Meningococcal Vaccines Market Size, Share, Trends and Forecast by Vaccine Type, Composition, Vaccine Serotype, Distribution Channel, End User, and Region, 2026-2034

Global Meningococcal Vaccines Market Size, Share, Trends & Forecast (2026-2034)

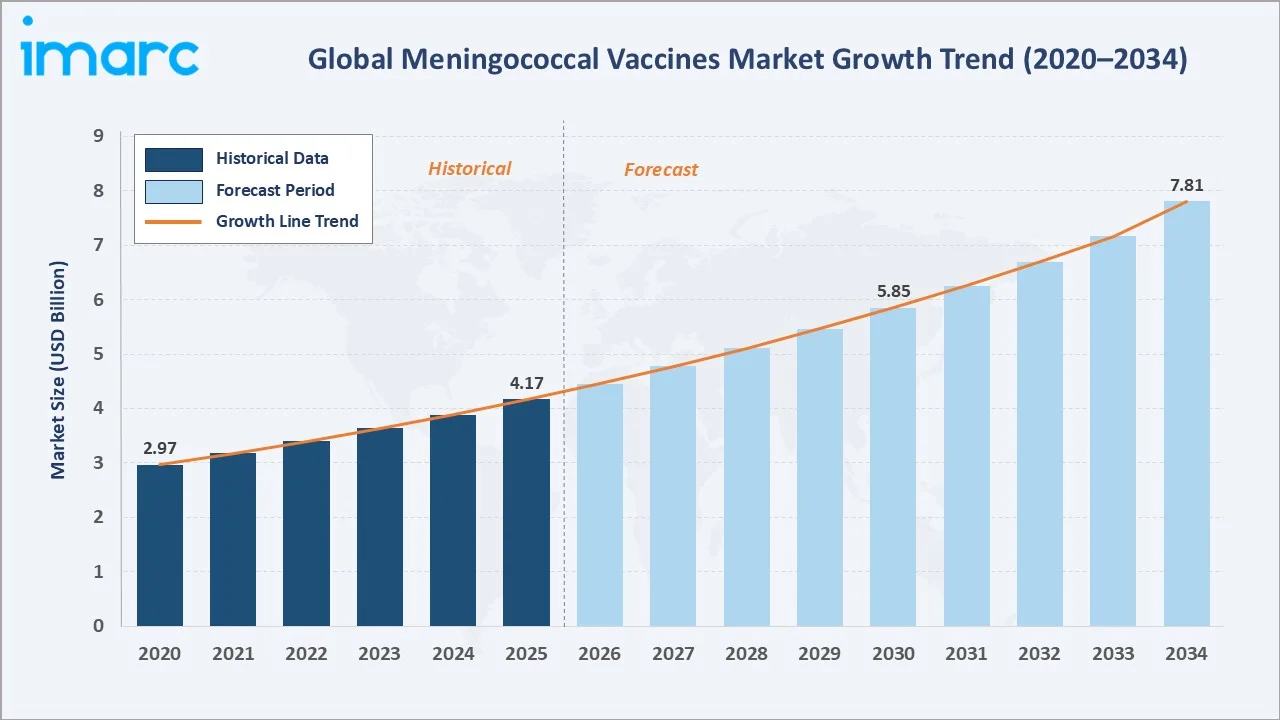

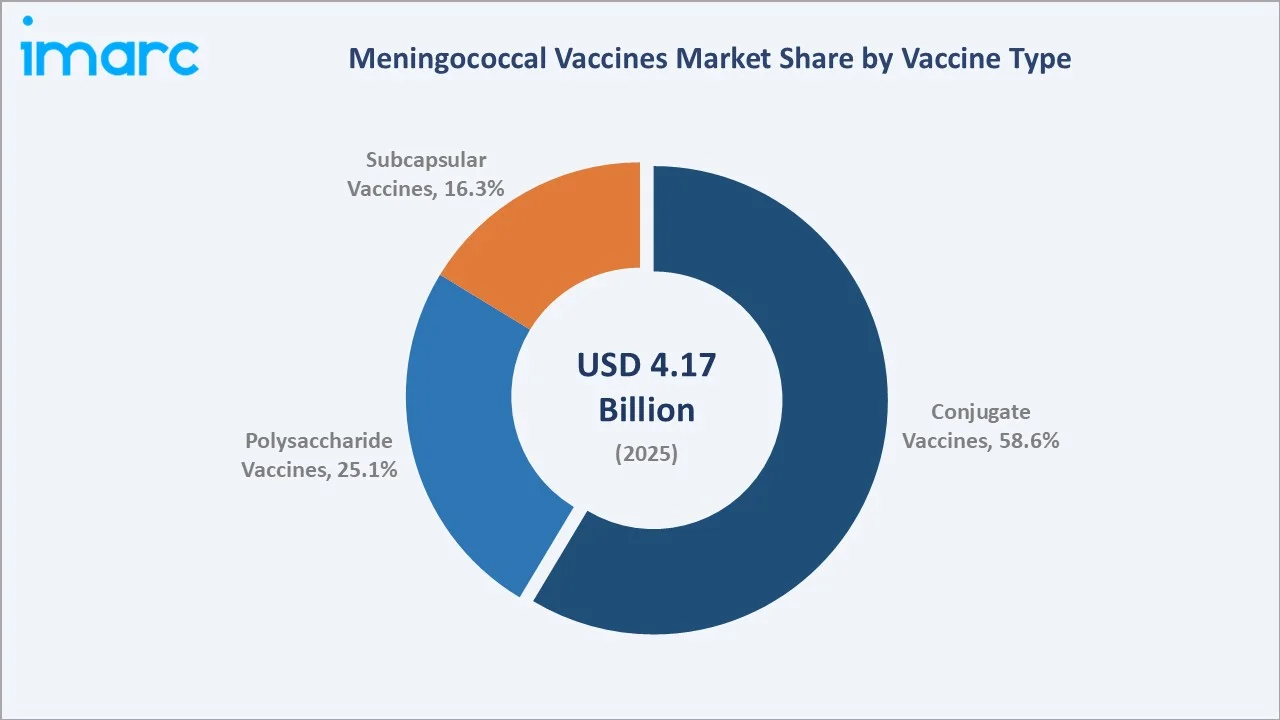

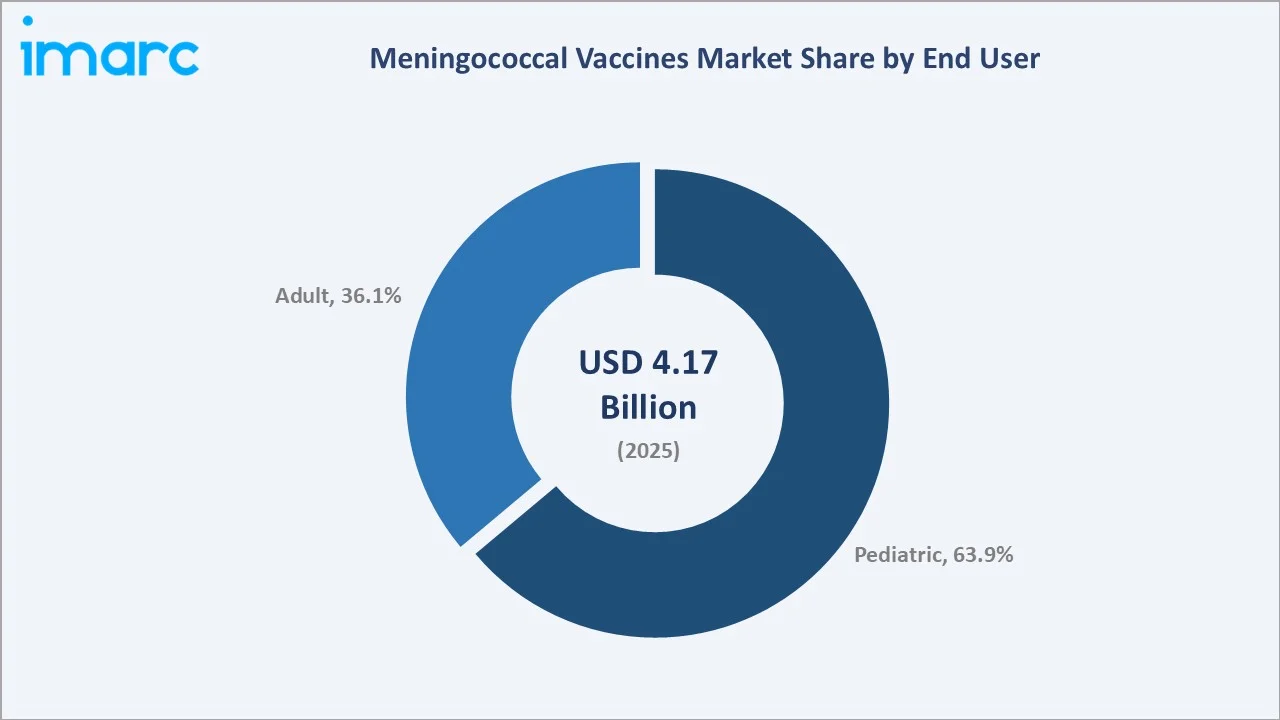

