Mexico Digital Signature Market Size, Share, Trends and Forecast by Component, Deployment Model, Enterprise Size, Industry Vertical, and Region, 2026-2034

Mexico Digital Signature Market Size, Share, Trends & Forecast (2026-2034)

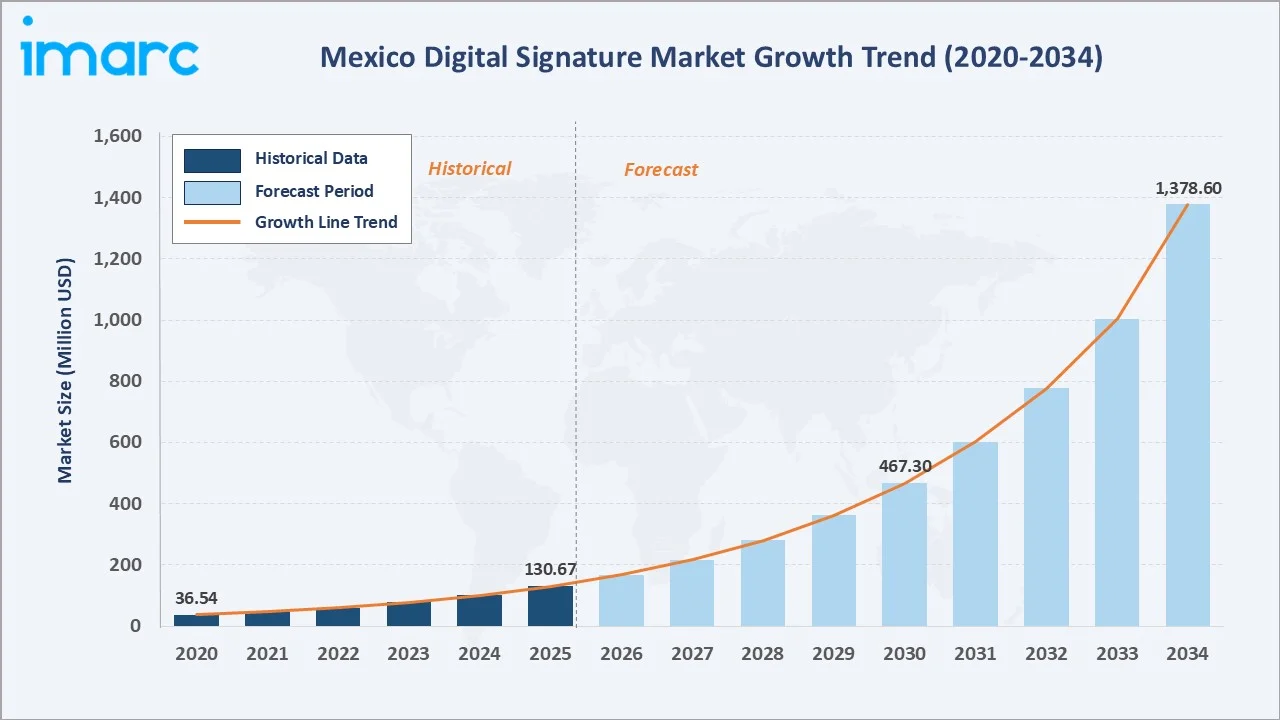

The Mexico digital signature market size reached USD 130.67 Million in 2025 and is projected to reach USD 1,378.60 Million by 2034, growing at a CAGR of 29.03% during 2026-2034. Increasing government digitalization initiatives, growing e-commerce adoption, demand for enhanced security in electronic transactions, and rising demand for paperless workflows are driving the market.

