Mexico Glass Market Size, Share, Trends and Forecast by Product Type, End Use Industry, and Region, 2026-2034

Mexico Glass Market Size, Share, Trends & Forecast (2026-2034)

The Mexico glass market reached USD 3.81 Billion in 2025 and is projected to reach USD 7.13 Billion by 2034, exhibiting a growth rate (CAGR) of 7.23% during 2026-2034. The construction sector in Mexico is presently generating substantial demand for glass products, with rising urban developments and infrastructure projects driving consistent consumption of annealed, processed, coated, reflective, and mirror glass. Architects and builders are increasingly using glass for its energy efficiency, durability, and aesthetic appeal in facades, windows, and partitions. Moreover, improvements in glass manufacturing technology, including automated tempering and low-emissivity coating processes, are bolstering market growth. Apart from this, the heightened production of efficient and electric vehicles in Mexico is expanding demand for automotive glazing, while growing solar installations are creating new opportunities for specialized solar glass products.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.81 Billion |

|

Forecast Market Size (2034) |

USD 7.13 Billion |

|

CAGR (2026-2034) |

7.23% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Processed Glass (34.8%, 2025) |

|

Dominant End Use Industry |

Building and Construction (56.3%, 2025) |

|

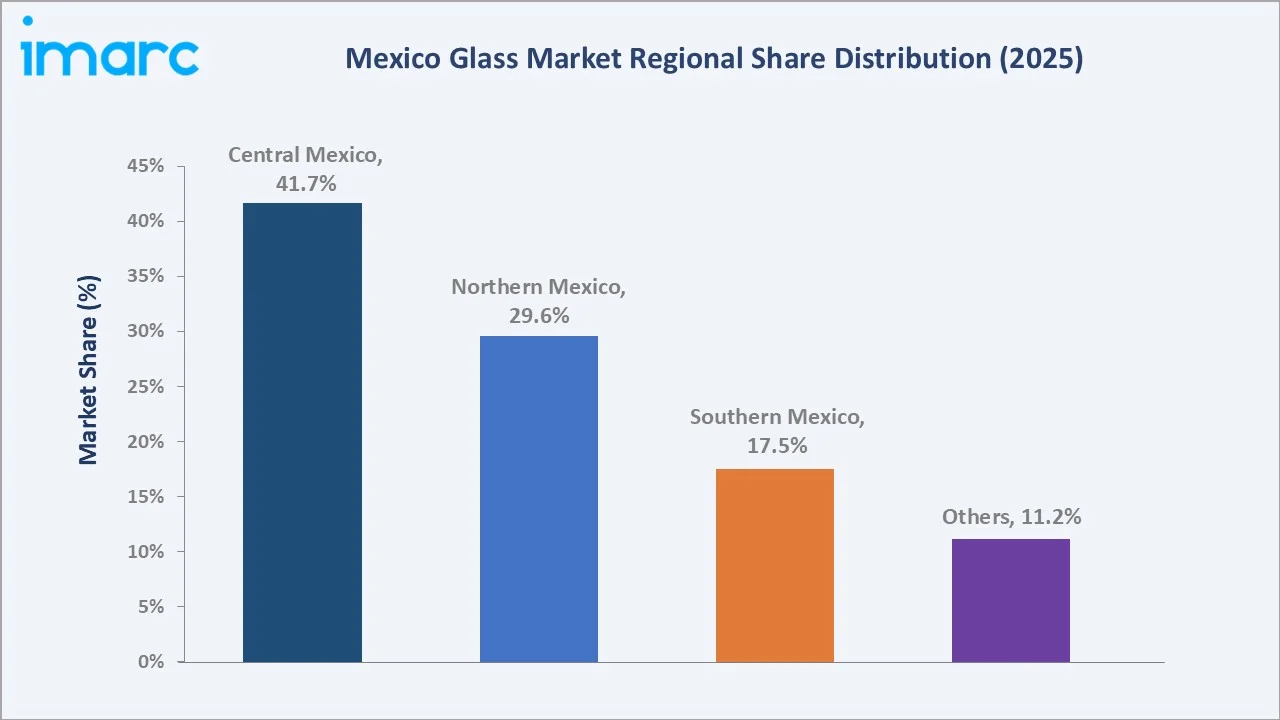

Leading Region |

Central Mexico (41.7%, 2025) |

The Mexico glass market expanded from USD 2.68 Billion in 2020 to USD 3.81 Billion in 2025, and is anchored at USD 5.40 Billion by 2030, before reaching USD 7.13 Billion by 2034. The post-pandemic recovery in construction and industrial activity, combined with rising nearshoring-led manufacturing investment, sustained above-trend growth in the Mexico glass market through 2022-2025, setting the stage for continued expansion across the forecast period.

