Mexico Oil and Gas Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Mexico Oil and Gas Market Summary:

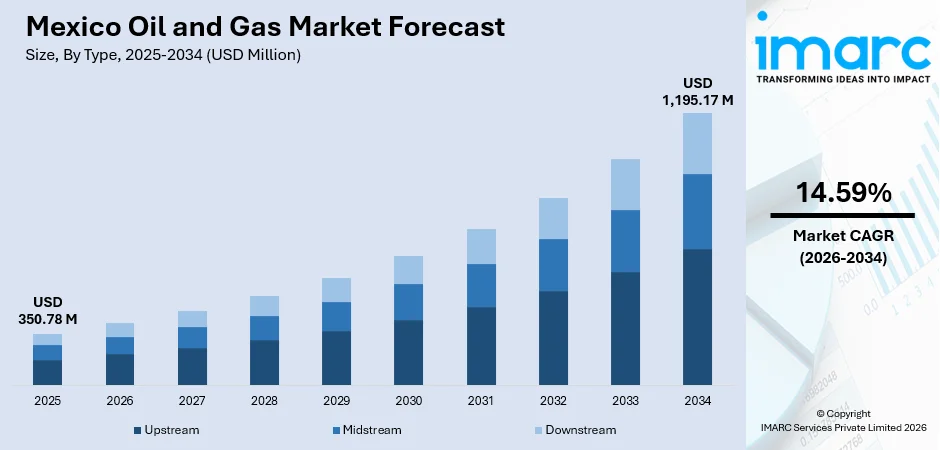

The Mexico oil and gas market size was valued at USD 350.78 Million in 2025 and is projected to reach USD 1,195.17 Million by 2034, growing at a compound annual growth rate of 14.59% from 2026-2034.

The Mexico oil and gas market is expanding as the country pursues upstream modernization, deepwater exploration, and infrastructure investments to reverse production declines. Energy reform initiatives, mixed contract frameworks, and rising natural gas consumption for power generation are reshaping the sector. Strengthening pipeline networks, growing refinery rehabilitation programs, and emerging LNG export capacity are further positioning Mexico as a strategic energy hub, driving sustained demand across upstream, midstream, and downstream value chains within the Mexico oil and gas market share.

Key Takeaways and Insights:

- By Type: Upstream dominates the market with a share of 49.5% in 2025, driven by intensified exploration activities, deepwater field development, and government-backed production recovery programs.

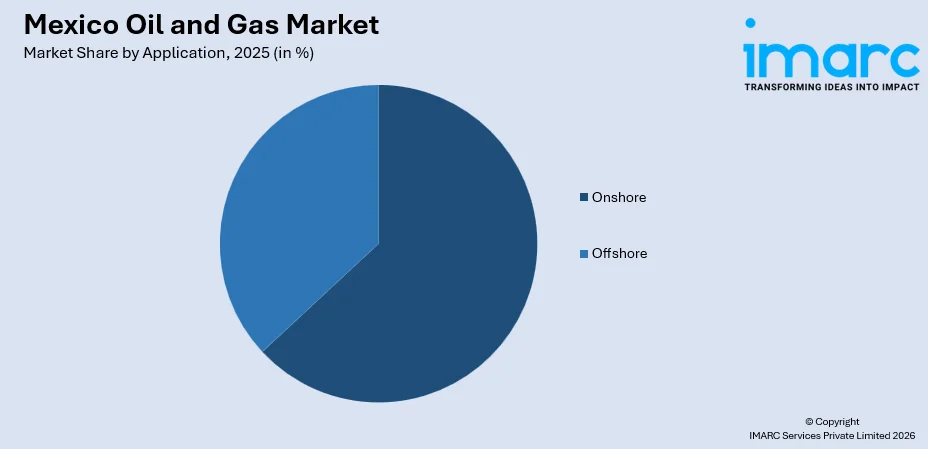

- By Application: Onshore leads the market with a share of 63.2% in 2025, supported by established production basins, mature field rehabilitation efforts, and mixed contract frameworks enabling private sector collaboration.

- By Region: Northern Mexico represents the largest segment with a market share of 38.6% in 2025, fueled by nearshoring-driven petrochemical demand, cross-border pipeline infrastructure, and natural gas-powered industrial growth.

