Medical Robotic Systems Market Report by Product (Surgical Robots, Rehabilitation Robots, Noninvasive Radiosurgery Robots, Hospital and Pharmacy Robots, Emergency Response Robotic Systems), Deployment Mode (On-premises, Cloud-based), End User (Hospitals, Ambulatory Surgical Centers, Rehabilitation Centers, and Others), and Region 2026-2034

Global Medical Robotic Systems Market

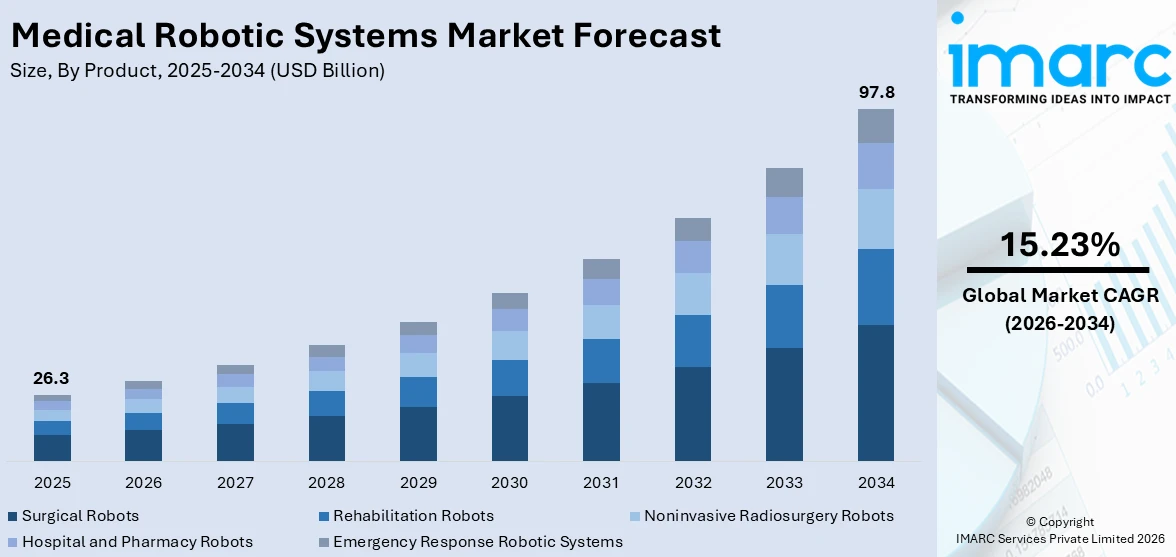

The global medical robotic systems market size reached USD 26.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 97.8 Billion by 2034, exhibiting a growth rate (CAGR) of 15.23% during 2026-2034. Technological innovations, the rising demand for minimally invasive surgeries, the surging prevalence of chronic diseases, and investment in healthcare are primarily driving the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 26.3 Billion |

| Market Forecast in 2034 | USD 97.8 Billion |

| Market Growth Rate 2026-2034 | 15.23% |

Medical Robotic Systems Market Analysis:

- Major Market Drivers: The increasing demand for minimally invasive surgeries (MIS), owing to the escalating preference for smaller incisions, fewer cuts, decreased scarring, reduced pain, improved safety, and faster recovery periods that are associated with MIS across the surgical domain, is propelling the market growth.

- Key Market Trends: The rising geriatric population and the continual technological advancements in novel surgical modalities are bolstering the market growth across the globe. Moreover, the augmenting need for automation in the healthcare industry, a considerable rise in the cases of trauma injuries, and the rapidly expanding medical tourism sector are also acting as significant growth-inducing factors.

- Competitive Landscape: Some of the prominent companies in the market include Accuray Incorporated, Globus Medical, Intuitive Surgical Operations, Inc, Johnson & Johnson, Medtronic plc, Omnicell, Siemens Healthineers AG, Smith+Nephew, Stereotaxis, Inc., Stryker Corporation, Titan Medical Inc., and Zimmer Biomet, among many others.

- Geographical Trends: North America exhibits a clear dominance in the market, on account of the novel advancements in robotic technologies such as surgical robots, rehabilitation robots, and robotic-assisted therapy systems. These advancements enhance precision, accuracy, and effectiveness in medical procedures, thereby driving adoption.

- Challenges and Opportunities: High initial costs and safety concerns associated with robotic systems are hampering the market growth. However, the rising usage of artificial intelligence (AI), machine learning, and haptics to enhance the capabilities and precision of medical robotic systems is expected to fuel the market over the forecasted period.

