Medical Specialty Bags Market Size, Share, Trends and Forecast by Product, End User, and Region, 2026-2034

Medical Specialty Bags Market Size, Share, Trends & Forecast (2026-2034)

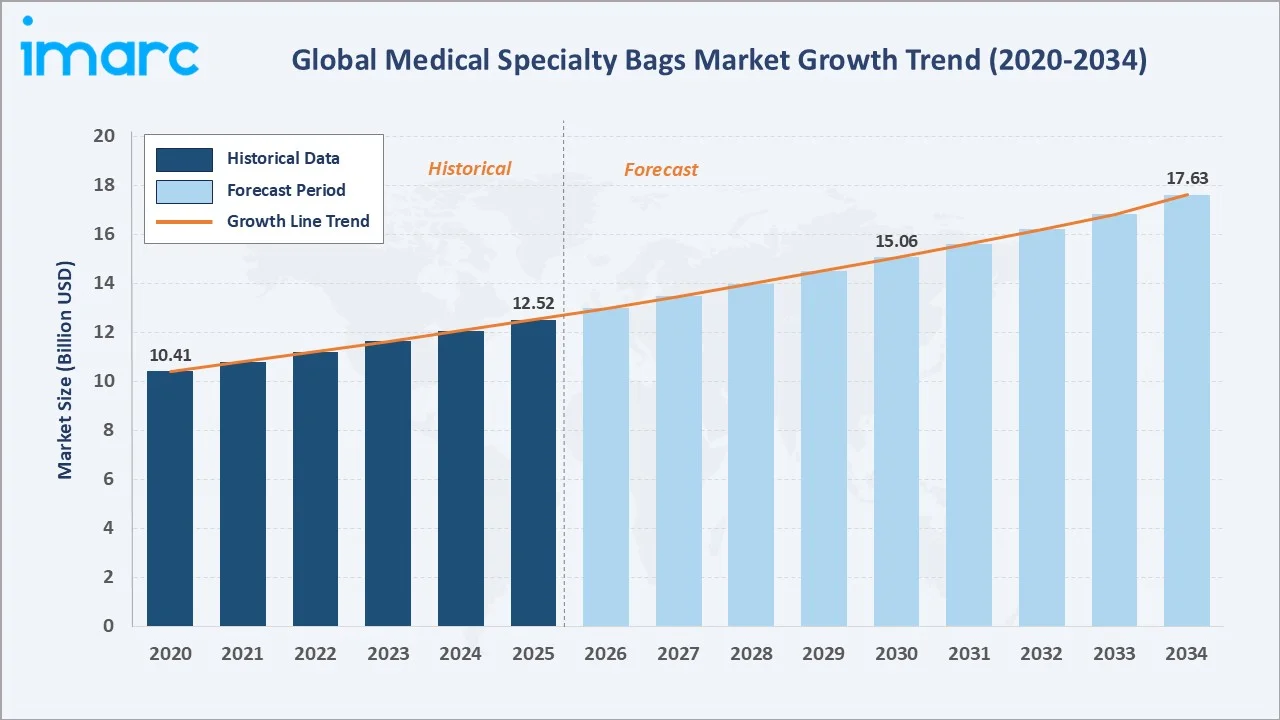

The medical specialty bags market was valued at USD 12.52 Billion in 2025 and is projected to reach USD 17.63 Billion by 2034, exhibiting a CAGR of 3.76% during 2026-2034. Rising prevalence of chronic conditions, increasing surgical procedure volumes, and surging adoption of home-based care are the primary drivers shaping the market growth. The International Diabetes Federation (IDF) Diabetes Atlas (2025) indicated that 11.1%, or 1 in 9 of adults aged 20-79, were diagnosed with diabetes, and more than 40% were unaware of their condition.

Ostomy collection bags lead the product segment at 27.5%, hospitals dominate the end user segment at 55.0%, and North America commands 32.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.52 Billion |

|

Forecast Market Size (2034) |

USD 17.63 Billion |

|

CAGR (2026-2034) |

3.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (32.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (25.1%, 2025) |

|

Leading Product |

Ostomy Collection Bags (27.5%, 2025) |

|

Leading End User |

Hospitals (55.0%, 2025) |

The medical specialty bags market expanded from USD 10.41 Billion in 2020 to USD 12.52 Billion in 2025, driven by rising chronic disease burden, expanding global surgical volumes, and accelerating adoption of home healthcare services. Anchored at USD 15.06 Billion in 2030, the forecast to USD 17.63 Billion by 2034 is supported by sustained hospital infrastructure investment and increasing penetration of specialty bag applications across emerging economies.

