Mexico Frozen Fruits and Vegetables Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Mexico Frozen Fruits and Vegetables Market Summary:

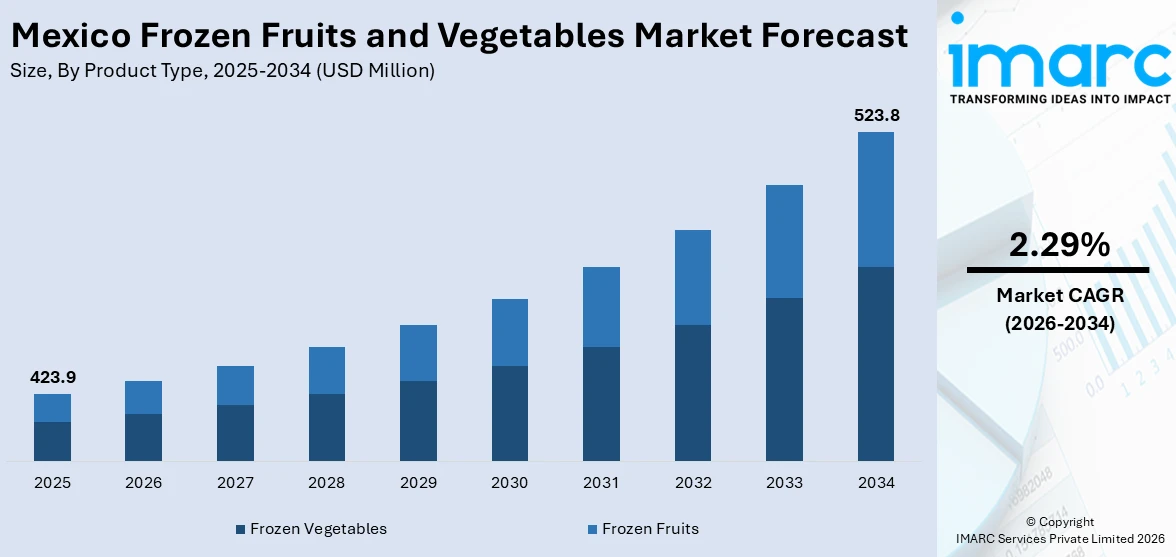

The Mexico frozen fruits and vegetables market size was valued at USD 423.9 Million in 2025 and is projected to reach USD 523.8 Million by 2034, growing at a compound annual growth rate of 2.29% from 2026-2034.

The Mexico frozen fruits and vegetables market is expanding steadily, driven by shifting consumer lifestyles, rising health awareness, and the growing need for convenient and nutritious food options. Rapid urbanization and dual-income household dynamics are increasing demand for easy-to-prepare meal solutions. Advancements in freezing technologies, particularly individual quick freezing, are improving product quality and nutritional retention, supporting broader adoption. Expanding cold chain infrastructure and the proliferation of organized retail and digital grocery platforms are widening distribution reach. These converging forces are reinforcing the Mexico frozen fruits and vegetables market share.

Key Takeaways and Insights:

- By Product Type: Frozen vegetables dominate the market with a share of 89.3% in 2025, owing to their widespread use in foodservice operations, household cooking, and food processing. Their extended shelf life, nutritional value, and year-round availability make them a preferred choice across consumer and commercial segments.