To get more information on this market, Request Sample

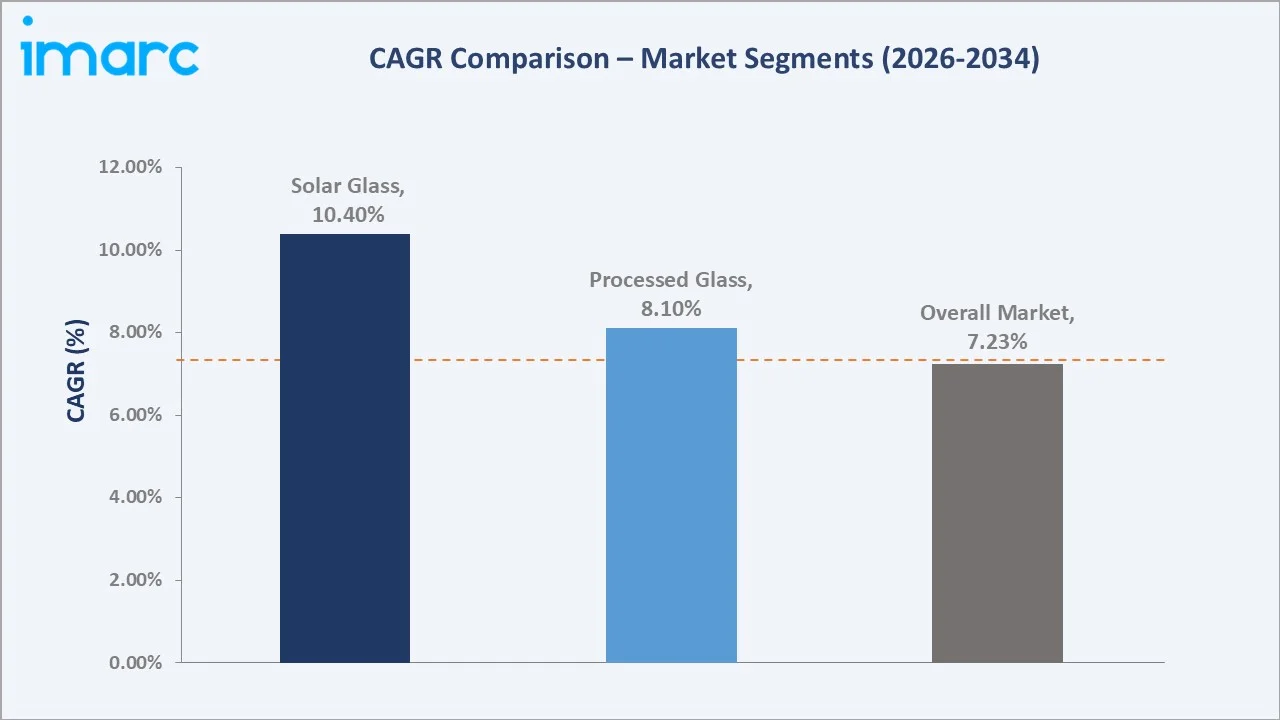

Solar glass is the fastest-growing product category at an estimated ~10.4% CAGR as Mexico's utility-scale and rooftop solar installations expand, while processed glass continues to outpace the overall market on sustained construction and automotive safety-glazing demand.

