Mexico Machine Tools Market Size, Share, Trends and Forecast by Tool Type, Technology Type, End Use Industry, and Region, 2026-2034

Mexico Machine Tools Market Size, Share, Trends & Forecast (2026-2034)

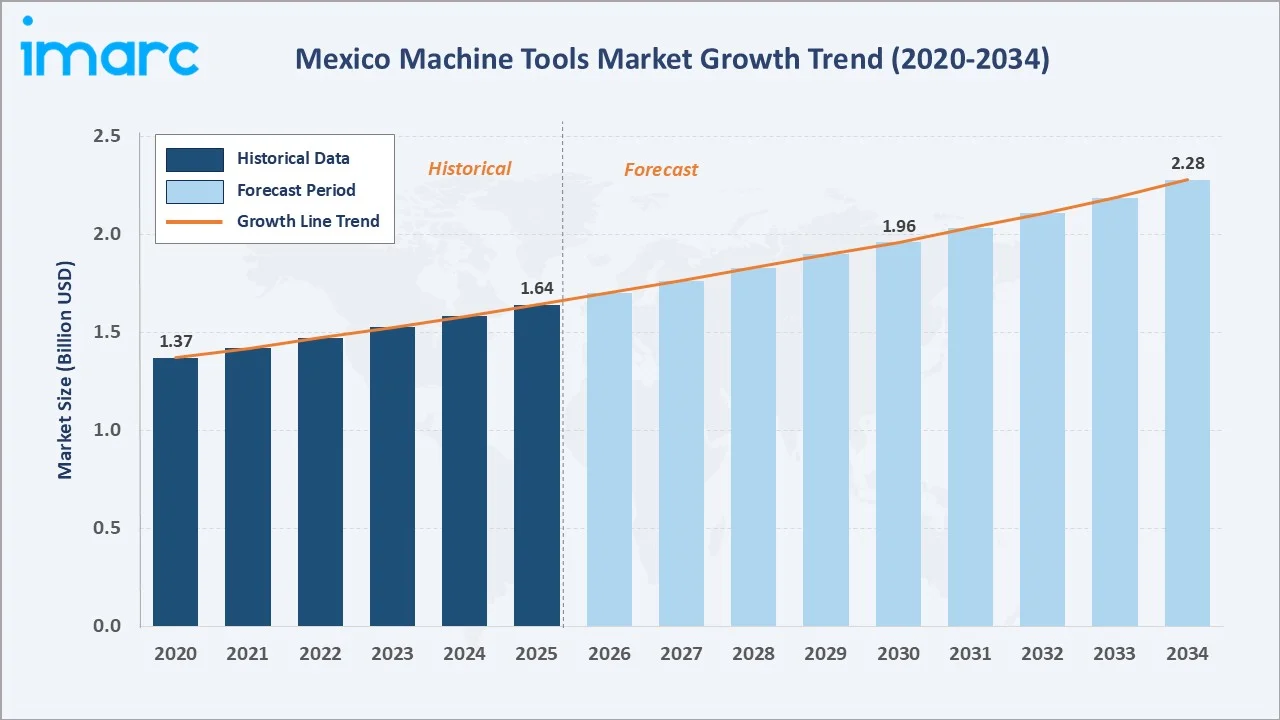

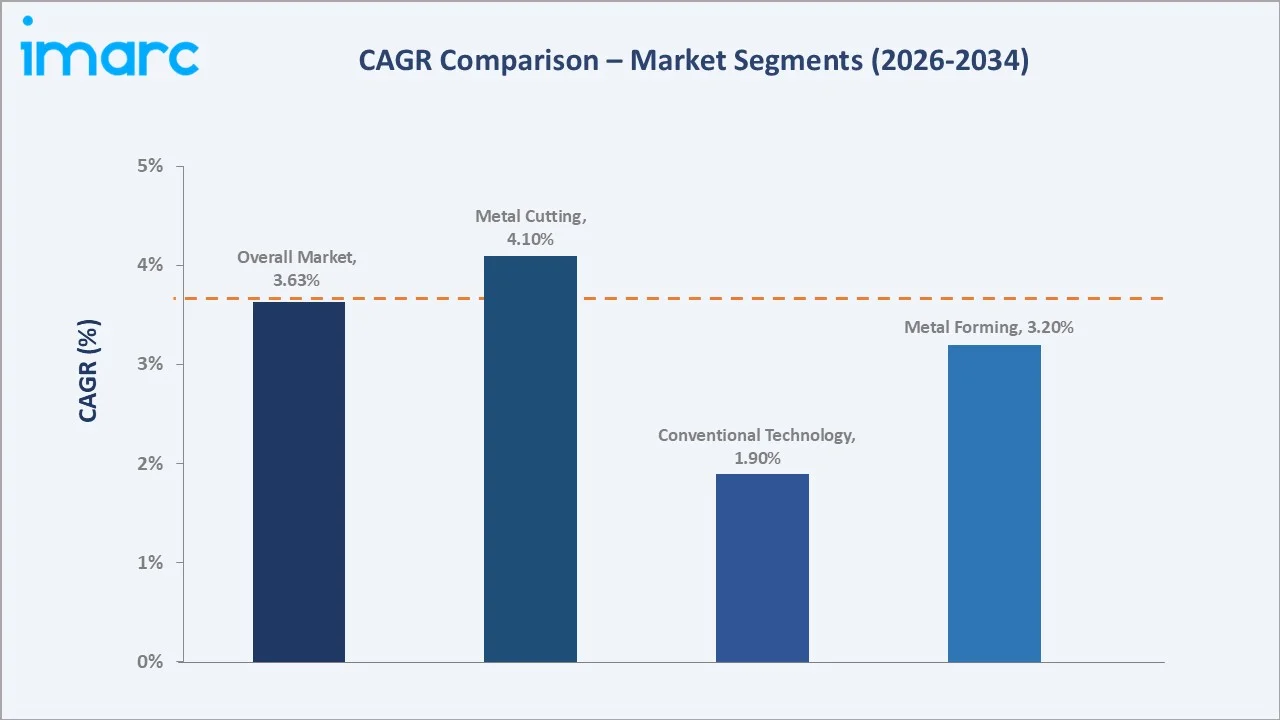

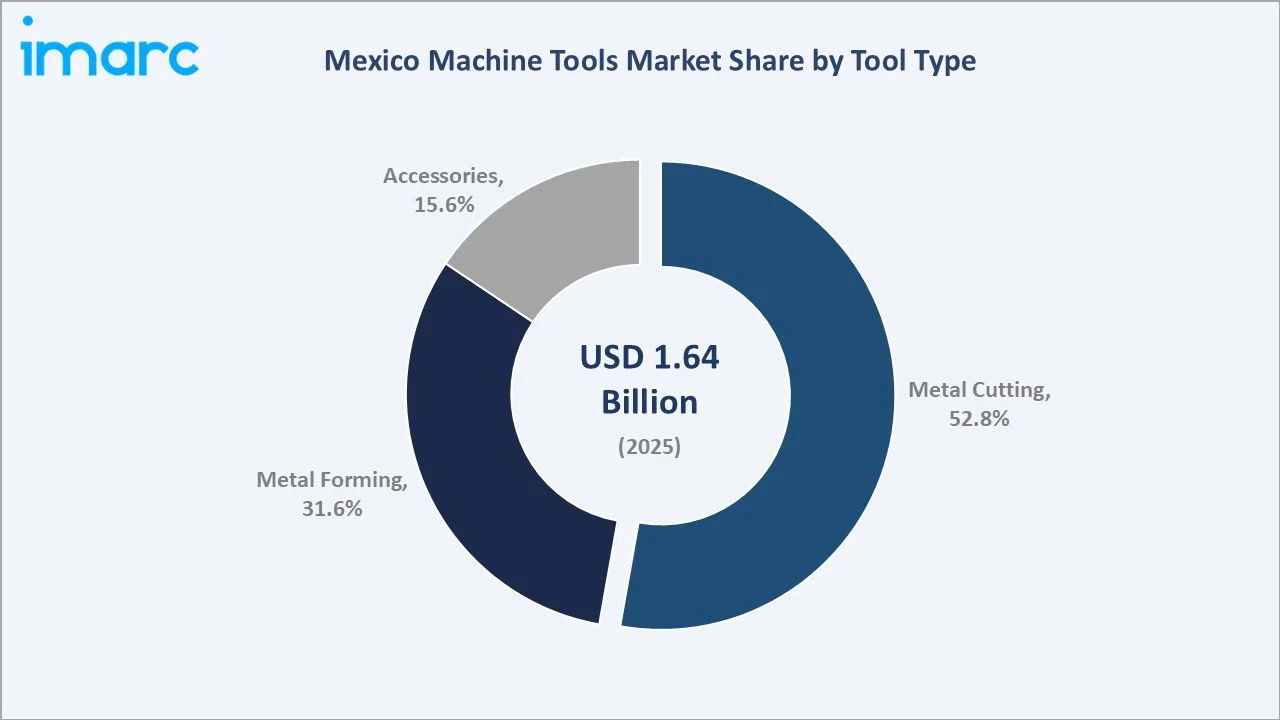

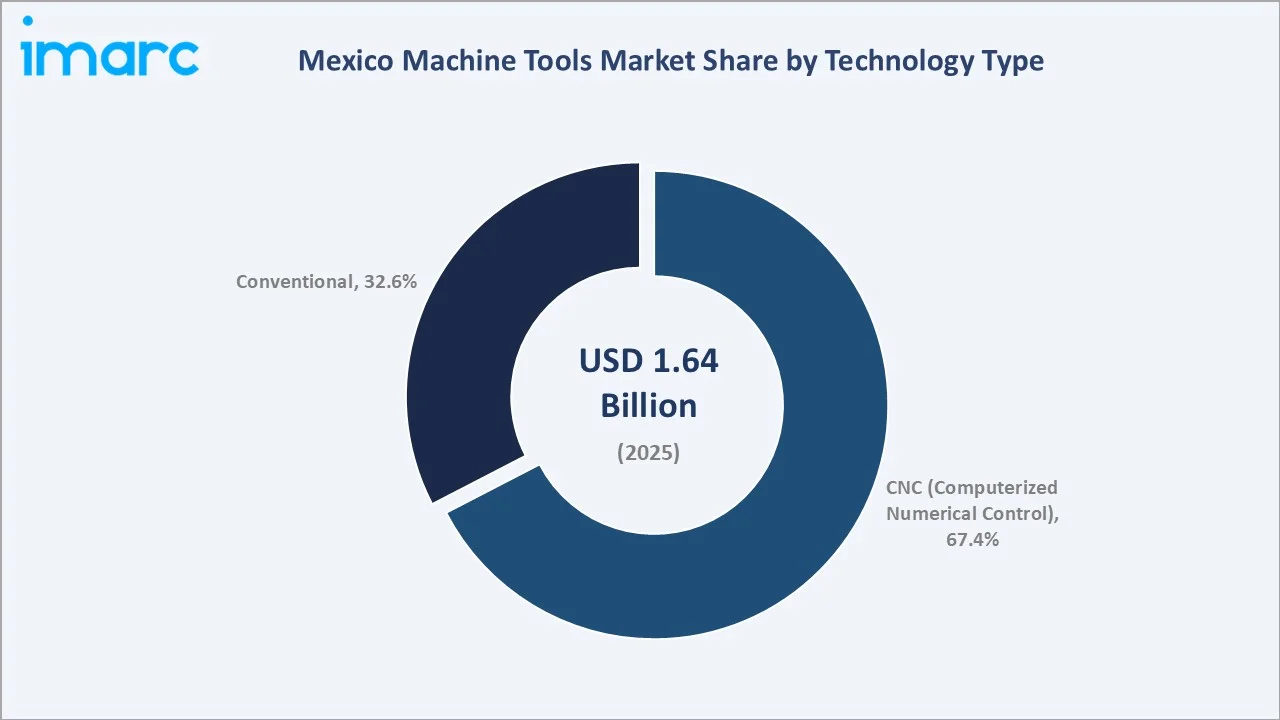

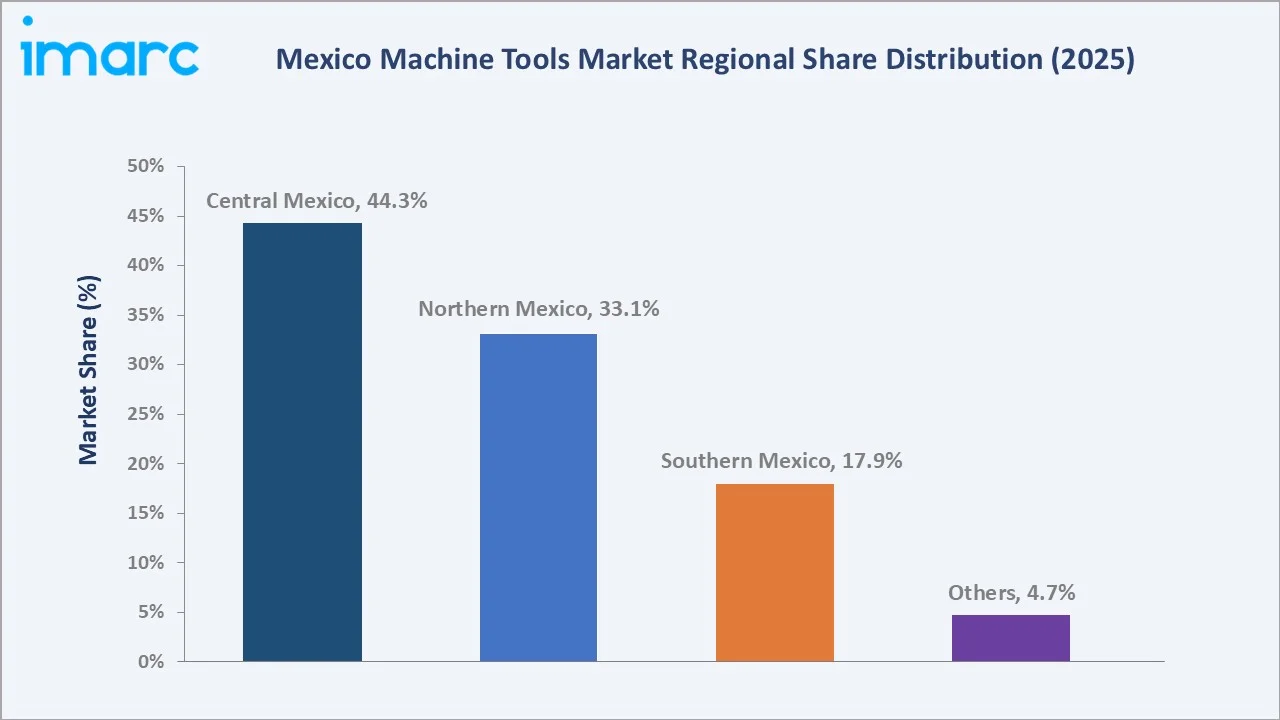

The Mexico machine tools market reached USD 1.64 Billion in 2025 and is projected to reach USD 2.28 Billion by 2034, growing at a CAGR of 3.63% during 2026-2034. The market is driven by rising industrial automation, nearshoring-led FDI inflows, automotive and aerospace expansion, USMCA trade advantages, and accelerating CNC technology adoption. Metal Cutting leads tool type at 52.8%, CNC dominates at 67.4%, and Central Mexico commands 44.3% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.64 Billion |

|

Forecast Market Size (2034) |

USD 2.28 Billion |

|

CAGR (2026-2034) |

3.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Tool Type |

Metal Cutting (52.8%, 2025) |

|

Dominant Technology Type |

CNC – 67.4% (2025) |

|

Leading Region |

Central Mexico (44.3%, 2025) |

