Military Robotics and Autonomous Systems Market Report by Technology (UAVs, UGVs, AUVs, and Others), Operation (Fully Autonomous, Semi-Autonomous), Platform (Land based, Air based, Sea based), End Use (Military and Defense, Homeland Security), Application (Intelligence, Surveillance, And Reconnaissance (ISR), Combat, Logistics, Search & Rescue, Mine Detection & Clearance, and Others), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Military Robotics and Autonomous Systems Market Size:

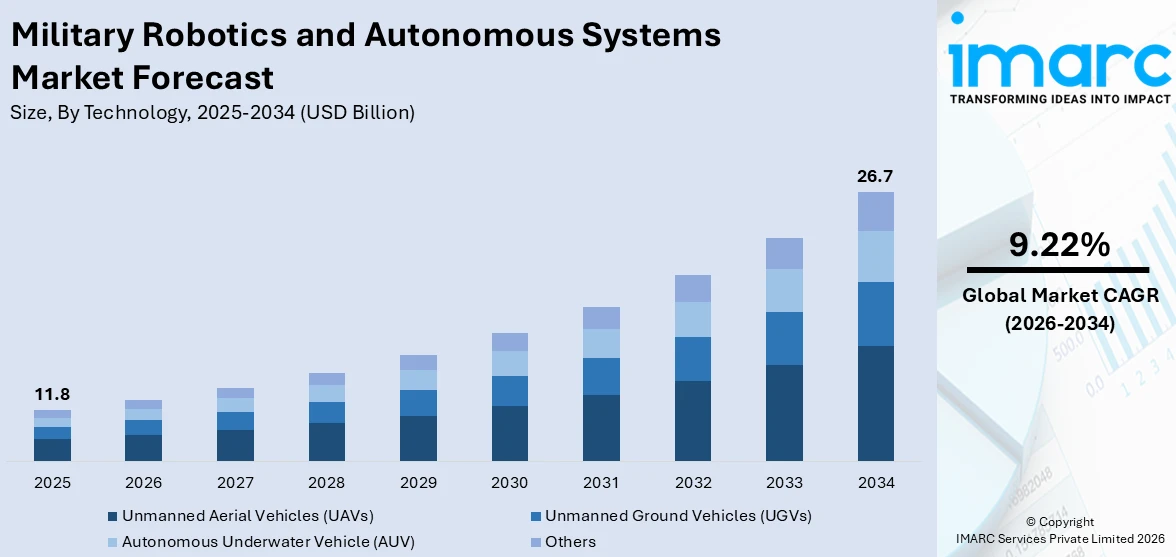

The military robotics and autonomous systems market size reached USD 11.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 26.7 Billion by 2034, exhibiting a growth rate (CAGR) of 9.22% during 2026-2034. North America dominated the market in 2025. The market is experiencing steady growth driven by increasing number of geopolitical tensions and security threats, rising number of collaborations and partnerships between companies, and the integration of advanced technologies, such as artificial intelligence (AI).

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 11.8 Billion |

| Market Forecast in 2034 | USD 26.7 Billion |

| Market Growth Rate (2026-2034) | 9.22% |

Military Robotics and Autonomous Systems Market Analysis:

- Major Market Drivers: The market is witnessing strong growth due to the rising focus on enhanced operational efficiency, along with increasing cybersecurity concerns.

- Key Market Trends: The market is showcasing rapid growth on account of the integration of advanced technologies.

- Geographical Trends: North America leads the market, driven by favorable government initiatives. However, Asia Pacific is emerging as a fast-growing market due to strategic partnerships.

- Competitive Landscape: Some of the major market players in the military robotics and autonomous systems industry include AeroVironment, Inc., Applied Intuition Government, Inc., BAE Systems, Elbit Systems Ltd., Ghost Robotics Corporation, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, Milrem Robotics, Northrop Grumman, QinetiQ, Rheinmetall AG, Teledyne FLIR LLC, and Thales, among many others.

- Challenges and Opportunities: While the market faces challenges, such as regulatory and legal uncertainty, it also encounters opportunities on account of the rising adoption of robotics and autonomous systems (RAS) for civilian applications, such as disaster response, law enforcement, and search and rescue operations.