To get more information on this market, Request Sample

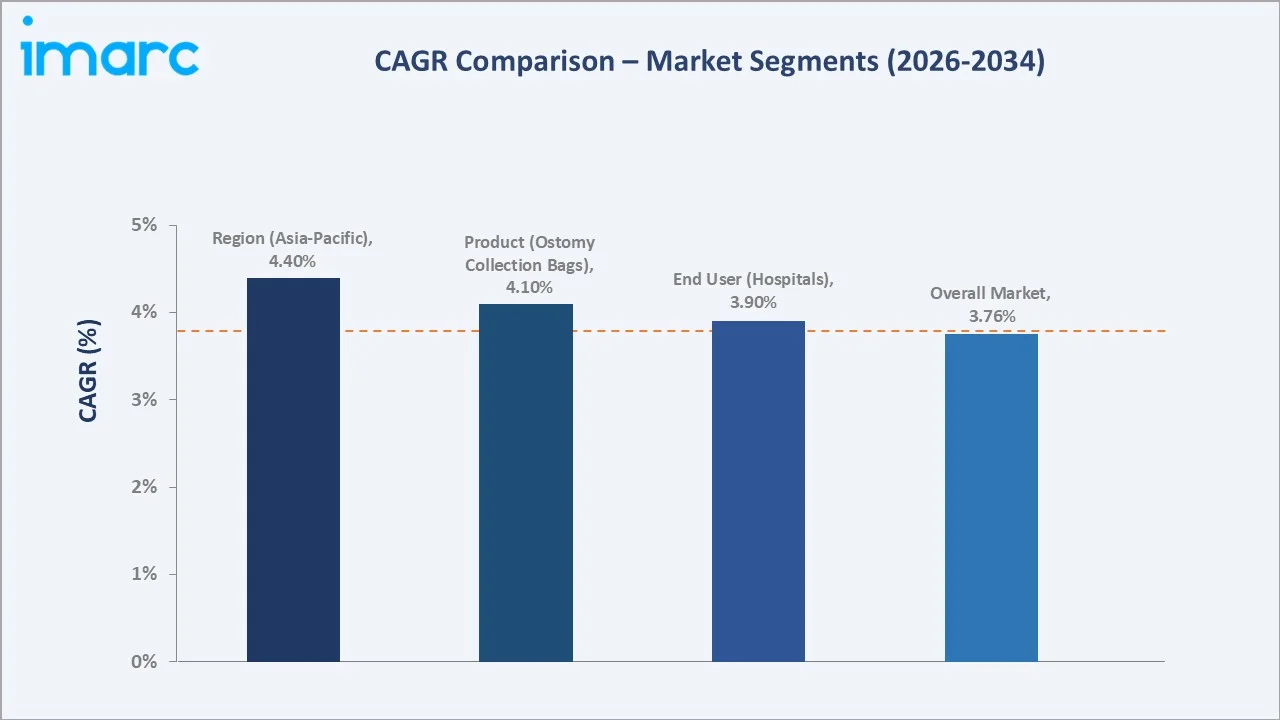

CAGR trajectories across product type and end user sub-segments show the ostomy collection bags and home healthcare segments expanding faster than the overall 3.76% market CAGR, driven by aging demographics, rising incidence of colorectal disorders, and growing patient preference for convenient home-based therapy solutions.

Executive Summary

The medical specialty bags market is on a steady growth trajectory from USD 10.41 Billion in 2020 to USD 17.63 Billion by 2034. Specialty bags have transitioned from niche consumables to critical components of modern clinical care across hospitals, surgical centers, and home health settings. Growing prevalence of chronic kidney disease, ostomy procedures, and intravenous therapy is underpinning persistent demand. Technological advancements in polymeric materials and sterilization methods are further enhancing product quality and safety.