- Key Players: The Mexico oil and gas market exhibits a consolidated competitive structure, with the state-owned national oil company maintaining dominant upstream and downstream positions while international energy majors contribute capital, technology, and operational expertise through structured partnerships, mixed development contracts, and strategic joint ventures across exploration, production, and refining segments.

To get more information on this market Request Sample

The Mexico oil and gas market is experiencing a period of transformation as the country seeks to balance energy sovereignty with selective private sector participation. Recent policy changes have introduced collaborative development models that allow the national oil company to partner with private operators while maintaining strategic control. These arrangements are helping attract new capital, technology, and expertise to both mature assets and frontier exploration areas. Deepwater activity is gradually advancing as projects move closer to development, supporting longer-term supply potential. At the same time, growing demand for natural gas, particularly for power generation, is reshaping upstream and midstream priorities. Expansion of gas transportation and export-oriented infrastructure is also improving market connectivity. Together, these factors are reinforcing investment confidence, enhancing production capabilities, and positioning Mexico’s oil and gas sector for sustained development over the medium to long term.

Mexico Oil and Gas Market Trends:

Expansion of Deepwater Exploration and Production

Mexico is advancing its deepwater frontier as new exploration and development projects take shape in the Gulf of Mexico. The country’s first ultra-deepwater production initiative, situated in the Perdido Fold Belt at a water depth of 2,500 meters, is targeting first oil by 2028 with peak output projected at over 100,000 barrels per day. The national oil company has strengthened its focus on deepwater exploration by advancing activity in offshore regions, signaling renewed commitment to unlocking untapped hydrocarbon potential. Increased attention on complex offshore resources is expected to stimulate long-term investment, technology deployment, and upstream development. These efforts are likely to play an important role in supporting future production growth and reinforcing the overall expansion of Mexico’s oil and gas market over the coming years.

Growth of LNG Export Infrastructure

Mexico is emerging as a Pacific-facing LNG export hub, leveraging its proximity to both U.S. natural gas supplies and Asian demand markets. The Energía Costa Azul LNG Phase 1 facility in Baja California, with a nameplate capacity of 3.25 million tonnes per annum, surpassed 92% construction completion by mid-2025 and is expected to commence commercial operations in spring 2026. On the Gulf coast, a 1.4 million tonne per annum floating LNG facility at Altamira shipped its first commercial cargo in July 2024, establishing a new offtake channel for domestically sourced and imported natural gas.

Rising Natural Gas Demand for Power Generation

Mexico’s electricity sector is increasingly reliant on natural gas-fired generation, driving sustained growth in gas consumption and pipeline infrastructure. US natural gas pipeline exports to Mexico averaged a record 7.5 billion cubic feet per day in May 2025, reflecting a structural increase in cross-border gas flows. The country is advancing plans to expand combined-cycle power generation capacity, supported by the development of new natural gas pipeline infrastructure. These pipeline projects are intended to strengthen regional gas distribution networks, improve supply reliability, and support rising demand from power generation and industrial users, reinforcing the role of natural gas in the evolving energy mix.

Market Outlook 2026-2034:

The Mexico oil and gas market is positioned for steady growth as the country advances upstream modernization, deepwater resource development, and expansion of natural gas infrastructure. Policy frameworks that encourage collaboration between state entities and private investors are helping attract capital, technology, and operational expertise. At the same time, increasing reliance on gas-fired power generation is strengthening demand for cross-border pipeline capacity and supporting midstream expansion. Together, these dynamics are enhancing production efficiency, improving energy security, and reinforcing the long-term growth outlook for Mexico’s oil and gas sector. The market generated a revenue of USD 350.78 Million in 2025 and is projected to reach a revenue of USD 1,195.17 Million by 2034, growing at a compound annual growth rate of 14.59% from 2026-2034.

Mexico Oil and Gas Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Upstream |

49.5% |

|

Application |

Onshore |

63.2% |

|

Region |

Northern Mexico |

38.6% |

Type Insights:

- Upstream

- Midstream

- Downstream

Upstream dominates with a market share of 49.5% of the total Mexico oil and gas market in 2025.