Executive Summary

The Mexico glass market reached USD 3.81 Billion in 2025, representing one of the country's most dynamic intersections of construction, automotive manufacturing, and energy-efficient building technology. The market encompasses raw material sourcing, float glass production, processing and fabrication, coating and finishing, and distribution to construction, automotive, and solar end users. Processed glass dominates at 34.8% through its widespread use in safety and customized glazing applications, building and construction leads end use at 56.3% on the back of Mexico's expanding urban infrastructure pipeline, and Central Mexico commands 41.7% of the market through its concentration of manufacturing plants and automotive OEM hubs.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Processed Glass - 34.8% share (2025) |

|

Dominant End Use Industry |

Building and Construction - 56.3% share (2025) |

|

Leading Region |

Central Mexico - 41.7% share (2025) |

|

Market Opportunity |

Solar glass integration; smart and self-cleaning glazing; EV automotive glass; green building retrofits; energy-efficient coating technology |

Key Analytical Observations Supporting The Above Data:

- Processed Glass at 34.8%: Processed glass dominates due to its large-scale use in tempered, laminated, and insulated forms across construction and automotive safety applications. These products are widely preferred by builders and automotive OEMs for their durability, customization potential, and compliance with safety regulations, supporting consistent demand growth.

- Building and Construction at 56.3%: Building and construction leads because temperature control, natural lighting, and energy efficiency are essential requirements for Mexico's expanding residential, commercial, and industrial construction pipeline. Green building codes and rising urbanization continue to reinforce this segment's leading position.

- Central Mexico at 41.7%: Central Mexico dominates due to its concentration of float glass manufacturing plants, proximity to automotive assembly hubs around Mexico City and Querétaro, and dense construction activity across the region's major metropolitan centers.

Mexico Glass Market Overview

The Mexico glass market encompasses the design, manufacturing, processing, and distribution of all glass product categories used across construction, automotive, and solar applications. The market spans raw material sourcing, float glass melting and forming, processing and fabrication, coating and finishing technology, and distribution and installation services that convert raw glass into finished architectural, automotive, and solar products.

Macroeconomic factors including population growth, urbanization, expanding manufacturing exports, and nearshoring-led industrial investment are accelerating glass adoption nationwide. In addition, rising automotive production, growing solar installations, and government-backed green building codes are encouraging the use of advanced, energy-efficient, and safety-certified glass products across Mexico's industrial and commercial landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

