Mexico Auto Parts Aftermarket Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Mexico Auto Parts Aftermarket Market Size, Share, Trends & Forecast (2026-2034)

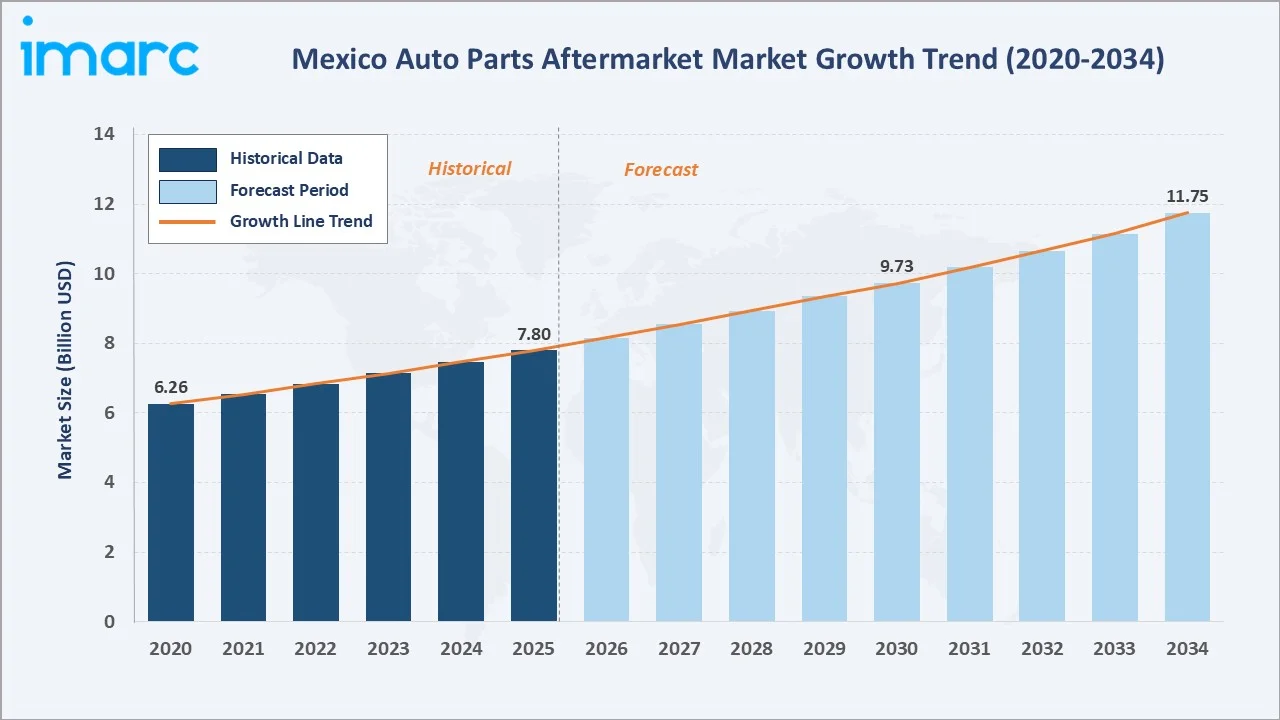

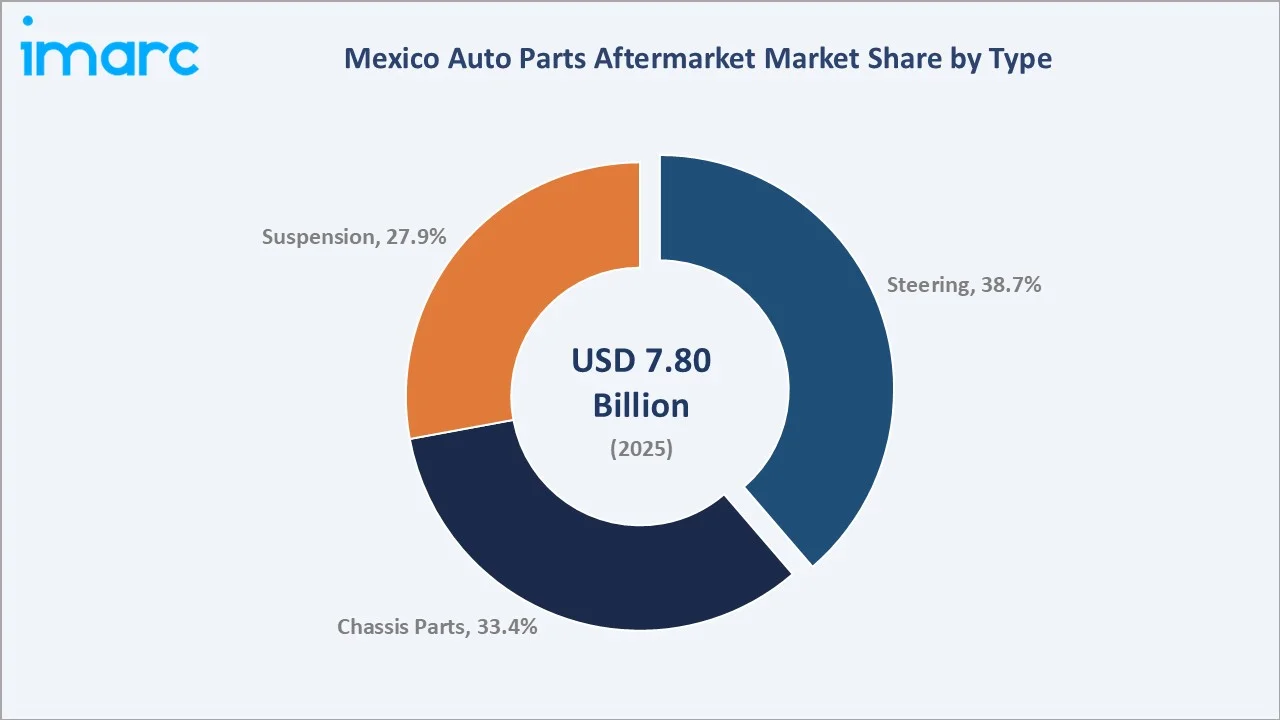

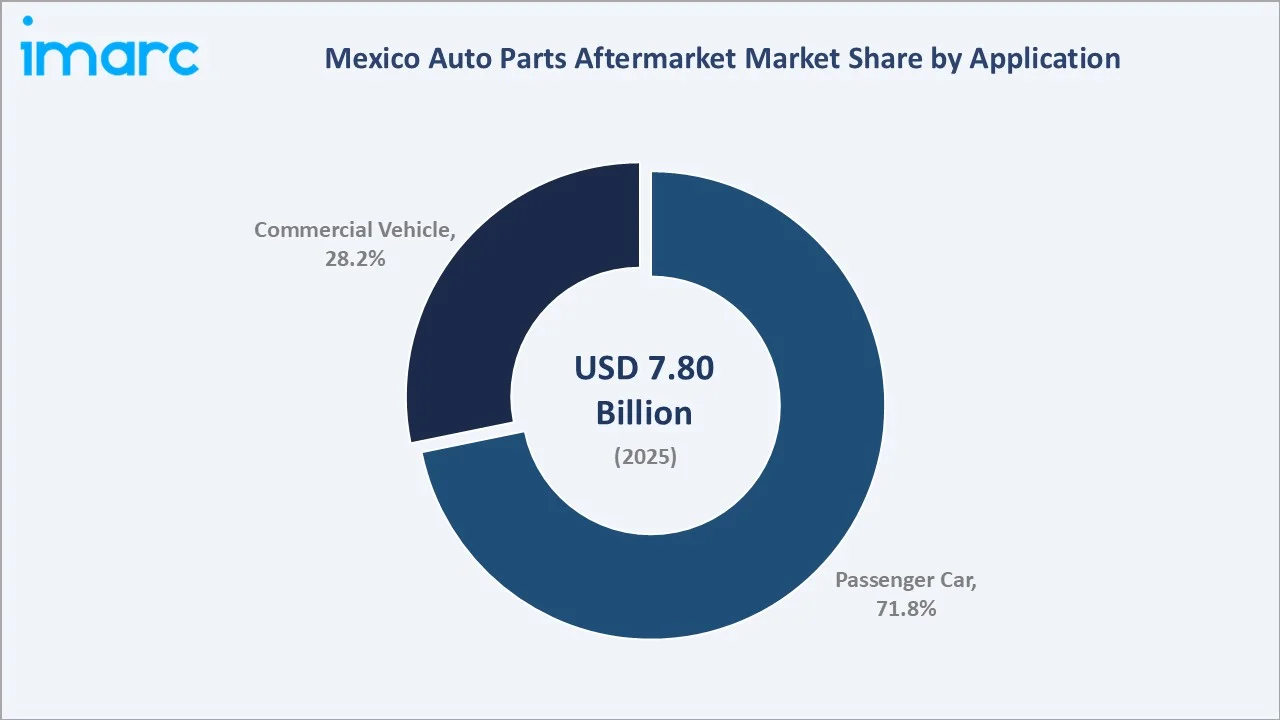

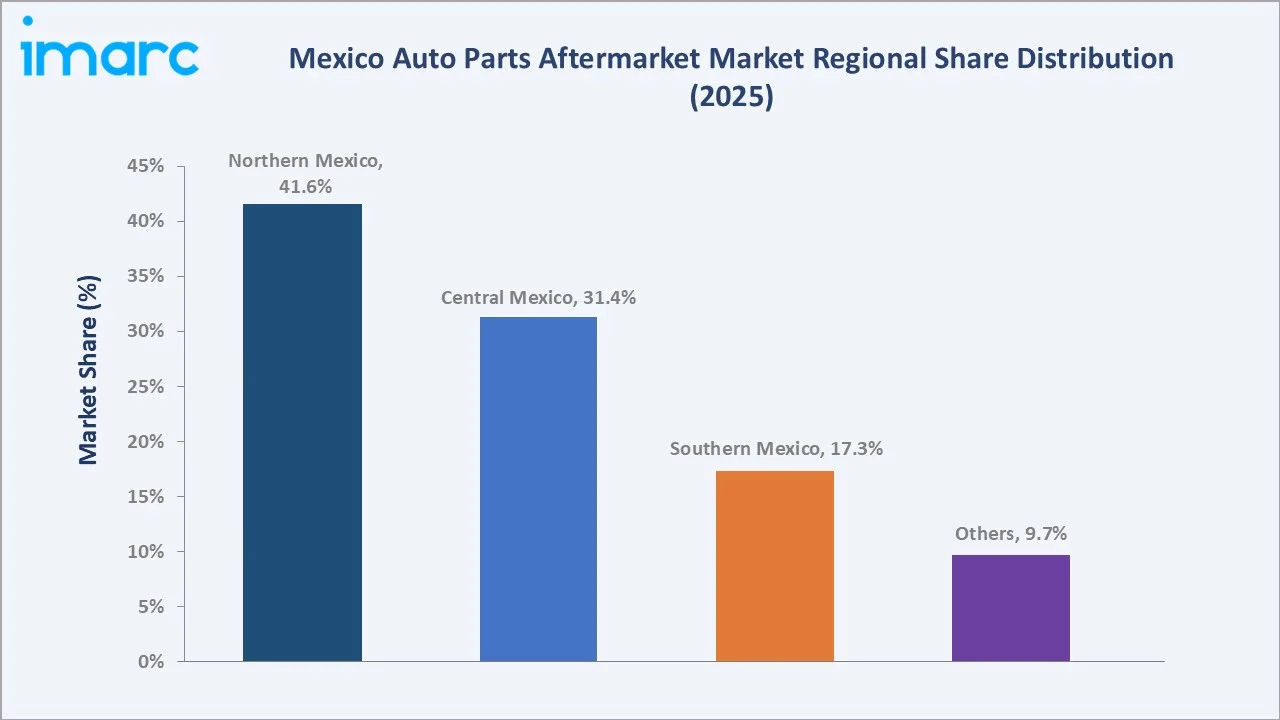

The Mexico auto parts aftermarket market reached USD 7.80 Billion in 2025 and is projected to reach USD 11.75 Billion by 2034, growing at a CAGR of 4.51% during 2026-2034. The market is driven by the country’s large and aging vehicle fleet, which creates consistent demand for replacement parts, maintenance, and repair services. Growth is further supported by rising vehicle ownership, cross-border parts trade, expanding independent workshops, and increasing demand for cost-effective aftermarket components. Mexico’s light vehicle sales increased by 5.0% in May 2026, with Mexico’s Instituto Nacional de Estadistica y Geografia (INEGI) reporting 127,107 units sold, compared with May 2025. This growth supports the Mexico auto parts aftermarket by expanding the vehicle base that will require replacement parts, maintenance, tires, batteries, lubricants, filters, and repair services over time. Steering leads type at 38.7%. Passenger car leads application at 71.8%. Northern Mexico leads at 41.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.80 Billion |