To get more information on this market Request Sample

Military Robotics and Autonomous Systems Market Drivers:

Operational efficiency and cost savings

As per Global Times, China launched the world's largest electric-powered quadruped bionic robot on 16 January 2022, which can carry up to 160 kilograms, run at up to 10 kilometers an hour, and is suitable for several kinds of terrains. The rising adoption of military RAS, as it offers enhanced efficiency by providing real time data gathering and analysis, is impelling the market growth. These capabilities benefit in improving decision-making processes and enabling quicker responses to dynamic situations. Various companies and governing agencies are investing in robotics that are operational in various terrain types, contributing to the broader expansion of the military robotics and autonomous systems market USA.

Changing nature of warfare

Unmanned aerial vehicles (UAVs), drones, and autonomous weapons are offering new capabilities for reconnaissance, surveillance, and precision strikes. The rising adoption of UAVs for asymmetric and urban warfare is supporting the market growth. Conflicts in densely populated cities present unique challenges for military forces, such as concerns about collateral damage, civilian casualties, and infrastructure destruction. Additionally, urban warfare can take many forms, ranging from guerrilla attacks to militia patrols to gang violence. As per the Hindustan Times, on 31 January 2024, security forces have unearthed a 130 meter-long and 6-foot-deep tunnel constructed by Maoists in Chhattisgarh. These tunnels provide both offensive and defensive advantages in guerrilla warfare.

Increasing number of geopolitical tensions and security threats

There is a rise in the number of geopolitical tensions and security threats across the globe that are leading to fatalities. The Journal of Peace Research claims that fatalities from organized violence increased by 97% as compared to the previous year, from 120,000 in 2021 to 237,000 in 2022. Geopolitical tensions and threats are leading to the increasing need for enhanced surveillance and reconnaissance capabilities. Military drones and autonomous surveillance systems offer valuable intelligence gathering without harming human lives. They can monitor borders, track troop movements, and gather information on potential threats, thereby improving situational awareness and preparedness.

Modernization of armed programs

Governing authorities of numerous countries are investing in the modernization of their armed forces, which is impelling the market growth. The Times of India reported that the Indian Army is investing in artificial intelligence (AI) innovations, revolutionizing modern warfare strategies. The army force introduced a multi-utility legged equipment (MULE), an autonomous load-bearing robot, on 13 September 2023. The robot offers exceptional versatility, as it has a 12 kg payload capacity and adaptable features, such as thermal cameras and radars. It also has dual communication capabilities that support both long term evolution (LTE) and wireless fidelity (Wi-Fi), making it suitable for short-range and long-range operations across diverse terrains, aligning with the latest military robotics and autonomous systems market trends.

Shift toward scalable and agile procurement

The US Department of Defense’s Replicator Program is driving a new procurement model focused on rapidly fielding large volumes of autonomous systems. Aimed at countering mass deployments by adversaries, this initiative prioritizes cost-effective, expendable platforms over high-end, complex systems. It encourages the integration of commercially available technologies and opens the defense market to non-traditional vendors, including startups and dual-use tech firms. By accelerating deployment timelines and lowering production costs, the program is reshaping demand dynamics in the military RAS market. This shift supports broader goals of deterrence, adaptability, and operational resilience, and is likely to influence defense procurement strategies in other countries facing similar strategic pressures.

Military Robotics and Autonomous Systems Market Opportunities:

Collaborations and partnerships between companies

Collaboration and agreements between defense contractors, technology companies, academia, and governing agencies are leading to innovations in the military RAS. For example, on 7 March 2024, Milrem Robotics, a leading robotics and autonomous systems developer of Europe, concluded its participation in the US Army Expeditionary Warrior Experiment (AEWE). The event, conducted in February in Fort Moore, USA, focuses on experimenting with new technology in realistic operational settings. In addition, in cooperation and partnership with the Dutch Ministry of Defence and at the invitation of the Dutch Robotics and Autonomous Systems (RAS) unit it allowed Milrem Robotics to present the capabilities of weaponized THeMIS Combat Unmanned Ground Vehicles (UGV).