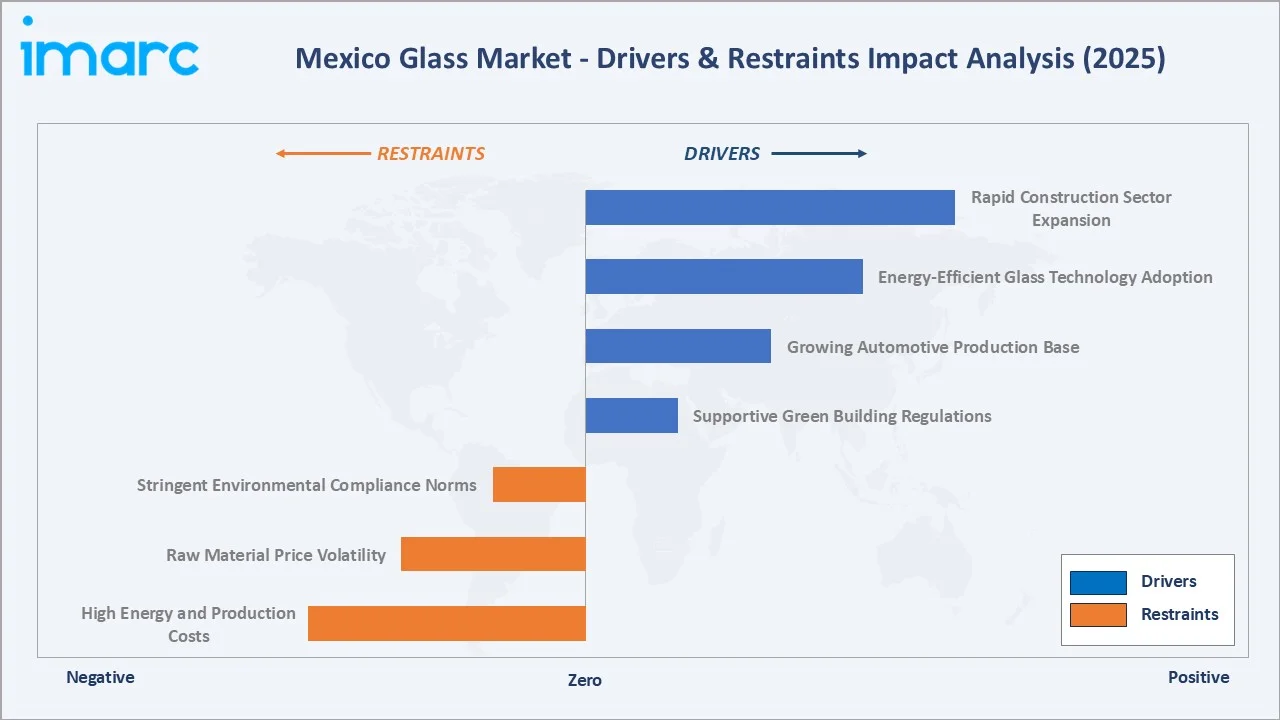

Market Drivers

- Rapid Construction Sector Expansion: Rising residential, commercial, and industrial construction activity across Mexico is generating sustained demand for facade, window, and partition glass. With growing urban developments and infrastructure improvements, architects and builders are increasingly specifying premium-quality glass for its attractiveness, energy efficiency, and longevity. The growing use of green building codes is further reinforcing demand for energy-efficient glazing across new commercial and residential developments nationwide.

- Energy-Efficient Glass Technology Adoption: Improvements in glass manufacturing technology, including smart glass, tempered glass, and energy-efficient low-emissivity coatings, are bolstering market growth. Producers are continuously refining manufacturing processes to minimize costs, increase product strength, and respond to specialized end-user requirements, while rising use of automated and robotic production lines is enhancing efficiency and uniformity in finished glass products.

- Growing Automotive Production Base: Mexico's position as a major automotive manufacturing and export hub is playing a critical role in driving glass demand. With the country serving as a production base for both domestic consumption and export, there is constant demand for windshield, side window, and sunroof glass, alongside niche products required by growing electric vehicle production.

- Supportive Green Building Regulations: Government-backed green building codes and infrastructure investment programs are encouraging the use of certified energy-efficient and safety glazing in new construction. Supportive regulatory frameworks around energy performance and building safety standards are expected to continue reinforcing structural demand for advanced glass products through the forecast period.

Market Restraints

- High Energy and Production Costs: Glass manufacturing is an energy-intensive process, and rising electricity and natural gas prices are significantly increasing operating costs across the industry. These cost pressures are particularly challenging for small and mid-sized producers, who often lack the scale to absorb input cost volatility, potentially limiting capacity expansion in price-sensitive market segments.

- Raw Material Price Volatility: Fluctuations in the cost of silica sand, soda ash, limestone, and other raw materials create pricing uncertainty across the glass supply chain. Since many of these inputs are partly imported, currency fluctuations further compound cost unpredictability for domestic manufacturers, affecting margin stability and long-term production planning.

- Stringent Environmental Compliance Norms: Stringent emission and environmental compliance requirements raise capital and operating expenditure for manufacturers, particularly older production facilities that require significant retrofitting investment. Compliance with evolving environmental norms can slow capacity expansion and increase the cost of entry for new market participants.

Market Opportunities

- Solar Glass Expansion: Rising demand for solar panel glazing presents significant growth potential as Mexico continues to expand utility-scale and rooftop solar installations to meet renewable energy targets. Companies that build solar glass production and coating capability are positioned to capture above-market growth as the renewable energy pipeline matures through 2034.

- Electric Vehicle Glass Demand: Growing electric and hybrid vehicle assembly across Mexico's automotive manufacturing base is opening opportunities for specialized lightweight, laminated, and acoustic-insulated glass products. As automakers expand EV production lines, glass suppliers with advanced automotive glazing capabilities stand to benefit from long-term supply agreements.

Market Challenges

- Raw Material Import Dependence: Dependence on imported soda ash and other specialty raw materials exposes Mexican glass manufacturers to currency fluctuations and global supply chain disruptions, which can affect production continuity and cost predictability, particularly during periods of international trade or logistics disruption.

- Skilled Labor Shortages: A shortage of skilled glass processing technicians and engineers constrains capacity expansion among regional fabricators. Training and workforce development requirements add to operating costs and can delay capacity scale-up for companies seeking to meet rising construction and automotive glass demand.

