radiopharmacy Networks

Health systems are increasingly building or partnering with hospital-based radiopharmacies operating dedicated cyclotrons to serve regional clusters of PET imaging centers. This network model is improving isotope availability while spreading capital costs across multiple downstream sites.

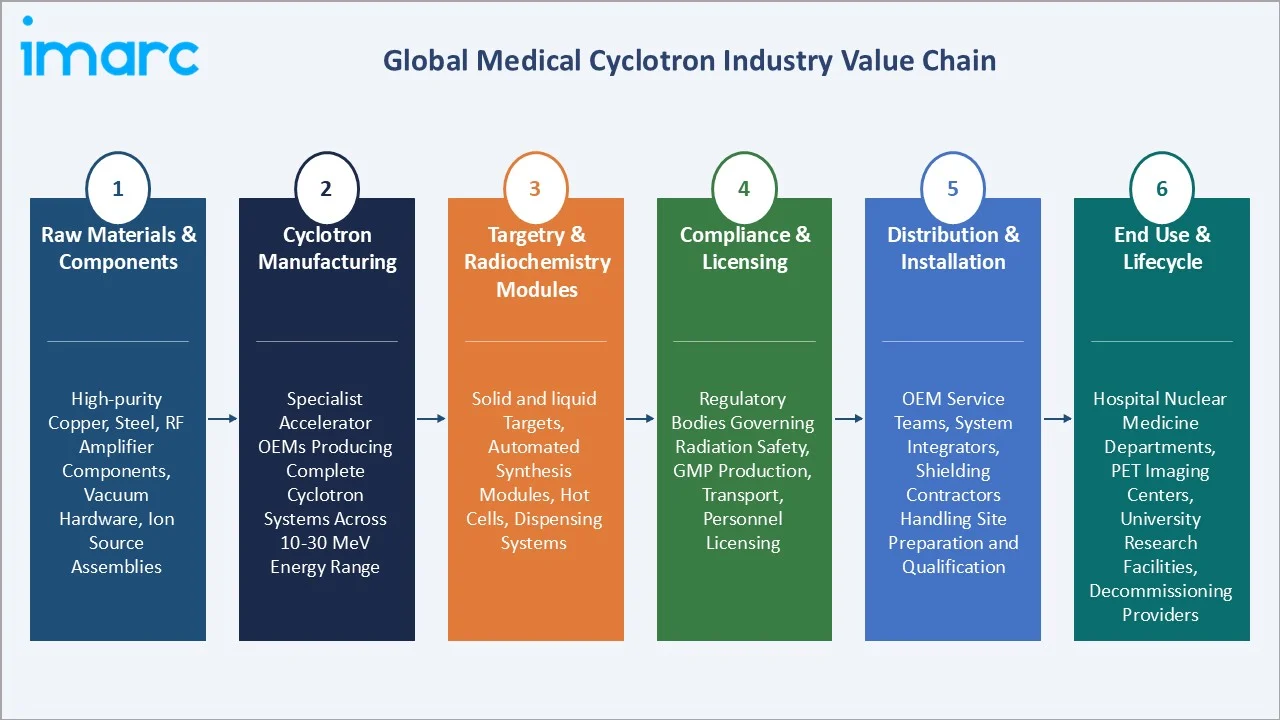

Industry Value Chain Analysis

The medical cyclotron value chain spans six stages from raw component supply through end-of-life decommissioning. Cyclotron manufacturing and targetry integration capture the highest value-add, while installation, qualification, and long-term service generate recurring downstream revenue in this regulated category.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Suppliers of high-purity copper and steel for magnets, RF amplifier components, vacuum hardware, and ion source assemblies serving accelerator OEMs |

|

Cyclotron Manufacturing |

Specialist accelerator OEMs producing complete cyclotron systems across the 10-30 MeV energy range for hospital, radiopharmacy, and research deployments |

|

Targetry & Radiochemistry Modules |

Providers of solid and liquid targets, automated synthesis modules, hot cells, and dispensing systems supporting downstream radiopharmaceutical production |

|

Compliance & Licensing |

National and international regulatory bodies governing radiation safety, GMP radiopharmaceutical production, transport, and personnel licensing |

|

Distribution & Installation |

OEM service teams, system integrators, and shielding contractors handling site preparation, commissioning, and qualification of cyclotron suites |

|

End Use & Lifecycle |

Hospital nuclear medicine departments, PET imaging centers, university research facilities, and accredited decommissioning service providers |

Vertically integrated players that combine cyclotron design, targetry, and chemistry-module manufacturing in-house tend to achieve superior service economics and lifecycle margins versus pure accelerator suppliers relying on third-party chemistry partners.

