Mexico Spices and Seasonings Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Mexico Spices and Seasonings Market Size, Share, Trends & Forecast (2026-2034)

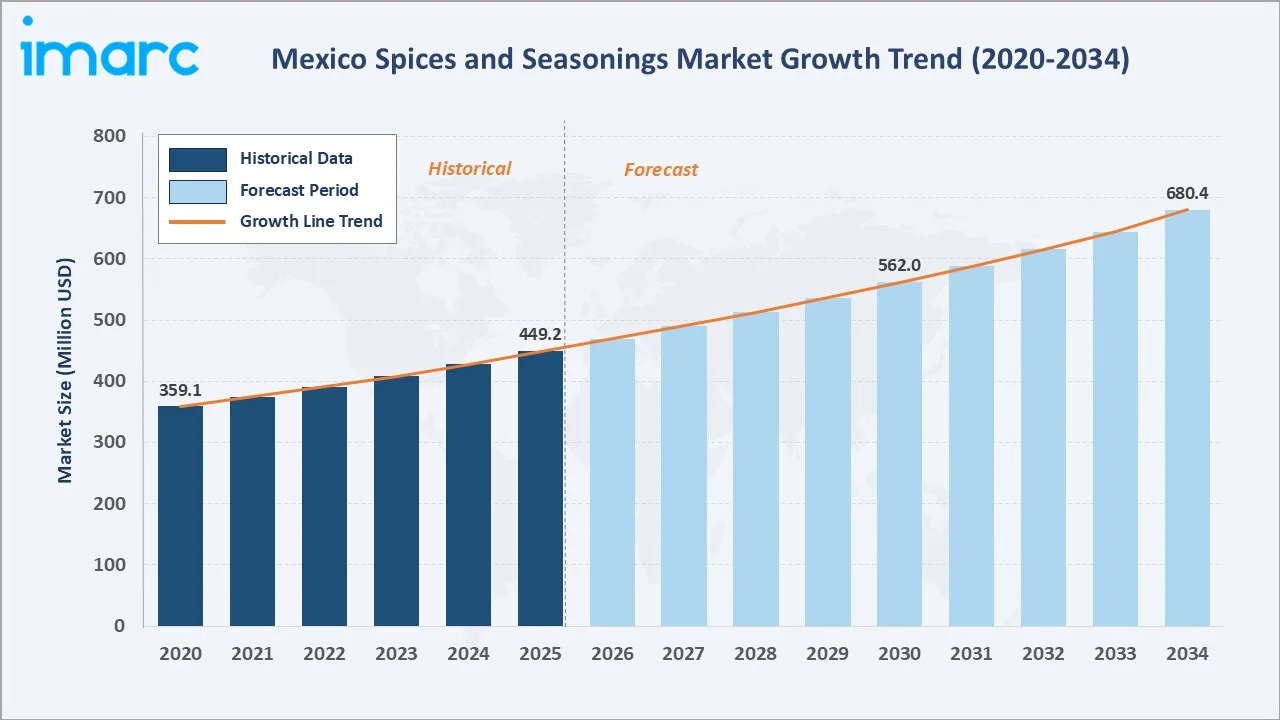

The Mexico spices and seasonings market was valued at USD 449.2 Million in 2025 and is projected to reach USD 680.4 Million by 2034, exhibiting a CAGR of 4.58% during 2026-2034. The market is fueled by Mexico's deep-rooted culinary heritage, rapid expansion of the food processing sector, and the growing global appetite for authentic Mexican flavors, reflecting Mexico's standing as one of Latin America's top spice-producing and exporting nations.

Spices lead the product segment at 48.9%, meat and poultry products dominate the application segment at 29.4%, and Central Mexico commands 42.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 449.2 Million |

|

Forecast Market Size (2034) |

USD 680.4 Million |

|

CAGR (2026-2034) |

4.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Central Mexico (42.8%, 2025) |

|

Second Largest Region |

Northern Mexico (31.5%, 2025) |

|

Leading Product |

Spices (48.9%, 2025) |

|

Leading Application |

Meat and Poultry Products (29.4%, 2025) |

The Mexico spices and seasonings market expanded from USD 359.1 Million in 2020 to USD 449.2 Million in 2025, driven by rising domestic food processing demand, expanding organized retail, and growing consumer interest in authentic flavors and branded seasoning products. Anchored at USD 562.0 Million in 2030, the forecast to USD 680.4 Million by 2034 is supported by increasing export-led demand for Mexican spice blends, the premiumization of regional culinary offerings, and growing penetration of private-label and artisan spice brands.