Emerging Market Trends

1. Energy-Efficient and Smart Glazing Adoption Accelerating Across Construction

Rising adoption of low-emissivity, self-cleaning, and dynamically tinted smart glass is transforming Mexico's residential and commercial construction sector. These technologies reduce energy consumption by controlling heat transfer and light penetration, helping building owners meet increasingly stringent green building codes. As energy costs rise and sustainability regulations tighten, demand for advanced coated glazing solutions is expected to grow steadily across both new construction and renovation projects nationwide.

2. Automotive Glass Demand Shifting Toward Electric Vehicle Platforms

Mexico's growing role as an electric and hybrid vehicle assembly hub is reshaping automotive glass demand toward lightweight, acoustically insulated, and laminated safety glass products. Vehicle manufacturers are increasingly specifying advanced glazing that supports weight reduction targets and enhanced cabin comfort, encouraging glass suppliers to expand specialized automotive glass production capacity to serve this evolving customer base.

3. Solar Glass Integration Expanding with Renewable Energy Investment

Growing investment in utility-scale and distributed solar installations is driving demand for specialized solar glass with high light transmittance, durability, and anti-reflective properties. As Mexico continues expanding its renewable energy capacity to meet national targets, solar glass is emerging as one of the fastest-growing product categories within the broader glass market.

4. Sustainable and Low-Carbon Glass Manufacturing Gaining Momentum

Glass manufacturers across Mexico are increasingly investing in furnace electrification, recycled cullet utilization, and energy-efficient production technologies to reduce the carbon footprint of glass manufacturing. These sustainability-linked investments are being driven by both regulatory pressure and customer demand for environmentally responsible building materials, positioning sustainable manufacturing as a long-term competitive differentiator.

Industry Value Chain Analysis

The Mexico glass value chain integrates raw material sourcing, glass melting and forming, processing and fabrication, coating and finishing, and distribution and installation, converting basic raw materials into finished architectural, automotive, and solar glass products.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Silica sand suppliers, soda ash and limestone producers, recycled cullet processors |

|

Glass Melting & Forming |

Float glass manufacturers, furnace and forming equipment operators |

|

Processing & Fabrication |

Tempering, laminating, and cutting service providers, glass processors |

|

Coating & Finishing |

Reflective and low-emissivity coating applicators, mirror backing specialists |

|

Distribution & Installation |

Glass distributors, construction contractors, automotive OEM suppliers |

The coating and finishing stage is the value chain's most technically differentiated phase, where low-emissivity and reflective coating technology determines the energy performance premium that processed and coated glass commands at retail. Efficient distribution and installation networks further sustain product quality through final handling and on-site application.

Technology Landscape in the Mexico Glass Industry

Float Glass Production Technology

Float glass production technology remains the foundation of Mexico's glass industry, enabling high-volume, uniform-thickness glass manufacturing for construction and automotive applications. Continuous investment in furnace efficiency and automated forming lines is helping manufacturers reduce energy consumption while improving output consistency and surface quality across large-scale production runs.

Low-Emissivity (Low-E) Coating Technology

Low-emissivity coating technology enables precise control over heat transfer and light transmission, helping reduce building energy consumption while maintaining natural daylighting. As green building codes expand across Mexico, coated glass technology is becoming a standard specification for new commercial and residential construction, supporting sustained demand for advanced coating production lines.

Automated Cutting, Tempering & Lamination Systems

Automated cutting, tempering, and lamination systems are improving precision, throughput, and safety compliance across glass processing operations. These systems enable manufacturers to meet the customized specifications required by construction and automotive customers while reducing material waste and production lead times, strengthening the competitiveness of Mexico's domestic glass processing sector.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Processed Glass |

34.8% |

2025 |

|

End Use Industry |

Building and Construction |

56.3% |

2025 |

|

Region |

Central Mexico |

41.7% |

2025 |

By Product Type

Processed glass leads the market at 34.8% (2025), reflecting strong demand for tempered, laminated, and insulated glass across construction and automotive safety applications requiring durability and customization.

To access detailed market analysis, Request Sample

Processed glass at 34.8% leads the Mexico glass market, reflecting strong demand for tempered, laminated, and insulated glass across construction and automotive safety applications requiring durability and customization. Processed glass's 8.1% CAGR is above the overall market rate of 7.23% through rising safety regulations and green building standards in Mexico's construction and automotive sectors, where processed glass remains the performance-driven material of choice.