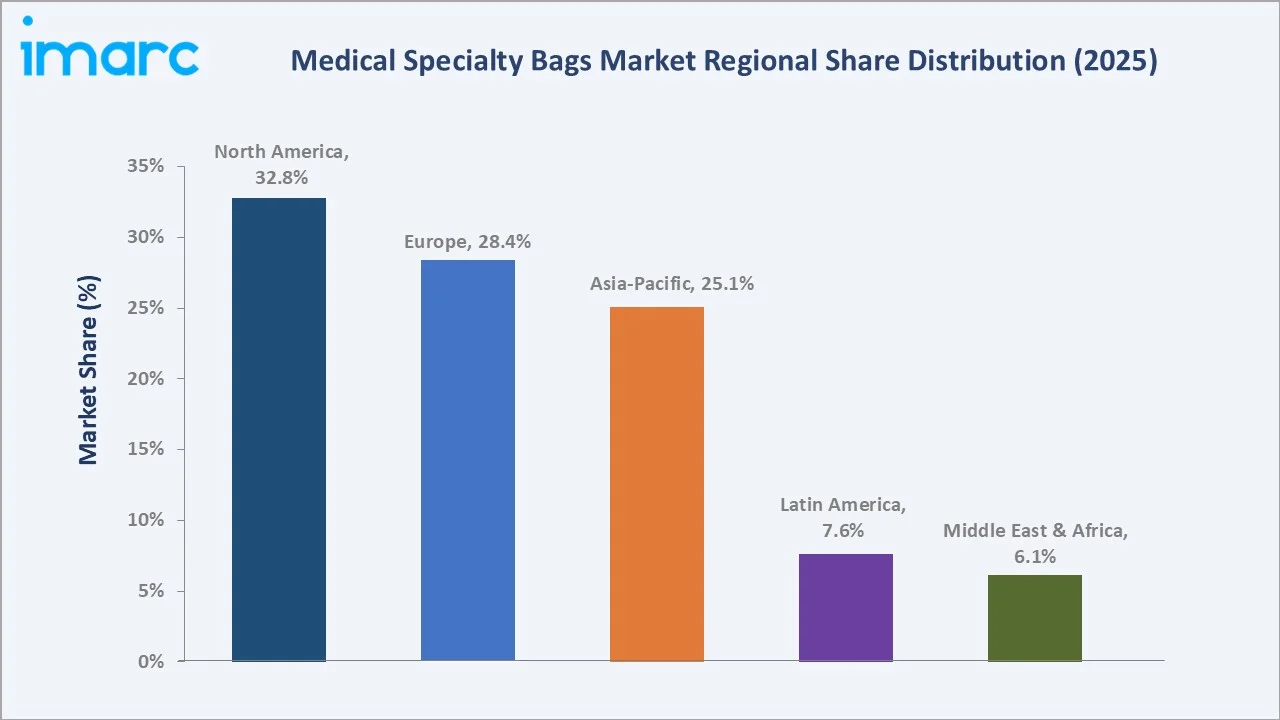

Ostomy collection bags dominate the product segment with a 27.5% share in 2025, supported by increasing colorectal cancer incidence and rising ostomy procedure volumes worldwide. The United Nations projects that by 2030, one in every six individuals globally will be 60 years old or over, intensifying the burden of age-related chronic conditions and reinforcing long-term procurement of medical specialty bags. Hospitals lead end user adoption at 55.0%, anchored by high patient volumes and centralized procurement. North America commands 32.8% regional share, led by the United States, driven by advanced healthcare infrastructure and comprehensive reimbursement frameworks.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Ostomy Collection Bags - 27.5% share (2025) |

|

Second Largest Product |

Intravenous Fluid Bags - 18.6% share (2025) |

|

Leading End User |

Hospitals - 55.0% share (2025) |

|

Second Largest End User |

Ambulatory Surgical Centers - 21.4% share (2025) |

|

Leading Region |

North America - 32.8% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 25.1% share (2025) |

|

Top Companies |

Baxter, B. Braun SE, Terumo Corporation |

Key Analytical Observations Supporting the Above Data:

- Ostomy collection bags dominate at 27.5%, supported by the consistent global volume of ostomy procedures and the long-term recurring need for reliable stoma management consumables across hospital, home care, and post-acute care settings.

- Intravenous fluid bags at 18.6% represent a foundational clinical consumable, driven by universal adoption in hospital settings for fluid management, medication delivery, and parenteral nutrition across all therapeutic areas.

- Hospitals lead end user adoption at 55.0%, owing to high inpatient volumes, centralized bulk procurement systems, and the broad clinical applicability of specialty bags across departments ranging from surgery to oncology and intensive care.

- Ambulatory surgical centers at 21.4% benefit from rising volumes of same-day surgical procedures, increasing preference for minimally invasive interventions, and growing reliance on cost-efficient outpatient care settings that require consistent use of sterile and disposable specialty bags across perioperative workflows. As per IMARC Group, the global minimally invasive surgery market size reached USD 59.3 Billion in 2025.

- North America at 32.8% leads regional share, underpinned by a mature healthcare infrastructure, strong reimbursement ecosystem, and high procedural volumes in the United States, complemented by robust post-acute and home care transitions.

Medical Specialty Bags Market Overview

Medical specialty bags are purpose-engineered flexible containers used across a wide range of clinical applications including ostomy care, intravenous fluid delivery, blood collection and storage, enteral feeding, peritoneal dialysis, anesthesia, and cadaver management. These products are manufactured from materials, such as polyvinyl chloride (PVC), polyethylene, polypropylene, and multi-layer laminate films, each selected for compatibility with specific medical substances, sterilization requirements, and handling characteristics.

The global ecosystem encompasses raw polymer suppliers, specialty film extruders, bag assemblers, sterilization service providers, regulatory compliance bodies, healthcare distributors, and hospital procurement systems. Increasing clinical specialization, expanding procedural volumes in both elective and emergency care settings, and the ongoing shift toward home-based therapy are collectively broadening the addressable market for specialty bags.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