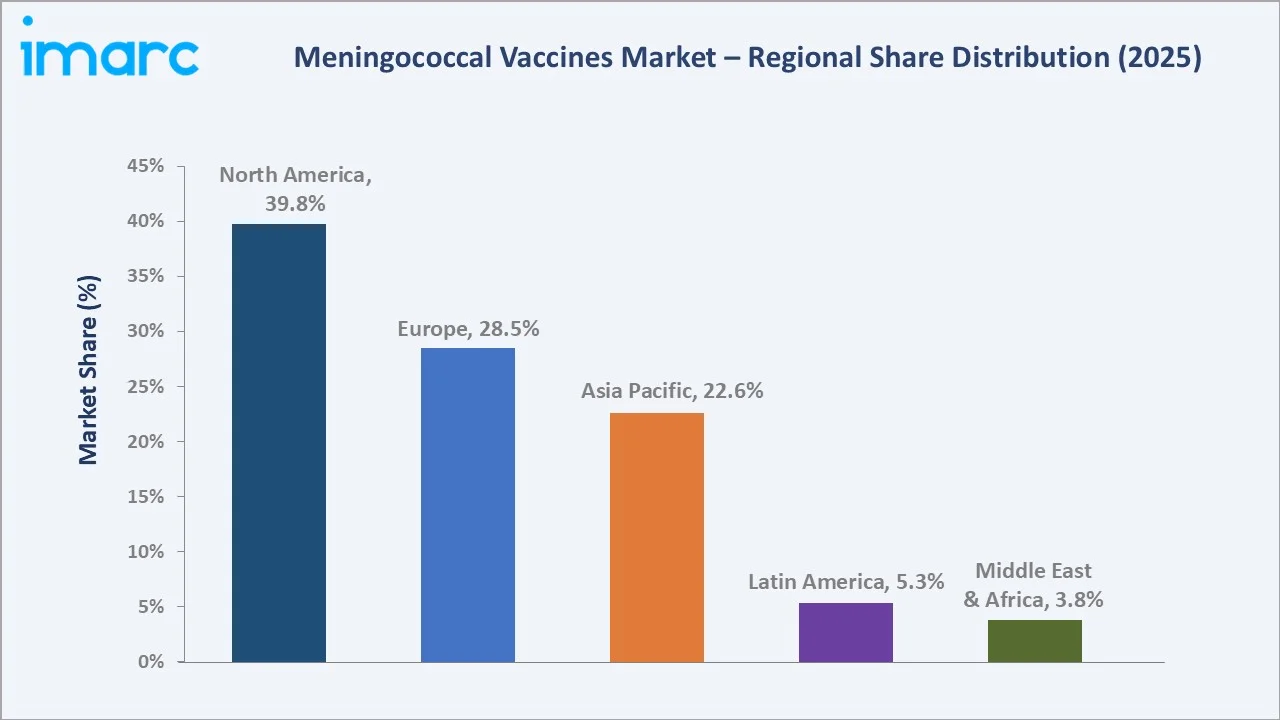

The global meningococcal vaccines market size reached USD 4.17 Billion in 2025 and is projected to reach USD 7.81 Billion by 2034, exhibiting a CAGR of 7.01% during 2026-2034. Rising disease burden, government immunization programs, and technological vaccine advances are the primary forces driving market growth.

