Mexico Autonomous Trucks Market Size, Share, Trends and Forecast by Level of Autonomy, Propulsion, Vehicle Type, Application, Sensor Type, ADAS Feature, and Region, 2026-2034

Mexico Autonomous Trucks Market Size, Share, Trends & Forecast (2026-2034)

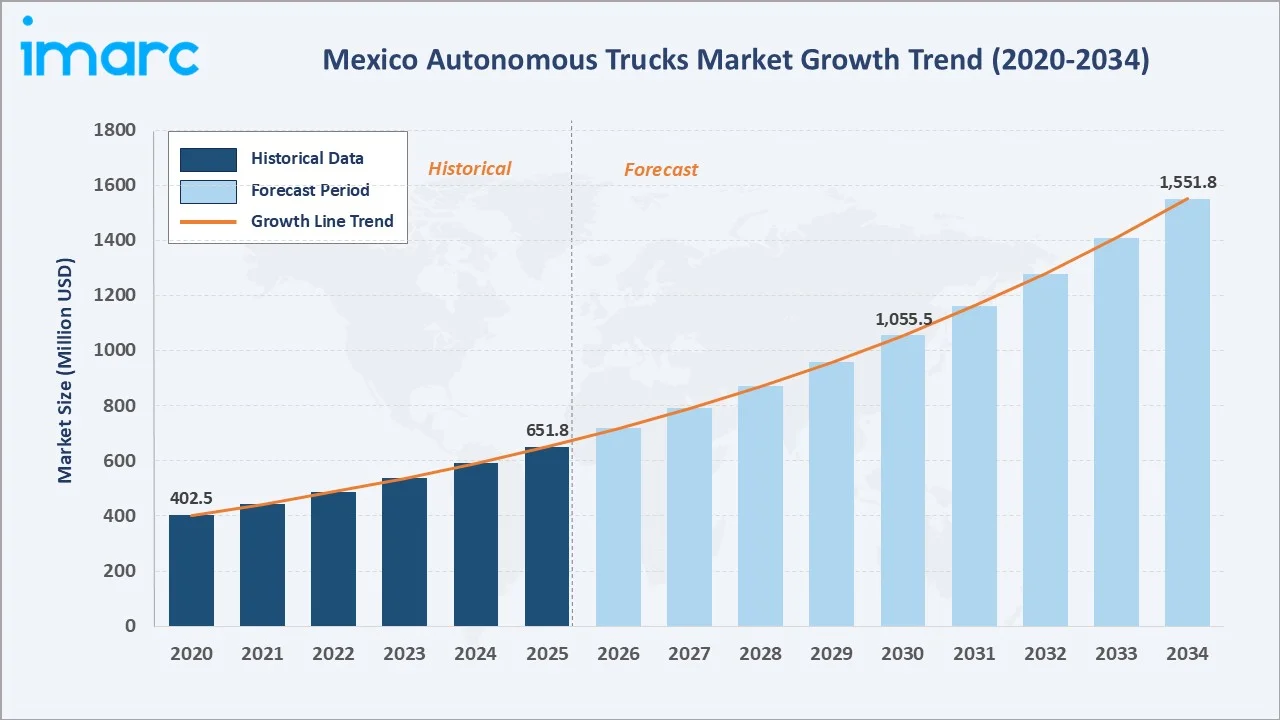

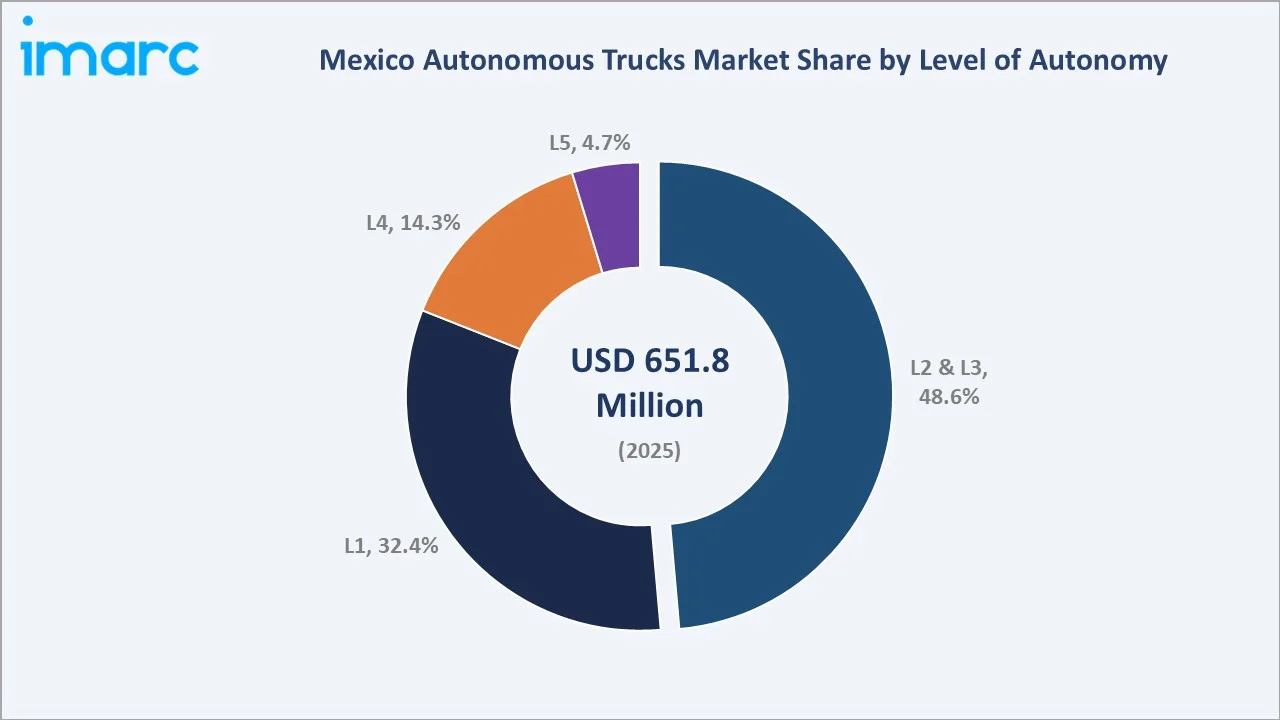

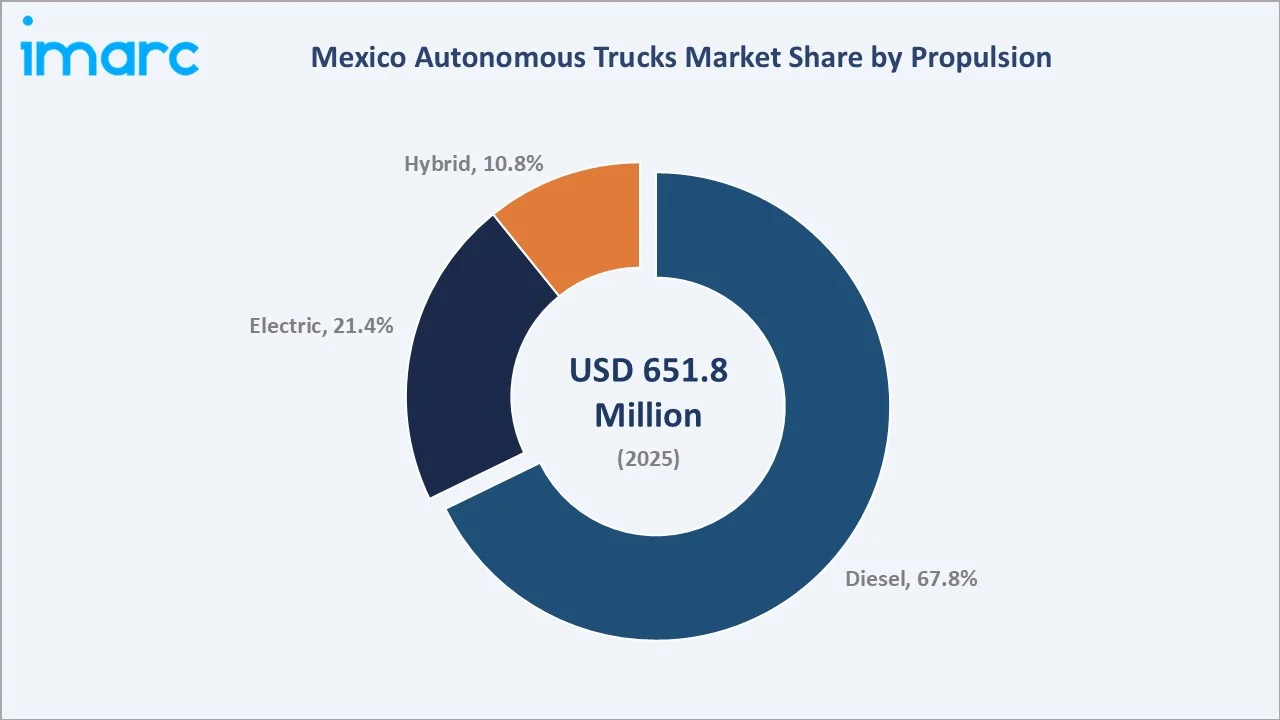

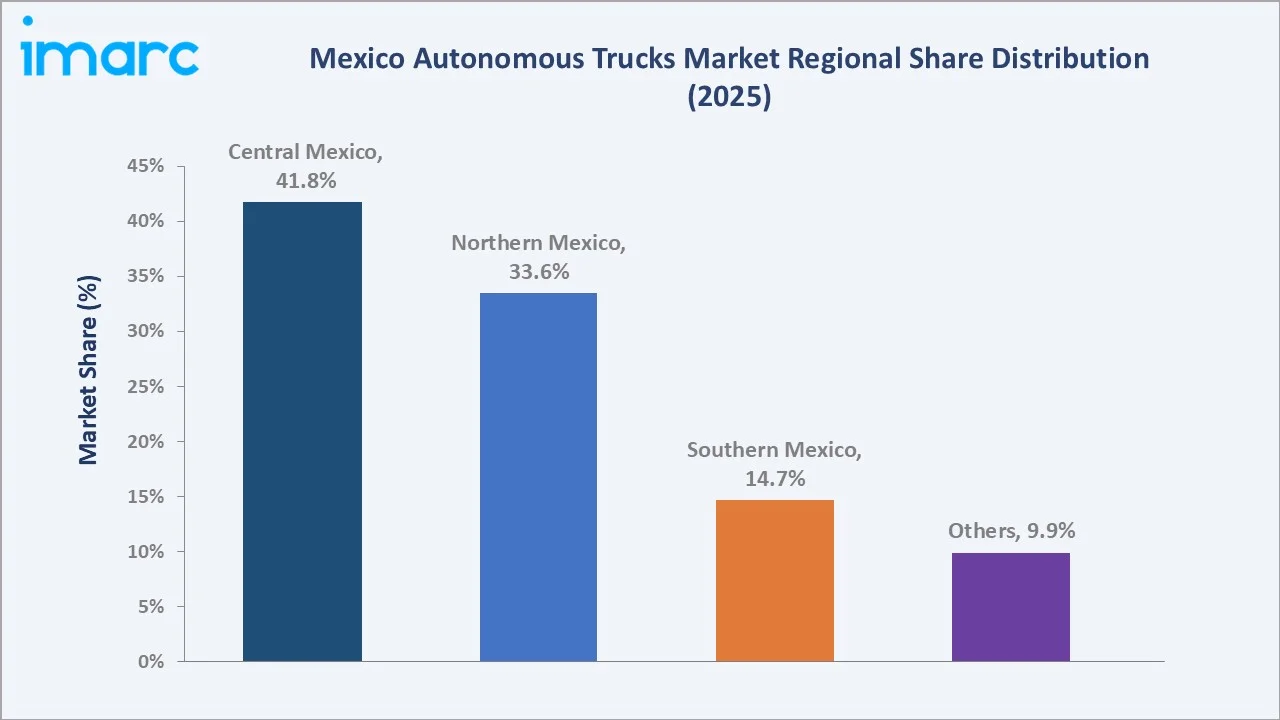

The Mexico autonomous trucks market reached USD 651.8 Million in 2025 and is projected to reach USD 1,551.8 Million by 2034, growing at a CAGR of 10.12% during 2026-2034. The market is driven by the growing need for safer, more efficient, and cost-effective freight movement across long-haul logistics corridors. Mexico produced 14,543 heavy-duty trucks and buses in May 2026, comprising 14,117 cargo trucks and tractors and 426 passenger buses. This strong production base supports the autonomous trucks market by creating a scalable platform for integrating ADAS, sensors, telematics, and autonomous driving systems into locally produced commercial vehicles. L2 & L3 lead level of autonomy at 48.6%. Diesel leads propulsion at 67.8%. Central Mexico leads at 41.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 651.8 Million |

|

Forecast Market Size (2034) |

USD 1,551.8 Million |

|

CAGR (2026-2034) |

10.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Level of Autonomy |

L2 & L3 (48.6%, 2025) |

|

Dominant Propulsion |

Diesel (67.8%, 2025) |

|

Leading Region |

Central Mexico (41.8%, 2025) |

The Mexico autonomous trucks market grew from USD 402.5 Million in 2020 to USD 651.8 Million in 2025, reflecting rising interest in automated freight technologies. It is projected to reach USD 1,055.5 Million by 2030 as logistics fleets adopt ADAS, telematics, and semi-autonomous driving systems. By 2034, the market is forecast to attain USD 1,551.8 Million, supported by cross-border trade, e-commerce logistics, fleet modernization, and demand for safer long-haul transport.

