Mexico Cheese Market Size, Share, Trends and Forecast by Source, Type, Product, Format, Distribution Channel, and Region, 2026-2034

Mexico Cheese Market Size, Share, Trends & Forecast (2026-2034)

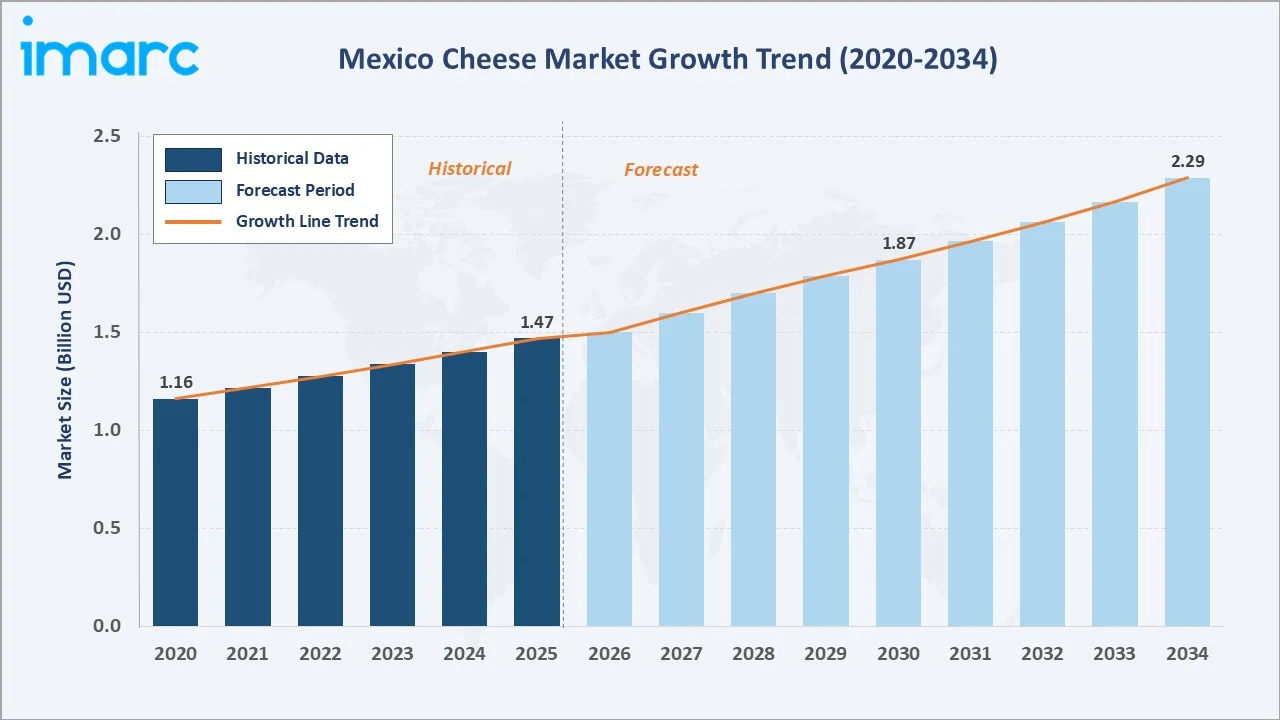

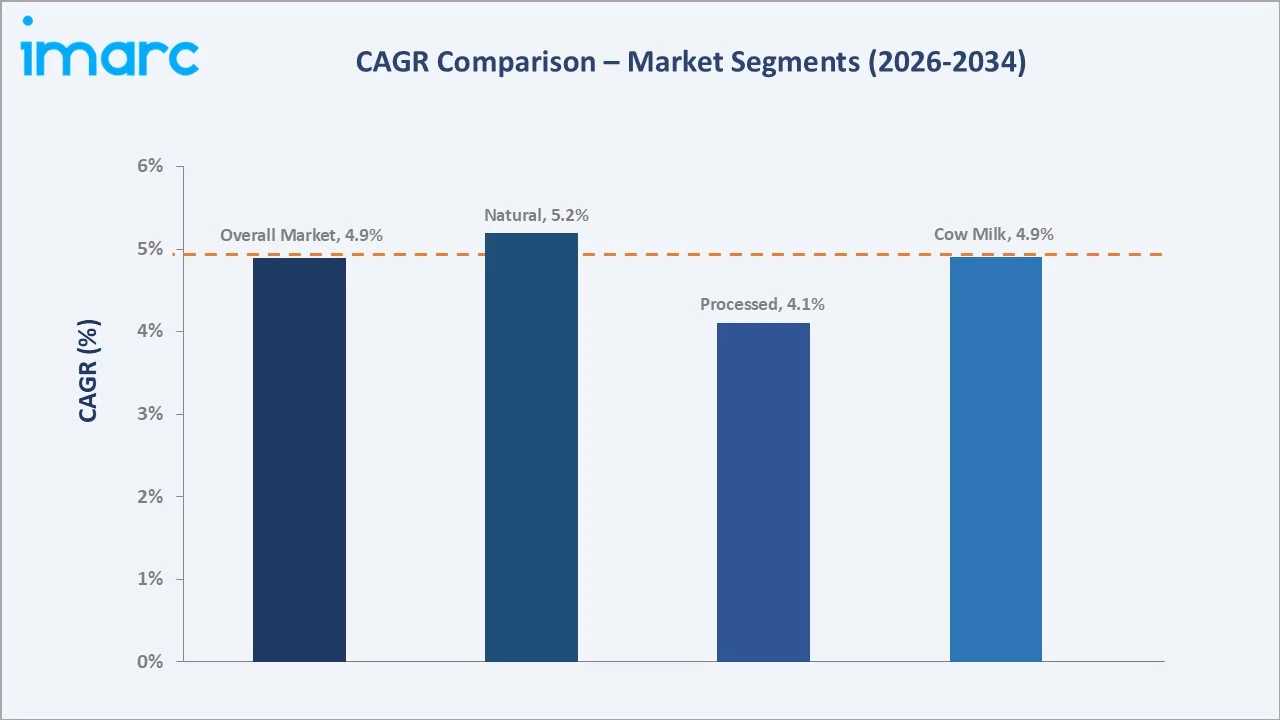

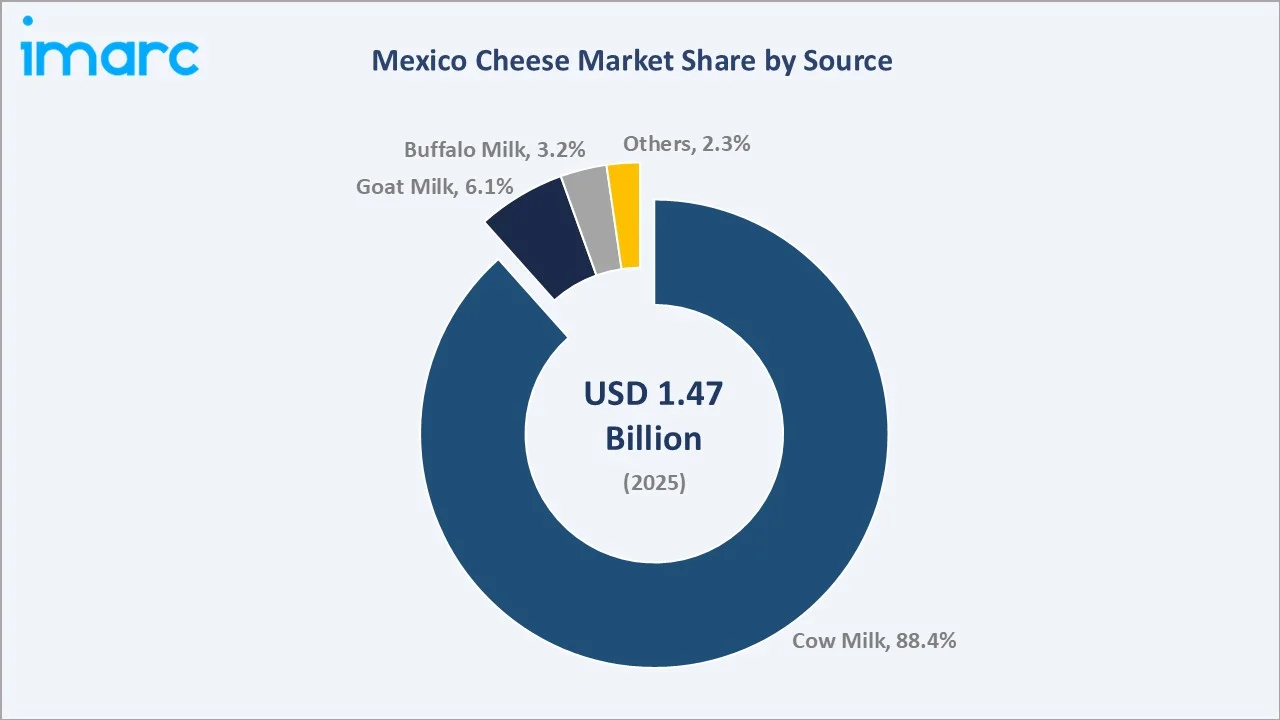

The Mexico cheese market reached USD 1.47 Billion in 2025 and is projected to reach USD 2.29 Billion by 2034, growing at a CAGR of 4.89% during 2026-2034. The market is driven by rising consumer demand for traditional and artisanal cheeses, increasing disposable income, expanding retail and foodservice sectors, and widespread influence of international cheese varieties on local tastes.