Conjugate vaccines dominate at 58.6% in 2025, while the pediatric segment leads end-user demand at 63.9%. North America commands a dominant 39.8% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.17 Billion |

|

Forecast Market Size (2034) |

USD 7.81 Billion |

|

CAGR (2026-2034) |

7.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.8% share, 2025) |

|

Second Largest Region |

Europe (28.5% share, 2025) |

|

Leading Vaccine Type |

Conjugate Vaccines (58.6%, 2025) |

|

Leading End User |

Pediatric (63.9%, 2025) |

The market growth from 2020 through 2034, with historical expansion to USD 4.17 Billion in 2025, reflects consistent immunization-driven demand. The forecast to USD 7.81 Billion captures accelerating pediatric programs, MenB vaccine adoption, and emerging market rollouts under international health funding frameworks.

To get more information on this market, Request Sample

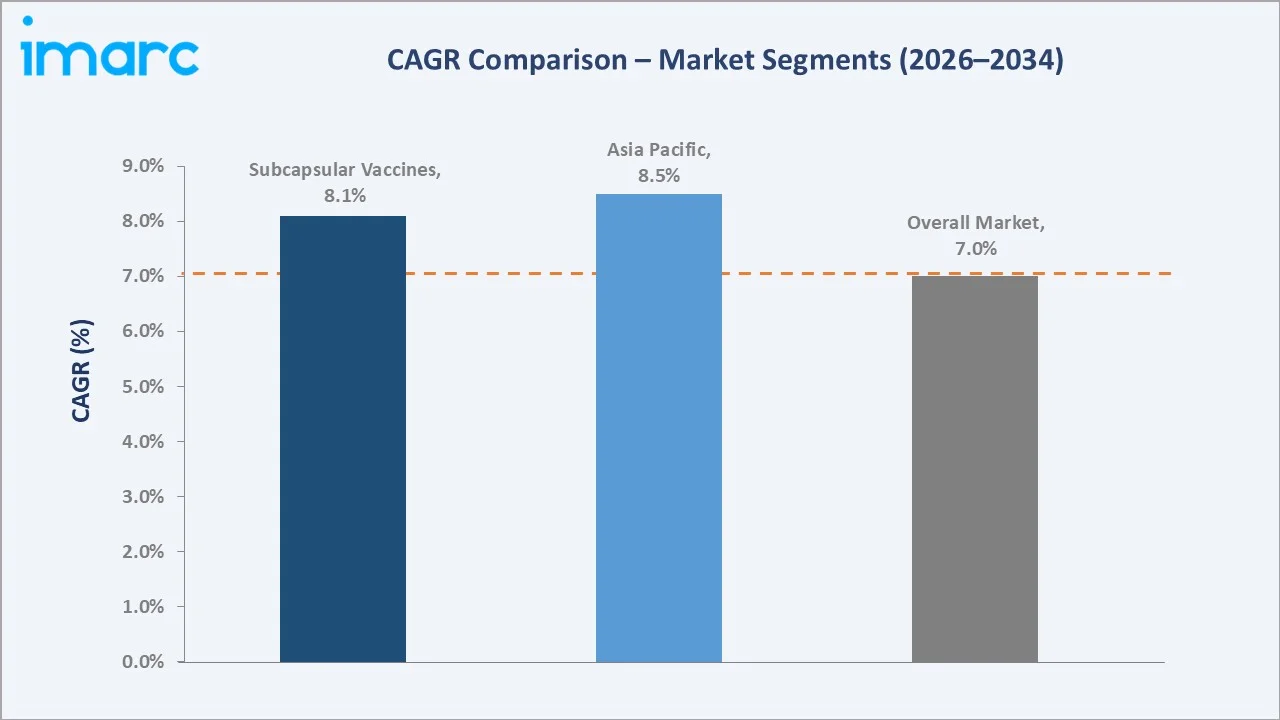

The CAGR trajectories across key vaccine type, end-user, and regional sub-segments, with subcapsular vaccines and Asia Pacific representing the fastest-growing categories, reflect the broad-based structural expansion within the global meningococcal vaccines industry through 2034.

Executive Summary

The global meningococcal vaccines market is on a sustained growth trajectory from USD 4.17 Billion in 2025 to USD 7.81 Billion by 2034. Meningococcal vaccines are critical public health tools targeting Neisseria meningitidis, which causes bacterial meningitis with significant case fatality rates even with modern antibiotic treatment.

Conjugate vaccines dominate at 58.6% in 2025, offering superior immunogenicity and herd immunity induction. Polysaccharide vaccines (25.1%) remain prevalent in lower-income settings due to affordability advantages, while subcapsular vaccines (16.3%) represent the fastest-growing innovation segment driven by MenB program expansion.

North America dominates at 39.8% in 2025, supported by well-established public health programs and adolescent vaccination mandates. Europe (28.5%) follows with robust national immunization schedules, while Asia Pacific (22.6%) is the fastest-growing region, driven by expanding universal immunization programs across high-population markets.

Key Market Insights

|

Insight |

Data |

|

Largest Vaccine Type |

Conjugate Vaccines – 58.6% share (2025) |

|

Leading End User |

Pediatric – 63.9% share (2025) |

|

Leading Region |

North America – 39.8% share (2025) |

|

Second Largest Region |

Europe – 28.5% share (2025) |

|

Top Companies |

GSK plc, Incepta Pharmaceuticals Ltd., Pfizer Inc., Sanofi, Serum Institute of India Pvt. Ltd., Walvax Biotechnology Co., Ltd. |

Key Analytical Observations Supporting the Above Data:

- Conjugate vaccines, with 58.6% share in 2025, dominate due to superior T-cell-dependent immunogenicity, enabling durable memory responses and herd immunity, critical advantages that make them the preferred choice for national immunization programs globally.

- Pediatric end-users, with 63.9% share in 2025, lead because meningococcal disease disproportionately affects infants and adolescents. WHO-recommended schedules mandate vaccination in early childhood, establishing pediatric care as the structural demand core.

- North America's 39.8% dominance reflects mandatory school-entry vaccination requirements, high physician recommendation rates, and comprehensive insurance reimbursement policies supporting routine meningococcal immunization across all age-eligible populations.

- Asia Pacific at 22.6% in 2025 represents the fastest-growing region as China, India, and Southeast Asian nations expand universal immunization programs and international health funding supports meningococcal vaccine introductions across high-burden countries.

Global Meningococcal Vaccines Market Overview

Meningococcal vaccines are biological immunization agents designed to protect against Neisseria meningitidis serogroups, including A, B, C, W, X, and Y — the causative agents of bacterial meningitis and septicemia. Product categories span conjugate, polysaccharide, and subcapsular protein formulations across mono and combination vaccine presentations.