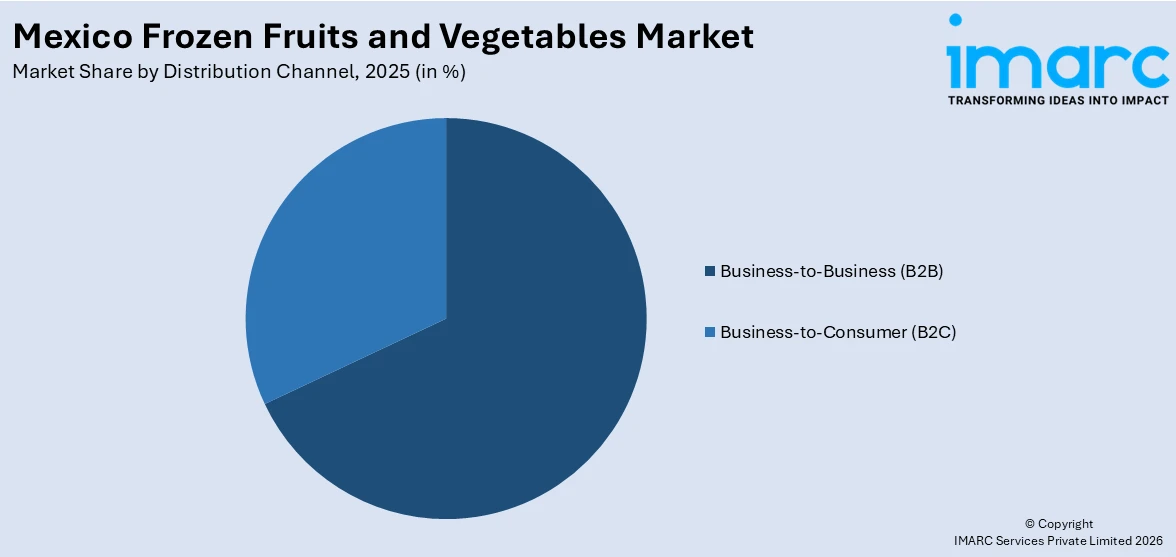

- By Distribution Channel: Business-to-business (B2B) leads the market with a share of 68.5% in 2025. This dominance is driven by high volume procurement from foodservice operators, restaurants, hotels, and food processing companies that rely on consistent, bulk supply of frozen produce for daily operations.

- By Region: Central Mexico represents the largest region with 45.5% share in 2025, driven by its concentration of major urban centers, dense foodservice networks, and a large consumer base with higher disposable income and greater exposure to modern retail formats.

- Key Players: Key players in the Mexico frozen fruits and vegetables market drive growth by expanding their product portfolios, investing in advanced freezing and packaging technologies, and strengthening nationwide distribution networks. Their focus on quality assurance, cold chain reliability, and partnerships with foodservice operators and retailers accelerates market penetration and supports consistent product availability across consumer and commercial segments.

To get more information on this market Request Sample

The Mexico frozen fruits and vegetables market is an emerging market, with consumers, retailers, and food service sectors becoming aware of the benefits of consuming frozen fruits and vegetables, which are cost-effective, healthy, and safe food products. Health-conscious consumerism is transforming the way people shop for products, with urban consumers demanding cleaner, less processed, and organic products, including frozen products. The emergence of organized retailing, including supermarkets and hypermarkets, is increasing the availability of frozen products in the market, hence increasing demand. The emergence of e-commerce sites is also increasing the availability of the products, enabling consumers to shop from the comfort of their homes. Food service is the major demand driver for frozen products, with restaurants, hotels, etc., consuming a large quantity of frozen products.

Mexico Frozen Fruits and Vegetables Market Trends:

Growing Consumer Shift Toward Convenient and Health-Focused Food Options

The fast pace of urban lifestyle, along with the awareness regarding healthy habits, is greatly impacting the shopping behavior of individuals for food products. The contemporary world is witnessing the need for healthy food products that save the precious time of individuals without compromising the health of the food being consumed. The frozen fruit and vegetable products have tremendous growth potential, keeping in view the fact that the products retain the vitamins, minerals, and flavor through the freezing process. The long shelf life of frozen food products is also a major advantage for individuals who want to avoid wastage of food products.

Expansion of Cold Chain Infrastructure and Logistics Capabilities

Investment in cold chain infrastructure across Mexico is accelerating, creating a more reliable and expansive distribution network for frozen produce. In March 2025, Emergent Cold LatAm inaugurated a new greenfield cold storage facility in Ciénega de Flores, Monterrey, with a 23,000-pallet capacity. Additionally, in December 2024, Canadian Pacific Kansas City and Americold announced plans to expand their cold chain partnership into Mexico, aiming to offer rail-based temperature-controlled freight solutions as a complement to traditional trucking corridors.