To get more information on this market, Request Sample

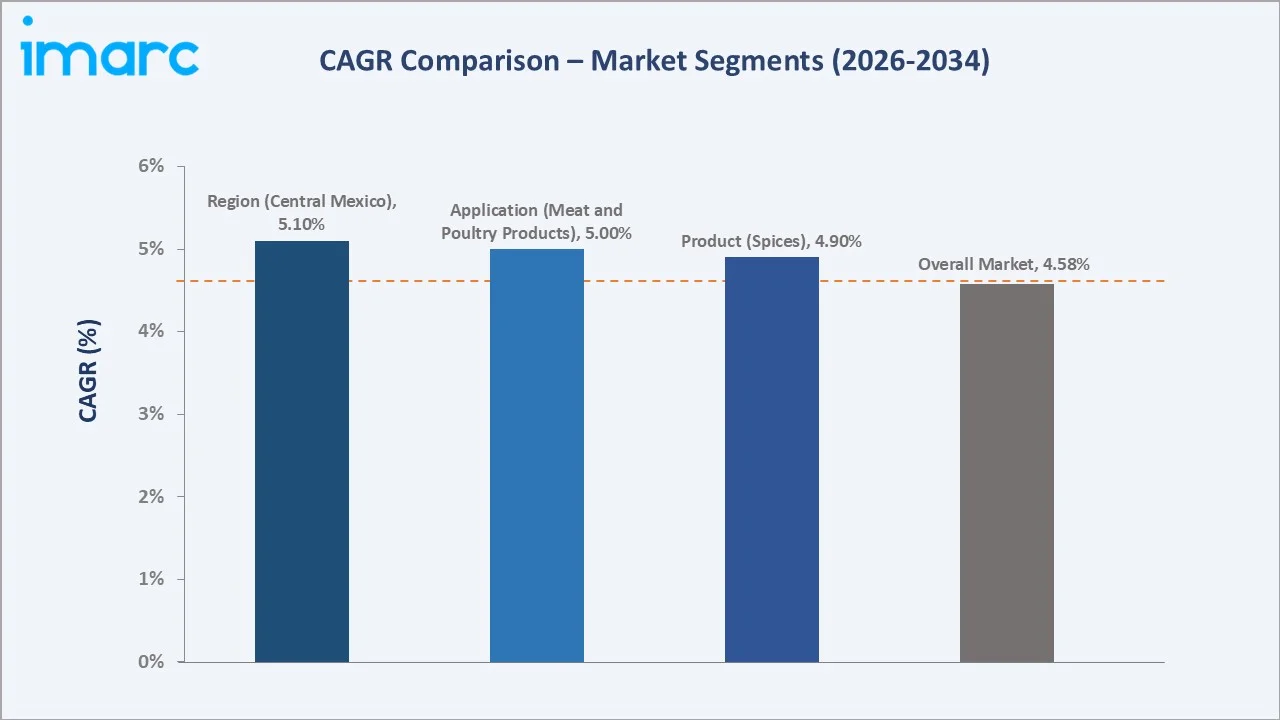

CAGR trajectories across product and application sub-segments show spices and meat and poultry products expanding at rates broadly consistent with the overall 4.58% market CAGR, supported by stable demand from food processing and packaged food manufacturers.

Executive Summary

The Mexico spices and seasonings market is on a sustained growth trajectory from USD 359.1 Million in 2020 to USD 680.4 Million by 2034. The segment has evolved from largely informal, bulk trade to an organized, brand-driven industry, with domestic manufacturers and international players competing across retail, foodservice, and industrial channels. Rich culinary traditions, Mexico's biodiversity in pepper and herb cultivation, and rising disposable incomes are underpinning demand across all categories.