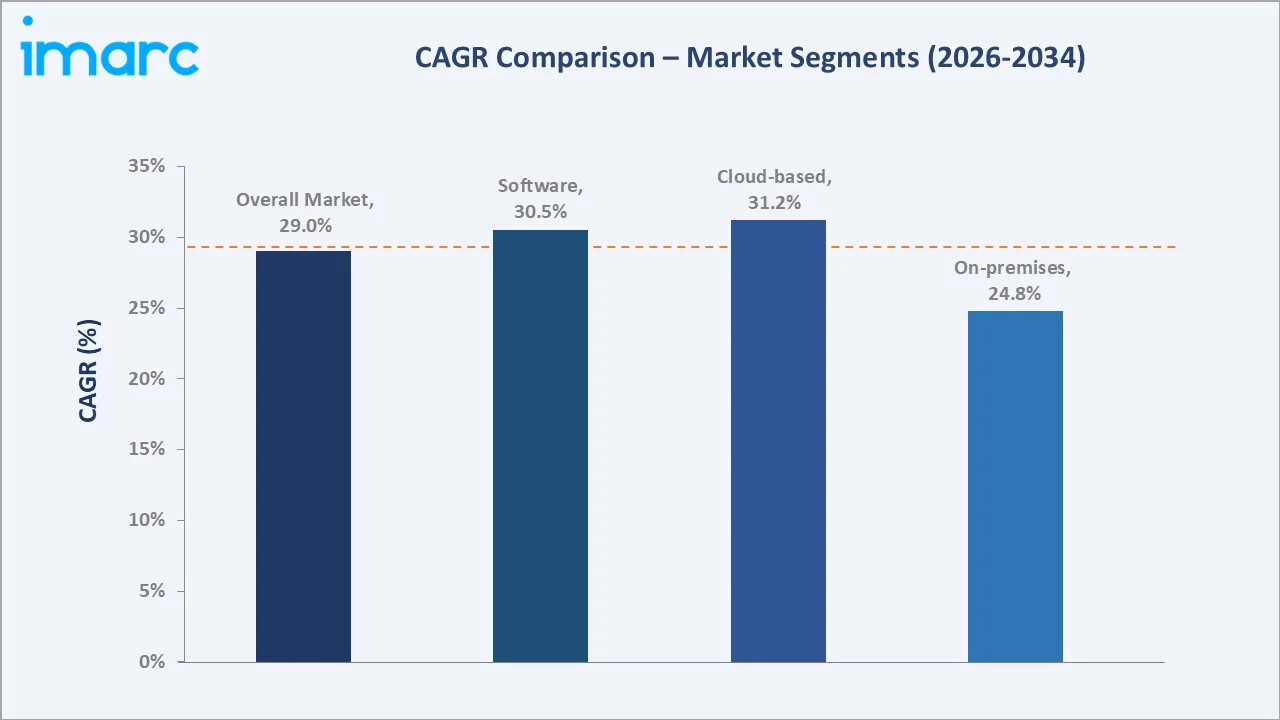

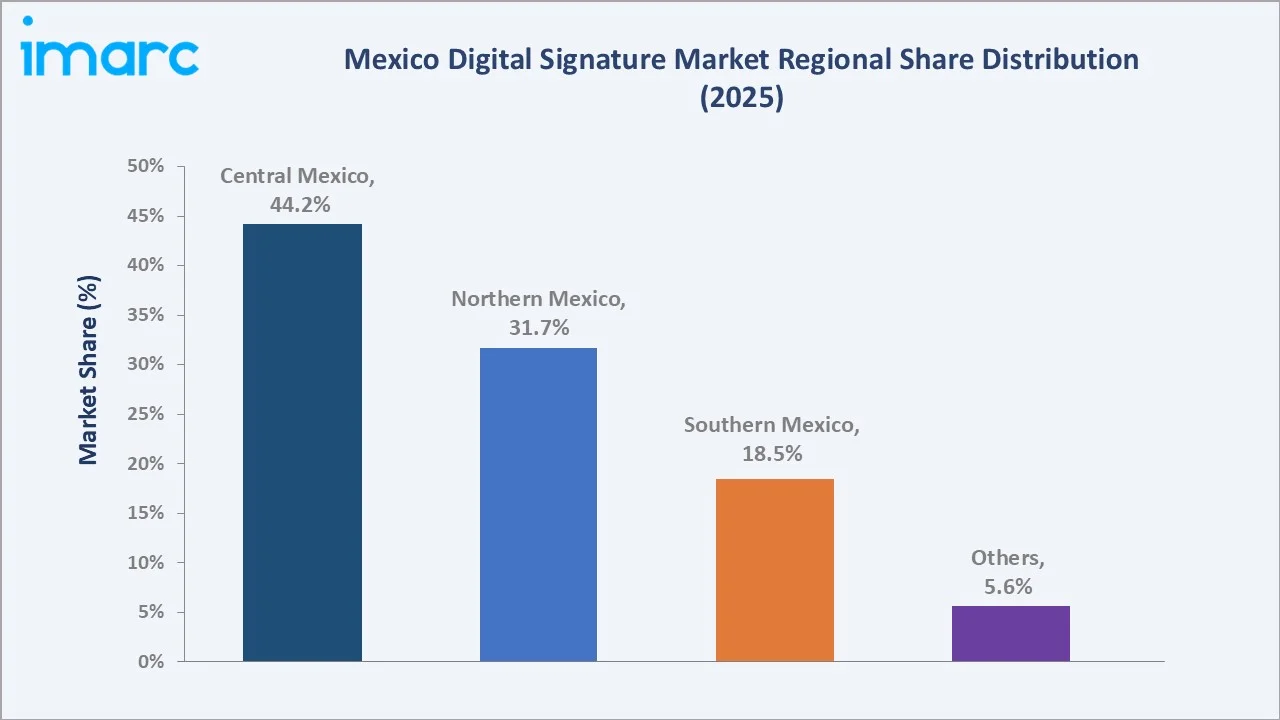

Software leads by component at 52.8%, cloud-based deployment commands 66.9%, and Central Mexico accounts for 44.2% of the regional market share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 130.67 Million |

|

Forecast Market Size (2034) |

USD 1,378.60 Million |

|

CAGR (2026-2034) |

29.03% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Software (52.8%, 2025) |

|

Dominant Deployment Model |

Cloud-based (66.9%, 2025) |

|

Leading Region |

Central Mexico (44.2%, 2025) |

The market expanded from USD 36.54 Million in 2020 to USD 130.67 Million in 2025, anchored at USD 467.30 Million in 2030 and forecast to reach USD 1,378.60 Million by 2034. Mexico’s SAT e-invoicing mandate created a structural demand baseline, while expanding e-commerce and fintech adoption accelerated multi-sector deployment throughout the historical period.

To get more information on this market, Request Sample

Software component grows fastest at approximately 30.5% CAGR as enterprise SaaS platform deployments proliferate across banking, healthcare, and government sectors. Cloud-based solutions at 31.2% CAGR outpace on-premises as SMEs and startups adopt scalable, API-driven signing tools without capital infrastructure expenditure.

Executive Summary

The Mexico digital signature market reached USD 130.67 Million in 2025, representing one of Latin America’s fastest-growing technology software markets driven by SAT’s e-invoicing compliance mandate, NOM-151 timestamp standards, accelerating BFSI digitalization, and widespread mobile commerce growth. The market is projected to reach USD 1,378.60 Million by 2034.

Software at 52.8% leads by component, capturing enterprise SaaS platform deployments and CRM-integrated signing solutions. Cloud-based deployment at 66.9% dominates due to Mexico’s high mobile penetration and SME cost-sensitivity to infrastructure investment. Central Mexico at 44.2% leads regionally through the concentration of financial institutions, multinational corporations, and government agencies in Mexico City and surrounding metropolitan areas.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Software – 52.8% share (2025) |