Rapid Growth of E-Commerce and Digital Grocery Platforms

Online grocery shopping is transforming how consumers access frozen fruits and vegetables, with digital platforms significantly expanding market reach. In 2024, Amazon Mexico collaborated with digital supermarket Jüsto to offer frozen food delivery within four hours across select Mexico City regions, responding to rising demand for convenient at-home grocery delivery. The proliferation of mobile applications, rapid delivery services, and e-commerce partnerships is making frozen produce more accessible to urban households seeking convenient at-home shopping solutions. Investments in last-mile delivery infrastructure and fulfillment centers are reducing delivery times, enabling consumers to order a wide variety of frozen fruits and vegetables directly from their homes.

Market Outlook 2026-2034:

The Mexico frozen fruits and vegetables market is expected to grow steadily over the forecast period, due to the increasing rate of urbanization, the growth of the cold chain infrastructure, and the increasing consumption of frozen food products. The demand for healthy, safe, and convenient food products is expected to remain strong over the forecast period. Continuous progress in freezing technology, along with the growth of organized retail, is expected to boost the market growth over the forecast period. The market generated a revenue of USD 423.9 Million in 2025 and is projected to reach a revenue of USD 523.8 Million by 2034, growing at a compound annual growth rate of 2.29% from 2026-2034.

Mexico Frozen Fruits and Vegetables Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Frozen Vegetables |

89.3% |

|

Distribution Channel |

Business-to-Business (B2B) |

68.5% |

|

Region |

Central Mexico |

45.5% |

Product Type Insights:

- Frozen Fruits

- Frozen Vegetables

Frozen vegetables dominate with a market share of 89.3% of the total Mexico frozen fruits and vegetables market in 2025.

Frozen vegetables dominate the frozen food segment in the Mexican market, with the majority of the market share attributed to the versatility, cost-effectiveness, and inalienable nature of frozen vegetables in foodservice and home cooking. A plethora of frozen vegetables, ranging from corn, peas, broccoli, carrots, green beans, and a mix of vegetables, is consumed across the foodservice and home markets. In the B2B segment, frozen vegetables are relied on to ensure consistency and cost-effectiveness, particularly in foodservice operations with high turnover volumes. Advances in the quality of blanching and individual quick-freezing techniques have also contributed to the taste, texture, and nutritional benefits of frozen vegetables, further increasing the acceptability and loyalty towards the product.

The preponderance of frozen vegetables is a function of deeply entrenched usage patterns throughout Mexico’s food value chain, which includes large-scale food processing companies, as well as independent restaurants and households. Domestic supply is driven by key agricultural states, including Michoacán, Guanajuato, and Sinaloa, which provide a wide variety of vegetables conducive to freezing, thereby enabling price competitiveness. Furthermore, government policies aimed at improving agricultural productivity and modernizing food processing have contributed to supply-side growth. Finally, changing consumer trends towards plant-based, low-calorie, and high-fiber foods are helping to expand the market for frozen vegetables as an essential household pantry item, especially among health-oriented households.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Business-to-Consumer (B2C)

- Supermarkets/Hypermarkets

- Independent Retailers

- Convenience Stores

- Online

- Others

- Business-to-Business (B2B)

Business-to-business (B2B) leads with a share of 68.5% of the total Mexico frozen fruits and vegetables market in 2025.

The B2B distribution channel serves as the primary demand driver for frozen fruits and vegetables in Mexico, underpinned by the country's vast and expanding foodservice sector. Restaurants, hotels, fast-food chains, catering companies, hospitals, schools, and food manufacturing firms rely on consistent, large-volume supplies of frozen produce to ensure operational continuity and menu standardization. The dependability, extended shelf life, and cost-effectiveness of frozen fruits and vegetables make them an indispensable ingredient across diverse commercial food preparation environments throughout the country.