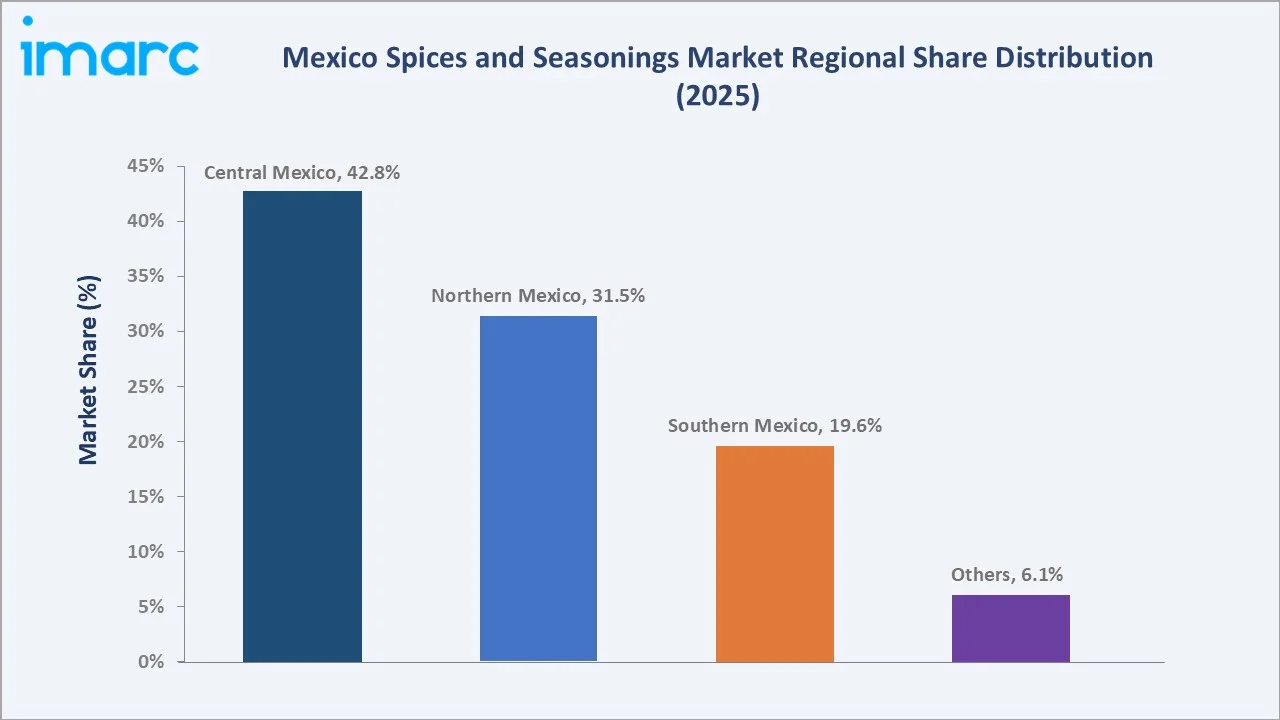

Spices dominate the product segment at 48.9% in 2025, reflecting the country's centuries-old tradition of chili and native spice cultivation. Meat and poultry products account for the leading application share at 29.4%, supported by robust domestic protein consumption and growing demand from food processing companies. Central Mexico commands 42.8% of the regional share, led by Mexico City's dense consumer base and concentration of food manufacturers and modern retail chains.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Spices – 48.9% share (2025) |

|

Second Largest Product |

Herbs – 27.6% share (2025) |

|

Leading Application |

Meat and Poultry Products – 29.4% share (2025) |

|

Second Largest Application |

Soups, Sauces and Dressings – 21.7% share (2025) |

|

Leading Region |

Central Mexico – 42.8% share (2025) |

|

Second Largest Region |

Northern Mexico – 31.5% share (2025) |

|

Top Companies |

McCormick & Company, Inc., Grupo Herdez, S.A.B. de C.V., Conservas La Costeña, S.A. de C.V., Unilever, Salsa Tamazula S.A. de C.V. |

Key Analytical Observations Supporting the Above Data:

- Spices dominance at 48.9% is anchored by Mexico's rich chili pepper diversity, deep-rooted culinary traditions, and well-established domestic supply chains for key varieties, such as ancho, guajillo, and chipotle.

- Herbs at 27.6% reflect strong household and foodservice demand for fresh and dried herbs, such as cilantro, epazote, and Mexican oregano, with growing crossover into international cuisine applications.

- Meat and poultry products at 29.4% are the largest application, driven by Mexico's substantial poultry and pork processing sector, which relies heavily on seasoning blends for marination, preparation, and value-added processing.

- Soups, sauces and dressings share at 21.7% is supported by strong demand for seasoning blends, spice mixes, and herb formulations used in condiments, ready-to-cook products, and convenience foods.

- Central Mexico at 42.8% leads the regional landscape, anchored by the Mexico City metropolitan area, Guadalajara, and Puebla, supported by a high concentration of food manufacturers, retailers, and foodservice chains.