|

Forecast Market Size (2034) |

USD 11.75 Billion |

|

CAGR (2026-2034) |

4.51% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Steering - 38.7% share (2025) |

|

Dominant Application |

Passenger Car - 71.8% share (2025) |

|

Leading Region |

Northern Mexico - 41.6% share (2025) |

The Mexico auto parts aftermarket market grew from USD 6.26 Billion in 2020 to USD 7.80 Billion in 2025, supported by rising vehicle ownership, aging fleet conditions, and steady repair and maintenance demand. The market is expected to reach USD 9.73 Billion by 2030, driven by higher demand for replacement parts, tires, batteries, filters, lubricants, and accessories. By 2034, it is forecast to reach USD 11.75 Billion, reflecting continued growth in independent workshops, e-commerce parts sales, and cross-border component supply.

To get more information on this market, Request Sample

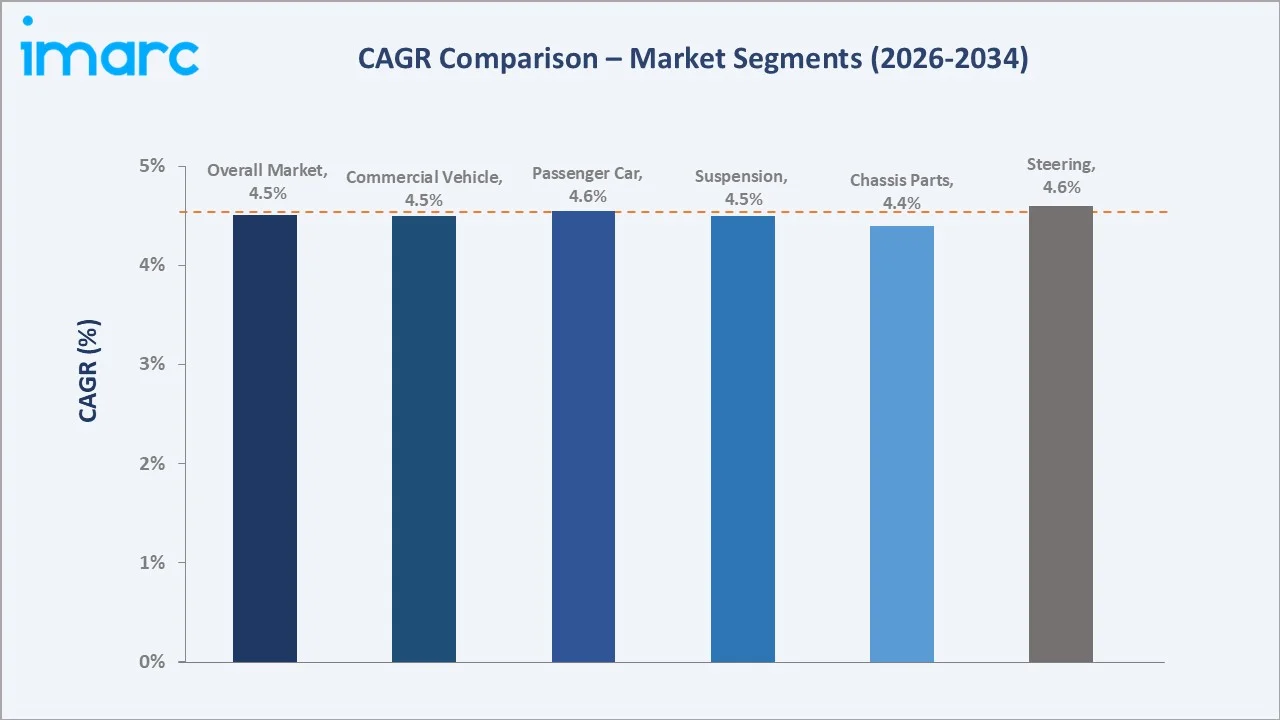

Steering grows fastest at ~4.6% CAGR through Mexico's pothole-and-rough-road driving conditions. Passenger car grows at ~4.6% CAGR through Mexico's rising middle-class vehicle ownership and used-car market expansion.

Executive Summary

Mexico auto parts aftermarket market is expanding steadily as a large vehicle base creates recurring demand for repair, maintenance, and replacement components. Growth is supported by rising light vehicle sales, aging vehicles, independent workshops, and cost-conscious consumers seeking affordable parts. Demand is strongest across tires, batteries, brake parts, filters, lubricants, and electrical components. E-commerce platforms and cross-border supply chains are reshaping parts availability and distribution. With the market forecast to reach USD 11.75 Billion by 2034, aftermarket services will remain a key pillar of Mexico’s automotive ecosystem. Steering at 38.7% leads through Mexico's road condition-driven wear. Passenger car at 71.8% leads Mexico's passenger car fleet. Northern Mexico leads regionally at 41.6% through a manufacturing cluster.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Steering - 38.7% share (2025) |

|

Dominant Application |

Passenger Car - 71.8% market share (2025) |

|

Leading Region |

Northern Mexico - 41.6% share (2025) |

|

Market Opportunity |

EV and hybrid aftermarket parts growing; e-commerce digital auto parts platform; used-car fleet demand for steering and suspension; commercial fleet management parts programs |

Key Analytical Observations Supporting The Above Data:

- Steering at 38.7%: The steering segment dominates as steering components are exposed to continuous wear from road conditions, frequent driving, and vehicle aging. Regular replacement of tie rods, steering racks, pumps, and related parts supports steady aftermarket demand.