Market growth and expansion

The demand for RAS is increasing on account of the ongoing modernization efforts by armed forces around the world. Various countries are upgrading their defense capabilities by acquiring advanced RAS technologies. As per Inside Defense, the US Army is focusing on new human-machine integrated formations initiative. These integrated formations are projected to bring robotic systems into units alongside humans. Their army is deploying robots for the first time beyond explosive ordnance units with the small multi-purpose equipment transport capability.

Rising investments in research and development (R&D)

The increasing investing in R&D activities to maintain strategic advantage and deter potential threats is supporting the growth of the market. This includes developing advanced weapons systems, sensor technologies, and intelligence capabilities to ensure superiority across various domains, including land, sea, air, space, and cyberspace. Besides this, companies are receiving funds from governing agencies to launch improved robotic systems. Teledyne FLIR Defense, part of Teledyne Technologies Incorporated, announced that it has received new orders worth US$ 62.1 Million from the U.S. Armed Services for its advanced and multi-mission robots on 7 July 2022.

Technology innovation and development

Key players are introducing advanced technologies in RAS by engaging in partnerships, agreements, and mergers and acquisitions (M&A). For instance, on 22 September 2022, Raytheon Missiles and Defense partnered with Northrop Grumman to develop the hypersonic attack cruise missile for the US Air Force (USAF). HACM is a first-of-its-kind weapon developed in conjunction with the Southern Cross Integrated Flight Research Experiment (SCIFiRE), a US and Australia project arrangement. HACM represents a breakthrough in hypersonic weapon technology that combines the characteristics of a cruise missile with the speed and maneuverability of a hypersonic vehicle. It can travel at ultra-high speeds, exceeding Mach 5, and deliver precision strikes against time-sensitive targets.

Key Technological Trends and Development:

Swarm autonomous unmanned systems

Innovations in swarm technology enable the coordination of large numbers of autonomous drones or robots and offer new capabilities for reconnaissance, surveillance, and enemy defenses. Swarm autonomous unmanned systems can move together through local network or satellite control systems. NewSpace Research and Technologies, a Bengaluru-based start-up delivered SWARM UAVs to Indian Army on 13 February 2023 as reported by The Print.

Vertical takeoff and landing (VTOL) UAVs

VTOL UAVs can take off and land vertically without the aid of a runway. They are known for their efficient, flexible, long-range flight. They can fly anytime and anywhere for different industrial fields, such as surveillance, mapping, surveying, and others. Furthermore, various companies are introducing VTOL for diverse purposes, such as Amber wings a UAV startup launched a compact hybrid VTOL drone ‘Atva’ for the transportation of cargo, medical supplies, and e-commerce deliveries reported by The Times of India on 11 October 2023.

Human-machine teaming

Human-machine teaming (HMT) is a new technology that involves combining the strengths of human cognition, intuition, and creativity with the computational power and speed of machines. It benefits in enhancing decision-making, situational awareness, and operational effectiveness on the battlefield. It is applied across various defense domains, including intelligence, surveillance, reconnaissance (ISR), logistics, cyber operations, and autonomous systems. Companies like Tomahawk Robotics collaborated with Rowden Technologies to provide its universal command and control technology and products for the United Kingdom's Army Future Capabilities Group Human Machine Teaming (HMT) tactical uncrewed systems fleet program on 23 February 2023 claimed by PR Newswire.

AI integration to enhance decision-making capabilities of military robots

The military sector is utilizing artificial intelligence (AI) in autonomous weapons and vehicle systems. AI-powered crewless aerial vehicles (UAVs) and ground vehicles and submarines are employed for reconnaissance, surveillance, and combat operations. AI benefits in enabling real-time data analysis, decision-making, and situational awareness. In addition, AI algorithms assist in analyzing data acquired from battlefield sensors and other sources to predict equipment failures before they occur. On 7 February 2024, the Australian military partnered with the UK and the US to showcase the operability of autonomous assets with AI in South Australia.

Military Robotics and Autonomous Systems Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on technology, operation, platform, end use, and application.