Mexico Spices and Seasonings Market Overview

Spices and seasonings encompass a wide range of products used to flavor, color, and preserve food. In Mexico, this market spans raw agricultural commodities, such as chili peppers, cumin, coriander, and oregano, as well as processed and value-added products, including blended seasonings, marinades, dry rubs, and specialty condiments.

The Mexican market ecosystem integrates smallholder and commercial agricultural producers, processing and blending facilities, packaging and labeling companies, distributors and logistics providers, organized retail and e-commerce platforms, foodservice operators, and industrial food processors. Together they form a vertically linked supply chain spanning cultivation, processing, distribution, and end-use consumption across household, commercial, and industrial segments.

Market Dynamics

To evaluate market opportunities, Request Sample

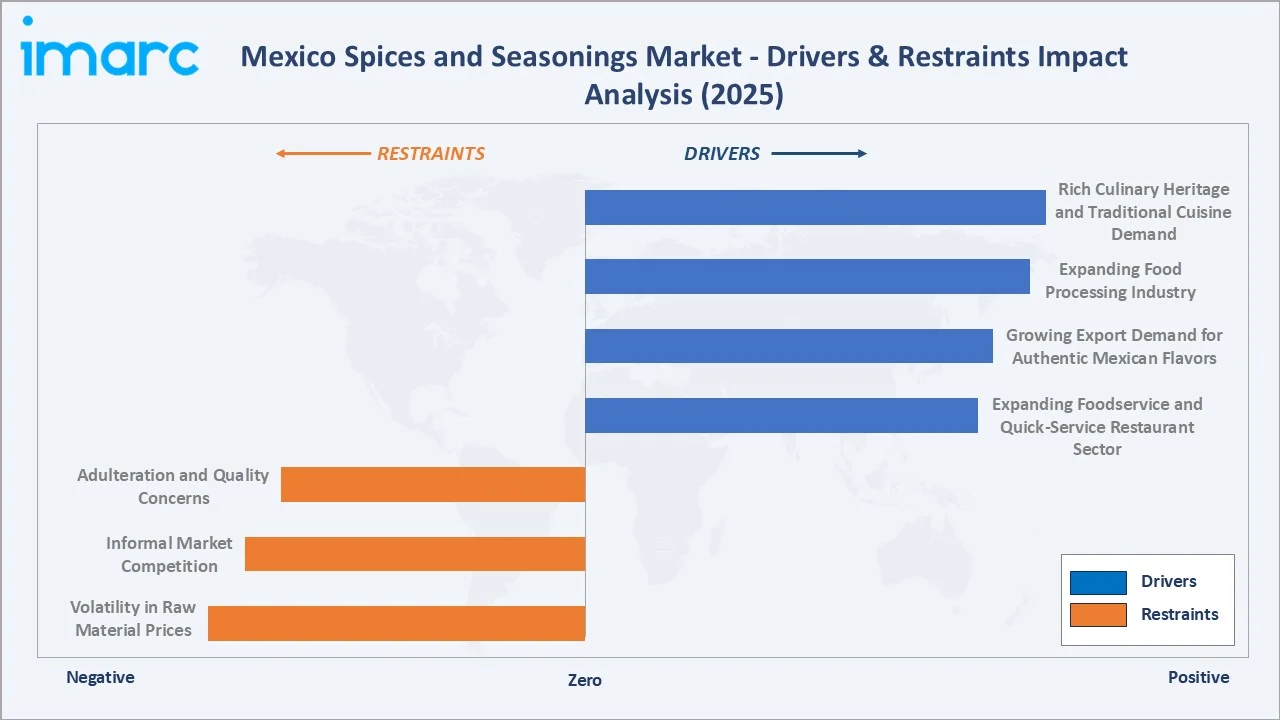

Market Drivers

- Rich Culinary Heritage and Traditional Cuisine Demand: Mexico's globally renowned culinary traditions, centered on complex mole sauces, regional chili preparations, and signature seasoning blends, generate consistent domestic demand for a wide range of spices, herbs, and seasoning products across households and foodservice operators.

- Expanding Food Processing Industry: The rapid growth of Mexico's food and beverage processing sector is substantially increasing demand for industrial-grade seasoning inputs. Meat processing, snack manufacturing, and ready-to-eat food production are among the highest-volume consumers of spice and seasoning products.

- Growing Export Demand for Authentic Mexican Flavors: Rising global consumer interest in Latin American and Mexican cuisine is driving export demand for authentic Mexican spice varieties and seasoning blends, particularly in the United States, European, and Asian markets.