The global ecosystem integrates antigen research organizations, vaccine manufacturers, contract development and manufacturing organizations, cold chain logistics providers, national immunization program authorities, international health agencies, healthcare providers, and diverse end-user populations across pediatric and adult segments.

Market Dynamics

To evaluate market opportunities, Request Sample

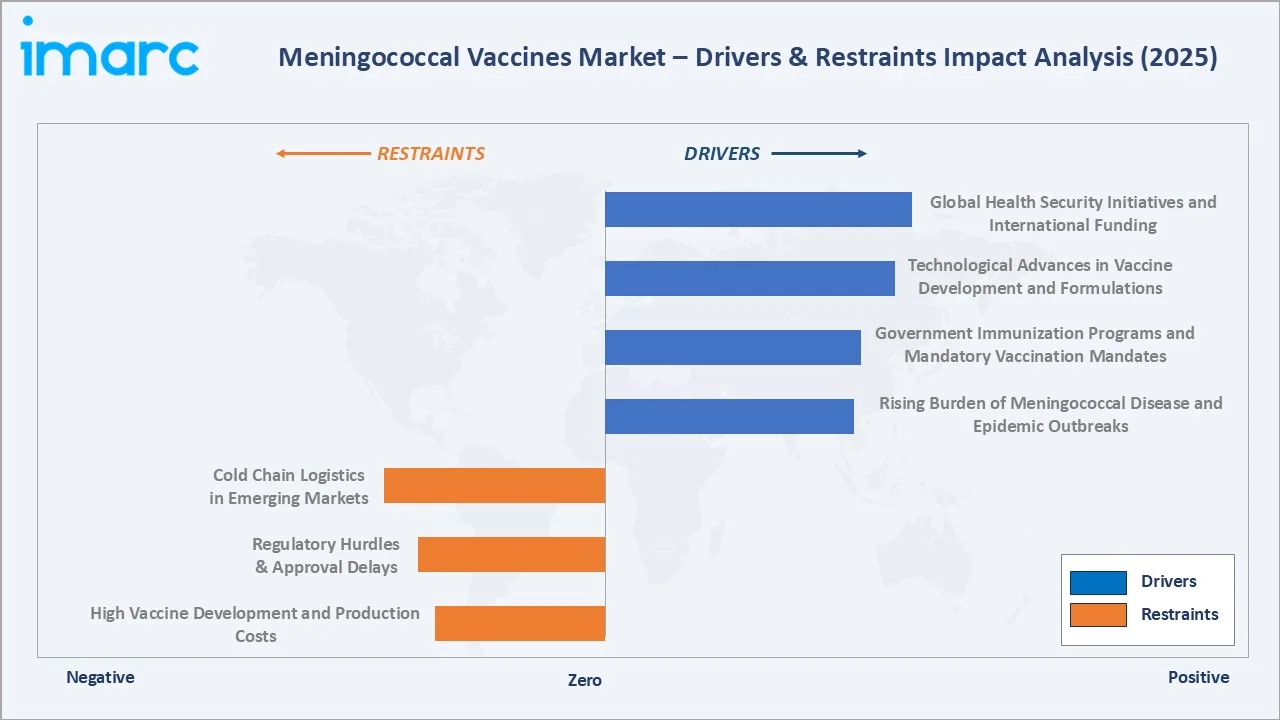

Market Drivers

- Rising Burden of Meningococcal Disease and Epidemic Outbreaks: Meningococcal disease outbreaks in Africa's meningitis belt and sporadic cases in high-income countries continuously reinforce public health urgency. The high fatality rate and risk of severe neurological sequelae in survivors drive proactive immunization policy adoption.

- Government Immunization Programs and Mandatory Vaccination Mandates: National immunization programs across North America, Europe, and increasingly Asia Pacific mandate meningococcal vaccination at key age milestones, infancy, early childhood, and adolescence, generating consistent, policy-driven institutional procurement demand.

- Technological Advances in Vaccine Development and Formulations: Innovations including ready-to-use liquid formulations, multi-component protein vaccines, and next-generation conjugation chemistry are improving vaccine tolerability, schedule flexibility, and immunogenic performance, expanding clinical adoption across age groups.

- Global Health Security Initiatives and International Funding: International commitments to the WHO Defeating Meningitis by 2030 roadmap, Gavi Vaccine Alliance programs, and UNICEF procurement frameworks are mobilizing substantial financing that expands meningococcal vaccine access in low- and middle-income countries globally.

Market Restraints

- High Vaccine Development and Production Costs: Meningococcal vaccine development requires complex biological manufacturing, including fermentation, conjugation chemistry, and multi-antigen formulation. These production requirements create high per-dose costs and limit market entry to well-capitalized pharmaceutical manufacturers with specialized biological manufacturing capabilities.

- Regulatory Hurdles and Approval Delays: Regulatory approval timelines for new meningococcal vaccine formulations are lengthy, requiring extensive clinical evidence across multiple serogroups and age groups. Post-marketing surveillance requirements and lot-release testing add operational complexity that constrains rapid supply scaling during outbreak response scenarios.

- Cold Chain Logistics Challenges in Emerging Markets: Meningococcal vaccines require consistent refrigerated storage throughout distribution. Inadequate cold chain infrastructure across sub-Saharan Africa and parts of South Asia results in vaccine wastage and limits effective program reach, increasing the total cost of immunization delivery and constraining coverage in the highest-burden geographies.

Market Opportunities

- Pan-Meningococcal Combination Vaccine Development: Development of single-dose vaccines covering all major serogroups represents a transformational commercial opportunity. Such products could consolidate current multi-injection regimens, improve schedule compliance, and create new premium market segments in both high-income and transitional healthcare systems.

- Expanding Adult Vaccination Programs: College students, military recruits, immunocompromised individuals, and travelers to endemic regions represent underserved adult vaccination segments with growing awareness and regulatory support. Expanding adult indications for existing vaccines represents a meaningful incremental market opportunity beyond core pediatric programs.

Market Challenges

- Vaccine Hesitancy and Public Awareness Gaps: Despite the disease's severity, meningococcal vaccine hesitancy persists in several markets. Low perceived disease risk and misinformation about vaccine side effects undermine program completion rates, requiring sustained public health communication investment from manufacturers and health authorities to maintain vaccination coverage levels.

- Competition from Alternative Bacterial Meningitis Prevention Strategies: Pneumococcal and Haemophilus influenzae type b vaccines address overlapping meningitis etiologies, sometimes competing for immunization program budget allocations in resource-constrained settings where public health authorities must prioritize among multiple bacterial meningitis prevention interventions simultaneously.