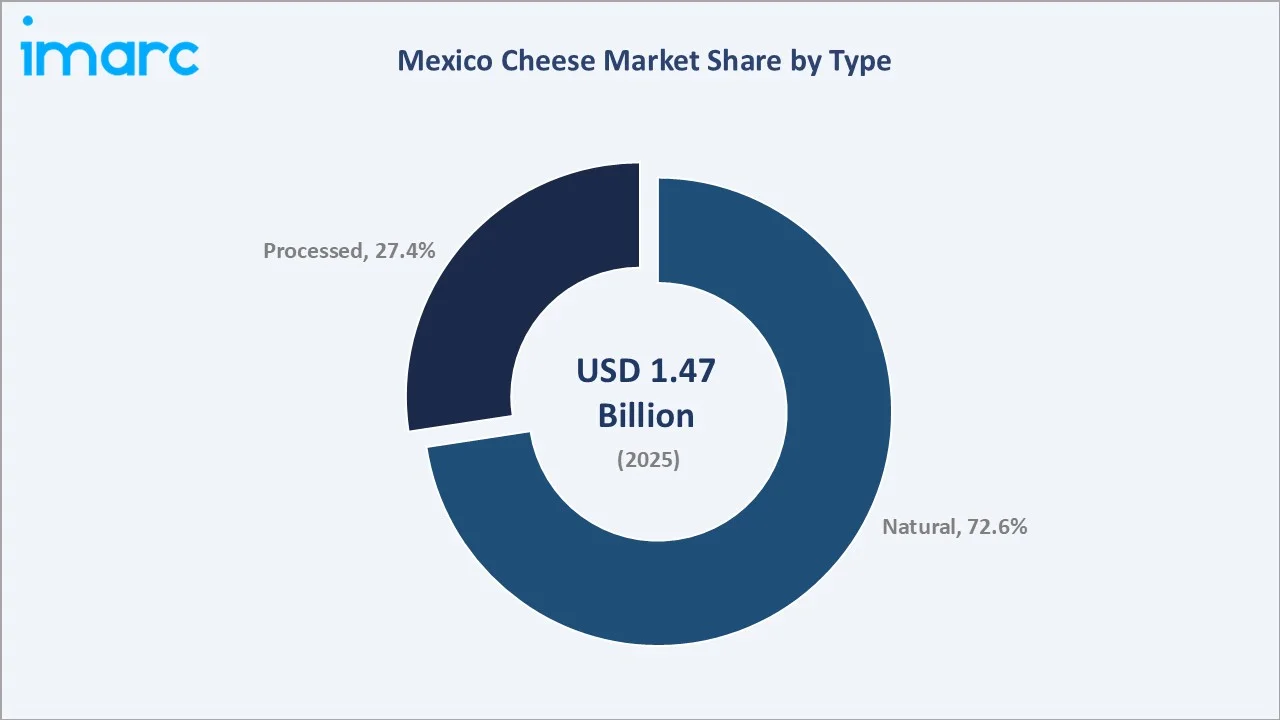

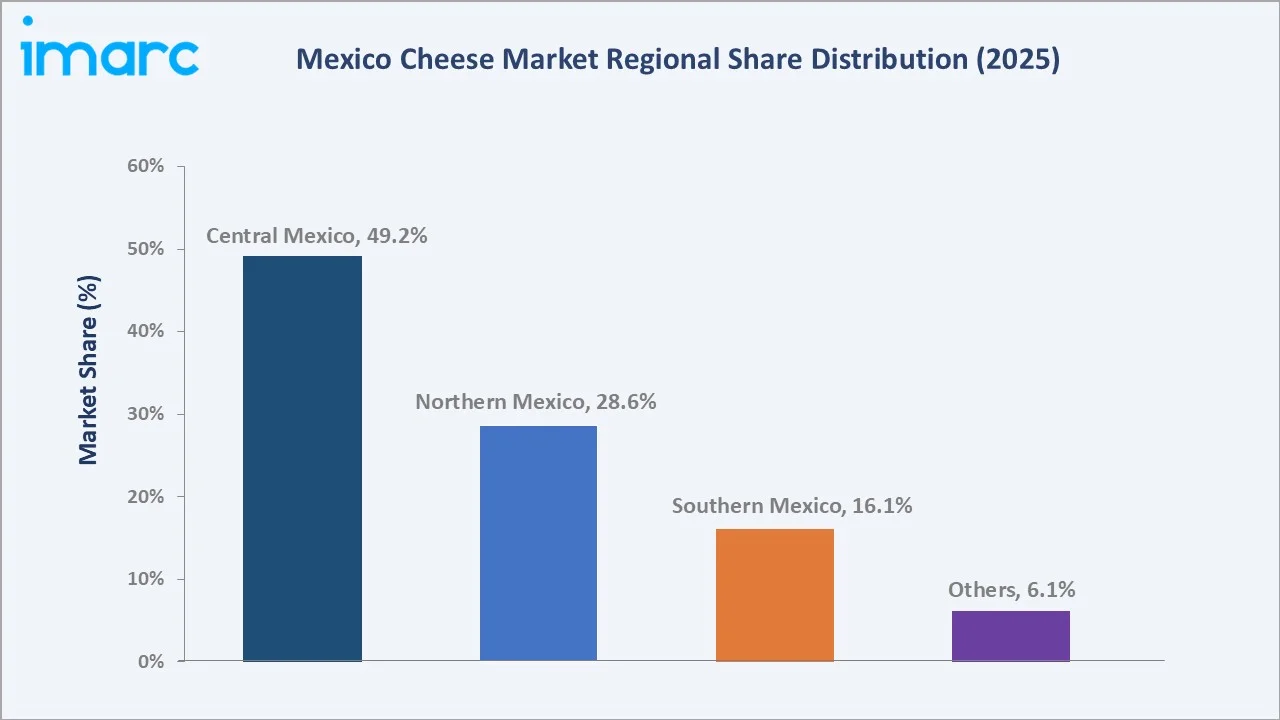

Natural cheese dominates at 72.6%. Cow milk leads sourcing at 88.4%. Central Mexico commands 49.2% of the market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.47 Billion |