|

Dominant Deployment Model |

Cloud-based – 66.9% market share (2025) |

|

Leading Region |

Central Mexico – 44.2% market share (2025) |

|

Market Opportunity |

AI-integrated CLM platforms; mobile biometric signing; SME SaaS adoption; NOM-151 compliant cloud trust services; fintech origination workflows |

Key Analytical Observations Supporting The Above Data:

- Software at 52.8%: Software dominates as enterprises across BFSI, healthcare, and government deploy SaaS signing platforms for contract lifecycle management, employee onboarding, and regulatory compliance. DocuSign and Adobe Sign offer localized integrations with SAT’s PAC platforms and Mexico-specific ERP systems, reinforcing the software segment’s leading position.

- Cloud-based at 66.9%: Cloud-based deployment leads due to affordability, scalability, and alignment with Mexico’s mobile-first business environment. SaaS platforms enable SMEs to access legally binding digital signature tools via APIs, reducing upfront capital expenditure and supporting remote workforce compliance requirements at lower total cost of ownership.

- Central Mexico at 44.2%: Central Mexico leads through Mexico City’s role as the country’s financial, governmental, and corporate hub. The high concentration of financial institutions, multinational headquarters, and federal government agencies drives consistent digital signature procurement and deployment at enterprise scale.

Mexico Digital Signature Market Overview

The Mexico digital signature market encompasses the design, delivery, and servicing of software platforms, hardware security modules, and professional services enabling cryptographic authentication of electronic documents under Mexico’s NOM-151 standard, FIEL/e.firma framework issued by SAT, and the FIREL standard from the Federal Judiciary (PJF).