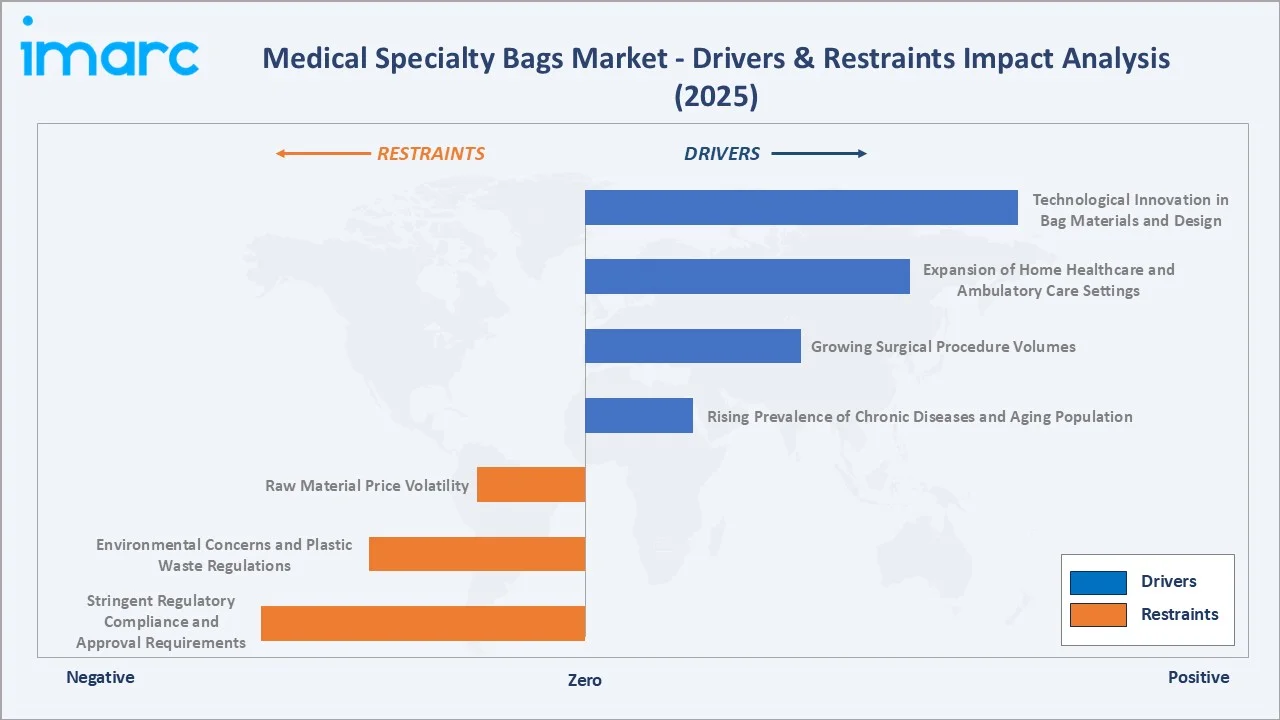

- Rising Prevalence of Chronic Diseases and Aging Population: The burden of chronic conditions, including colorectal cancer, chronic kidney disease, diabetes, and digestive disorders, is expanding significantly. As per Colorectal Cancer Statistics, 2026, the United States will see close to 159,000 new colorectal cancer cases, translating to 440 diagnoses daily.

- Growing Surgical Procedure Volumes: Increasing access to surgical care in emerging economies, combined with rising elective procedure rates in developed markets, is expanding the clinical demand for sterile packaging bags, anesthesia breathing bags, and blood bags. Procedural growth across oncology, orthopedics, and gastrointestinal surgery is contributing to consistent volume-based procurement across hospital systems.

- Expansion of Home Healthcare and Ambulatory Care Settings: The global shift toward decentralized care delivery is accelerating adoption of specialty bags in home and outpatient settings. Patients managing chronic conditions such as renal failure and ostomy at home require reliable, user-friendly bag products, driving volume growth in continuous ambulatory peritoneal dialysis (CAPD) bags, ostomy bags, and enteral feeding bags outside traditional hospital environments.

- Technological Innovation in Bag Materials and Design: Continuous improvement in multilayer polymer films, anti-kink tubing, leak-proof sealing technologies, and ergonomic closure systems is enhancing product performance and patient comfort. These innovations are supporting premium product adoption and enabling manufacturers to differentiate on quality in an otherwise commoditized product category.

Market Restraints

- Stringent Regulatory Compliance and Approval Requirements: Medical specialty bags are subject to rigorous safety, sterility, and biocompatibility standards enforced by agencies, including the FDA and the European Medicines Agency (EMA). Compliance with evolving ISO standards, device classification requirements, and market-specific certification processes adds significant time and cost to product development and market entry for manufacturers.

- Environmental Concerns and Plastic Waste Regulations: Growing regulatory and public pressure to reduce single-use plastic consumption in healthcare is challenging manufacturers of PVC-based specialty bags. Restrictions on plasticizers, such as DEHP, bans on certain polymers, and mandatory recyclability requirements in the European Union, are compelling material reformulation and increasing production costs across the value chain.

- Raw Material Price Volatility: Fluctuations in petrochemical feedstock prices directly impact the cost of PVC, polyethylene, and polypropylene used in bag manufacturing. Supply chain disruptions and geopolitical factors affecting polymer supply chains create cost uncertainty that manufacturers struggle to pass through fully in price-sensitive healthcare procurement environments.

Market Opportunities

- Emerging Market Healthcare Infrastructure Investment: Rapid hospital infrastructure expansion across Asia-Pacific, Latin America, and the Middle East and Africa is creating substantial demand for medical specialty bags in markets previously underserved by quality consumables. Government-led universal health coverage initiatives in countries, such as India, Indonesia, Brazil, and Saudi Arabia, are driving public hospital procurement at scale.