|

Forecast Market Size (2034) |

USD 2.29 Billion |

|

CAGR (2026-2034) |

4.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Natural (72.6%, 2025) |

|

Dominant Source |

Cow Milk (88.4%, 2025) |

|

Leading Region |

Central Mexico (49.2%, 2025) |

The market expanded from USD 1.16 Billion in 2020 to USD 1.47 Billion in 2025 - growing consistently over five years - anchored at USD 1.87 Billion in 2030 and forecast to reach USD 2.29 Billion by 2034. Mexico's strong dairy farming tradition and growing urban middle class underpin steady long-term demand growth, while premiumization of traditional varieties and expansion of the foodservice sector accelerate market development.

To get more information on this market, Request Sample

Natural cheese at 72.6% grows through rising premiumization of traditional Mexican varieties and premium artisanal production. Cow milk at 88.4% reflects the country's established bovine dairy farming base. Central Mexico at 49.2% grows through its concentration of dairy processing infrastructure and Mexico City's large consumer market.

Executive Summary

The Mexico cheese market reached USD 1.47 Billion in 2025, representing one of Latin America's most culturally entrenched dairy product categories driven by Mexico's deep traditional cheese heritage and evolving consumer preferences toward premium and international varieties. The EV traction motor is the defining powertrain component of the BEV. The market is projected to reach USD 2.29 Billion by 2034.

Natural cheese at 72.6% dominates through widespread integration in traditional Mexican cuisine, regional heritage production, and the broad consumer base for Oaxaca, Panela, Cotija, Manchego, and Chihuahua varieties. Cow milk at 88.4% leads through Mexico's established dairy cattle farming base and existing industrial processing infrastructure. Central Mexico at 49.2% leads through industrial processing concentration, population density, and retail infrastructure.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Natural - 72.6% share (2025) |

|

Dominant Source |

Cow Milk - 88.4% market share (2025) |

|

Leading Region |

Central Mexico - 49.2% market share (2025) |

|

Market Opportunity |

Premium artisanal cheese; plant-based alternatives; export growth; international variety expansion |

Key Analytical Observations Supporting the Above Data:

- Natural at 72.6%: Natural cheese dominates as it encompasses traditional Mexican varieties that are integral to Mexican cuisine and household consumption, supported by deep cultural roots and widespread availability across all retail formats and price points.

- Cow Milk at 88.4%: Cow milk dominates cheese sourcing due to the widespread availability of bovine dairy farming across major Mexican dairy states and established processing infrastructure built around cow milk cheese production.

- Central Mexico at 49.2%: Central Mexico leads due to its concentration of major dairy processors, proximity to Mexico City's vast consumer base, well-developed cold chain infrastructure, and the presence of leading cheese manufacturers including Grupo Lala S.A.B. de C.V. and Sigma Alimentos S.A. de C.V.

Mexico Cheese Market Overview

The Mexico cheese market encompasses the production, processing, distribution, and retail sale of all cheese varieties consumed within Mexico, including traditional Mexican cheeses, processed cheese products, and imported international varieties spanning natural and processed cheese categories across all distribution channels and consumer segments.

The ecosystem integrates dairy farmers, raw milk processors, cheese manufacturers, cold chain logistics providers, retail distributors, foodservice operators, and regulatory bodies. Macroeconomic factors include rising urbanization, growing middle-class income, foodservice expansion, and increasing consumer exposure to international culinary trends through travel and digital media.

Market Dynamics

To evaluate market opportunities, Request Sample

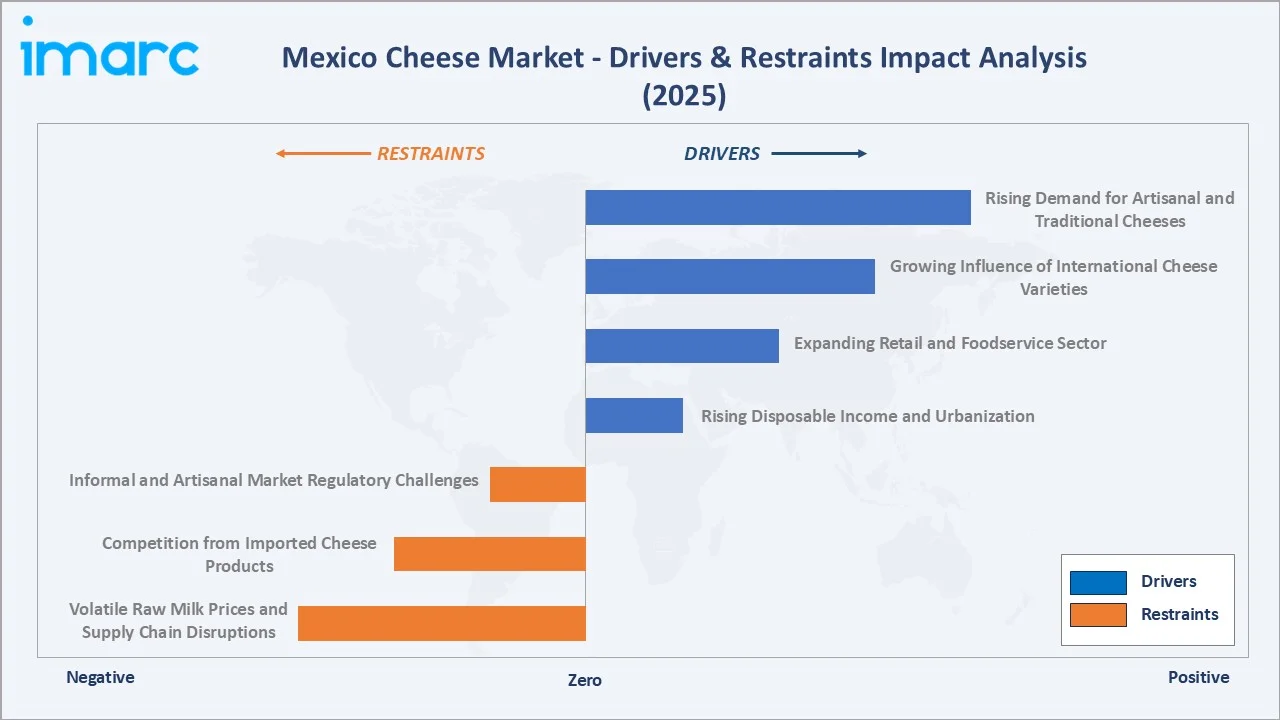

Market Drivers

- Rising Demand for Artisanal and Traditional Cheeses: Mexico's consumers increasingly prefer artisanal and traditional cheese varieties for their authentic flavors, cultural significance, and high quality. Traditional quesillo from Oaxaca, known for its distinctive microbiota and sensory attributes, is gaining domestic and export recognition. Retail and specialty stores have expanded their artisanal cheese offerings, boosting market penetration and premium pricing power for producers of heritage varieties.

- Growing Influence of International Cheese Varieties: Consumers are increasingly accessing imported cheeses such as Gouda, Brie, Cheddar, and Parmesan through supermarkets, delis, and specialty stores. In 2024, the U.S. fulfilled over 85% of Mexico's cheese imports in the first half of the year. Foodservice operators, pizzerias, fast-food chains, and gourmet restaurants, are spurring demand for mozzarella, blue cheese, and Parmesan across urban centers, driving overall market breadth.

- Expanding Retail and Foodservice Sector: Mexico's organized retail sector continues expanding, with national retail sales growing. Supermarkets, hypermarkets, and specialty stores are increasing specialty cheese shelf space, while the foodservice sector recovery has driven significant volume growth in cheese consumption through restaurants, cafes, and QSR chains nationwide.

- Rising Disposable Income and Urbanization: Mexico's growing urban middle class is driving premiumization in food consumption, with consumers willing to pay higher prices for quality cheese products. Rising disposable income is enabling adoption of premium imported varieties alongside traditional domestic cheeses, expanding the overall addressable market for higher-value cheese products across metropolitan and secondary urban centers.

Market Restraints

- Volatile Raw Milk Prices and Supply Chain Disruptions: Fluctuating raw milk prices create margin pressure for cheese manufacturers, particularly smaller-scale producers. Supply chain disruptions and rising feed costs for dairy cattle periodically constrain milk availability, leading to price volatility that affects manufacturing cost structures and retail pricing competitiveness in the Mexico cheese market.

- Competition from Imported Cheese Products: The dominant presence of U.S. cheese imports, fulfilling over 85% of Mexico's import requirements, creates significant competitive pressure for domestic manufacturers. The EU-Mexico trade agreement reducing dairy tariffs is expected to intensify competition from European cheese imports, challenging domestic producers on quality and price positioning simultaneously.

- Informal and Artisanal Market Regulatory Challenges: Mexico's substantial informal artisanal cheese market creates regulatory and quality standardization challenges. Small-scale producers operating outside formal regulatory frameworks can undercut formal market prices, limit growth of organized sector participants and creating food safety concerns that affect overall market reputation and consumer confidence in artisanal categories.

Market Opportunities

- Premium Specialty and Imported Cheese Expansion: The growing appetite for diverse international cheese varieties presents significant opportunity for premium specialty cheese retailers and importers. As Mexican consumers become more exposed to global culinary trends through travel, social media, and restaurant experiences, demand for premium European and North American varieties is expected to accelerate through the forecast period.

- Plant-Based and Functional Cheese Innovation: Emerging consumer interest in plant-based diets and lactose-free alternatives opens a nascent but growing market segment for innovative cheese alternatives. As plant-based food technology improves taste and texture parity with dairy cheese, early movers in Mexico's plant-based cheese space can capture health-conscious consumer segments in urban markets.

Market Challenges

- Cold Chain Infrastructure Limitations in Southern Mexico: Inadequate cold chain infrastructure in Southern Mexico constrains cheese distribution efficiency in this region, limiting shelf-life management and increasing logistics costs. This creates barriers to market penetration for formal sector participants seeking to expand beyond Central and Northern Mexico's well-developed distribution networks.

- Price Sensitivity Limiting Premium Segment Growth: Despite rising incomes, significant portions of Mexico's consumer base remain price-sensitive, limiting the addressable market for premium and imported cheese varieties. This creates a bifurcated market structure where traditional domestic varieties dominate volume while premium segments remain relatively constrained in scale and geographic reach.

Emerging Market Trends

1. Premiumization of Traditional Mexican Cheese Varieties

Artisanal and heritage cheese varieties such as Oaxaca quesillo, aged Cotija, and Chihuahua cheese are experiencing premiumization as producers invest in quality certification, branding, and packaging. This trend is creating higher-value market segments within the traditional cheese category and enabling premium price realization for regional producers across domestic and export channels.

2. E-Commerce and Direct-to-Consumer Cheese Distribution

Online cheese retail and specialty cheese delivery services are gaining traction in Mexico's urban centers, enabling smaller artisanal producers to reach consumers directly. Digital platforms are reducing distribution barriers for niche and specialty cheese products, expanding accessible market geography beyond traditional retail coverage areas and creating new revenue streams for producers.

3. Foodservice-Driven Cheese Innovation and Diversification

Mexico's expanding foodservice sector—including fast-casual and gourmet dining—is driving innovation in cheese application and variety. Restaurant chains are introducing diverse cheese-based offerings, and fusion applications combining Mexican and international cheese varieties are expanding consumer exposure to new flavor profiles, driving broader category awareness and trial.

4. Sustainability and Traceability in Dairy Cheese Production

Growing consumer awareness of environmental sustainability and food provenance is driving demand for traceable, sustainably produced cheese. Leading manufacturers are responding with farm-to-table marketing initiatives, sustainable packaging adoption, and organic certification programs that align with evolving consumer values across health-conscious urban consumer segments.

Industry Value Chain Analysis

The Mexico cheese value chain integrates raw milk procurement, cheese manufacturing, quality testing and packaging, cold chain logistics, retail and foodservice distribution, and end consumer delivery. The value chain's commercial structure is evolving toward greater formalization and premiumization, driven by organized retail growth and foodservice sector expansion across urban and semi-urban markets.

|

Stage |

Key Participants |

|

Raw Material & Milk Sourcing |

Dairy farmers and cooperatives supplying raw cow, goat, and buffalo milk from key dairy states across Northern and Central Mexico |

|

Cheese Manufacturing |

Industrial cheese processors, regional dairies, and artisanal small-scale producers across all cheese type categories |

|

Quality Testing & Packaging |

COFEPRIS-certified quality laboratories, automated packaging lines, cold storage and modified atmosphere packaging facilities |

|

Cold Chain & Logistics |

Refrigerated transport fleet, cold storage distribution centers, and regional distribution networks across all major markets |

|

Retail & Foodservice Distribution |

Supermarkets, hypermarkets, specialty stores, QSR chains, restaurants, and wholesale distributors serving all consumer segments |

|

Aftersales & Consumer Service |

Product freshness management, consumer education on cheese varieties, and producer brand engagement with end consumers |

The raw milk sourcing tier remains the value chain's most cost-sensitive stage, with raw milk representing 60-70% of cheese manufacturing input cost. The retail distribution tier is experiencing the most rapid structural change as e-commerce and modern trade channels expand at the expense of traditional trade formats across urban Mexico.

Technology Landscape in the Mexico Cheese Industry

Automated Cheese Manufacturing Technology

Advanced automated cheese vats, precision temperature control systems, and continuous production lines are enabling Mexican industrial cheese manufacturers to improve product consistency, reduce labor costs, and increase production capacity. Leading producers like Grupo Lala S.A.B. de C.V. and Sigma Alimentos S.A. de C.V. are investing in modern manufacturing technologies to drive operational efficiency.

Modified Atmosphere Packaging (MAP) Technology

MAP technology is extending shelf life of fresh and semi-hard cheese varieties, enabling broader distribution reach and reducing waste in Mexico's distribution network. This technology is particularly important for natural cheese varieties including Oaxaca and Panela where shelf-life management directly affects product quality and retail performance across extended distribution geographies.

Cold Chain Traceability Technology

The European Union and Mexico finalized a trade agreement that removed tariffs on various EU dairy products, including cheese. This agreement is expected to increase competitive pressure on domestic producers, accelerating investment in cold chain traceability technology, IoT-enabled temperature monitoring, and digital provenance recording as key quality differentiation tools.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Natural |

72.6% |

2025 |

|

Source |

Cow Milk |

88.4% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

Format |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

49.2% |

2025 |

By Type

The natural cheese segment leads at 72.6% in 2025, driven by the deep cultural integration of traditional Mexican cheese varieties into daily consumption habits and the broad product portfolio spanning fresh, semi-hard, and aged natural cheese varieties. Natural cheese encompasses Mexico's most consumed varieties including Oaxaca, Panela, Cotija, Manchego, and Chihuahua.

To access detailed market analysis, Request Sample

Processed cheese at 27.4% captures the convenience-oriented and foodservice segments where standardized melting properties, extended shelf life, and cost efficiency are prioritized. Processed cheese is widely used in fast-food applications, institutional food service, and mass retail formats where consistency and price competitiveness drive procurement decisions across all distribution channels.