The market expanded from USD 1.37 Billion in 2020 to USD 1.64 Billion in 2025, anchored at USD 1.96 Billion in 2030 and forecast to reach USD 2.28 Billion by 2034. The nearshoring momentum from USMCA created a structural manufacturing investment cycle that sustained machine tool demand growth even during global supply chain disruptions, which recovered sharply through 2023-2025 as new automotive and aerospace plants commenced operations in Mexico.

To get more information on this market, Request Sample

Metal Cutting at 52.8% grows at ~4.1% CAGR as EV component machining, precision aerospace parts, and automotive powertrain production require advanced CNC lathes and machining centers. CNC technology at 67.4% accelerates as Industry 4.0 adoption expands across automotive and electronics manufacturing. Central Mexico at 44.3% leads through concentration of automotive OEMs, aerospace facilities, and precision engineering clusters in the Bajío industrial region.

Executive Summary

The Mexico machine tools market reached USD 1.64 Billion in 2025, representing one of Latin America's most dynamic manufacturing equipment markets shaped by nearshoring trends and industrial modernization. The market is projected to reach USD 2.28 Billion by 2034, delivering steady growth anchored by automotive production expansion and CNC technology adoption across the manufacturing base.

Metal Cutting at 52.8% dominates by serving the highest-value precision machining applications across automotive, aerospace, and engineering sectors. CNC technology at 67.4% leads through superior productivity, repeatability, and Industry 4.0 integration capability. Central Mexico at 44.3% commands the largest regional share through its dense concentration of Tier-1 automotive suppliers and global OEM facilities in the Bajío and Mexico City industrial corridors.

Key Market Insights

|

Insight |

Data |

|

Dominant Tool Type |

Metal Cutting – 52.8% share (2025) |

|

Dominant Technology |

CNC (Computerized Numerical Control) – 67.4% market share (2025) |

|

Leading Region |

Central Mexico – 44.3% market share (2025) |

|

Market Opportunity |

CNC adoption in SMEs; nearshoring-driven FDI; EV component machining; aerospace precision tooling |

Key Analytical Observations Supporting the Above Data:

- Metal Cutting at 52.8%: The metal cutting segment dominates as it serves the most precision-demanding applications in Mexico's automotive and aerospace manufacturing base. Advanced CNC machining centers and turning centers enable high-volume, tight-tolerance component production required by automotive OEMs and their Tier-1 supplier networks established across the Bajío industrial region.