- Expanding Foodservice and Quick-Service Restaurant Sector: As per IMARC Group, the Mexico food service market size reached USD 38.4 Billion in 2025. Mexico's growing urban middle class and expanding restaurant, hotel, and institutional catering sectors are creating sustained demand for high-quality, consistent seasoning products tailored to professional food preparation.

Market Restraints

- Volatility in Raw Material Prices: Seasonal fluctuations, climatic variability, and supply chain disruptions affecting key spice and herb production areas contribute to input price volatility, compressing manufacturer margins and creating pricing uncertainty across the supply chain. Global logistics disruptions have periodically driven up transportation costs for imported spice inputs, adding further pressure on domestic processors.

- Adulteration and Quality Concerns: The prevalence of adulterated and low-quality spice products in informal market channels undermines consumer trust, creates competitive disadvantages for branded producers, and poses food safety challenges requiring regulatory intervention.

- Informal Market Competition: A significant share of spice and seasoning sales in Mexico occurs through informal channels, including traditional markets, street vendors, and unregistered producers, limiting the addressable market for organized and branded players.

Market Opportunities

- Premiumization and Organic Spice Products: Growing consumer awareness around clean-label, organic, and sustainably sourced ingredients is creating opportunities for premium spice and seasoning products targeting health-conscious and food-aware consumers.

- E-Commerce and Digital Retail Expansion: The rapid growth of online grocery and specialty food platforms in Mexico is opening new distribution channels for artisan, regional, and premium spice brands that would otherwise lack access to traditional brick-and-mortar retail networks.

Market Challenges

- Climate Change and Agricultural Risk: Increasing frequency of extreme weather events, shifting rainfall patterns, and rising temperatures are posing risks to domestic spice and herb cultivation, particularly in key agricultural regions.

- Regulatory Compliance and Labeling Standards: Evolving food labeling regulations require manufacturers to reformulate products, update packaging, and invest in compliance infrastructure, adding costs particularly for smaller producers.

Emerging Market Trends

1. Clean Label, Organic, and Functional Spice Demand

Consumer demand for transparent ingredient sourcing, organic certification, and health-functional seasonings is accelerating product innovation among leading spice manufacturers. Brands are expanding organic and non-GMO certified product lines, introducing functional blends with antioxidant or anti-inflammatory positioning, and reformulating existing products to reduce sodium content.

2. Premiumization of Regional and Artisan Spice Blends

There is growing market appetite for regionally distinctive and artisan-crafted spice and seasoning products that offer authentic flavor profiles beyond mass-market standards. Producers from Oaxaca, Veracruz, and the Yucatán Peninsula are increasingly marketing geographically specific spice varieties and traditional mole and achiote preparations to premium domestic and international consumers, creating differentiated value propositions within an otherwise commoditized segment.

3. Expansion of Spice-Forward Ready-to-Use and Convenience Formats

Growing consumer preference for convenience in food preparation is driving demand for pre-blended, portion-controlled, and ready-to-use spice and seasoning formats including marinades, spice kits, recipe blends, and liquid seasonings. These formats reduce preparation time while delivering consistent flavors, appealing to younger urban consumers and time-constrained households across Mexico's growing metropolitan areas.

4. Digital and E-Commerce Distribution Channels

The rapid expansion of e-commerce platforms and digital grocery delivery services is enabling specialty, artisan, and regional spice brands to reach national and international consumers beyond traditional geographic limits. Online channels are driving discoverability for niche spice producers and enabling consumer education around authentic culinary applications, supporting both category expansion and market premiumization.

Industry Value Chain Analysis

The Mexico spices and seasonings value chain spans six stages from raw material sourcing through end-use consumption. Processing and blending, distribution infrastructure, and retail or foodservice channel management capture the highest value-add, while agricultural raw material quality and sourcing conditions form the foundational competitive differentiator across the supply chain.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Agricultural farms, spice growers, herb cultivators, and salt producers supplying raw inputs across key growing regions |

|

Processing & Blending |

Food manufacturers, spice processors, blending facilities, and contract manufacturers transforming raw inputs into finished products |

|

Quality Control & Packaging |

Quality assurance labs, certification bodies, packaging suppliers, and regulatory compliance teams ensuring product safety and standards |

|

Distribution & Logistics |

Wholesale distributors, cold chain operators, third-party logistics providers, and supply chain management companies |

|

Retail & Foodservice |

Supermarkets, hypermarkets, specialty food stores, online platforms, restaurants, hotels, and institutional food buyers |

|

End Use & Consumption |

Households, food processing companies, foodservice operators, and industrial end users consuming finished spice and seasoning products |

Vertically integrated players with ownership of proprietary blending capabilities, established distribution networks, and strong retail partnerships are positioned to capture greater value across the chain than those reliant on third-party processing or distribution infrastructure.