Quick-service restaurants and fast-casual dining establishments represent particularly significant contributors to B2B frozen produce demand, utilizing frozen vegetables as core menu ingredients across high-turnover kitchen operations. The scalability and portion consistency offered by frozen produce align well with the operational requirements of chained foodservice formats, where standardized recipes and predictable ingredient costs are essential. As Mexico's foodservice sector continues to expand alongside rising urbanization and growing consumer appetite for dining-out experiences, B2B demand for frozen fruits and vegetables is expected to remain robust throughout the forecast period.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

Central Mexico represents the largest region with 45.5% share of the total Mexico frozen fruits and vegetables market in 2025.

Central Mexico holds the dominant share of the frozen fruits and vegetables market, anchored by the high concentration of population, economic activity, and foodservice infrastructure across the region. Mexico City serves as the epicenter of modern retail, institutional catering, and large-scale food manufacturing, generating substantial and consistent demand for frozen produce. The region hosts major wholesale distribution hubs that facilitate efficient movement of food products across urban and commercial networks. Guadalajara, situated in the neighboring state of Jalisco, further amplifies regional demand as a prominent commercial and industrial center.

The dense population of urban centers in Central Mexico supports a highly active foodservice sector, with quick-service restaurants, hotel chains, corporate cafeterias, and institutional buyers driving consistent high-volume demand for frozen vegetables and fruits. Rising disposable incomes and growing exposure to modern consumption patterns among middle-class households are also boosting retail demand for frozen produce in the region. The availability of advanced cold storage and logistics infrastructure in metropolitan corridors further supports reliable year-round supply. As new supermarket and hypermarket locations continue to open in Central Mexico's expanding suburban zones, the region's market share is expected to remain robust throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Mexico Frozen Fruits and Vegetables Market Growing?

Rising Urbanization and Demand for Convenient, Nutritious Food Options

Mexico's rapid urbanization is a primary structural driver of frozen produce demand. Urban lifestyles characterized by extended working hours, dual-income households, and reduced time for meal preparation are increasing reliance on quick, ready-to-cook food solutions. Frozen fruits and vegetables offer an appealing combination of nutritional quality, ease of use, and long shelf life, making them well suited to the demands of busy urban consumers. The growing working-age population in metropolitan centers such as Mexico City, Guadalajara, and Monterrey is expanding the addressable consumer base for frozen produce. The influence of Western dietary patterns and international food culture is also accelerating demand, as consumers adopt recipes and cuisines that feature a broad range of vegetables and fruits not always available fresh year-round. Awareness about the nutritional equivalence and in some cases superiority of frozen produce compared to extended-shelf fresh alternatives is gradually shifting consumer attitudes. The Mexican government's public health campaigns promoting fruit and vegetable consumption, particularly in the context of addressing obesity and chronic disease, are further reinforcing household consumption of frozen produce as part of a balanced diet.

Expansion of Organized Retail and E-Commerce Distribution Channels

The broadening of organized retail infrastructure across Mexico is significantly expanding the physical availability of frozen fruits and vegetables for consumers. Hypermarkets, supermarkets, and warehouse clubs operated by major chains continue to grow their footprint, bringing dedicated freezer sections and diverse frozen produce ranges to more communities. These formats benefit from high consumer footfall, wide product assortments, and strong promotional capabilities that drive category awareness. The parallel growth of e-commerce is creating an additional and fast-expanding distribution layer, enabling brands to reach a wider and more geographically dispersed consumer base through digital grocery platforms and rapid home delivery services.

Strengthening Cold Chain Infrastructure Supporting Market Reach

Investment in cold chain logistics infrastructure is a key enabler of market growth, ensuring that frozen produce can be reliably stored, transported, and delivered while maintaining product quality and food safety standards. Significant investments are being channeled into refrigerated warehousing, last-mile delivery, and IoT-enabled temperature monitoring systems. In March 2025, the Asociación Nacional de Empresas de Transporte en Frío (ANETIF) and the Global Cold Chain Alliance signed a strategic partnership to strengthen cold chain capacity, improve workforce standards, and promote certifications across Mexico. Cold storage expansion is particularly notable in key agricultural and commercial states, with new facilities designed to connect producers and distributors with major port corridors. These investments are reducing supply chain bottlenecks, lowering product spoilage rates, and enabling frozen produce to reach a wider range of retail and foodservice customers across both urban and emerging regional markets.