By Source

Cow milk leads at 88.4% due to Mexico's dominant dairy cattle farming base across major dairy states including Jalisco, Coahuila, Durango, Chihuahua, and Guanajuato. The established processing infrastructure built around cow milk cheese production and the wide consumer familiarity with cow milk cheese characteristics reinforce this segment's dominant position across all cheese product categories.

Goat milk cheese at 6.1% captures the artisanal and specialty premium segment, primarily in artisan production regions of Central and Southern Mexico. Buffalo milk at 3.2% represents a niche but growing segment, with mozzarella-style varieties gaining recognition in gourmet foodservice. Other sources at 2.3% include sheep milk and mixed milk varieties from artisan producers.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico Cheese Market Drivers & Characteristics |

|

Central Mexico |

49.2% |

Driven by its high population density, concentration of major industrial dairy processors, well-developed cold chain and retail infrastructure, and proximity to Mexico City's vast consumer base |

|

Northern Mexico |

28.6% |

Driven by strong dairy farming heritage, Chihuahua cheese heritage production, cross-border U.S. trade influence, and growing industrial dairy manufacturing investment across key northern states |

|

Southern Mexico |

16.1% |

Driven by rich artisanal cheese traditions including Oaxaca quesillo heritage production, growing domestic tourism demand for regional cheeses, and increasing formal sector investment in artisanal variety development |

|

Others |

6.1% |

Emerging consumption zones including Baja California, Pacific Coast, and Yucatán Peninsula with growing modern retail penetration and rising cheese consumption driven by urbanization and tourism |

Central Mexico, at 49.2%, leads through its concentration of major dairy processing facilities, Mexico City's 22 million-plus consumer metropolitan area, and the most developed supermarket and hypermarket infrastructure in the country.

Northern Mexico, at 28.6%, benefits from its rich dairy farming heritage, particularly in Chihuahua, Coahuila, and Durango, which includes traditional Chihuahua cheese production, one of Mexico's most distinctive regional varieties. U.S. cheese import flows through northern border crossing points also influence consumption patterns and variety preferences in this region.

Competitive Landscape

The Mexico cheese market competitive landscape is moderately concentrated with three distinct competitive tiers: industrial dairy conglomerates with broad cheese portfolios, regional and specialty cheese manufacturers serving specific geographic and variety niches, and international companies competing through imported cheese brands and local production operations across key categories.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Chilchota |

Cottage Cheese, Ranchero Chilchota, Panela Cheese Basket Chilchota, Durangueño Double Cream, Chilchota Asadero Cheese, Chilchota Adobera Cheese |

Market Leader |

Specialist cheese manufacturer based in the Laguna region, Mexico's key dairy production heartland, with deep regional sourcing and production expertise |

|

Danone |

Dairy and fresh cheese products |

Niche Player |

Global dairy company with consumer-health focused product positioning and strong brand equity in health-oriented dairy segments across urban Mexican consumer markets |

Key players include Chilchota, Danone, and others.

Key Company Profiles

Danone

Danone is a France-based global food and beverage company with a operating presence in Mexico, competing in the dairy and plant-based categories through a health-focused portfolio of fermented dairy products, yogurts, and fresh dairy offerings across retail and foodservice channels nationwide.

- Key Products: Activia, Danonino, Danette, and Oikos yogurt and fermented dairy products; Bonafont water; plant-based dairy alternatives under the Bye Bye Muu brand across health-oriented retail segments.

- Strategic Focus: Advancing its "Renew Danone" strategy in Mexico by strengthening dairy product portfolios, expanding plant-based alternatives, and deepening sustainability commitments through regenerative agriculture, recycled packaging initiatives, and B-Corp certification, while maintaining leadership in the yogurt and fermented dairy segments across urban Mexican consumer markets.

Chilchota

Chilchota is a Mexico-based specialist dairy company and one of Mexico's largest cheese producers, headquartered in Gómez Palacio, Durango, within the Comarca Lagunera, the country's most important milk-producing region, with a vertically integrated supply chain spanning to national and North American distribution.

- Key Products: Cottage Cheese, Ranchero Chilchota, Panela Cheese Basket Chilchota, Durangueño Double Cream, Chilchota Asadero Cheese, Chilchota Adobera Cheese, and others.

- Strategic Focus: Maintaining and expanding its position as one of Mexico's leading cheese manufacturers through vertically integrated operations across five divisions, agriculture, livestock, stables, transportation, and commercialization, broadening its multi-tier brand portfolio, and growing exports to North American market.

Market Concentration Analysis

The Mexico cheese market is moderately concentrated at the industrial manufacturer level, with the top 5-6 key players collectively accounting for approximately 55-65% of formal sector cheese production value. The informal artisanal segment represents an estimated 20-30% of total cheese production volume.

Market concentration is evolving as the EU-Mexico trade agreement introducing reduced tariffs on European dairy products intensifies import competition while also creating new distribution opportunities.