- CNC at 67.4%: CNC technology leads as manufacturers increasingly require programmable, repeatable, and IoT-compatible machine tools to support Industry 4.0 factory operations. The USMCA-driven influx of automotive and electronics FDI demands CNC-equipped production lines with digital integration capability across Mexico's manufacturing base.

- Central Mexico at 44.3%: Central Mexico leads through its high density of automotive OEMs, aerospace manufacturers, and precision engineering facilities in industrial clusters around Querétaro, San Luis Potosí, Guanajuato, and the Mexico City metropolitan industrial area.

Mexico Machine Tools Market Overview

The Mexico machine tools market encompasses the procurement, sale, and servicing of all power-driven machines used to shape, cut, form, and finish metals and other materials across manufacturing industries. The market covers metal cutting machines, metal forming machines, and associated accessories sold to automotive, aerospace, electrical, consumer goods, and precision engineering end users.

The ecosystem integrates global machine tool OEMs, authorized Mexican distributors, CNC controller suppliers, cutting tool manufacturers, industrial automation integrators, and manufacturing plants. Macroeconomic factors include nearshoring momentum from USMCA, automotive electrification investment, FDI incentives, government nearshoring policy, and expansion of industrial parks near U.S. border states and the Bajío region.

Market Dynamics

To evaluate market opportunities, Request Sample

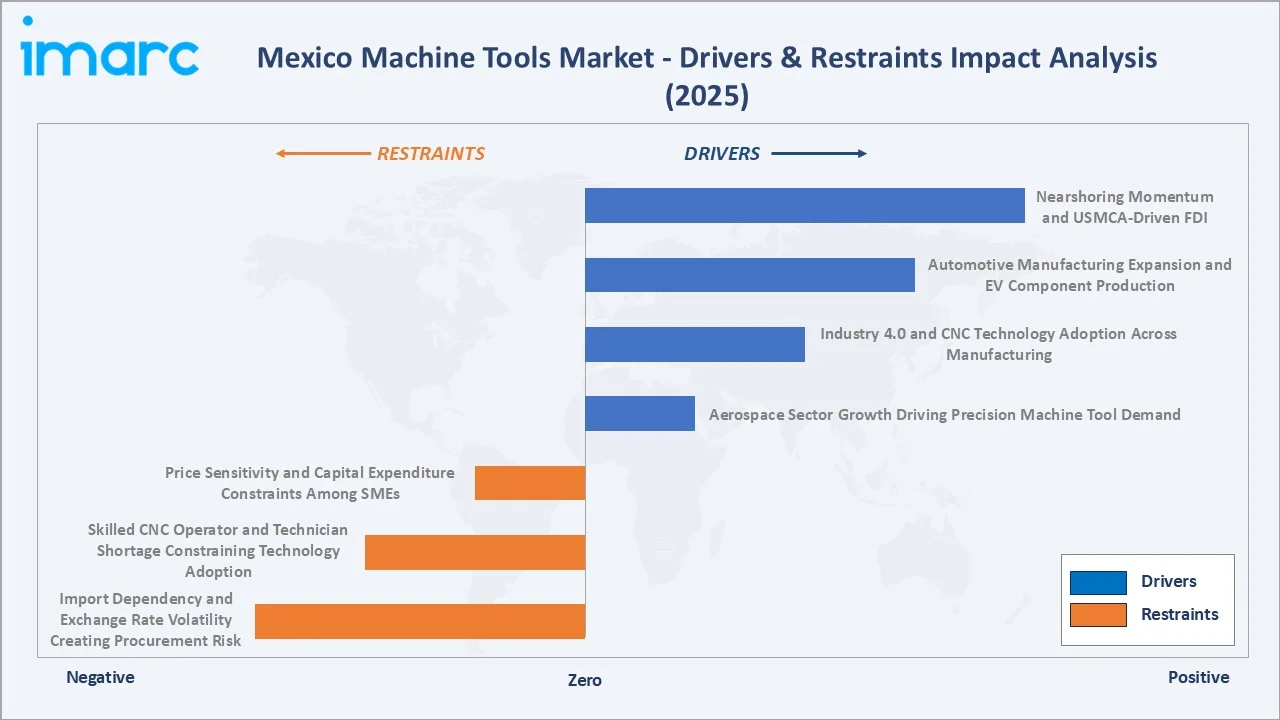

Market Drivers

- Nearshoring Momentum and USMCA-Driven FDI: Mexico continues attracting substantial manufacturing FDI driven by USMCA trade advantages and nearshoring strategies. Mexico's Ministry of Economy reported 209 FDI initiatives generating over 99,700 jobs from January to September 2024, with USD 64 Billion in investments, of which manufacturing accounts for 56% of FDI inflow, directly increasing demand for CNC machine tools to equip new production facilities across Mexico.

- Automotive Manufacturing Expansion and EV Component Production: Mexico is the world's seventh-largest automotive producer, with major OEMs expanding EV component production. Automakers require advanced CNC machining centers, turning machines, and grinding equipment to produce lightweight structures, battery casings, motor components, and powertrain parts. The EV transition accelerates demand for precision metal cutting tools capable of machining aluminum, composites, and specialty steels.

- Industry 4.0 and CNC Technology Adoption Across Manufacturing: Industrial automation adoption is accelerating across Mexico's manufacturing sector. Companies are investing in smart factories with CNC machines, robotics, and IoT-connected systems to increase productivity and reduce human error. CNC machine tools with digital controls and Industry 4.0 integration are in high demand, as evidenced by FABTECH Mexico 2025 in Monterrey attracting 12,970 professionals and showcasing 350+ machines across 27,000 square meters.