- Passenger Car at 71.8%: The passenger car segment dominates the market because it represents the largest vehicle base in Mexico and requires frequent maintenance and replacement parts. High daily usage, aging vehicles, and cost-conscious owners drive steady demand for aftermarket components.

- Northern Mexico at 41.6%: Northern Mexico dominates regionally due to its strong concentration of automotive manufacturing hubs, cross-border trade with the United States, and dense logistics networks. High vehicle usage, industrial activity, and easy access to replacement parts support strong aftermarket demand across the region.

Mexico Auto Parts Aftermarket Market Overview

Mexico auto parts aftermarket encompasses the supply chain of replacement, maintenance, and repair parts for the Mexico vehicle fleet through two primary channels: independent aftermarket and dealer/OE. The market is unique due to its strong link with the US supply chain, large aging vehicle fleet, and cost-sensitive repair culture. Demand is supported by both formal distributors and a wide network of independent workshops, local retailers, and informal repair channels. Northern Mexico’s manufacturing base and cross-border logistics further strengthen parts availability, making the market highly dynamic and replacement-driven. Macroeconomic factors include rising vehicle ownership, growth in disposable income, expansion of cross-border automotive trade, and increasing industrial activity.

Market Dynamics

To evaluate market opportunities, Request Sample

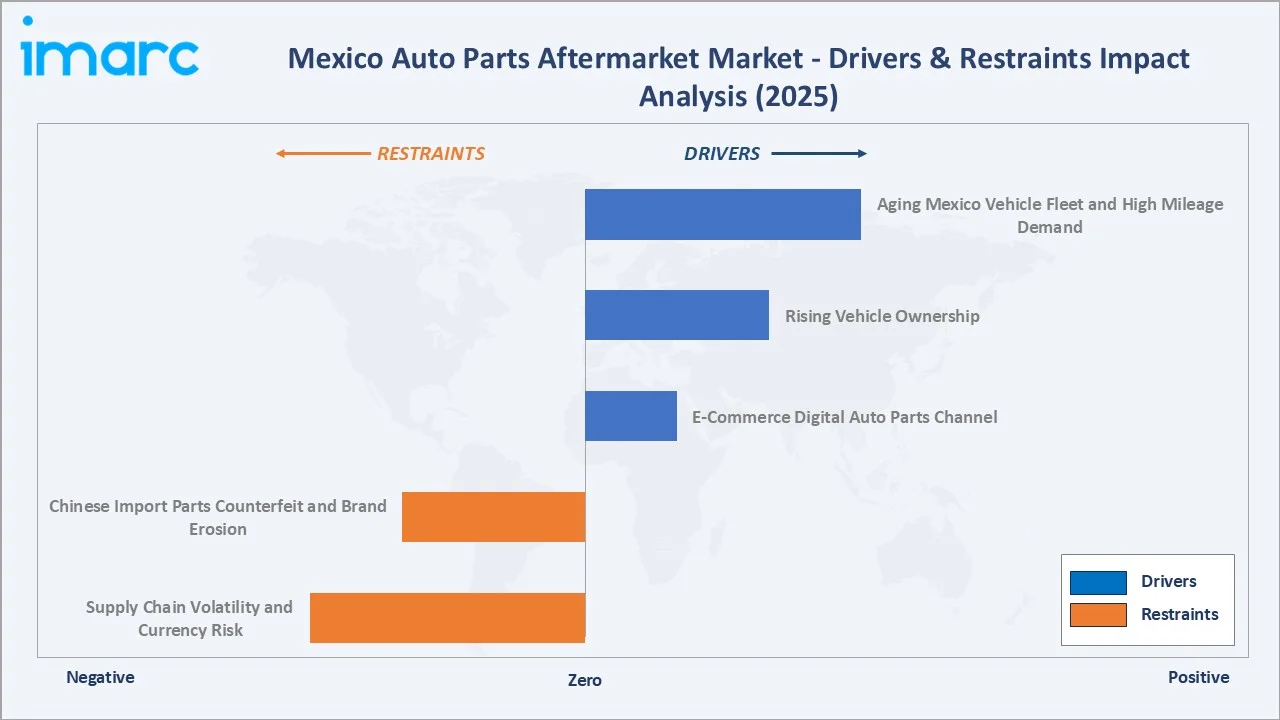

Market Drivers

- Aging Mexico Vehicle Fleet and High Mileage Demand: Aging Mexico vehicle fleet and high-mileage demand are major drivers, as older vehicles require more frequent repairs and component replacements. High daily usage, long commuting distances, commercial vehicle wear, and uneven road conditions increase demand for steering, suspension, brakes, tires, batteries, filters, and lubricants. Many consumers prefer repairing vehicles rather than replacing them due to cost sensitivity, supporting independent workshops and aftermarket part suppliers. As more vehicles remain on the road beyond warranty periods, recurring maintenance demand continues to expand the aftermarket.

- Rising Vehicle Ownership: According to Mexico’s Instituto Nacional de Estadistica y Geografia (INEGI), light vehicle sales reached 127,107 units in May 2026, representing a 5.0% increase compared with May 2025. This rising vehicle ownership is expanding the number of vehicles that require regular servicing, repairs, and replacement components. As more households and businesses purchase cars, demand increases for tires, batteries, filters, brakes, lubricants, lighting, and steering parts. Growing vehicle ownership also strengthens the customer base for independent garages, retail parts stores, and online aftermarket platforms. Over time, newly sold vehicles enter the post-warranty cycle, creating recurring aftermarket demand.

- E-Commerce Digital Auto Parts Channel: E-commerce digital auto parts channels are making replacement components more accessible to consumers, workshops, and small retailers. Online platforms allow buyers to compare prices, check compatibility, access wider product ranges, and source parts faster than traditional channels. Digital sales are especially useful for cost-conscious customers seeking affordable branded or private-label components. As internet penetration, mobile payments, and last-mile delivery improve, online auto parts distribution is becoming an important growth channel for the aftermarket.