Technology Landscape in the Mexico Spices and Seasonings Industry

Processing Automation and Quality Control Technologies

Advanced processing technologies including optical sorting, machine vision quality inspection, and automated grinding and blending systems are being adopted by leading manufacturers to improve product consistency, reduce contamination risk, and optimize production efficiency. These technologies are enabling scale-up of premium product lines and supporting compliance with export-grade quality standards.

Traceability and Supply Chain Digitization

Digital traceability systems using blockchain and IoT sensor technology are increasingly being deployed to track spice products from farm to shelf, supporting food safety compliance, clean-label verification, and export certification requirements. These tools are particularly relevant for certified organic and geographic indication products seeking premium market positioning.

Flavor Science and Product Innovation

Advances in flavor chemistry, encapsulation technology, and sensory science are enabling manufacturers to develop heat-stable, slow-release, and targeted-delivery spice formulations suitable for processed food applications. Innovation in this area is supporting product differentiation in the industrial and foodservice segments, where performance characteristics are as important as flavor authenticity.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Spices |

48.9% |

2025 |

|

Application |

Meat and Poultry Products |

29.4% |

2025 |

|

Region |

Central Mexico |

42.8% |

2025 |

By Product

Spices command a 48.9% majority share in 2025, anchored by Mexico's deep tradition of chili pepper cultivation and the central role of dried spices in domestic cuisine. The segment benefits from strong agricultural supply chains, established export markets, and growing demand from food processors requiring consistent and high-volume spice inputs.

To access detailed market analysis, Request Sample

Herbs at 27.6% in 2025 capture a significant secondary share, driven by widespread use of fresh and dried herbs including cilantro, epazote, and oregano across household cooking and professional food preparation.

By Application

Meat and poultry products dominate with 29.4% share in 2025, reflecting the central importance of spice and seasoning inputs in Mexico's substantial poultry, pork, and beef processing industries, where marination, preparation, and value-added processing rely heavily on consistent seasoning formulations.

Soups, sauces and dressings at 21.7% represent the second-largest application, driven by strong consumer demand for ready-to-use sauces, salsas, and cooking sauces that incorporate complex spice blends.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central Mexico |

42.8% |

Large urban consumer base, high food processing activity, dense retail network, and strong demand for branded and packaged spice products |

|

Northern Mexico |

31.5% |

Growing industrial food sector, strong proximity to United States export routes, expanding foodservice and quick-service restaurant chains |

|

Southern Mexico |

19.6% |

Rich indigenous spice traditions, growing agribusiness investment, rising domestic consumption, and expanding regional cuisine influence |

|

Others |

6.1% |

Emerging rural markets, increasing modern trade penetration, and gradual shift from informal to organized spice distribution channels |

Central Mexico at 42.8% in 2025 leads the regional landscape, anchored by the Mexico City metropolitan area, Guadalajara, and Puebla. The concentration of food manufacturers, organized retail chains, and high-density urban consumer markets supports sustained leadership across both branded and private-label spice and seasoning categories.

Northern Mexico at 31.5% is a key growth region, driven by its proximity to the United States market, expanding industrial food processing capacity in states such as Sonora, Chihuahua, and Nuevo León, and a well-developed logistics infrastructure supporting both domestic distribution and cross-border trade in spice and seasoning products.

Competitive Landscape

The Mexico spices and seasonings market is moderately consolidated, with established multinational brands and strong domestic players competing across retail, foodservice, and industrial channels. Brand equity, product range depth, agricultural sourcing capabilities, and distribution network reach form the key competitive moats in this category.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

McCormick & Company, Inc. |

McCormick Herbs & Spices |

Leader |

Global portfolio diversification, product innovation, and market leadership in spices, mayonnaise, and condiments |

|

Grupo Herdez, S.A.B. de C.V. |

Herdez, Doña María, Búfalo |

Leader |

Deep Mexican market presence, broad brand portfolio, and wide retail and export distribution across domestic and international channels |

|

Conservas La Costeña, S.A. de C.V. |

La Costeña Salsas and Sauces |

Leader |

Market-leading position in sauces, dips and condiments, broad domestic distribution, and strong category depth in peppers and salsas across several countries |

| Unilever |

Knorr |

Leader |

Broad consumer reach, strong advertising investment, and extensive presence in household and foodservice channels across Mexico |

|

Salsa Tamazula S.A. de C.V. |

Salsa Valentina, Tamazula Mexican Hot Sauce |

Emerging |

Recognized regional hot sauce brand with growing national distribution, expanding product range, and presence in both domestic and United States export channels |

Key players include McCormick & Company, Inc., Grupo Herdez, S.A.B. de C.V., Conservas La Costeña, S.A. de C.V., Unilever, and Salsa Tamazula S.A. de C.V., among others.

