Metal Casting Market Size, Share, Trends and Forecast by Process, Material Type, End Use, Components, Vehicle Type, Electric and Hybrid Type, Application, and Region, 2026-2034

Global Metal Casting Market Size, Share, Trends & Forecast (2026-2034)

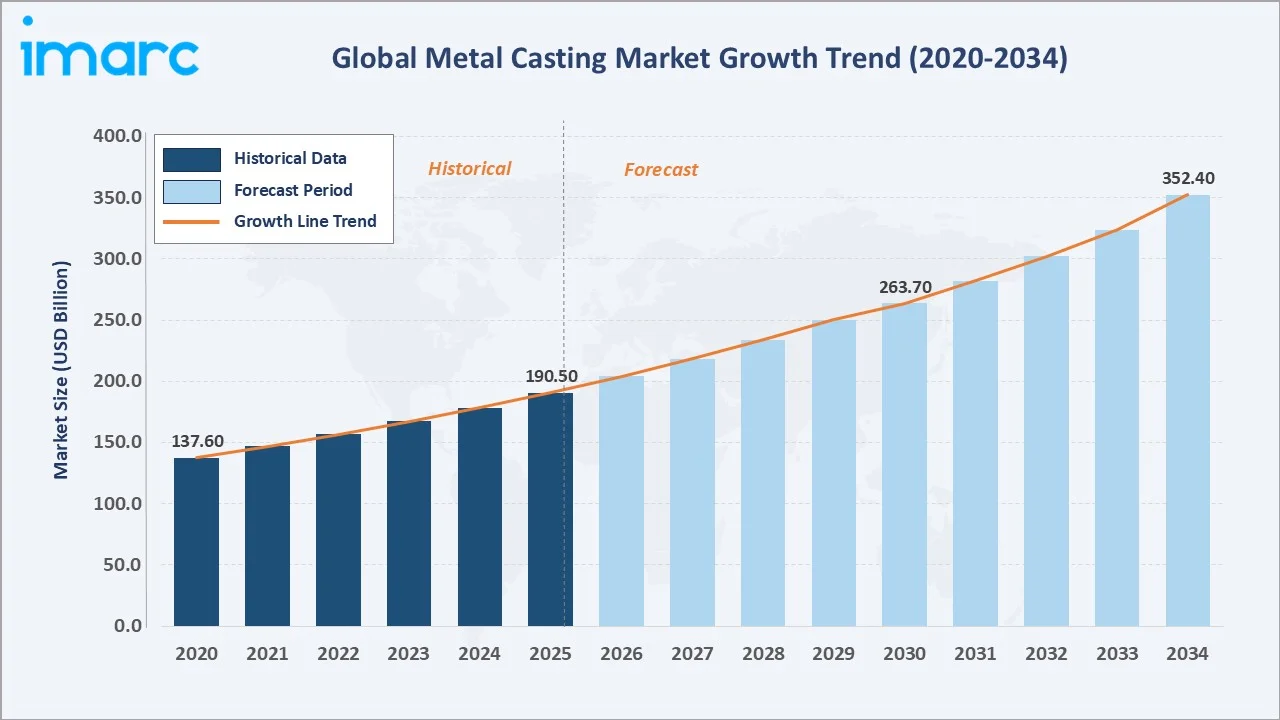

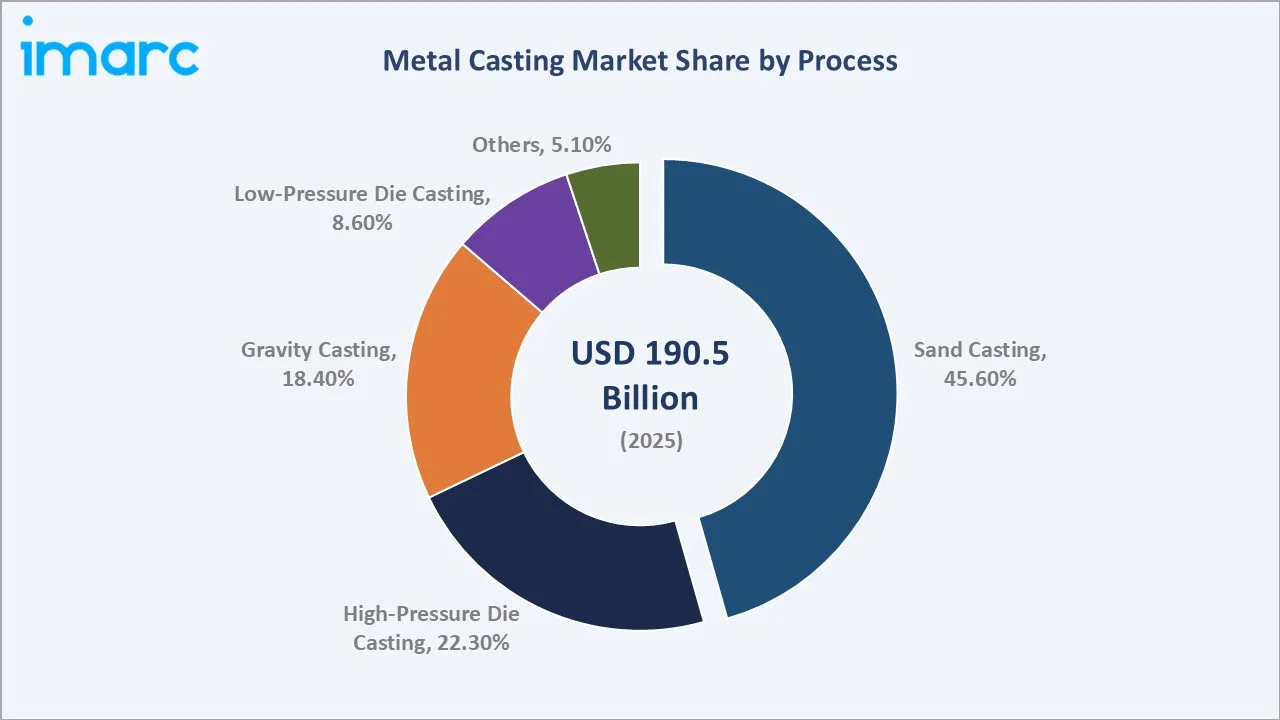

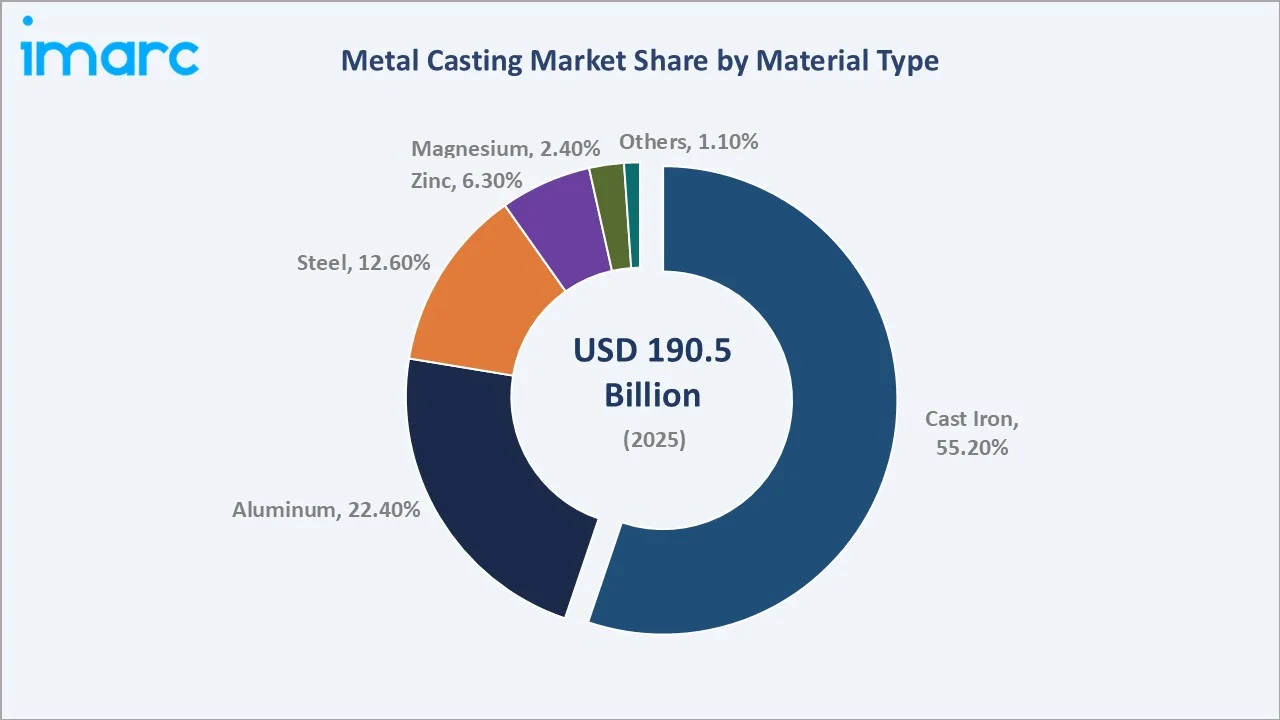

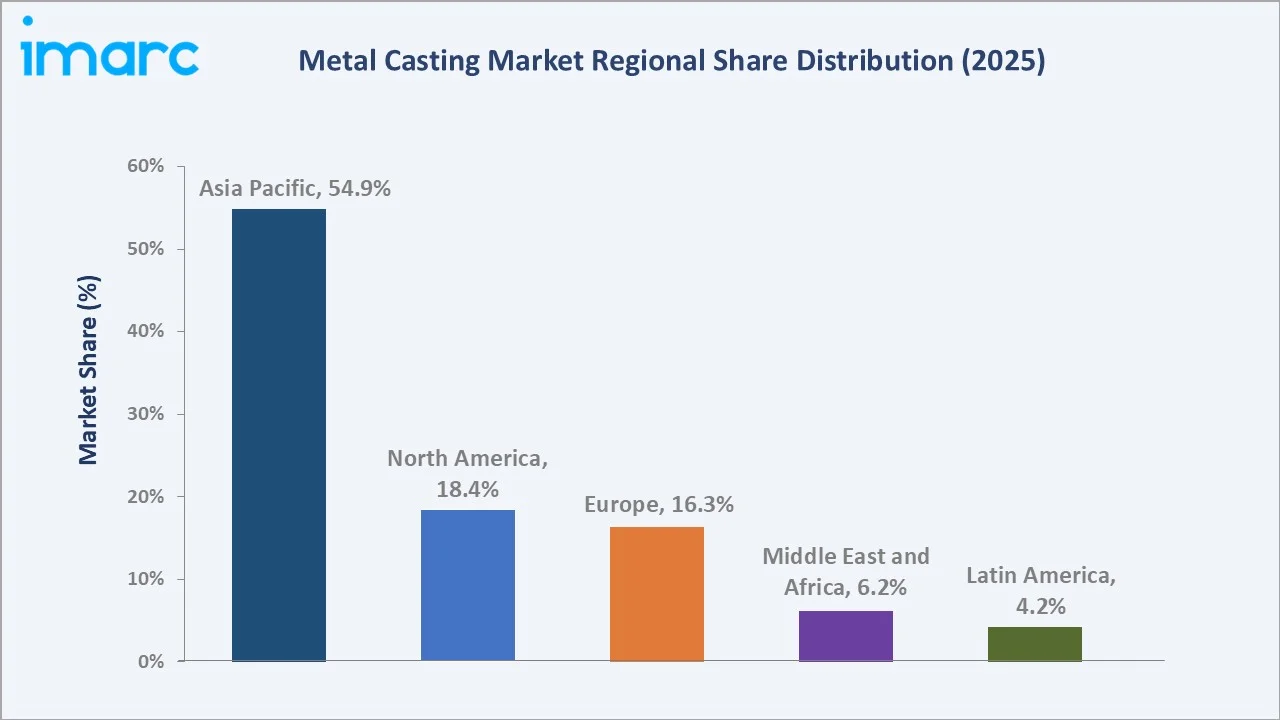

The global metal casting market size reached USD 190.5 Billion in 2025 and is projected to reach USD 352.4 Billion by 2034, at a CAGR of 6.70% during 2026-2034. Rapid industrialization, with 2.3% growth in industrial sectors globally in 2023, soaring demand for lightweight automotive and aerospace components, and large-scale infrastructure development across Asia Pacific and emerging economies are the key growth catalysts. Sand casting leads the process segment at 45.6%, cast iron dominates the material type segment at 55.2%, and Asia Pacific commands the largest regional share at 54.9% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 190.5 Billion |

|

Forecast Market Size (2034) |

USD 352.4 Billion |

|

CAGR (2026-2034) |

6.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest and Fastest-growing Region |

Asia Pacific (54.9%, 2025) |

|

Leading Process |

Sand Casting (45.6%, 2025) |

|

Leading Material Type |

Cast Iron (55.2%, 2025) |

The metal casting market trajectory from 2020 through 2034, grew from USD 137.6 Billion in 2020 to USD 190.5 Billion in 2025, anchored at USD 263.7 Billion in 2030 before reaching USD 352.4 Billion by 2034. This steady progression reflects the structural role of metal casting as a foundational manufacturing process across automotive, industrial, and infrastructure sectors.