- Eco-Friendly and PVC-Free Specialty Bag Development: Growing regulatory and institutional demand for sustainable medical consumables is creating a clear opportunity for manufacturers developing PVC-free, DEHP-free, and biodegradable specialty bag alternatives. Healthcare systems in northern Europe and North America are increasingly preferring environmentally compliant products in their procurement frameworks, rewarding early movers in sustainable bag innovation.

Market Challenges

- Intense Price Competition and Commoditization: Several categories within the medical specialty bags market, particularly IV fluid bags and sterile packaging bags, face significant pricing pressure from low-cost manufacturers in Asia. Maintaining margin while competing on quality and compliance against commodity producers represents an ongoing challenge for established international brands.

- Supply Chain Complexity and Sterilization Dependencies: Specialty bag manufacturing depends on validated sterilization services, specialized polymer film suppliers, and multi-step assembly processes that introduce supply chain vulnerability. Disruptions to sterilization capacity, as observed during periods of ethylene oxide supply constraints, can delay product availability and create procurement challenges for healthcare providers.

Emerging Market Trends

1. Transition to PVC-Free and DEHP-Free Bag Materials

Regulatory pressure across the European Union and North America is accelerating the industry-wide shift away from traditional PVC-and-DEHP formulations toward safer multilayer polymer alternatives. Healthcare institutions are updating procurement policies to preference DEHP-free products across IV fluid bags, blood bags, and enteral feeding applications. Manufacturers investing in polyolefin-based multilayer films and bioplastic alternatives are positioned to capture premium pricing in eco-conscious markets while ensuring long-term regulatory compliance across increasingly stringent global frameworks.

2. Growth of Home-Based CAPD and Enteral Feeding Applications

CAPD and home enteral nutrition are transitioning from primarily institutional settings to predominantly home-based delivery models. Improved bag connectivity systems, user-friendly disconnection mechanisms, and telehealth integration are supporting patient self-management with greater confidence and clinical safety. Manufacturers are also developing lightweight, portable, and contamination-resistant bag designs to improve convenience and support safe long-term use in home care environments.

3. Integration of Smart Connectivity in IV Fluid and Drug Delivery Bags

Emerging smart IV bag technologies incorporate RFID tracking, barcode verification, and sensor-embedded films capable of detecting fill levels, temperature deviations, and drug integrity in real time. These innovations are entering clinical trials across leading hospital systems in North America and Europe. Integration of smart connectivity addresses critical medication safety concerns, including wrong-drug and wrong-dose errors, supporting adoption by hospital pharmacy and nursing leadership while commanding significant price premiums over conventional IV bags.

4. Expansion of Single-Use Cadaver and Bio-Containment Bag Applications

Increasing adoption of biosafety protocols in hospital mortuaries, disaster response planning, and international patient repatriation is driving growing demand for high-integrity cadaver and bio-containment bags. Standardization of mortuary consumable specifications across public health systems is expanding the addressable market for this niche but fast-growing segment.

Industry Value Chain Analysis

The medical specialty bags value chain spans six stages from raw polymer supply through clinical end use and post-use waste management. Bag assembly and sterilization capture the highest value-add, while distributor and GPO relationships generate downstream competitive advantages in institutional healthcare procurement.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of PVC resin, polyolefin polymers, plasticizers, and barrier film materials, along with upstream chemical producers supporting medical-grade polymer production |

|

Polymer Film & Component Manufacturing |

Specialty film extruders and component producers manufacturing medical-grade polymer films, tubing, connectors, and fitment components for bag assembly |

|

Bag Assembly & Integration |

Contract manufacturers and OEM producers assembling sterile bag systems by combining films, tubes, ports, and fitments into finished specialty bag products |

|

Sterilization & Quality Assurance |

Sterilization service providers using ethylene oxide, gamma irradiation, or e-beam methods to validate sterility, along with quality laboratories performing biocompatibility and endotoxin testing |

|

Distribution & Logistics |

Medical device distributors, healthcare GPOs, specialty logistics providers, and hospital supply chain operators managing temperature-controlled and sterile product distribution |

|

End Use & Post-Use Management |

Hospitals, ambulatory surgical centers, home health agencies, patients and caregivers; medical waste management firms handling post-use disposal and regulated waste processing |

Vertically integrated players that control polymer compounding, bag assembly, and sterilization in-house achieve superior cost control and supply security compared with manufacturers relying on third-party sterilization services and external polymer film suppliers.

Technology Landscape in the Medical Specialty Bags Industry

Advanced Polymer Film and Material Innovation

Multilayer coextruded films combining polyolefin, polyamide, and EVOH barrier layers are replacing traditional mono-layer PVC constructions across multiple specialty bag categories. These advanced materials offer superior oxygen and moisture barrier performance, broader chemical compatibility, and improved biocompatibility, enabling safer product designs for drug admixture, blood storage, and nutrition delivery applications.

Sealing and Closure Technology Advancement

High-frequency welding, ultrasonic sealing, and laser-based fusion technologies are enabling stronger, more consistent seals in specialty bag manufacturing, reducing defect rates and improving hermetic integrity. Automated leak detection systems using pressure differential and laser scanning are being integrated into production lines to achieve near-zero defect output at commercial scale.