- Aerospace Sector Growth Driving Precision Machine Tool Demand: Mexico's aerospace manufacturing sector, concentrated in Querétaro and Baja California, is driving demand for high-precision 5-axis machining centers and grinding machines. Aerospace components require exceptionally tight tolerances achievable only with advanced CNC machine tools. Rising aircraft production orders from global aerospace OEMs translate into sustained capital investment in precision machine tools across Mexico.

Market Restraints

- Price Sensitivity and Capital Expenditure Constraints Among SMEs: Mexico's manufacturing base includes a large proportion of small and medium enterprises operating with limited capital budgets. High upfront costs of advanced CNC machine tools create access barriers. SMEs often defer capital investment in modern machine tools, limiting market penetration of premium CNC equipment and sustaining demand for lower-cost conventional alternatives in job shop and general machining segments.

- Skilled CNC Operator and Technician Shortage Constraining Technology Adoption: A shortage of qualified CNC operators, programmers, and maintenance technicians constrains machine tool adoption in Mexico. Advanced CNC machines require specialized training for programming, operation, and upkeep. The skills gap increases operational risk for manufacturers considering CNC upgrades, slowing technology adoption and creating productivity gaps that limit the full economic return on machine tool investment.

- Import Dependency and Exchange Rate Volatility Creating Procurement Risk: Mexico relies heavily on imported machine tools from Germany, Japan, and the United States. Exchange rate volatility between the Mexican peso and major currencies directly increases the local-currency cost of imported machine tools. Currency depreciation episodes reduce purchasing power for capital equipment buyers, suppressing demand and extending investment decision cycles among domestically focused manufacturers.

Market Opportunities

- CNC Technology Adoption in SME Segment: The growing affordability of entry-level CNC machine tools and supportive government training programs are opening CNC adoption opportunities in Mexico's large SME manufacturing base. As mid-range CNC machine prices decline and financing options expand, SMEs are increasingly transitioning from conventional to CNC equipment, creating a significant untapped demand pool for machine tool suppliers targeting this segment.

- Nearshoring-Driven Greenfield Manufacturing Investment: The sustained nearshoring momentum driven by USMCA and global supply chain diversification is creating large-scale greenfield manufacturing investment opportunities across Mexico's industrial zones. New automotive, electronics, and aerospace facilities require comprehensive machine tool procurement programs, offering machine tool OEMs and distributors substantial order opportunities through the forecast period.

Market Challenges

- Local Content and Technology Transfer Requirements Creating Supplier Pressure: Government industrial policy initiatives and automotive OEM local content requirements are creating pressure on global machine tool suppliers to establish deeper local manufacturing and service infrastructure in Mexico. Meeting local content thresholds while maintaining technology standards and cost competitiveness presents a structural challenge for international machine tool OEMs operating in the Mexican market.

- Competition from Lower-Cost Asian Machine Tool Suppliers Intensifying in Mexico: Lower-cost machine tool manufacturers from China, Taiwan, and South Korea are increasingly competing in Mexico's mid-market and SME machine tool segments, offering competitive pricing that challenges established Japanese, German, and American suppliers. As the quality gap narrows, price pressure intensifies across the conventional and entry-level CNC machine tool segments throughout Mexico's manufacturing regions.

Emerging Market Trends

1. Smart Factory Integration and Industry 4.0 Machine Tool Connectivity

Machine tool manufacturers are embedding IoT sensors, real-time monitoring, and digital twin capabilities into CNC systems. Mexican manufacturers are adopting cloud-connected machine tools to enable predictive maintenance, reduce unplanned downtime, and improve quality control. This trend is accelerating as automotive, and electronics OEMs mandate Industry 4.0 compliance across their Mexican supplier networks throughout the industrial zones.

2. Five-Axis Machining Adoption for Aerospace and EV Component Complexity

Five-axis CNC machining centers are gaining adoption in Mexico's aerospace and EV manufacturing sectors. These machines enable complex geometries, reduce fixturing requirements, and improve surface finish quality. As Mexico's aerospace cluster in Querétaro expands and EV component machining requirements intensify, 5-axis machining center demand is growing above the overall market CAGR through 2034.

3. Collaborative Robotics Integration with CNC Machine Tool Systems

Collaborative robots are being integrated with CNC machine tools for automated part loading, unloading, and quality inspection in Mexican manufacturing facilities. This combination extends machine utilization hours, reduces manual labor costs, and improves process consistency. Nearshoring manufacturers establishing new facilities in Mexico are prioritizing collaborative robot-equipped machine tool cells as standard configuration.

4. Local Service Network Expansion by Global Machine Tool Suppliers in Mexico

Global machine tool OEMs are expanding their local service networks in Mexico to support growing installed bases. Localized spare parts inventories, certified service technicians, and rapid-response maintenance contracts are becoming competitive differentiators. Cincinnati Incorporated expanded its Mexican distribution network through its long-standing partner Samat, reinforcing the trend of enhanced local market commitment.