Market Restraints:

What Challenges the Mexico Frozen Fruits and Vegetables Market is Facing?

Inadequate Cold Chain Coverage in Rural and Semi-Urban Areas

Despite significant investments in cold chain infrastructure across major metropolitan corridors, gaps persist in rural and semi-urban regions where refrigerated warehousing and transportation networks remain limited. The overall availability of refrigerated transport capacity continues to fall short of growing market demand, creating constraints for last-mile delivery of frozen produce to underserved areas. These infrastructure shortfalls restrict market reach, elevate distribution costs, and contribute to product quality inconsistencies in peripheral markets, posing a notable challenge to nationwide frozen produce accessibility.

Consumer Perception of Inferior Quality Relative to Fresh Produce

A persistent segment of Mexican consumers, particularly in traditional and rural communities, holds the perception that frozen fruits and vegetables are nutritionally inferior or of lower quality compared to fresh alternatives. This belief, though increasingly contradicted by scientific evidence supporting the nutritional equivalence of properly frozen produce, continues to limit category trial among certain demographic groups. Overcoming this ingrained attitude requires sustained investment in consumer education, point-of-sale communication, and product quality demonstration, which adds to marketing costs for manufacturers and retailers operating in the frozen produce space.

Volatility in Agricultural Input Costs and Supply Chain Disruptions

Frozen fruit and vegetable producers in Mexico face exposure to fluctuating agricultural input costs, including energy prices for cold storage operations, raw material availability tied to seasonal harvests, and logistical cost pressures driven by fuel price variability. Supply chain disruptions caused by extreme weather events, water scarcity in key agricultural states, and broader macroeconomic pressures can affect raw material availability and production planning. These factors introduce pricing unpredictability and margin pressures, making it challenging for producers and distributors to maintain stable pricing for downstream retail and foodservice customers.

Competitive Landscape:

The Mexico frozen fruits and vegetables market has a moderately competitive nature with the presence of local producers, regional processors, and multinational food organizations. In the Mexico frozen fruits and vegetables market, the level of competition is based on the quality of the product, the reliability of the cold chain, diversity, and the distribution network. Local food processors in the major agricultural regions of the country, such as Michoacan, Guanajuato, and Baja California, are using the advantage of proximity to the raw material source to provide a cost-effective product. Major players are focusing on individual quick freezing, organic products, and private label manufacturing partnerships to increase the product's reach in the foodservice, retail, and export markets. Strategic partnerships with the cold chain and retail organizations are helping the food processors in the Mexico frozen fruits and vegetables market to increase the reliability of the food supply and penetration.

Mexico Frozen Fruits and Vegetables Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Frozen Fruits, Frozen Vegetables |

| Distribution Channels Covered |

|

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Mexico Frozen Fruits and Vegetables Market Report

The Mexico frozen fruits and vegetables market size was valued at USD 423.9 Million in 2025.

The Mexico frozen fruits and vegetables market is expected to grow at a compound annual growth rate of 2.29% from 2026-2034 to reach USD 523.8 Million by 2034.

Frozen vegetables dominated the market with a share of 89.3%, driven by widespread use across foodservice and household segments, year-round demand, versatility in cooking applications, and strong alignment with the nutritional preferences of health-conscious consumers.

Key factors driving the Mexico frozen fruits and vegetables market include rising urbanization and changing consumer lifestyles, growing health consciousness, expansion of organized retail and e-commerce channels, strengthening cold chain infrastructure, and increasing adoption of frozen produce by foodservice operators.

Major challenges include inadequate cold chain coverage in rural and semi-urban areas, persistent consumer perceptions of frozen produce being inferior to fresh alternatives, and volatility in agricultural input costs and supply chain disruptions that affect pricing stability and production consistency.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)