To get more information on this market, Request Sample

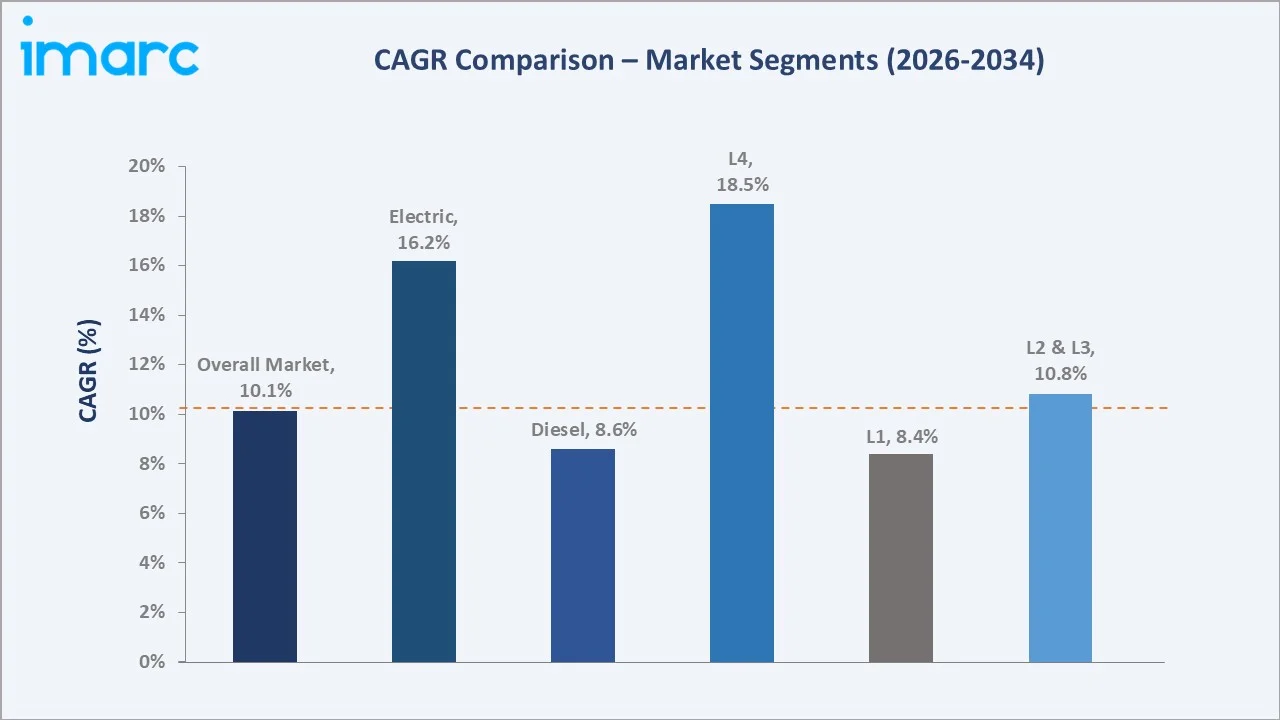

L4 grows fastest at ~18.5% CAGR through corridor pilots and cross-border automation. Electric propulsion grows at ~16.2% CAGR through nearshoring EV fleet adoption. L2 & L3 grow at ~10.8% CAGR as ADAS becomes standard equipment across Mexico fleets.

Executive Summary

Mexico autonomous trucks market is moving from early pilots toward fleet-level commercialization. Growth is supported by cross-border freight intensity, rising logistics automation, and the need to improve road safety and driver productivity. Heavy-duty vehicle production capacity gives Mexico a strong base for integrating ADAS, telematics, sensors, and AI navigation systems. Adoption is expected to strengthen across long-haul cargo, industrial logistics, and e-commerce distribution corridors. Overall, autonomous trucking is becoming a strategic tool for modernizing Mexico’s freight ecosystem. L2 & L3 at 48.6% leads through the ADAS-equipped fleet. Diesel at 67.8% leads through the legacy Mexico fleet. Central Mexico leads regionally at 41.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Level of Autonomy |

L2 & L3 - 48.6% share (2025) |

|

Dominant Propulsion |

Diesel - 67.8% market share (2025) |

|

Leading Region |

Central Mexico - 41.8% share (2025) |

|

Market Opportunity |

L4 Mexico highway corridor pilots; electric autonomous truck nearshoring; port drayage L4 automation; Mining L4 off-road; V2X 5G corridor deployment |

Key Analytical Observations Supporting The Above Data:

- L2 & L3 at 48.6%: The L2 & L3 segment is dominant as these automation levels are commercially viable, easier to deploy, and already integrated through ADAS, adaptive cruise control, lane-keeping, and collision avoidance systems. They offer safety and efficiency gains without requiring full regulatory readiness for driverless trucks.

- Diesel at 67.8%: The diesel segment dominates as heavy-duty freight transportation is heavily reliant on diesel-powered fleets due to their superior range, payload capacity, and established refueling infrastructure. Most autonomous driving technologies are currently being deployed on existing diesel truck platforms, accelerating their adoption.

- Central Mexico at 41.8%: Central Mexico dominates due to its strong logistics corridors, dense industrial clusters, and proximity to major manufacturing and distribution hubs. The region’s freight movement across automotive, retail, e-commerce, and cross-border supply chains supports faster adoption of ADAS-enabled and semi-autonomous trucking solutions.

Mexico Autonomous Trucks Market Overview

The Mexico autonomous trucks market encompasses self-driving and semi-autonomous heavy-duty vehicles equipped with ADAS, sensors, radar, LiDAR, cameras, telematics, and AI-based navigation systems. It includes automation levels ranging from driver-assistance features to higher autonomous capabilities for freight movement. The market covers diesel, electric, and hybrid truck platforms used in long-haul logistics, industrial transport, port operations, and distribution networks. It also includes supporting software, fleet management systems, connectivity infrastructure, and aftermarket integration services. Macroeconomic factors include rising industrial output, expanding cross-border trade with the US, growth in logistics and e-commerce activities, and increasing investments in transportation infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