Breakup by Technology:

- Unmanned Aerial Vehicles (UAVs)

- Unmanned Ground Vehicles (UGVs)

- Autonomous Underwater Vehicle (AUV)

- Others

Unmanned aerial vehicles (UAVs) account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the technology. This includes unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), autonomous underwater vehicle (AUV), and others. According to the report, unmanned aerial vehicles (UAVs) represented the largest segment.

Unmanned aerial vehicles (UAVs) are aircraft that can be remotely controlled by a human operator or operate autonomously based on pre-programmed instructions or artificial intelligence (AI) algorithms. UAVs are widely available in various shapes and sizes, ranging from small handheld models to large and advanced aircraft for military, commercial, scientific, and recreational purposes. Additionally, there is a rise in the adoption of UAVs for various purposes.

The number of unmanned aircraft systems (UAS) produced is anticipated to grow from 2 million units in 2021 to 6.5 million in 2030 as per the International Civil Aviation Organization (ICAO).

Breakup by Operation:

- Fully Autonomous

- Semi-Autonomous

Semi-autonomous holds the largest share of the industry

A detailed breakup and analysis of the market based on the operation have also been provided in the report. This includes fully autonomous and semi-autonomous. According to the report, semi-autonomous accounted for the largest market share.

Semi-autonomous operates with a combination of automated features and human control or supervision. In this system, certain tasks or functions are automated, but human intervention or oversight is still required for decision-making, monitoring, and intervention if necessary. In addition, various military forces of several countries are investing in semi-autonomous systems like the Israel Defense Forces (IDF) launched its new semi-autonomous robotic ground vehicle called the Jaguar on 6 May 2021. It is capable of driving by itself to a predetermined destination while spotting and bypassing obstacles using sensors and an advanced driving system.

Breakup by Platform:

- Land Based

- Air Based

- Sea Based

Land based represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the platform. This includes land based, air based, and sea based. According to the report, land based represented the largest segment.

Land based are systems that are conducted on the surface of the Earth. They comprise ground vehicles, artillery and missile systems, and command and control systems. They are deployed on land for offensive and defensive purposes. Moreover, various companies and governing agencies are engaging in agreements to encourage land-based systems. The European Commission signed an agreement to launch the Land Tactical Collaborative Combat (LATACC) project coordinated by Thales to improve the collaborative capabilities of European coalition forces on 17 January 2024. Moreover, the project aims to enable the different land combat systems being developed by each member state to coordinate their actions in coalition with very short response times.

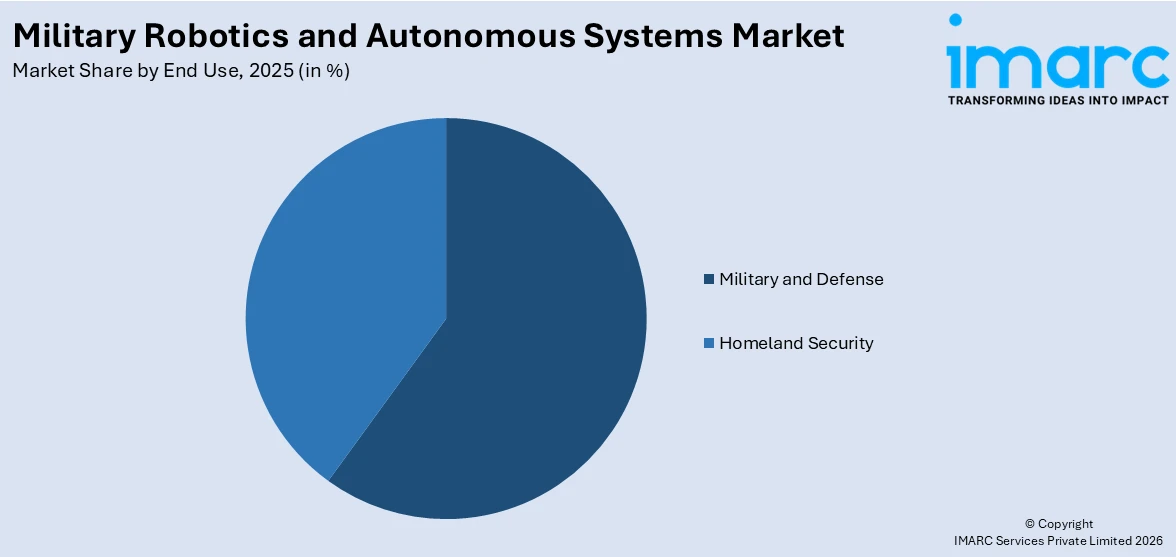

Breakup by End Use:

Access the comprehensive market breakdown Request Sample

- Military and Defense

- Homeland Security

Military and defense exhibit a clear dominance in the market

A detailed breakup and analysis of the market based on the end use have also been provided in the report. This includes military and defense and homeland security. According to the report, military and defense accounted for the largest market share.

Military and defense forces are increasingly conducting a variety of operations, including combat operations, peacekeeping missions, humanitarian assistance, disaster relief, counterterrorism operations, and other activities to protect national interests and support international stability. They are also investing in RAS to tackle various geopolitical situations and threats. Governing agencies of India are allocating huge funds to these sectors for maintaining peace worldwide. The Ministry of Defence represents an enhancement of INR 68,371.49 crore (13%) over the budget of 2022-23 as per the Press Information Bureau.

Breakup by Application:

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Combat

- Logistics

- Search and Rescue

- Mine Detection and Clearance

- Others

Intelligence, surveillance, and reconnaissance (ISR) dominates the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes intelligence, surveillance, and reconnaissance (ISR), combat, logistics, search and rescue, mine detection and clearance, and others. According to the report, intelligence, surveillance, and reconnaissance (ISR) represented the largest segment.

Intelligence, surveillance, and reconnaissance (ISR) include manned and unmanned airborne, space-borne, maritime, and terrestrial systems that play critical roles in support of military operations. ISR systems range in size from mobile devices to satellites. They also use unstructured data to extract and analyze insights. Moreover, they excel in operating within hostile environments, mitigating the risk to human lives, and thereby serving as invaluable assets for military intelligence operations. In October 2023, army engineers from the Military College of Electronics and Mechanical Engineering (MCEME) in Secunderabad (India) unveiled ‘Robotic Buddy’, a versatile robot that serves various battlefield needs. It can remotely detect humans, track specific areas, measure distances, and transmit intelligence, surveillance, and target acquisition (ISR) data.

Regional Insights:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest military robotics and autonomous systems market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Latin America (Brazil, Mexico, and others); Middle East; and Africa. According to the report, North America represents the largest regional market for military robotics and autonomous systems.

North America is a hub for technological innovation in the defense sector. Leading defense contractors and research institutions in the region are developing advanced military robotics and autonomous systems. The US Deputy Secretary of Defense Kathleen Hicks on 30 August 2023 claimed that the United States military plans to start using thousands of autonomous weapons systems in the next two years. Besides this, governing agencies in the region are allocating funds for defense procurement and research and development (R&D) activities.

Analysis Covered Across Each Country:

- Historical, current, and future market performance

- Historical, current, and future performance of the market based on technology, operation, platform, end use, and application.

- Competitive landscape

- Government regulations

Competitive Landscape:

- The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the major market players in the military robotics and autonomous systems industry include AeroVironment, Inc., Applied Intuition Government, Inc., BAE Systems, Elbit Systems Ltd., Ghost Robotics Corporation, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, Milrem Robotics, Northrop Grumman, QinetiQ, Rheinmetall AG, Teledyne FLIR LLC, and Thales.

- Key players in the market are focusing on introducing advanced autonomous vehicles that offer superior features. They are also engaging in partnerships and mergers and acquisitions (M&A) to develop robotic defense systems. Besides this, various players are focusing on various trials that involve a wide range of challenging scenarios for their products. For example, on 6 July 2023, Milrem Robotics achieved success during the recent autonomy trials conducted by the Estonian Military Academy. The trials showcased the superior capabilities of Milrem Robotics’ unmanned ground system, THeMIS, when equipped with the company’s intelligent functions kit, MIFIK.