Technology Landscape in the Global Medical Cyclotron Industry

Magnet and Beam Technology Innovation

Modern medical cyclotrons increasingly use compact warm-iron magnets with optimized pole geometry to deliver higher beam currents within smaller footprints. Superconducting magnet designs are progressing toward commercial deployment, promising further reductions in vault size and energy consumption per produced curie.

Targetry and Radiochemistry Automation

Solid-target systems for metallic radionuclides, such as zirconium-89 and copper-64, are becoming standard alongside legacy liquid-target fluorine-18 capability. Fully automated dispensing and quality-control modules are improving yield consistency, reducing operator radiation exposure, and supporting GMP compliance at scale.

Digital Connectivity and Predictive Maintenance

Connected cyclotron systems with cloud-based monitoring, remote diagnostics, and predictive maintenance dashboards are enabling real-time tracking of beam parameters and component health. These features help operators schedule preventive servicing, reduce unplanned downtime, and optimize daily isotope batch yields.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Ring Cyclotron |

54.5% |

2025 |

| Product Type | Cyclotron 16-18 MeV |

56.0% |

2025 |

| End User | Hospitals | 40.2% |

2025 |

|

Region |

North America |

39.4% |

2025 |

By Type

Ring cyclotron commands a 54.5% majority share in 2025, supported by high beam-current capability, robust multi-isotope production schedules, and proven reliability at large radiopharmacy hubs. These systems are preferred where centralized output volumes justify higher capital outlay.

To get more information on this market, Request Sample

Azimuthally varying field (AVF) cyclotron at 45.5% in 2025 serves hospital-based PET centers and decentralized radiopharmacies that prioritize compact footprint and lower siting cost. These systems are also preferred where dedicated single-isotope production schedules dominate, with continued growth driven by improvements in compact magnet design and self-shielding solutions.

By Product Type

Cyclotron 16-18 MeV dominates with 56.0% share in 2025, reflecting its versatility for routine fluorine-18 production while also supporting metallic radionuclides, such as gallium-68 and copper-64. The energy range balances production yield against shielding cost, making it the workhorse choice for most radiopharmacies. It is also widely supported by OEM service networks across leading regions.

Cyclotron 19-24 MeV holds 18.7% share, supporting theranostic-grade isotopes, such as zirconium-89 and iodine-124. This energy range enables flexible production of both diagnostic and emerging therapeutic isotopes, positioning this segment as a preferred choice for mid- to high-capacity clinical and research facilities.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.4% |

High PET imaging procedure density, mature reimbursement frameworks, and strong public funding for nuclear medicine research |

|

Europe |

25.8% |

Established radiopharmacy networks, supportive cross-border isotope supply arrangements, and growing investment in theranostic clinical pipelines |

|

Asia-Pacific |

20.6% |

Expanding hospital infrastructure, rising oncology burden, growing healthcare expenditure, and supportive government initiatives for nuclear medicine |

|

Latin America |

8.1% |

Increasing access to PET imaging in major urban centers, growing private healthcare investment, and rising public sector capacity-building initiatives |

|

Middle East and Africa |

6.1% |

Expanding cancer care infrastructure, growing investment in tertiary hospitals, and increasing focus on regional self-sufficiency in radioisotope supply |

North America at 39.4% in 2025 leads the global market, supported by dense PET-CT installed bases, mature reimbursement coverage, and a strong network of academic medical centers operating active radiopharmaceutical research programs. Well-established service ecosystems and broad nuclear medicine training pipelines further reinforce regional dominance.

