Mexico Semiconductor Foundry Market Size, Share, Trends and Forecast by Technology Node, Foundry Type, Application, and Region, 2026-2034

Mexico Semiconductor Foundry Market Overview:

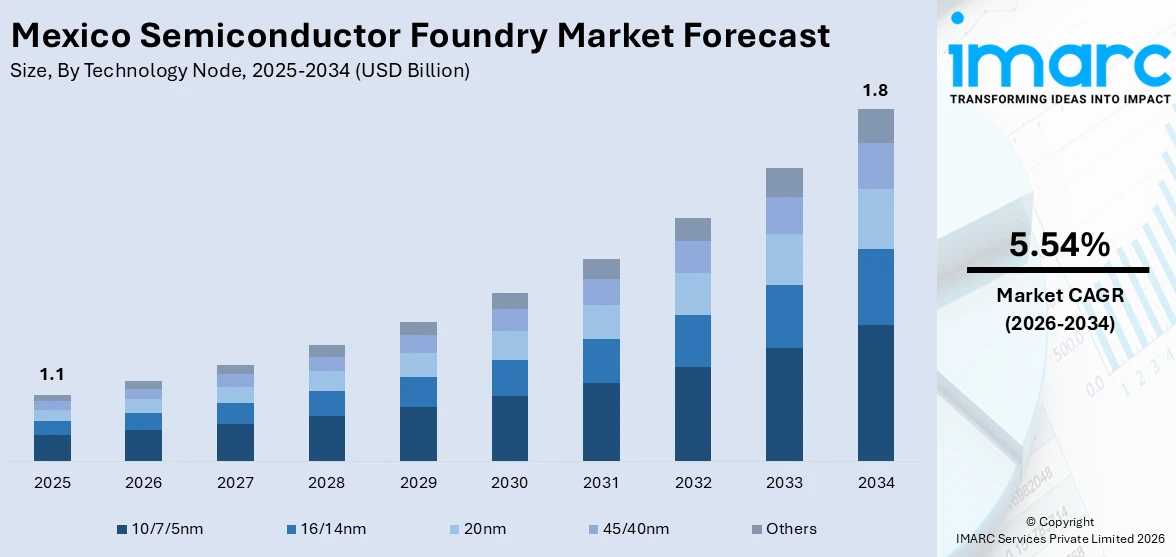

The Mexico semiconductor foundry market size reached USD 1.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 1.8 Billion by 2034, exhibiting a growth rate (CAGR) of 5.54% during 2026-2034. The market is driven by rising demand for automotive chips, fueled by the country’s strong auto manufacturing sector. Nearshoring trends, cost advantages, and USMCA trade benefits also attract investments. Government incentives and supply chain diversification efforts further enhance growth, positioning Mexico as a key semiconductor hub in North America.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.1 Billion |

| Market Forecast in 2034 | USD 1.8 Billion |

| Market Growth Rate 2026-2034 | 5.54% |

Mexico Semiconductor Foundry Market Trends:

Increasing Demand for Automotive Semiconductors in Mexico

The rising demand for automotive semiconductors is majorly driven by the Mexico semiconductor foundry market growth. Mexico became the fourth-largest auto parts producer in the world, and it is poised to become the fifth-largest vehicle manufacturer by the end of 2025. Having produced over 200,000 units and securing 68 new investments in electromobility just this year, the country is quickly moving towards EVs. With U.S. automotive giants and China's EV makers establishing localized supply chains for them, Mexico's fledgling foundry sector is fast becoming integral to the future of the automotive sector. Mexico is all set to play a key role as the future of auto technology in North America transforms, with over 170 Tier 1 and Tier 2 suppliers of EV components. Mexico is a key hub for automotive manufacturing, hosting major global automakers and suppliers. As vehicles become more advanced with electric powertrains, ADAS (Advanced Driver Assistance Systems), and connected car technologies, the need for specialized chips has accelerated. Local foundries are expanding their capabilities to meet this demand, supported by government incentives and foreign investments. Additionally, the USMCA trade agreement strengthens supply chain integration with the U.S., further enhancing semiconductor production for automotive applications. With global chip shortages highlighting the need for regional supply resilience, Mexico is positioning itself as a strategic player in North America’s semiconductor ecosystem. This trend is further creating a positive Mexico semiconductor foundry market outlook.

To get more information on this market Request Sample

Growth in Nearshoring Semiconductor Production

Mexico’s semiconductor foundry market is benefiting from the global shift toward nearshoring, as companies seek to reduce supply chain risks. The country’s proximity to the U.S., cost-competitive labor, and established manufacturing infrastructure make it an attractive location for semiconductor production. Mexico has attracted over USD 7.8 Billion of foreign direct investment (FDI) for electronics manufacturing, which includes USD 206 Million for 2023. It offers tax breaks of up to 76% on equipment for semiconductor manufacturing, positioning itself as an ever-more-important player in the global chip supply chain. Some major cities, including Monterrey, Tijuana, and Reynosa, are becoming sophisticated electronics centers, serving large manufacturers such as LG, Samsung, and Time Interconnect. With 487 electronics firms and a growing demand from the automotive and telecommunications sectors, Mexico's foundry and semiconductor landscape is poised for substantial growth. Many U.S. and Asian firms are exploring partnerships with Mexican foundries to diversify their supply chains away from geopolitical hotspots. Additionally, government initiatives, such as tax incentives and R&D support, are encouraging investment in local semiconductor fabrication. The growing demand for consumer electronics, IoT devices, and industrial automation chips is expanding the Mexico semiconductor foundry market share. As global companies prioritize regionalized production, Mexico is emerging as a key nearshoring destination for semiconductor manufacturing, fostering technological advancement and economic growth in the sector.