Emerging Market Trends

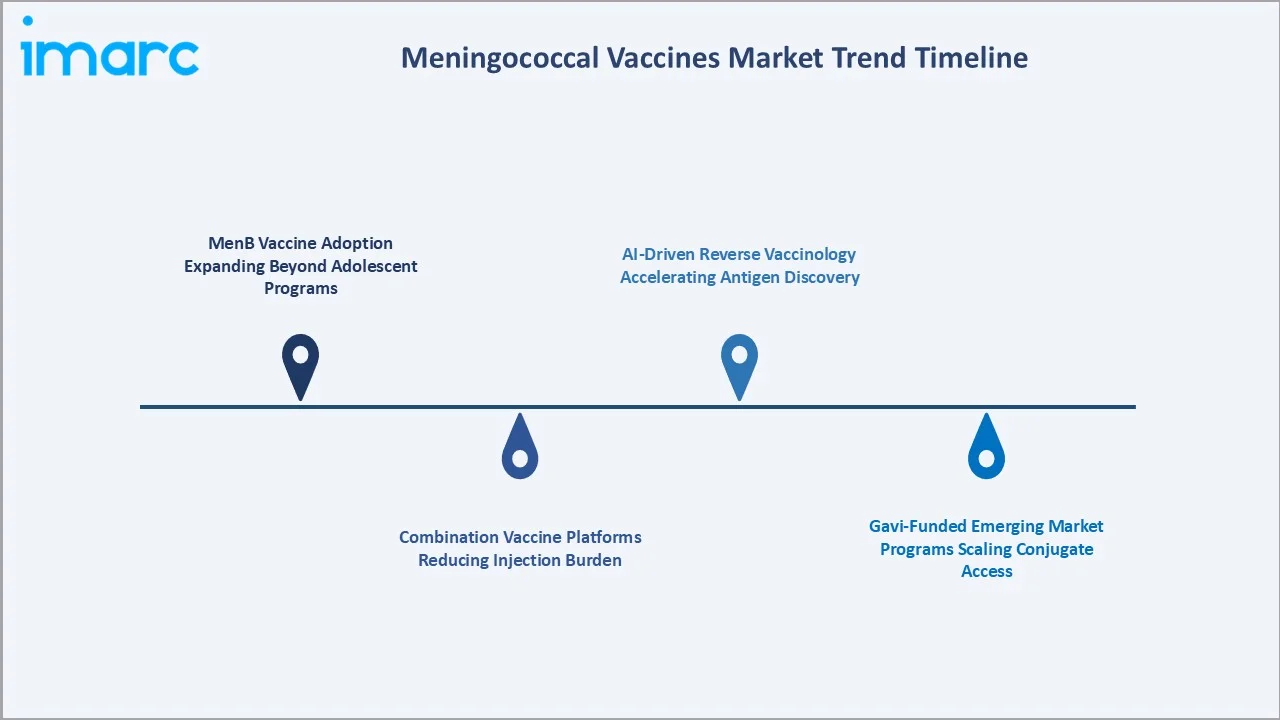

1. MenB Vaccine Adoption Expanding Beyond Adolescent Programs

Bexsero and Trumenba are progressively gaining national immunization schedule inclusion beyond their initial adolescent indications. Demonstrated effectiveness in reducing meningococcal B incidence in countries with routine infant programs is driving policy adoption across Europe and select high-income markets in the Asia Pacific and North America.

2. Combination Vaccine Platforms Reducing Injection Burden

Pharmaceutical companies are investing in pentavalent and hexavalent combination vaccines incorporating meningococcal antigens alongside standard childhood immunization components. Reducing injection count per immunization schedule dramatically improves program compliance and healthcare system operational efficiency in both high-income and emerging markets.

3. AI-Driven Reverse Vaccinology Accelerating Antigen Discovery

Machine learning platforms analyzing Neisseria meningitidis genomic databases are identifying novel conserved protein antigens for next-generation subcapsular vaccines. This approach is being applied to serogroup X vaccine candidates and pan-serogroup antigen identification, compressing development timelines versus traditional approaches.

4. Gavi-Funded Emerging Market Programs Scaling Conjugate Access

Gavi's Meningococcal Vaccine Partnership has facilitated delivery of conjugate vaccines across Africa's meningitis belt. New conjugate product introductions targeting additional serogroups are being negotiated under Advance Market Commitment pricing structures, enabling broader access in low-income countries with high endemic disease burden.