The upstream segment leads the Mexico oil and gas market as the country intensifies exploration and production activities across onshore basins and deepwater prospects. The national oil company’s Strategic Plan 2025–2035 prioritizes prolific southeast basins and emerging plays in Veracruz, Burgos, and Tampico-Misantla regions. In 2025, the government introduced mixed development contracts allowing private partners to contribute capital and technology, while the state retains a minimum 40% participating interest, attracting fresh investment into mature and frontier fields.

Deepwater exploration is receiving increased focus as offshore initiatives advance in key regions such as the Perdido Fold Belt and the Sureste Basin. Large-scale projects highlight a renewed strategic emphasis on unlocking complex offshore resources. At the same time, development of onshore strategic fields continues to support natural gas supply growth. Together, these upstream efforts are essential for stabilizing production levels, improving resource utilization, and strengthening Mexico’s long-term energy security by ensuring a more balanced and resilient hydrocarbon supply base.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Offshore

- Onshore

Onshore leads with a share of 63.2% of the total Mexico oil and gas market in 2025.

The onshore application segment holds the largest share of the Mexico oil and gas market, underpinned by established production infrastructure across the southeast and northeast basins. The national oil company is concentrating its near-term production recovery efforts on onshore conventional reservoirs, where it has extensive operational experience and established well networks. Nine of the 21 planned mixed contracts target onshore fields, including Tupilco Terciario, Sini-Caparroso, and Pánuco, reflecting the government’s focus on revitalizing mature onshore assets.

Onshore gas-rich fields are becoming increasingly important in meeting Mexico’s domestic energy requirements. Key producing areas in the southeastern basins are strengthening the national gas supply and supporting power generation and industrial demand. At the same time, authorities are assessing the potential of unconventional onshore resources in northern and eastern basins as part of a broader strategy to diversify supply sources. These efforts aim to reduce reliance on imported natural gas, enhance energy security, and create a more balanced upstream portfolio that supports long-term stability in the country’s oil and gas sector.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

Northern Mexico represents the highest revenue with a 38.6% share of the total Mexico oil and gas market in 2025.

Northern Mexico dominates the regional oil and gas market due to its role as a key center for cross-border energy trade and industrial growth driven by nearshoring trends. Expanding manufacturing activity and petrochemical development in this region are significantly increasing demand for natural gas, refined fuels, and industrial feedstocks. Proximity to the United States and well-established pipeline connections support a reliable gas supply to major industrial hubs. These advantages position northern Mexico as a critical demand center, reinforcing its importance in the country’s evolving energy landscape.

The region benefits from expanding natural gas infrastructure and increased pipeline connectivity, supporting a reliable fuel supply for power generation and industrial use. Growing logistics and transportation activity in border states is also driving higher downstream fuel consumption, particularly for diesel. The combination of industrial expansion, infrastructure development, and close access to US energy supplies positions Northern Mexico as a key driver of growth within the country’s oil and gas market.

Market Dynamics:

Growth Drivers:

Why is the Mexico Oil and Gas Market Growing?

Introduction of Mixed Development Contracts and Regulatory Reform

Recent energy policy reforms have positioned mixed development contracts as the main pathway for private sector participation in Mexico’s upstream industry. This model allows the national oil company to maintain a significant ownership interest while partnering firms provide capital, advanced technology, and operational capabilities. Such collaborations are supporting the revitalization of mature onshore assets and encouraging exploration in underdeveloped areas. By sharing risks and resources, these partnerships are improving project viability and accelerating development timelines. The framework is fostering a more balanced and diversified investment environment, strengthening upstream activity and enhancing long-term production prospects across Mexico’s oil and gas sector.

Deepwater Exploration and Ultra-Deepwater Project Development

Mexico’s deepwater resources are emerging as an important driver of oil and gas market expansion as offshore projects progress toward development and production. Increased focus on complex deepwater and shallow-water fields reflects a broader strategy to unlock underexplored resources and strengthen long-term supply potential. These initiatives are drawing advanced offshore technologies, specialized expertise, and international investment into the sector. At the same time, coordinated development of offshore assets is helping diversify the upstream portfolio beyond mature onshore fields. Together, these offshore efforts are enhancing reserve replacement, supporting production stability, and reinforcing Mexico’s position as a competitive destination for offshore exploration and development in the global energy market.

