Mexico Vehicle Financing Market Size, Share, Trends and Forecast by Vehicle Type, Loan Provider, Vehicle Condition, Purpose Type, and Region, 2026-2034

Mexico Vehicle Financing Market Size, Share, Trends & Forecast (2026-2034)

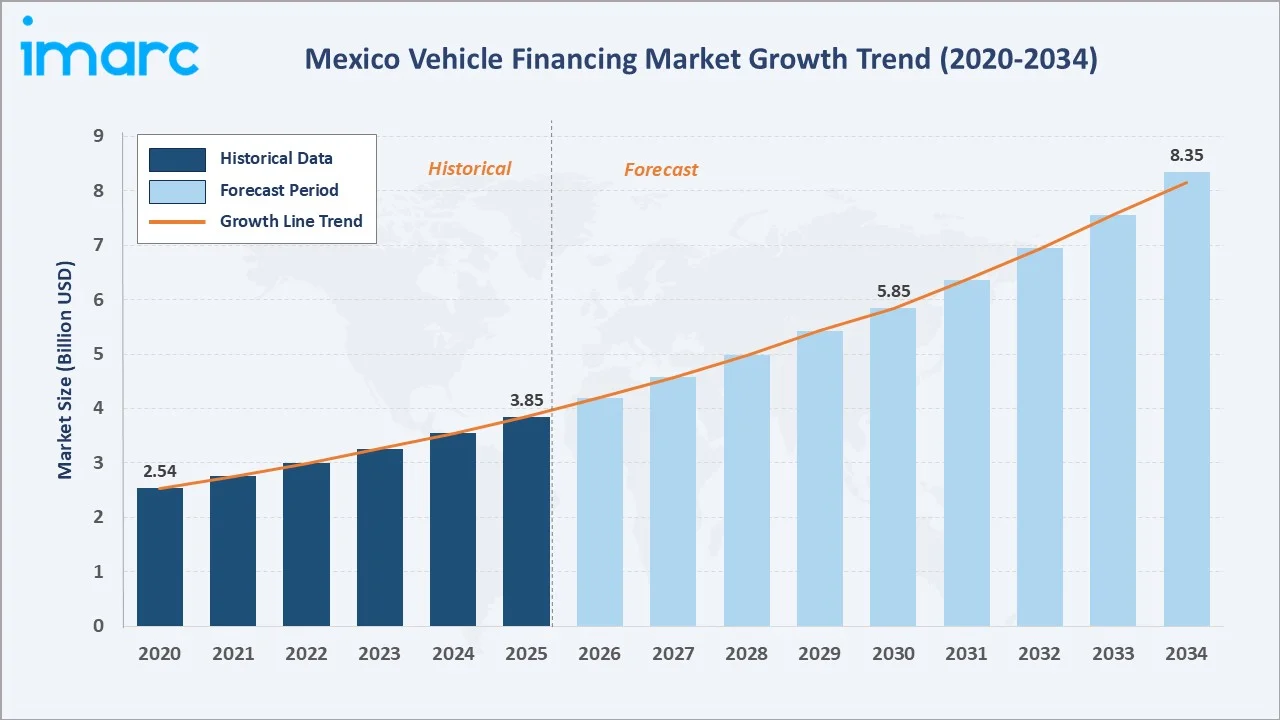

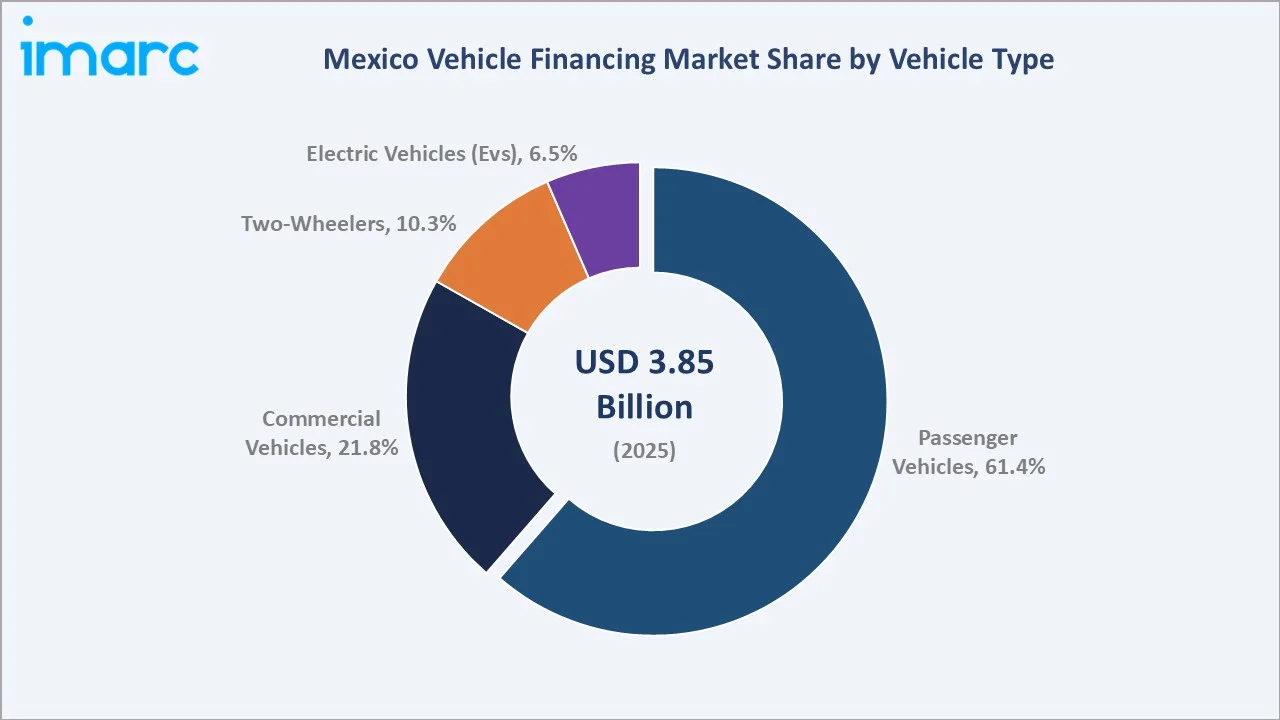

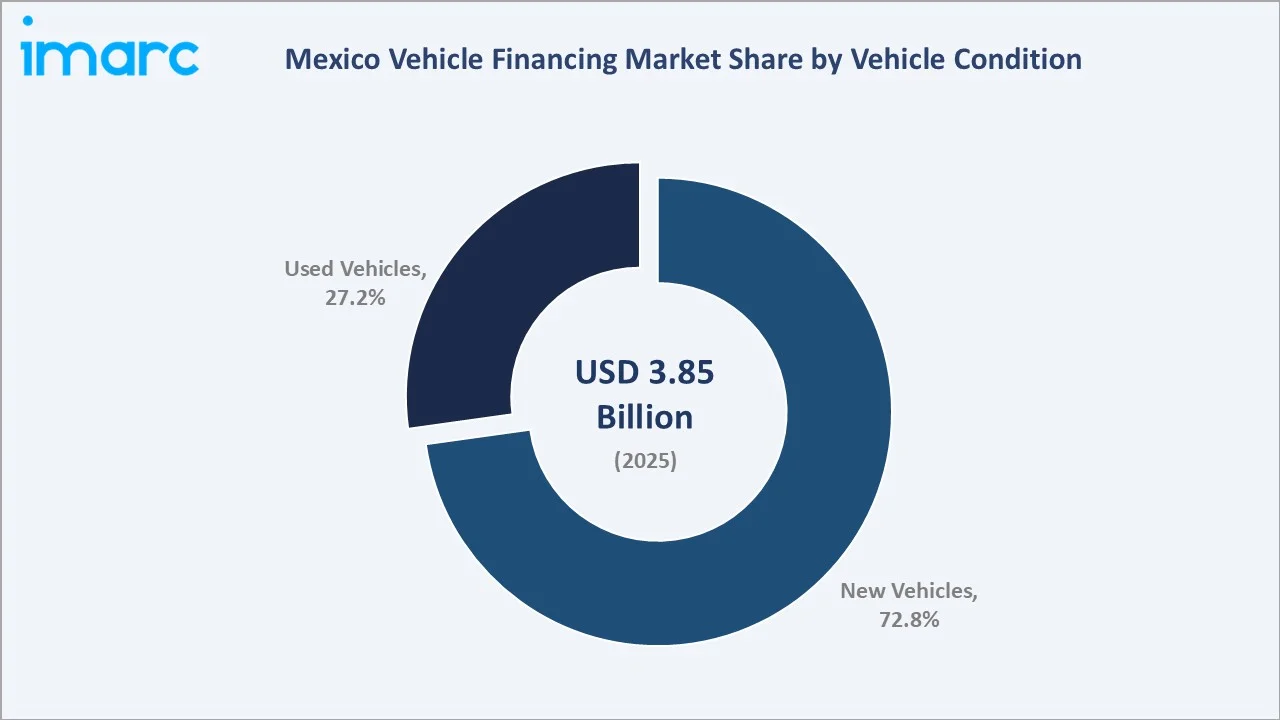

The Mexico vehicle financing market reached USD 3.85 Billion in 2025 and is projected to reach USD 8.35 Billion by 2034, growing at a CAGR of 8.71% during 2026-2034. Rising automobile sales, accelerating adoption of digital lending platforms, and expanding government financial inclusion policies are the primary growth catalysts. Passenger vehicles lead the vehicle-type segment with a 61.4% share in 2025, while new vehicles dominate the vehicle-condition segment at 72.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.85 Billion |