Asia-Pacific at 20.6% is the highest-growth region through 2034. Rising oncology incidence, expanding tertiary hospital infrastructure, and government-led nuclear medicine programs across countries, such as China, India, Japan, and South Korea, are accelerating regional expansion.

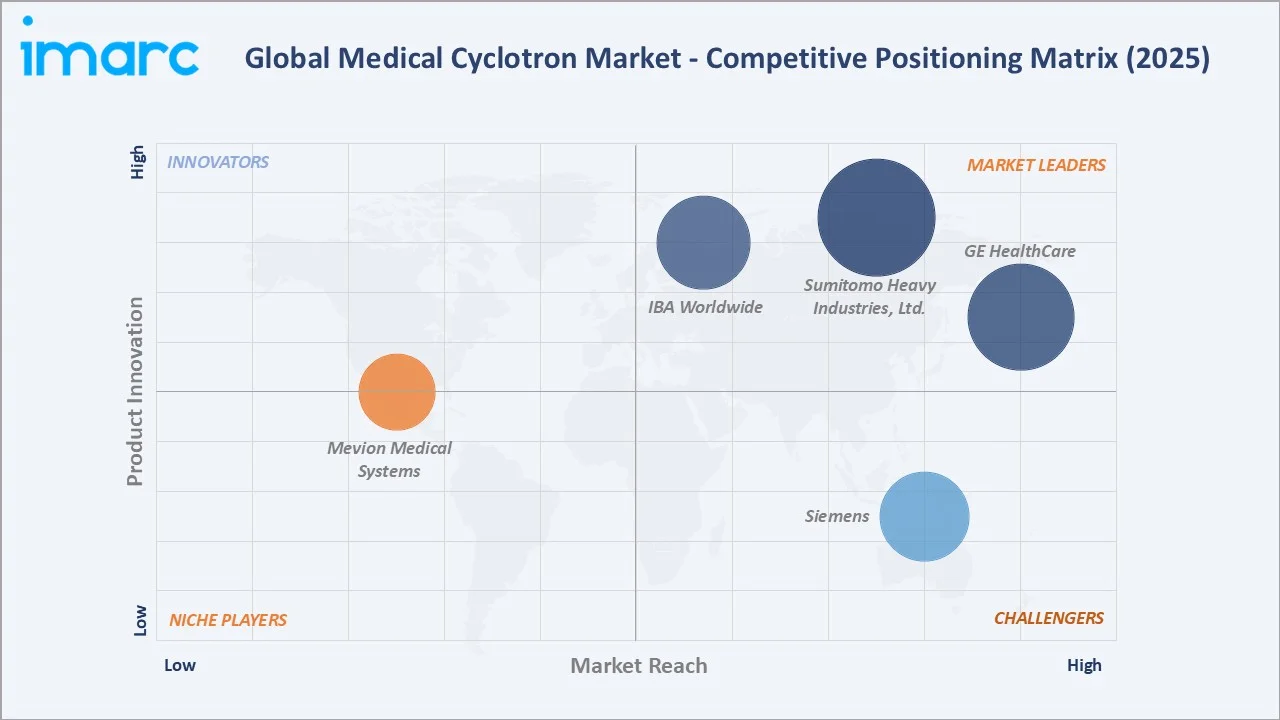

Competitive Landscape

The global medical cyclotron market is moderately consolidated, with global leaders dominating installed-base share and long-term service revenue while regional specialists compete in compact-system and research-focused niches. Service-network depth and chemistry-module integration form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

IBA Worldwide |

Cyclone® KEY, Cyclone® KIUBE, |

Leader |

Broad energy range; large global installed base; integrated chemistry solutions |

|

GE HealthCare |

PETtrace 800 Series |

Leader |

Strong hospital relationships; bundled PET imaging plus cyclotron offering |

|

Sumitomo Heavy Industries, Ltd. |

CYPRIS® MP-30 |

Leader |

Compact Azimuthally Varying Field (AVF) Cyclotron designs; deep Asia-Pacific presence and service network |

|

Siemens |

Eclipse Cyclotron |

Challenger |

Integrated radiopharmacy platforms; focus on workflow automation and decentralized isotope production |

|

Mevion Medical Systems |

MEVION S250i, MEVION S250-FIT |

Emerging |

Compact superconducting accelerators for proton therapy; single-room solutions |

Key players include IBA Worldwide, GE HealthCare, Sumitomo Heavy Industries, Ltd., Siemens, and Mevion Medical Systems, among others.