Analysis Covered for Each Player:

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Military Robotics and Autonomous Systems Market News:

- In June 2025, Anduril and Rheinmetall partnered to develop autonomous air systems and propulsion technologies for Europe’s defense sector. Their collaboration would integrate Anduril’s autonomous air capabilities into Rheinmetall’s Battlesuite framework and explore solid rocket motor applications. This move supports the growing demand in the military robotics and autonomous systems market, emphasizing AI-driven solutions and enhanced operational readiness across European defense programs.

- In February 2025, Ukraine’s Defense Ministry launched a new initiative to expand the use of unmanned ground systems, forming dedicated robotics units within frontline combat brigades. The defense minister emphasized the goal of building a tech-driven army to handle high-risk tasks while reducing casualties. These systems support combat, evacuation, logistics, and demining, reflecting Ukraine’s shift toward autonomous warfare in response to ongoing conflict.

- In January 2025, Palladyne AI and Red Cat Holdings completed a successful test flight where multiple Teal drones, using Palladyne Pilot AI software, autonomously collaborated to detect, prioritize, and track ground targets. The demonstration showed advanced drone coordination and sensor-sharing under limited communication, marking a step forward in AI-driven military robotics and autonomous systems for defense operations.

- In October 2024, the Australian Army’s 1st Armoured Regiment conducted a major demonstration of robotics and autonomous systems, testing uncrewed vehicles, AI command-and-control systems, and combat teaming tech. Collaborating with industry and the Army’s Battle Lab, the event highlighted how emerging autonomy can boost battlefield effectiveness, increase lethality, and keep soldiers out of direct harm, with strong support from local companies and defense innovation offices.

- In September 2024, Textron Systems and Kodiak Robotics integrated Kodiak’s self-driving system into the RIPSAW M3, an uncrewed robotic ground vehicle built for defense missions. Designed to enhance safety and reduce risk to personnel, the vehicle reflects growing momentum in autonomous military robotics. Both companies plan to pursue further opportunities with the US and allied defense forces to advance ground vehicle automation.

Military Robotics and Autonomous Systems Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Unmanned Aerial Vehicles (UAVs), Unmanned Ground Vehicles (UGVs), Autonomous Underwater Vehicle (AUV), Others |

| Operations Covered | Fully Autonomous, Semi-Autonomous |

| Platforms Covered | Land Based, Air Based, Sea Based |

| End Uses Covered | Military and Defense, Homeland Security |

| Applications Covered | Intelligence, Surveillance, And Reconnaissance (ISR), Combat, Logistics, Search and Rescue, Mine Detection and Clearance, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AeroVironment, Inc., Applied Intuition Government, Inc., BAE Systems, Elbit Systems Ltd., Ghost Robotics Corporation, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, Milrem Robotics, Northrop Grumman, QinetiQ, Rheinmetall AG, Teledyne FLIR LLC, Thales, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the military robotics and autonomous systems market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global military robotics and autonomous systems market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the military robotics and autonomous systems industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Military Robotics and Autonomous Systems Market Report

The military robotics and autonomous systems market was valued at USD 11.8 Billion in 2025.

The military robotics and autonomous systems market is projected to exhibit a CAGR of 9.22% during 2026-2034, reaching a value of USD 26.7 Billion by 2034.

The military robotics and autonomous systems market is driven by rising defense spending, demand for force protection, advancements in AI and sensor technologies, increased battlefield automation, and the need for remote operations in hostile environments. Geopolitical tensions and modernization programs also play a significant role in accelerating adoption across domains.

North America dominated the military robotics and autonomous systems market in 2025 due to high defense budgets, strong R&D capabilities, early adoption of advanced technologies, and significant investments in unmanned and AI-driven systems.

Some of the major players in the military robotics and autonomous systems market include AeroVironment, Inc., Applied Intuition Government, Inc., BAE Systems, Elbit Systems Ltd., Ghost Robotics Corporation, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, Milrem Robotics, Northrop Grumman, QinetiQ, Rheinmetall AG, Teledyne FLIR LLC, Thales, etc.

Demand for UAVs is growing due to their effectiveness in surveillance, reconnaissance, and precision strikes without risking human lives. They offer real-time data, lower operational costs, and extended mission endurance. Rising border tensions, counterterrorism efforts, and technological improvements in sensors, AI, and communication systems further fuel their adoption globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)