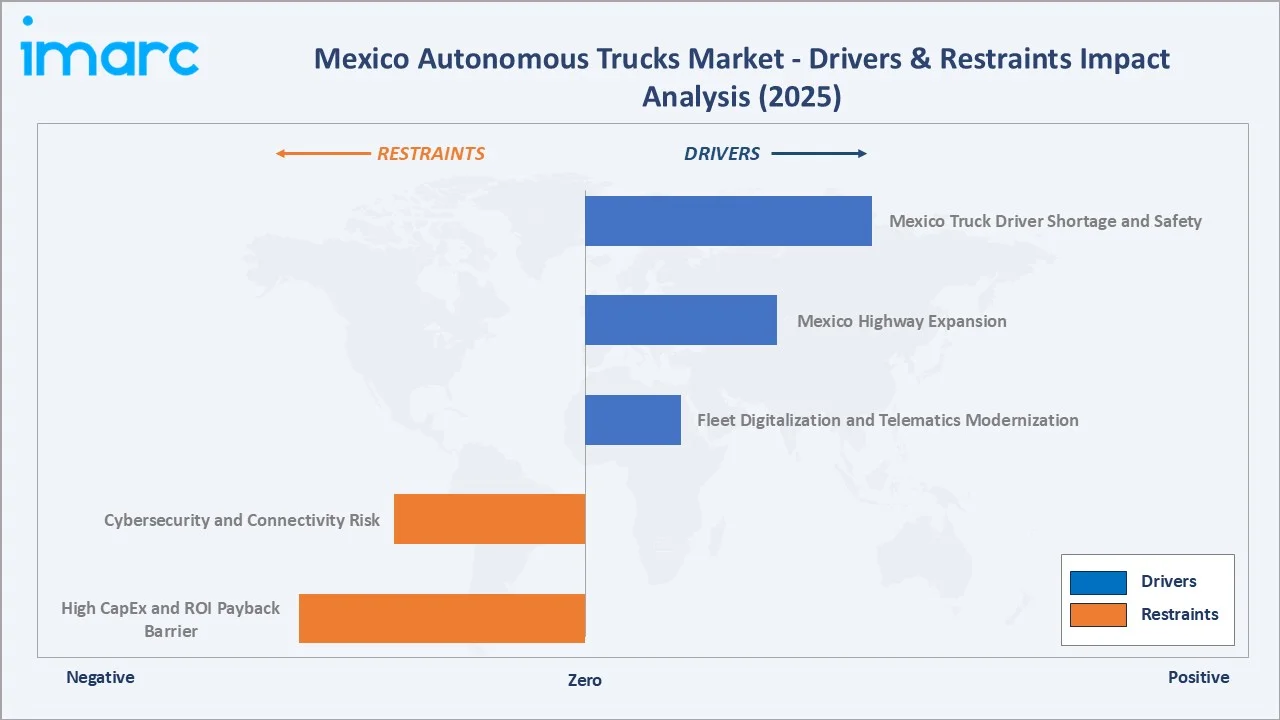

Market Drivers

- Mexico Truck Driver Shortage and Safety: Mexico currently faces a shortage of approximately 96,000 truck drivers. Logistics operators are increasingly adopting L2 and L3 autonomous systems to reduce dependence on scarce drivers, improve fleet utilization, and address rising labor costs. Advanced driver-assistance features such as adaptive cruise control, lane-keeping assistance, and collision avoidance systems help reduce accident risks on long-haul freight routes. As freight demand continues to grow, autonomous trucks are becoming a strategic solution for enhancing safety, operational efficiency, and supply chain reliability across Mexico.

- Mexico Highway Expansion: The Government of Mexico, through the Ministry of Infrastructure, Communications and Transportation (SICT), stated that MXN 69.299 billion was invested for 2026 to upgrade national highway infrastructure. SICT head Jesús Esteva Medina also announced that MXN 5.999 billion was directed toward building 388 artisanal roads, covering 888 kilometers across 18 states. Investments in highways, bypasses, and cross-border transport routes enable smoother deployment of autonomous driving technologies on long-haul freight networks. Better infrastructure supports the reliable operation of sensors, cameras, and vehicle-to-infrastructure systems while reducing operational disruptions. As freight volumes grow, modern highway networks are accelerating fleet modernization and increasing the commercial viability of autonomous trucks in Mexico.

- Fleet Digitalization and Telematics Modernization: Fleet digitalization and telematics modernization are accelerating the adoption of autonomous trucks across Mexico's freight sector. Logistics operators are increasingly deploying GPS tracking, real-time fleet monitoring, predictive maintenance, and connected vehicle platforms to improve efficiency and reduce operating costs. These digital systems generate the data infrastructure required for autonomous navigation, route optimization, and remote fleet management. As fleets become more connected and data-driven, the transition toward higher levels of vehicle automation becomes faster and more economically viable.

Market Restraints

- Cybersecurity and Connectivity Risk: Cybersecurity and connectivity risk are hampering the market as connected trucks depend on GPS, telematics, sensors, cloud platforms, and vehicle-to-infrastructure communication. Any cyberattack, signal disruption, data breach, or software vulnerability can affect vehicle safety, routing, and fleet operations. Limited network reliability in some corridors may also restrict real-time monitoring and remote diagnostics. These risks increase compliance, insurance, and technology costs, slowing large-scale fleet adoption.

- High CapEx and ROI Payback Barrier: High CapEx and ROI payback barriers are hampering the market as autonomous systems require costly sensors, cameras, radar, LiDAR, computing units, telematics platforms, and software integration. Fleet operators may hesitate to invest when payback depends on fuel savings, labor optimization, lower accident rates, and higher asset utilization over several years. Smaller logistics firms face greater difficulty financing these upgrades, limiting adoption beyond large fleets. Uncertainty around regulations, infrastructure readiness, and maintenance costs further delays large-scale deployment.

Market Opportunities

- Autonomous Freight Corridors and Cross-Border Logistics: Autonomous freight corridors and cross-border logistics supporting safer and more efficient movement of goods across key trade routes with the US. High freight volumes between manufacturing hubs, ports, warehouses, and border crossings make long-haul routes suitable for semi-autonomous truck deployment. US land borders with Canada and Mexico continue to support more than USD 1 Trillion in annual cross-border trade. In 2025, freight movement between the US and Mexico reached USD 872.8 Billion, increasing 3.9% compared with 2024. Dedicated or well-mapped corridors can improve route predictability, reduce driver fatigue, and optimize fleet utilization. As Mexico strengthens its highway and logistics infrastructure, autonomous freight corridors can become an important platform for commercial-scale adoption.

- Electric Autonomous Truck Deployment: Electric autonomous truck deployment combining automation with lower-emission freight transport. As logistics companies seek to reduce fuel costs and meet sustainability targets, electric trucks equipped with ADAS and autonomous systems can improve both operating efficiency and environmental performance. These vehicles are especially attractive for urban delivery, port logistics, and fixed-route distribution, where charging and route planning are easier to manage. Growing investment in fleet electrification and smart mobility infrastructure can further support the adoption of electric autonomous trucks across Mexico.

Market Challenges

- Public Acceptance and Trust Concerns: Public acceptance and trust concerns challenge the market as fleet operators, drivers, regulators, and the public may be cautious about sharing roads with self-driving heavy vehicles. Concerns around safety, accident liability, job displacement, and system reliability can slow regulatory approvals and commercial deployment. Any high-profile malfunction or crash could further weaken confidence in autonomous trucking technologies. Building trust will require transparent testing, strong safety records, driver training, and clear communication on how autonomous systems improve road safety and logistics efficiency.

- Data Privacy and Vehicle Software Security Issues: Data privacy and vehicle software security issues challenge the market as connected trucks continuously collect and transmit fleet, route, driver, cargo, and operational data. Weak software protection can expose fleets to hacking, data theft, unauthorized vehicle access, or manipulation of navigation and control systems. This creates safety, liability, and compliance concerns for logistics operators and technology providers. As autonomous trucks rely on cloud platforms, OTA updates, and telematics, strong encryption, secure software architecture, and regular cybersecurity testing become essential for market adoption.

Emerging Market Trends

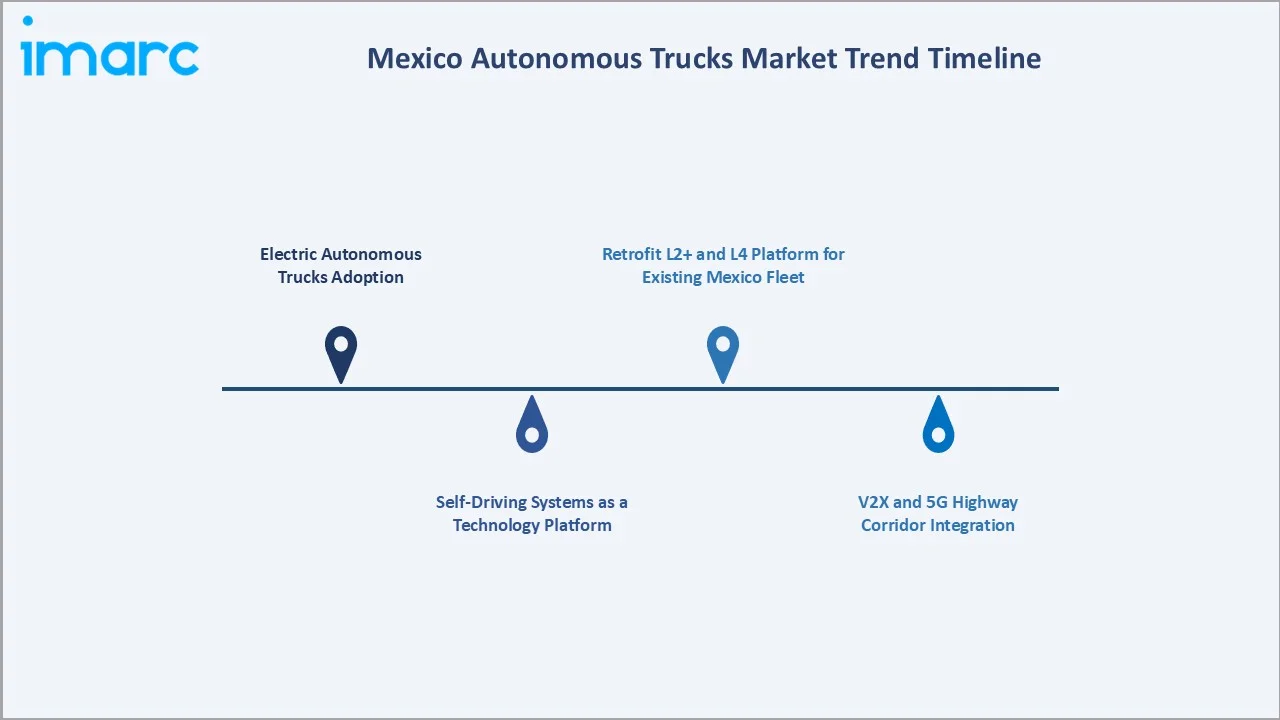

1. Electric Autonomous Trucks Adoption

Electric autonomous truck adoption is emerging as fleet operators look to combine automation with lower-emission logistics. Electric platforms paired with ADAS, telematics, AI routing, and autonomous driving systems can reduce fuel dependence and improve operating efficiency. Adoption is likely to grow first in fixed-route freight, port logistics, industrial zones, and urban distribution, where charging infrastructure can be planned. As sustainability goals and fleet modernization accelerate, electric autonomous trucks are becoming an important next-generation freight solution.

2. Self-Driving Systems as a Technology Platform

Self-driving systems as a technology platform are emerging as companies shift from selling complete vehicles to integrating autonomous driving software into existing truck fleets. In January 2025, Kodiak AI and Atlas Energy Solutions announced that Atlas completed 100 proppant deliveries using two RoboTrucks equipped with Kodiak’s self-driving system. The milestone marks the first customer-owned RoboTrucks to begin driverless commercial semi-truck operations. After initial off-road driverless deliveries in the Permian Basin, Atlas can now conduct its own autonomous deliveries across West Texas and Eastern New Mexico using Kodiak’s technology. This model allows fleet operators to upgrade trucks gradually without replacing entire fleets. It also supports partnerships between OEMs, logistics firms, and technology providers, accelerating commercial adoption across freight corridors and industrial logistics operations.

3. V2X and 5G Highway Corridor Integration

V2X and 5G highway corridor integration enables trucks to communicate with roads, traffic systems, fleet control centers, and nearby vehicles. Low-latency 5G connectivity supports real-time data exchange for route planning, hazard alerts, platooning, and remote monitoring. As Mexico upgrades highways and logistics corridors, connected infrastructure can improve the safety and reliability of autonomous truck operations. This trend is expected to support the gradual deployment of higher autonomy levels on long-haul and cross-border freight routes.

4. Retrofit L2+ and L4 Platform for Existing Mexico Fleet

Retrofit L2+ and L4 platforms for existing Mexico fleets are emerging as operators seek automation benefits without replacing entire truck fleets. Retrofit kits allow existing diesel and electric trucks to be upgraded with ADAS, sensors, cameras, radar, telematics, AI software, and autonomous control modules. L2+ systems support near-term safety and driver-assistance improvements, while L4 platforms can be tested on controlled routes, ports, mines, and industrial corridors. This trend lowers adoption barriers, extends fleet asset life, and accelerates gradual autonomous truck deployment in Mexico.

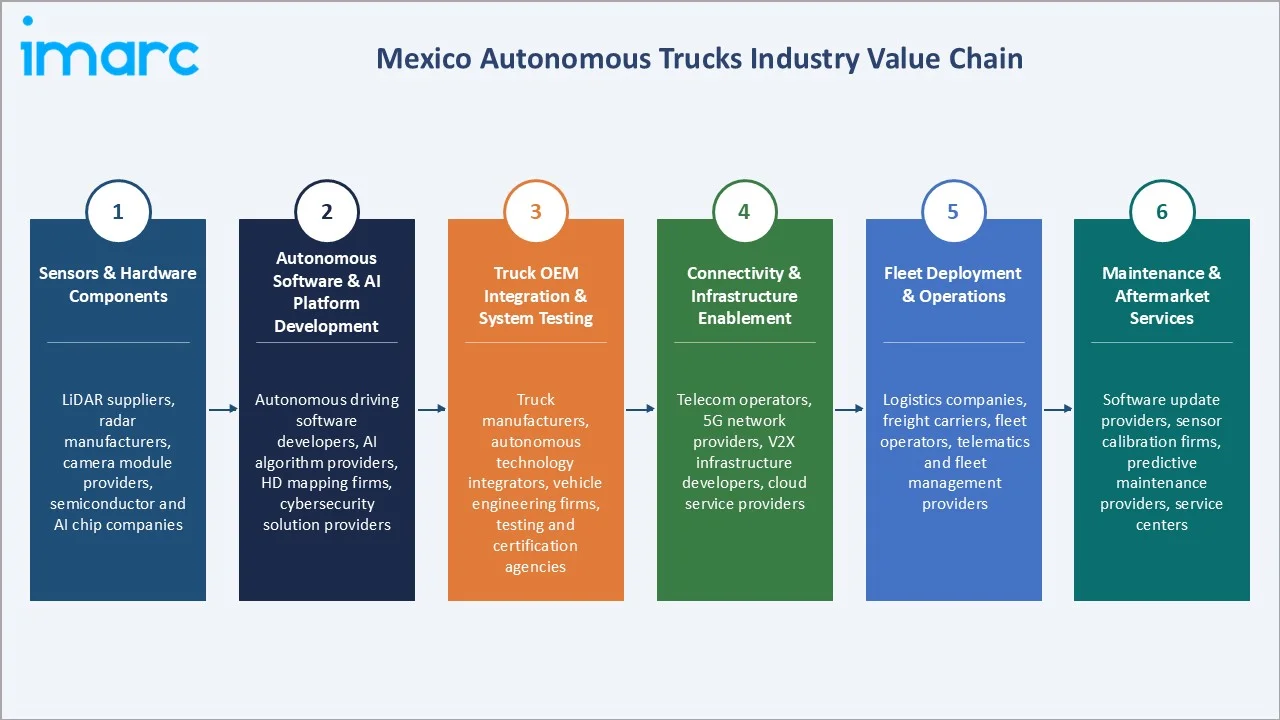

Industry Value Chain Analysis

Mexico autonomous trucks value chain integrates sensors & hardware components, autonomous software & AI platform development, truck OEM integration & system testing, connectivity & infrastructure enablement, fleet deployment & operations, and maintenance & aftermarket services.

|

Stage |

Key Participants |

|

Sensors & Hardware Components |

LiDAR suppliers, radar manufacturers, camera module providers, semiconductor and AI chip companies |

|

Autonomous Software & AI Platform Development |

Autonomous driving software developers, AI algorithm providers, HD mapping firms, cybersecurity solution providers |

|

Truck OEM Integration & System Testing |

Truck manufacturers, autonomous technology integrators, vehicle engineering firms, testing and certification agencies |

|

Connectivity & Infrastructure Enablement |

Telecom operators, 5G network providers, V2X infrastructure developers, cloud service providers |

|

Fleet Deployment & Operations |

Logistics companies, freight carriers, fleet operators, telematics and fleet management providers |

|

Maintenance & Aftermarket Services |

Software update providers, sensor calibration firms, predictive maintenance providers, service centers |

The autonomous software and AI platform development stage is the most value-added stage. It controls core vehicle intelligence, including perception, decision-making, route optimization, HD mapping, and safety validation. This stage also creates recurring revenue through software licensing, updates, cybersecurity, analytics, and fleet management services.

Technology Landscape in the Mexico Autonomous Trucks Industry

Sensor and Perception Technology

Sensor and perception technology enable vehicles to detect, classify, and respond to surrounding road conditions in real time. Advanced combinations of LiDAR, radar, cameras, ultrasonic sensors, and AI-based perception software improve object recognition, lane detection, obstacle avoidance, and collision prevention. These technologies are critical for operating autonomous trucks safely across highways, industrial zones, and cross-border freight corridors. As sensor accuracy improves and costs decline, perception systems are becoming a foundational element of large-scale autonomous truck deployment in Mexico.

Vehicle-to-Everything (V2X) Communication Technology

Vehicle-to-Everything (V2X) communication technology enables real-time communication between trucks, infrastructure, traffic systems, and other vehicles. V2X enhances situational awareness through instant sharing of traffic conditions, road hazards, weather updates, and route information. Combined with 5G connectivity, it supports safer autonomous driving, platooning, and more efficient freight operations across major logistics corridors. As Mexico modernizes its transportation infrastructure, V2X is becoming a critical enabler of scalable and reliable autonomous trucking ecosystems.

Smart Infrastructure and Connected Highway Technologies

Smart infrastructure and connected highway technologies enable seamless interaction between vehicles and transportation networks. Intelligent traffic systems, connected road sensors, digital signage, smart tolling, and roadside communication units provide real-time information on traffic flow, road conditions, and potential hazards. These technologies improve route optimization, operational efficiency, and autonomous driving safety across major freight corridors. As Mexico expands smart transportation investments, connected highways will play a critical role in supporting large-scale deployment of autonomous trucking solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Level of Autonomy |

L2 and L3 |

48.6% |

2025 |

|

Propulsion |

Diesel |

67.8% |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Sensor Type |

🔒 |

🔒 |

2025 |

|

ADAS Feature |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

41.8% |

2025 |

By Level of Autonomy

L2 & L3 leads at 48.6% (2025), through ADAS-equipped trucks with adaptive cruise control (ACC), lane keep assist, automatic emergency braking, blind spot monitoring, and partial highway autopilot (L3), and International LT ADAS in Mexico fleet.

To access detailed market analysis, Request Sample

L1 at 32.4% reflects NOM-mandatory ADAS features across Mexico's broad commercial truck fleet. L4 at 14.3% grows fastest at ~18.5% CAGR. L5 at 4.7% reflects dedicated port, mine, and terminal driverless pilot deployments.

By Propulsion

Diesel leads at 67.8% (2025), due to its strong use in long-haul freight, heavy payload transport, and cross-border logistics. Existing diesel refueling infrastructure and large installed truck fleets support faster deployment of autonomous and ADAS technologies. Most near-term autonomous truck retrofits are expected to be built around diesel platforms.

Electric at 21.4% grows fastest at ~16.2% CAGR, gaining momentum as logistics firms seek lower-emission and lower fuel-cost freight solutions. Electric autonomous trucks are especially suitable for fixed-route delivery, port logistics, urban distribution, and industrial corridors where charging infrastructure can be planned efficiently. Hybrid at 10.8% reflects diesel-electric hybrid in regional and urban distribution routes through hybrid offerings.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico Autonomous Trucks Market Drivers & Characteristics |

|

Central Mexico |

41.8% |

Supported by dense manufacturing clusters, major logistics hubs, high freight traffic, and extensive highway connectivity linking industrial centers with domestic and export markets. |

|

Northern Mexico |

33.6% |

Driven by strong cross-border trade with the United States, concentration of automotive and industrial facilities, and growing adoption of fleet automation technologies across key freight corridors. |

|

Southern Mexico |

14.7% |

Reflects increasing infrastructure development, port connectivity projects, and rising demand for autonomous logistics solutions supporting agriculture, energy, and regional distribution networks. |

|

Others |

9.9% |

Other regions, including the Bajío industrial corridor, Yucatán Peninsula, and Pacific Coast, are expanding logistics activities, industrial investments, smart transportation initiatives, and growing freight movement across emerging economic zones. |

Central Mexico's 41.8% dominance is supported by dense manufacturing clusters, logistics hubs, and strong highway connectivity across major industrial corridors. Northern Mexico's 33.6% driven by US–Mexico cross-border freight, automotive production, and high-volume export logistics.

