Mexico Activewear Market Size, Share, Trends and Forecast by Product Type, Material Type, Pricing, Age Group, Distribution Channel, End User, and Region, 2026-2034

Mexico Activewear Market Size, Share, Trends & Forecast (2026-2034)

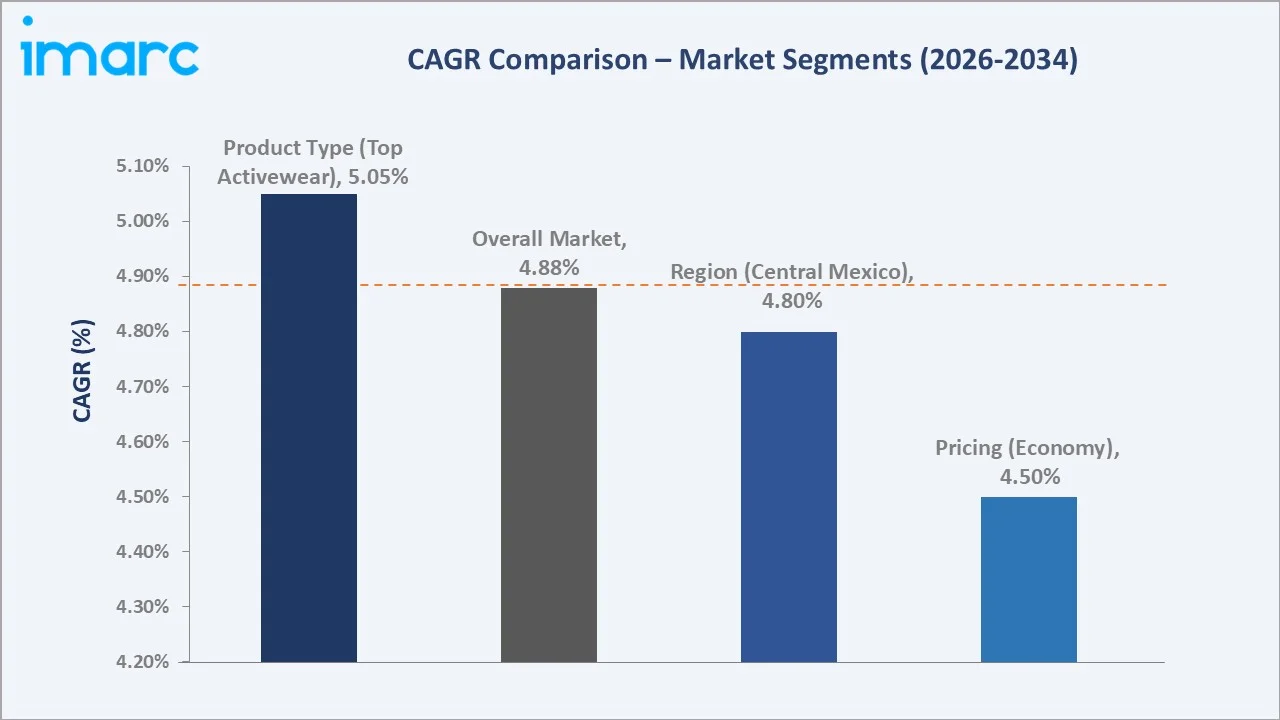

The Mexico activewear market was valued at USD 6.53 Billion in 2025 and is projected to reach USD 10.15 Billion by 2034, exhibiting a CAGR of 4.88% during 2026-2034. Rising health and fitness awareness, the mainstreaming of athleisure, fast-growing e-commerce, expanding female sports participation, and demand for performance and sustainable fabrics are the primary drivers shaping market growth.

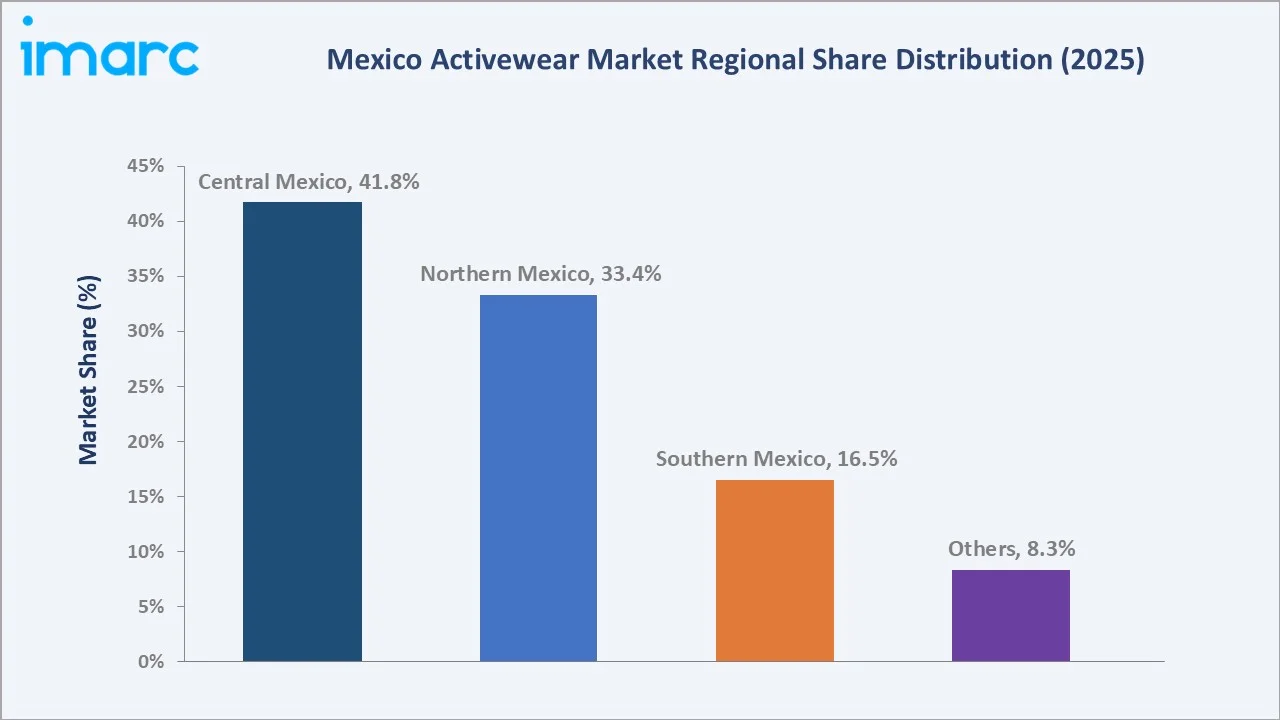

Top activewear leads the product type segment at 31.6%, economy dominates pricing at 63.5%, and Central Mexico commands 41.8% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.53 Billion |

|

Forecast Market Size (2034) |

USD 10.15 Billion |

|

CAGR (2026-2034) |

4.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Central Mexico (41.8%, 2025) |

|

Second Largest Region |

Northern Mexico (33.4%, 2025) |

|

Leading Product Type |

Top Activewear (31.6%, 2025) |

|

Leading Pricing |

Economy (63.5%, 2025) |

The Mexico activewear market expanded from USD 5.14 Billion in 2020 to USD 6.53 Billion in 2025, supported by widening fitness culture, the casualization of everyday wardrobes, and rapid growth of online retail across urban centers. Anchored at USD 8.28 Billion in 2030, the forecast to USD 10.15 Billion by 2034 is underpinned by premiumization, expanding women's lines, and deeper omnichannel distribution across the country.

To get more information on this market, Request Sample

CAGR trajectories across product type and pricing sub-segments show premium apparel, swimwear, and outerwear expanding faster than the overall 4.88% market CAGR, driven by premiumization, rising disposable income, and growing demand for specialized performance categories.

Executive Summary

The Mexico activewear market is on a steady growth path, advancing from USD 5.14 Billion in 2020 toward USD 10.15 Billion by 2034. Activewear has shifted from purely athletic use to mainstream daily wear, blending performance, comfort, and style. Rising gym participation, fitness culture, and athleisure adoption are widening the consumer base across age groups.

Top activewear leads the product type segment at 31.6% in 2025, supported by strong demand for t-shirts, tops, and jerseys. Economy dominates pricing at 63.5% on the back of value-driven middle-income buyers. Central Mexico commands 41.8% of regional share, led by high population density and increasing disposable incomes.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Top Activewear - 31.6% share (2025) |

|

Second Largest Product Type |

Bottom Activewear - 26.8% share (2025) |

|

Leading Pricing |

Economy - 63.5% share (2025) |

|

Second Largest Pricing |

Premium - 36.5% share (2025) |

|

Leading Region |

Central Mexico - 41.8% share (2025) |

|

Second Largest Region |

Northern Mexico - 33.4% share (2025) |

|

Top Companies |

Nike, Inc., adidas AG, Puma SE, lululemon athletica, New Balance |

Key Analytical Observations Expanding On The Data Above:

- Top activewear dominance at 31.6% is anchored by everyday demand for t-shirts, tank tops, hoodies, and sports jerseys that bridge gym, lifestyle, and casual use.

- Bottom activewear at 26.8% is sustained by strong sales of leggings, joggers, shorts, and track pants, supported by the athleisure shift toward comfortable, versatile lower-body apparel.

- Economy leadership at 63.5% reflects the price sensitivity of middle-income buyers, who favor accessible, value-driven activewear across mass retail and informal channels.

- Premium at 36.5% is expanding as health-conscious, brand-aware consumers trade up. Rising demand for performance fabrics, innovative product features, and international sportswear brands is supporting growth across the premium activewear segment.

- Central Mexico at 41.8% leads regional demand, anchored by Mexico City and surrounding states, supported by high population density, disposable income, and concentrated retail infrastructure.

Mexico Activewear Market Overview

Activewear refers to apparel designed for sports, exercise, and active lifestyles, spanning tops, bottoms, outerwear, innerwear, and swimwear worn across gym, running, training, outdoor, and everyday casual settings. The market covers performance garments engineered with moisture-wicking, stretch, and breathable fabrics, as well as lifestyle pieces that blend athletic function with fashion.

The market ecosystem integrates fiber and fabric suppliers, textile mills and apparel manufacturers, global and local brands, distributors, specialty and department-store retailers, e-commerce platforms, and end consumers. Regulatory bodies and labeling norms shape product standards, while logistics and marketing partners support delivery.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Health and Fitness Awareness: Growing concern over lifestyle-related conditions is pushing Mexicans toward regular exercise and gym memberships. The OECD Health Statistics published in 2023 indicated that Mexico had the highest prevalence of diabetes among member countries, with the condition affecting 16.9% of the population, accelerating health-driven demand for activewear and performance apparel.

- Athleisure and Casualization of Apparel: The blending of athletic and casual wear has made activewear acceptable for work, travel, and social settings, expanding occasions of use and broadening the addressable consumer base.

- E-commerce and Omnichannel Retail: Rapid growth of online marketplaces and brand websites is widening access to activewear, especially among younger, digitally engaged shoppers in both metro and secondary cities.

- Growing Female Sports Participation: Rising female engagement in fitness, running, and team sports is fueling demand for women's activewear, one of the fastest-growing segments in the market.

Market Restraints

- Price Sensitivity and Economy Skew: A large value-seeking, middle-income base concentrates demand in the economy tier, compressing margins and limiting premium adoption across much of the market.

- Counterfeit and Gray-Market Products: Informal commerce sustains a sizeable counterfeit and gray-market channel that dilutes brand value and undercuts legitimate retailers.

- Import Dependence and Input Costs: Reliance on imported fabrics and finished goods exposes brands to currency volatility and freight costs, pressuring pricing and supply stability.

Market Opportunities

- Premiumization and Women's Activewear: Trading up among health-conscious consumers and rising female participation create room for premium lines, technical fabrics, and specialized fits beyond the economy tier.

- Local Brand Growth and Sustainability: Domestic brands aligning with local preferences, sustainable materials, and competitive pricing can capture share, especially as shoppers increasingly value authenticity and homegrown labels.

Market Challenges

- Intense Global Brand Competition: A crowded field of international and local brands fuels price wars and heavy marketing spend, making it difficult for new entrants to build durable share.