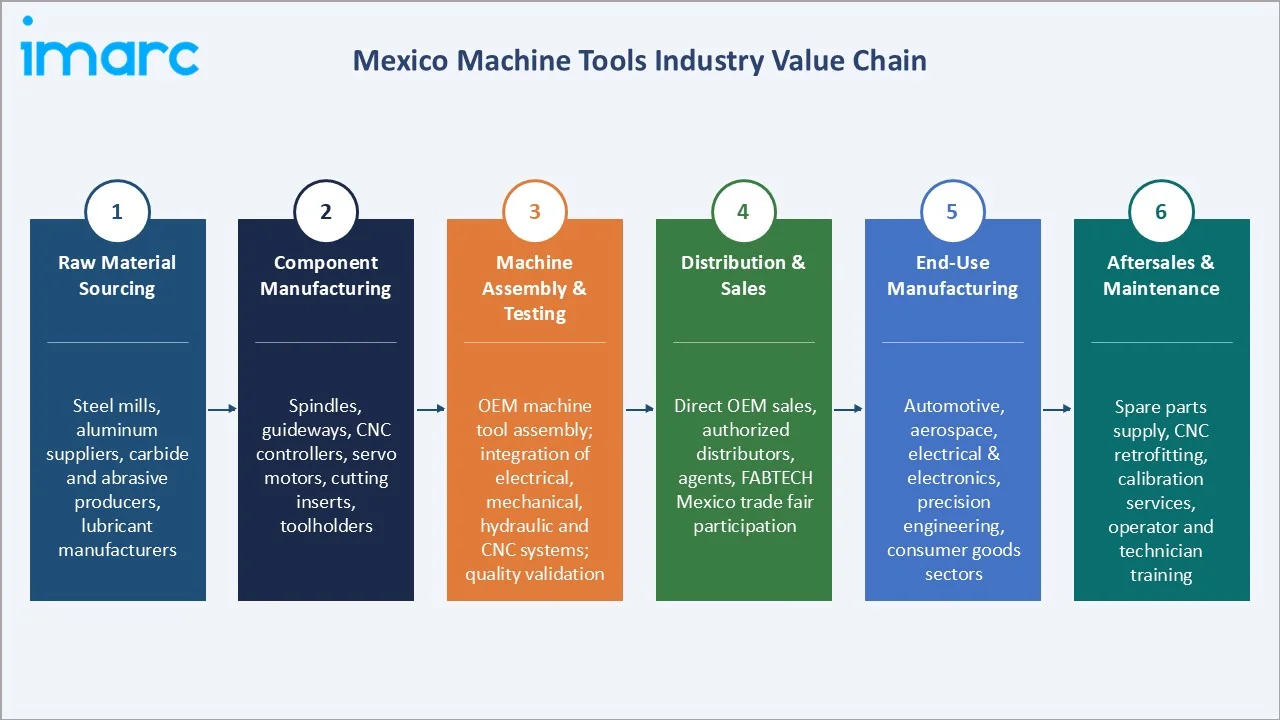

Industry Value Chain Analysis

The Mexico machine tools value chain integrates raw material and component sourcing, machine assembly and testing, distribution and sales, end-use manufacturing deployment, and aftersales maintenance. The commercial architecture is progressively shifting toward integrated automation cells combining machine tools with robotic systems as automotive and electronics OEMs seek turnkey production solutions.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Steel mills, aluminum suppliers, carbide and abrasive producers, lubricant manufacturers |

|

Component Manufacturing |

Spindles, guideways, CNC controllers, servo motors, cutting inserts, toolholders |

|

Machine Assembly & Testing |

OEM machine tool assembly; integration of electrical, mechanical, hydraulic and CNC systems; quality validation |

|

Distribution & Sales |

Direct OEM sales, authorized distributors, agents, FABTECH Mexico trade fair participation |

|

End-Use Manufacturing |

Automotive, aerospace, electrical & electronics, precision engineering, consumer goods sectors |

|

Aftersales & Maintenance |

Spare parts supply, CNC retrofitting, calibration services, operator and technician training |

The distribution and sales tier is the Mexico machine tools value chain's most commercially critical stage for international OEMs. Authorized distributors with strong technical service capabilities and local spare parts availability command premium positioning. Aftersales service capability is increasingly a primary purchase criterion as manufacturers prioritize uptime reliability over initial machine tool purchase price.

Technology Landscape in the Mexico Machine Tools Industry

CNC (Computerized Numerical Control) Technology

CNC technology offers superior programmability, repeatability, and digital integration capability, making it the dominant choice for precision manufacturing across Mexico's automotive, aerospace, and electronics sectors. CNC machine tools enable complex part geometries, multi-axis operations, and real-time process monitoring, supporting higher productivity and tighter dimensional tolerances. Their compatibility with Industry 4.0 systems is accelerating adoption across Mexico's growing manufacturing base.

Conventional Machine Tool Technology

Conventional machine tools offer operational simplicity, lower upfront cost, and minimal operator training requirements, making them suitable for basic machining tasks in SMEs, educational institutions, and maintenance workshops. While conventional technology is being progressively displaced by CNC in high-volume and precision applications, it remains relevant for cost-sensitive buyers requiring straightforward metal cutting and forming capabilities without complex digital controls.

Five-Axis and Multi-Tasking Machining Technology

In July 2025, DMG Mori launched eight world premieres focused on Machining Transformation (MX) pillars, featuring new 5-axis models including the DMC 55 H Twin and DMC 65 monoBLOCK 2, targeting aerospace and precision engineering applications. Five-axis and multi-tasking CNC technology enables single-setup machining of complex components, reducing cycle time and improving accuracy for Mexico's aerospace and automotive powertrain manufacturing sectors, driving adoption in high-value precision manufacturing clusters.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Tool Type |

Metal Cutting |

52.8% |

2025 |

|

Technology Type |

CNC |

67.4% |

2025 |

|

End Use Industry |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

44.3% |

2025 |

By Tool Type

Metal Cutting leads at 52.8% in 2025, encompassing CNC machining centers, CNC lathes, grinding machines, and laser cutting systems serving the highest-value precision manufacturing applications across Mexico's automotive, aerospace, and precision engineering sectors.

To access detailed market analysis, Request Sample

Metal Forming at 31.6% captures press brakes, stamping presses, and roll forming machines serving Mexico's high-volume automotive body panel, chassis, and structural component production. Accessories at 15.6% represent cutting inserts, toolholders, workholding devices, and machine attachments supporting the overall installed base of metal cutting and forming machines across manufacturing sectors.

By Technology Type

CNC technology at 67.4% dominates through its productivity, repeatability, and digital integration advantages for high-volume and precision manufacturing. CNC machine tools are mandated by automotive and aerospace OEMs for component supply qualification, driving accelerating adoption across Mexico's Tier-1 and Tier-2 supplier base throughout the industrial corridors.

Conventional technology at 32.6% persists in smaller job shops, educational institutions, and maintenance machining applications where the investment justification for CNC equipment is not yet established. Conventional machine tools serve cost-sensitive buyers requiring basic metal shaping capability without the programming complexity and capital cost of CNC systems across Mexico.