Southern Mexico's 14.7% gaining traction as infrastructure upgrades, port access, and regional distribution networks improve freight movement. Others at 9.9% are emerging through industrial expansion and smart mobility investments.

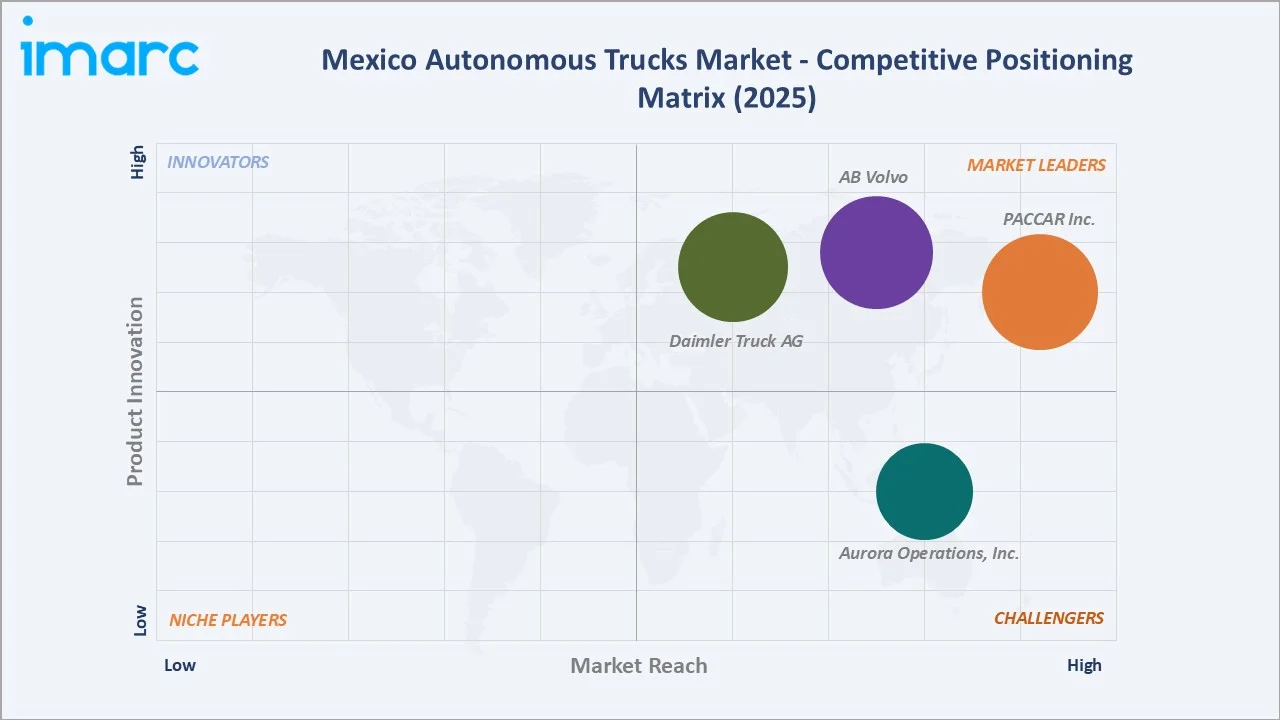

Competitive Landscape

The Mexico autonomous trucks market is moderately concentrated, with competition led by global truck OEMs, autonomous driving technology developers, and fleet management solution providers. Major participants are focusing on Level 2+ and Level 4 autonomous platforms, AI-driven perception systems, telematics integration, and connected fleet solutions. Strategic partnerships between truck manufacturers, logistics operators, and autonomous software companies are becoming increasingly important for commercialization.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Daimler Truck AG |

Freightliner Cascadia Truck |

Market Leader |

Daimler Truck AG plays a critical, foundational role in autonomous trucking. By manufacturing the autonomous-ready Freightliner Cascadia, the company directly supplies the physical trucks for automated driving. |

|

AB Volvo |

Volvo VNL Autonomous |

Market Leader |

AB Volvo’s role in Mexico's autonomous trucking sector centers primarily on manufacturing, supply chain scale, and cross-border freight integration. While Volvo’s active driverless operations are primarily rolling out in the United States, Mexico acts as the foundational manufacturing hub that enables this ecosystem. |

|

PACCAR Inc. |

T680, T880 |

Market Leader |

PACCAR’s role in Mexico’s autonomous trucking sector centers primarily on vehicle manufacturing and technology integration rather than on-road testing. Through its wholly-owned subsidiary, Kenworth Mexicana, PACCAR produces the autonomous-ready platforms that drive the company's global driverless initiatives. |

|

Aurora Operations, Inc. |

Aurora Driver |

Strong Challenger |

Aurora Operations, Inc. primarily operates within the United States, forming the foundation for self-driving freight hauling. While their driverless trucks do not currently cross the Mexico border on public roads, they play a critical logistical role in the Mexico-US supply chain by moving international freight along major Sunbelt corridors and border-adjacent routes. |

Companies are also investing in HD mapping, V2X connectivity, cybersecurity, and remote fleet monitoring capabilities to strengthen their market positions. As pilot deployments expand across freight corridors and industrial logistics applications, competition is expected to intensify around technology performance, safety validation, and operational scalability.

Key Company Profiles

Daimler Truck AG

Daimler Truck AG is one of the leading commercial vehicle manufacturers, offering trucks, buses, and mobility solutions through brands such as Mercedes-Benz Trucks and Freightliner. The company is a prominent participant in the autonomous trucking ecosystem through advanced driver assistance systems, connected vehicle technologies, and autonomous driving development programs. In Mexico, Daimler benefits from a strong manufacturing, distribution, and service network that supports freight transportation and fleet modernization.

- Key Products: Freightliner Cascadia Truck.

- Recent Developments: In April 2025, Daimler Truck North America began supplying its newest flagship on-highway trucks to Torc Robotics’ autonomous testing fleet. Built on the fifth-generation Freightliner Cascadia, the autonomous-ready trucks include redundant braking and steering systems and are designed for future series production. Alongside testing in New Mexico, Texas, and Arizona, the vehicles will also run autonomously on a new Texas route between Laredo and Dallas.

- Strategic Focus: Advancing autonomous freight transportation through the development of Level 2+ and Level 4 autonomous truck technologies, leveraging its partnerships with autonomous driving software providers and AI technology firms.

AB Volvo

AB Volvo is a leader in commercial vehicles, transportation solutions, and autonomous mobility technologies through its truck brands, including Volvo Trucks and Renault Trucks. The company is actively developing autonomous driving solutions for freight transport, logistics, mining, and industrial applications, supported by advanced connectivity, AI, and telematics platforms. In Mexico, Volvo participates in the heavy-duty trucking market through truck sales, fleet services, and connected transportation solutions serving logistics and industrial customers.