To get more information on this market, Request Sample

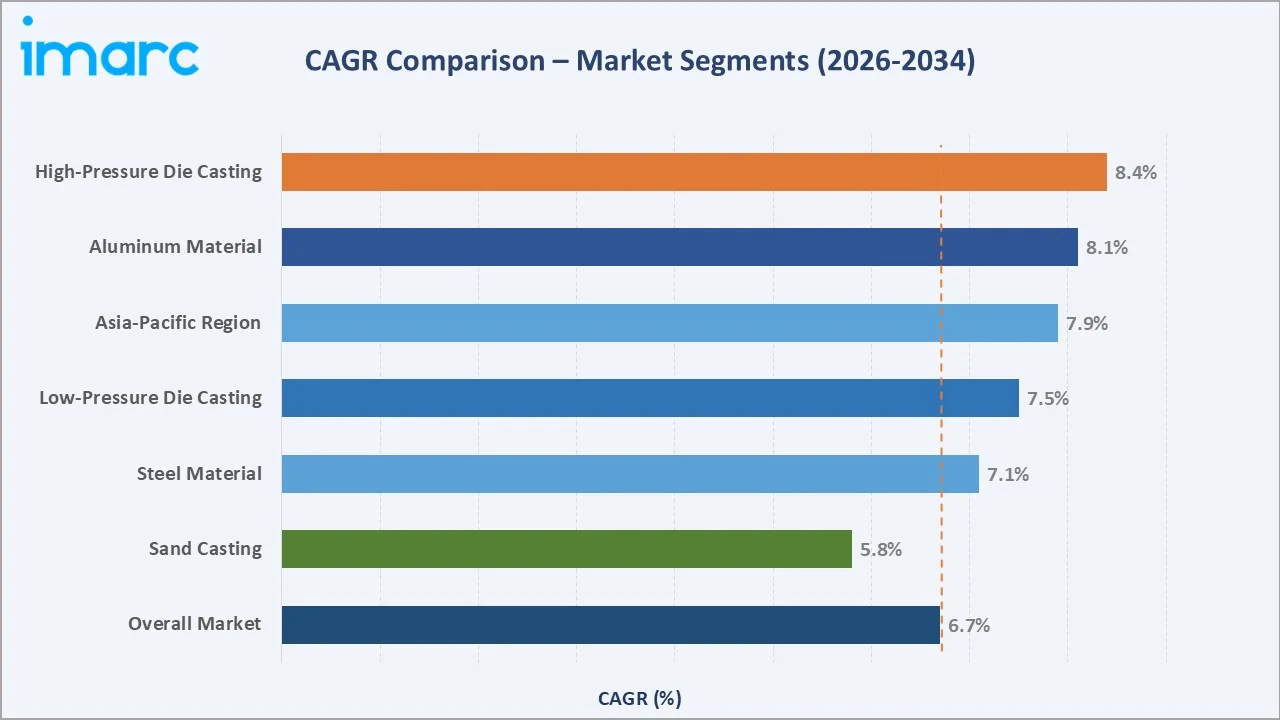

The CAGR across key segments, high-pressure die casting leads at ~8.4% CAGR and aluminum material at ~8.1%, both significantly above the overall 6.70% market rate, reflecting the automotive industry’s shift to lightweight, high-precision aluminum components for electric vehicles (EVs) and fuel-efficient platforms through 2034.

Executive Summary

The global metal casting market is expanding at a 6.70% CAGR from USD 190.5 Billion in 2025 to USD 352.4 Billion by 2034. Metal casting is a manufacturing process in which molten metal is poured into a mold cavity, allowed to solidify, and then removed to produce a component. Casting processes span sand casting, gravity casting, high-pressure die casting, low-pressure die casting, investment casting, and centrifugal casting, each suited to different material types, production volumes, dimensional tolerances, and surface finish requirements across a wide range of end-use applications.

Sand casting commands 45.6% of the process share in 2025 as the most versatile and cost-effective process for large, complex ferrous and non-ferrous components. High-pressure die casting (HPDC) at 22.3% is growing fastest at ~8.4% CAGR, driven by its dominance in automotive aluminum component production where precision, thin walls, and high-volume throughput are essential. Cast iron retains the largest material type share at 55.2%, valued for its excellent machinability, vibration damping, and cost-effectiveness in engine blocks, pipes, and heavy machinery, while aluminum at 22.4% is growing fastest at ~8.1% CAGR as EV manufacturers specify lightweight aluminum castings for battery housings, motor casings, and structural components.

Asia Pacific dominates at 54.9% regional share in 2025, driven by China’s massive foundry industry, producing over 51.4 million tons of steel annually alongside India’s rapidly expanding automotive and infrastructure casting sectors. North America (18.4%) and Europe (16.3%) maintain significant shares anchored by premium aerospace, defense, and heavy industrial casting capabilities.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Process |

Sand Casting – 45.6% (2025) |

|

Leading Material Type |

Cast Iron – 55.2% (2025) |

|

Leading and Fastest Growing Region |

Asia Pacific – 54.9% (2025) |

Key Analytical Observations Supporting The Above Data:

- Sand casting at 45.6% (2025) remains irreplaceable for large ferrous castings, engine blocks exceeding 200kg, industrial pump housings, and structural infrastructure components. Over 60% of all metal castings are produced by the sand casting process.

- Cast iron at 55.2% (2025) maintains dominance through its structural role in global industrial infrastructure. Gray iron and ductile iron castings serve water and sewage infrastructure, municipal manholes, industrial gearboxes, and machine tool beds where cast iron’s vibration damping and compressive strength are unmatched by alternative materials at equivalent cost.