The ecosystem integrates cloud platform vendors, PKI certificate authorities, digital identity verification providers, enterprise software integrators, and government regulatory bodies. Macroeconomic factors include government digitalization mandates, fintech sector growth, rising e-commerce transaction volumes, and Mexico’s nearshoring-driven corporate expansion requiring scalable document management infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

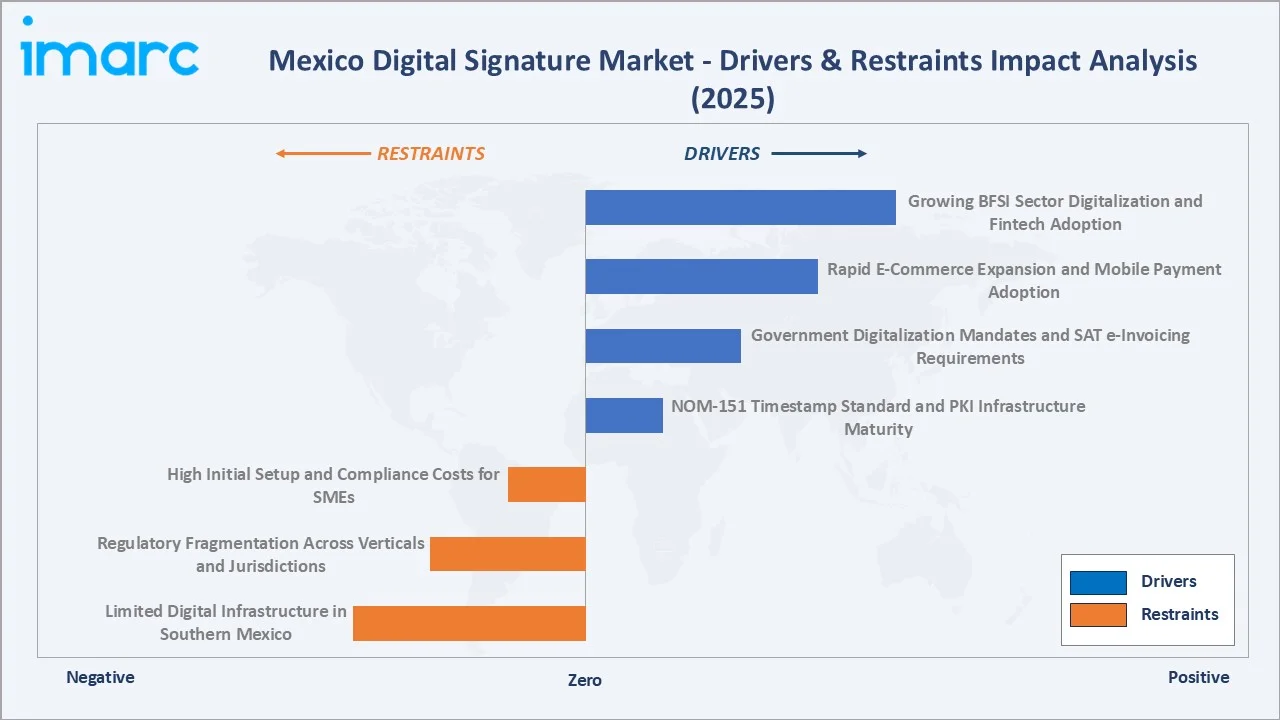

Market Drivers

- Government Digitalization Mandates and SAT e-Invoicing Requirements: Mexico’s SAT mandates digital signatures for all electronic invoices (CFDI) and fiscal documents, creating a structural, compliance-driven baseline demand for digital signature solutions. Mexico approved reforms to legally recognize electronic promissory notes under the “functional equivalence” principle, broadening the legal scope of digital signatures across credit and commercial transactions.

- Rapid E-Commerce Expansion and Mobile Payment Adoption: The increasing adoption of e-commerce, digital payments, and online business transactions is driving demand for secure electronic signature solutions. Businesses across retail, logistics, financial services, and other industries are increasingly implementing API-integrated digital signing tools to streamline document workflows, enhance customer experience, and ensure regulatory compliance, thereby expanding the addressable market for compliant digital signing infrastructure.

- Growing BFSI Sector Digitalization and Fintech Adoption: Banks, insurers, and fintech platforms use digital signatures to expedite customer onboarding, loan approvals, and account management. DocuSign’s services accept fiscal certificates issued by Mexico’s SAT for document signing, ensuring local regulatory compliance. The proliferation of neobanks and embedded finance platforms creates an expanding addressable market for compliant digital signature infrastructure.

- NOM-151 Timestamp Standard and PKI Infrastructure Maturity: Mexico’s NOM-151 standard establishes requirements for preserving data integrity and legal validity of electronic messages. Increasing PKI infrastructure maturity, combined with SAT-authorized Certification Service Providers, reduces legal uncertainty and supports broader enterprise adoption across healthcare, real estate, and government sectors.