Market Restraints

- Chinese Import Parts Counterfeit and Brand Erosion: Chinese import parts, counterfeits, and brand erosion are intensifying price competition and pressuring margins for established suppliers. Low-cost imported components can attract price-sensitive consumers, but inconsistent quality and counterfeit risks may reduce trust in branded aftermarket products. Counterfeit steering, braking, suspension, and electrical parts also create safety concerns and increase warranty and reputational risks for distributors and repair workshops. As unverified products enter informal and online channels, genuine brands face difficulty protecting market share and maintaining premium pricing.

- Supply Chain Volatility and Currency Risk: Supply chain volatility and currency risk increase uncertainty in parts availability, pricing, and distributor margins. Many aftermarket components depend on imported raw materials, finished parts, and cross-border logistics, making the market vulnerable to freight delays, port congestion, and supplier disruptions. Fluctuations in the Mexican peso against the U.S. dollar can raise import costs for parts sourced from the United States, China, and other markets. These pressures can increase retail prices, reduce affordability for consumers, and squeeze margins for workshops, wholesalers, and retailers.

Market Opportunities

- EV Aftermarket Parts and Charging-Related Components: EV aftermarket parts and charging-related components represent an emerging opportunity as electric and hybrid vehicle adoption gradually increases. Mexico’s electrified vehicle market achieved a new record in March 2026, with 16,374 electrified vehicles sold, representing a 33.9% year-on-year increase compared with March 2025, according to data presented jointly by AMIA, AMDA, and INA. EVs create demand for specialized components such as battery cooling systems, sensors, power electronics, brake components, tires, thermal management parts, and charging accessories. Workshops and distributors that invest early in EV diagnostics, technician training, and compatible parts inventories can capture higher-value service demand. As charging infrastructure expands and more EVs enter the post-warranty cycle, this segment is expected to become an important long-term growth avenue.

- Advanced Inventory Management and Supply Chain Digitalization: Advanced inventory management and supply chain digitalization help distributors, retailers, and workshops improve parts availability and reduce stockouts. Digital platforms can track demand patterns, vehicle parc data, SKU movement, and regional inventory needs more accurately. This is especially important in a fragmented market where incorrect parts, delayed delivery, and excess inventory can reduce margins. By adopting warehouse automation, real-time inventory visibility, and predictive ordering systems, aftermarket players can improve service speed, lower costs, and strengthen customer loyalty.

Market Challenges

- Increasing Vehicle Technology Complexity: Increasing vehicle technology complexity is becoming a major challenge as modern vehicles incorporate advanced electronics, ADAS features, sensors, connectivity systems, and software-driven components. Repairing and diagnosing these vehicles requires specialized tools, technical training, and access to proprietary OEM data. Independent workshops may face difficulties sourcing compatible parts and maintaining the skills needed to service newer vehicle models. As a result, operating costs rise and some repair work shifts toward authorized dealerships, creating competitive pressure for traditional aftermarket providers.

- Counterfeit Product Safety and Quality Concerns: Counterfeit product safety and quality concerns weaken trust in replacement parts sold through informal, low-cost, and online channels. Counterfeit or poor-quality brakes, steering, suspension, lighting, and electrical components can increase accident risks, vehicle failures, and repair complaints. These issues create reputational damage for genuine brands, distributors, and workshops when customers cannot easily distinguish authentic from fake products. They also force legitimate suppliers to invest more in packaging security, traceability, dealer education, and quality assurance, increasing operating costs.

Emerging Market Trends

1. E-Commerce and Digital Auto Parts

E-commerce and digital auto parts are emerging as consumers, workshops, and small retailers increasingly use online platforms to source replacement components. Digital channels make it easier to compare prices, verify part compatibility, access wider inventories, and purchase branded or value parts quickly. This trend is also improving distribution efficiency by connecting suppliers, warehouses, and repair shops through real-time ordering systems. As mobile payments, logistics networks, and marketplace adoption expand, online auto parts sales are becoming a key growth channel in Mexico’s aftermarket.

2. EV and Hybrid Aftermarket Parts

EV and hybrid aftermarket parts are emerging as electrified vehicle sales gradually expand. These vehicles create new demand for battery-related components, thermal management systems, sensors, power electronics, regenerative braking parts, specialized tires, and charging accessories. Aftermarket suppliers and workshops are beginning to prepare for EV diagnostics, technician training, and high-voltage safety requirements. As more electric and hybrid vehicles move beyond warranty coverage, this segment is expected to become a higher-value growth area.

3. AI-Powered Workshop Management Platforms

AI-powered workshop management platforms are an emerging trend in Mexico’s auto parts aftermarket as repair businesses move from manual processes to digital, data-driven operations. These platforms integrate diagnostics, appointment scheduling, inventory tracking, parts sourcing, invoicing, and customer management into one system. In February 2026, Pitz, a Mexico-based workshop digitalization startup, introduced an auto parts marketplace within its AI-powered management platform. The solution links diagnostics, parts procurement, and workshop operations in one system, helping more than 260,000 repair and maintenance businesses reduce inefficiencies, improve productivity, and protect margins in a largely analog aftermarket sector. As Mexico’s aftermarket remains highly fragmented and largely analog, AI-enabled platforms can improve margins, service quality, and operational efficiency for independent garages.

4. Commercial Fleet Maintenance Programs

Commercial fleet maintenance programs are emerging as logistics, ride-hailing, delivery, rental, and industrial fleets require predictable uptime and lower operating costs. Fleet operators are increasingly adopting scheduled maintenance contracts, bulk parts procurement, telematics-based service alerts, and preferred workshop networks. This creates recurring demand for tires, brakes, filters, lubricants, suspension parts, batteries, and diagnostics services. As Mexico’s e-commerce, manufacturing, and cross-border freight sectors expand, organized fleet maintenance is becoming a higher-value aftermarket growth channel.

Industry Value Chain Analysis

Mexico auto parts aftermarket value chain integrates raw material & component manufacturing, auto parts manufacturing, national distribution & import channels, regional wholesale & retail, workshop & service installation, and vehicle owner & fleet end use.

|

Stage |

Key Participants |

|

Raw Material & Component Manufacturing |

Steel, rubber, plastic, electronics, battery, lubricant, and mechanical component suppliers |

|

Auto Parts Manufacturing |

OEM component makers, aftermarket parts producers, private-label manufacturers, and remanufacturers |

|

National Distribution & Import Channels |

Importers, authorized distributors, warehouse operators, logistics providers, and cross-border suppliers |

|

Regional Wholesale & Retail |

Regional wholesalers, tiendas, organized auto parts retailers, e-commerce platforms, and marketplace sellers |

|

Workshop & Service Installation |

Independent garages, repair shops, fleet maintenance centers, tire shops, and dealer service networks |

|

Vehicle Owner & Fleet End Use |

Passenger car owners, commercial fleets, logistics operators, ride-hailing drivers, and small businesses |

The workshop & service installation stage is typically the most value-added segment in the Mexico auto parts aftermarket value chain. This is where parts are diagnosed, selected, installed, calibrated, and integrated into vehicles, generating higher labor and service margins than pure parts distribution. The stage also benefits from recurring maintenance, customer relationships, technical expertise, and increasingly digital diagnostics, making it a key driver of profitability and customer retention.

Technology Landscape in the Mexico Auto Parts Aftermarket Industry

Digital Catalogs and Parts Identification Technology

Digital catalogs and parts identification technology improve accuracy in parts selection and reduce ordering errors. These platforms use VIN-based lookup, barcode scanning, vehicle databases, and real-time inventory integration to quickly match components with specific vehicle models. Workshops and retailers can identify compatible parts faster, shortening repair times and improving customer satisfaction. As e-commerce and digital procurement expand, advanced parts identification systems are becoming essential tools for distributors, garages, and aftermarket retailers.

Remanufacturing and OE-Fix Technology

Remanufacturing and OE-fix technology provide cost-effective alternatives to new replacement components. Remanufactured starters, alternators, steering systems, brake calipers, and electronic modules help extend vehicle life while reducing material waste and repair costs. OE-fix solutions improve upon original equipment designs to address recurring performance or reliability issues found in specific vehicle models. As consumers seek affordable repairs and sustainability gains importance, remanufacturing and OE-fix technologies are gaining wider acceptance across workshops and parts distributors.

Connected Diagnostics and Scan-Tool Integration

Connected diagnostics and scan-tool integration help workshops identify vehicle faults more accurately and quickly. Modern scan tools connect with onboard vehicle systems to read error codes, sensor data, emissions issues, and electronic component failures. When integrated with parts catalogs and inventory systems, diagnostics can directly recommend compatible replacement components, reducing repair time and ordering mistakes. As vehicles become more electronic and software-driven, connected diagnostic tools are becoming essential for independent workshops to remain competitive.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Steering |

38.7% |

2025 |

|

Application |

Passenger Car |

71.8% |

2025 |

|

Region |

Northern Mexico |

41.6% |

2025 |

By Type

Steering leads at 38.7% (2025), through rack-and-pinion replacement, tie rod and ball joint, power steering pump, and steering column for Mexico's pothole-and-rough-road driving.

To access detailed market analysis, Request Sample

Chassis parts at 33.4% reflects control arm, sway bar link, wheel bearing, hub assembly, and chassis bushing for Mexico's road-impact chassis wear. Suspension at 27.9% reflects Monroe shock absorber, coil spring, strut mount, and stabilizer link driven by Mexico's pothole-dominant road network.

By Application

Passenger cars lead at 71.8% (2025), represent the largest vehicle base and generate frequent replacement demand. High daily usage, aging ownership patterns, and post-warranty repairs support strong demand for brakes, tires, filters, batteries, steering, and suspension parts.

Commercial vehicle at 28.2% reflects Mexico's logistics expansion (nearshoring supply chain), PEMEX fleet, and inter-city bus fleet.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico Auto Parts Aftermarket Market Drivers & Characteristics |

|

Northern Mexico |

41.6% |

Supported by strong automotive manufacturing clusters, extensive cross-border trade with the United States, high commercial vehicle activity, and a well-developed distribution network serving both OEM and aftermarket channels. |

|

Central Mexico |

31.4% |

Reflects its large vehicle population, concentration of major metropolitan areas, dense network of repair workshops, and strong demand for replacement parts from passenger cars, fleets, and public vehicles. |

|

Southern Mexico |

17.3% |

Driven by growing vehicle ownership, increasing road transportation activity, expanding independent repair networks, and rising demand for affordable aftermarket components in cost-sensitive markets. |

|

Others |

9.7% |

Other regions are driven by localized demand from tourism, agriculture, logistics, mining activities, and regional vehicle maintenance requirements. |

Northern Mexico's 41.6% dominance is supported by its strong automotive manufacturing base, extensive cross-border trade activity, and dense network of distributors, wholesalers, and repair workshops. Central Mexico's 31.4% benefiting from high vehicle ownership levels, major urban centers such as Mexico City, and a large concentration of passenger vehicles requiring regular maintenance and replacement parts.

Southern Mexico's 17.3% witnessing steady growth due to expanding vehicle penetration, improving road infrastructure, and increasing demand for affordable aftermarket components. Others at 9.7% include the Bajío automotive cluster, the Pacific Coast commercial fleet, and the Gulf Coast fleet parts.