- Key Products: Volvo VNL Autonomous.

- Strategic Focus: Accelerating autonomous freight transportation through the integration of AI-driven autonomous driving systems, advanced safety technologies, and connected fleet solutions across its commercial vehicle portfolio.

Market Concentration Analysis

The Mexico autonomous trucks market is currently moderately concentrated, with a limited number of global truck OEMs, autonomous driving technology developers, and advanced mobility companies controlling most pilot projects and commercial deployments. Major participants such as Daimler Truck AG, AB Volvo, PACCAR Inc., and Aurora Operations, Inc. are leveraging proprietary AI, perception systems, and fleet management platforms to build competitive advantages. High technological complexity, substantial R&D requirements, safety validation costs, and regulatory barriers limit new entrants. Strategic partnerships between OEMs, logistics operators, telecommunications providers, and autonomous software firms are becoming increasingly important for market penetration. As commercialization expands across freight corridors and cross-border logistics routes, market concentration is expected to gradually decline with the entry of additional technology providers and fleet integrators.

Investment & Growth Opportunities

Highest Growth Segments

L4 (~18.5% CAGR), electric propulsion (~16.2% CAGR), Northern Mexico corridor (~15% CAGR), port drayage L4 (~17% CAGR), and Pemex and mining L4 (~12% CAGR) represent Mexico autonomous trucks highest-growth investment vectors through 2034.

Investment Themes

- Electric autonomous truck fleet: Investment is attractive as logistics operators seek lower-emission freight, reduced fuel costs, and automated fleet efficiency across fixed-route delivery, industrial corridors, and urban distribution.

- Port drayage L4 automation: Ports offer controlled, repetitive routes where L4 autonomous trucks can improve container movement, reduce turnaround time, and support safer high-volume freight operations.

Future Market Outlook (2026-2034)

Mexico's autonomous trucks market is projected to grow from USD 651.8 Million in 2025 to USD 1,551.8 Million by 2034, delivering a 10.12% CAGR over the forecast period through cross-border freight L4 automation, electric autonomous truck adoption, L4 port drayage scaling, V2X 5G highway corridor deployment, and Pemex mining L4 off-road. The market's anchor value of USD 1,055.5 Million in 2030 represents Mexico autonomous trucks at L4 commercial mainstream inflection.

Three structural forces define Mexico autonomous trucks market growth through 2034. First, rising freight volumes, expanding manufacturing activity, and growing US–Mexico cross-border trade are increasing demand for more efficient and scalable transportation solutions. Second, persistent truck driver shortages, labor costs, and safety concerns are accelerating investment in autonomous driving technologies and advanced fleet automation. Third, ongoing modernization of highways, logistics corridors, telematics networks, 5G connectivity, and smart transportation infrastructure is creating the foundation required for large-scale deployment of autonomous trucks.

Research Methodology

Primary Research

Primary research comprised interviews with fleet operators, logistics companies, truck OEMs, autonomous technology providers, and telematics vendors. It also included discussions with industry experts, transport associations, and infrastructure stakeholders to assess adoption readiness, safety concerns, investment priorities, and deployment timelines in Mexico.

Secondary Research

Secondary research encompassed analysis of company annual reports, investor presentations, government transportation publications, logistics industry databases, trade association reports, autonomous vehicle regulations, and freight transportation statistics. The research also reviewed OEM announcements, technology partnerships, pilot projects, academic studies, and industry publications to evaluate market trends, competitive dynamics, technology adoption, and long-term growth prospects.

Forecasting Models

Forecasting models used historical market sizing, freight demand trends, autonomous technology adoption curves, and fleet modernization patterns. Scenario-based modelling assessed L2/L3 adoption, L4 commercialization timelines, regulatory readiness, and infrastructure development. CAGR, bottom-up fleet penetration, and top-down macroeconomic models were triangulated to estimate growth through 2034.

Mexico Autonomous Trucks Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Levels of Autonomy Covered | L1, L2 and L3, L4, L5 |

| Propulsions Covered | Diesel, Electric, Hybrid |

| Vehicle Types Covered | Light Duty Trucks, Medium Duty Trucks, Heavy Duty Trucks |

| Applications Covered | Last Mile Delivery Trucks, Mining Trucks, Shuttles |

| Sensor Types Covered | Camera, Radar, Lidar, Ultrasonic, Others |

| ADAS Features Covered | Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Blind Spot Detection (BSD), Intelligent Park Assist (IPA), Lane Keep Assist (LKA), Traffic Jam Assist (TJA), Highway Pilot (HP) |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Daimler Truck AG, AB Volvo, PACCAR Inc., Aurora Operations Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico autonomous trucks market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico autonomous trucks market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico autonomous trucks industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Autonomous Trucks Market Report

The Mexico autonomous trucks market reached USD 651.8 Million in 2025, driven by expanding freight movement, rising US–Mexico cross-border trade, and growing demand for safer and more efficient long-haul logistics. Driver shortages, fleet digitalization, highway modernization, telematics adoption, and advancements in ADAS, AI, sensors, and autonomous navigation are further accelerating market growth.

The Mexico autonomous trucks market grows at 10.12% CAGR during 2026-2034, reaching USD 1,551.8 Million by 2034. The CAGR reflects driver shortage, highway expansion, L4 pilots, and EV transition.

L2 & L3 leads at 48.6% as they offer near-term automation benefits while keeping human drivers involved for supervision and safety. These systems are easier to deploy than fully driverless trucks and support features such as adaptive cruise control, lane keeping, collision avoidance, and automated highway driving.

Diesel leads at 67.8% as most heavy-duty freight fleets still depend on diesel trucks for long-haul range, high payload capacity, and reliable refueling access. Existing diesel platforms also make it easier for fleet operators to integrate ADAS, telematics, and autonomous driving systems without replacing entire fleets.

Central Mexico leads at 41.8% due to its dense manufacturing base, logistics hubs, and strong highway connectivity. High freight movement across automotive, retail, industrial, and distribution corridors supports faster adoption of autonomous and ADAS-enabled trucks.

Leading companies include Daimler Truck AG, AB Volvo, PACCAR Inc., Aurora Operations, Inc., among others.

The market is projected to reach approximately USD 1,055.5 Million by 2030, supported by rising freight automation and fleet modernization. Growth will be driven by ADAS adoption, telematics integration, highway upgrades, and expanding cross-border logistics demand.

Three priority investment opportunities include the deployment of autonomous freight corridors connecting major manufacturing and cross-border trade routes, expansion of electric autonomous truck fleets for sustainable logistics operations, and development of L4 autonomous solutions for ports, industrial zones, and mining applications. Additional opportunities exist in V2X infrastructure, telematics platforms, HD mapping, and fleet management software that support large-scale autonomous transportation ecosystems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)