|

Forecast Market Size (2034) |

USD 8.35 Billion |

|

CAGR (2026-2034) |

8.71% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

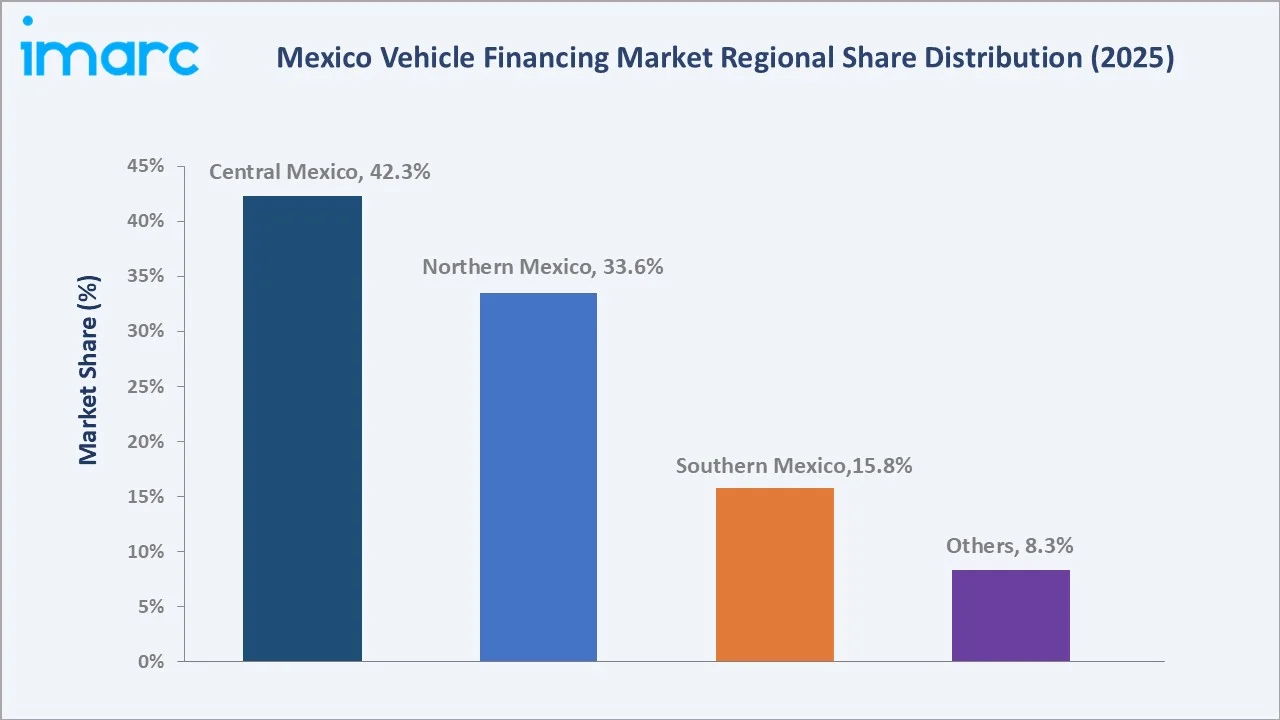

Central Mexico leads regionally, holding a 42.3% market share in 2025, anchored by the highest density of vehicle dealerships, commercial banks, and captive OEM finance operations in the country. Passenger vehicles command the largest vehicle-type share at 61.4%, driven by sustained consumer demand for personal mobility solutions, while new vehicles dominate the vehicle-condition segment at 72.8%, reflecting the preference for certified manufacturer warranties and lower interest rates on new vehicle loans.

To get more information on this market, Request Sample

Mexico’s vehicle financing market is underpinned by three structural forces: the country’s growing middle class driving demand for personal mobility, rapid digitalization of financial services enabling broader credit access, and government policies promoting financial inclusion across underserved urban and rural populations. These forces collectively sustain above-average CAGR through 2034, making vehicle financing one of Mexico’s most dynamic consumer financial services sectors.

Executive Summary

The Mexico vehicle financing market is experiencing robust expansion, driven by converging demand from passenger vehicle buyers, growing commercial fleet operators, and an increasingly active used-vehicle financing ecosystem. The market was valued at USD 3.85 Billion in 2025 and is forecast to reach USD 8.35 Billion by 2034, growing at a CAGR of 8.71%. This trajectory is anchored by Mexico’s sustained automotive production and sales activity, near-record USMCA-driven vehicle output, and the rapid maturation of digital lending channels that are bringing vehicle financing access to broader consumer segments.

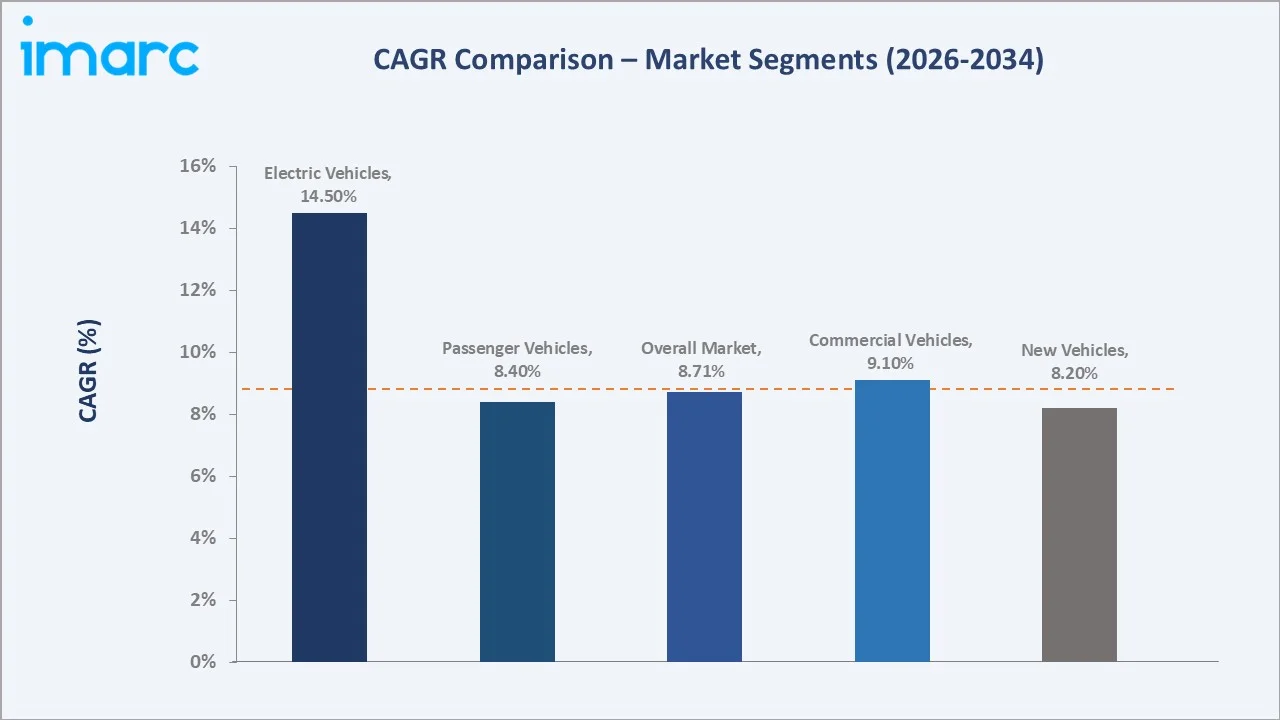

Passenger vehicles dominate the vehicle-type segment with a 61.4% share, reflecting the central role of personal vehicle ownership in Mexican urban mobility. Commercial vehicles at 21.8% reflect sustained logistics and goods transport financing demand, while two-wheelers at 10.3% represent growing demand for affordable mobility financing. Electric vehicles, though currently at 6.5%, represent the fastest-growing segment at an estimated 14.5% CAGR through 2034 as EV adoption accelerates under government incentive programs and OEM-captive financing offers.

New vehicles command a dominant 72.8% share of the vehicle-condition segment, supported by competitive dealer financing rates, OEM promotional offers, and consumer preference for warranty-backed purchases. Used vehicles at 27.2% are growing faster, driven by rising price sensitivity among middle and lower-income consumers and the expansion of dedicated used-vehicle financing platforms. Leading institutions collectively hold approximately 65–70% of market revenue through established branch networks and OEM partnerships.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Passenger Vehicles – 61.4% share (2025) |

|

Fastest Growing Vehicle Type |

Electric Vehicles (EVs) – ~14.5% CAGR (2026-2034) |

|

Largest Vehicle Condition |

New Vehicles – 72.8% share (2025) |

|

Fastest Growing Vehicle Condition |

Used Vehicles – ~9.8% CAGR (2026-2034) |

|

Leading Region |

Central Mexico – 42.3% share (2025) |

|

Top Companies |

BANCO BILBAO VIZCAYA ARGENTARIA, SA, Banco Santander S.A., Grupo Financiero Banorte, The Bank of Nova Scotia, TOYOTA MOTOR CORPORATION |

Key Analytical Observations Supporting the Above Data:

- Passenger vehicles account for 61.4% of Mexico’s vehicle financing market in 2025. This dominance reflects Mexico’s expanding urban middle class and the critical role of personal vehicle ownership in cities where public transportation coverage remains incomplete. Retail automotive financing in Mexico reached a record penetration rate of 75.5% during the first four months of 2026, supported by aggressive commercial strategies from automakers and their captive finance companies.

- New vehicles command 72.8% share (2025) of the market by vehicle condition, driven by consumer preference for certified manufacturer warranties, competitive new vehicle interest rates offered through OEM-captive programs, and the broader availability of financing products from banks and NBFCs for new vehicle purchases.

- Electric vehicles represent only 6.5% of the 2025 market but are projected to grow fastest with approximately 14.5% CAGR. Dedicated EV financing products from BBVA Mexico and Banorte, combined with federal EV adoption incentives and OEM promotional financing rates for EV models, are accelerating EV loan originations from a low base, setting the stage for significant share expansion through 2034.

- Central Mexico’s 42.3% regional share (2025) exhibits Mexico City’s status as the country’s automotive retail hub, with the highest density of new vehicle dealerships, established branch banking infrastructure, and the largest concentration of employed consumers with verifiable income supporting formal credit access.

Mexico Vehicle Financing Market Overview

Vehicle financing encompasses the range of credit products, auto loans, leasing arrangements, and revolving credit facilities, used by consumers and businesses to purchase or operate passenger vehicles, commercial vehicles, two-wheelers, and electric vehicles. Mexico’s market is served by commercial banks, non-banking financial companies (NBFCs), OEM-captive finance subsidiaries, credit unions, and emerging fintech lenders, each targeting distinct customer segments and vehicle categories.

Macroeconomic drivers include Mexico’s Finance Ministry projection of economic growth in the range of 1.8% to 2.8% for 2026, a formal sector employment base generating bankable consumer income, and the USMCA agreement sustaining Mexico’s automotive manufacturing competitiveness. Vehicle production reached a record 3.989 million units in 2024, representing a 5.6% increase, creating a steady supply of new vehicles feeding the dealership and financing ecosystem.

Market Dynamics

To evaluate market opportunities, Request Sample

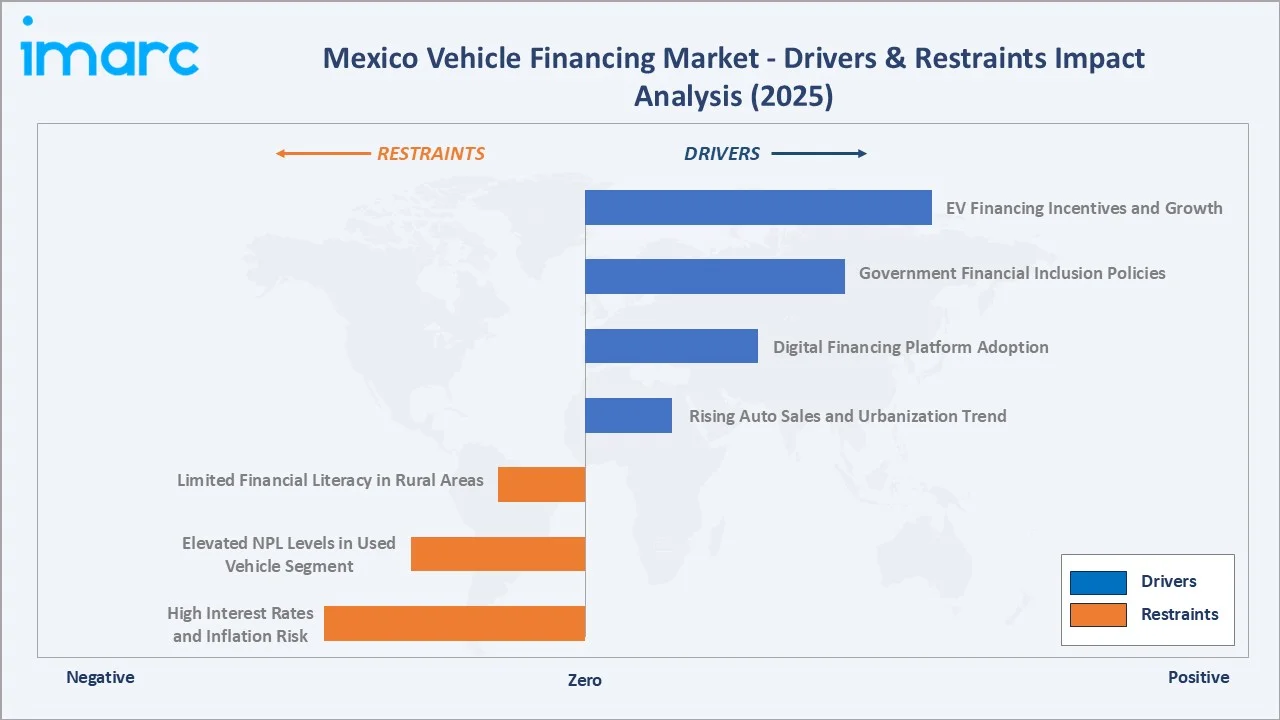

Market Drivers

- Rising Auto Sales and Urbanization Trend: Mexico’s automotive industry produced 1,642,083 light vehicles during the first five months of 2026, creating a structurally growing demand for financing solutions. Urban population growth at 1.22% from 2023 to 2024 and the continuing expansion of Mexico’s middle class are generating first-time vehicle buyers who rely on financing to make their initial auto purchase.

- Digital Financing Platform Adoption: Digitalization is transforming Mexico’s vehicle financing landscape, with fintech platforms, mobile banking applications, and OEM digital marketplaces enabling rapid loan pre-approvals and real-time eligibility assessments. BBVA Mexico’s digital lending platform and Santander’s auto digital portal are processing a growing share of loan originations online, reducing transaction costs and improving customer experience.

- Government Financial Inclusion Policies: Mexico’s government continues to expand financial inclusion through programs that benefit vehicle financing access. The Finabien credit program, launched in February 2024 under President Obrador’s directive through Financiera para el Bienestar, extended credit access to previously underserved recipients of government welfare programs.

- EV Financing Incentives and Growth: Mexico’s nascent EV ecosystem is creating a new, high-growth financing sub-segment. The federal government’s EV incentive framework, combined with OEM promotional financing rates, is stimulating first-time EV purchase financing across middle-income urban consumers. As EV model availability increases from brands in Mexico, dedicated EV loan products from major banks are expected to gain significant share through 2034.

Market Restraints

- High Interest Rates and Inflation Risk: Despite the monetary easing cycle beginning in 2024, Mexico’s auto loan interest rates remain elevated relative to the United States and other OECD markets, ranging from 12–22% annually for standard consumer vehicle loans, depending on credit profile and vehicle type. This pricing environment limits affordability for lower-income consumers and increases monthly repayment burdens for all borrowers, constraining the pace of financing market growth below its theoretical potential.

- Elevated NPL Levels in Used Vehicle Segment: Non-performing loan (NPL) ratios in Mexico’s used-vehicle financing segment are approximately 2–3 percentage points higher than in new-vehicle financing, reflecting the higher credit risk profile of used-vehicle borrowers and the lower collateral quality of aging vehicle assets. This elevated NPL environment has led some traditional banks to maintain conservative underwriting standards for used-vehicle loans, limiting credit availability precisely in the segment with the highest consumer demand growth.

- Limited Financial Literacy in Rural Areas: Despite urban financial infrastructure improvements, rural and peri-urban Mexico continues to face significant financial literacy gaps that constrain vehicle financing adoption. Many rural consumers lack familiarity with formal credit products, are uncertain about their eligibility, or distrust formal lending institutions, preferring informal financing arrangements. This literacy gap limits market penetration in Southern Mexico and rural areas of Northern Mexico, capping the total addressable market for formal vehicle financing below its demographic potential.

Market Opportunities

- Used Vehicle Financing Expansion: The used vehicle financing segment, currently representing 27.2% of the market by vehicle condition, offers significant growth potential as fintech-enabled underwriting makes it possible to serve credit-constrained consumers with efficient loan origination at acceptable risk levels. Used vehicle penetration in Mexico’s vehicle stock is significantly higher than in new vehicles, yet formal financing penetration remains comparatively low, representing an underpenetrated opportunity of USD 800 Million–1 Billion by 2028.

- Commercial Fleet and MSME Financing: Mexico’s micro, small, and medium enterprises (MSME) sector, which represents nearly 99% of businesses and generates 72% of employment, requires commercial vehicle financing for logistics, transport, and service delivery operations. Current commercial vehicle financing at 21.8% market share is underpenetrated relative to Mexico’s MSME population, as many micro-enterprise operators lack access to formal commercial vehicle credit.

Market Challenges

- Informal Economy and Credit History Gaps: A significant proportion of Mexico’s economically active population operates in the informal economy without formal payroll records, creating substantial credit history gaps that prevent access to standard bank auto loan products. Traditional credit scoring models based on formal income documentation exclude these consumers, limiting the addressable market for formal vehicle financing and requiring alternative data-based underwriting approaches that many established lenders have not yet fully developed.

- Currency Volatility and Import Cost Pressures: Mexico’s automotive market depends significantly on imported vehicle models and components priced in US dollars. Peso depreciation episodes increase vehicle prices in domestic currency terms, compressing affordability and raising the loan amounts required for purchase. Exchange rate volatility also increases operating cost uncertainty for auto finance institutions with dollar-denominated funding, creating margin management challenges that can limit pricing competitiveness in consumer markets.

Emerging Market Trends

1. Rapid Expansion of Used Vehicle Digital Financing Ecosystems

Mexico’s used vehicle market is undergoing a structural transformation driven by technology-enabled platforms that are digitizing the entire purchase and financing experience. Platforms offering integrated vehicle inspection, pricing, and instant financing approval are compressing the used-vehicle purchase cycle from weeks to hours, dramatically improving consumer experience and lender risk visibility. This digital ecosystem maturation is bringing the used-vehicle financing segment toward parity with new-vehicle financing in terms of origination efficiency, credit quality assessment, and customer satisfaction, positioning it for above-market growth through 2034.

2. OEM-Captive Finance Growth and EV Promotional Financing

OEM-captive finance subsidiaries, including Toyota Financial Services Mexico, Volkswagen Financial Services, and GM Financial Mexico, are aggressively expanding their market presence through dealer-embedded financing offers and EV-specific promotional programs. These captive finance arms offer below-market interest rates subsidized by manufacturers’ marketing budgets to drive vehicle sales volume, creating competitive pressure on bank auto loan products. The EV-specific financing segment is particularly active, with multiple OEMs offering 0–3.9% annual rate financing on EV models to accelerate adoption, a trend expected to intensify as EV model portfolios expand through 2027–2030.

3. AI-Driven Credit Scoring and Alternative Data Underwriting

Mexican auto finance institutions are increasingly deploying artificial intelligence and machine learning models that incorporate alternative data sources to assess creditworthiness for borrowers who lack traditional credit bureau records. This AI-driven underwriting revolution is expanding the formal auto financing market to millions of previously unbanked or thin-file consumers, particularly in the informal economy. Fintech platforms are leading this transformation, while traditional banks are investing in their own alternative data capabilities to avoid losing market share to digital-native competitors.

4. Embedded Finance and Dealer Digital Ecosystem Integration

The integration of vehicle financing directly into automotive retail digital platforms is creating seamless “embedded finance” experiences that reduce consumer friction and increase financing conversion rates at the point of sale. BBVA Mexico and Santander have established API partnerships with major automotive digital marketplaces and OEM digital platforms to embed pre-approved financing offers directly in the vehicle browsing experience. This embedded finance model is expected to capture an increasing share of auto loan originations from traditional branch-based processes through 2034.

Industry Value Chain Analysis

Mexico’s vehicle financing value chain spans vehicle manufacturing through loan disbursement and borrower repayment management, with each stage occupied by specialized institutions whose performance directly influences product pricing, credit availability, and consumer experience.

|

Stage |

Key Players / Examples |

|

Vehicle Manufacturers |

OEM automotive brands with captive finance arms, EV manufacturers offering direct financing, and commercial vehicle producers |

|

Dealerships & Distributors |

Authorized new vehicle dealers, used-vehicle lots, certified pre-owned networks, and digital automotive marketplace platforms |

|

Financing Providers |

Commercial banks, NBFCs, OEM-captive finance subsidiaries, credit unions, and fintech lenders |

|

Credit & Risk Assessment |

Credit bureaus, AI underwriting platforms, KYC, and identity verification providers |

|

Loan Disbursement |

Digital disbursement platforms, bank payment processing systems, dealer finance desk operations, and OEM direct finance portals |

|

Borrower & End User |

Individual consumer borrowers, MSME commercial vehicle operators, corporate fleet managers, and ride-share platform drivers |

Technology Landscape in the Mexico Vehicle Financing Industry

Digital Lending Platforms and Mobile-First Auto Finance

Mobile banking applications and dedicated digital auto-finance platforms have emerged as the dominant origination channels for vehicle loans in Mexico’s urban markets. BBVA Mexico’s mobile application enables end-to-end vehicle loan applications with instant credit decisions based on customer banking history and bureau data, while Santander’s digital auto portal connects prospective borrowers with dealer inventory and financing options in a single integrated flow. Loan application-to-approval cycles that required 3–5 business days through traditional branch processes are now completed in minutes through digital channels, improving customer experience and increasing financing conversion rates.

AI-Based Credit Decisioning and Risk Management

Advanced machine learning models are reshaping credit decisioning in Mexico’s auto finance industry, enabling lenders to make faster, more accurate credit assessments by analyzing thousands of data points beyond traditional bureau scores. Banorte and HSBC Mexico have deployed proprietary AI underwriting models that incorporate vehicle valuation data, income pattern analysis, and behavioral banking data to generate real-time credit decisions for auto loan applications. These AI systems are particularly valuable in assessing creditworthiness for self-employed and informal-sector borrowers who lack formal payroll documentation but demonstrate strong financial management behaviors through digital transaction patterns.

OEM Digital Finance Integration and Embedded Lending

Automotive manufacturers are integrating financing capabilities directly into their consumer digital touchpoints, creating seamless purchase experiences where vehicle selection and financing approval occur within a single platform. Toyota Financial Services Mexico’s digital portal and GM Financial’s dealer portal connectivity enable consumers to receive personalized financing offers based on their vehicle selection and profile without visiting a bank branch.

Digital Identity Verification and Open Banking Infrastructure

Mexico’s regulatory advancement in open banking infrastructure, mandated under the Fintech Law of 2018, is enabling lenders to access customer financial data from multiple institutions with consumer consent, creating more comprehensive credit profiles for auto loan underwriting. Digital identity verification using biometric authentication and electronic signature platforms is eliminating the paper-based documentation requirements that previously slowed loan origination, particularly for used-vehicle financing, where faster processing is critical to matching the pace of informal sales transactions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Passenger Vehicles |

61.4% |

2025 |

|

Vehicle Condition |

New Vehicles |

72.8% |

2025 |

|

Loan Provider |

🔒 |

🔒 |

2025 |

|

Purpose Type |

🔒 |

🔒 |

2025 |

|

Region |

Central Mexico |

42.3% |

2025 |

By Vehicle Type

Passenger vehicles dominate the market with a 61.4% share in 2025. This segment encompasses personal auto loans for sedans, SUVs, hatchbacks, and minivans purchased by individual consumers and small families across Mexico’s urban and suburban markets. The passenger vehicle financing segment is anchored by strong OEM-captive finance programs, competitive bank auto loan products, and sustained consumer demand from a growing middle class prioritizing personal mobility.

To access detailed market analysis, Request Sample

Commercial vehicles represent 21.8% of the market, serving MSME logistics operators, construction companies, passenger transport businesses, and corporate fleet managers who rely on financing to acquire pickups, trucks, buses, and commercial vans. Two-wheelers at 10.3% reflect growing demand for affordable mobility financing, supported by rising urban commuting needs and expanding delivery services. Electric vehicles, currently at 6.5%, are the fastest-growing type segment, projected to reach approximately 12–15% of vehicle financing volume by 2034 as EV model availability expands and financing costs decrease.

By Vehicle Condition

New vehicles command a dominant 72.8% share in 2025, reflecting the structural preference of both consumers and lenders for new vehicle financing. Consumers benefit from manufacturer warranties, competitive OEM promotional financing rates, and the reliability assurance of an unused vehicle, while lenders prefer new vehicles as collateral due to their higher liquidation value and predictable depreciation schedules.

Used vehicles represent 27.2% of the market and are growing at a faster pace (~9.8% CAGR) as digital platforms, including Kavak, Seminuevos.com, and bank-backed used-vehicle finance programs, make pre-owned vehicle credit more accessible. Rising new-vehicle prices driven by global semiconductor cost pressures and peso depreciation are pushing price-sensitive consumers toward the used-vehicle segment, structurally expanding the addressable market for used-vehicle financing through 2034.

Regional Market Insights

Central Mexico’s market leadership (42.3%, 2025) reflects its status as Mexico’s most developed consumer financial services market. Mexico City and the surrounding metropolitan area concentrate the country’s highest vehicle dealership density, the headquarters of all major commercial banks, and the largest pool of formally employed consumers with bankable income profiles, creating the optimal environment for vehicle financing market depth and product sophistication.

Northern Mexico at 33.6% represents the country’s most commercially active vehicle financing zone outside of the capital. Monterrey’s large industrial base, including automotive, steel, and FMCG manufacturing, generates significant commercial vehicle fleet financing demand from logistics operators and production companies.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Central Mexico |

42.3% |

Mexico City metropolitan area’s highest vehicle dealership and bank branch density; largest formally employed consumer base; highest disposable income levels |

|

Northern Mexico |

33.6% |

Monterrey’s industrial and commercial economic base, generating fleet and commercial vehicle financing demand; border region cross-border vehicle import financing |

|

Southern Mexico |

15.8% |

Infrastructure development programs stimulating commercial vehicle financing; growing middle class in Oaxaca and Chiapas state capitals; tourism sector vehicle leasing |

|

Others |

8.3% |

Agricultural and energy sector vehicle financing in secondary states; government program-driven financial inclusion expanding rural auto credit access; growing fintech platform penetration in underserved communities |

Competitive Landscape

Mexico’s vehicle financing market exhibits moderate-to-high concentration, with the top institutions collectively holding approximately 65–70% of market revenue in 2025. Commercial banks dominate through established dealer finance desk relationships and broad branch networks, while OEM-captive finance subsidiaries compete aggressively on promotional interest rates supported by manufacturer marketing budgets.

|

Company Name |

Key Products/ Solutions |

Market Position |

Core Strength |

|

BANCO BILBAO VIZCAYA ARGENTARIA, SA |

Auto Loan, Leasing, EV Finance |

Market Leader |

One of the largest digital auto-finance platform; AI underwriting; broadest branch and dealer network coverage |

|

Banco Santander S.A. |

Commercial Vehicle Financing, Crédito Automotriz Santander |

Market Leader |

OEM partnership depth; strong dealer finance desk penetration; digital origination capabilities |

|

Grupo Financiero Banorte |

Banorte Auto Rental, Banorte Used Cars, New Car Payroll, New Cars Payroll Used Cars, Preferred Auto Loan, Banorte Green Car Rental |

Strong Challenger |

Leading domestic bank brand; MSME commercial vehicle expertise; AI credit decisioning investment |

|

The Bank of Nova Scotia |

Crédito Automotriz, AutoMatch, CrediAuto, Invoice Value, ExCrediAuto, Safer Fleet |

Challenger |

Competitive pricing; Latin American network synergies; growing used-vehicle finance capability |

|

TOYOTA MOTOR CORPORATION |

Toyota Financial Services Traditional Plan, Plan Balloon, Annual Plan, Financial leasing, Pure Lease |

OEM Leader |

OEM-captive promotional rates; Toyota/Lexus ecosystem integration; EV and hybrid financing leadership |

Commercial banks compete primarily on branch network coverage, digital channel capability, and breadth of financial service relationships. OEM-captive finance companies compete on promotional interest rate offers, seamless dealership integration, and brand-aligned financing experiences.

Key Company Profiles

BANCO BILBAO VIZCAYA ARGENTARIA, SA

BANCO BILBAO VIZCAYA ARGENTARIA SA’s subsidiary, BBVA Mexico, is one of the largest commercial banks and the leading vehicle financing institution by loan portfolio volume. The company serves both individual consumers and corporate fleet customers through its nationwide branch network and digital banking platforms.

- Product Portfolio: BBVA Auto Loan (new and used vehicles), BBVA Leasing, BBVA EV Finance (competitive rates for electric and hybrid vehicles), and BBVA Fleet Financing for corporate customers.

- Recent Developments: In July 2025, BBVA Mexico allocated an average of MXN 578 million per month to finance hybrid and electric vehicles, marking a 47% increase vs. 2024 and raising green vehicle loans to 15% of its auto portfolio. The bank’s partnership with Omoda Jaecoo has financed 8,565 units since May 2023, while BBVA plans to expand green auto financing through Chinese brands, including Geely, Great Wall Motor, and Neta Auto.

- Strategic Focus: Digital-first auto loan origination; AI underwriting expansion for informal economy borrowers; EV financing product development; deepened OEM-captive co-financing partnerships.

Banco Santander S.A.

Banco Santander S.A.’s subsidiary Santander Mexico is one of Mexico’s largest commercial banks and a leading vehicle financing institution with particular strength in new vehicle dealer finance programs.

- Product Portfolio: Santander Crédito Auto, Santander Auto Digital (online loan application), and Commercial Vehicle Financing.

- Recent Developments: In September 2025, Santander México has financed more than 2,700 Tesla electric vehicles since 2020, totaling nearly MXN 1.82 billion. Santander also became the first bank in Mexico to join the Electro Mobility Association (EMA), supporting EV financing and charging-infrastructure projects as Mexico’s EV and hybrid sales continue to expand.

- Strategic Focus: OEM-captive partnership expansion; used-vehicle finance digital transformation; MSME commercial vehicle product development; Northern Mexico market share growth.

Market Concentration Analysis

Mexico’s vehicle financing market exhibits moderate-to-high concentration at the top tier, with the leading institutions holding 65–70% of total market revenue. Below the top players, a competitive secondary tier of 15–20 institutions, including domestic banks, regional credit unions, and specialized fintech platforms, serves niche segments.

Consolidation is progressing through digital capability investment rather than M&A, with the top institutions competing to establish dominant digital origination platforms that reduce marginal origination costs and improve borrower experience. OEM-captive finance subsidiaries are the primary disruptive force, as their manufacturer-subsidized interest rate offers are structurally advantaged versus third-party bank products, particularly for new vehicle financing.

Investment & Growth Opportunities

Fastest Growing Segments

Electric vehicle financing (~14.5% CAGR) and used vehicle financing (~9.8% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined addressable opportunity of approximately USD 2.5–3 Billion by 2030 within Mexico’s vehicle financing ecosystem, as EV adoption accelerates and the used-vehicle digital marketplace matures into a fully formal financing channel.

Emerging Market Expansion

Southern Mexico, currently representing only 15.8% of the national vehicle financing market revenue, offers significant underpenetrated growth potential. Government infrastructure investment through the Tren Maya, Interoceanic Corridor, and regional highway programs is generating economic activity, income growth, and vehicle purchase demand in states including Oaxaca, Chiapas, Yucatan, and Veracruz. Financial institutions establishing dealer finance relationships and digital lending channels in these markets early are positioned to capture structurally growing financing demand through 2034.

Venture and Institutional Investment Trends

- The Fintech Law framework continues to attract venture capital into Mexico’s auto lending space. Dedicated used-vehicle fintech lenders and embedded finance platforms are attracting Series A and B investment rounds, with aggregate sector investment reaching an estimated USD 200–300 Million annually through 2025. This venture investment is accelerating product innovation and underwriting technology development that benefits the broader market.

- EV infrastructure investment from major institutional investors is accelerating Mexico’s charging network expansion, which in turn reduces consumer range anxiety barriers to EV purchase, creating a virtuous cycle that expands EV financing demand. Financial institutions with established EV lending products are positioned to capture disproportionate benefit from this infrastructure investment wave through 2028–2032.

Future Market Outlook (2026-2034)

Mexico’s vehicle financing market is positioned for sustained, high-growth expansion through 2034. From a base of USD 3.85 Billion in 2025, the market is projected to reach USD 8.35 Billion by 2034, representing total incremental value creation of USD 4.5 Billion at a CAGR of 8.71%.

This growth is underpinned by Mexico’s automotive industry scale, its deepening integration into North American vehicle supply chains through USMCA, and the progressive digitalization of lending that is expanding credit access to previously underserved consumer segments.

The financing mix will shift toward higher-value and specialty segments by 2034. Electric vehicle financing is projected to grow from 6.5% to approximately 15–18% of market volume, while used-vehicle financing’s share is expected to rise from 27.2% to approximately 32–35% as digital platforms mature. Commercial vehicle financing will benefit from Mexico’s continued nearshoring-driven logistics growth. The digital origination channel is projected to account for more than 50% of auto loan originations by 2030, up from an estimated 25–30% in 2025.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including auto loan product managers at major commercial banks, OEM-captive finance executives, vehicle dealership finance directors, fintech lending company founders, and CONDUSEF regulatory officials. Expert input validated market sizing, product mix trends, digital origination adoption rates, and regional demand dynamics.

Secondary Research

Secondary research encompassed institution annual reports, Banco de México credit market data, INEGI vehicle registration statistics, AMIA (Asociación Mexicana de la Industria Automotriz) automotive sales data, AMDA dealership association reports, CONDUSEF consumer finance transparency publications, and industry analysis publications covering Mexico’s financial services and automotive sectors.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating vehicle sales volume projections, auto loan penetration rates by vehicle type and consumer segment, average loan amounts by vehicle category, and lender revenue data. A base-case CAGR of 8.71% reflects consensus estimates validated against Banco de México credit trends, lender investor guidance, and AMIA vehicle sales projections from 2020 to 2025.

Mexico Vehicle Financing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Electric Vehicles (EVs) |

| Loan Providers Covered | Banks, Non-Banking Financial Companies (NBFCs), Original Equipment Manufacturers (OEMs) Financing, Credit Unions, Others |

| Vehicle Conditions Covered | New Vehicles, Used Vehicles |

| Purpose Types Covered | Loan, Leasing |

| Regions Covered | Northern Mexico, Central Mexico, Southern Mexico, Others |

| Companies Covered | BANCO BILBAO VIZCAYA ARGENTARIA, SA, Banco Santander S.A., Grupo Financiero Banorte, The Bank of Nova Scotia, TOYOTA MOTOR CORPORATION, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Mexico vehicle financing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Mexico vehicle financing market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Mexico vehicle financing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Mexico Vehicle Financing Market Report

The Mexico vehicle financing market reached USD 3.85 Billion in 2025 and is projected to reach USD 8.35 Billion by 2034, growing at a CAGR of 8.71% during 2026-2034.

Passenger vehicles lead with a 61.4% market share in 2025, driven by sustained consumer demand for personal mobility, competitive OEM-captive financing rates, and the central role of automobile ownership in Mexican urban and suburban lifestyles.

New vehicles dominate with a 72.8% market share in 2025, supported by consumer preference for warranty-backed purchases, competitive OEM promotional financing rates, and lender preference for new vehicles as higher-quality loan collateral with more predictable depreciation.

Central Mexico leads with a 42.3% share in 2025, anchored by Mexico City’s concentration of vehicle dealerships, bank headquarters, OEM-captive finance operations, and the largest formally employed consumer base with bankable income profiles.

Some of the leading institutions include BANCO BILBAO VIZCAYA ARGENTARIA, SA, Banco Santander S.A., Grupo Financiero Banorte, The Bank of Nova Scotia, and TOYOTA MOTOR CORPORATION, competing through digital origination capabilities, OEM dealer partnerships, and broad product portfolios spanning new and used vehicle financing.

EV financing growth is driven by expanding OEM promotional rate programs, federal government EV adoption incentives, increasing EV model availability from brands, and growing consumer awareness of EV total-cost-of-ownership advantages.

Key challenges include elevated auto loan interest rates relative to developed markets, limiting affordability, and the informal economy’s exclusion of a large consumer population from traditional credit bureau-based underwriting.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)