Smart Bag and Connectivity Integration

Connected bag technologies embedding RFID tags, temperature indicators, and sensor-integrated films are enabling real-time monitoring of IV drug stability, blood bag storage conditions, and CAPD dwell volumes. These digital enhancements support medication safety programs, cold chain compliance verification, and remote patient monitoring integration in home health settings.

Eco-Compatible Material Development

Research into bioplastic specialty bags using polylactic acid (PLA), polyhydroxyalkanoates (PHA), and bio-sourced polyolefins is progressing toward commercial-scale validation. Early adopters are conducting pilot procurement programs with sustainable bag options in northern European healthcare systems, where regulatory and institutional sustainability mandates are most advanced.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Ostomy Collection Bags |

27.5% |

2025 |

|

End User |

Hospitals |

55.0% |

2025 |

|

Region |

North America |

32.8% |

2025 |

By Product

Ostomy collection bags command a 27.5% majority share in 2025, driven by the global rise in colorectal cancer incidence, inflammatory bowel disease prevalence, and associated surgical stoma creation rates. These bags serve as indispensable, daily-use consumables for ostomy patients, generating consistent and predictable replacement demand across both hospital supply and direct-to-patient retail channels.

To access detailed market analysis, Request Sample

Intravenous fluid bags at 18.6% in 2025 represent a foundational clinical consumable with universal hospital demand, spanning hydration therapy, drug admixture, parenteral nutrition, and chemotherapy delivery. Demand is further supported by the increasing prevalence of chronic diseases, rising surgical volumes, and the continued expansion of emergency and critical care services across healthcare systems.

By End User

Hospitals dominate with a 55.0% share in 2025, reflecting the broad clinical applicability of specialty bags across inpatient departments including surgery, intensive care, oncology, nephrology, and emergency medicine. Centralized bulk procurement, clinical standardization programs, and GPO contracts reinforce hospitals as the primary and most stable demand channel for medical specialty bag products.

Ambulatory surgical centers at 21.4% in 2025 represent the fastest-growing institutional channel, as surgical procedures continue migrating from inpatient to outpatient settings in response to cost pressure and patient preference for shorter stay durations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

32.8% |

Advanced healthcare infrastructure, strong reimbursement frameworks, high surgical procedure volumes, and growing home healthcare adoption driving specialty bag demand |

|

Europe |

28.4% |

Robust hospital network, favorable regulatory environment, growing aging population, and increasing adoption of home-based dialysis and ostomy management solutions |

|

Asia-Pacific |

25.1% |

Expanding hospital infrastructure, rising surgical volumes, government healthcare investment, growing chronic disease prevalence, and increasing product awareness |

|

Latin America |

7.6% |

Improving healthcare access, rising chronic disease burden, growing hospital expenditure, and expanding surgical and ambulatory care capacity |

|

Middle East and Africa |

6.1% |

Healthcare infrastructure development, government investment in medical facilities, rising chronic disease rates, and increasing adoption of modern clinical consumables |

North America at 32.8% in 2025 leads the medical specialty bags market, driven by a dense network of hospitals and ambulatory surgical centers, comprehensive insurance coverage for specialty medical consumables, and strong adoption of home healthcare services.

Europe at 28.4% benefits from established universal healthcare systems across Germany, France, the United Kingdom, and Italy, which maintain consistent centralized procurement of specialty bag products. Aging demographics and growing chronic kidney disease and colorectal disorder prevalence are sustaining long-term demand, while EU regulatory frameworks promoting PVC-free products are driving product innovation investment across the region.

