Metal Furniture Market Size, Share, Trends and Forecast by Type, Distribution Channel, Application, and Region, 2026-2034

Metal Furniture Market Size and Share:

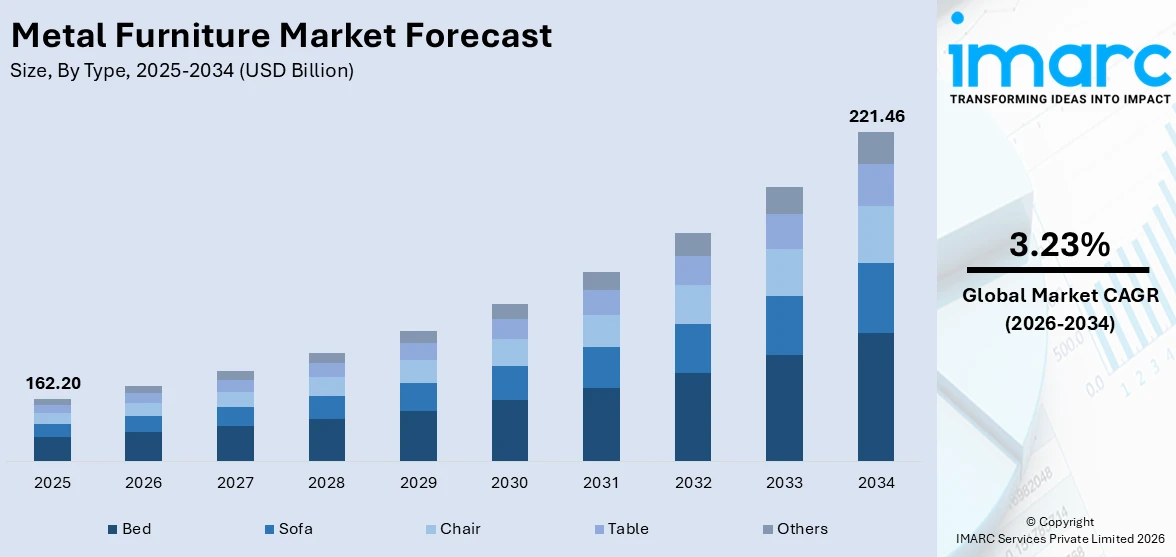

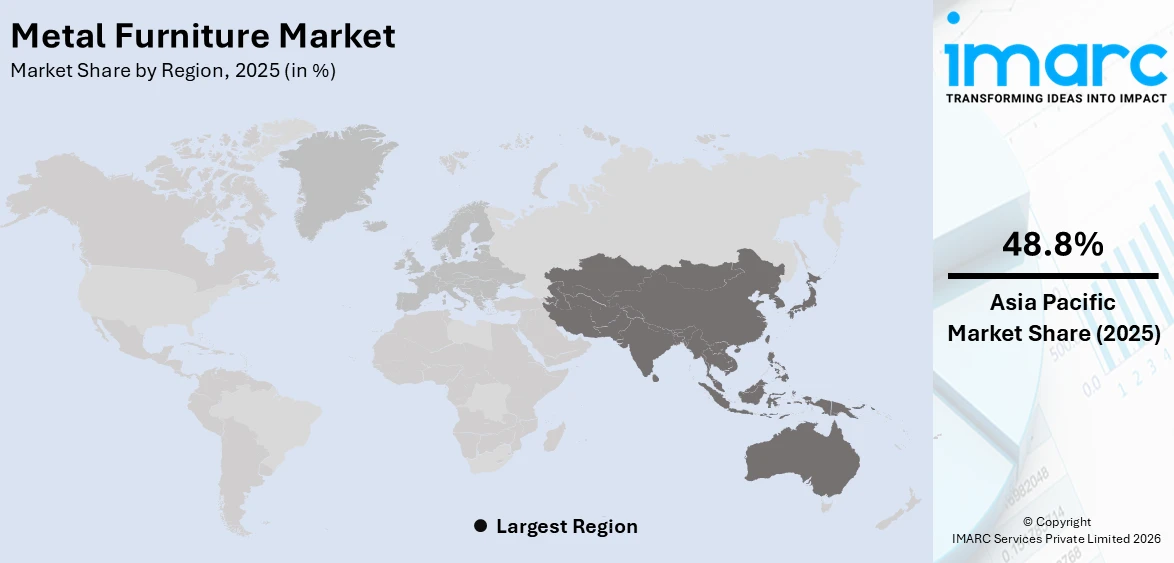

The global metal furniture market size was valued at USD 162.20 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 221.46 Billion by 2034, exhibiting a CAGR of 3.23% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 48.8% in 2025. The region's robust manufacturing base, expansive construction activity, and rapidly growing urban middle class continue to drive demand for diverse metal furniture products across residential and commercial applications, strengthening the overall metal furniture market share.