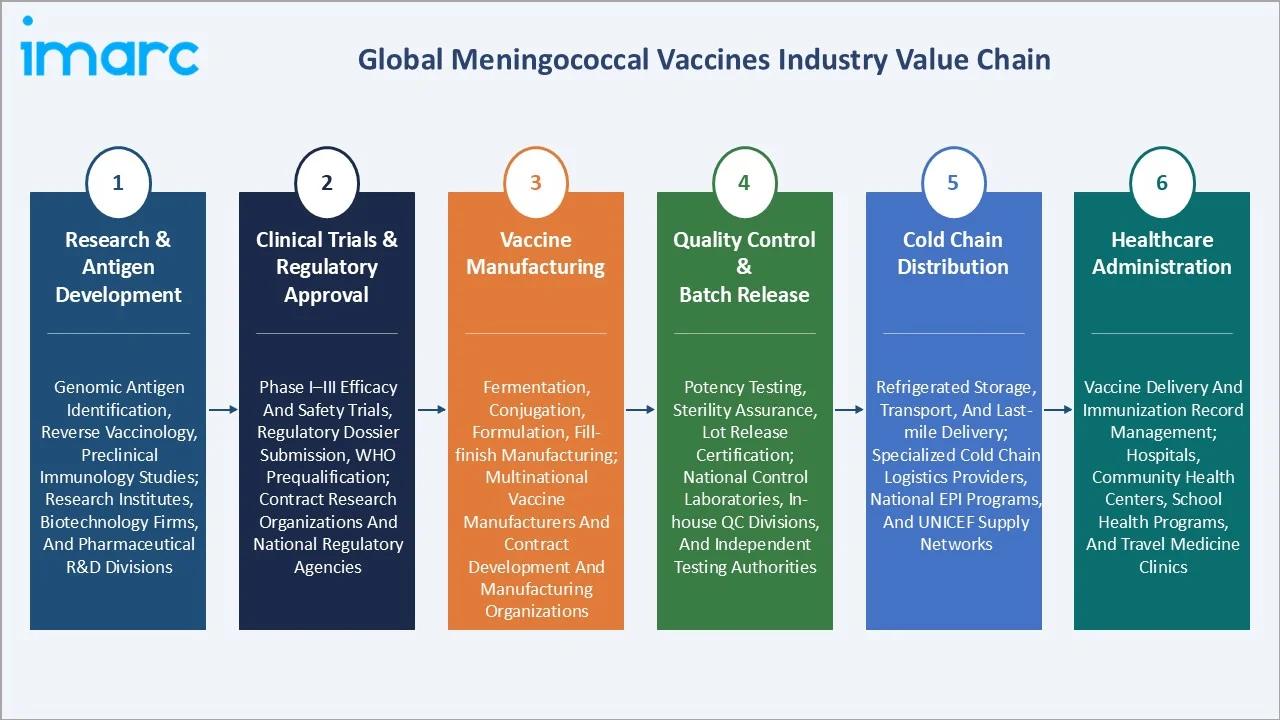

Industry Value Chain Analysis

The meningococcal vaccines value chain spans six stages from antigen research through healthcare administration. Vaccine manufacturing and quality control capture the highest value-add margins, while cold chain distribution generates significant infrastructure investment requirements, favoring well-capitalized manufacturers and logistics partners.

|

Stage |

Key Activities / Players |

|

Research & Antigen Development |

Genomic antigen identification, reverse vaccinology, preclinical immunology studies; research institutes, biotechnology firms, and pharmaceutical R&D divisions |

|

Clinical Trials & Regulatory Approval |

Phase I–III efficacy and safety trials, regulatory dossier submission, WHO prequalification; contract research organizations and national regulatory agencies |

|

Vaccine Manufacturing |

Fermentation, conjugation, formulation, fill-finish manufacturing; multinational vaccine manufacturers and contract development and manufacturing organizations |

|

Quality Control & Batch Release |

Potency testing, sterility assurance, lot release certification; national control laboratories, in-house QC divisions, and independent testing authorities |

|

Cold Chain Distribution |

Refrigerated storage, transport, and last-mile delivery; specialized cold chain logistics providers, national EPI programs, and UNICEF supply networks |

|

Healthcare Administration |

Vaccine delivery and immunization record management; hospitals, community health centers, school health programs, and travel medicine clinics |

Technology Landscape in the Meningococcal Vaccines Industry

Conjugation Technology: Polysaccharide-Protein Carrier Chemistry

Conjugate vaccine production involves chemical attachment of meningococcal polysaccharide antigens to carrier proteins, including CRM197, tetanus toxoid, and diphtheria toxoid. Reductive amination and cyanylation conjugation methods create T-cell-dependent immunogenicity, enabling immunological memory essential for long-term protection.

Outer Membrane Vesicle and NOMV Platforms

Native outer membrane vesicle technology uses genome-based identification of conserved surface proteins, providing broad strain coverage for serogroup B vaccines that cannot use polysaccharide approaches due to immunological cross-reactivity with human tissue. NOMV platforms form the foundation of the most advanced MenB vaccine formulations.

mRNA Vaccine Platform Applications

Post-pandemic mRNA technology success has prompted leading vaccine developers to explore mRNA-based meningococcal vaccine candidates. mRNA platforms offer accelerated development timelines and potential for pan-serogroup antigen combinations, potentially transforming meningococcal vaccine manufacturing economics and immunogen design flexibility.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vaccine Type |

Conjugate |

58.6% |

2025 |

|

Composition |

🔒 |

🔒 |

2025 |

|

Vaccine Serotype |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

Pediatric |

63.9% |

2025 |

|

Region |

North America |

39.8% |

2025 |

By Vaccine Type

Conjugate vaccines command a 58.6% majority share in 2025, attributed to superior immunological performance and the WHO recommendation for national immunization program inclusion. Conjugates induce T-cell-dependent responses, generating B-memory cells and herd immunity not achievable with plain polysaccharide formulations.

To access detailed market analysis, Request Sample

Polysaccharide vaccines at 25.1% retain significant presence in adult booster programs and resource-limited settings where conjugate affordability constraints exist. Bivalent, trivalent, and quadrivalent polysaccharide formulations serve outbreak response and mass immunization campaign requirements effectively at competitive price points.

Subcapsular protein vaccines at 16.3% represent the innovation frontier, exclusively targeting serogroup B through protein antigens. Growing at the fastest CAGR among vaccine types, subcapsular vaccines are expanding into college student and infant programs globally as clinical evidence of real-world effectiveness strengthens policy recommendations.

By End User

The pediatric segment commands 63.9% share in 2025, driven by WHO-recommended infant immunization schedules and adolescent catch-up programs. Meningococcal disease incidence peaks in infants and teenagers, establishing pediatric vaccination as the structural demand core for global immunization programs and institutional procurement planning.

The adult segment at 36.1% in 2025 encompasses college students, military recruits, asplenic individuals, complement-deficient patients, laboratory personnel, and travelers to endemic regions. Adult vaccination programs are expanding as regulatory guidelines broaden recommendations and outbreak-related risk awareness increases globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.8% |

Mandatory school immunization requirements; comprehensive insurance reimbursement; strong ACIP recommendations for adolescent and adult programs |

|

Europe |

28.5% |

National immunization schedule expansions; MenB infant and adolescent programs; established surveillance and rapid outbreak response infrastructure |

|

Asia Pacific |

22.6% |

Universal immunization program expansion; government adolescent health initiatives; international funding support for meningococcal vaccine introduction |

|

Latin America |

5.3% |

Regional public health authority programs; growing adolescent vaccination mandates; expanding MenACWY conjugate adoption in national schedules |

|

Middle East & Africa |

3.8% |

Mandatory Hajj vaccination requirements; meningitis belt conjugate programs; outbreak response campaigns and international health funding initiatives |

North America's 39.8% market dominance in 2025 stems from mandatory adolescent vaccination requirements, comprehensive insurance reimbursement through public health funding programs, and active physician recommendation practices embedding meningococcal vaccination into routine adolescent and young adult healthcare visits.

Europe, with 28.5% in 2025, reflects pioneering national MenB infant programs and broad adolescent MenACWY catch-up campaigns that have achieved strong coverage rates. Continental European nations are progressively expanding meningococcal vaccine schedules following disease burden evidence and published program effectiveness data.

Asia Pacific at 22.6% in 2025 represents the fastest-growing regional opportunity. Expanding national immunization program scopes, growing adolescent health investments, and international health funding support are driving meningococcal vaccine market growth across multiple high-population markets in the region.

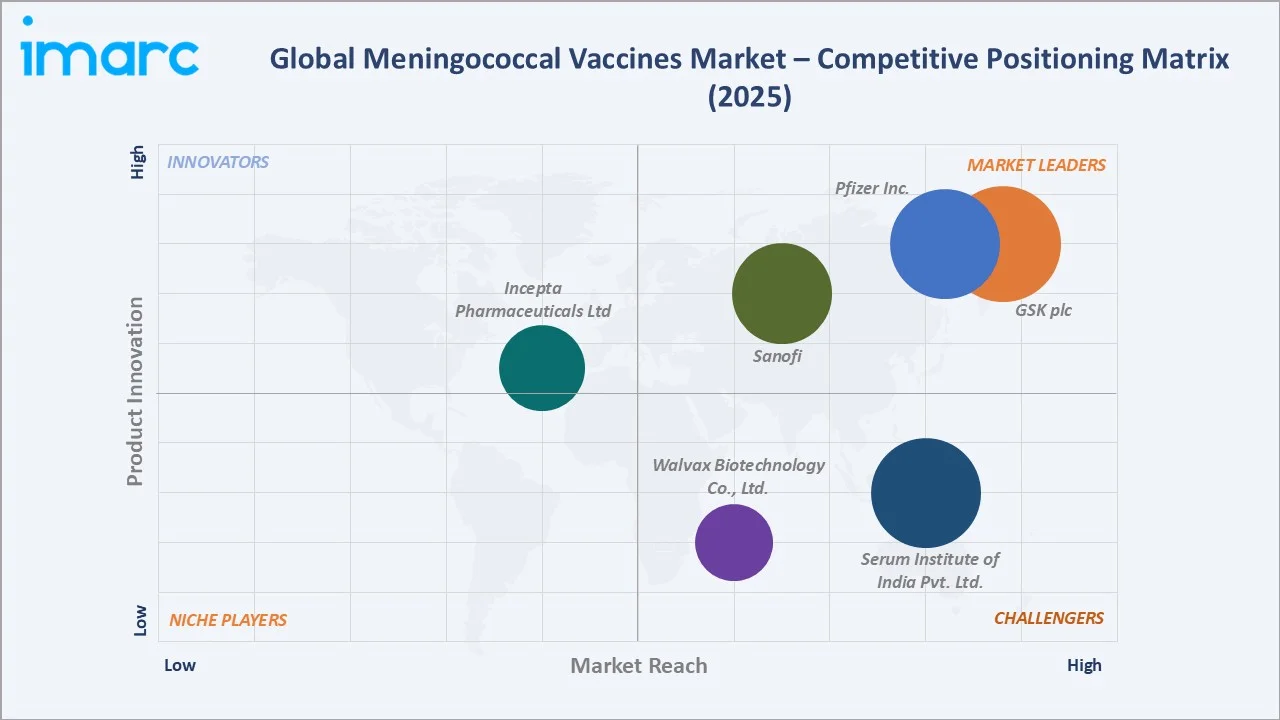

Competitive Landscape

The global meningococcal vaccines market is highly concentrated, with leading multinational pharmaceutical companies collectively commanding the majority of global revenue. Market entry barriers are substantial due to regulatory complexity, biological manufacturing requirements, and the need for extensive clinical evidence across multiple serogroups and age groups.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

GSK plc |

Bexsero, Menveo, Penmenvy |

Leader |

MenB & quadrivalent conjugate leadership; infant to adult programs; global NIP partnerships |

|

Incepta Pharmaceuticals Ltd. |

Ingovax ACWY |

Emerging |

South Asia markets; affordable polysaccharide formulations; public health program access |

|

Pfizer Inc. |

Trumenba, Penbraya |

Leader |

MenB & broad-spectrum conjugate portfolio; adolescent leadership; next-generation pipeline |

|

Sanofi |

Menactra, MenQuadfi |

Leader |

Quadrivalent conjugate leadership; global NIP partnerships; emerging market access programs |

|

Serum Institute of India Pvt. Ltd. |

MenAfriVac, MenFive |

Challenger |

Africa meningitis belt supply; international health organization partnerships; cost-effective manufacture |

|

Walvax Biotechnology Co., Ltd. |

ACYW135 Conjugate, Group A and Group C Meningococcal Conjugate Vaccine |

Challenger |

China and emerging Asia markets; government tender supply; expanding product pipeline |

Key players include GSK plc, Incepta Pharmaceuticals Ltd., Pfizer Inc., Sanofi, Serum Institute of India Pvt. Ltd., Walvax Biotechnology Co., Ltd., and others.

Key Company Profiles

GSK plc

GSK is the global leader in meningococcal vaccines, headquartered in London, United Kingdom. GSK holds the broadest meningococcal vaccine portfolio globally, with products serving infant, adolescent, and adult vaccination programs across a wide range of national immunization schedules in both high-income and emerging markets.

- Product Portfolio: Bexsero, Menveo, Penmenvy

- Recent Developments: In February 2025, GSK received U.S. FDA approval for PENMENVY, its new 5-in-1 meningococcal vaccine designed to protect against five major strains of Neisseria meningitidis, A, B, C, W, and Y. The vaccine is approved for use in individuals aged 10 to 25 years and aims to broaden protection against invasive meningococcal disease with two-dose series administered six months apart.

- Strategic Focus: GSK's meningococcal strategy centers on defending Bexsero's MenB leadership through lifecycle management and expanded age indications, while leveraging Menveo and partnerships to address the growing quadrivalent conjugate market in high-growth Asia Pacific and Latin American geographies.

Pfizer Inc.

Pfizer Inc. is a global biopharmaceutical leader headquartered in New York, United States, with a significant meningococcal vaccine franchise. Pfizer's products serve complementary market segments, with strong positioning in the US adolescent market supported by regulatory guideline alignment and active physician advocacy programs.

- Product Portfolio: Trumenba, Penbraya

- Recent Developments: In October 2023, Pfizer received U.S. FDA approval for PENBRAYA, the pentavalent meningococcal vaccine designed to protect against the five most common serogroups of Neisseria meningitidis, A, B, C, W, and Y, in adolescents and young adults aged 10 to 25 years. The approval marks a significant expansion in meningococcal disease prevention by combining broad protection into a single vaccine.