Market Restraints

- High Initial Setup and Compliance Costs for SMEs: Implementing enterprise-grade digital signature solutions, particularly on-premises PKI infrastructure, requires significant capital investment in hardware security modules, certificate authority setup, and IT integration. For Mexico’s large SME base, these upfront costs create adoption barriers, limiting penetration in micro and small enterprise segments.

- Regulatory Fragmentation Across Verticals and Jurisdictions: Mexico’s digital signature legal framework spans multiple regulatory bodies, including SAT for fiscal documents, PJF for judicial filings, and sector-specific regulators in healthcare and real estate. This fragmentation creates interoperability challenges, increasing compliance costs and slowing cross-sector platform standardization.

- Limited Digital Infrastructure in Southern Mexico: Regional disparities in digital infrastructure quality, internet penetration, and device access limit cloud-based digital signature adoption in Southern Mexico and rural areas. Inadequate connectivity and limited digital literacy reduce consumer confidence and constrain market penetration beyond major urban centers.

Market Opportunities

- AI-Integrated Contract Lifecycle Management (CLM) Platforms: The integration of AI capabilities into digital signature platforms, enabling automated contract review, intelligent clause extraction, and predictive workflow routing, represents a significant growth opportunity. In March 2025, Adobe launched the Adobe Experience Platform Agent Orchestrator, signaling a shift toward intelligent agreement management that Mexican enterprises are increasingly evaluating for procurement and legal operations.

- SME SaaS Adoption and Mobile-First Signing Platforms: Mexico’s estimated 4.1 million small and medium-sized enterprises (SMEs) represent an underpenetrated market for affordable, mobile-first digital signature SaaS platforms. Local providers including Mifiel, Signatura, and Cincel are capturing this segment with NOM-151-compliant, Spanish-language platforms and flexible subscription pricing, creating substantial headroom for market expansion.

Market Challenges

- Cross-Border Interoperability and Legal Recognition Issues: Mexican enterprises operating in cross-border trade with the United States and Europe face challenges ensuring digitally signed documents comply with multiple regulatory frameworks simultaneously, including NOM-151, US ESIGN Act, and EU eIDAS standards. This interoperability gap increases compliance complexity and legal risk for multinationals and export-oriented businesses.

- Cybersecurity Risks and Certificate Authority Vulnerabilities: The increasing sophistication of cyberattacks targeting PKI infrastructure, including certificate spoofing and man-in-the-middle attacks, poses a sustained challenge to digital signature trust frameworks. Enterprises must invest continuously in certificate revocation management, multi-factor authentication layers, and tamper-evident audit trails, increasing total cost of ownership.

Emerging Market Trends

1. Mobile-First Digital Signing and Biometric Authentication

Mobile platforms are becoming the primary interface for digital signature execution as smartphone penetration exceeds 75% of Mexico’s adult population. Platforms integrating biometric authentication, including facial recognition and fingerprint validation under NOM-151, are gaining traction among fintech and BFSI clients seeking frictionless, legally binding identity verification during the signing process.

2. Blockchain-Anchored Digital Signature Integrity

Emerging platforms are incorporating blockchain timestamping to create immutable audit trails for signed documents. This approach enhances non-repudiation and document integrity verification, particularly in real estate, legal, and cross-border trade applications where long-term evidentiary standards are critical to contractual enforcement and regulatory compliance.

3. AI-Powered Contract Analytics and Intelligent Workflow Automation

DocuSign’s acquisition of Lexion and Adobe’s launch of AI agent orchestration tools signal the industry’s transition from simple e-signature tools to intelligent agreement management platforms. Mexican enterprises in banking and insurance are beginning to evaluate AI-integrated CLM solutions that automate contract review, flag risk clauses, and route approvals dynamically.

4. Government-Issued Digital Identity Integration with Private Sector Platforms

The integration of SAT’s e.firma and the PJF’s FIREL credentials into private sector digital signature platforms is expanding the legal validity of enterprise-signed documents for government interactions. Cincel, accredited as Mexico’s first cloud Trust Service Provider by the Ministry of Economy, exemplifies this trend by enabling full NOM-151 compliance and biometric identity verification within a single cloud-based platform.

Industry Value Chain Analysis

The Mexico digital signature market value chain integrates cryptographic infrastructure provisioning, platform software development, professional services delivery, enterprise integration, and post-sale compliance support. Cloud deployment has progressively displaced hardware-centric on-premises architecture as the dominant commercial format for the market.

|

Stage |

Key Participants |

|

PKI & Certificate Authority Infrastructure |

Provision root certificates, hardware security modules (HSMs), and CA services enabling legally valid digital signatures under Mexico’s NOM-151 and SAT e.firma frameworks |

|

Platform & Software Development |

Develop signing workflows, API libraries, CLM platforms, and mobile signing tools integrating NOM-151 and SAT CFDI compliance for enterprise and SME clients |

|

Hardware Security Modules (HSM) |

Manufacture cryptographic hardware for on-premises PKI deployments in banking, judicial, and government sectors requiring local key management and data sovereignty |

|

Professional Services & Integration |

Implement digital signature platforms into ERP, CRM, and document management systems; provide compliance consulting, training, and workflow automation services |

|

Enterprise End-User Deployment |

BFSI, healthcare, government, real estate, and HR functions deploying digital signature tools for contract execution, regulatory compliance, and workforce management workflows |

|

Compliance & Audit Support |

Legal advisory firms, NOM-151 timestamping authorities, and document archiving services ensuring long-term legal validity, retrievability, and evidentiary compliance |

The PKI and certificate authority tier is the market’s most regulated stage, governed by SAT-authorized CSPs and the Ministry of Economy. The software and SaaS platform tier is experiencing the fastest commercial growth as enterprises shift from hardware-centric to cloud-native digital signature infrastructure throughout the forecast period.

Technology Landscape in the Mexico Digital Signature Industry

Public Key Infrastructure (PKI) Technology

PKI technology underpins all legally valid digital signatures in Mexico through the issuance, management, and revocation of digital certificates. SAT’s e.firma (FIEL) credential system and NOM-151 timestamping standards provide the legal framework for PKI-based signatures, enabling enterprises to execute contracts with government-recognized cryptographic validity.

Cloud-Based SaaS Signing Platform Technology

Cloud-based SaaS signing platforms deliver digital signature functionality via APIs and web interfaces, enabling integration with ERP, CRM, and document management systems without capital infrastructure investment. Platforms including DocuSign, Adobe Acrobat Sign, Mifiel, and Cincel offer localized compliance with SAT’s CFDI invoicing requirements and NOM-151 standards, supporting both individual and enterprise use cases at scale.

AI and Machine Learning for Contract Intelligence

AI and ML capabilities are being integrated into digital signature platforms to automate contract review, extract key clauses, identify risk language, and predict optimal workflow routing. In March 2025, Adobe launched its AI Agent Orchestrator with strategic partnerships with Microsoft, SAP, and ServiceNow, enabling AI-driven document automation into mainstream enterprise signing workflows across Mexico.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

52.8% |

2025 |

|

Deployment Model |

Cloud-based |

66.9% |

2025 |

|

Enterprise Size |

🔒 |

🔒 |

2025 |

|

Industry Vertical |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

44.2% |

2025 |

By Component

Software leads at 52.8% in 2025, encompassing enterprise SaaS signing platforms, CLM tools, and API-integrated document workflow software. Software dominates as enterprises across BFSI, government, and healthcare deploy platform-based signing solutions rather than hardware-centric alternatives, driven by lower deployment costs and faster integration timelines.

To access detailed market analysis, Request Sample

Services at 31.4% capture professional implementation, integration consulting, training, and post-deployment compliance support as enterprises require specialized guidance for NOM-151 and SAT compliance. Hardware at 15.8% represents HSM procurement and smart card infrastructure for government and regulated financial institutions requiring on-premises cryptographic key management.

By Deployment Model

Cloud-based deployment leads at 66.9% in 2025, driven by Mexico’s mobile-first business environment, SME adoption of subscription-based tools, and the availability of SAT-compliant cloud signing APIs from DocuSign, Adobe, and Mifiel. Cloud-based solutions align with remote work requirements and eliminate hardware capital expenditure, accelerating enterprise and SME adoption.

On-premises deployment at 33.1% serves government agencies, regulated financial institutions, and judicial entities requiring local cryptographic key management and data sovereignty. Hybrid models are emerging where sensitive data is stored locally but signing is facilitated through cloud access, balancing security requirements with operational flexibility.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Central Mexico |

44.2% |

Concentration of financial institutions, federal government agencies, and multinational headquarters in Mexico City drives consistent enterprise digital signature adoption and deployment |

|

Northern Mexico |

31.7% |

Industrial clusters, maquiladora operations, nearshoring-driven corporate expansion, and cross-border trade with the United States create sustained demand for digital document authentication |

|

Southern Mexico |

18.5% |

Emerging adoption driven by government digital transformation programs, growing SME formalization, and expanding mobile internet access in regional cities including Mérida, Oaxaca, and Puebla |

|

Others |

5.6% |

Nascent adoption in more remote regions, supported by federal e-government initiatives extending digital signature access and raising awareness among underserved municipalities |

Central Mexico, at 44.2%, leads through Mexico City’s role as the financial and government capital, hosting the majority of regulated enterprises, federal ministries, and Fortune 500 Mexico offices requiring enterprise digital signature infrastructure for contract management and regulatory compliance workflows.

Northern Mexico, at 31.7%, reflects Monterrey’s and Ciudad Juárez’s roles as manufacturing and nearshoring hubs where cross-border trade documentation and supplier contract workflows drive adoption. Southern Mexico, at 18.5%, represents an emerging market growing through federal digitalization programs and increasing SME formalization in regional centers.

Competitive Landscape

The Mexico digital signature market features a moderately concentrated competitive structure with two distinct tiers: global enterprise platform providers with localized Mexico compliance capabilities, and domestic cloud trust service providers offering government-accredited NOM-151 and e.firma-integrated solutions for local enterprises and SMEs.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Docusign, Inc. |

Docusign eSignature, Docusign CLM, Docusign IAM |

Market Leader |

Global leader in e-signature and contract lifecycle management with SAT fiscal certificate acceptance and deep CRM/ERP integrations |

|

Adobe |

Adobe Acrobat Sign, Adobe Document Cloud |

Market Leader |

PDF-native signing platform integrated with Microsoft 365, Salesforce, and SAP; AI agent orchestration capabilities for enterprise workflows |

|

Entrust Corporation |

Entrust Signhost, Entrust PKI, nShield 5 HSM |

Strong Challenger |

Specializes in PKI infrastructure, digital certificates, and HSM hardware for regulated financial and government on-premises deployments |

Key players include Docusign, Inc., Adobe, Entrust Corporation, and others.

Key Company Profiles

Docusign, Inc.

Docusign, Inc. is a United States-based company specializing in e-signature and intelligent agreement management platforms with a strong presence in Mexico through SAT fiscal certificate acceptance and Spanish-language platform support for enterprise and SME clients.

- Key Products: DocuSign eSignature, DocuSign CLM, DocuSign IAM Platform.

- Recent Developments: In March 2025, DocuSign engaged in a strategic partnership with Algebrik AI to integrate e-signature capabilities into loan origination workflows. DocuSign’s Mexico operations accept fiscal certificates issued by SAT for legally binding document signing.

- Strategic Focus: Expanding intelligent agreement management through AI integration, deepening CRM and ERP platform integrations, and broadening Latin America compliance capabilities including support for NOM-151 and SAT e.firma frameworks.

Adobe

Adobe is a United States-based digital media and experience software company offering digital signature capabilities through Adobe Acrobat Sign, integrated within its Document Cloud and Creative Cloud ecosystem for enterprise and individual users.

- Key Products: Adobe Acrobat Sign, Adobe Document Cloud.

- Strategic Focus: Integrating AI agent orchestration into document and signing workflows, expanding enterprise API partnerships, and delivering AI-enhanced contract creation and management solutions across BFSI, healthcare, and enterprise verticals in Mexico and Latin America.

Market Concentration Analysis

The Mexico digital signature market is moderately concentrated at the enterprise platform level, with the top four key players collectively accounting for approximately 45–55% of Mexico’s enterprise digital signature platform revenue. Domestic providers including Cincel and Mifiel account for an estimated 10–15% of the overall market, with particularly strong penetration in the SME and government-adjacent segments.

Market concentration is declining over the forecast period as domestic cloud Trust Service Providers gain Ministry of Economy accreditation and new entrants develop specialized vertical-focused signing platforms for healthcare, real estate, and legal applications. The SAT compliance requirement creates a structural market floor that supports both global and domestic providers simultaneously, preventing winner-take-all dynamics and sustaining a diverse competitive ecosystem through 2034.

Investment & Growth Opportunities

Highest Growth Segments

Software component (~30.5% CAGR), cloud-based deployment (~31.2% CAGR), AI-integrated CLM platforms (~35%+ CAGR from smaller base), mobile biometric signing (~28% CAGR), BFSI digital signature integration (~32% CAGR), and government-to-citizen digital identity signing (~27% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

SME SaaS digital signature adoption represents Mexico’s largest underpenetrated market segment. Mexico’s estimated 4.1 million SMEs, of which fewer than 15% currently use digital signature platforms, create a structurally expanding addressable market for affordable, NOM-151-compliant SaaS tools with mobile-first interfaces and flexible per-document pricing.