The metal furniture market growth is propelled by a range of interrelated drivers operating at the global level. Rapid urbanization is expanding the consumer base for metal furniture, as growing urban populations seek durable, affordable, and space-efficient furnishing solutions. Rising commercial construction activities, including the development of office complexes, hospitality establishments, educational institutions, and healthcare facilities, are generating strong demand for robust metal furniture suited to high-traffic environments. The increasing adoption of modular and customizable furniture systems in workplace design further amplifies this demand. Manufacturers are able to provide more design options at reasonable prices thanks to developments in metal fabrication technology, such as laser cutting, powder coating, and cold-rolling procedures.

Growing environmental awareness is also driving interest in metal furniture owing to its recyclability and long product lifespan, which align with increasingly stringent sustainability mandates and green building standards worldwide.

The United States has become an important market in the metal furniture market due to various reasons. The country has a high home improvement and home renovation culture, which has led to steady consumer spending on home furniture. The country has a high demand for long-lasting home furniture made from metals. The country has a well-developed retail infrastructure in place, which has led to steady and high home furniture consumption per capita. The country is witnessing an increased trend towards home office space, which has led to an increased demand for home office furniture such as desks and storage units made from metals.

To get more information on this market Request Sample

Metal Furniture Market Trends:

Rising Preference for Premium Metal Products

The rising consumer interest in premium and design-focused home decor items is resulting in significant changes in the metal furniture market. The rising incomes in both developed and emerging countries are creating a new wave of consumers who are increasingly looking for metal furniture items that not only provide strength and longevity but are also design-focused and offer a high level of aesthetic appeal. Customization is another area that is gaining significant attention in the metal furniture market, with the option of powder coating in a variety of colors and the use of hand-forged techniques and the integration of materials with other materials like wood and upholstery being major draw factors for high-end consumers in the residential and hospitality sectors. The impact of the rise of social media platforms is another significant factor that is creating a buzz in the metal furniture market.

Expansion of Global Trade and E-Commerce Channels

Cross-border trade and the proliferation of e-commerce platforms are fundamentally reshaping how metal furniture reaches end consumers globally. Online marketplaces have dramatically lowered entry barriers for manufacturers, enabling even small and mid-sized producers to access international customers without extensive physical retail networks. This democratization of global distribution has intensified competition while simultaneously broadening consumer choice. The metal furniture market trends indicate that digitally native furniture brands, those building their entire business models around e-commerce, influencer marketing, and data-driven inventory management, are gaining share at the expense of legacy physical retailers. At the same time, traditional manufacturers are investing in digital storefronts, augmented reality product visualization tools, and faster last-mile logistics to remain competitive.

Infrastructure Development Driving Commercial Demand

Large-scale infrastructure development projects, particularly the construction of office towers, government buildings, transportation hubs, educational institutions, and healthcare facilities, are serving as key demand drivers for the metal furniture industry. As urbanization accelerates across emerging economies, governments are investing heavily in public infrastructure, creating substantial procurement opportunities for durable and cost-effective metal furniture solutions. Public sector agencies, hospitality chains, and large institutional buyers typically prefer metal furniture for high-traffic commercial environments due to its resilience, low maintenance requirements, and widespread compliance with fire safety and building regulations. The metal furniture market forecast points to sustained demand from commercial buyers as construction pipelines in Asia, the Middle East, and Africa remain active.

Metal Furniture Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global metal furniture market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, distribution channel, and application.