Surging Natural Gas Demand and Infrastructure Expansion

Mexico’s rising electricity demand and ongoing industrial expansion are significantly increasing natural gas consumption and cross-border imports. As power generation needs grow, the country is strengthening its reliance on natural gas to ensure a stable and efficient energy supply. Plans to expand combined-cycle power capacity over the coming years will further elevate gas demand, reinforcing its central role in the energy mix. Infrastructure development is also advancing to support this growth. Projects such as the Southeast Gateway Gas Pipeline and the Centauro del Norte pipeline are enhancing distribution networks and extending access to previously underserved regions, improving reliability and supporting long-term industrial and economic development.

Market Restraints:

What Challenges the Mexico Oil and Gas Market is Facing?

Declining Legacy Field Production and Aging Infrastructure

Mexico’s mature oil fields are facing declining production as natural depletion continues to exceed investment in enhanced recovery and asset maintenance. Aging refinery infrastructure also limits downstream performance, as operational inefficiencies constrain utilization levels. These issues underscore the fact that there should be a long-term investment and modernization of both upstream and downstream sectors of the oil and gas value chain.

Financial Constraints and Supplier Payment Delays

The state-owned oil company is expected to carry one of the largest debt burdens among global oil producers, and by the end of 2025, it will owe substantial amounts to its suppliers. The slow payment has limited the activity of the service companies and the enthusiasm of the private sector towards long-term upstream relationships. These monetary pressures inhibit the rate of new project development, and it is restrictive to attract international capital to be spent on exploration programs.

Regulatory Uncertainty and Institutional Restructuring

The 2025 energy reform consolidated multiple regulatory bodies into a new National Energy Commission, centralizing oversight under the energy ministry. While aimed at streamlining governance, the institutional restructuring has introduced short-term uncertainty regarding permitting timelines, contract enforcement, and approval processes. Some international operators have paused new acreage commitments pending greater regulatory clarity.

Competitive Landscape:

The Mexico oil and gas market exhibits a consolidated competitive structure dominated by the state-owned national oil company, which controls the majority of upstream production assignments and downstream refining capacity. International energy majors participate through structured partnerships, mixed development contracts, and technical service agreements, contributing capital and advanced technologies for deepwater exploration and enhanced recovery operations. The 2025 energy reform has redefined competitive dynamics by establishing mixed contract frameworks that balance state sovereignty with private sector expertise. Competition is intensifying in midstream and downstream segments as nearshoring-driven demand growth attracts investment in pipeline infrastructure, petrochemical facilities, and LNG export terminals across northern and coastal regions.

Recent Developments:

- In September 2025, the government announced the signing of 11 mixed contracts with private sector partners as the initial phase of a plan to close 21 such agreements, aiming to generate approximately USD 8 billion in investment and add up to 450,000 barrels per day of crude oil production by 2033.

- In July 2024, the first commercial LNG cargo was shipped from a 1.4 million tonne per annum floating LNG facility at Altamira on the Gulf coast, marking the inauguration of Mexico’s Gulf-facing LNG export capability.

Mexico Oil and Gas Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Upstream, Midstream, Downstream |

| Applications Covered | Offshore, Onshore |

|

Regions Covered |

Northern Mexico, Central Mexico, Southern Mexico, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Mexico Oil and Gas Market Report

The Mexico oil and gas market size was valued at USD 350.78 Million in 2025.

The Mexico oil and gas market is expected to grow at a compound annual growth rate of 14.59% from 2026-2034 to reach USD 1,195.17 Million by 2034.

Upstream, holding the largest revenue share of 49.5% in 2025, remains the dominant type segment in the Mexico oil and gas market, driven by intensified exploration activities, deepwater field development programs, and government-backed mixed contract frameworks enabling private sector investment.

Key factors driving the Mexico oil and gas market include the introduction of mixed development contracts attracting private investment, deepwater exploration initiatives in the Perdido and Sureste basins, rising natural gas demand for power generation, and expanding LNG export infrastructure.

Major challenges include declining legacy field production and aging infrastructure, financial constraints and supplier payment delays limiting upstream investment, regulatory uncertainty from institutional restructuring, and supply chain bottlenecks affecting service company operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)