Investment & Growth Opportunities

Highest Growth Segments

Artisanal and specialty natural cheese (above-market CAGR through premium positioning), goat milk cheese (~5.8% CAGR), Southern Mexico regional cheese expansion (~5.5% CAGR), e-commerce cheese retail (~15%+ CAGR from near-zero base), plant-based cheese alternatives (~20%+ CAGR as market develops), and premium international variety distribution represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Premium Mexican cheese export development represents a significant opportunity as growing international recognition of regional varieties such as Oaxaca quesillo and aged Cotija creates export demand. The January 2025 EU-Mexico trade agreement also creates reciprocal market access opportunities for Mexican specialty cheese exports to European gourmet and specialty retail channels.

Investment Themes

- Artisanal cheese formalization and branding: Formalizing artisanal cheese production through quality certification, branding investment, and premium packaging to capture value migration from commodity to premium segments as consumer willingness to pay for authentic quality increases across Mexico's urban consumer base.

- Cold chain expansion in Southern Mexico: Investment in cold chain infrastructure in Southern Mexico to unlock Mexico's richest artisanal cheese heritage region, enabling Oaxaca and neighboring states' production potential for both domestic premium distribution and international export market development.

Future Market Outlook (2026-2034)

The Mexico cheese market is projected to grow from USD 1.47 Billion in 2025 to USD 2.29 Billion by 2034, delivering a 4.89% CAGR over the forecast period. The market's anchor value of USD 1.87 Billion in 2030 represents Mexico's cheese industry at a key commercial inflection point where premium traditional varieties and international cheese segments achieve substantial scale alongside the established mass market base.

Three structural forces define Mexico cheese market growth through 2034. The premiumization of traditional Mexican cheese varieties creates a higher per-unit value growth above volume growth as consumers increasingly pay premium prices for quality-certified artisanal versions of Oaxaca, Cotija, and Chihuahua varieties. The foodservice sector's continued expansion drives consistent volume demand across cheese types, particularly mozzarella, processed cheese, and specialty varieties used in fast-casual and gourmet dining applications. The expanding modern retail infrastructure enables broader geographic reach and specialty cheese category development, bringing premium varieties to consumers in secondary cities and semi-urban markets previously underserved by specialty cheese distribution.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including dairy processing executives, cheese retail category managers, foodservice procurement specialists, artisanal cheese producers, cold chain logistics operators, and regulatory compliance officers across Central, Northern, and Southern Mexico regions.

Secondary Research

Secondary research encompassed company annual reports and investor presentations; SAGARPA and SIAP dairy production statistics; CANILEC industry association data; ANTAD retail sales data; COFEPRIS food regulatory publications; USDA Foreign Agricultural Service Mexico dairy market reports; and Mexico dairy industry trade publications. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up consumption model: (i) per-capita cheese consumption growth by income segment; (ii) retail and foodservice channel volume projections; (iii) premium segment migration rates and average price trajectory; (iv) import penetration adjustment for EU trade agreement impact on competitive dynamics and domestic producer pricing power.

Mexico Cheese Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Cow Milk, Buffalo Milk, Goat Milk, Others |

| Types Covered | Natural, Processed |

| Products Covered | Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others |

| Formats Covered | Slices, Diced/Cubes, Shredded, Blocks, Spreads, Liquid, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Chilchota, Danone, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico cheese market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico cheese market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico cheese industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Cheese Market Report

The Mexico cheese market reached USD 1.47 Billion in 2025, driven by natural cheese dominance at 72.6%, cow milk sourcing leadership at 88.4%, and Central Mexico commanding 49.2% regional market share through its concentration of dairy processing infrastructure, population density, and consumer demand.

The Mexico cheese market grows at 4.89% CAGR during 2026-2034, reaching USD 2.29 Billion by 2034, reflecting steady urbanization, rising income-driven premiumization, expanding retail and foodservice distribution, and evolving consumer preferences for diverse cheese varieties across all regional markets.

Natural cheese leads at 72.6%, driven by the deep integration of traditional Mexican cheese varieties—including Oaxaca, Panela, Cotija, and Manchego—into daily household consumption and the established cultural heritage of artisanal cheese production across Mexico's key dairy regions in the North, Center, and South.

Cow milk dominates at 88.4% through Mexico's established bovine dairy farming base in key dairy states including Jalisco, Chihuahua, Coahuila, and Durango, supported by the established industrial processing infrastructure built around cow milk cheese manufacturing across all major cheese categories.

Central Mexico leads at 49.2% through its concentration of major industrial dairy processors, Mexico City's large consumer base, well-developed supermarket and hypermarket infrastructure, and strong cold chain logistics networks connecting cheese manufacturers to retail and foodservice distribution across the country.

Leading companies include Chilchota, Danone, and others.

The Mexico cheese market is projected to reach USD 1.87 Billion by 2030, supported by continued urbanization, foodservice sector growth, expanding modern retail cheese categories, and the gradual premiumization of traditional Mexican cheese varieties toward higher-value artisanal and specialty product formats across all major distribution channels.

Three priority investment opportunities: artisanal cheese formalization and branding to capture premium segment value migration; cold chain infrastructure expansion in Southern Mexico to unlock Oaxaca region's cheese production potential; and plant-based cheese alternative development to serve Mexico's growing health-conscious and lactose-intolerant urban consumer segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)