Key Company Profiles

IBA Worldwide

IBA Worldwide is a Belgium-headquartered specialist in particle accelerators with one of the largest installed bases of medical cyclotrons globally, serving PET radiopharmacy hubs, hospitals, and research centers across several countries.

- Product Portfolio: Cyclone® KEY, Cyclone® KIUBE, Cyclone® IKON, Cyclone® 30XP, and Cyclone® 70 platforms

- Recent Developments: In May 2025, IBA Worldwide signed a contract with PET Pharm Bio to install a Cyclone® IKON cyclotron in Taipei, Taiwan, to support PET and SPECT isotope production. The new PET Pharm Bio radiopharmacy would gain from IBA IntegraLab® design and third-party integration services, guaranteeing complete GMP compliance for this production center

- Strategic Focus: Broad energy-range portfolio spanning low-energy PET production to high-energy research applications, integrated chemistry solutions, and recurring service revenue from a deep global installed base.

GE HealthCare

GE HealthCare is a leading global medical technology provider serving the medical cyclotron market through its PETtrace 800 Series platform. The system emphasizes high-yield isotope production, operational reliability, and scalable configurations suited for both hospital and commercial radiopharmacy settings.

- Product Portfolio: PETtrace 800 Series cyclotrons, integrated PET-CT scanner ecosystem.

- Recent Developments: In June 2025, GE HealthCare unveiled an updated version of its MIM Encore imaging software. The new version incorporates GE HealthCare's unique algorithms and functionalities aimed at enhancing image quality, automating reports, and optimizing workflows in oncology, cardiology, and neurology.

- Strategic Focus: Bundled hospital relationships combining PET imaging, cyclotron, and chemistry modules, with a strong global service footprint across high-income markets.

Sumitomo Heavy Industries, Ltd.

Sumitomo Heavy Industries, Ltd. is a Japan-based industrial conglomerate whose Industrial Equipment Division supplies the medical cyclotron market through its CYPRIS® MP-30 multi-particle platform, with a strong installed base across Asia-Pacific.

- Product Portfolio: CYPRIS® MP-30 multi-particle 30 MeV cyclotron capable of producing both PET and theranostic radioisotopes, supported by automated FDG and PET tracer synthesis solutions.

- Recent Developments: Sumitomo Heavy Industries, Ltd. continues to expand its service network across Asia-Pacific, supporting the rollout of new hospital-based radiopharmacies in Japan, China, and South Korea. Ongoing investments in after-sales support and maintenance capabilities are enhancing system uptime and long-term customer retention.

- Strategic Focus: Compact Azimuthally Varying Field (AVF) Cyclotron designs optimized for hospital deployment, combined with deep service capabilities and established relationships across Asian healthcare systems.

Market Concentration Analysis

The global medical cyclotron market is moderately concentrated, with the top five companies (IBA Worldwide, GE HealthCare, Sumitomo Heavy Industries, Ltd., Siemens, and Mevion Medical Systems) estimated to hold approximately 60-70% of global installed-base share in 2025.

Barriers to entry include high R&D investment in magnet and RF technology, multi-year regulatory qualification cycles for new platforms, and the deep service-network capabilities needed to support 24x7 hospital operations, favoring well-capitalized incumbents with established global footprints.

Consolidation is accelerating through chemistry-module bundling, long-term service contracts, and partnerships with radiopharmaceutical sponsors. Scale advantages in manufacturing, qualification, and after-sales service are further reinforcing the competitive position of established leaders.

Investment & Growth Opportunities

Fastest-Growing Segments

Cyclotron 24 MeV and Above and the cyclotron 19-24 MeV range expand faster than the overall 6.93% market CAGR through 2034, driven by theranostic isotope demand and broader research applications. Asia-Pacific is the fastest-growing regional segment as healthcare investment scales across the region.