Investment Themes

- NOM-151-compliant cloud Trust Service Provider infrastructure: The Ministry of Economy’s accreditation framework for cloud Trust Service Providers creates a regulatory moat for platforms achieving full compliance, representing a structural competitive advantage in government and regulated enterprise markets through 2034.

- AI-integrated contract analytics for BFSI and legal sectors: Integration of AI-powered clause analysis, risk flagging, and workflow automation into digital signing platforms creates high-value differentiation opportunities in Mexico’s fast-growing banking, insurance, and legal services sectors, where contract volume and compliance complexity justify premium platform pricing.

Future Market Outlook (2026-2034)

The Mexico digital signature market is projected to grow from USD 130.67 Million in 2025 to USD 1,378.60 Million by 2034, delivering a 29.03% CAGR over the forecast period. The market’s anchor value of USD 467.30 Million in 2030 represents a digital signature industry at a major commercial inflection point, where cloud-based SaaS platforms will have fully displaced hardware-centric solutions across most enterprise segments.

Three structural forces define the market’s growth trajectory through 2034. Mexico’s SAT compliance mandate creates a non-discretionary baseline demand pool that grows with GDP and business formation rates. The SME digitalization wave, accelerated by post-pandemic remote work adoption and e-commerce growth, will add millions of first-time digital signature users to the market. AI integration into CLM platforms will increase average revenue per enterprise user by enabling premium subscription tiers with intelligent automation capabilities.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025–2026), including Chief Information Officers, digital transformation leads at Mexican banks, SAT-accredited Certification Service Providers, e-signature platform product managers, and government e-governance program directors.

Secondary Research

Secondary research encompassed company annual reports, Mexico SAT regulatory publications, Ministry of Economy Trust Service Provider accreditation records, AMIPCI digital economy reports, Banxico digital payments statistics, INEGI enterprise digitalization surveys, and global digital signature market forecast reports. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a bottom-up adoption model: (i) enterprise and SME counts by sector; (ii) digital signature penetration rates by enterprise size; (iii) average annual platform spending per user by component and deployment mode; (iv) growth rate adjustments for regulatory changes, technology adoption curves, and macroeconomic factors specific to the Mexican digital economy.

Mexico Digital Signature Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software, Services |

| Deployment Models Covered | On-premises, Cloud-based |

| Enterprise Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Industry Verticals Covered | BFSI, Education, Human Resource, IT and Telecommunication, Government, Healthcare and Life Science, Real Estate, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Docusign, Inc., Adobe, Entrust Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico digital signature market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico digital signature market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico digital signature industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Digital Signature Market Report

The Mexico digital signature market reached USD 130.67 Million in 2025, driven by SAT e-invoicing mandates, software platforms at 52.8% share, cloud-based deployment leading at 66.9%, and Central Mexico commanding 44.2% of the regional market through enterprise and government concentration.

The market grows at 29.03% CAGR during 2026-2034, reaching USD 1,378.60 Million by 2034, reflecting SAT compliance demand, SME SaaS adoption, AI-integrated CLM expansion, and rising fintech and BFSI digital transformation investment across Mexico.

Software leads at 52.8%, capturing enterprise SaaS platform deployments for contract execution, employee onboarding, and regulatory compliance workflows. Software grows at approximately 30.5% CAGR through AI integration, API ecosystem expansion, and increasing CRM and ERP platform partnerships.

Cloud-based deployment leads at 66.9% through Mexico’s mobile-first business environment, SME cost sensitivity, and SAT-compliant cloud APIs. Cloud-based solutions grow fastest at approximately 31.2% CAGR as adoption expands beyond large enterprises into the SME segment throughout the forecast period.

Central Mexico leads at 44.2% through Mexico City’s concentration of financial institutions, multinational corporations, and federal government agencies deploying enterprise digital signature infrastructure for contract management and regulatory compliance workflows.

Leading companies include Docusign, Inc., Adobe, Entrust Corporation, and others.

The Mexico digital signature market is projected to reach USD 467.30 Million by 2030, representing the inflection at which AI-integrated CLM platforms become mainstream, mobile biometric signing achieves widespread SME adoption, and cloud-based deployment surpasses 75% market share across all enterprise segments.

Three priority investment opportunities: NOM-151-compliant cloud Trust Service Provider infrastructure capturing the government-accredited signing market, AI-integrated CLM platforms serving Mexico’s fast-growing BFSI and legal verticals, and SME-focused mobile-first SaaS platforms targeting Mexico’s 4 million+ underpenetrated small and medium enterprises.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)