- Uneven Premium Retail Access: Limited premium retail and experiential formats in smaller cities constrain reach for higher-priced lines, slowing premium penetration outside major metros.

Emerging Market Trends

1. Mainstreaming of Athleisure and Studio Culture

Activewear is increasingly worn beyond the gym, blending into daily and workwear wardrobes. Growing consumer preference for versatile, comfortable, and fashion-forward apparel is encouraging brands to introduce multifunctional collections suited for fitness, travel, and everyday wear.

2. E-commerce and Omnichannel Expansion

Online marketplaces, brand-direct stores, and quick-commerce are widening access to activewear. Omnichannel models that integrate physical stores with digital catalogs are improving discovery, fit guidance, and delivery across urban and secondary markets.

3. Sustainability and Performance Fabrics

Demand for recycled, moisture-wicking, and durable performance textiles is rising as consumers weigh both function and environmental impact. Brands are introducing eco-conscious lines and traceable materials to differentiate in a crowded field.

4. Premiumization and Women's Lines

Health-conscious and brand-aware consumers are trading up to premium fits, technical fabrics, and women-specific designs. This shift is broadening assortments beyond the economy tier and supporting higher average selling prices.

Industry Value Chain Analysis

The Mexico activewear value chain spans six stages, from raw materials and manufacturing through distribution, e-commerce, and end use. Brand design, retail, and digital channels capture the highest value-add, while sustainable sourcing and supply reliability increasingly determine competitive position.

|

Stage |

Key Players / Examples |

|

Raw Materials & Fabrics |

Fiber producers, yarn spinners, and technical-textile suppliers providing performance and sustainable materials |

|

Manufacturing & Production |

Textile mills, cut-make-trim units, and apparel manufacturers producing for domestic and export demand |

|

Brand & Product Design |

Global and local activewear brands managing design, branding, and product development |

|

Distribution & Wholesale |

Importers, wholesalers, and distributors supplying specialty, department, and sports retailers |

|

Retail & E-commerce |

Specialty stores, department stores, marketplaces, and brand websites delivering to end users |

|

End Use & Lifecycle |

Consumers, customer support, resale channels, and after-sales services supporting long-term engagement |

Vertically integrated brands that control design, sourcing, and direct-to-consumer channels are positioned to capture greater value than players reliant on third-party manufacturing and distribution.

Technology Landscape in the Mexico Activewear Industry

Performance Fabrics and Material Innovation

Brands are adopting moisture-wicking, four-way-stretch, antimicrobial, and recycled fabrics to improve comfort and sustainability. Material innovation is central to differentiation, enabling lighter, more durable, and climate-adaptive garments for diverse activities.

E-commerce, Personalization, and Data

Digital platforms use data analytics and personalization to recommend products, improve fit guidance, and streamline checkout. Virtual try-on, size advisors, and targeted marketing are enhancing online conversion and reducing returns.

Omnichannel and Supply Chain Digitization

Retailers are integrating inventory, fulfillment, and customer data across stores and online channels. Digital supply chains, demand forecasting, and faster replenishment are improving availability and responsiveness.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Top Activewear |

31.6% |

2025 |

|

Material Type |

🔒 |

🔒 |

2025 |

|

Pricing |

Economy |

63.5% |

2025 |

|

Age Group |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

41.8% |

2025 |

By Product Type

Top activewear commands a 31.6% majority share in 2025, driven by everyday demand for t-shirts, tops, tank tops, hoodies, and sports jerseys that span gym, training, and casual use. The segment benefits from broad appeal across age groups and frequent repeat purchases.

To access detailed market analysis, Request Sample

Bottom activewear at 26.8% in 2025 covers leggings, joggers, shorts, and track pants, supported by the athleisure shift toward versatile lower-body apparel. Strong female demand for leggings and tights reinforces this segment's momentum.

By Pricing

Economy dominates with 63.5% share in 2025, reflecting the price sensitivity of Mexico's middle-income consumers and the strength of value-driven mass and informal retail. The tier remains the default entry point for first-time and budget-conscious buyers.