Emerging Markets

Asia-Pacific at 20.6% is the highest-growth region, with China, India, Japan, and South Korea leading new installations. Brazil, Saudi Arabia, and South Africa represent the largest untapped opportunities as expanding cancer care infrastructure, rising healthcare spending, and government-led nuclear medicine programs unlock new capacity.

Venture & Investment Trends

Venture capital is concentrated in compact superconducting accelerator design, theranostic isotope production startups, automated radiochemistry platforms, and AI-driven cyclotron operations. Investment is also expanding into hospital-based radiopharmacy networks and cross-border isotope supply infrastructure.

Future Market Outlook (2026-2034)

The global medical cyclotron market is forecast to expand from USD 265.4 Million in 2025 to USD 493.8 Million by 2034 at a CAGR of 6.93%, adding roughly USD 228.4 Million in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: theranostic isotope demand; compact self-shielded system adoption; hospital-based radiopharmacy network expansion; and digitalization of cyclotron operations through AI-assisted workflows.

By 2034, mid-energy cyclotrons capable of producing both diagnostic and theranostic isotopes are expected to become the default hospital configuration in leading markets, while cyclotron 10-12 MeV systems will fill gaps in regional PET coverage across emerging economies.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at leading cyclotron manufacturers, hospital nuclear medicine directors, radiopharmacy operations heads, regulatory consultants, and academic researchers, validating market sizing, regional demand, type splits, and product type evolution.

Secondary Research

Secondary sources included the IAEA Directory of Cyclotrons, Society of Nuclear Medicine and Molecular Imaging publications, World Nuclear Association reports, peer-reviewed nuclear medicine journals, government health statistics, and annual reports, press releases, and investor presentations from listed and private manufacturers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining PET-CT procedure volumes, average cyclotron capital cost per unit, theranostic isotope demand, and hospital procurement pipelines. Scenario analysis addressed reimbursement, regulatory, and component-supply variability.

Medical Cyclotron Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Ring Cyclotron, Azimuthally Varying Field (AVF) Cyclotron |

| Product Types Covered | Cyclotron 10-12 MeV, Cyclotron 16-18 MeV, Cyclotron 19-24 MeV, Cyclotron 24 MeV and Above |

| End Users Covered | Hospitals, Diagnostic Centers, Research and Academic Institutes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | IBA Worldwide, GE HealthCare, Sumitomo Heavy Industries, Ltd., Siemens, Mevion Medical Systems, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical cyclotron market from 2020-2034.

- The medical cyclotron market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical cyclotron industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Medical Cyclotron Market Report

The global market was valued at USD 265.4 Million in 2025, supported by rising PET imaging volumes, growing oncology burden, and expanding hospital-based radiopharmacy capacity.

The market is projected to grow at 6.93% CAGR from 2026 to 2034, reaching USD 493.8 Million, supported by theranostics demand and broader nuclear medicine adoption globally.

Ring cyclotron leads at 54.5% in 2025, supported by high beam-current capability and multi-isotope flexibility. Azimuthally Varying Field (AVF) cyclotron at 45.5% serves hospital-based PET centers.

Cyclotron 16-18 MeV dominates at 56.0% in 2025, driven by high demand for routine PET isotopes, such as Fluorine-18, across established diagnostic imaging workflows.

North America commands 39.4% in 2025, led by the United States, supported by advanced healthcare infrastructure, high PET imaging volumes, and strong investment in cyclotron networks. Asia-Pacific at 20.6% is the fastest-growing region through 2034.

Leading players include IBA Worldwide, GE HealthCare, Sumitomo Heavy Industries, Ltd., Siemens, and Mevion Medical Systems, among others.

Hospital radiopharmacies enable on-site production of short-lived PET isotopes, reducing reliance on long-distance distribution and ensuring reliable supply for daily imaging schedules.

Key restraints include high capital cost, stringent regulatory and licensing requirements, shortage of skilled radiopharmaceutical workforce, and complex radiation shielding constraints.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)