Analysis by Type:

- Bed

- Sofa

- Chair

- Table

- Others

Bed holds 34.3% of the market share. Metal beds constitute the most popular form of metal furniture in the global marketplace due to their structural integrity, pest resistance to termites, and durability when compared to wooden beds. Metal beds are the most preferred form of beds for both residential and commercial applications such as hotels, dormitories, hospitals, and armed forces' accommodations. Metal beds come in a variety of styles that range from simple powder-coated beds to ornate wrought iron beds to satisfy different design requirements. Metal beds' compatibility with different mattresses and easy assembly add to their overall appeal. In the residential sector, the growing demand for low-maintenance long-life beds is contributing to the overall demand for metal beds. Additionally, the rise of compact living spaces in urban environments has spurred interest in functional metal bed designs that incorporate storage compartments and modular configurations, expanding the product's utility and driving consistent sales across global markets.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Direct Distribution

- Specialty Stores

- Online Stores

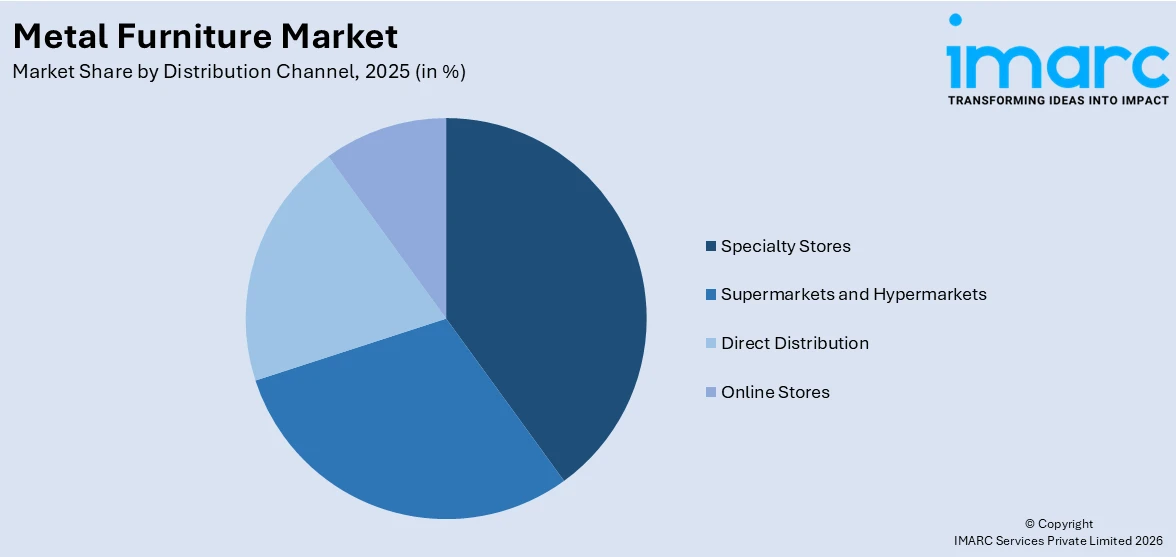

Specialty stores lead the market with a share of 38.5%. Specialty furniture retailers occupy the leading position in the metal furniture distribution landscape owing to their ability to offer curated product selections, expert consultation, and immersive showroom experiences that online channels cannot fully replicate. These stores attract quality-conscious buyers who prefer to physically assess furniture before purchase, particularly for high-involvement decisions such as bedroom sets, dining tables, and accent pieces. By focusing primarily on furniture and home décor categories, specialty retailers can invest in knowledgeable staff, flexible financing, and comprehensive after-sales services including assembly and delivery. This retail experience drives stronger customer loyalty and higher average order values compared to mass merchandise formats. Specialty stores also benefit from their ability to showcase the craftsmanship and finishing quality of metal products, which is a key purchase criterion for premium segment consumers. Their positioning in prime retail locations and shopping districts further supports consistent foot traffic and sustained demand among both residential and commercial buyers.

Analysis by Application:

- Commercial

- Residential

Commercial dominates the market, with a share of 66.7%. The commercial segment encompasses a wide range of end-user environments including office spaces, hotels, restaurants, hospitals, educational institutions, and government facilities, all of which demand metal furniture for its unmatched durability, hygiene compliance, and resistance to heavy usage. Metal furniture is the preferred choice in these settings due to its ability to withstand the rigors of constant use, ease of maintenance, and compatibility with fire safety standards and health regulations. Bulk procurement by institutional buyers, including hotel chains, corporate real estate developers, and hospital management groups, contributes significantly to this segment's dominant position. Furthermore, the rapid global expansion of the hospitality sector, coworking office spaces, and large-format educational campuses continues to generate sustained high-volume demand. As businesses increasingly prioritize cost efficiency and lifecycle value in their procurement decisions, metal furniture's combination of low total cost of ownership, standardized sizing, and wide customizability positions the commercial segment for continued dominance across international markets.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 48.8% of the share, holds the leading position in the market. The dominance of the region can be explained by a combination of its large-scale manufacturing capabilities, availability of raw materials on a large scale, and its massive consumer base. The region includes countries like China, India, Japan, South Korea, and Vietnam, among others, which can be considered both manufacturing and consumption bases for metal furniture. China, for instance, has one of the most vertically integrated manufacturing bases for furniture globally, with a strong supplier network, low labor costs, and export-friendly infrastructure. Similarly, India has a strong domestic market due to its ever-expanding middle class in cities, affordable housing initiatives by the government, and a thriving hospitality sector. At the same time, the rapid construction of commercial spaces in Southeast Asian countries like Indonesia, Vietnam, and the Philippines has fueled the need for metal furniture for institutional use. All these factors have cumulatively helped the Asia Pacific region maintain its dominant position.

Key Regional Takeaways:

North America Metal Furniture Market Analysis

North America represents a significant and steadily growing regional market for metal furniture, driven by consistent investments in residential renovation, commercial real estate development, and institutional procurement. The United States and Canada collectively maintain high per-capita furniture expenditure, supported by mature retail infrastructure, high homeownership rates, and a robust corporate real estate market. Growing interest in home improvement and interior redesign has generated strong demand for metal furniture across bedrooms, living rooms, and home office configurations, as consumers gravitate toward durable and low-maintenance alternatives to wood. The commercial segment—encompassing offices, hospitality venues, educational institutions, and healthcare facilities—continues to represent the primary driver of bulk metal furniture procurement in North America. The metal furniture market outlook for the region remains optimistic, supported by sustained investment in property renovation and new construction.

United States Metal Furniture Market Analysis

The United States holds 80.00% of the metal furniture market in North America. The country constitutes the largest single national market for metal furniture within the North American region, supported by robust demand from both residential and commercial end users. A well-established culture of periodic home renovation and interior redesign drives strong replacement demand among homeowners, with metal furniture increasingly favored for its durability, aesthetic versatility, and resistance to pests. The commercial real estate sector—including office parks, hotel chains, educational campuses, and healthcare networks—represents a consistent source of large-volume institutional procurement. Additionally, the growing popularity of outdoor living spaces has driven significant demand for weather-resistant metal patio and garden furniture across American households. The accelerating adoption of hybrid work arrangements has further augmented residential demand for metal office furniture, including desks, storage units, and ergonomic seating.

Europe Metal Furniture Market Analysis

Europe represents a mature but dynamic market for metal furniture, characterized by strong design heritage, stringent sustainability standards, and diversified demand across residential, commercial, and institutional end-use categories. Countries such as Germany, France, the United Kingdom, Italy, and Spain maintain highly developed retail environments and well-established commercial real estate sectors that generate consistent demand for quality metal furnishings. The region's emphasis on circular economy principles and low-carbon procurement is directing institutional buyers toward recyclable and sustainably manufactured furniture, a category in which metal products hold a natural advantage. Europe's substantial renovation activity further supports demand: the European Union's Renovation Wave initiative targets the deep retrofit of 35 million buildings across member states by 2030, encompassing upgrades to both structure and interior fixtures, including furniture replacements. This large-scale program is expected to drive substantial procurement activity for commercial and residential metal furniture across Western and Central Europe throughout the remainder of the decade.

Asia-Pacific Metal Furniture Market Analysis

Asia-Pacific constitutes the largest and most rapidly expanding regional market for metal furniture globally, driven by the convergence of high-volume manufacturing output, expanding domestic consumption, and accelerating commercial construction. China serves as both the world's foremost producer and exporter of metal furniture, supported by an extensive and vertically integrated manufacturing infrastructure. India's residential sector is experiencing robust growth, underpinned by government-backed housing programs: the Pradhan Mantri Awas Yojana-Urban 2.0 scheme, launched in 2024, targets the development of 10 million urban housing units backed by a total government investment of approximately INR 10 Lakh Crore, generating substantial downstream demand for household furnishings including metal furniture. Japan, South Korea, and Australia represent premium end-markets where design quality and sustainability credentials are key purchasing criteria, supporting higher-value metal furniture products and reinforcing the region's position as the global market leader.

Latin America Metal Furniture Market Analysis

Latin America represents an emerging but steadily expanding market for metal furniture, propelled by ongoing urbanization, rising incomes, and increasing commercial construction across key economies. Brazil and Mexico serve as the region's primary consumption markets, driven by large and growing urban populations and expanding hospitality and retail sectors. The region's rapid transition toward urban living has generated significant demand for affordable, durable, and space-efficient metal furniture across both residential and commercial applications. A thriving hospitality sector, particularly in coastal tourism destinations, further amplifies procurement of outdoor and contract-grade metal furniture. Government investments in social housing and urban infrastructure continue to support broader market expansion, creating consistent downstream demand across the region.

Middle East and Africa Metal Furniture Market Analysis

The Middle East and Africa region is an increasingly attractive growth market for metal furniture, fueled by extensive government-backed construction programs, rapid urban development, and a thriving hospitality sector. The Gulf Cooperation Council countries are driving particularly strong demand, with major urban planning and infrastructure projects generating bulk procurement requirements for commercial and institutional metal furniture. The MENA Construction Monitor reported that the MENA region awarded construction projects during the first half of 2025, reflecting the scale of infrastructure activity that drives downstream demand for durable furnishing solutions across offices, hotels, and public facilities throughout the region.

Competitive Landscape:

The competitive landscape of the international market for metal furniture is found to be highly fragmented, with a wide range of multinational conglomerates, regional manufacturers, and design-focused companies competing in terms of pricing, quality, aesthetics, and environmental considerations. The competitive landscape is becoming increasingly influenced by digital transformation, as firms continue to invest in digital infrastructure, augmented reality-based product visualization, and B2B digital procurement solutions to reach a wider customer base. Environmental considerations have become an important differentiator in recent times, as multinational firms in the industry continue to use recycled materials, low-VOC powder coatings, and sustainable design approaches in their products to capitalize on the institutional sector’s increasing demand for sustainable procurement. At the same time, there is an increasing use of automation technologies in metal fabrication, including CNC machining, robotic welding, and laser cutting, to improve quality, as well as efficiently manage production costs.

The report provides a comprehensive analysis of the competitive landscape in the metal furniture market with detailed profiles of all major companies, including:

- Chyuan Chern Co., Ltd.

- Godrej Interio

- HH2 Home

- Inter IKEA Systems B.V.

- Lehni AG

- Oliver Metal Furniture

- Simpli Home

- Steelcase Inc.

- Williams-Sonoma Inc.

Metal Furniture Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment

|

| Types Covered | Bed, Sofa, Chair, Table, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Direct Distribution, Specialty Stores, Online Stores |

| Applications Covered | Commercial, Residential |

| Regions Covered | Asia-Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia; Brazil, Mexico |

| Companies Covered | Chyuan Chern Co., Ltd., Godrej Interio, HH2 Home, Inter IKEA Systems B.V., Lehni AG, Oliver Metal Furniture, Simpli Home, Steelcase Inc., Williams-Sonoma Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the metal furniture market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global metal furniture market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the metal furniture industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Metal Furniture Market Report

The metal furniture market was valued at USD 162.20 Billion in 2025.

The metal furniture market is projected to exhibit a CAGR of 3.23% during 2026-2034, reaching a value of USD 221.46 Billion by 2034.

The metal furniture market is driven by rapid urbanization and expanding commercial construction, which generate sustained demand for durable institutional furnishings. Growing consumer preference for low-maintenance, long-lasting residential furniture, advancements in metal fabrication technologies offering greater design variety, and increasing adoption of e-commerce distribution channels that broaden global market access are among the key factors propelling market expansion.

Asia-Pacific currently dominates the metal furniture market, accounting for a share of 48.8%. The region benefits from a large-scale, highly integrated manufacturing ecosystem, favorable raw material availability, rapidly expanding urban populations, and robust commercial construction activity, all of which sustain strong domestic production and growing export demand for metal furniture products.

Some of the major players in the metal furniture market include Chyuan Chern Co., Ltd., Godrej Interio, HH2 Home, Inter IKEA Systems B.V., Lehni AG, Oliver Metal Furniture, Simpli Home, Steelcase Inc., Williams-Sonoma Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)