Regional Market Insights

|

Region |

Share (2025) |

Key Machine Tools Market Drivers & Characteristics |

|

Central Mexico |

44.3% |

Industrial hub; major automotive OEMs in Bajío; Querétaro aerospace cluster; highest FDI concentration in manufacturing |

|

Northern Mexico |

33.1% |

USMCA nearshoring advantage; maquiladora zones; Monterrey metalworking cluster; border state manufacturing density |

|

Southern Mexico |

17.9% |

Growing via Special Economic Zones; Interoceanic Corridor investment; early-stage demand for basic machine tools |

|

Others |

4.7% |

Emerging industrial corridors with early-stage demand for entry-level machine tool capabilities |

Central Mexico at 44.3% leads through Mexico's highest concentration of industrial manufacturing activity. The Bajío region, encompassing Querétaro, Guanajuato, Aguascalientes, and San Luis Potosí, hosts major automotive OEMs and their Tier-1 supplier networks requiring advanced CNC machine tools for high-precision component production across multiple vehicle platforms and aerospace manufacturing programs.

Northern Mexico at 33.1% reflects the maquiladora manufacturing ecosystem concentrated along the U.S. border from Tijuana to Matamoros. USMCA nearshoring has intensified FDI in Monterrey's metalworking cluster and border-state manufacturing parks, driving sustained demand for machine tools across electronics, automotive, and general manufacturing sectors with proximity advantage to U.S. supply chains.

Southern Mexico at 17.9% represents a growing but earlier-stage market supported by government Special Economic Zones and the Interoceanic Corridor infrastructure investment. New manufacturing investment is gradually increasing demand for basic to intermediate machine tool capabilities across the southern industrial corridor, particularly for light manufacturing and assembly operations.

Competitive Landscape

The Mexico machine tools competitive landscape is moderately concentrated with global Tier-1 OEMs dominating through technology leadership, service network depth, and brand positioning, while regional distributors and lower-cost Asian suppliers compete on price in SME and conventional machining segments across Mexico.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

DMG Mori Co., Ltd. |

CNC Machining Centers, Turn-Mill Machines |

Market Leader |

Global Tier-1; advanced CNC platforms; EV-specific 5-axis machining solutions for Mexico automotive OEMs |

|

Yamazaki Mazak Corporation |

Multi-Tasking Turning Centers, 5-Axis Machining Centers |

Market Leader |

Multi-tasking and smart factory IoT integration; enhanced digital twin and CNC connectivity |

|

Trumpf |

Laser Cutting Systems, CNC Punching Machines |

Strong Challenger |

Sheet metal processing leadership; high-power fiber laser cutting and smart factory integration |

|

AMADA CO., LTD. |

Laser Cutting Machines, Press Brakes, Punch Presses |

Strong Challenger |

Sheet metal fabrication specialist; expanded Mexico distribution and service partnerships |

|

Haas Automation, Inc |

CNC Vertical Machining Centers, CNC Lathes |

Established Player |

Affordable CNC for SMEs; strong North American presence; high installed base in Mexico job shops |

|

Okuma Corporation |

CNC Lathes, Machining Centers, Grinders |

Established Player |

Thermal stability technology; Thermo-Friendly Concept for precision in Mexico's manufacturing environment |

Key players include DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Trumpf, AMADA CO., LTD., Haas Automation, Inc, Okuma Corporation, and others.

Key Company Profiles

DMG Mori Co., Ltd.

DMG Mori Co., Ltd. is a Japan-Germany joint company and global leader in CNC machine tool manufacturing with strong presence in Mexico's automotive and aerospace manufacturing sectors through its advanced CNC machining centers and turning machines deployed across major manufacturing clusters in the Bajío and northern border regions.

- Key Products: CNC Machining Centers (DMC series), CNC Turning Centers (CLX, CTX series), 5-Axis Machining Centers, Hybrid Additive-Subtractive Machines.

- Strategic Focus: Expanding integrated CNC machining solutions with digital platform connectivity, combining machine tools with IoT monitoring and predictive maintenance for smart factory integration across automotive and aerospace manufacturing clusters in Mexico.

Yamazaki Mazak Corporation

Yamazaki Mazak Corporation is a Japan-based global machine tool manufacturer specializing in multi-tasking machines, 5-axis machining centers, and smart factory integration solutions with significant market presence across Mexico's precision manufacturing sectors in automotive and aerospace industries.

- Key Products: Multi-Tasking Machining Centers (INTEGREX series), 5-Axis CNC Machining Centers (VARIAXIS series), CNC Turning Centers (QUICK TURN series), Laser Cutting Machines.

- Strategic Focus: Strengthening smart factory integration capabilities through advanced CNC control systems and machine connectivity solutions, enabling Mexico manufacturers to achieve higher automation levels across automotive and precision engineering applications.

Trumpf

Trumpf is a Germany-based global technology leader in laser cutting systems and CNC sheet metal processing machines with strong positioning in Mexico's automotive, aerospace, and general manufacturing sheet metal fabrication sectors through direct sales and distributor networks.

- Key Products: TruLaser Fiber Laser Cutting Systems, TruBend Press Brakes, TruPunch CNC Punching Machines, TruMatic Combination Machines.

- Strategic Focus: Expanding fiber laser cutting system portfolio with higher power options and automated material handling integration, enabling high-throughput fabrication operations for Mexico's growing automotive and aerospace manufacturing base through the forecast period.

Market Concentration Analysis

The Mexico machine tools market is moderately concentrated at the global OEM and authorized distributor level, with the top four key players collectively accounting for approximately 35-45% of Mexico's CNC machine tool revenue. Authorized distributor networks account for an estimated 60-70% of total machine tool sales volume in Mexico, as most international OEMs operate through local distribution rather than direct sales infrastructure.

Market concentration is declining over the forecast period as lower-cost Asian machine tool manufacturers from China, Taiwan, and South Korea gain quality certification and market acceptance in Mexico's SME and mid-market segments. Nearshoring-driven demand growth is creating sufficient market expansion to sustain revenue growth for established global OEMs even as new entrants capture incremental market share across the conventional and entry-level CNC segments through 2034.