Key Company Profiles

McCormick & Company, Inc.

McCormick & Company, Inc. is a global leader in flavor, headquartered in Hunt Valley, Maryland, United States, founded in 1889. The company manufactures, markets, and distributes spices, herbs, seasoning mixes, condiments, and other flavorful products to the entire food industry, including consumers, foodservice operators, and food manufacturers.

- Product Portfolio: McCormick Herbs & Spices product line encompassing a broad range of dried herbs, ground and whole spices, seasoning blends, and flavor enhancers for household and professional food preparation applications.

- Recent Developments: In August 2025, McCormick & Company, Inc. announced a definitive agreement to acquire a controlling 75% stake in McCormick de Mexico from Grupo Herdez for USD 750 Million.

- Strategic Focus: Expanding market presence across spices, condiments, and adjacent food categories through integrated operations in Mexico, sustained investment in brand building, and leveraging global flavor expertise to drive innovation and category growth.

Grupo Herdez, S.A.B. de C.V.

Grupo Herdez, S.A.B. de C.V. is a leading Mexican food company founded in 1914 and headquartered in Mexico City. The company operates across the food and frozen segments, offering a diversified portfolio of sauces, condiments, and canned foods.

- Product Portfolio: Herdez-branded salsas, cooking sauces, and homestyle condiments; Doña María Mole Adobo Paste; and Búfalo hot sauces and condiments, alongside a broad range of canned and packaged food products.

- Recent Developments: The firm has been expanding its brand presence across domestic and international markets, investing in product innovation across its core sauce and condiment categories, and strengthening its distribution network to capture growing demand for authentic Mexican food products in both retail and foodservice channels.

- Strategic Focus: Deepening domestic retail and foodservice distribution across core condiment and sauce categories, expanding the international reach of its heritage brands, and investing in product portfolio innovation to address evolving consumer preferences in both the domestic and export markets.

Conservas La Costeña, S.A. de C.V.

Conservas La Costeña, S.A. de C.V. is a leading Mexican food company founded in 1923 and headquartered in Ecatepec de Morelos, State of Mexico. The company specializes in the manufacture and distribution of canned and preserved food products, including chili peppers, salsas, sauces, beans, canned vegetables, and condiments.

- Product Portfolio: La Costeña Salsas and Sauces; a broad range of Mexican condiments and preserved food products.

- Recent Developments: The firm has been expanding its retail distribution reach in domestic and international markets, investing in packaging modernization, and growing its product range to meet rising global demand for authentic Mexican condiment products across retail, foodservice, and institutional channels.

- Strategic Focus: Maintaining domestic market leadership across the sauces, dips, and condiments category, expanding international distribution through established partnerships in North America, Europe, and Latin America, and investing in product and packaging innovation to serve growing demand for Mexican food products globally.

Market Concentration Analysis

The Mexico spices and seasonings market is moderately fragmented, with established branded manufacturers competing alongside numerous regional, local, and artisan producers. While organized retail is dominated by well-recognized brands, the strong presence of traditional markets, independent producers, and informal distribution channels contributes to a diverse and competitive market landscape.

Barriers to entry in the branded segment include established consumer brand loyalty, the need for scalable processing and blending infrastructure, multi-state distribution capabilities, and regulatory compliance under Mexico's evolving food safety and labeling standards. These factors favor well-capitalized incumbents with established supply chains and strong retail partnerships.

Consolidation among mid-tier producers is likely to continue as compliance costs rise, organized retail demands for consistent supply quality and packaging standards increase, and larger players pursue strategic acquisitions to broaden geographic and category reach within the domestic market.

Investment & Growth Opportunities

Fastest-Growing Segments

Snacks and convenience food expand at an above-average rate, driven by the rapid growth of Mexico's snack and ready-to-eat food industry and increasing consumer demand for bold, regionally inspired flavor profiles. Manufacturers are broadening seasoning portfolios with innovative flavor blends and convenient formats to meet evolving consumer preferences across packaged food categories.