To get more information on this market Request Sample

Medical Robotic Systems Market Trends:

Increasing Demand for Minimally Invasive Surgeries

The increasing adoption of robotic systems for minimally invasive surgeries drives the market growth. Patients prefer minimally invasive surgery due to the lower risk of complications and reduced hospitalization periods. For instance, according to a cross-sectional study of 305 VV-afflicted patients at Zhejiang Rongjun Hospital between January 2022 and June 2023 evaluated the treatment preferences of the patients. Out of the 96 patients who selected an option of treatment, nearly 24.0% went with traditional surgery, and 76.0% went with MIT. Moreover, manufacturers are expanding their product offerings and upgrading existing systems to meet the demand for advanced surgical capabilities and technological innovations. For instance, in April 2024, Manipal Hospital, Kharadi, launched advanced robotic knee replacement surgery, which promised more precision, faster recovery times, and less discomfort than traditional surgeries. This provides advantages, such as sub-millimeter accuracy during implant surgery, a lower risk of infection, and the prospect of speedier recovery and release within 24 hours. This breakthrough technique allows patients to have minimally invasive surgery with reduced recovery periods, higher precision, and a better quality of life. These factors are further driving the medical robotic systems market growth.

Adoption of Surgical Robots

Surgical robots offer superior precision, skill, and accuracy compared to traditional surgical techniques. They enable surgeons to perform complex procedures. For instance, according to an article published by Mayo Clinic, during surgery, robotic technology can help surgeons be more precise, flexible, and in control. When compared to conventional surgical techniques, robotic technology also improves the visibility of the operating site. Surgeons can carry out intricate and delicate treatments with robotic surgery that would be challenging or impossible to accomplish with other techniques. Besides this, favorable regulatory approvals and reimbursement policies for robotic-assisted surgeries support market growth. Healthcare regulatory bodies recognize the clinical benefits of robotic systems and encourage their adoption through streamlined approval processes. For example, in March 2024, Intuitive received U.S. Food and Drug Administration (FDA) 510(k) certification for their fifth-generation multiport robotic system, called da Vinci 5. With more than 150 improvements, it boasts the first force-sensing technology, a next-generation 3D display and image processing, and increased precision. With customizable posture and the option to make changes while using the console, the da Vinci 5 system's revamped console provides surgeons with increased comfort. These factors are further escalating the growth of the global medical robotic systems market.

Technological Advancements

Modern medical robotic systems leverage advanced imaging technologies, such as high-definition cameras, 3D visualization, and real-time image processing. These technologies provide surgeons with detailed, magnified views of the surgical site, enabling precise manipulation of tissues and organs. For instance, in June 2024, Endiatx, a medical technology company, unveiled its robotic pill to the market. The PillBot is an ingestible robotic capsule that has cameras, sensors, and wireless communication capabilities, allowing clinicians to investigate the gastrointestinal tract with unprecedented accuracy and control. Enhanced accuracy reduces the risk of human error and improves surgical outcomes, particularly in complex procedures. Besides this, AI and machine learning algorithms are increasingly integrated into medical robotic systems to enhance decision-making capabilities and automate complex tasks. AI-powered systems can analyze vast amounts of data in real-time, predict surgical outcomes, and assist surgeons in planning and executing procedures more effectively. For example, in October 2023, Body Vision Medical launched a new software update for its LungVision™ navigation and real-time imaging platform. The update includes the latest AI Tomography imaging algorithm, a streamlined workflow for robotic-assisted bronchoscopy (RAB), reduced radiation exposure for medical staff and patients during lung nodule biopsy procedures, etc. These factors are further driving the medical robotic systems market size.

Global Medical Robotic Systems Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global medical robotic systems market report, along with forecasts at the global, regional, and country level from 2026-2034. Our report has categorized the market based on product, deployment mode, and end user.