Premium at 36.5% is expanding as health-conscious, brand-aware consumers trade up to technical fabrics, specialized fits, and global brands. Premiumization is supported by rising disposable income and growing fitness engagement in major cities.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central Mexico |

41.8% |

Dense urban population, high disposable income, concentrated retail infrastructure, and strong fitness and athleisure adoption |

|

Northern Mexico |

33.4% |

Industrial economy, higher purchasing power, proximity to the United States, and growing sports and outdoor participation |

|

Southern Mexico |

16.5% |

Emerging digital adoption, expanding youth engagement, tourism-led demand, and rising tier-2 city participation |

|

Others |

8.3% |

Developing retail access, growing e-commerce penetration, and gradual expansion of fitness culture |

Central Mexico at 41.8% in 2025 leads the regional landscape, anchored by Mexico City and surrounding states. High population density, a large concentration of disposable income, and a mature retail base support sustained leadership across both physical and online channels.

Northern Mexico at 33.4% follows, supported by an industrial economy, higher purchasing power, and strong cross-border retail influence.

Competitive Landscape

The Mexico activewear market is moderately fragmented, with global brands leading on reach, product depth, and marketing scale, while local players compete on price, regional relevance, and cultural branding. Brand strength, distribution, product innovation, and omnichannel capability form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Nike, Inc. |

Nike |

Leader |

Global sportswear leader with performance apparel, footwear, and a growing direct-to-consumer and digital ecosystem |

|

adidas AG |

adidas |

Leader |

Diversified sportswear brand with strong performance and lifestyle ranges and broad retail distribution |

|

Puma SE |

PUMA |

Leader |

Sport-lifestyle brand combining performance categories with fashion-led collaborations and youth marketing |

|

lululemon athletica |

lululemon |

Innovator |

Premium athletic and athleisure brand with a community-led retail model and technical-fabric focus |

|

New Balance |

New Balance |

Challenger |

Performance and lifestyle brand with strong footwear heritage and expanding apparel ranges |

Key players include Nike, Inc., adidas AG, Puma SE, lululemon athletica, and New Balance, among others.

Key Company Profiles

Nike, Inc.

Nike, Inc. is a leading global athletic footwear and apparel company with a strong presence across performance and lifestyle categories. The company markets its products worldwide through retail, wholesale, and digital channels, and maintains a significant presence in the Mexican market.

- Product Portfolio: A broad range of performance and lifestyle apparel, footwear, and accessories spanning running, training, football, and basketball, including tops, bottoms, and outerwear.

- Recent Developments: The company has continued to expand its performance and lifestyle product portfolio, strengthen digital and omnichannel capabilities, and enhance consumer engagement through innovation, retail investments, and brand partnerships.

- Strategic Focus: Strengthening sport-led brand positioning, balancing direct-to-consumer and wholesale channels, and advancing product innovation across performance and lifestyle ranges.

adidas AG

adidas AG is a leading global sportswear company offering performance and lifestyle apparel and footwear. It maintains a broad retail and wholesale presence across major markets, including Mexico.

- Product Portfolio: Performance and lifestyle apparel, footwear, and accessories spanning football, running, training, and lifestyle ranges, including tops, bottoms, and outerwear.

- Recent Developments: The company has continued to invest in product innovation, brand marketing, and its performance and lifestyle ranges to strengthen its competitive position across markets.

- Strategic Focus: Driving growth through product innovation, sports partnerships, and expanded omnichannel distribution.

Puma SE

Puma SE is a global sport-lifestyle company offering performance and lifestyle apparel and footwear. Its products are distributed widely through retail and online channels, including in Mexico.

- Product Portfolio: Performance and lifestyle apparel, footwear, and accessories spanning football, running, training, and motorsport, including tops, bottoms, and outerwear.

- Recent Developments: The company has continued to focus on brand revitalization, product innovation, and marketing to strengthen its sport-lifestyle positioning.

- Strategic Focus: Expanding sport-lifestyle appeal through product innovation, collaborations, and broader distribution.

Market Concentration Analysis

The Mexico activewear market is moderately concentrated, with global leaders such as Nike, Inc., adidas AG, and Puma SE accounting for a significant portion of branded apparel sales, while a long tail of regional and local brands serves value segments and niche demand.

Barriers to entry include high marketing and customer-acquisition costs, the need for broad distribution across physical and digital channels, and the scale required to compete on price and product. These factors favor well-capitalized incumbents with established brand equity.