Emerging Markets

Northern Mexico is emerging as a high-growth region, anchored by rapid industrial food processing expansion, growing cross-border trade activity with the United States, and an expanding urban consumer base seeking branded and premium seasoning products. The region represents significant opportunity for manufacturers able to align product offerings with both domestic consumption trends and export market requirements.

Venture & Investment Trends

Investment is flowing into organic and clean-label spice processing facilities, premium packaging and branding capabilities, and digital retail infrastructure for specialty spice and seasoning brands. Capital is also directed toward traceability and supply chain digitization platforms that support export certification requirements and compliance with international food safety standards.

Future Market Outlook (2026-2034)

The Mexico spices and seasonings market is forecast to expand from USD 449.2 Million in 2025 to USD 680.4 Million by 2034 at a CAGR of 4.58%, adding roughly USD 231.2 Million in incremental market value over the forecast period.

Four forces will shape the market through 2034: continued expansion of Mexico's industrial food processing sector; growing global demand for authentic Mexican flavors driving export-oriented production; rising domestic consumer preference for premium, organic, and clean-label products; and the ongoing formalization of the spice supply chain through improved traceability, quality standards, and organized retail penetration.

By 2034, the Mexico spices and seasonings market is expected to be defined by a larger share of value-added and branded products, with artisan, regional, and certified organic categories capturing growing consumer interest. Sustainability in agricultural sourcing, compliance with evolving food safety regulations, and innovation in product formats and flavor applications are expected to further differentiate leading players and drive value creation across the market.

Research Methodology

Primary Research

Primary research included structured interviews with spice and seasoning manufacturers, food processing company procurement executives, retail buyers, agricultural sector representatives, and regulatory specialists, validating market sizing, regional demand patterns, segmentation dynamics, and competitive positioning within the Mexico spices and seasonings market.

Secondary Research

Secondary sources included Mexico's Secretariat of Agriculture and Rural Development (SADER) agricultural production data, INEGI national economic census reports, Secretariat of Economy trade statistics, PROFECO consumer data, industry association publications, and annual reports, investor presentations, and press releases from key market participants.

Forecasting Models

Market forecasts used top-down and bottom-up models combining domestic food production volumes, per capita spice consumption data, food processing industry growth trajectories, export demand evolution, and macroeconomic indicators including GDP growth, inflation, and household disposable income. Scenario analysis addressed agricultural supply disruptions, regulatory changes, and shifts in organized versus informal market dynamics.

Mexico Spices and Seasonings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Applications Covered | Meat and Poultry Products, Snacks and Convenience Food, Soups, Sauces and Dressings, Bakery and Confectionery, Frozen Products, Beverages, Others |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | McCormick & Company, Inc., Grupo Herdez, S.A.B. de C.V., Conservas La Costeña, S.A. de C.V., Unilever, Salsa Tamazula S.A. de C.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico spices and seasonings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico spices and seasonings market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico spices and seasonings industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Spices and Seasonings Market Report

The Mexico spices and seasonings market was valued at USD 449.2 Million in 2025, driven by rich culinary heritage, expanding food processing demand, and growing consumer interest in branded and premium seasoning products.

The market is projected to grow at a CAGR of 4.58% from 2026-2034, reaching USD 680.4 Million, supported by expanding food processing sector demand, growing export opportunities, and increasing consumer preference for premium and clean-label seasoning products.

Spices lead at 48.9% in 2025, driven by Mexico's extensive chili pepper cultivation, deep culinary traditions, and strong demand from both domestic consumers and food processing companies.

Meat and poultry products dominate at 29.4% in 2025, fueled by substantial domestic protein processing industry demand.

Central Mexico commands 42.8% in 2025, led by Mexico City's dense consumer base, high concentration of food manufacturers, and well-developed modern retail infrastructure.

Leading players include McCormick & Company, Inc., Grupo Herdez, S.A.B. de C.V., Conservas La Costeña, S.A. de C.V., Unilever, and Salsa Tamazula S.A. de C.V., among others.

Mexico's globally recognized culinary traditions, centered on chili peppers, mole preparations, and complex regional spice blends, generate deep and consistent domestic demand for diverse spice and seasoning categories, supporting both household consumption and professional food preparation across the country.

Key trends include growing demand for clean-label and organic spice products, premiumization of regional and artisan seasoning blends, expansion of convenience-oriented spice formats, and the accelerating role of e-commerce and digital retail channels in reaching urban consumers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)