Investment & Growth Opportunities

Highest Growth Segments

Metal Cutting tool type (~4.1% CAGR), CNC technology adoption in SME segment (~5.2% CAGR from lower base), 5-axis machining center segment (~6.5% CAGR driven by aerospace and EV applications), collaborative robot-integrated CNC cells (~8-10% CAGR from smaller base), Central Mexico industrial cluster expansion (~4.3% CAGR), and Northern Mexico nearshoring manufacturing corridor (~4.0% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

EV component machining represents the Mexico machine tools market's highest per-unit-value emerging opportunity, with battery casing, motor housing, and powertrain component machining centers at USD 250,000-800,000 per unit generating 3-5x the per-unit revenue of standard machining centers at equivalent specifications. USMCA-mandated regional content requirements for automotive production create structurally growing demand for advanced machine tools throughout Mexico's automotive manufacturing corridor through 2034.

Investment Themes

- CNC machine tool distribution and service network expansion targeting nearshoring manufacturers in Mexico: The sustained nearshoring investment wave is creating large-scale machine tool procurement opportunities across Mexico's industrial zones. Machine tool distributors with strong technical service capabilities, local spare parts inventories, and certified technician networks are positioned to capture premium market share as new automotive, aerospace, and electronics facilities require ongoing machine tool support infrastructure throughout the forecast period.

- Five-axis machining center positioning for automotive EV component and aerospace precision applications in Mexico: Mexico's expanding EV component manufacturing base and growing aerospace cluster in Querétaro are driving demand for 5-axis CNC machining centers capable of handling complex geometries in aluminum, titanium, and specialty alloys. Suppliers positioning advanced 5-axis machining solutions with Mexico-specific application support, operator training, and productivity guarantees are best placed to capture this high-value emerging procurement segment through 2034.

Future Market Outlook (2026-2034)

The Mexico machine tools market is projected to grow from USD 1.64 Billion in 2025 to USD 2.28 Billion by 2034, delivering a 3.63% CAGR over the forecast period. The market's anchor value of USD 1.96 Billion in 2030 represents a machine tools industry at a significant structural inflection, where CNC technology will have displaced conventional machine tools as the dominant format across most Mexico's manufacturing sectors, and nearshoring-driven manufacturing investment will have deepened both demand volume and quality requirements for advanced machine tools.

Three structural forces define Mexico machine tools market growth through 2034 with high confidence. The nearshoring manufacturing investment cycle creates a self-reinforcing demand dynamic where new facilities generate sustained machine tool procurement demand across both initial equipment and ongoing replacement cycles. The automotive electrification transition multiplies the precision machining requirements per vehicle above simple production volume growth, creating an additional demand multiplier for advanced CNC machine tools. The aerospace sector expansion in Querétaro and broader Mexico industrial zones creates additive high-precision machine tool demand above the already steady automotive and general manufacturing demand base.

Research Methodology

Primary Research

Primary research comprised structured interviews with 40+ industry stakeholders (2025), including machine tool OEM country managers, authorized distributor executives, automotive Tier-1 procurement managers, aerospace manufacturing engineers, and industrial automation specialists operating across Mexico's major manufacturing regions.

Secondary Research

Secondary research encompassed company annual reports, Mexico Ministry of Economy FDI reports, INEGI industrial production statistics, FABTECH Mexico 2025 exhibition data, USMCA trade flow analysis, and machine tool import data from Mexico's Secretariat of Economy. Over 50 secondary sources reviewed comprehensively.

Forecasting Models

Market revenue forecasts developed using end-use demand-based bottom-up model: (i) manufacturing output growth by sector in Mexico; (ii) capital expenditure rates for machine tools by sector; (iii) machine tool replacement cycle and installed base expansion; (iv) technology mix shift from conventional to CNC applying historical adoption trajectory across industrial segments.

Mexico Machine Tools Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Tool Types Covered | Metal Cutting, Metal Forming, Accessories |

| Technology Types Covered | Conventional, CNC (Computerized Numerical Control) |

| End Use Industries Covered | Automotive, Aerospace and Defense, Electrical and Electronics, Consumer Goods, Precision Engineering, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Trumpf, AMADA CO., LTD., Haas Automation, Inc, Okuma Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico machine tools market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico machine tools market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico machine tools industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Machine Tools Market Report

The Mexico machine tools market reached USD 1.64 Billion in 2025, driven by nearshoring FDI, automotive expansion, CNC technology adoption, Metal Cutting leading at 52.8%, CNC at 67.4%, and Central Mexico commanding 44.3% regional share in the Bajío industrial region.

The Mexico machine tools market grows at 3.63% CAGR during 2026-2034, reaching USD 2.28 Billion by 2034, reflecting steady FDI-driven manufacturing expansion, CNC penetration into SME segments, and automotive and aerospace sector sustained growth.

Metal Cutting leads at 52.8% in 2025, capturing the highest-value precision machining applications across automotive, aerospace, and precision engineering sectors. Metal Cutting grows at approximately 4.1% CAGR through EV component machining demand and aerospace precision requirements.

CNC (Computerized Numerical Control) technology dominates at 67.4% in 2025, driven by automotive and aerospace OEM qualification requirements, Industry 4.0 adoption, and the productivity advantages of programmable machining over conventional manual operation across all manufacturing sectors.

Central Mexico leads at 44.3% through its concentration of automotive OEMs, aerospace facilities, and precision engineering clusters in the Bajío industrial region encompassing Querétaro, Guanajuato, Aguascalientes, and San Luis Potosí.

Leading companies include DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Trumpf, AMADA CO., LTD., Haas Automation, Inc, Okuma Corporation, and others.

The Mexico machine tools market is projected to reach approximately USD 1.96 Billion by 2030, with CNC machine tools achieving above 72% technology share, EV component machining creating new demand pools, and nearshoring FDI sustaining capital investment in advanced manufacturing equipment.

Three priority investment opportunities: CNC machine tool distribution and service network expansion targeting nearshoring manufacturers, 5-axis machining center positioning for automotive EV component and aerospace applications, and collaborative robot integration services combining CNC machine tools with automation systems for SME market penetration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)