- Asia Pacific’s 54.9% regional dominance in 2025 reflects decades of foundry industry development driven by low labor costs, proximity to raw material supply chains, and integration with global automotive and industrial OEM supply chains.

Global Metal Casting Market Overview

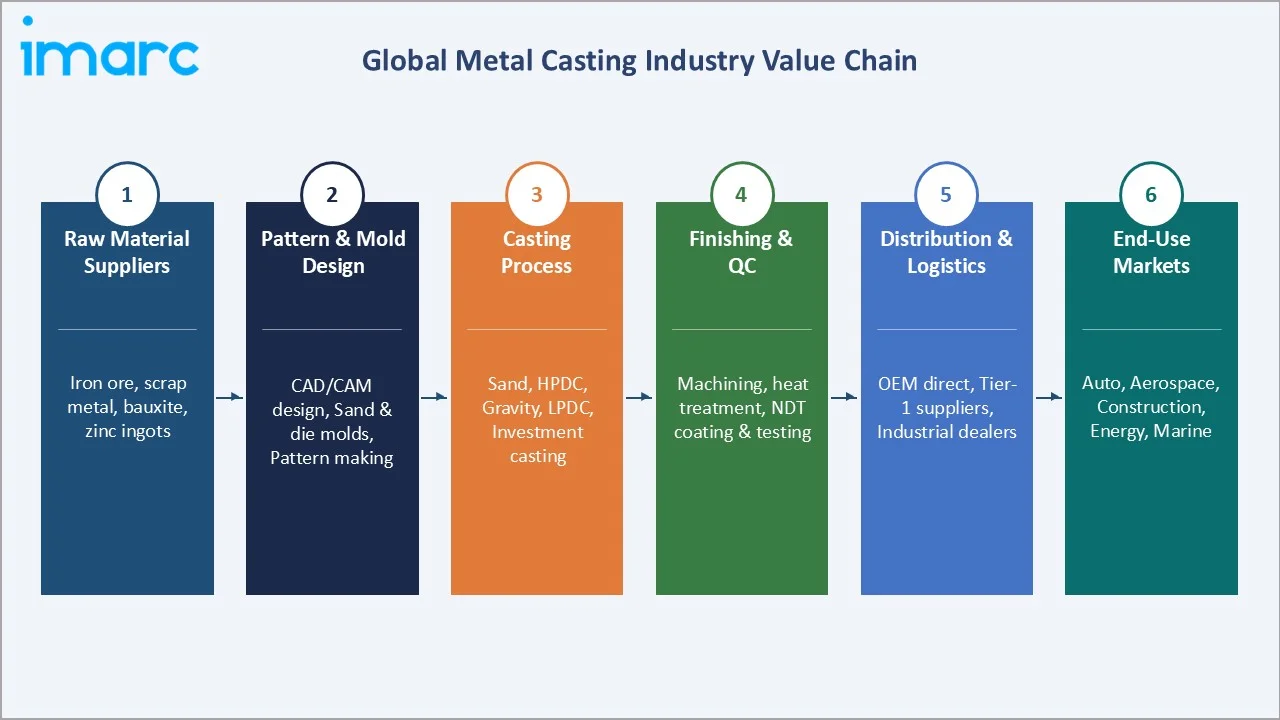

Metal casting is a foundational manufacturing process in which molten metal is poured into a shaped cavity, formed by sand, ceramic, or metal dies, allowed to solidify under gravity or pressure, and then removed to produce a finished or near-net-shape component. The process accommodates virtually all metallic alloys, including gray and ductile iron, carbon and alloy steels, aluminum, magnesium, zinc, copper, nickel superalloys, and titanium. Casting is the preferred process for complex internal geometries, large components, and high-volume production where machining from billet would be impractical or uneconomical.

Applications span every major industrial sector: automotive (engine blocks, transmission housings, suspension components, EV battery enclosures), aerospace and defense (turbine blades, structural airframe brackets, landing gear components), construction and infrastructure (water pipes, municipal castings, structural brackets), energy (wind turbine hubs, pump casings, valve bodies), and industrial machinery (gearbox housings, compressor casings, machine tool beds). The ecosystem integrates raw material suppliers, pattern and mold manufacturers, foundry operations, machining and finishing services, and OEM and Tier-1 distribution networks, all governed by a comprehensive framework of ISO, ASTM, DIN, and JIS casting quality standards.

Market Dynamics

To evaluate market opportunities, Request Sample

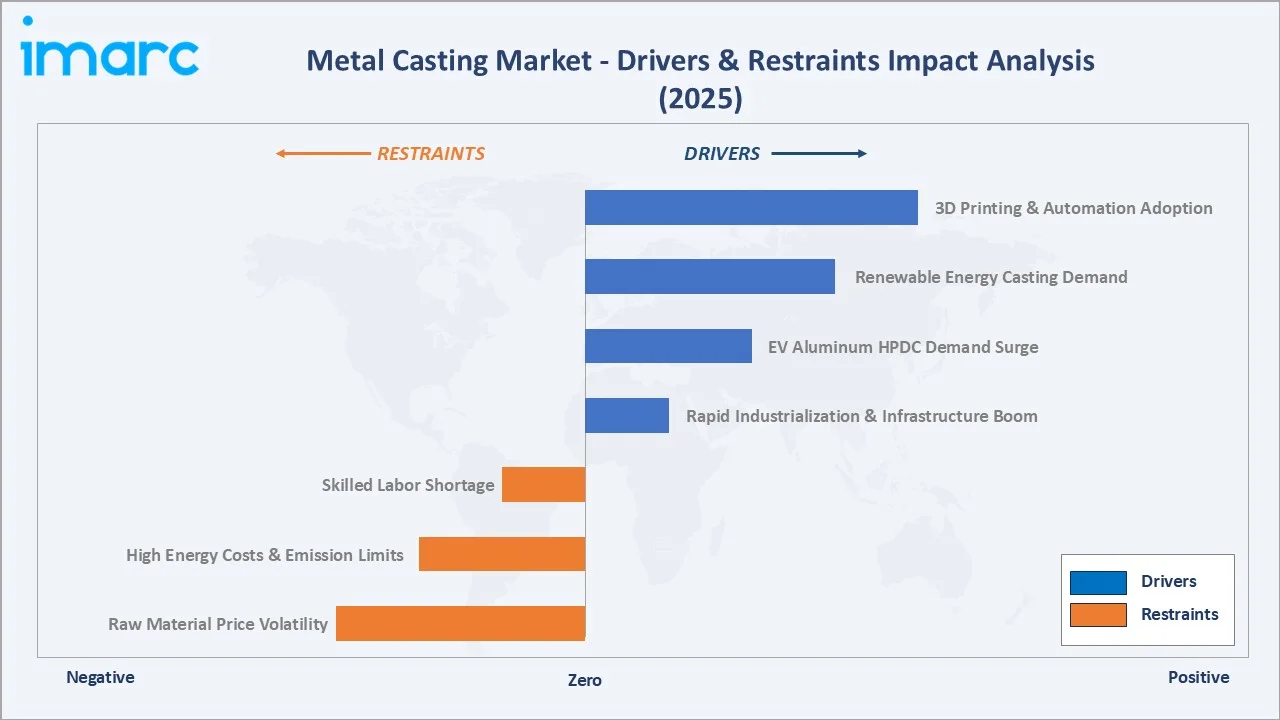

Market Drivers

- Accelerating Global Industrialization and Infrastructure Investment: Global energy investment exceeded USD 3 trillion in 2024, with USD 2 trillion going to clean energy technologies and infrastructure. This global infrastructure investment, with water infrastructure, transportation, and energy systems collectively representing the largest demand pools for metal castings.

- EV Revolution Driving Aluminum Casting Demand: The global electric car sales reached 14 Million units in 2023, with each EV requiring 30–70% more aluminum casting content than equivalent ICE vehicles.

- Renewable Energy Infrastructure Requiring Specialty Castings: The global wind power market installed 116 GW of new capacity in 2023, with each onshore turbine nacelle and hub containing 8–15 metric tons of ductile iron casting.

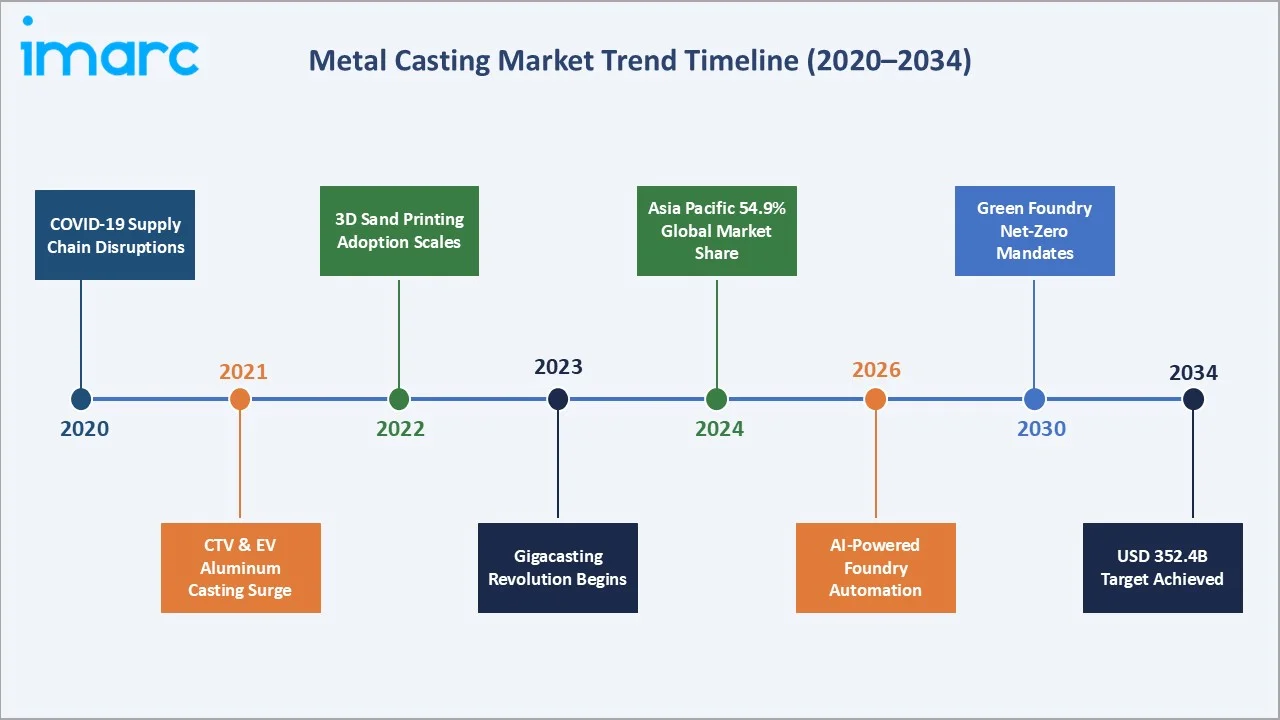

- Technological Advancement Enhancing Casting Quality and Efficiency: 3D sand printing, using binder-jetting to produce complex sand molds directly from digital files without pattern tooling, reduces mold lead time from 8–16 weeks to 2–5 days for complex one-off or short-run castings.

Market Restraints

- High Energy Costs and Raw Material Price Volatility: Metal casting is an energy-intensive manufacturing process, with iron foundries consuming 500–1,200 kWh per metric ton of castings produced, directly impacting foundry input costs and margin predictability.

- Stringent Environmental Regulations Increasing Compliance Investment: Iron foundries generate silica dust, heavy metal particulates, volatile organic compounds (VOCs), and significant CO2 emissions, making them among the most regulated manufacturing operations globally.

- Skilled Labor Shortage in Advanced Casting Technologies: The foundry industry globally faces a critical skills shortage in metallurgists, pattern makers, mold designers, and automation engineers.

Market Opportunities

- Aerospace and Defense Casting Demand Surge: Each commercial aircraft contains USD 500,000–2,000,000 in casting content (superalloy turbine blades, titanium structural castings, aluminum engine nacelles), creating a 10+ year structural demand backlog for precision aerospace foundries.

- Additive Manufacturing Hybrid Processes and Tooling Disruption: The combination of 3D printed sand molds with conventional metal pouring is enabling previously impossible casting geometries at competitive unit costs for medium-volume production.

Market Challenges

- Gigacasting Consolidation Threatening Tier-2 Foundry Volumes: Gigacasting reduces vehicle production time by up to 30%, hampering the market growth

- Decarbonization Pressure on Iron Foundry Business Model: Iron casting production is carbon-intensive, with coke-fired cupola furnaces generating high tons of CO2 per metric ton of castings, creating long-term regulatory and customer pressure.

Emerging Market Trends

1. Gigacasting Revolutionizing Automotive Structural Manufacturing

Drone footage from the site indicates that Tesla’s Fremont Giga Press machines currently operate at a cycle time of around 170 seconds per casting, likely because they have not yet reached full optimization. In comparison, IDRA estimates an ideal cycle time of approximately 80–90 seconds, suggesting there is significant room for Tesla to improve efficiency at its Fremont facility.

2. Digital Foundry and AI-Powered Process Control

Industry 4.0 adoption in foundries, encompassing real-time melt quality sensors, AI-powered solidification simulation, and automated pouring systems, is reducing scrap rates and improving dimensional consistency for critical aerospace applications.

3. Sustainable and Green Casting Technologies

European foundries are leading the transition to electric induction melting, binder-free sand reclamation, and low-emission core manufacturing driven by EU IED regulations and OEM Scope 3 requirements.

4. Aluminum Intensification in Automotive Platforms

A study commissioned by European Aluminium and carried out by Ducker Carlisle reveals that the average aluminium content in European vehicles rose by 18%, increasing from 174 kg in 2019 to 205 kg in 2022. The report also forecasts continued growth, with aluminium usage expected to reach 237 kg per vehicle by 2026 (up 15.6%) and 256 kg by 2030 (a 24.9% increase), demonstrating the commercial viability of premium structural casting at automotive production volumes.

5. Emerging Market Foundry Modernization

India, Southeast Asia, and Latin America are experiencing rapid foundry modernization driven by OEM localization mandates, PLI production incentive schemes, and increasing export opportunities.

Industry Value Chain Analysis

The metal casting value chain creates highest margin at the specialty precision casting and pattern design stages, where aerospace superalloy investment casters achieve EBIT margins of 20–30% versus 5–10% for commodity iron foundries competing in infrastructure pipe markets.

|

Stage |

Key Players & Examples |

|

Raw Materials |

Iron ore, pig iron, aluminum ingot, zinc, scrap metal, foundry sand |

|

Casting Process |

Iron sand casting, ductile iron automotive, aluminum die casting, aluminum rolling and casting |

|

Finishing & Quality Control |

Machining, Heat treatment, Inspection, Coating |

|

Distribution & Logistics |

OEM direct supply, Tier-1 automotive, industrial distributors, project-specific delivery for infrastructure |

Precision aerospace investment casting, producing nickel superalloy turbine blades and vanes for jet engines, captures high finished casting value. This 4,000–8,000x value range across the casting industry creates a bifurcated competitive landscape where capital intensity, metallurgical expertise, and process certification requirements segment the market into distinct competitive tiers.

Technology Landscape in the Metal Casting Industry

High-Pressure Die Casting (HPDC) and Gigacasting

HPDC has undergone a step-change evolution with the introduction of large-scale structural casting. Traditional HPDC operated at 400–2,500-tonne clamping force for small-to-medium automotive components; Gigacasting operates at 6,000-9,000 tonnes for integrated structural castings up to 1.8m x 1.5m footprint.

3D Sand Printing and Additive Mold Making

Binder-jetting 3D sand printers deposit furan or phenolic binder onto silica or ceramic sand layers at 200–500 μm resolution, producing mold cavities for casting without pattern tooling. Complex internal cooling channels, draft-free cavities, and undercuts, impossible in conventional sand casting without complex core assembly, are achieved in single-piece printed molds. Hybrid processes combining 3D-printed cores with automated green sand molding machines are enabling rapid-iteration prototype casting alongside high-volume series production in the same foundry.

Real-Time Process Monitoring and AI Defect Detection

Thermal imaging cameras monitoring molten metal temperature during pouring, X-ray computed tomography for 100% internal defect inspection, and eddy-current testing for surface crack detection are collectively enabling statistical process control (SPC) in real-time.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Process | Sand Casting | 45.6% | 2025 |

| Material Type | Cast Iron | 55.2% | 2025 |

| End Use | Automotive and Transportation | 51.5% | 2025 |

| Components | Alloy Wheels | 12.12% | 2025 |

| Vehicle Type | Passenger Cars | 53.1% | 2025 |

| Electric and Hybrid Type | Hybrid Electric Vehicles | 90.1% | 2025 |

| Application | Body Assemblies | 28.5% | 2025 |

| Region | Asia-Pacific | 54.9% | 2025 |

By Process

Sand casting commands 45.6% in 2025, maintaining its position as the most widely used casting process due to its cost-effectiveness, material flexibility, and ability to produce components. Over 60% of all metal castings are produced by the sand casting process.

To access detailed market analysis, Request Sample

High-pressure die casting (HPDC) at 22.3% (2025) growing at ~8.4% CAGR is the most dynamic process segment. Gravity casting at 18.4% serves permanent mold aluminum and copper alloy applications including automotive cylinder heads, wheels, and decorative hardware where surface finish and dimensional consistency are critical. Low-pressure die casting at 8.6% bridges the gap between gravity and HPDC for medium-complexity aluminum automotive and structural components including alloy wheels, cylinder blocks, and battery module housings.

By Material Type

Cast iron retains 55.2% material share in 2025, sustained by its irreplaceable functional properties across infrastructure, heavy industry, and traditional automotive drivetrain applications. Ductile (nodular) iron, with tensile strength of 400–900 MPa and excellent fatigue resistance, is the dominant cast iron grade for automotive crankshafts, differential housings, wind turbine hubs, and industrial gear housings.

Aluminum at 22.4% growing fastest at ~8.1% CAGR is the transformative material category driven by EV adoption. Steel casting at 12.6% serves mining, construction equipment, and railway applications where high strength and impact resistance are required. Zinc at 6.3% serves consumer electronics, hardware, and small precision component applications through HPDC processes achieving wall thicknesses below 0.5mm. Magnesium at 2.4% is growing in automotive and electronics where its density advantage justifies its 2–3x premium over aluminum per kilogram.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

Asia Pacific |

54.9% |

China 51.4M MT annual output, PLI automotive scheme, Belt & Road infra investment, EV casting demand |

|

North America |

18.4% |

US defense casting authorization, aerospace backlog 14,000+ aircraft, GM/Ford Gigacasting adoption |

|

Europe |

16.3% |

Airbus delivery target, EU Green Deal, BMW/VW aluminum casting shift, Georg Fischer sustainability leadership |

|

Middle East & Africa |

6.2% |

Saudi Vision 2030, UAE construction boom, Africa infrastructure gap, petrochemical equipment castings demand |

|

Latin America |

4.2% |

Mexico nearshoring investment, Brazil automotive casting, mining equipment castings Chile/Peru |

Asia Pacific’s dominant 54.9% regional share in 2025 is structurally anchored by China’s foundry industry growth, representing global casting output volume. China’s automotive industry, produced 12.4 million electric cars in 2024, is the largest single demand source for aluminum HPDC castings globally. India’s casting industry growth, with the PLI automotive scheme.