Consolidation pressures are rising as global brands deepen direct-to-consumer reach and local players seek scale through retail partnerships and sponsorships. Strategic alliances with retailers, marketplaces, and sports organizations reinforce competitive positioning.

Investment & Growth Opportunities

Fastest-Growing Segments

Premium and swimwear are expanding fastest, supported by premiumization, rising disposable income, and growing leisure and outdoor participation. Outerwear is the next-fastest category, benefiting from technical product demand and lifestyle crossover.

Emerging Markets

Southern Mexico is the fastest-growing region, anchored by rising digital adoption, expanding youth engagement, and tourism-led demand. The region represents untapped opportunity for brands that localize content.

Venture & Investment Trends

Capital is flowing into e-commerce, omnichannel retail, sustainable materials, and women's activewear lines. Investment in local brands and direct-to-consumer models is rising as players target value-conscious, digitally engaged consumers.

Future Market Outlook (2026-2034)

The Mexico activewear market is forecast to expand from USD 6.53 Billion in 2025 to USD 10.15 Billion by 2034 at a CAGR of 4.88%, adding meaningful incremental value over the forecast period.

Four forces will shape the market through 2034: deeper athleisure and casualization, e-commerce and omnichannel expansion, premiumization led by women's and technical lines, and the rise of sustainable, locally relevant products.

By 2034, activewear in Mexico is expected to be defined by mainstream daily use, a stronger premium segment, and a more balanced contest between global leaders and fast-growing local brands.

Research Methodology

Primary Research

Primary research included structured interviews with brand executives, retailers, distributors, e-commerce specialists, and industry experts, validating market sizing, regional demand, product mix, and pricing dynamics.

Secondary Research

Secondary sources included national statistical publications, trade and industry data, company annual reports, press releases, and investor presentations from listed apparel and footwear companies.

Forecasting Models

Market forecasts combined top-down and bottom-up models using consumer demand indicators, retail and e-commerce trends, pricing evolution, and macroeconomic variables, with scenario analysis addressing growth pace.

Mexico Activewear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Top Activewear, Bottom Activewear, Innerwear, Swimwear, Outerwear |

| Material Types Covered | Nylon, Polyester, Cotton, Neoprene, Polypropylene, Spandex |

| Pricings Covered | Economy, Premium |

| Age Groups Covered | 1-15 Years, 16-30 Years, 31-44 Years, 45-64 Years, more than 65 Years |

| Distribution Channels Covered | Online Stores, Offline Stores |

| End Users covered | Men, Women, Kids |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Nike Inc., adidas AG, Puma SE, lululemon athletica, New Balance, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico activewear market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico activewear market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico activewear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Activewear Market Report

The Mexico activewear market was valued at USD 6.53 Billion in 2025, driven by rising fitness culture, athleisure adoption, e-commerce growth, and expanding demand across product and pricing segments.

The market is projected to grow at a 4.88% CAGR from 2026 to 2034, reaching USD 10.15 Billion, supported by premiumization, women's lines, and omnichannel retail expansion.

Top activewear leads at 31.6% in 2025, driven by everyday demand for t-shirts, tops, and jerseys.

Economy dominates at 63.5% in 2025, reflecting price-sensitive middle-income buyers. The segment also benefits from broad availability through mass retail, discount stores, supermarkets, and online marketplaces, making activewear accessible to a wide consumer base.

Central Mexico commands 41.8% in 2025, led by high population density, disposable income, and concentrated retail infrastructure across Mexico City and surrounding states.

Leading players include Nike, Inc., adidas AG, Puma SE, lululemon athletica, and New Balance, among others.

Key drivers include rising health and fitness awareness, athleisure and casualization of apparel, e-commerce and omnichannel retail growth, and increasing female participation in sports and fitness.

Major challenges include intense competition from global and local brands, price sensitivity, counterfeit and gray-market products, import dependence, and uneven premium retail access in smaller cities.

E-commerce is widening access through marketplaces, brand websites, and quick-commerce, improving discovery and delivery, especially among younger, digitally engaged consumers in urban and secondary markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)