Mexico Semiconductor Manufacturing Equipment Market Size, Share, Trends and Forecast by Equipment Type, Fab Facility, Product Type, Dimension, Supply Chain Participant, and Region, 2026-2034

Mexico Semiconductor Manufacturing Equipment Market Overview:

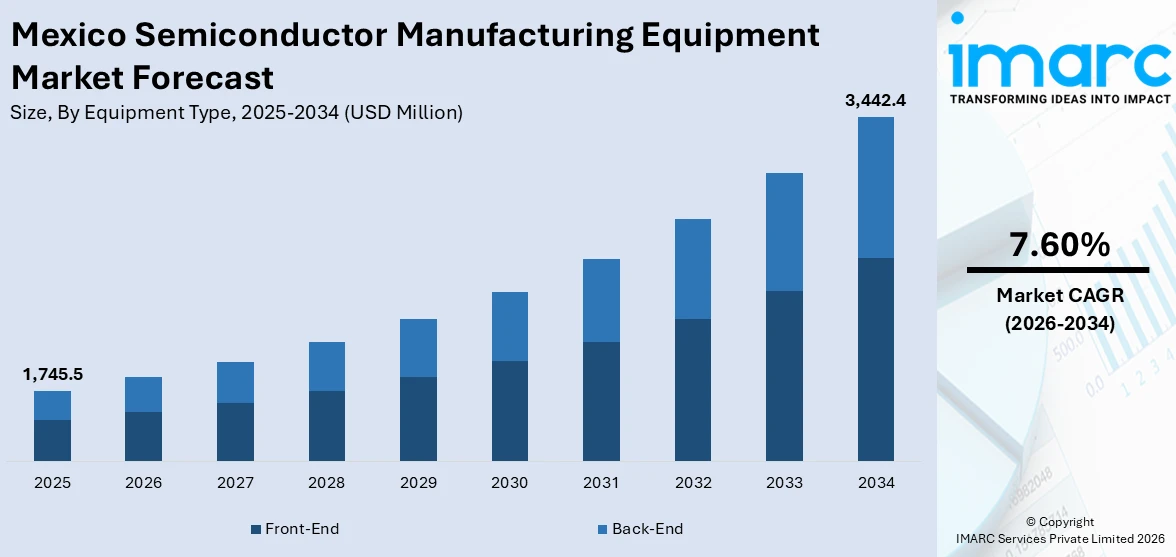

The Mexico semiconductor manufacturing equipment market size reached USD 1,745.5 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 3,442.4 Million by 2034, exhibiting a growth rate (CAGR) of 7.60% during 2026-2034. Rising demand for advanced electronics, technological innovation across industries, strategic collaborations between academia and private sector, growing investment in automation, government incentives supporting the technology sector, focus on sustainable production technologies, heightened demand for semiconductors in emerging industries, expansion of R&D centers, diversification of semiconductor categories are some of the factors positively impacting the Mexico semiconductor manufacturing equipment market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,745.5 Million |

| Market Forecast in 2034 | USD 3,442.4 Million |

| Market Growth Rate 2026-2034 | 7.60% |

Mexico Semiconductor Manufacturing Equipment Market Trends:

Expansion of Advanced Electronics Manufacturing and Technological Adaptation

The expansion of Mexico’s advanced electronics manufacturing sector stands as a major driver behind the semiconductor manufacturing equipment market. Mexico is rapidly enhancing its capabilities to produce high-performance components required across automotive, telecommunications, consumer electronics, and industrial automation sectors. On November 7, 2024, ISE Labs, a subsidiary of ASE Technology Holding, announced the acquisition of land in Axis 2 Industrial Park, Tonalá (Guadalajara Metropolitan Area) to establish a new semiconductor packaging and testing facility. The facility, expected to create over 500 jobs in its first year, will focus on outsourced semiconductor assembly and test (OSAT) services, supporting ASE's strategy to strengthen its North American presence. With Jalisco accounting for 70% of Mexico’s semiconductor market, this investment positions the state as the first in Mexico and Latin America to offer full OSAT services to major semiconductor companies across North America. Additionally, the increasing adoption of 5G networks, electric vehicles, and smart devices is reshaping demand patterns for semiconductor components, encouraging broader investment in precision manufacturing technologies. The Mexico semiconductor manufacturing equipment market forecast indicates that companies are integrating high-precision equipment, including lithography, ion implantation, and wafer inspection systems, to meet stringent design requirements. Mexico's workforce development initiatives are also supporting advanced technical training aligned with semiconductor production needs. Research and innovation clusters are forming near key industrial hubs, enabling faster technology transfer and improving competitiveness. The push for technological adaptation is also driving the adoption of sustainable manufacturing practices, smart factory concepts, and end-to-end automation solutions. Mexican semiconductor facilities are increasingly incorporating energy-efficient production systems, emission reduction initiatives, and water recycling technologies. Equipment vendors are responding by offering modular, flexible solutions that support sustainable production while maintaining operational excellence.

To get more information on this market Request Sample

Government Incentives and Strategic Policy Frameworks

Government incentives and strategic frameworks form a second major force behind the growth of Mexico’s semiconductor manufacturing equipment sector. Financial incentives, tax benefits, and regulatory reforms have created a highly favorable investment environment, aligning public infrastructure projects and education initiatives with the needs of semiconductor manufacturers. Policy initiatives and regulatory clarity have created measurable momentum in Mexico semiconductor manufacturing equipment market trends. The Mexico semiconductor manufacturing equipment market growth is driven in part by federal and state-level commitments to streamline business processes, enhance industrial parks, and build technology-oriented educational institutions. The focus on securing domestic semiconductor capabilities is also resulting in the formation of specialized industrial clusters, attracting both equipment manufacturers and semiconductor producers to Mexico’s innovation corridors. International cooperation agreements related to semiconductor production have been initiated, supporting technology transfer and research collaboration. Analysts tracking Mexico semiconductor manufacturing equipment market trends point to a growing emphasis on strategic autonomy and resilience in high-tech sectors. The Mexico semiconductor manufacturing equipment market outlook reflects continued optimism based on Mexico’s ability to meet global standards for quality, innovation, and supply reliability, establishing its position as a future leader in semiconductor manufacturing across the Americas. Trade agreements, particularly the United States-Mexico-Canada Agreement (USMCA), have strengthened Mexico’s position within North American supply chains, providing access to a large consumer market while ensuring tariff advantages. On February 8, 2025, Mexico launched the National Center for Semiconductor Design “Kutsari”, aiming to strengthen its domestic semiconductor capabilities and reduce reliance on foreign technology. The center, headquartered across Puebla, Jalisco, and Sonora, will focus on semiconductor design for automotive, medical, and household industries, with plans to expand into manufacturing and assembly by 2030. To support innovation, the government will reform patent laws, reduce approval times to three years, and initiate an Accelerated Training Program to develop skilled semiconductor designers. Infrastructure projects such as smart cities and regional tech hubs are further reinforcing demand for semiconductor technologies and related manufacturing solutions.

Mexico Semiconductor Manufacturing Equipment Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on equipment type, fab facility, product type, dimension, and supply chain participant.

Equipment Type Insights:

- Front-End

- Lithography

- Deposition

- Cleaning

- Wafer Surface Conditioning

- Others

- Back-End

- Testing

- Assembly and Packaging

- Dicing

- Bonding

- Metrology

- Others

The report has provided a detailed breakup and analysis of the market based on the equipment type. This includes front-end (lithography, deposition, cleaning, wafer surface conditioning, and others) and back-end (testing, assembly and packaging, dicing, bonding, metrology, and others).

Fab Facility Insights:

Access the comprehensive market breakdown Request Sample

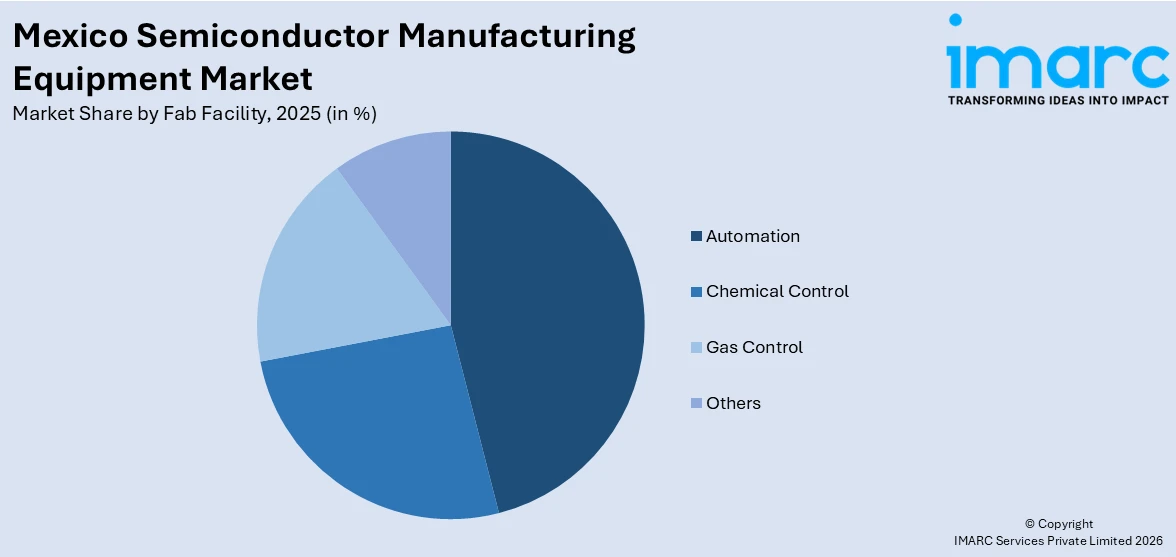

- Automation

- Chemical Control

- Gas Control

- Others

The report has provided a detailed breakup and analysis of the market based on the fab facility. This includes automation, chemical control, gas control, and others.

Product Type Insights:

- Memory

- Logic Components

- Microprocessor

- Analog Components

- Optoelectronic Components

- Discrete Components

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes memory, logic components, microprocessor, analog components, optoelectronic components, discrete components, and others.

Dimension Insights:

- 2D

- 2.5D

- 3D

The report has provided a detailed breakup and analysis of the market based on dimension. This includes 2D, 2.5D, and 3D.

Supply Chain Participant Insights:

- IDM Firms

- OSAT Companies

- Foundries

The report has provided a detailed breakup and analysis of the market based on supply chain participants. This includes IDM firms, OSAT companies, and foundries.

Regional Insights:

- Northern Mexico

- Central Mexico

- Southern Mexico

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include Northern Mexico, Central Mexico, Southern Mexico, and others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Mexico Semiconductor Manufacturing Equipment Market News:

- January 24, 2024: Intel officially opened Fab 9 in Rio Rancho, New Mexico, as part of a USD 3.5 Billion investment to manufacture advanced semiconductor packaging technologies, including Foveros 3D packaging. Fab 9 marks Intel’s first high-volume factory for 3D advanced packaging in the United States, supporting mass production with integrated supply chain efficiency alongside Fab 11X. The expansion has generated hundreds of new Intel jobs, over 3,000 construction jobs, and 3,500 additional jobs statewide, reinforcing Intel’s commitment to sustainable operations through 100% renewable electricity use and significant water restoration efforts.

Mexico Semiconductor Manufacturing Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered |

|

| Fab Facilities Covered | Automation, Chemical Control, Gas Control, Others |

| Product Types Covered | Memory, Logic Components, Microprocessor, Analog Components, Optoelectronic Components, Discrete Components, Others |

| Dimensions Covered | 2D, 2.5D, 3D |

| Supply Chain Participants Covered | IDM Firms, OSAT Companies, Foundries |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Mexico semiconductor manufacturing equipment market performed so far and how will it perform in the coming years?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of equipment type?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of fab facility?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of product type?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of dimension?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of supply chain participant?

- What is the breakup of the Mexico semiconductor manufacturing equipment market on the basis of region?

- What are the various stages in the value chain of the Mexico semiconductor manufacturing equipment market?

- What are the key driving factors and challenges in the Mexico semiconductor manufacturing equipment market?

- What is the structure of the Mexico semiconductor manufacturing equipment market and who are the key players?

- What is the degree of competition in the Mexico semiconductor manufacturing equipment market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico semiconductor manufacturing equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico semiconductor manufacturing equipment market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico semiconductor manufacturing equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)