North America (18.4%, 2025) is experiencing a casting demand renaissance driven by US manufacturing reshoring, defense spending, and the infrastructure investment super-cycle. Europe (16.3%) is navigating the dual challenge of energy cost pressure and EV transition, with aluminum HPDC investment accelerating while traditional iron foundries face structural volume decline as ICE vehicle production falls toward 2035 European ICE sales ban targets.

Competitive Landscape

|

Company Name |

Key Brand / Segment |

Market Position |

Core Strength |

|

Precision Castparts Corp. |

PCC Structurals, PCC Airfoils |

Leader |

One of the largest aerospace casting companies |

|

Alcoa Corporation |

Aluminum Castings |

Leader |

Vertically integrated bauxite-alumina-aluminum, sustainability-linked aluminum |

|

Nemak |

HPDC (High Pressure Die Casting), LPDC (Low Pressure Die Casting), GSPM (Gravity in Semi-Permanent Mould), Rotacast, CPS (Core Package System), ductile iron sand casting |

Leader |

Largest independent automotive aluminum caster |

|

Waupaca Foundry Inc.(a Monomoy Capital Partners company) |

Iron Castings |

Leader |

Largest iron foundry, gray & ductile iron |

|

Ryobi Ltd. |

Aluminum Die Casting |

Challenger |

Japan & North America HPDC, thin-wall aluminum structural capability |

|

Endurance Technologies Ltd. |

Aluminum Die Casting |

Emerging |

India & Europe two-wheeler & passenger car HPDC |

The global metal casting market is highly fragmented. However, concentration is significantly higher in specific sub-segments: aerospace investment casting, automotive aluminum HPDC, and iron pipe casting.

Key Company Profiles

Precision Castparts Corp.

Precision Castparts Corp., a wholly-owned subsidiary of Berkshire Hathaway Inc., is the world’s largest manufacturer of complex metal components and products for the aerospace, power generation, and industrial markets.

- Product Portfolio: PCC Structurals, PCC Airfoils.

- Recent Developments: PCC accelerated production capacity expansion in response to commercial aerospace delivery backlogs.

- Strategic Focus: PCC’s strategy concentrates exclusively on high-complexity, high-value casting and forging where regulatory qualification requirements, proprietary metallurgical processes, and sole-source customer relationships create durable competitive barriers.

Nemak

Nemak is the world’s largest independent manufacturer of aluminum components for the automotive industry. Nemak acquired GF Casting Solutions’ Automotive Business, further strengthening its position as a global leader in lightweight automotive components and mobility solutions.

- Product Portfolio: HPDC (High Pressure Die Casting), LPDC (Low Pressure Die Casting), GSPM (Gravity in Semi-Permanent Mould), Rotacast, CPS (Core Package System), ductile iron sand casting

- Recent Developments: In February 2026, Nemak completed the acquisition of the automotive business of GF Casting Solutions for US$336 million, pioneering a major step in its global expansion and shift toward sustainable mobility solutions.

- Strategic Focus: Nemak’s strategic transformation centers on transitioning its revenue mix from traditional ICE powertrain castings to EV structural and e-mobility casting.

Alcoa Corporation

Alcoa Corporation is one of the world’s largest aluminum producers, operating across bauxite mining, alumina refining, aluminum smelting, and casting.

- Product Portfolio: Aluminum Castings

- Recent Developments: In October 2025, Alcoa secured its fourth consecutive award for innovation in megacasting. The honor highlights the C891F EZCastPlus alloy, which was used in an advanced integrated front cabin triangular beam casting for the Xiaomi YU7 electric SUV.

- Strategic Focus: Alcoa’s casting strategy focuses on the premium end of the aluminum value chain, aerospace-grade high-strength alloys, sustainable EcoLum certification for ESG-driven automotive customers, and advanced alloy innovation through the ELYSIS and Airware programs, rather than competing in commodity casting markets where Asian producers maintain decisive cost advantages.

Waupaca Foundry Inc.

Waupaca Foundry Inc., owned by Monomoy Capital Partners, is one of the largest iron foundry companies in North America, producing gray and ductile iron castings.

- Product Portfolio: Iron Castings

- Recent Developments: In October 2025, Waupaca Foundry started the final stage of a multiyear, $100 million-plus capital investment program to modernize operations, enhance worker safety and provide advanced foundry technology to meet the needs of its customers.

- Strategic Focus: Waupaca’s strategy emphasizes scale efficiency in high-volume gray and ductile iron casting for automotive and agricultural markets, continuous automation investment to offset US labor cost disadvantages versus Asian competitors, and selective diversification into ductile iron castings for EV truck platforms where iron still plays roles in differential housings and structural components despite the EV powertrain transition.

Market Concentration Analysis

The global metal casting market is highly fragmented at the aggregate level. The top 5 players account for only 20–30% of total market revenue in 2025, a fragmentation level reflecting the industry’s structure as thousands of small and mid-size foundries serving regional markets with commodity sand and iron castings. However, concentration is significantly higher in premium sub-segments: aerospace investment casting, automotive aluminum HPDC, and iron pipe casting.

Consolidation is accelerating in three specific market segments. EV structural casting is consolidating around Gigacasting-capable HPDC specialists as OEMs reduce supplier counts from 20+ to 2–3 key casting partners for integrated underbody systems. Aerospace investment casting is re-consolidating. European iron foundry consolidation, driven by energy cost pressure and volume decline from EV transition, is expected to reduce European iron foundry count through closures and M&A.

Investment & Growth Opportunities

Fastest-Growing Segments

High-pressure die casting at ~8.4% CAGR is the highest-growth process segment, driven by Gigacasting adoption and EV structural casting. Investment in 6,000–9,000-tonne HPDC machine capability, including tooling, robotic handling, and thermal management, represents the single highest-return capital deployment in the metal casting industry, with estimated ROI periods of 3–5 years for EV platform programs with 8–10 year volume commitments. Aluminum material at ~8.1% CAGR is the fastest-growing material category, with EV battery housing casting growing within the aluminum segment.

Emerging Markets

India is the most attractive emerging market investment destination for metal casting. India’s PLI Automobile scheme, National Infrastructure Pipeline, and Make in India defense manufacturing mandate collectively create a government-backed demand environment growing at 8–10% CAGR. Southeast Asia, Vietnam, Thailand, and Indonesia, is attracting casting investment from Chinese foundries seeking production diversification amid US-China trade tensions, with Vietnam’s casting export value growing 25–35% annually in 2023–2024. Mexico’s nearshoring boom is creating greenfield aluminum die casting investment opportunities in Nuevo León and Guanajuato close to relocated US automotive assembly plants.

Venture and Investment Trends

3D sand printing and additive mold making startups are attracting investments in venture and strategic investment annually, leading capital raises for large-format and ceramic additive casting mold platforms. Green foundry technology, electric induction melting, hydrogen-based iron reduction, and CO2-capture cupola systems are attracting EU green transition funding committed across member states. Private equity firms are actively building foundry roll-up platforms, targeting 8–12x EBITDA acquisition multiples for specialty precision casting businesses with long-term OEM contracts.

Future Market Outlook (2026-2034)

The global metal casting market is positioned for sustained structural growth through 2034, underpinned by the irreplaceable role of casting as the primary manufacturing process for complex metal components across transportation, energy, and industrial sectors. From USD 190.5 Billion in 2025, the market is forecast to reach USD 263.7 Billion by 2030 and USD 352.4 Billion by 2034, representing USD 161.9 Billion in absolute incremental value creation over the nine-year forecast horizon at a consistent 6.70% CAGR.

Technological disruptions expected between 2026 and 2034 include the full commercial adoption of Gigacasting, AI-autonomous foundries operating 20–24 hours with minimal human intervention, and the first commercial-scale zero-carbon iron production using hydrogen-based direct reduction by 2030–2032. These disruptions will simultaneously create growth opportunities (Gigacasting machine investment, green foundry capital expenditure) and destroy value for traditional iron foundries unable to adapt to EV powertrain substitution and increasingly stringent carbon compliance requirements.

Research Methodology

Primary Research

Primary research encompassed over 65 structured interviews in 2024–2025 with metal casting market participants including plant directors and VP-level executives, automotive OEM sourcing managers, aerospace casting engineers, industrial equipment buyers, renewable energy procurement managers specifying ductile iron wind turbine castings; and regional foundry association representatives from the American Foundry Society (AFS), European Association of Foundry Industry (CAEF), and Institute of Indian Foundrymen (IIF).

Secondary Research

Key secondary sources include Chinese Casting Association Annual Report, World Steel Association Short Range Outlook, International Aluminum Institute Automotive Aluminum Report, GWEC Global Wind Report, IEA Net Zero 2050 renewable capacity forecast, American Foundry Society State of the Foundry Industry Survey, European Association of Foundry Industry Production Statistics, and trade journals Foundry Management & Technology, Modern Casting, and Giesserei.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied in parallel. Bottom-Up aggregates casting demand by process category across material type in each regional market, cross-validated against end-use application demand. Top-Down calibrates against global manufacturing output, automotive production forecasts, and wind energy installation roadmaps.

Metal Casting Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Processes Covered | Sand Casting. Gravity Casting, High-Pressure Die Casting (HPDC), Low-Pressure Die Casting (LPDC), Others |

| Material Types Covered | Cast Iron, Aluminum, Steel, Zinc, Magnesium, Others |

| End Uses Covered | Automotive and Transportation, Equipment and Machine, Building and Construction, Aerospace and Military, Others |

| Components Covered | Alloy Wheel, Clutch Casing, Cylinder Head, Cross Car Beam, Crank Case, Battery Housing, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Electric and Hybrid Types Covered | Hybrid Electric Vehicles (HEV), Battery Electric Vehicles (BEV), Plug-In Hybrid Electric Vehicles (PHEV) |

| Applications Covered | Body Assemblies, Engine Parts, Transmission Parts, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Precision Castparts Corp., Alcoa Corporation, Nemak, Waupaca Foundry Inc.(a Monomoy Capital Partners company), Ryobi Ltd., Endurance Technologies Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the metal casting market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global metal casting market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the metal casting industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Metal Casting Market Report

The global metal casting market reached USD 190.5 Billion in 2025, growing from USD 137.6 Billion in 2020. Growth is driven by industrialization, EV aluminum casting demand, and infrastructure investment globally.

The market is projected to reach USD 352.4 Billion by 2034 at a CAGR of 6.70%, passing through USD 263.7 Billion in 2030. EV-driven aluminum HPDC growth and Asia Pacific industrialization are key forecast drivers.

Sand casting leads at 45.6% in 2025, valued for versatility and cost-effectiveness in large, complex iron and steel components. High-pressure die casting is fastest-growing at ~8.4% CAGR due to EV aluminum structural casting adoption.

Cast iron dominates at 55.2% in 2025 for infrastructure, engine blocks, and heavy industrial applications. Aluminum is fastest-growing at ~8.1% CAGR, driven by EV battery housings, motor casings, and Gigacasting structural components.

Asia Pacific leads at 54.9% in 2025, with China and India foundries producing, driven by the automotive PLI scheme and infrastructure.

Asia Pacific at 54.9% (2025) is also growing fastest at ~7.9% CAGR, driven by China EV adoption, India PLI automotive scheme, and Southeast Asia nearshoring investment.

Key players include Precision Castparts Corp., Alcoa Corporation, Nemak, Waupaca Foundry Inc.(a Monomoy Capital Partners company), Ryobi Ltd., and Endurance Technologies Ltd.

Gigacasting uses 6,000-9,000 tonne HPDC machines to produce single-piece vehicle underbody castings replacing 70+ components. Pioneered by Tesla and adopted by Volvo and NIO, it drives HPDC market growth and consolidates casting supplier counts.

EV adoption increases aluminum casting demand by 30-70% per vehicle versus ICE vehicles. Battery housing, motor casings, and structural castings are growing 18-22% annually. Tesla Gigacasting alone consolidates 40-70 separate castings into single large HPDC components.

Key challenges include energy cost volatility, EU IED emission regulations, US foundry worker shortfall, and EV Gigacasting consolidating supplier volumes.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)