Breakup by Product:

- Surgical Robots

- Orthopedic Surgical Robots

- Neurosurgical Robotic Systems

- Laparoscopy Robotic Systems

- Steerable Robotic Catheters

- Rehabilitation Robots

- Assistive Robots

- Prosthetics

- Orthotics

- Therapeutic Robots

- Exoskeleton Robotic Systems

- Noninvasive Radiosurgery Robots

- TrueBeam STx Radiosurgery System

- CyberKnife Robotic Radiosurgery System

- Gamma Knife Perfexion Radiosurgery System

- Hospital and Pharmacy Robots

- Telemedicine Robots

- I.V. Robots

- Cart Transportation Robots

- Emergency Response Robotic Systems

Surgical robots represented the largest segment

The report has provided a detailed breakup and analysis of the market based on the product. This includes surgical robots (orthopedic surgical robots, neurosurgical robotic systems, laparoscopy robotic systems, and steerable robotic catheters), rehabilitation robots (assistive robots, prosthetics, orthotics, therapeutic robots, and exoskeleton robotic systems), noninvasive radiosurgery robots (TrueBeam STx radiosurgery system, cyberknife robotic radiosurgery system and gamma knife perfexion radiosurgery system), hospital and pharmacy robots (telemedicine robots, I.V. robots, and cart transportation robots), and emergency response robotic systems. According to the report, surgical robots represented the largest market segmentation.

According to the medical robotic systems market overview, surgical robots enable minimally invasive procedures with smaller incisions, reduced trauma to surrounding tissues, and faster recovery times compared to traditional open surgeries. Patients benefit from less pain, shorter hospital stays, and quicker return to normal activities, driving demand for robotic-assisted surgeries. They offer enhanced precision and accuracy in surgical maneuvers, leveraging advanced imaging, robotic arm talent, and real-time feedback mechanisms. Surgeons can perform complex procedures with greater control and precision, minimizing risks and improving surgical outcomes. For instance, in June 2024, SS Innovations, the developer of India’s first indigenous surgical robotic system, launched SSI Mantra 3, a robotic system that enables affordable access to the next generation of surgical innovation.

Breakup by Deployment Mode:

- On-premises

- Cloud-based

The report has provided a detailed breakup and analysis of the market based on the deployment mode. This includes on-premises and cloud-based.

On-premises medical robotic systems are hosted and managed within the healthcare facility’s infrastructure, typically within a dedicated surgical suite or operating room. Moreover, healthcare providers have full control over the system’s hardware, software, and data management, which is positively influencing the medical robotic systems market prediction. This allows for stringent security measures and compliance with healthcare data privacy regulations. At the same time, cloud-based medical robotic systems leverage cloud computing infrastructure to store data and perform computational tasks remotely. This enables access to robotic capabilities from multiple locations, including different healthcare facilities and remote surgical centers.

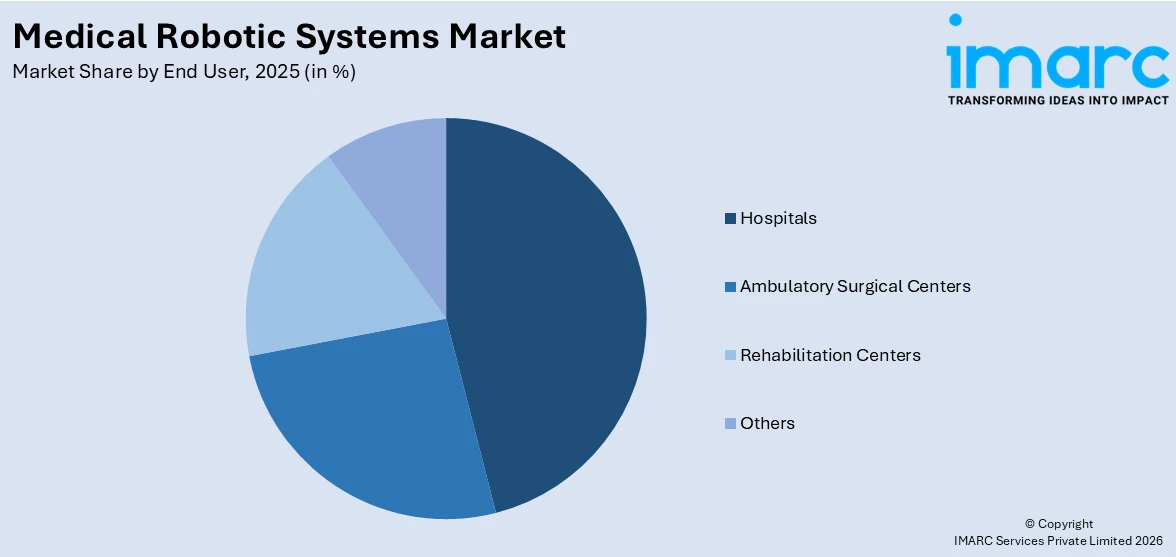

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Ambulatory Surgical Centers

- Rehabilitation Centers

- Others

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals, ambulatory surgical centers, rehabilitation centers, and others.

Hospitals are major users of medical robotic systems, particularly for complex surgeries that require precision and advanced capabilities. Robotic systems enable surgeons to perform intricate procedures with enhanced precision, reducing the risk of complications and improving patient outcomes. While ASCs increasingly adopt medical robotic systems for performing minimally invasive surgeries (MIS), such as laparoscopic procedures, hernia repairs, and outpatient orthopedic surgeries. Robotic-assisted techniques allow ASCs to offer advanced surgical options with quicker recovery times and reduced post-operative pain. Besides this, in rehabilitation centers, medical robotics are used for neurorehabilitation therapies and assistive technologies. Robotic exoskeletons, prosthetics, and rehabilitation robots help patients regain mobility, improve muscle strength, and facilitate recovery from neurological conditions and musculoskeletal injuries.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America accounts for the largest market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

According to the medical robotic systems market statistics, continuous innovation in robotic technology, including AI integration, advanced imaging capabilities, and enhanced surgical navigation systems, has expanded the applications and precision of medical robotic systems in the region. These advancements improve surgical outcomes and patient safety, driving adoption across various specialties. Moreover, there is an increasing preference for minimally invasive procedures due to reduced recovery times, shorter hospital stays, and improved patient outcomes. Medical robotic systems enable surgeons to perform complex surgeries through smaller incisions with greater precision, enhancing the appeal of robotic-assisted procedures. For instance, in September 2023, U.S. Medical Innovations (USMI) and the Jerome Canady Research Institute for Advanced and Biological Technological Sciences (JCRI-ABTS) launched the new Canady Robotic AI Surgical System.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major market companies have also been provided. Some of the key players in the market include:

- Accuray Incorporated

- Globus Medical

- Intuitive Surgical Operations, Inc

- Johnson & Johnson

- Medtronic plc

- Omnicell

- Siemens Healthineers AG

- Smith+Nephew

- Stereotaxis, Inc.

- Stryker Corporation

- Titan Medical Inc.

- Zimmer Biomet

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Medical Robotic Systems Market Recent Developments:

- June 2024: SS Innovations, the developer of India’s first indigenous surgical robots, launched SSI Mantra 3, a robotic system.

- June 2024: Endiatx, a medical technology company, unveiled its robotic pill, an ingestible capsule with cameras, sensors, and wireless communication capabilities. This capsule allows clinicians to investigate the gastrointestinal tract with unprecedented accuracy and control.

- April 2024: Manipal Hospital, Kharadi, introduced advanced robotic knee replacement surgery, which offers more precision, faster recovery times, and less discomfort than traditional surgeries.

Medical Robotic Systems Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Deployment Modes Covered | On-premises, Cloud-based |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Rehabilitation Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Accuray Incorporated, Globus Medical, Intuitive Surgical Operations, Inc, Johnson & Johnson, Medtronic plc, Omnicell, Siemens Healthineers AG, Smith+Nephew, Stereotaxis, Inc., Stryker Corporation, Titan Medical Inc., Zimmer Biomet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical robotic systems market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global medical robotic systems market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical robotic systems industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global medical robotic systems market was valued at USD 26.3 Billion in 2025.

We expect the global medical robotic systems market to exhibit a CAGR of 15.23% during 2026-2034.

The rising need for automation in the healthcare industry, along with the growing adoption of robotic systems, such as computer-controlled electromechanical devices, that utilize the actions of the surgeon on one side to control the effector on the other side, is primarily driving the global medical robotic systems market.

The sudden outbreak of the COVID-19 pandemic had led to postponement of elective various surgical interventions to reduce the risk of the coronavirus infection upon hospital visits and interaction with medical equipment, thereby negatively impacting the global market for medical robotic systems.

Based on the product, the global medical robotic systems market can be bifurcated into surgical robots, rehabilitation robots, non-invasive radiosurgery robots, hospital and pharmacy robots, and emergency response robotic systems. Currently, surgical robots hold the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global medical robotic systems market include Accuray Incorporated, Globus Medical, Intuitive Surgical Operations, Inc, Johnson & Johnson, Medtronic plc, Omnicell, Siemens Healthineers AG, Smith+Nephew, Stereotaxis, Inc., Stryker Corporation, Titan Medical Inc., and Zimmer Biomet.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)