By End Use Industry

Building and construction leads end use industry at 56.3% (2025), supported by Mexico's expanding residential, commercial, and infrastructure development pipeline and rising adoption of green building standards.

Building and Construction at 56.3% dominates the Mexico glass market by end use industry, driven by large-scale infrastructure development, commercial real estate expansion, and growing residential construction activity requiring high-performance glazing solutions. Building and Construction's 6.8% CAGR is supported by Mexico's urbanization momentum and green building adoption, while automotive at 24.8% benefits from Mexico's position as a major vehicle export hub, and solar glass at 10.7% remains among the fastest-growing categories as renewable energy installations expand nationwide.

Regional Market Insights

|

Region |

Share (2025) |

Key Mexico Glass Market Drivers & Characteristics |

|

Central Mexico |

41.7% |

Driven by concentration of glass manufacturing plants, automotive OEM hubs, and dense urban construction activity. |

|

Northern Mexico |

29.6% |

Supported by export-oriented manufacturing, cross-border automotive supply chains, and industrial construction. |

|

Southern Mexico |

17.5% |

Growing on rising infrastructure investment and tourism-related commercial construction. |

|

Others |

11.2% |

Reflects smaller regional markets with emerging construction and renovation activity. |

Central Mexico's leadership is anchored by its concentration of float glass plants and automotive assembly hubs around Mexico City, Querétaro, and surrounding industrial corridors, while Northern Mexico benefits from cross-border manufacturing integration with the United States.

Competitive Landscape

The Mexico glass market competitive landscape comprises integrated float glass manufacturers, global glazing majors, and regional processing specialists competing on product quality, energy efficiency, and distribution reach.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Guardian Glass, LLC |

Commercial Glass, Residential Glass |

Established Player |

Provides advanced coated and high-performance glass solutions for commercial and residential construction in Mexico. |

|

AGC Inc. |

Architectural and automotive glass |

Established Player |

Supplies automotive and flat glass products supporting Mexico's vehicle manufacturing and construction sectors. |

|

Xinyi Glass Holdings Limited |

Float glass, automotive glass, solar glass |

Challenger |

Expanding presence in Mexico through float and solar glass supply for construction and renewable energy applications. |

Key Company Profiles

Guardian Glass, LLC

Guardian Glass supplies high-performance float and coated glass products to Mexico's commercial, residential, and architectural construction sectors through an extensive regional distribution network.

- Key Products: Float glass, low-emissivity coated glass, and fabricated glass solutions.

- Recent Developments: In January 2026, Guardian Glass, LLC launched Bird1st™ UV, a bird-friendly architectural glass featuring a UV-reflective coating that helps reduce bird collisions while maintaining high transparency. The product complies with New York City's Local Law 15 bird-safe glazing requirements and expands Guardian Glass's portfolio of sustainable, energy-efficient architectural glass solutions.

- Strategic Focus: Prioritizes energy performance, architectural innovation, and regional distribution expansion.

AGC Inc.

AGC Inc. operates an automotive glass manufacturing plant in Villa de Reyes, San Luis Potosi, Mexico, supplying laminated and tempered automotive glass to vehicle manufacturers across North America.

- Key Products: Laminated and tempered automotive glass, including Wideye infrared-transparent glazing and Temperlite high-impact-resistant glass.

- Recent Developments: In March 2025, AGC Glass Europe, a subsidiary of AGC Inc., inaugurated a refurbished flat glass production line at its Barevka plant in Teplice, Czech Republic, featuring the world's first hybrid pilot furnace for flat glass manufacturing under the Volta R&D Project. The new production line is designed to significantly reduce the carbon footprint of flat glass production and supports AGC's strategy to advance low-carbon architectural glass manufacturing.

- Strategic Focus: Focuses on automotive glazing innovation, safety performance, and expanding its North American manufacturing footprint

Market Concentration Analysis

The Mexico glass market is moderately concentrated, with a small number of large integrated manufacturers controlling float glass production, while processing, fabrication, and distribution remain fragmented across numerous regional players. Leading manufacturers maintain competitive advantage through vertical integration, technology partnerships, and proximity to automotive and construction demand centers, while smaller processors compete on customization, service quality, and regional responsiveness.

Investment & Growth Opportunities

Highest Growth Segments

Solar glass (~10.4% CAGR), processed glass (~8.1% CAGR), and automotive glazing (~7.6% CAGR) represent the highest-growth product and application categories within the Mexico glass market through 2034, outpacing the overall market growth rate.

Emerging Investment Opportunities

Energy-efficient coating capacity, solar glass production scale-up, and automotive glazing specialization represent the largest near-term investment opportunities, as government sustainability programs and OEM supply agreements continue to expand addressable demand.

Investment Themes

- Sustainable Glass Manufacturing: expanding low-carbon furnace technology and recycled glass capacity to meet sustainability-linked construction demand, positioning early movers to capture premium pricing for certified low-carbon glass products.

- Automotive Glass Capacity Expansion: developing specialized automotive glazing capacity aligned with Mexico's growing electric and hybrid vehicle production base, supporting long-term OEM supply partnerships.

- Solar Glass Production Scale-Up: scaling solar glass production to support utility-scale and rooftop solar installations, capturing demand from Mexico's expanding renewable energy investment pipeline.

- Smart Manufacturing & AI-Enabled Quality Control: deploying AI-enabled quality inspection and predictive maintenance platforms on production lines to reduce defect rates and unplanned downtime, supporting margin expansion for manufacturers that adopt smart factory technology early.

Future Market Outlook (2026-2034)

The Mexico glass market is projected to grow from USD 3.81 Billion in 2025 to USD 7.13 Billion by 2034, delivering a 7.23% CAGR over the forecast period. The market's anchor value of USD 5.40 Billion by 2030 represents a structural midpoint at which energy-efficient and solar glazing technologies will have moved from early adoption toward mainstream specification, automotive glass demand will be increasingly shaped by electric vehicle production, and Central Mexico's manufacturing base will have further consolidated its position as the country's primary glass production hub.

Three structural forces underpin this growth trajectory through 2034. First, green building codes and energy-efficiency mandates across Mexican states are creating policy-backed demand for coated and low-emissivity glazing that is largely independent of short-term construction cycles. Second, Mexico's expanding role as a North American automotive and nearshoring manufacturing hub is sustaining structural demand for both architectural and automotive glass. Third, continued investment in renewable energy infrastructure is positioning solar glass as one of the market's fastest-growing categories, supported by falling technology costs and expanding utility-scale and distributed solar deployment nationwide.

Research Methodology

Primary Research

Primary research comprised structured interviews and consultations with industry stakeholders, including glass manufacturing executives, construction and automotive procurement specialists, technology providers, and regional market experts across Mexico's glass value chain.

Secondary Research

Secondary research encompassed glass industry publications, construction and automotive trade statistics, government regulatory filings, company annual reports, and market data from trade associations and international glass manufacturing bodies.

Forecasting Models

Market revenue forecasts were developed using a segment-level bottom-up model incorporating product type, end use industry, and regional demand components, validated against historical market trends and macroeconomic indicators for construction and automotive output.

Mexico Glass Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Annealed Glass, Coater Glass, Reflective Glass, Processed Glass, Mirrors |

| End User Industries Covered | Building and Construction, Automotive, Solar Glass, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | Guardian Glass LLC, AGC Inc., Xinyi Glass Holdings Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico glass market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico glass market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico glass industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Glass Market Report

The Mexico glass market reached USD 3.81 Billion in 2025, driven by rising construction activity, automotive production growth, and increasing adoption of energy-efficient glazing technologies.

The market is projected to grow at a CAGR of 7.23% during 2026-2034, reaching USD 7.13 Billion by 2034.

Processed glass leads the market with a 34.8% share in 2025, driven by demand for tempered, laminated, and insulated glass in construction and automotive applications.

Building and construction leads end use industry with a 56.3% share in 2025, supported by Mexico's expanding residential, commercial, and infrastructure development pipeline.

Central Mexico leads with a 41.7% share in 2025, supported by its concentration of glass manufacturing plants and proximity to automotive OEM hubs.

Leading companies include Guardian Glass, LLC, AGC Inc. and Xinyi Glass Holdings Limited among others.

The market is projected to reach approximately USD 5.40 Billion by 2030, anchored by sustained construction, automotive, and solar glass demand.

Solar glass integration, electric vehicle automotive glazing, and energy-efficient coating technology represent the largest growth opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)