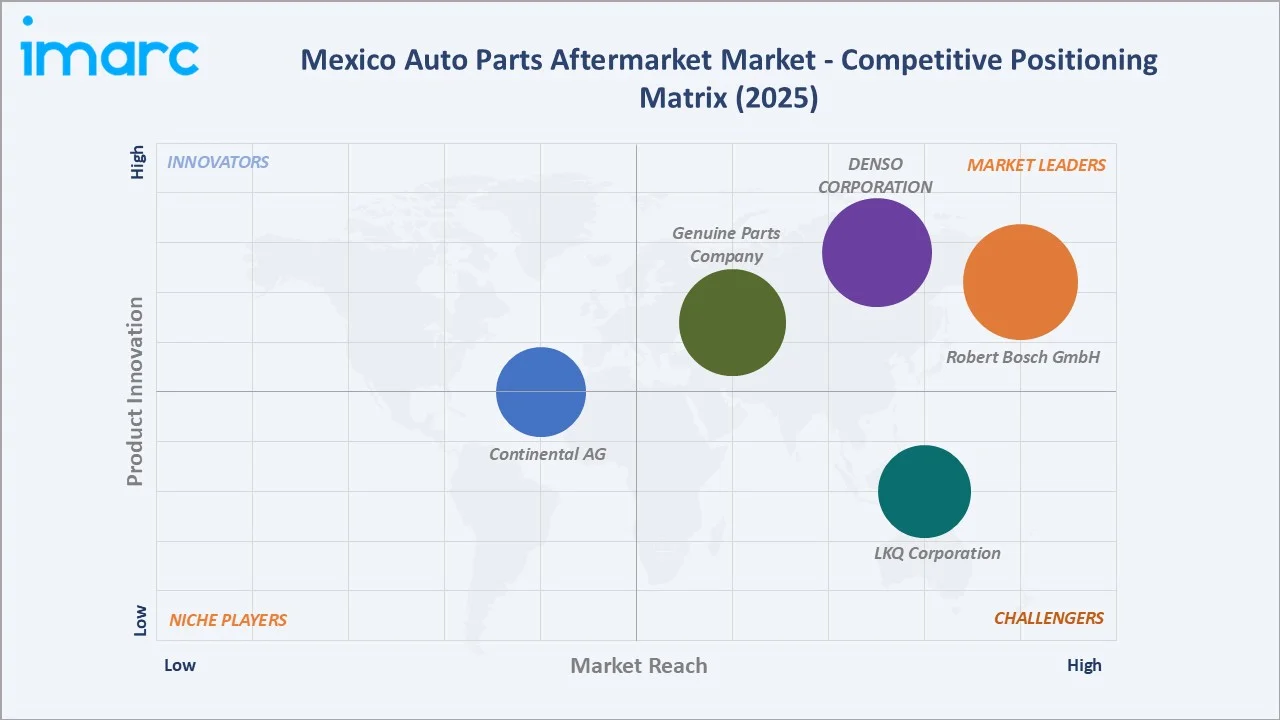

Competitive Landscape

The Mexico auto parts aftermarket market is moderately fragmented, with competition spanning global component manufacturers, domestic distributors, organized retail chains, e-commerce platforms, and thousands of independent parts suppliers. Major players compete on product availability, brand reputation, distribution reach, pricing, and technical support services. Organized retailers such as large auto parts chains continue expanding their store footprints and digital capabilities, increasing pressure on traditional wholesalers and informal channels.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Robert Bosch GmbH |

Accumulators, Alternators and Starters, Spark plugs, Fuel Injection Components, Filters, Brakes, Ignition System, Diesel Injection Systems |

Market Leader |

Robert Bosch GmbH acts as a primary original equipment manufacturer (OEM) and Mobility Aftermarket supplier in Mexico, delivering replacement parts, advanced diagnostic tools, and software directly to workshops. |

|

DENSO CORPORATION |

A/C & Engine Cooling, O2 & A/F Sensors, Rotating Electrical, Filters, Spark Plugs |

Market Leader |

DENSO CORPORATION operates a major Tier 1 supply chain and aftermarket presence in Mexico. It leverages robust local production to supply replacement parts and accessories for independent and commercial aftermarket channels. |

|

Genuine Parts Company |

Bike Racks, Air Intakes, Bull Bars, Cargo Carriers, Window Deflectors, Towing & Hitches |

Market Leader |

Genuine Parts Company plays a strategic role in the Mexican automotive aftermarket through the distribution of replacement parts, accessories, and service items under the NAPA brand. |

|

LKQ Corporation |

Axle / Suspension, Engine Compartment, Exterior, Fuel System, Heating / Air, Interior, Lighting, Wheels |

Strong Challenger |

LKQ Corporation serves as a leading value-added distributor of alternative collision and mechanical replacement parts, recycled OEM components, and specialty accessories in the Mexican automotive aftermarket. |

|

Continental AG |

Actuators and motors, Air Spring Replacement, Batteries, Brakes, Sensors, Fuel Systems |

Established Player |

Continental AG is a leading tier-1 supplier in Mexico's auto parts aftermarket, leveraging its massive local manufacturing footprint to supply replacement tires and OE-quality spare parts like sensors and fuel pumps. |

Market participants are also investing in inventory management, e-commerce platforms, AI-enabled workshop solutions, and faster delivery networks to strengthen customer retention. As vehicle technology becomes more complex, suppliers with strong diagnostic support, broad product portfolios, and nationwide distribution capabilities are gaining a competitive advantage.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH is one of the leading automotive technology and aftermarket suppliers operating in Mexico’s auto parts aftermarket. The company offers a broad portfolio of replacement products, including braking systems, batteries, filters, spark plugs, sensors, steering components, diagnostics equipment, and workshop solutions. Bosch benefits from its strong OEM relationships, extensive distribution network, and established brand recognition across independent workshops, fleet operators, and organized retail channels.

- Key Products: Accumulators, Alternators and Starters, Spark plugs, Fuel Injection Components, Filters, Brakes, Ignition System, Diesel Injection Systems.

- Strategic Focus: Strengthening its position in Mexico’s auto parts aftermarket through a combination of premium replacement parts, advanced vehicle diagnostics, and connected workshop solutions.

DENSO CORPORATION

DENSO CORPORATION is a leading automotive technology and components supplier with a growing presence in Mexico’s auto parts aftermarket. The company offers a wide range of replacement products, including spark plugs, ignition components, sensors, fuel system parts, air-conditioning systems, filters, wiper blades, and thermal management solutions.

- Key Products: A/C & Engine Cooling, O2 & A/F Sensors, Rotating Electrical, Filters, Spark Plugs.

- Strategic Focus: Expanding its aftermarket presence in Mexico through high-quality replacement parts, technical service support, and stronger distributor partnerships.