Mexico Semiconductor Foundry Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on technology node, foundry type, and application.

Technology Node Insights:

- 10/7/5nm

- 16/14nm

- 20nm

- 45/40nm

- Others

The report has provided a detailed breakup and analysis of the market based on the technology node. This includes 10/7/5nm, 16/14nm, 20nm, 45/40nm, and others.

Foundry Type Insights:

- Pure Play Foundry

- IDMs

A detailed breakup and analysis of the market based on the foundry type have also been provided in the report. This includes pure play foundry and IDMs.

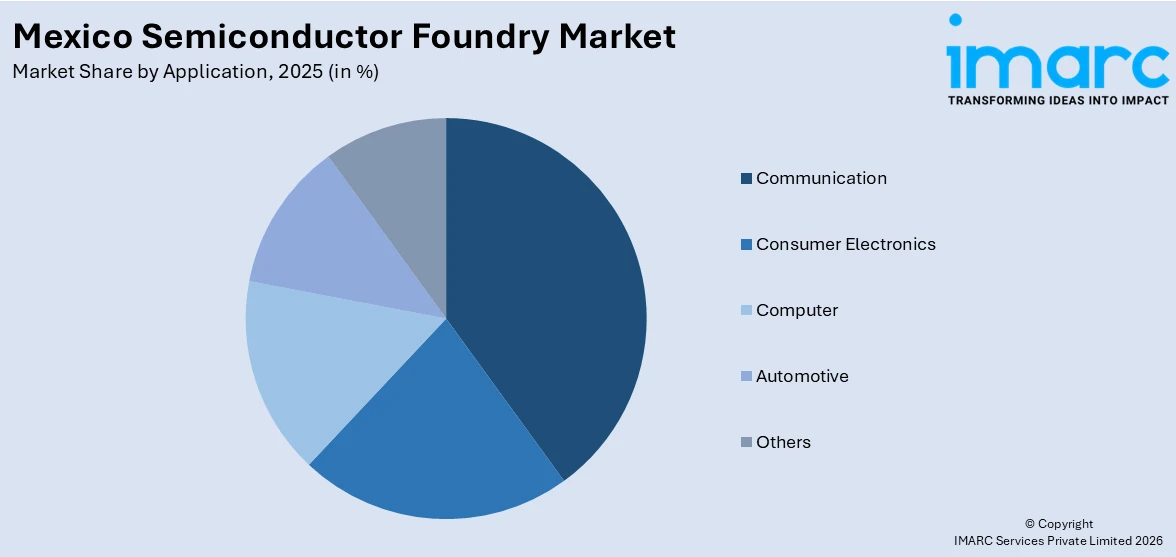

Application Insights:

Access the comprehensive market breakdown Request Sample

- Communication

- Consumer Electronics

- Computer

- Automotive

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes communication, consumer electronics, computer, automotive, and others.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include Northern Mexico, Central Mexico, Southern Mexico, and Others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Mexico Semiconductor Foundry Market News:

- October 09, 2024: Foxconn announced building an Nvidia super chip GB200 assembly factory in Guadalajara, Mexico, in response to the increasing global demand for AI servers. With more than USD 500 Million already invested in Mexico, this facility will cater to the next-generation Blackwell platforms, incorporating cutting-edge liquid cooling and thermal technologies. This move further solidifies Mexico's position as an emerging hub for high-performance semiconductor assembly and AI-driven foundry activities.

Mexico Semiconductor Foundry Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technology Nodes Covered | 10/7/5nm, 16/14nm, 20nm, 45/40nm, Others |

| Foundry Types Covered | Pure Play Foundry, IDMs |

| Applications Covered | Communication, Consumer Electronics, Computer, Automotive, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Mexico semiconductor foundry market performed so far and how will it perform in the coming years?

- What is the breakup of the Mexico semiconductor foundry market on the basis of technology node?

- What is the breakup of the Mexico semiconductor foundry market on the basis of foundry type?

- What is the breakup of the Mexico semiconductor foundry market on the basis of application?

- What is the breakup of the Mexico semiconductor foundry market on the basis of region?

- What are the various stages in the value chain of the Mexico semiconductor foundry market?

- What are the key driving factors and challenges in the Mexico semiconductor foundry market?

- What is the structure of the Mexico semiconductor foundry market and who are the key players?

- What is the degree of competition in the Mexico semiconductor foundry market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico semiconductor foundry market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico semiconductor foundry market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico semiconductor foundry industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade