Middle East Sportswear Market Size, Share, Trends and Forecast by Product, Distribution Channel, End User, and Country 2026-2034

Middle East Sportswear Market Size, Share, Trends & Forecast (2026-2034)

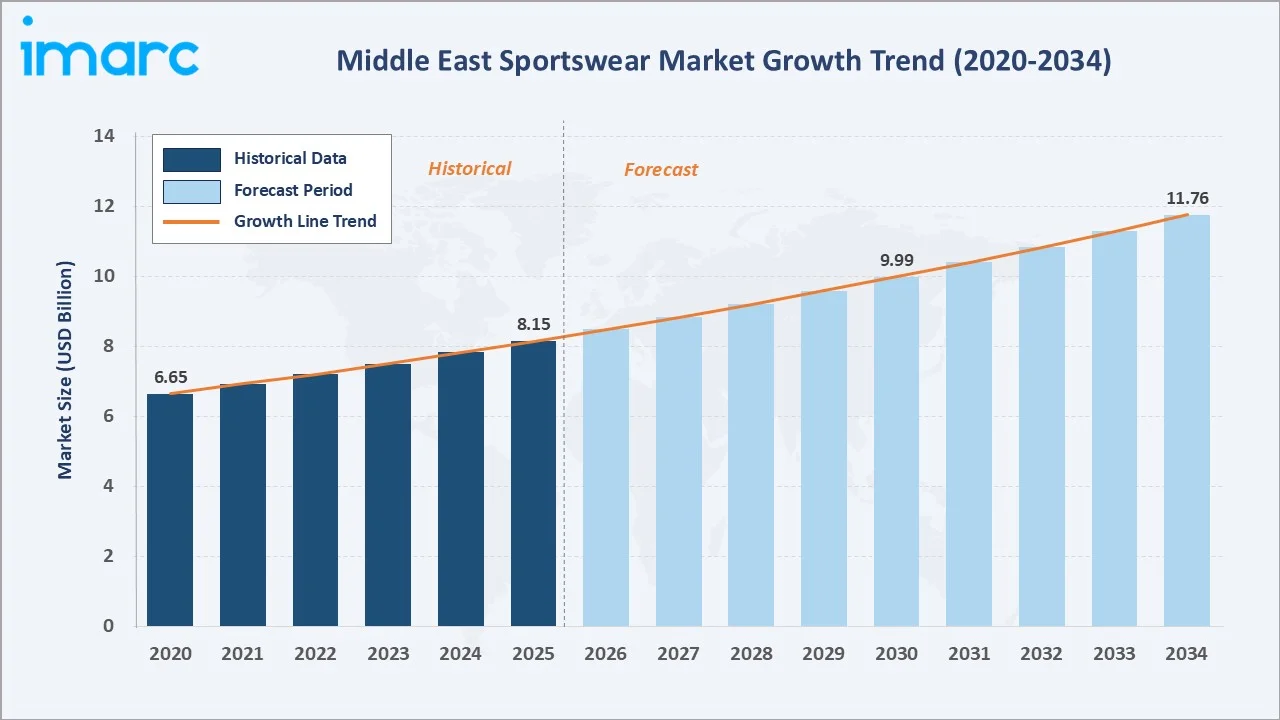

The Middle East sportswear market size reached USD 8.15 Billion in 2025 and is projected to reach USD 11.76 Billion by 2034, exhibiting a CAGR of 4.16% during 2026-2034. The region's rapidly growing fitness culture, government-backed sports programs such as Saudi Arabia's Vision 2030, rising female athlete participation, and expanding e-commerce infrastructure are the primary drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.15 Billion |

|

Forecast Market Size (2034) |

USD 11.76 Billion |

|

CAGR (2026-2034) |

4.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

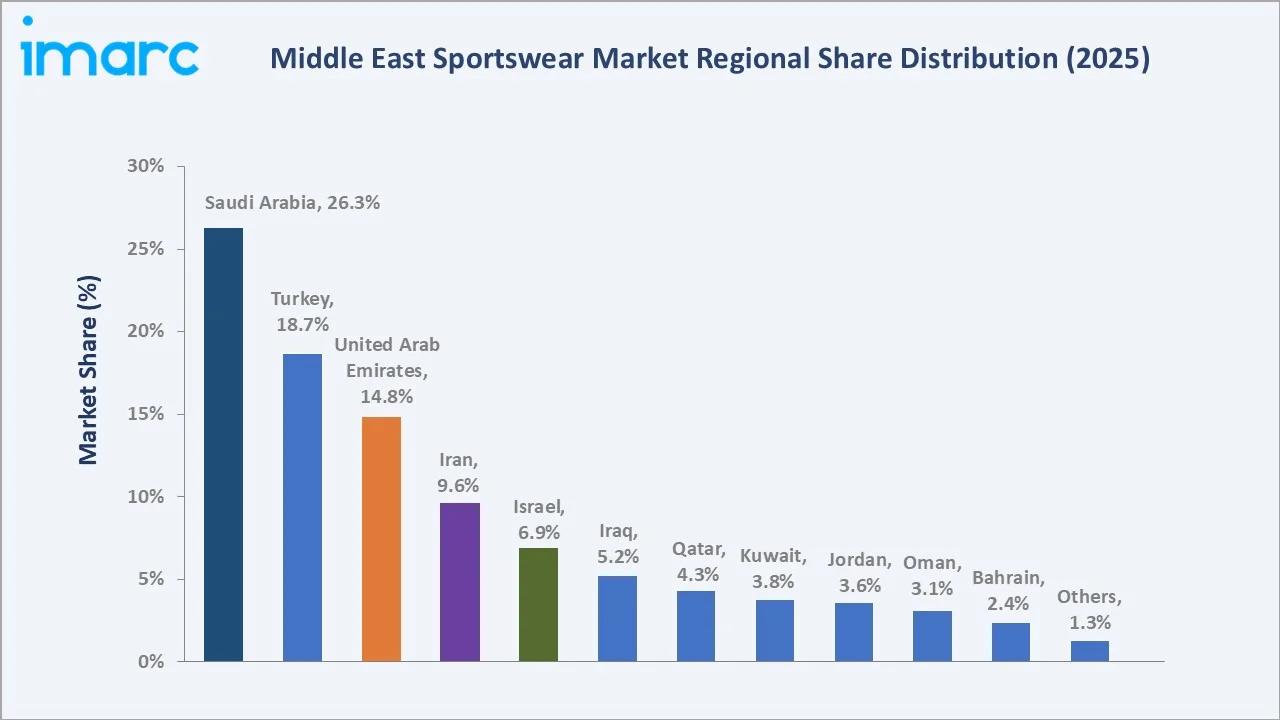

Saudi Arabia (26.3% share, 2025) |

|

Fastest Growing Country |

Saudi Arabia |

|

Leading Product |

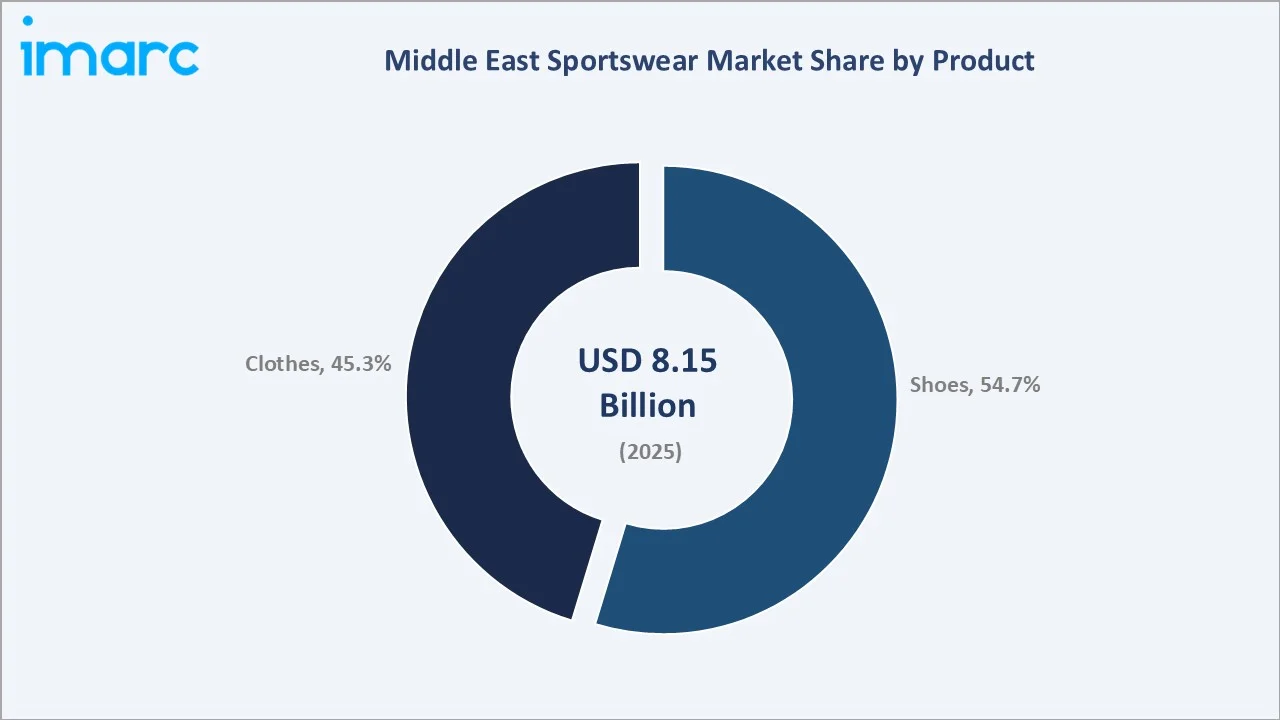

Shoes (54.7%, 2025) |

|

Leading End User |

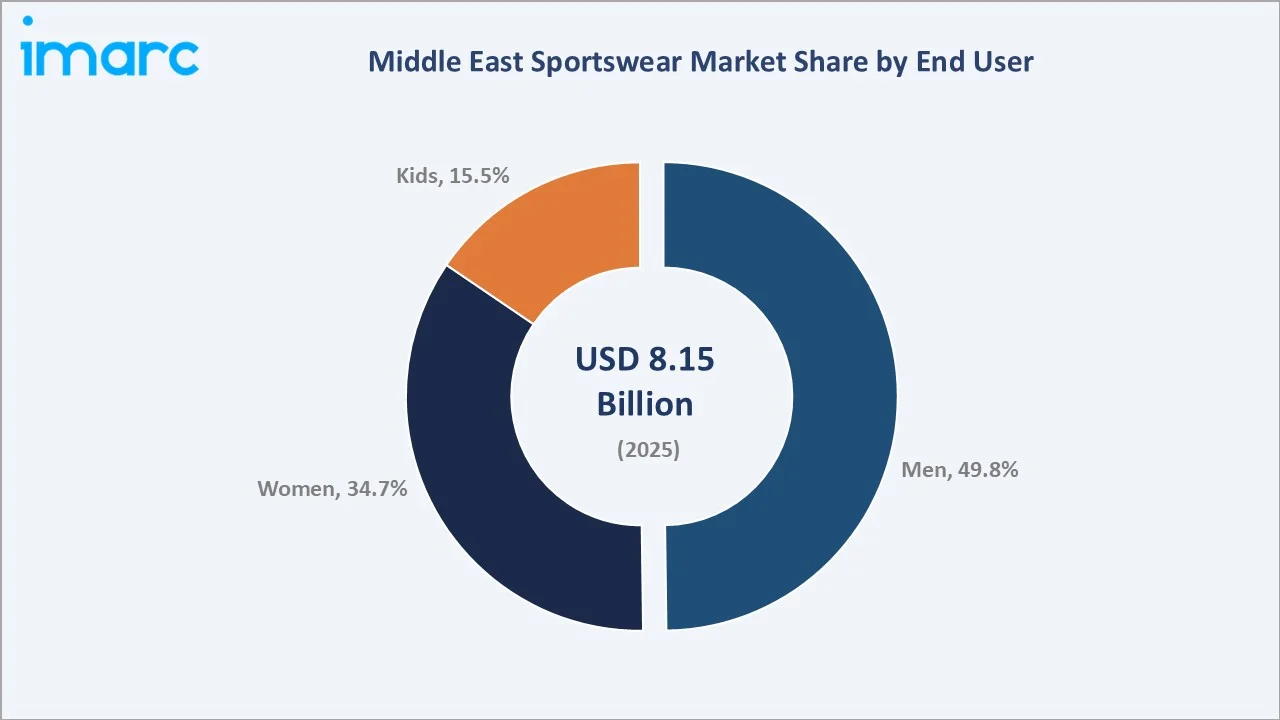

Men (49.8%, 2025) |

The Middle East Sportswear Market growth trajectory (2020–2034) shows a strong shift from steady post-pandemic recovery to accelerated expansion driven by fitness adoption, athleisure trends, and rising disposable incomes across GCC countries.

To get more information on this market, Request Sample

The chart above illustrates the Middle East sportswear market's historical expansion from USD 6.65 Billion in 2020 to USD 8.15 Billion in 2025, alongside the forecast growth trajectory reaching USD 11.76 Billion by 2034, driven by sustained CAGR of 4.16% through fitness adoption and infrastructure investment.

Executive Summary

The Middle East sportswear market is experiencing a sustained growth phase, underpinned by structural demographic shifts, lifestyle transformation, and ambitious government investment in sport and wellness. Valued at USD 8.15 Billion in 2025, the market is forecast to reach USD 11.76 Billion by 2034 at a CAGR of 4.16%.

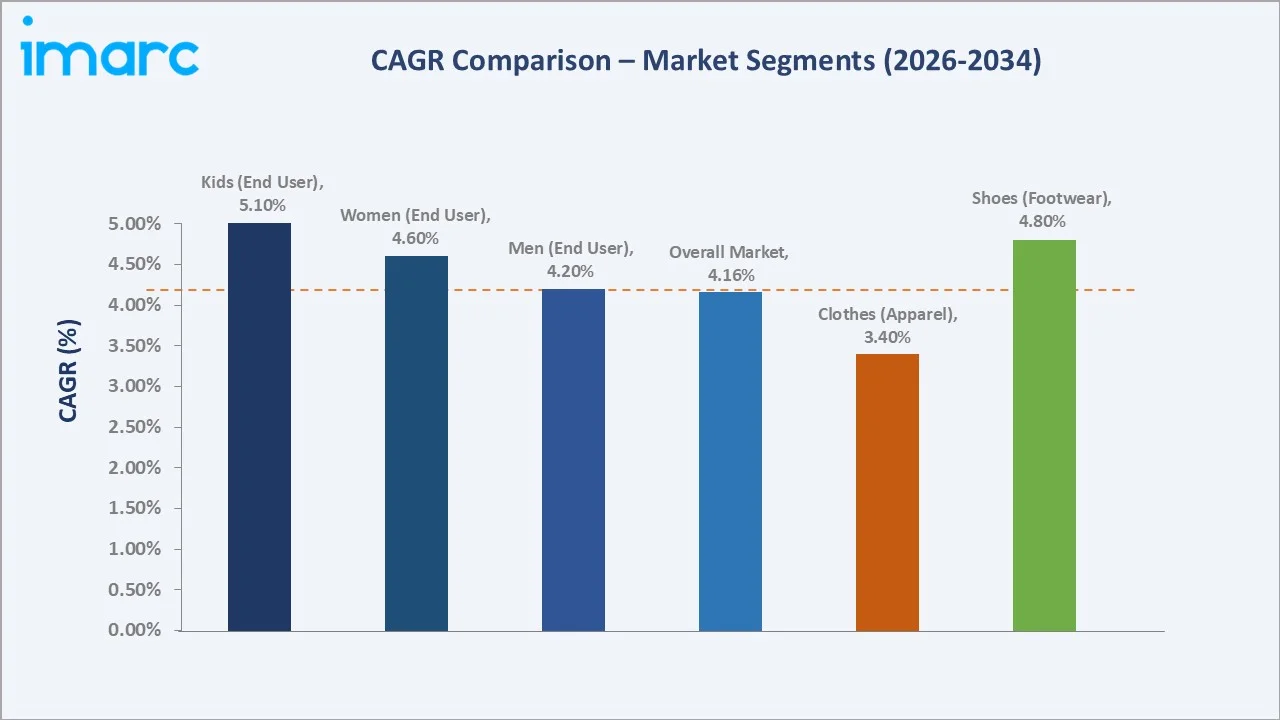

Shoes dominate the product mix with a 54.7% revenue share in 2025, reflecting strong demand for athletic footwear in football, running, and gym training. The clothing segment holds the remaining 45.3% and is growing steadily, propelled by athleisure adoption and performance apparel purchases. Among end users, men lead at 49.8%, though the women's segment is the fastest-growing cohort, expanding at approximately 4.6% CAGR through 2034 as female sports participation increases across the region, supported by regulatory liberalization in key markets.

Saudi Arabia commands a dominant 26.3% share, followed by Turkey at 18.7% and the UAE at 14.8%. Government initiatives - particularly Vision 2030 and the UAE's National Sports Strategy - are converting passive policy support into active sportswear procurement demand. E-commerce is an accelerating force; online channel growth is outpacing brick-and-mortar retail, enabling global brands to reach previously underserved markets. The competitive landscape is led by Nike, Adidas, and Puma, with Decathlon gaining ground through its value-for-money vertical integration model across physical and digital channels.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Shoes - 54.7% share (2025) |

|

Second Product |

Clothes - 45.3% share (2025) |

|

Largest End User |

Men - 49.8% share (2025) |

|

Fastest Growing End User |

Women - ~4.6% CAGR (2026-2034) |

|

Leading Country |

Saudi Arabia - 26.3% revenue share (2025) |

|

Second Country |

Turkey - 18.7% revenue share (2025) |

|

Top Companies |

Nike, Inc., Adidas AG, Puma SE, Under Armour, Decathlon, Asics Corporation, New Balance, and Lotto Sport Italia Spa |

|

Market Opportunity |

Smart sportswear & e-commerce expansion |

Supporting Analytical Observations:

- Shoes' 54.7% dominance in 2025 reflects the region's strong football culture, driven by widespread football participation and the global rise of sneaker culture across UAE, Saudi Arabia, and Turkey.

- The Clothes segment's 45.3% share is gaining momentum via the athleisure megatrend, with demand for tracksuits, hoodies, and performance T-shirts growing across both sports and casual lifestyle occasions.

- Men's 49.8% majority reflects higher participation in organized sports and fitness club memberships. Gym penetration in Saudi Arabia grew by over 16.8% between 2020 and 2023, directly expanding performance apparel and footwear demand.

- Women's segment at 34.7% is the fastest-growing end-user cohort, supported by government-mandated inclusion in physical education curricula and increased female gym membership across GCC countries.

- Saudi Arabia's 26.3% dominance is underpinned by Vision 2030 investments targeting 40% sports participation by 2030, allocating over USD 13.3 Billion to sports and recreation infrastructure through 2025-2030.

- Turkey's 18.7% share reflects a strong domestic manufacturing base, enabling cost-competitive local brands to coexist with global players across footwear and activewear categories.

Middle East Sportswear Market Overview

Sportswear, also referred to as athletic apparel, encompasses clothing and footwear specifically designed for physical performance, fitness activity, and athletic participation. Products in this category include tracksuits, athletic shoes, hoodies, compression garments, shorts, and sport-specific performance apparel, crafted from flexible, moisture-wicking materials such as polyester-spandex blends, nylon-cotton composites, and advanced technical fabrics. Applications span football, basketball, running, cycling, gym training, swimming, and outdoor recreation.

The Middle East market sits at the intersection of accelerating fitness culture, demographic youth bulges, rising disposable incomes, and active government investment. Saudi Arabia's Vision 2030 and the UAE's National Sports Strategy are transforming sports from leisure activity to economic development priority, embedding sportswear demand into the region's structural growth narrative through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

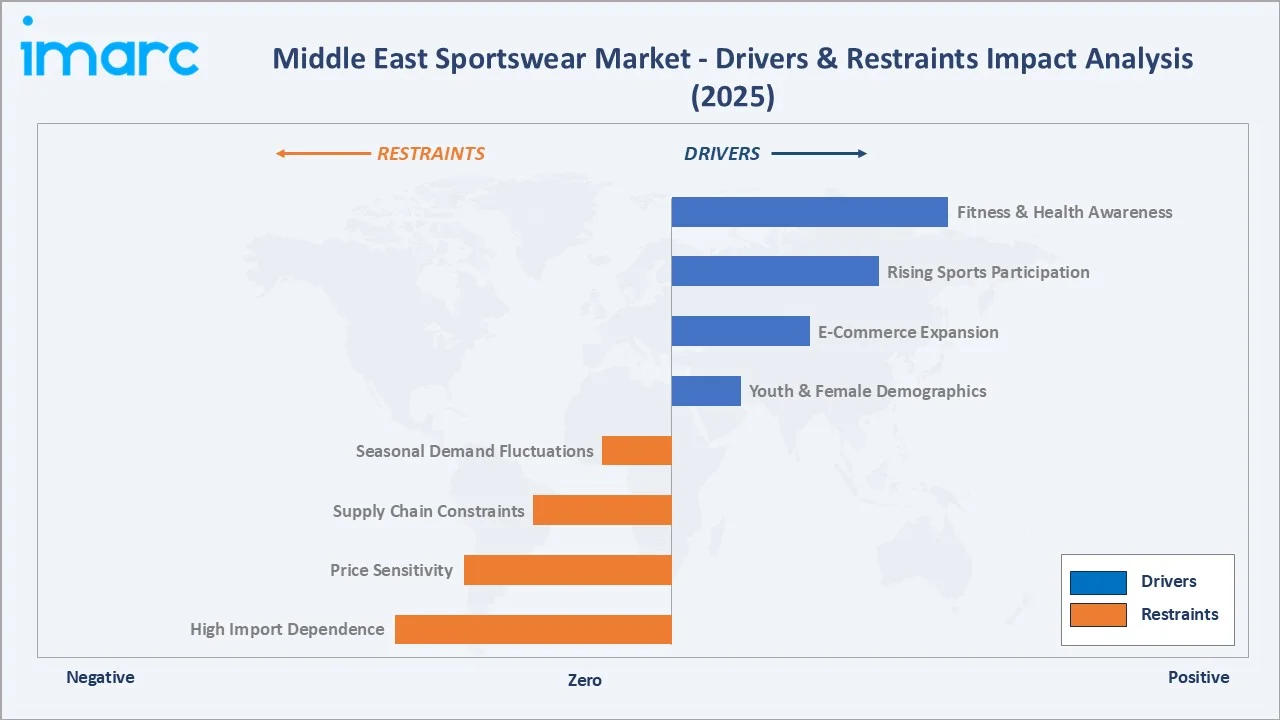

Market Drivers

- Rising Fitness and Health Awareness: Health-conscious lifestyles are reshaping consumer behaviour across the Middle East. The KSA fitness service market is transforming and is valued at approximately USD 1.06 billion in 2025. Government wellness campaigns and school-level physical education mandates are embedding fitness as a cultural norm, directly sustaining sportswear demand.

- Government Sports Programs and Vision 2030: Saudi Arabia's Vision 2030 targets 40% physical activity participation among citizens by 2030. The government has allocated approximately USD 13 Billion to sports infrastructure. These initiatives are directly stimulating institutional and consumer sportswear procurement.

- Growing Female Sports Participation: The removal of restrictions on women's sports participation in Saudi Arabia, combined with increased female inclusion in physical education across GCC nations, has created a new and rapidly expanding consumer segment. Women's sportswear demand is growing at approximately 4.6% CAGR through 2034.

- E-Commerce and Digital Retail Expansion: Smartphone penetration exceeds 90% in Saudi Arabia and UAE in 2025. Online sportswear channels are growing at rates significantly outpacing offline retail, supported by improved regional logistics, social commerce influence, and direct-to-consumer strategies deployed by global brands including Nike and Adidas.

Market Restraints

- High Dependency on Imports: Limited domestic production and increasing reliance on imports exposes the Middle East sportswear market to supply chain disruptions, currency volatility, and higher landed costs, thereby limiting price competitiveness in premium segments.

- Price Sensitivity Beyond GCC Core Markets: Markets such as Iraq, Jordan, and Oman exhibit significant price sensitivity, limiting premium brand penetration. Value-oriented purchasing behavior constrains average selling price expansion in these sub-markets.

- Seasonal Demand Fluctuations: Extreme summer heat in Gulf states reduces outdoor sports activity and associated sportswear purchasing during peak summer months, creating seasonal demand troughs that complicate inventory planning.

Market Opportunities

- Women's Sportswear Sub-Category: The women's segment represents the most structurally underpenetrated growth opportunity. Female-specific product lines, including sport hijabs, modest activewear, and performance swimwear, are growing rapidly. Global brands investing in this sub-category stand to capture disproportionate share.

- Smart and Technology-Integrated Sportswear: Demand for smart fabrics, compression analytics garments, and wearable technology-integrated sportswear is nascent but accelerating, particularly in UAE and Saudi Arabia. Brands offering technology-enhanced performance products at accessible price points can establish first-mover positioning.

- Direct-to-Consumer Digital Channels: Regional e-commerce platforms, social commerce, and brand apps represent a major untapped opportunity for market penetration. Digital channels bypass traditional retail margin structures, enabling brands to offer competitive pricing while capturing higher margins.

Market Challenges

- Brand Proliferation and Competitive Saturation: The proliferation of global, regional, and private-label sportswear brands is intensifying shelf space competition and compressing brand loyalty cycles. Consumers in UAE and Saudi Arabia exhibit higher brand-switching behaviour than global averages.

- Counterfeit and Grey Market Competition: Counterfeit sportswear, particularly across footwear categories, represents a significant revenue diversion. Grey market imports reduce effective addressable market size for legitimate brand distributors.

Emerging Market Trends

1. Athleisure and Fashion-Sport Convergence

The boundary between sportswear and everyday fashion is increasingly blurring. A large share of sportswear demand in the UAE is now driven by casual, non-athletic use, making athleisure a key growth engine for both premium and mid-range apparel brands. Global labels such as Adidas and Puma are expanding regionally tailored collections that blend modest fashion influences with performance-oriented fabrics.

2. Rise of Female Sports Participation

The structural shift in female consumer behaviour is among the most significant trends in the Middle East sportswear market. Women's segment CAGR of approximately 4.6% outpaces the market average. Saudi Arabia's inclusion of girls' physical education in public schools since 2017 has created a sustained pipeline of young female sportswear consumers reaching purchasing maturity through 2030.

3. Smart and Technology-Integrated Apparel

Smart fabrics integrating biometric monitoring, temperature regulation, and muscle compression analytics are moving from laboratory development into early commercial adoption. Although still a niche segment of overall sportswear revenues in the Middle East, it is expected to scale significantly by 2034, led by demand from high-income consumers in the UAE and Saudi Arabia.

4. Sustainability and Eco-Friendly Materials

Environmental consciousness is emerging as a purchase criterion, particularly among younger consumers in UAE and Israel. Brands offering recycled polyester, organic cotton blends, or water-efficient manufacturing certifications are gaining preference in premium retail channels. Adidas' Parley Ocean plastic collections have achieved double-digit sell-through rates in regional outlets.

5. E-Commerce and Social Commerce Acceleration

Social commerce - purchasing via Instagram, TikTok, and Snapchat - is growing rapidly in the region. Influencer-driven sportswear marketing is achieving conversion rates 3-4x higher than traditional digital advertising. Platforms such as Noon Sports and international marketplaces are investing in regional warehousing to reduce delivery times, removing a key barrier to online sportswear purchasing.

Industry Value Chain Analysis

The Middle East sportswear value chain spans six integrated stages from raw material sourcing through end-consumer purchase. Each stage presents distinct competitive dynamics and margin structures relevant to overall Middle East sportswear market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Polyester, nylon, cotton, spandex, synthetic rubber |

|

Component Manufacturers |

Fabric mills, mesh weavers, foam/insole suppliers, zipper makers |

|

OEM / Brand Manufacturers |

Nike, Inc., Adidas AG, Puma SE, Under Armour, Decathlon |

|

Quality & Certification |

ISO 9001, Oeko-Tex, country-specific compliance bodies |

|

Distribution Channels |

Retail stores, specialty sports outlets, online platforms |

|

End Users |

Men, Women, Kids - athletes, fitness enthusiasts, casual wearers |

Brand manufacturers - particularly Nike, Inc., Adidas AG, Puma SE - hold the highest strategic value by integrating materials, design intellectual property, and digital commerce ecosystems into unified consumer propositions. Meanwhile, e-commerce platforms and direct-to-consumer brands are restructuring distribution, allowing manufacturers to bypass traditional multi-tier retail and capture higher margins while enhancing direct consumer data capture.

Technology Landscape in the Sportswear Industry

Advanced Fabric and Materials Innovation

Polyester-spandex blends remain the dominant material platform, offering stretch, moisture management, and durability at accessible price points. However, technical fabric innovation is accelerating. Graphene-infused textiles offering thermal regulation, antimicrobial properties, and conductivity for biometric monitoring are transitioning from premium niche to commercial mainstream. Recycled synthetic fibers - including ocean-recovered PET used by Adidas in its Parley line - are gaining commercial scale, with production expected to account for over 20% of synthetic sportswear fabrics globally by 2030.

Smart Connectivity and Wearable Integration

Sportswear’s convergence with wearable technology is forming a new hybrid product category. Compression garments with embedded EMG sensors, GPS-enabled running apparel, and IoT-connected footwear with pressure-mapping capabilities are transitioning from early-stage innovation to commercially viable offerings. In the Middle East, fitness technology retailers in the UAE are reporting strong year-on-year growth in smart sportswear interest, while integration with platforms such as Apple Health, Samsung Health, and regional fitness applications is accelerating consumer adoption.

E-Commerce Technology and Digital Commerce

Augmented reality (AR) virtual try-on tools deployed by Nike, Inc. and Adidas AG across regional e-commerce platforms are improving digital shopping experiences and reducing return rates. AI-driven personalization engines are also enhancing product recommendation accuracy, contributing to higher basket sizes on sports e-commerce platforms. In parallel, advancements in regional logistics infrastructure, including same-day delivery in the UAE and next-day fulfillment in Saudi Arabia, are significantly reducing delivery friction and strengthening online adoption of sportswear.

Automation in Manufacturing and Quality Control

Automation in sportswear manufacturing is improving production efficiency and reducing per-unit costs while shortening lead times. Turkish manufacturers, which supply a significant share of regional demand, are increasingly investing in automated cutting, bonding, and quality inspection systems, strengthening Turkey’s position as a key technologically advanced production hub. In footwear assembly in particular, robotics adoption is expected to deliver notable cost reductions by 2030.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Shoes |

54.7% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

End User |

Men |

49.8% |

2025 |

|

Region |

Saudi Arabia |

26.3% |

2025 |

By Product

To access detailed market analysis, Request Sample

Shoes dominate the Middle East sportswear market with a 54.7% share in 2025, equivalent to approximately USD 4.46 Billion. Demand is driven by the region's strong football culture, rapidly growing running and gym communities, and the global sneaker/lifestyle footwear trend. Athletic footwear is the most visible sportswear category in regional retail, commanding premium shelf space in mall-based sports stores.

By End User

Men represent the largest end-user segment at 49.8% of total market revenue in 2025, underpinned by higher male participation in organized sport, corporate fitness programs, and recreational athletics. Football, basketball, running, and gym training collectively drive the majority of male sportswear purchases. Premium brand adoption is highest in this segment, with Nike and Adidas commanding above-average brand loyalty among male consumers in Saudi Arabia and UAE.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Saudi Arabia |

26.3% |

Vision 2030 fitness programs, young demographics, rising female participation |

|

Turkey |

18.7% |

Strong manufacturing base, growing domestic sports culture |

|

UAE |

14.8% |

High disposable income, tourism, luxury sportswear demand |

|

Iran |

9.6% |

Large youth population, growing fitness awareness |

|

Israel |

6.9% |

High per-capita income, technology-driven fitness trends |

|

Iraq |

5.2% |

Recovering retail sector, urbanization-driven demand |

|

Qatar |

4.3% |

Post-FIFA 2022 sports legacy, high-income consumer base |

|

Kuwait |

3.8% |

Affluent consumer base, premium brand preference |

|

Jordan |

3.6% |

Growing youth fitness culture, e-commerce adoption |

|

Oman |

3.1% |

Increasing sportswear adoption, outdoor sports growth |

|

Bahrain |

2.4% |

Small but affluent market, e-commerce growth |

|

Others |

1.3% |

Emerging markets with nascent sportswear sectors |

Saudi Arabia commands a dominant 26.3% revenue share in 2025. National sports clubs, new fitness facility networks, and school physical education expansion are creating sustained, multi-year sportswear demand pipelines. Female market liberalization is unlocking a previously untapped consumer segment. Saudi Arabia is also investing in hosting global sports events.

Turkey holds a substantial 18.7% market share. The country benefits from a strong domestic textile and sportswear manufacturing ecosystem that enables local brands to compete effectively against global imports on price and turnaround time. Turkey's young, sports-active population and growing middle class sustain domestic consumption. The country's strategic position as a manufacturing hub for European and Middle Eastern markets provides incremental economic value that reinforces its overall sportswear market position.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Nike, Inc. |

Nike / Air Max, Jordan |

Leader |

Innovation, global distribution, digital ecosystem |

|

Adidas AG |

Adidas / Originals, Boost |

Leader |

Design leadership, sustainability, Middle East presence |

|

Puma SE |

Puma / King, Future |

Challenger |

Football heritage, fashion-sport crossover appeal |

|

Under Armour |

UA / Project Rock |

Challenger |

Performance tech, rapid regional expansion |

|

Decathlon |

Decathlon / Kipsta, Kalenji |

Challenger |

Value pricing, vertical integration, wide SKU range |

|

Asics Corporation |

Asics / Gel series |

Niche Player |

Running specialty, biomechanics R&D |

|

New Balance |

New Balance / Fresh Foam |

Niche Player |

Premium running, lifestyle crossover |

|

Lotto Sport Italia Spa |

Lotto / Leggenda |

Emerging |

Tennis/football niche, regional distribution expansion |

The Middle East sportswear market's competitive landscape is moderately fragmented. Global powerhouses Nike, Inc., Adidas AG, Puma SE collectively account for an estimated 45-50% of regional premium market revenue in 2025.

Decathlon has emerged as a significant value-tier disruptor, leveraging its vertically integrated model to offer broad product ranges at competitive price points across physical megastores and online channels.

Strategic differentiation is occurring along three axes: technology-led performance, sustainability credentials, and value-price integration. Under Armour is deploying a focused performance-athlete strategy to consolidate its fitness and CrossFit consumer base in GCC markets. Local and regional brands are competitive in the entry-level segment in Turkey, Iran, and Egypt, leveraging proximity manufacturing advantages.

Key Company Profiles

Nike, Inc.

Nike, Inc. is an American multinational corporation and the world’s largest designer, marketer, and distributor of athletic footwear, apparel, equipment, and accessories. Headquartered near Beaverton, Oregon, USA. It serves consumers across North America, Europe, the Middle East, Africa, Greater China, and Asia Pacific.

- Product Portfolio: Nike's Middle East product portfolio includes React and ZoomX performance running shoes, Air Max lifestyle footwear, Dri-FIT and Pro compression apparel, and sport-specific equipment for football (Mercurial, Phantom), basketball (Kobe, LeBron), and training.

- Recent Developments: In 2026, Nike launched its “Style By” concept in the Middle East for Ramadan, bringing sport-inspired fashion into the modest lifestyle and seasonal dressing space. The campaign reinterprets sportswear through breathable performance fabrics and versatile layering, reflecting how consumers in the UAE, Saudi Arabia, and Qatar adapt clothing for Ramadan’s daily rhythm.

- Strategic Focus: Nike's Middle East strategy centers on direct-to-consumer digital acceleration, member program expansion, and culturally resonant product campaigns targeting the region's young, aspirational demographic. The brand is investing in Arabic-language digital content and partnership with regional sports leagues.

Adidas AG

Adidas AG is a German multinational corporation and one of the world’s leading manufacturers of sportswear, footwear, apparel, and sporting goods. Headquartered in Herzogenaurach, Germany, the company has strong presence across Middle Eastern retail markets with particular strength in UAE and Saudi Arabia.

- Product Portfolio: Adidas's regional portfolio spans Ultraboost running footwear, Predator and Copa football boots, Originals lifestyle apparel, Parley ocean-plastic sustainability collections, and sports-specific performance gear across football, tennis, and training.

- Recent Developments: In 2025, Adidas launched its Spring/Summer 2025 Sportswear Collection in the Middle East in collaboration with Saudi label Kaf by Kaf. The collection debuted at Adidas’s first regional runway show in Saudi Arabia and is now available in select global stores.

- Strategic Focus: Adidas is targeting sustainability leadership, football market penetration through Saudi Pro League and Turkish Super Lig sponsorships, and expansion of its women's modest sportswear range to capitalize on the growing female athlete segment.

Puma SE

Puma SE is a German multinational company specializing in the design, development, and marketing of sportswear, footwear, apparel, and accessories. It is one of the world’s leading athletic brands, known for combining sport performance with lifestyle and fashion positioning. The company is headquartered in Herzogenaurach, Germany.

- Product Portfolio: Puma's regional offering includes Future and King football boots, Velocity and Nitro running footwear, and the Puma x AMI, Puma x Skepta lifestyle collaborations that drive premium brand culture awareness among younger consumers.

- Recent Developments: In 2025, Puma opened its new City Walk store in Dubai, introducing the brand’s global “Field of Play” retail concept to the Middle East. The store features an immersive design focused on performance, lifestyle, and sport categories, showcasing footwear, apparel, and accessories in a modern experiential format.

- Strategic Focus: Puma is focusing on brand culture partnerships, football sponsorships, and digital influencer collaborations to strengthen its position with 18-30-year-old consumers in GCC and Turkish markets.

Market Concentration Analysis

The Middle East sportswear market exhibits moderate fragmentation. The top three players - Nike, Inc., Adidas AG, Puma SE- collectively account for an estimated 45-50%% of total regional market revenue in 2025.

The market is experiencing a bifurcated consolidation dynamic. At the premium tier, global leaders are consolidating through brand equity investment, digital channel ownership, and regional athlete sponsorships that create durable consumer loyalty. Simultaneously, value-tier competition is intensifying as Decathlon's multi-sport house brand model, Turkish domestic manufacturers, and Chinese sportswear entrants pressure mid-market price points.

This dual dynamic is compressing the competitive viability of mid-tier mono-brand sportswear companies without strong regional identity or technological differentiation. Consolidation through brand acquisition, regional distribution partnerships, and digital commerce investment is expected to reduce the number of commercially viable independent regional brands.

Investment & Growth Opportunities

Fastest-Growing Segments

The women's sportswear sub-segment is the highest-growth structural opportunity, growing at approximately 4.6% CAGR through 2034. Brands developing modest activewear product lines tailored to regional aesthetic and functional preferences have limited competition and significant margin upside. The Kids segment at 15.5% is growing steadily as school sports programs expand, driven by Vision 2030's youth development investment.

Emerging Market Expansion

Iraq and Iran represent the region's most underpenetrated large markets. Iraq's recovering retail infrastructure and Iran's large youth population represent significant medium-term volume opportunities as market access improves. Oman and Jordan are experiencing accelerating fitness culture penetration, creating retail expansion windows for brands with regional distribution capacity. Qatar's post-FIFA 2022 sports legacy infrastructure continues to generate elevated long-term sportswear demand.

Venture and Strategic Investment Trends

Regional sports technology ventures are attracting rising investor interest. Fitness app platforms, sports e-commerce marketplaces, and smart apparel startups in the UAE and Saudi Arabia have secured growing venture funding in recent years. International sportswear brands are increasingly pursuing joint ventures and franchise agreements to navigate market entry complexities in markets such as Iran and Iraq. Decathlon’s equity expansion model partnering with local franchise operators for rapid store rollout serves as a reference framework for competitors seeking non-organic market share expansion.

Future Market Outlook (2026-2034)

The Middle East sportswear market forecast projects steady value expansion from USD 8.15 Billion in 2025 to USD 11.76 Billion by 2034 at a CAGR of 4.16%. Growth will be driven by a combination of structural demographic tailwinds, continued government investment in sports culture, and accelerating digital commerce penetration.

Saudi Arabia will retain regional leadership while accelerating through Vision 2030's final phase. The 2034 FIFA World Cup - for which Saudi Arabia is the leading host candidate - represents a multi-year sportswear demand catalyst that would significantly elevate market scale during the 2030-2034 period. UAE will sustain premium value growth through continued sports tourism investment and a growing affluent expatriate consumer base. Turkey will maintain its dual role as both a significant consumer market and the region's primary manufacturing hub.

Technology disruption will reshape competitive differentiation. Smart sportswear, AI-driven personalization in e-commerce, and sustainability mandates will redefine product development priorities. Brands investing in direct-to-consumer digital infrastructure and regionally relevant product design will capture disproportionate market share gains through 2034. The women's and kids' segments will grow faster than the overall market, creating distinct sub-market opportunities for brands with appropriate product portfolios.

Research Methodology

Primary Research

IMARC Group's primary research process involves conducting structured interviews with industry stakeholders including brand executives, regional distributors, sports retailers, fitness facility operators, and category buyers. Primary interviews contribute approximately 30-40% of the total data inputs, providing real-time validation of market sizing estimates, competitive positioning, and emerging trend identification across key markets including Saudi Arabia, UAE, and Turkey.

Secondary Research

Secondary research encompasses analysis of published trade data, government sports investment reports, company annual reports and investor presentations, customs and trade statistics, sports federation participation data, and independent industry publications. Key secondary data sources include national sports councils, retail trade associations, GCC government economic diversification reports, and brand investor presentations.

Forecasting Models

Market sizing and forecasting employ a combination of bottom-up and top-down methodologies. The bottom-up approach aggregates country-level and segment-level revenue estimates derived from product category volumes, average selling prices, and consumer penetration rates. The top-down approach applies macro-economic and demographic multipliers to regional fitness participation data and retail spend per capita.

Middle East Sportswear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Shoes, Clothes |

| Distribution Channels Covered | Online Stores, Retail Stores |

| End Users Covered | Men, Women, Kids |

| Countries Covered | Saudi Arabia, Turkey, Israel, United Arab Emirates, Iran, Iraq, Qatar, Kuwait, Oman, Jordan, Bahrain, Others |

| Companies Covered | Nike, Inc., Adidas AG, Puma SE, Under Armour, Decathlon, Asics Corporation, New Balance, Lotto Sport Italia Spa, etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Middle East sportswear market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Middle East sportswear market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Middle East sportswear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Middle East Sportswear Market Report

The Middle East sportswear market reached USD 8.15 Billion in 2025, driven by rising fitness awareness, expanding youth demographics, and government-led sports initiatives.

The market is projected to reach USD 11.76 Billion by 2034, advancing at a CAGR of 4.16% during 2026-2034, supported by e-commerce growth and female sports participation.

The Middle East sportswear market is expected to grow at a CAGR of 4.16% between 2026 and 2034.

Shoes dominate with a 54.7% market share in 2025, driven by demand for athletic footwear in football, running, and gym activities across the region.

Men represent the largest end-user segment at 49.8% in 2025, reflecting higher male participation in organized sports and fitness activities.

Saudi Arabia leads with a 26.3% market share in 2025, backed by Vision 2030 sports investments and a young, fitness-conscious population.

Key drivers include rising health awareness, growing female sports participation, government sports programs (Vision 2030), and rapid e-commerce adoption in the region.

Key players include Nike, Inc., Adidas AG, Puma SE, Under Armour, Decathlon, Asics Corporation, New Balance, and Lotto Sport Italia Spa.

Key trends include smart/tech-integrated apparel, athleisure crossover, sustainability-driven products, rising female athlete segments, and direct-to-consumer digital channels.

Online sportswear sales are growing at a significantly higher rate, driven by smartphone penetration, social media influence, and improved regional logistics infrastructure.

Saudi Arabia's Vision 2030 promotes sport, wellness, and active lifestyles, boosting sportswear demand and creating long-term structural growth for the market.

The market is moderately fragmented. Global leaders hold dominant positions, while regional players and value-oriented brands compete effectively in specific countries.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)