Market Concentration Analysis

The Mexico auto parts aftermarket exhibits a moderately fragmented market structure, with competition distributed among global component manufacturers, domestic suppliers, organized retail chains, e-commerce platforms, and independent distributors. International players such as major OEM-affiliated brands maintain strong positions in premium product categories, while regional suppliers compete aggressively on pricing and local availability. Organized retail networks and digital marketplaces are steadily increasing their market influence through broader product assortments and improved distribution capabilities. Despite the presence of established brands, a large share of sales still flows through independent workshops and fragmented distribution channels. As vehicle technology advances and consumers increasingly prioritize quality and authenticity, market share is gradually consolidating toward companies with strong brands, technical support capabilities, and nationwide distribution networks.

Investment & Growth Opportunities

Highest Growth Segments

EV aftermarket emerging (~10-15% CAGR), USMCA nearshoring auto parts export (~6-8% CAGR), steering (~4.6% CAGR), organized retail expansion, digital e-commerce (~8-10% CAGR), and commercial fleet management programs represent Mexico's auto parts highest-growth investment vectors through 2034.

Investment Themes

- E-Commerce Digital Auto Parts Platform: Investment in digital auto parts platforms is gaining momentum as workshops, retailers, and vehicle owners increasingly prefer online sourcing channels. Platforms offering VIN-based part identification, real-time inventory visibility, integrated logistics, and digital payments can capture growing demand while improving supply chain efficiency and customer reach.

- EV and Hybrid Aftermarket Parts: The rapid growth of electric and hybrid vehicle adoption is creating demand for specialized aftermarket products such as batteries, thermal management systems, power electronics, charging accessories, and high-voltage components. Early investment in EV-focused parts distribution, diagnostics, and technician training can position companies to benefit from this emerging high-value aftermarket segment.

Future Market Outlook (2026-2034)

Mexico's auto parts aftermarket market is projected to grow from USD 7.80 Billion in 2025 to USD 11.75 Billion by 2034, delivering a 4.51% CAGR over the forecast period through aging fleet demand, USMCA nearshoring auto parts manufacturing expansion, rising Mexico vehicle ownership, e-commerce digital channel disruption, and emerging EV aftermarket. The market's anchor value of USD 9.73 Billion in 2030 represents Mexico auto parts aftermarket at digital and EV inflection.

Three structural forces define Mexico’s auto parts aftermarket growth through 2034. First, the country’s large and aging vehicle fleet is creating steady replacement demand across tires, batteries, filters, brakes, steering, and suspension components. Second, rising vehicle ownership and expanding commercial fleet activity are increasing repair frequency and parts consumption. Third, e-commerce platforms, organized retail expansion, and digital workshop tools are reshaping distribution, improving parts access, and supporting higher aftermarket penetration.

Research Methodology

Primary Research

Primary research comprised interviews with auto parts distributors, retailers, independent workshops, fleet operators, and component suppliers across Mexico. It also included validation of replacement demand, pricing trends, distribution channels, and regional service patterns.

Secondary Research

Secondary research encompassed government vehicle sales data, automotive association reports, trade statistics, company publications, and industry databases. It also reviewed aftermarket trends, vehicle parc development, import activity, e-commerce adoption, and competitive positioning.

Forecasting Models

Forecasting models combined historical aftermarket sales trends, vehicle parc growth, vehicle age distribution, replacement cycles, and macroeconomic indicators to project future demand. The analysis incorporated segment-level forecasting for parts categories, vehicle types, and distribution channels. Scenario-based modeling and expert validation were used to assess the impact of electrification, e-commerce adoption, and fleet expansion on long-term market growth.

Mexico Auto Parts Aftermarket Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Steering, Chassis Parts, Suspension |

| Applications Covered | Passenger Car, Commercial Vehicle |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Robert Bosch GmbH, DENSO CORPORATION, Genuine Parts Company, LKQ Corporation, Continental AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico auto parts aftermarket market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico auto parts aftermarket market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico auto parts aftermarket industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Auto Parts Aftermarket Market Report

The Mexico auto parts aftermarket market reached USD 7.80 Billion in 2025, driven by a large and aging vehicle fleet, rising passenger car ownership, and steady demand for replacement parts such as tires, brakes, batteries, filters, steering, and suspension components. Growth is further supported by expanding e-commerce channels, organized retail networks, independent workshops, and increasing commercial fleet maintenance needs.

The Mexico auto parts aftermarket market grows at 4.51% CAGR during 2026-2034, reaching USD 11.75 Billion by 2034. The CAGR reflects aging fleet demand, USMCA nearshoring, rising vehicle ownership, e-commerce digital channel, and emerging EV aftermarket.

Steering leads at 38.7% due to frequent wear of steering racks, tie rods, pumps, bearings, and related components under high-mileage driving conditions. Mexico’s aging vehicle fleet, uneven road quality, and strong repair-over-replacement behavior create steady aftermarket demand for steering parts.

Passenger cars lead at 71.8% as they account for the largest share of the country’s vehicle parc and generate the highest volume of routine maintenance and replacement activities. Frequent usage, growing ownership levels, and an aging stock of vehicles drive sustained demand for components such as brakes, batteries, filters, steering, suspension, and engine parts.

Northern Mexico leads at 41.6% due to its strong automotive manufacturing base, proximity to the U.S. border, and well-developed cross-border parts distribution network. High commercial vehicle movement, industrial activity, and dense workshop presence further support strong demand for replacement components and maintenance services.

Leading companies include Robert Bosch GmbH, DENSO CORPORATION, Genuine Parts Company, LKQ Corporation, and Continental AG, among others.

The market is projected to reach approximately USD 9.73 Billion by 2030, supported by sustained replacement demand from an expanding and aging vehicle fleet. Growth will also be driven by e-commerce parts platforms, organized retail expansion, and rising commercial fleet maintenance needs.

Three priority investment opportunities are emerging within Mexico’s auto parts aftermarket. First, e-commerce and digital auto parts platforms are gaining traction as workshops and consumers increasingly shift toward online procurement. Second, EV and hybrid aftermarket parts present long-term growth potential as electrified vehicle adoption accelerates and demand rises for batteries, thermal management systems, and charging-related components. Third, AI-enabled workshop management and diagnostics solutions offer opportunities to improve repair efficiency, inventory control, and customer service across Mexico’s highly fragmented repair ecosystem.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)