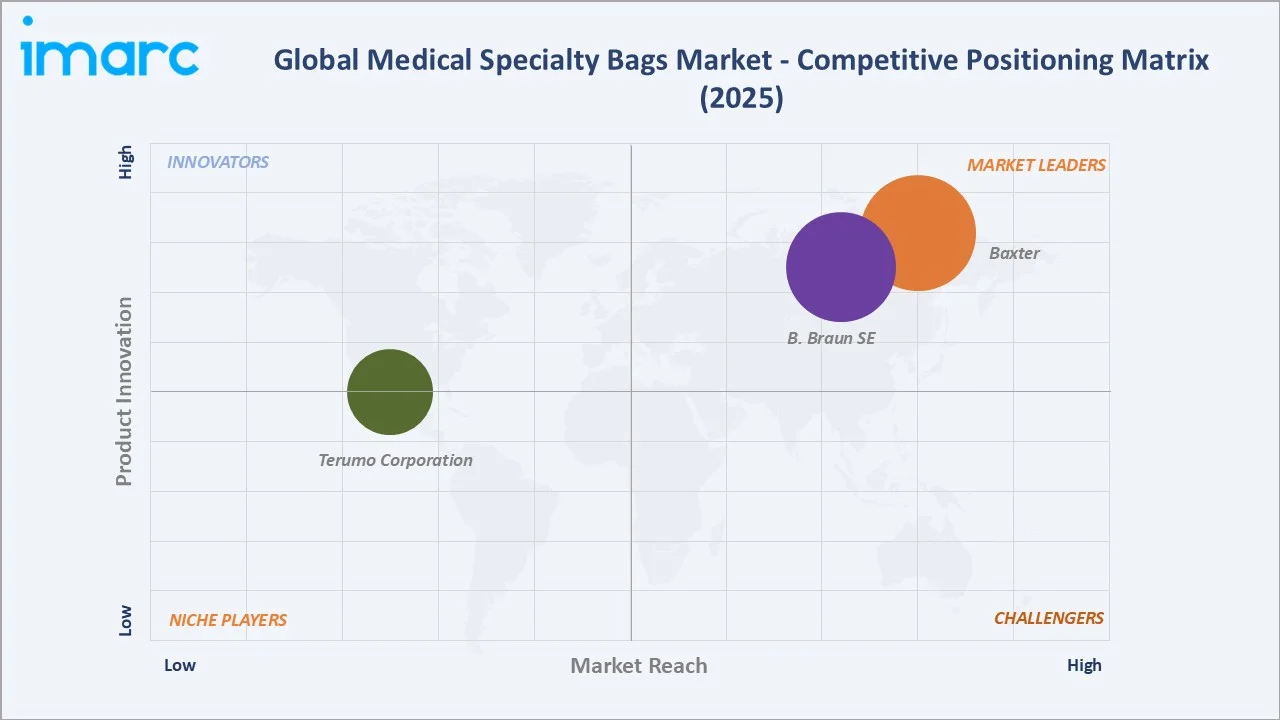

Competitive Landscape

The medical specialty bags market is moderately fragmented, with global leaders dominating institutional procurement relationships and brand recognition while specialized regional players serve niche product categories, including ostomy, blood banking, and home dialysis. Portfolio breadth, clinical data strength, regulatory certifications, and distributor network depth form the primary competitive moats in this market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Baxter |

Viaflex, AVIVA, VIAFLO |

Leader |

Comprehensive IV fluid bag and drug admixture portfolio; deep hospital formulary presence and broad global distribution network across infusion therapy |

|

B. Braun SE |

Ecoflac Plus, EXCEL IV Bag |

Leader |

Integrated IV fluid bag and infusion system solutions; vertically integrated manufacturing and broad European and emerging market reach |

|

Terumo Corporation |

TERUFLEX |

Emerging |

Specialized blood bag and transfusion system portfolio; strong in Asia-Pacific markets with growing global distribution expansion |

Key players include Baxter, B. Braun SE, and Terumo Corporation, among others.

Key Company Profiles

B. Braun SE

B. Braun SE is a German healthcare company offering an integrated portfolio of IV fluid bags, infusion therapy, pain management, and hospital pharmacy products, with vertically integrated manufacturing spanning multiple European and international facilities.

- Product Portfolio: Ecoflac Plus Closed System IV containers, EXCEL IV Bag.

- Recent Developments: B. Braun SE has continued expanding its EXCEL IV Bag portfolio across North American and global hospital markets. The EXCEL IV Bag is manufactured without PVC, DEHP, or natural rubber latex, reflecting the company's commitment to safer and more sustainable IV fluid delivery solutions for hospitals transitioning away from conventional PVC-based containers.

- Strategic Focus: Vertical integration in IV bag manufacturing; PVC-free product leadership through the EXCEL IV Bag and Ecoflac Plus portfolios; expansion of integrated infusion and pharmacy compounding solutions across hospitals and ambulatory care centers globally.

Terumo Corporation

Terumo Corporation is a Japanese medical device company with a leading position in blood management, transfusion medicine, and cardiovascular care, offering a comprehensive range of blood bag systems and apheresis products to blood banks and transfusion services globally.

- Product Portfolio: TERUFLEX Blood Bag Systems

- Recent Developments: Terumo Corporation has advanced its TERUFLEX Blood Bag System portfolio with improved oxygen-reduced storage configurations designed to extend red blood cell storage duration, supporting blood bank inventory optimization programs in hospital and national blood service settings across Asia-Pacific and globally.

- Strategic Focus: Blood management system leadership in Asia-Pacific; advancing leukoreduction-compatible blood bag systems through the TERUFLEX portfolio; expanding global blood bank partnerships through integrated transfusion technology offerings.

Market Concentration Analysis

The medical specialty bags market is moderately concentrated, with the top companies - Baxter, B. Braun SE, and Terumo Corporation - estimated to collectively hold approximately 55-65% of the global market by revenue in 2025.

Barriers to entry are meaningful and include product-specific FDA and CE marking requirements, validated sterilization process qualification, multi-year GPO and hospital supply contract relationships, and the clinical evidence programs needed to displace incumbent products from hospital formularies. These factors favor well-capitalized established players with deep manufacturing expertise and regulatory track records.

Consolidation is progressing through portfolio acquisitions targeting adjacent specialty bag categories, manufacturing capacity expansion in low-cost regions, and strategic partnerships with healthcare GPOs and distributor networks. Scale advantages in polymer compounding, bag assembly automation, and sterilization access are reinforcing the competitive position of integrated leaders relative to single-category specialists.

Investment & Growth Opportunities

Fastest-Growing Segments

Home healthcare at 15.3% is the fastest-growing end user segment, expanding beyond the overall 3.76% market CAGR through 2034, as CAPD, home enteral nutrition, and ostomy management programs accelerate patient transitions from institutional to home care settings. Ambulatory surgical centers at 21.4% are the fastest-growing end user, as outpatient surgical volumes grow across orthopedic, gastrointestinal, and oncological procedures.

Emerging Markets

Asia-Pacific at 25.1% is the highest-growth region, with China, India, Japan, and Southeast Asian nations driving the strongest incremental demand through 2034. Rising surgical infrastructure, universal health coverage expansion, and chronic disease burden growth are unlocking mass-market procurement across all major specialty bag categories. Latin America and the Middle East and Africa represent earlier-stage opportunities where improving hospital density and growing medical consumable standards are progressively expanding the accessible market.

Venture & Investment Trends

Investment activity in the medical specialty bags space is concentrated in sustainable material innovation (PVC-free and biodegradable film technologies), smart bag connectivity platforms integrating IoT sensors with hospital management systems, home dialysis ecosystem expansion, and manufacturing automation enabling quality improvement at reduced per-unit cost. Healthcare infrastructure funding in emerging markets, particularly through public-private partnership frameworks in India, Indonesia, and Gulf Cooperation Council countries, is further expanding the downstream procurement base for specialty bag manufacturers.

Future Market Outlook (2026-2034)

The medical specialty bags market is forecast to expand from USD 12.52 Billion in 2025 to USD 17.63 Billion by 2034 at a CAGR of 3.76%, adding approximately USD 5.11 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: persistent growth in age-related chronic disease requiring specialty bag consumables; accelerating home care adoption across dialysis, ostomy, and enteral nutrition management; material innovation driving PVC-free product transitions across institutional procurement; and expanding healthcare infrastructure in Asia-Pacific and other emerging regions unlocking new patient populations.

By 2034, home healthcare and ambulatory surgical centers will collectively represent a significantly larger share of specialty bag consumption than in 2025, reflecting the structural shift away from inpatient-centric care delivery models. North America will maintain its leading position, while Asia-Pacific will narrow the gap through above-average growth rates sustained by ongoing public health investment and rising middle-class healthcare access.

Research Methodology

Primary Research

Primary research included structured interviews with procurement managers at leading hospital systems, ostomy and continence care nurses, home health agency directors, dialysis center operators, blood bank administrators, and specialty medical device distributors. These engagements validated market sizing, end user adoption trends, product preferences, pricing dynamics, and regional demand patterns.

Secondary Research

Secondary sources included WHO global health statistics, United Nations population projections, FDA and EMA regulatory databases, ISO standards documentation, annual reports and investor presentations from publicly listed companies, as well as healthcare procurement and hospital supply chain publications.

Forecasting Models

Market forecasts were developed using top-down and bottom-up models combining procedure volume projections, average bag consumption rates per procedure and patient type, institutional procurement growth drivers, and regional healthcare infrastructure expansion trajectories. Scenario analysis addressed aging demographic acceleration, home care adoption rates, and raw material cost variation.

Medical Specialty Bags Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Anesthesia Breathing Bags, Blood Bags, Sterile Packaging Bags, Ostomy Collection Bags, Enteral Feeding Bags, Cadaver Bags, Continuous Ambulatory Peritoneal Dialysis (CAPD) Bags, Intravenous Fluid Bags, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Home Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Baxter, B. Braun SE,Terumo Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the medical specialty bags market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global medical specialty bags market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the medical specialty bags industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Medical Specialty Bags Market Report

The medical specialty bags market was valued at USD 12.52 Billion in 2025, driven by rising chronic disease prevalence, growing surgical volumes, and expanding home healthcare adoption worldwide.

The market is projected to grow at a CAGR of 3.76% from 2026 to 2034, reaching USD 17.63 Billion, supported by aging demographics and expanding healthcare infrastructure in emerging markets.

Ostomy collection bags lead with a 27.5% share in 2025, driven by rising colorectal disorder incidence and consistent replacement demand from the global ostomy patient population.

Hospitals dominate with a 55.0% end user share in 2025, anchored by broad clinical applicability of specialty bags across inpatient departments and centralized GPO procurement frameworks.

North America commands a 32.8% share in 2025, led by the United States, driven by advanced hospital infrastructure, comprehensive reimbursement coverage, and high procedural volumes.

Key players include Baxter, B. Braun SE, and Terumo Corporation, among others.

Growth is driven by expanding home CAPD, ostomy care, and enteral nutrition programs, improving product usability, patient preference for home-based therapy, and cost-reduction priorities across healthcare systems.

Key challenges include stringent regulatory compliance requirements, environmental regulations on PVC and plasticizer use, raw material price volatility, and competitive pricing pressure from low-cost manufacturers.

Opportunities include sustainable PVC-free material innovation, smart connected IV bag platforms, home dialysis ecosystem expansion, and emerging market hospital supply chain development across Asia-Pacific and Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)