- Strategic Focus: Pfizer's strategy leverages its Trumenba differentiation in adolescent and college markets, while positioning Nimenrix for global NIP adoption in Europe and emerging markets. Its mRNA platform experience positions Pfizer as a key developer of next-generation pan-serogroup meningococcal vaccine candidates.

Sanofi

Sanofi is a leading global pharmaceutical company headquartered in Paris, France, with one of the most established meningococcal quadrivalent vaccine franchises worldwide. Sanofi's Vaccines division manages products across the US, European, and emerging market national immunization programs with a growing next-generation portfolio.

- Product Portfolio: Menactra, MenQuadfi

- Recent Developments: In May 2025, Sanofi received U.S. FDA approval to expand the use of its meningococcal vaccine MenQuadfi to infants as young as six weeks old, making it the first vaccine of its kind approved for this age group in the United States. The vaccine protects against four major strains of Neisseria meningitidis, A, C, W, and Y, which can cause severe and potentially life-threatening infections such as meningitis and bloodstream infections.

- Strategic Focus: Sanofi's meningococcal strategy transitions the global quadrivalent market toward MenQuadfi, leveraging superior thermostability and broader age indications for emerging market penetration, while defending North American leadership through established payer relationships and guideline-aligned product positioning.

Market Concentration Analysis

The global meningococcal vaccines market is highly concentrated, contrasting with more fragmented commodity markets. The leading manufacturers collectively hold the majority of global market revenue, reflecting substantial regulatory and biological manufacturing barriers that limit new entrant ability to compete across multiple serogroups.

Regional concentration patterns differ meaningfully. North America and Europe are served primarily by the major multinational vaccine companies. Asia Pacific domestic markets are addressed by regional manufacturers alongside multinational suppliers. Consolidation through licensing, co-marketing agreements, and pipeline asset acquisition continues globally.

Investment & Growth Opportunities

Fastest-Growing Segments

Subcapsular protein vaccines represent the highest-growth product segment, driven by MenB program expansion and next-generation protein antigen pipeline candidates. The Asia Pacific region represents the broadest untapped immunization opportunity with multiple high-population markets expanding meningococcal vaccine coverage.

Emerging Markets

Africa's meningitis belt countries, with Gavi transition-phase economies expanding meningococcal conjugate coverage, represent the next large-scale immunization market. Potential national immunization program inclusions of quadrivalent conjugate vaccines in high-population emerging markets would create substantial incremental procurement demand.

Venture & Investment Trends

Biotech investment in pan-meningococcal vaccine platforms is growing, with developers of broad-coverage subcapsular vaccine candidates attracting significant funding. Partnership structures between multinational vaccine companies and cost-efficient contract manufacturers are creating new technology transfer and co-development investment models.

Future Market Outlook (2026-2034)

The global meningococcal vaccines market is forecast to expand from USD 4.17 Billion in 2025 to USD 7.81 Billion by 2034 at a CAGR of 7.01%, adding substantial incremental annual market value over the forecast period. This sustained growth reflects global immunization program expansion and continuous vaccine innovation.

Three forces will most significantly shape the market through 2034: WHO's Defeating Meningitis by 2030 roadmap implementation, pan-meningococcal combination vaccine approvals consolidating multi-injection regimens, and mRNA platform adaptation enabling more responsive and flexible meningococcal vaccine development and manufacture.

Research Methodology

Primary Research

Primary research encompassed structured interviews with meningococcal vaccine industry stakeholders, including senior medical affairs managers, national immunization program officials, WHO vaccine policy experts, hospital procurement specialists, and pediatric infectious disease clinicians across North America, Europe, and Asia Pacific regions.

Secondary Research

Key secondary sources include WHO Global Vaccine Action Plan documentation, UNICEF Supply Division procurement reports, CDC ACIP recommendations, EMA vaccine assessment reports, Gavi program documentation, SAGE working group reports on meningococcal vaccines, and peer-reviewed publications in leading infectious disease and vaccine journals.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating immunization coverage rates, birth cohort sizing, epidemiological disease burden data, government procurement budgets, and pricing trend analysis across reimbursed and out-of-pocket market segments worldwide.

Meningococcal Vaccines Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vaccine Types Covered | Conjugate, Polysaccharide, Subcapsular |

| Compositions Covered | Mono Vaccines, Combination Vaccines |

| Vaccine Serotypes Covered | MenACWY, MenB & Manic, MenC, MenA, MenAC, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Institutional Sales, Others |

| End Users Covered | Pediatric, Adult |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GSK plc, Incepta Pharmaceuticals Ltd., Pfizer Inc., Sanofi, Serum Institute of India Pvt. Ltd., Walvax Biotechnology Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the meningococcal vaccines market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global meningococcal vaccines market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the meningococcal vaccines industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Meningococcal Vaccines Market Report

The global meningococcal vaccines market reached USD 4.17 Billion in 2025, reflecting consistent demand from government immunization programs, rising disease burden awareness, and expanding adolescent and pediatric vaccination mandates across global markets.

The market is projected to reach USD 7.81 Billion by 2034, growing at a CAGR of 7.01% during 2026-2034, driven by WHO meningitis elimination programs, new subcapsular vaccine launches, and Asia Pacific immunization program expansion.

Conjugate vaccines lead with a 58.6% share in 2025, valued for superior immunogenicity, herd immunity induction, and WHO recommendation for national immunization program inclusion from infancy through adolescence across high-income and transitional economies.

The pediatric segment leads at 63.9% in 2025, driven by infant and adolescent immunization schedule mandates, since meningococcal disease disproportionately affects young children and teenagers, establishing pediatric as the structural demand core globally.

North America commands a dominant 39.8% market share in 2025, driven by mandatory school vaccination requirements, comprehensive public health funding, and active CDC guideline recommendations for meningococcal immunization across key age groups.

Subcapsular protein vaccines are the fastest-growing type, driven by MenB program expansion in Europe and the US, and next-generation protein antigen candidates addressing serogroup X and pan-serogroup protection needs across emerging and high-income markets.

Leading companies include GSK plc, Incepta Pharmaceuticals Ltd., Pfizer Inc., Sanofi, Serum Institute of India Pvt. Ltd., Walvax Biotechnology Co., Ltd., and others.

Key applications include routine pediatric immunization, adolescent school and college entry vaccination, military and high-risk adult programs, pre-travel immunization for endemic region visitors, and outbreak response mass immunization campaigns globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)